The design and implementation of index insurance initiatives: Three challenges for policy

26

The Design and Implementation of Index Insurance Initiatives: 3 Challenges for Policy Michael R Carter NBER & University of California, Davis BASIS I4 Index Insurance Innovation Initiative http://basis.ucdavis.edu Workshop on Developing Policy Innovations for the Pastoralist Rangelands International Livestock Research Institute, Nairobi June 8, 2015 M.R. Carter Index Insurance Design & Implementation

Transcript of The design and implementation of index insurance initiatives: Three challenges for policy

The Design and Implementation of Index Insurance Initiatives:

3 Challenges for Policy

Michael R Carter

NBER & University of California, DavisBASIS I4 Index Insurance Innovation Initiative

http://basis.ucdavis.edu

Workshop on Developing Policy Innovations for the Pastoralist RangelandsInternational Livestock Research Institute, Nairobi

June 8, 2015

M.R. Carter Index Insurance Design & Implementation

What Can Index Insurance Do?

Know that risk is directly costly

Makes Households Poor when it leads them to adopt less riskyactivities, but lower returning activitiesKeeps Households Poor when it leads them accumulateunproductive ’buffer’ assets

Deepens capital constraints also as

Cuts off self-finance by holding of ’unproductive’ savingsDiscourages external finance (credit), especially when risk iscorrelated

Reducing risk via insurance should address all these problemsNote also that when twined with technology adoption,insurance becomes relatively inexpensiveBut can insurance really work for low wealth agricultural &pastoralist households?

M.R. Carter Index Insurance Design & Implementation

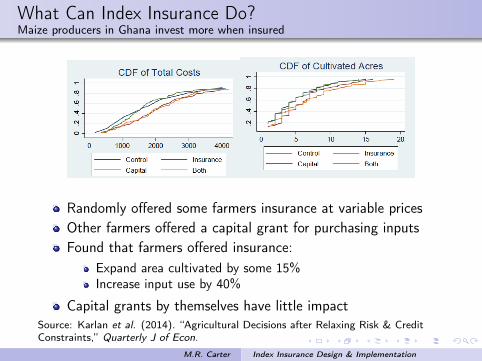

What Can Index Insurance Do?Maize producers in Ghana invest more when insured

Randomly offered some farmers insurance at variable pricesOther farmers offered a capital grant for purchasing inputsFound that farmers offered insurance:

Expand area cultivated by some 15%Increase input use by 40%

Capital grants by themselves have little impactSource: Karlan et al. (2014). “Agricultural Decisions after Relaxing Risk & CreditConstraints,” Quarterly J of Econ.

M.R. Carter Index Insurance Design & Implementation

What Can Index Insurance Do?Cotton producers in Mali invest more when insured

Designed a dual-scale index contract with radically lower basisriskInsurance offered to a random subset of villages–find that ininsured villages:

Area planted to cotton & input use increased by 45%Output & income increased as expected (result not statisticallysignificant)

Currently scaling up in Burkina Faso

Source: Elabed & Carter (2014) “Ex-ante Impacts of Agricultural Insurance: Evidencefrom a Field Experiment in Mali,” Working Paper

M.R. Carter Index Insurance Design & Implementation

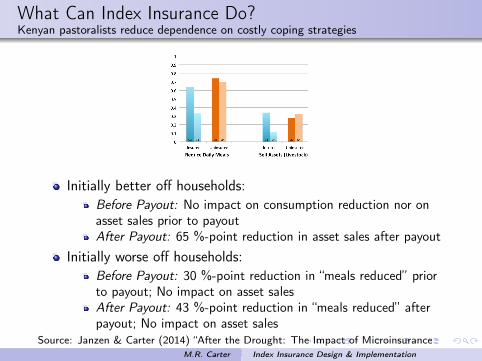

What Can Index Insurance Do?Kenyan pastoralists reduce dependence on costly coping strategies

IBLI Insurance had payout in October 2011 after a prolongeddrought that sparked 30-40% livestock mortalityOctober 2011 survey asked insured and uninsured householdshow they had been coping with the drought prior to thepayout/survey & how they anticipated coping after thepayout/survey

M.R. Carter Index Insurance Design & Implementation

What Can Index Insurance Do?Kenyan pastoralists reduce dependence on costly coping strategies

Initially better off households:Before Payout: No impact on consumption reduction nor onasset sales prior to payoutAfter Payout: 65 %-point reduction in asset sales after payout

Initially worse off households:Before Payout: 30 %-point reduction in “meals reduced” priorto payout; No impact on asset salesAfter Payout: 43 %-point reduction in “meals reduced” afterpayout; No impact on asset sales

Source: Janzen & Carter (2014) “After the Drought: The Impact of Microinsuranceon Consumption Smoothing and Asset Protection,” NBER Working Paper No. 19702.M.R. Carter Index Insurance Design & Implementation

Policy Challenges for Index Insurance

Achieving these social protection and growth impacts faces keypolicy challenges:

1 Cost-effective, integrated social protection system

Response: Public provision of minimum insurance protectionfor vulnerable families

2 Quality contracts that do not fail households when losses occur

Response: Public certification of index insurance quality

3 Competitive insurance (risk) pricing

Response: Backstop public reinsurance facility

Let’s look at each of these

M.R. Carter Index Insurance Design & Implementation

Challenge 1Cost-effective, integrated social protection system

Cash transfers, food aid & other forms of social protectiontarget those who are poor and have perhaps becomeeconomically unviable/stuckClear financial logic to protecting the vulnerable so that theydo not fall into destitution and become transfer eligibleAnd yet public funds devoted to the vulnerable divertsresources from the already poorWhile the ability of the vulnerable to pay for their owninsurance is limited, analysis suggests that some public fundingof insurance for the vulnerable can be cost effective

M.R. Carter Index Insurance Design & Implementation

Challenge 1Cost-effective, integrated social protection system

Constant budget policy experimentsCash transfers for indigent50% insurance subsidy for poor and vulnerable, with residualbudget spent on cash transfers

M.R. Carter Index Insurance Design & Implementation

Challenge 1Cost-effective, integrated social protection system

In the policy simulation, insurance subsidy works well becauseit harnesses two forces:

Restores assets so families do not collapseEnhances investment incentives so families can prudentiallyinvest & reduce vulnerability

Together these forces bring the dramatic drops in chronicpoverty & increases in self-relianceKey features of this approach

Public purchase (or partial purchase) helps make the market(& instills confidence)Unlike ad hoc schemes in some South American countries,individuals can buy insurance beyond the publicly-fundedmargin, enhancing investment incentives & growth

M.R. Carter Index Insurance Design & Implementation

Challenge 2Quality contracts that do not fail households

Disappointed (angry) farmers & what are sometimes called“Basis Risk Events” have punctuated the importance ofdesigning contracts that protect farmersThe problem is far from trivial as the following analysis of therelationship between average losses and indemnity paymentsunder rainfall insurance in India shows:

Clarke, D. et al. (2012). “Weather Based Crop Insurance in India.”

Such contract failures can also hurt lenders & destroy trust &confidence in insurance companies (and government)

M.R. Carter Index Insurance Design & Implementation

Challenge 2Quality contracts that do not fail households

At its simplest, insurance should stabilize income flows (and,or protect assets), underwriting:

More stable consumption and stable investment in humancapital (nutrition & education) that are subject to’irreversiblilities’Improved investment incentives by reducing the risk of capitalloss

A simple picture can help frame our thinking:

M.R. Carter Index Insurance Design & Implementation

Challenge 2Quality contracts that do not fail households

Perfect insurance will put a level floor under familiesIndex insurance will never reach that level of protectionHowever, can use a localized (say village level) area yieldcontract as a benchmarkKeep in mind that index insurance will not be the answer ifrisk is not the constraint or if most risk is individual (notcommon or covariate)

M.R. Carter Index Insurance Design & Implementation

Challenge 2Quality contracts that do not fail households

Safe minimum quality standard:

Expected utility allows calculation of a ’reservation’ pricedefined as the maximum amount an individual could pay for acontract without making herself worse offA safe minimum quality standard might be: Reservation Price> Market PriceLet’s look at a real example from Tanzanian rice cultivation

M.R. Carter Index Insurance Design & Implementation

Challenge 2Measuring insurance quality for rice farmers in Northern Tanzania

M.R. Carter Index Insurance Design & Implementation

Challenge 2Village-level Area Yield vs. Optimized Satellite-based Contract

For each small area (“village”), we collected 10 years ofretrospective data on yieldsBest satellite predictor of village yields proved to be based on’Gross Primary Production’ (based on EVI, FPAR & LAI)Let’s compare this (cheap to administer) satellite based indexwith an (expensive) village-level area yield contract:

50

010

00

15

00

20

00

25

00

30

00

Pre

dic

ted

yie

ld (

kg/a

cre

)

500 1000 1500 2000 2500Actual yield (kg/acre)

Predicted vs. actual area yields in Makindube

M.R. Carter Index Insurance Design & Implementation

Challenge 2Will I get paid probability measure

Consider a contract that pays anytime either measured orsatellite predicted village yields fall below average:

0.1

.2.3

.4.5

.6.7

.8.9

1

Pro

bab

ility

of pa

you

t

0 .2 .4 .6 .8 1 1.2 1.4Plot-level yield (% of historic mean)

95% Confidence Interval Satellite Index Contract

Area-Yield Contract

Probability of receiving a payout by zone-level yields

M.R. Carter Index Insurance Design & Implementation

Challenge 2How much will I get paid measure

M.R. Carter Index Insurance Design & Implementation

Challenge 2Reservation Price Quality Measure

Actuarially fair prices for these contracts are 130 kg of riceper-hectare insuredUnrealistically, assuming no local risk sharingMinimalist Quality Standard: Reservation Price > MarketPrice of Contract

M.R. Carter Index Insurance Design & Implementation

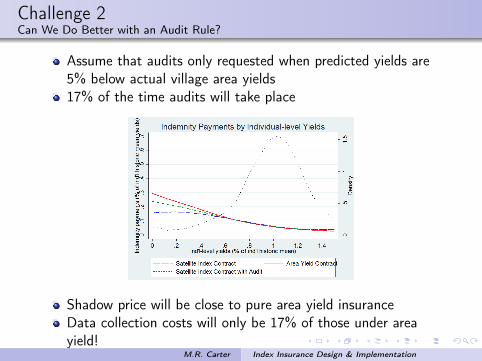

Challenge 2Can We Do Better with an Audit Rule?

Can see that the satellite does well separating good from bad,but has trouble distinguishing quite bad from slightly bad

What if we augmented satellite index with an audit on demandscheme:

Agreed upon crop cut methodology at village levelIncentive compatible penalties to prevent unnecessary audits

M.R. Carter Index Insurance Design & Implementation

Challenge 2Can We Do Better with an Audit Rule?

Assume that audits only requested when predicted yields are5% below actual village area yields17% of the time audits will take place

Shadow price will be close to pure area yield insuranceData collection costs will only be 17% of those under areayield!

M.R. Carter Index Insurance Design & Implementation

Challenge 2

Work here suggests a safe minimum quality standard:

Reservation Price > Market PriceNote that even if insurance is subsidized, beneficiaries wouldbe better if simply given the subsidy rather than given cheapinsurance that approximates a lottery ticket

Issues of quality assurance are very important:

Clarke & Wren-Lewis (2014) make a very compelling argumentthat without quality certification standards, markets will supplylow quality contracts predominate

Much to learn about how to implement those standards, butalso how to design contracts that meet those standards

M.R. Carter Index Insurance Design & Implementation

Challenge 3Competitive Pricing

Some jargon:

The actuarially fair price (or pure premium) of an insurancecontract is equal to the expected payouts under the contractTo cover administration costs (which should be low for indexinsurance) & cost of capital, insurance companies have tomark-up or load the cost of insurance (in US crop insurance,the mark-up results in a price that is between 125% and 130%of the ’AFP’)

A number of index insurance pilots have faced prices of175-200% of AFP–why?

Thin markets, small project size & lack of competition/interestSparse data and uncertainty-penalized pricing

It is clear that prices at this level are non-starters for lowwealth householdsWhat is to be done?

M.R. Carter Index Insurance Design & Implementation

Challenge 3Competitive Pricing

With generous support from various donors, the IFC’s GlobalIndex Insurance Facility (GIIF) has to date provided an acrossthe board subsidy on prices set by private industry to variousprojects, including IBLIThe USAID-funded Global Action Network on Index Insurance,collaboration with the ILO & I4 is now in conversation withIFC & the World Bank about alternative ways to lower price

Let a public sector entity (not allergic to uncertainty) carry thelayers of risk that are most worrisome to the private sectorLet a public sector entity serve a broker role, transparentlypricing and putting out to bid contracts with certified riskestimates (perhaps bundling together multiple projects in thespirit of the African Risk Capacity)This same entity could also certify quality

Note that creating a minimum demand based on publicpurchase of basic insurance coverage could further help bringdown prices

M.R. Carter Index Insurance Design & Implementation

In Conclusion

While we are beginning to see that index insurance can realizeits promise to fundamentally alter income growth & povertydynamics, it is no magic bulletSubstantial challenges remain to be resolved if index insuranceis to fully reach its promiseThe KLIP program is promising, not only because it iswell-designed, but also because it will likely help us answermany of the key challenges about index insurance that we havediscussed todayForward!

M.R. Carter Index Insurance Design & Implementation

Thank you!

M.R. Carter Index Insurance Design & Implementation