The D. Allan Bromley Memorial Lecture: Bringing Advanced Innovation to Manufacturing William B....

39

The D. Allan Bromley Memorial Lecture: Bringing Advanced Innovation to Manufacturing William B. Bonvillian Director, MIT Washington Office University of Ottawa, May 14, 2012

-

Upload

jenifer-parramore -

Category

Documents

-

view

215 -

download

2

Transcript of The D. Allan Bromley Memorial Lecture: Bringing Advanced Innovation to Manufacturing William B....

The D. Allan Bromley Memorial Lecture: Bringing Advanced Innovation to Manufacturing

William B. BonvillianDirector, MIT Washington OfficeUniversity of Ottawa, May 14, 2012

D. Allan Bromley 2

Background: The U.S.-Canada PartnershipU.S.-Canada – the largest bilateral trade relationship in the

history of the world –Total merchandise trade: $530B (2007 pre-recession)

Enhanced through deep trade agreements - U.S.-Canada Auto Pact of 1965 to NAFTA

U.S.-Canada economies highly integrated – comparable standards of living and industrial structure

U.S. (pre-recession 2007): $300B in in imports from Canada and $230B in exports

We must care a lot about each other I bring today a perspective on U.S. manufacturing but it affects

both nations

I will outline steps I believe the U.S. must consider, and have been active in a number, but will leave details on the actions and who the actors might be to Q&A

3

BACKGROUND POINTS

---why “manufacturing matters”

4

Hollowing Out?Employment:

Down almost 1/3 in a decade

Investment:Manufacturing fixed capital investment declined (accounting

for costs) in the 2000s for the first time since the data has been collected

Output:Adjusting gov’t data (for foreign component origin and

inflationary assumptions in IT and energy sectors), manufacturing output value declined in the 2000s

Decline in 16 of 19 sectors

Productivity:If output lower than assumed, productivity is lower

5

We have been assuming we have been losing manufacturing jobs because of productivity gainsRecent work – “The Race Against the Machine,” for example - is

telling us that multiplying productivity gains from IT are displacing work as we know it.

Yet, historically - most recently in the tech boom of the 90’s - productivity gains, although disruptive initially, grow more jobs

Maybe that history is still true – and maybe we need to search for our profound job losses in the manufacturing sector.

That means “The Great Recession” is structural, not business cycle, so the Keynesian stimulus tools we have been applying won’t work well.

The Manufacturing Hollowing Out is why these aren’t working – requires a Structural strategy not a maco-economic strategy

6

Sharp Decline in Mfg. Employment, 2000-2010 -- drop so steep that productivity gain can’t explain

7

Manufacturing Remains a Major Sector

Manufacturing = $1.7 Trillion of $15T U.S. economy

Employs 12 million in workforce of 140m

Dominates the U.S. innovation system – 70% of of industrial R&D, 80% of patents, employs 64% of scientists and engineers,

The currency of international trade is complex high value goods – 80% of U.S. exports are high value goods (capital goods,

industrial supplies, transport goods, medicines)U.S. pre recession ‘07: $500B deficit in goods – on track to

return to that levelServices surplus ($160B) growing gradually but will not offset

manufacturing deficit in foreseeable future

8

9

Underlying Issue: Our “Innovate here/Produce Here” AssumptionSince WWII - U.S. economy organized around

leading the world in technology advance. US led all but one of the innovation waves of the 20th

century – and growth economics tell us that technological & related innovation = 60%+ of growth

from aviation to electronics, to nuclear power, to computing, to the internet, to biotech

Missing an innovation wave is serious: Japan led quality mfg.; 1973-1991 tough for U.S. – GDP and productivity 1% below historical averagesResponse: ‘90s IT innovation wave and record growth

Our operating assumption - we would innovate here and WE would translate those innovations into products Would realize the full range of economic gains from

innovation at all stages It worked – world’s richest economy

10

“Innovate here/Produce here” Bonds Breaking?

With global economy, assumption of innovate here/produce here no longer holds. In some industrial sectors, can now sever

R&D and design from production –That brings the economic foundation of our

innovation-based economy into question. Why invest in innovation here if gains elsewhere?

Last 25 years – IT/electronics allowed severing of R&D/design from production via IT-based specs; commodity goods, tooDistributed Manufacturing – Apple iPod

example

But other sectors still require deep connection between R&D and production – constant reengineering and improvements to cut costs

11

Mind The Connection between R&D/Design and Production in Different Sectors3 basic kinds of produced goods:

(1) IT, (2)bio/pharma, and complex (3) electro- mechanical-aero

First – can sever R&D/design from production using batch processing (bio/pharma), IT specs (IT goods)

Electro-mechanical-aero – tie R&D/prod.– variables too complexEnergy, for ex., is in the 3rd electro-mechanical category – need

to connect R&D/design with production

If offshore production, will design/R&D follow?Distributed Mfg.: risk losing production; the rest: lose production, will design/innovation follow?

Underlying all this: Competing with low cost/wage high tech competitors: must have production productivity gainsThat means new innovation req’d: technology and

processes

12

If Manufacturing is changing, what are the New “Geopolitics of Manufacturing”?U.S. has gone through 3 phases:

1789-1945 – Alexander Hamilton saw that U.S. independence and security would be built on its commercial strength – U.S. pursued strong self-dependence in manufacturing through WW2

1945-1993 – Cold war competition with Marxist economic system – U.S. strategy: North America, Western Europe, Japan in a system of mutual economic dependence and integrated economies among allies.

1993-now: Clinton: unified global economy is way to integrate China into the world system – manufacturing would be global – decentralized and integrated

If manufacturing is no long a tool of national security, can technology leadership shift?

13

Historical Examples of Manufacturing Shifts 1

4

Competiveness Then and Now – much more complex

JAPAN v. U.S. – 1970’S – 80’S

CHINA v. U.S. - Today

High cost, high wage, advanced technology economy – comparable to the U.S.

Low cost, low wage, increasingly advanced technology economy

U.S. had entrepreneurial advantage, Japan had industrial policy advantage

Entrepreneurial and pursuing industrial policy

Rule of Law Limited Rule of Law

IP Protections Extensive IP theft

Subsidizes currency, buys U.S. debt

Following Japan’s model: subsidizes currency and largest holder of U.S. debt

15

This Competition = Eroding U.S. Advanced Technology Sectors

Shifted abroad:Every brand of notebook computerEvery mobile/handheldDisplays

Shifting abroad? Major erosion in:Advanced materialsComputing and communicationsRenewable energy technologies and storageSemiconductor production

The Kindle could not be made in the U.S.

$100B trade deficit advanced tech goods

16

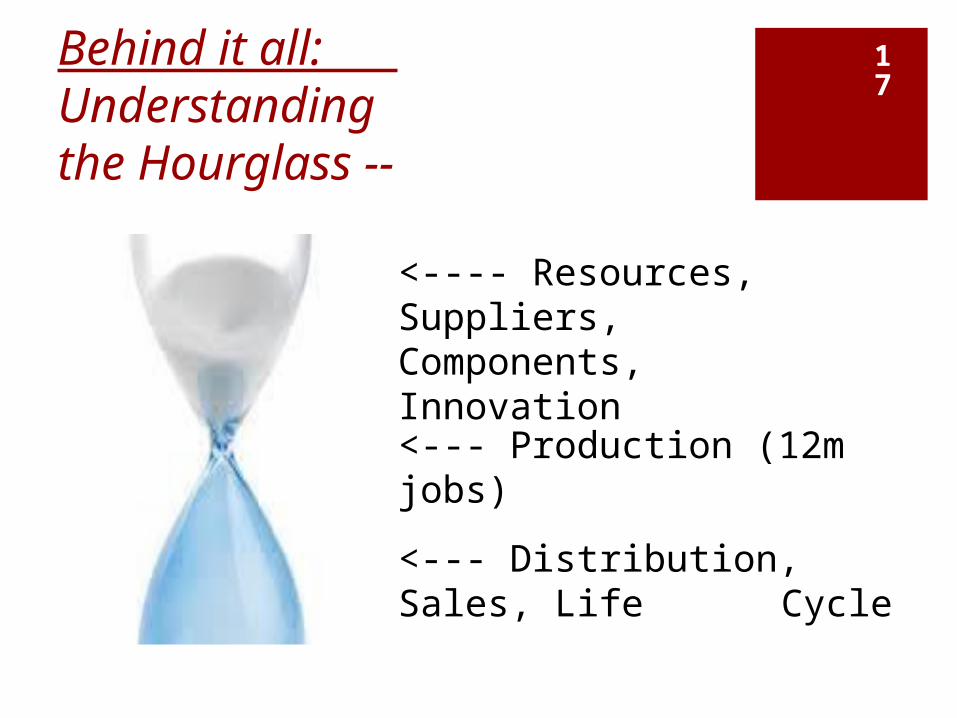

Behind it all: Understanding the Hourglass --

<---- Resources, Suppliers, Components, Innovation

<--- Production (12m jobs)

<--- Distribution, Sales, Life Cycle

17

It is an Hourglass because we know Mfg. is a Job Multiplier:Economic Policy Institute: Mfg. job

multiplier - 2.90

Milken Institute: 2.50 multiplier

Zobel (Germany) smart manufacturing factory supports 5.2 additional jobs

High-tech manufacturing industries appear to have greater multipliers - Electronic computer manufacturing multiplier of 16

[ITIF 4/11 summary]

18

Change in Median Household Income, 2000-2011 (inflation adj.)

19

+2

0

-2

-4

-6

-8

-10

-12

CAUSE: STRUCTURAL RECESSION – Centered in Mfg.Source: G.Green, J.Coder (10/11, based on Census Bur. Data)

If it is a structural recession with a base in manufacturing, this

requires:

Innovation in Advanced

Manufacturing:

9 Steps to consider

20

Need to Keep in Mind the Levels in the US Manufacturing Sector

Three elements in US mfg.:Large Multinationals (MNCs) – very international - will

locate in low cost production centers for productivity gains; need to be in emerging markets

Start-up and entrepreneurial firms – increasingly offshoring production – not a core competency, can’t get financing- So: next gen technologies shift?

300,000 small manufacturers – suppliers, component makers – bulk of US mfgThinly capitalized, risk adverse, no R&D

21

Step #1: What technology advances = new manufacturing productivity = new paradigms?

“Network centric”

– mix of advanced IT, RFID, sensors in every stage and element, new decision making from “big data” analytics, advanced robotics, supercomputing w/adv’d simulation & modeling

Advanced materials

“materials genome” – ability with supercomputing to design all possible materials with designer features

Biomaterials, bio fabrication, syntehtic biology

Lightweighting everything

Nanomanufacturing

fabrication at the nano-scale

Mass Customization

Production of one at cost of mass production (ex.: 3D printing/additive mfg, etc.)

Distribution efficiency

IT advances that yield distribution efficiencies (incl. in supply chain)

Energy Efficiency – energy is “waste

22

These tech paradigms are not optional – Companies will have to meet them

Timetable – starting to see these adv’d mfg. technologies emerge – will be pervasive in next 15 years

Just as with “Lean Mfg.” (way US firms responded to Japan’s model of the 70s-80s), today’s firms will need to pursue these advanced technologies because the competitive efficiencies are major

How will mass of 300,000 US SMEs adapt to these tech advances? Big challenge

US: strength on the design side – real limits on the commercialization and scale-ability side which advanced mfg. innovation would enable

US is not yet working systematically on this agenda

23

Step #2 – Pick Tech Paradigms that Apply across SectorsManufacturing is sectoral, but with

increasing sectoral overlap for complex, high value goods An airplane is complex system: aero

design, electronics, IT, materials, etc.

Technology paradigms have to make sense in the sectors

Run a matrix – technology options against sectors they apply to – pick technologies with payoff across sectors

Include emerging sectors

24

MATRIX: Tech Sectors/Mfg. Paradigms 25

Sector and Mfg. Pardigm

Bio/pharma

Aero-space

IT/electronics

Heavy Equip ment

Digital search, network

New energy

Trans port

Network -centric

x x x x x x x

Advanced materials

x x x x x x

Nano Mfg. x x x x x x x

Mass Customi-zation

x x x x x x x

Distribution Efficiency

x x x x x x

Energy Efficiency

x x x x x x x

Step #3 – Technology is Not Enough…Need to Look at all Three:

A) New Adv’d Mfg. Technology Paradigms - first building block

B) But need Process – adapt to production system

C) Then need Business and Organizational Model – has to work economically

26

Step #4:, It’s no longer Manufacturing or Services21st Century firm increasingly fuses services,

production, supply chain management and innovation – IBM’s Lou Gerstner originated this model in the

90’sMany of these capabilities are knowledge “intangibles”

not fixed assets – learning to tie new equipment and technologies to new processes – fusing IT-informed services models with new mfg.

What is this emerging firm model? How pervasive? is it vertical or horizontal? is it integrated or the result of flexible leveraging other

firms’ specialty capabilities? Business model stage - will need to look at optimal

combined mfg./services model

27

Step #5: Need to Look Over Our Shoulders

Look at competitor nation strategiesHard to understand the future of U.S.

manufacturing without evaluating the context of global manufacturer competitors and their strategies – learn from them – they are doing this and have “top down” not just “bottom up”

Look at: China/India/Brazil – large emerging Germany/Japan – large established High wage & cost – yet major mfg. surpluses

Korea/Taiwan – smaller scale, key nichesExpanding mfg. employment

28

Step #6: Build the Workforce - Most of mfg. is now defined as services –

Need a new level of fused knowledge, skills in both

STEM Ed req’d; mfg.: pervasive basic STEM skill sets

Ed system doesn’t understand that innovation requires “mind and hand” “intelligent hand” - mix of skills, experimentalists and theorists –

learning by doing Additive manufacturing in schools?

It’s not just design as a stand-alone stage, design is over time also the ability to make, as well – education needs to incorporate

Very hard, still, despite distributed IT manufacturing, to sever design from production – mutually informative

Community college skills role w/industry certificationNew adv’d mfg. engineering curriculum – how to develop process

from lab bench technologies – lost in engineering curriculum

29

Step #7: Innovation Organization - The Pipeline and the Seams

US pipeline innovation model organized with heavy federal basic research investment, some applied (from DOD) Limited investment in manufacturing R&D (including tech, process,

business model) - $800m – and not interagency

We institutionalize the “Valley of Death” in our R&D model

profound problems at the seams of the innovation pipeline – big disconnects between actors U.S. research strong; scaling/commercialization a problem:

Research – basic research agencies, univ’sApplied and later stages – industry, some DOD supportBut other intermediate steps will need public-private

connections –further down the pipeline to commercializationNot just R&D–pre-production networked organizational models

30

We Need these Guys - DOD: Operates at Every Stage of the Innovation System - Historically Central Player

- Role in Adv’d Mfg.?REMEMBER -

DOD’s 20th Century

Innovation Waves:

Aviation

Electronics

Nuclear Power

Space

Computing

The Internet

31

Step #8: Build Regional Infrastructure

No longer the Old Pipeline model – gov’t does Research and industry picks up the rest

Now: host of intermediary steps require public/private connections

Especially important: the TestbedWhere 300,000 SME’s test the efficiency and cost of new

mfg. technologies – they lack resources for this stageMfg. is regional not national – need to be in regional

clusters

32

Research > Development > Prototype > Demonstration > Testbed > Production at Scale

Step #9: Financing Innovation - “5 Year Yardstick” doesn’t work in Mfg.

The Breakthrough system – the pipeline: federal R&D, univ. research, startups/entrepreneurs, VC’s angel, IPO’s 5-year yardstick based on IT model: VC’s fund

technologies no more than 2/3 years from commercialization, then the flip to an IPO within 3 years

New manufacturing technology paradigms probably require the breakthrough innovation system

But advanced manufacturing doesn’t fit the 5 year yardstick

33

5-Year vs. 10-year Yardstick:Manufacturing doesn’t fit the 5-year yardstick:

New mfg. tech’s face the Valley of Death – Then they face the “Mountain of Death” – getting to market

launch at scale: major financing and price competitive at the outset of launch

34

Valley of Death – 5 year scale up - creating connections and funding to move from research to late stage development

Mountain of Death: 10+ year scale up; major financing needed to scale, price competitive from moment of market launch

+

Work-Arounds for the Mountain

Manufacturing – the 10+year yardstick Requires deeper, longer term, patient capitalization/finance

than ITLonger time to stage entry and to scale – 10+ years not 5It’s a complex, established “legacy” sector

US better at bringing innovation into new areas, not at introducing innovation into legacy areas

Different mindset – can’t create a company to sell it, as in IT, biotech

Work-Arounds for the Mountain of Death:Front end of the innovation system:

R&D programs designed for the breakthrough and to drive down prices/reduce production costsUS research agencies: “NMP” – Not My Problem – look at just research

not the implementation – change?ARPA-E and EERE considering

Back end of the innovation system?Andrew Lo – portfolio approach

Small commitments by large nos. of investors – use the internet Crowd-funding? Lotteries?

35

Remember Innovation Organization Effects for the 3 kinds of Mfg Firms Different ---MNC’s

Respond to competitive cost competition by locating where they need to Will locate R&D near production when nexus needed – can go abroad,

avoid risk of adv’d technologies by offshoring to low cost

Entreprenurial/Startups pursuing scaleable tech’s VC’s won’t fund mfg. – not core competency So: Offshore production – reduce risk and costs But risk product control – knowledge spillover Lose next gen technologies

Small Manufacturers – bulk of US manufacturing Need productivity gains to stay competitive Lack resources, tech dev/access – so need proven technologies, processes Lack testbeds, financing for productivity options – miss tech waves

36

Remember the Steps:#1- Technology advances that yield new

manufacturing paradigms #2 – Matrix - Pick new manufacturing technology

paradigms that apply across range of manufacturing sectors

#3 – Technology alone is not enough – also need process and business model

#4 –Fuse Services and Manufacturing#5 – Other nations - Better look over our

shoulder #6 – Build the Workforce #7 – Innovation Organization – Look at those

intermediary stages#8 – Build Regional Infrastructure#9 – Financing – The 5 vs. 10 year yardstick

37

Remember: Manufacturing Scales

Economics focused on “decreasing returns”

Brian Arthur – helped us understand “increasing returns” tech advance lock in a standard, geometric increaseExs.: railroads, cars, Microsoft operating

system,desktops, iPod-iPad-iPhone,

Services scale slowly – face to face

Manufacturing key to “increasing returns” in an economy – fundamental to strong growth

38

Wrap- up:Focus here is innovation, the supply side

– the demand side also needs attention: taxes, trade, regulation -- But: it’s STRUCTURAL NOT MACRO-ECONOMIC

Remember the Hourglass - we must understand the tie between production and other employment sectors – that’s why mfg. must be taken seriously

And Remember, Manufacturing Scales – key to growth

39