The Cultural Industries in CARICOM: Trade, Investment ... · The Cultural Industries in CARICOM:...

22

The Cultural Industries in CARICOM: Trade, Investment & Development Challenges Dr. Keith Nurse Senior Lecturer, Institute of International Relations, UWI. Coordinator, Arts and Cultural Enterprise Management Programme, Director, bloom: creative industries exchange

Transcript of The Cultural Industries in CARICOM: Trade, Investment ... · The Cultural Industries in CARICOM:...

The Cultural Industries in CARICOM:Trade, Investment & Development Challenges

Dr. Keith NurseSenior Lecturer, Institute of International Relations, UWI.Coordinator, Arts and Cultural Enterprise Management Programme, Director, bloom: creative industries exchange

2

Key Elements of the EU Proinvest - CRNM Study

• Phase 1 - Global & Regional Situational Analysis

• Phase 2 - Economic Impact Assessment and Competitiveness Analysis

• Phase 3 - Trade & Industrial Policies• Phase 4 - Strategic Industrial Action Plan

Synergies between theCreative Economy & Other Sectors

CREATIVE ARTS

CREATIVE INDUSTRIES

CREATIVE ECONOMY

ICTs

Intellectual Property

Tourism

Ecommerce

Services

Media

Arts Education

Manufacturing

The Creators

Composers/Songwriters Performing artistsAuthors

Secondary Investors

Facilitators

Primary Investors

Manufacturers (CDs, DVDs, Print)Distribution (Import/export, wholesale) Retailers, Venue operators, Broadcasters

ManagersBooking agentsTicket agentsLawyers/accountantsPromotion/advertisingTechnical services

• Purchases of (CDs, books, videos)• Audience at public performance

venues/exhibitions• Live performance (club, concert,

theatre)

• listeners to broadcast (radio, TV, Internet)

• subscribers to online services

Consumer(The Audience)

The Value – Chain in the Creative Industries

Publishers Record CompaniesPromotersDirectors

5

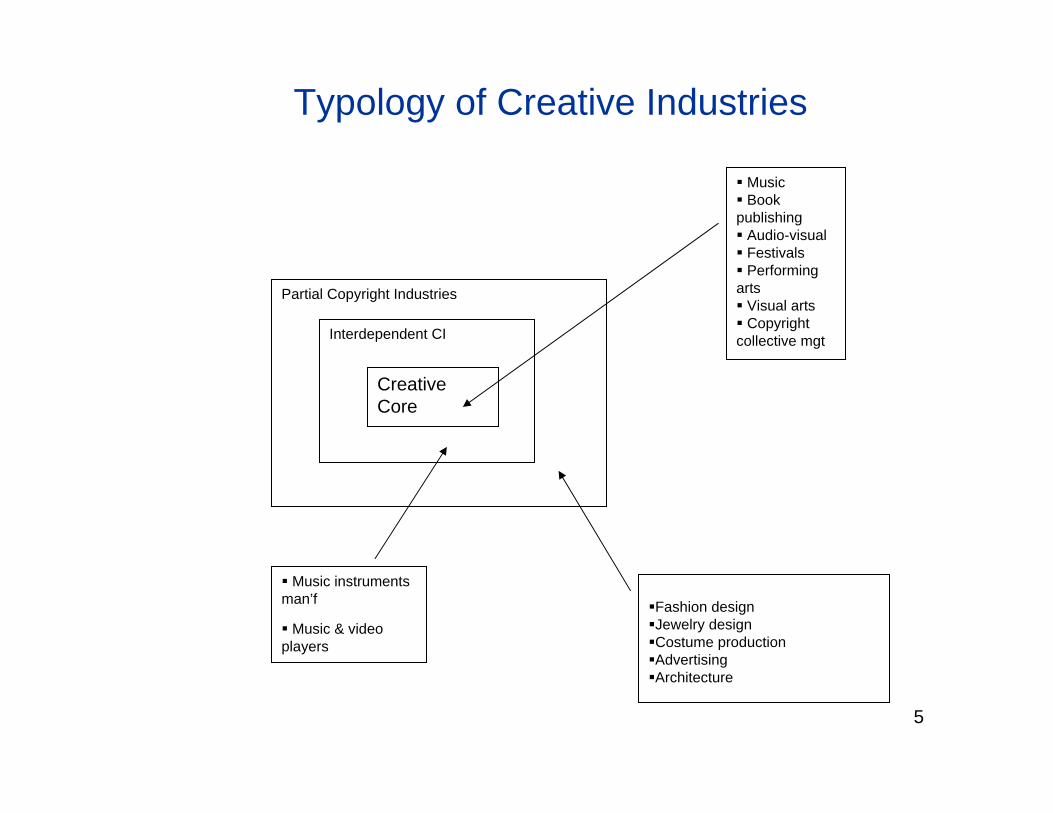

Typology of Creative Industries

Creative Core

Interdependent CI

Partial Copyright Industries

MusicBook

publishingAudio-visualFestivalsPerforming

artsVisual artsCopyright

collective mgt

Music instruments man’f

Music & video players

Fashion designJewelry designCostume productionAdvertisingArchitecture

6

Income Streams in the Creative Industries

Goods

Visible EarningsBooksCDsDVDsPaintingsMusic

instrumentsGarments &

jewelry

Services

Invisible EarningsLive

performancesDesign servicesRecord

engineeringLegal services

Intellectual property

Invisible EarningsRoyalty incomeLicensing feesCollective

administrationDigital rights

management

7

Global Trends

Global estimates forecast that the creative industries

will grow by 33% in the next four years (PWC, Entertainment & Media Report, 2005 - 2009).

Consumer demand for creative content is driving the

new sales (30 - 50%) in computers, broadband, cell phones, ecommerce (IFPI Music & Internet, 2006).

8

Regional Context for the Creative Industries

The Caribbean has significant capability and untapped potential in the creative industries.

The global demand for Caribbean creative industries is growing and provides good returns on investment.

The Caribbean can improve its competitiveness once the human resources, innovation pathways, industry institutions and governmental agencies are upgraded and harmonized.

9

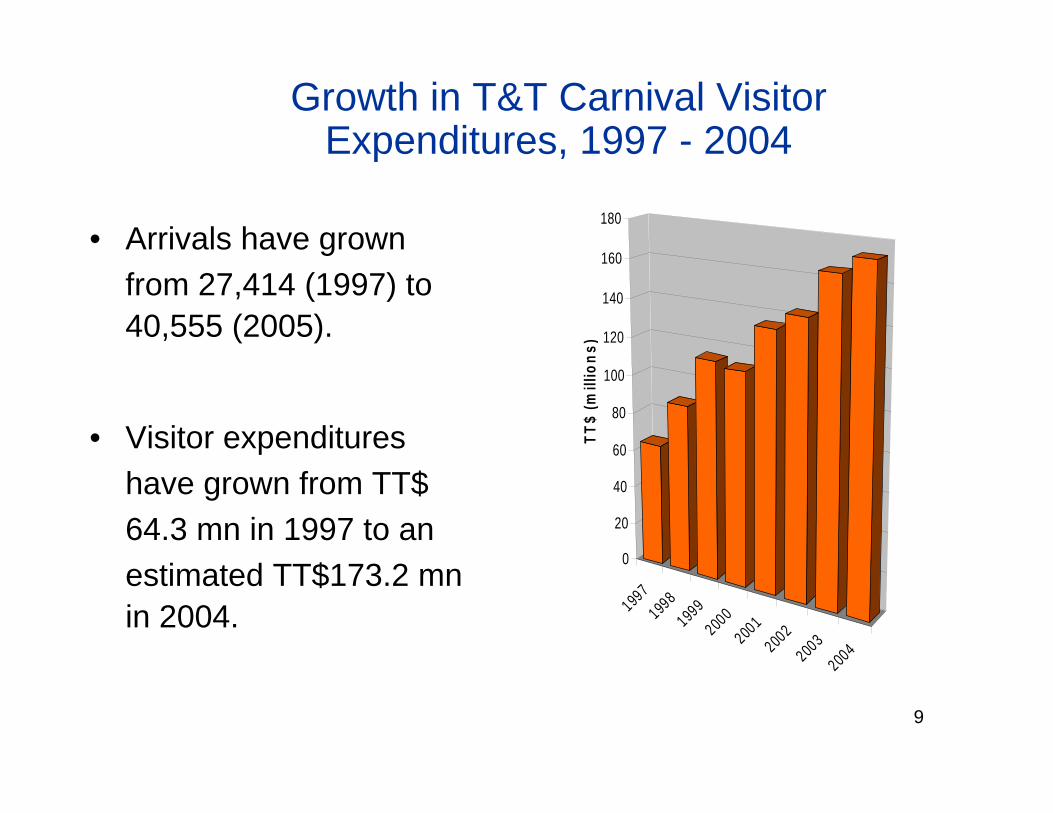

Growth in T&T Carnival Visitor Expenditures, 1997 - 2004

• Arrivals have grown from 27,414 (1997) to 40,555 (2005).

• Visitor expenditures have grown from TT$ 64.3 mn in 1997 to an estimated TT$173.2 mn in 2004. 1997

19981999

20002001

20022003

2004

0

20

40

60

80

100

120

140

160

180

TT$

(mill

ions

)

Top Selling Caribbean Artists in the US Market

24

12

8.5

6.5 6.5 6

4 3.5 32.5 2 2

0

5

10

15

20

25U

nits

(in

milli

ons)

Bob M

arley

Shagg

yBilly

Oce

anBah

a Men

Wyc

lef Je

anSea

n Pau

l

Juan

Luis

Guerra

Celia C

ruz

Harry B

elafon

teRiha

nna

Peter T

osh

Eddy G

rant

Source: RIAA.com* The RIAA®'s certification levels are based on unit shipments (minus returns) from manufacturers to a wide range of accounts, including non-retail record clubs, mail order houses, specialty stores, units shipped for Internet fulfilment or direct marketing sales, such as TV-advertised albums.

11

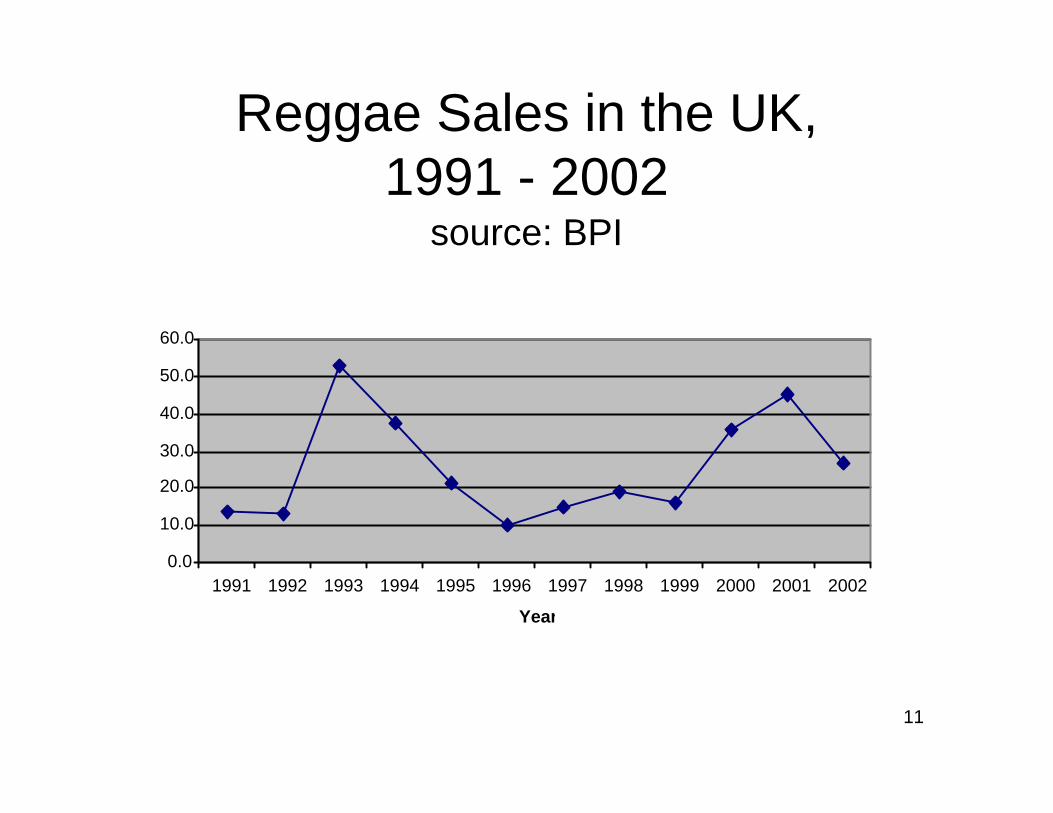

Reggae Sales in the UK,1991 - 2002

source: BPI

0.0

10.0

20.0

30.0

40.0

50.0

60.0

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Year

12

ECONOMIC IMPACT OFCARIBBEAN MUSIC INDUSTRY

•Festival tourism•Live performance•Recording industry

•$20 - 25mEastern Caribbean

•Live performance•Festival tourism•Recording industry

•$20 - 25mBarbados

•Festival tourism•Live performance•Recording industry

•$50 - 60mTrinidad & Tobago

•Recording industry•Live performance•Festival tourism

• $80 - 100m•15,000 persons

Jamaica

Key sub-sectorsFEX (US$m)Employment

Countries

Caribbean Exports & Imports of Books for 2002

1.3

169.4

0.2 2.59.6

64.5

7.92.7

0

20

40

60

80

100

120

140

160

180

Exp

orts

(U

S$

000'

s)

Anguil

laBarb

ados

Belize

Domini

caGren

ada

Guyan

aJa

maica

St. Luc

ia

St. Vinc

ent &

Gren

adine

s

7,479.10

38,202.00

0

5000

10000

15000

20000

25000

30000

35000

40000

Impo

rts

(US$

000

's)

Anguil

laBarb

ados

Belize

Domini

caGren

ada

Guyan

aJa

maica

St. Luc

ia

St. Vinc

ent &

Gre

nadin

es

Source: Adapted from UNESCO (2005) Study on International Flows of Cultural Goods between 1998–2002.

14

Comparing the Caribbean with other Countries

-60000

-40000

-20000

0

20000

40000

60000

Barbados Fiji Jamaica Mauritius

Cultural Merchandise Trade, Selected SIDS, 2002

ExportsImportsBalance

15

REALITIES OF THE MARKETPLACE

• Strong capabilities in artistic/creative production but weak entrepreneurial/industrial context.

• A small but lucrative domestic market dominated to a great extent by foreign firms, imports and broadcasts.

• Small companies that are reliant on external firms and agents for distribution and export marketing.

• Increased contribution to exports, employment, GDP and the tourism sector.

• Harmonization & internationalization of copyright regulations (WTO-TRIPs, WIPO copyright & digital treaties).

16

BUSINESS & TECHNOLOGY PARADIGM

• Outdated production and artistic facilities.• Reliance on external manufacturing, distribution,

promotions and export marketing.

• Rapid transformations in products, production and distribution processes (e.g. Internet, MP3, ecommerce, iPod, iTunes, youtube).

• Concentration of firms and convergence of media in the various cultural industries (e.g. multimedia).

• Copyright protection and enforcement being challenged by new technologies (e.g. P2P file sharing).

17

THE OPERATING ENVIRONMENT

• Under-developed infrastructure in terms of trade, industrial and intellectual property policy.

• Weak institutional capacity and advocacy capability.

• Shortage of training and upgrading in the artistic & entrepreneurial aspects.

• The role of government in funding & investing in the cultural industries is largely under-developed.

18

RATIONALE FOR REGIONAL TRADE/INDUSTRIAL/INNOVATION

POLICY

• To address the problem of market failure.• To assist resource reallocation from declining

to rising sectors. • To correct externalities associated with

specific industries. • To enhanced the competitiveness of regional

firms in globally oligopolistic markets.

19

SPECIFIC NEEDS OF THE CULTURAL INDUSTRIES

• Investment in human capital development is a critical area because the cultural industries start with the creativity of the artist.

• Intellectual property protection & administration is essential to stymie copyright infringement and recoup investment

• Heavy marketing (e.g. media access) and brandingbased on genre is required to build audience loyalty and create hits.

• Innovation and technological upgrading is vital to boost global competitiveness.

20

STRATEGIC REGIONAL GOALS

• Improve institutional capacity, networking and advocacy capability of industry (e.g CCL, CME, CAPNET).

• Upgrade training in the artistic & entrepreneurial aspects (e.g. UWI-ACEM).

• Advocate for trade policy in services and intellectual property (e.g. CRNM, Min of Trade, IPOs).

• Align government funding & investment with the goals of the cultural industries (JAMPRO, BDC,TIDCO, OECS-EDU).

21

STRATEGIC REGIONAL GOALS

• Boost competitiveness & export capabilities through business support services, trade fairs (Caribbean Export, JAMPRO, TIDCO, OECS-EDU).

• Identify benchmarks and document sector’s performance (GDP, exports, employment).

• Continuous strategic planning for each of the sectors.

• Establish institutional capacity to conduct research and marketing intelligence (UWI).

Creative Industries Exchange

International Organizations:UNESCO, CISAC, WIPO, IFPI, IPA

bloomcreative industries exchange

CaribbeanExport

RCC

Industry Assoc

CopyrightOrganizationsTourism

Agencies

CSOs

CRNM