The crisis and ArcelorMittal post crisiscorporate.arcelormittal.com/~/media/Files/A/... · ·...

22

The crisis and ArcelorMittal post crisis 16 September 2009 – Investor day – London & New York Lakshmi Mittal – Chairman and Chief Executive Officer

Transcript of The crisis and ArcelorMittal post crisiscorporate.arcelormittal.com/~/media/Files/A/... · ·...

The crisis and ArcelorMittal post crisis

16 September 2009 – Investor day – London & New York

Lakshmi Mittal – Chairman and Chief Executive Officer

1

Disclaimer

Forward-Looking Statements This document may contain forward-looking information and statements about

ArcelorMittal and its subsidiaries. These statements include financial projections and estimates and their underlying assumptions, statements regarding plans, objectives and expectations with respect to future operations, products and services, and statements regarding future performance. Forward-looking statements may be identified by the words “believe,” “expect,” “anticipate,”“target” or similar expressions. Although ArcelorMittal’s management believes that the expectations reflected in such forward-looking statements are reasonable, investors and holders of ArcelorMittal’s securities are cautioned that forward-looking information and statements are subject to numerous risks and uncertainties, many of which are difficult to predict and generally beyond the control of ArcelorMittal, that could cause actual results and developments to differ materially and adversely from those expressed in, or implied or projected by, the forward-looking information and statements. These risks and uncertainties include those discussed or identified in the filings with the Luxembourg Stock Market Authority for the Financial Markets (Commission de Surveillance du Secteur Financier) and the United States Securities and Exchange Commission (the “SEC”) made or to be made by ArcelorMittal, including ArcelorMittal’s Annual Report on Form 20-F for the year ended December 31, 2008 filed with the SEC. ArcelorMittal undertakes no obligation to publicly update its forward-looking statements, whether as a result of new information, future events, or otherwise.

2

Agenda

• The crisis and ArcelorMittal• The steel market post crisis• ArcelorMittal post crisis

3

The crisis and ArcelorMittal

4

Since September 2008, steel demand has fallen by mo re than 50% in Europe and the US*estimates at crisis trough**West EuropeSources: World Steel Association (WSA) and ArcelorMittal

US crude steel production and capacity utilization during crisis

The worst crisis in the developed world since the 30’s

-80%

-60%

-40%

-20%

0%

1932vs

1929

1945vs

1939

1975vs

1974

1983vs

1979

1993vs

1989

2009Evs

2007

20%

40%

60%

80%

100%

Steel production decline (LH)

Annual capacity utilisation* (RH)

Europe** crude steel production and capacity utilization during crisis

-80%

-60%

-40%

-20%

0%

1932vs

1929

1946vs

1944

1958vs

1955

1975vs

1973

1982vs

1978

1991vs

1988

2009Evs

2007

20%

40%

60%

80%

100%

Steel production decline (LH)

Annual capacity utilisation* (RH)

5

ArcelorMittal 3 dimensional strategy based on its h igh level of geographic diversification, value added products and integration mitigates cris is but had to be reinforced

* South America, Africa and CIS** China, Asia, Europe and US average (source SBB)*** Downstream integration is calculated as shipments distributed through AM3S divided by total shipments to steel service centers

ArcelorMittal shipments by region (base 100 in Q2 08)

ArcelorMittal upstream and downstream integration (%)

ArcelorMittal steel price and spot global HRC price (USD/t)

ArcelorMittal pre-existing strategy was not sufficient to face such a crisis

ProductGeography Value Chain

40

50

60

70

80

90

100

110

2Q08 3Q08 4Q08 1Q09 2Q09

North America Europe Emerging*

400

500

600

700

800

900

1,000

1,100

1,200

1,300

2Q08 3Q08 4Q08 1Q09 2Q09

ArcelorMittal price Spot global HRC price**

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

2Q08 3Q08 4Q08 1Q09 2Q09

Iron ore integration Distribution integration***

6

ArcelorMittal reaction to crisis

ArcelorMittal quarterly crude steel production (million tonnes)

Production cut announced in September 2008 and new industrial and financial plan initiated in October 2008

0

5

10

15

20

25

30

35

Q1 20

06Q2

2006

Q3 20

06Q4

2006

Q1 20

07Q2

2007

Q3 20

07Q4

2007

Q1 20

08Q2

2008

Q3 20

08Q4

2008

Q1 20

09Q2

2009

Production reduced by 50% since Q4 2008

Main industrial and financial initiatives:

• September 2008: Production cut announced

• October 2008: CAPEX plan cut, debt reduction target set, SG&A cost reduction plan initiated

• Q4 2008: Net debt reduced by USD 6bn

• February 2009: Cost cutting accelerated, working capital target announced, dividend cut, refinancing initiated (forward start facilities)

• April 2009: Issuance of convertible bonds• May 2009: Capital increase• May & June 2009: Issuance of bonds resulting in

total of USD 11.4bn of financing in Q2• End June 2009: Year-end debt reduction target

of USD 10bn nearly achieved

7* Assuming 5% cost reduction** Assuming plants hot-iddle cost is 25% of full costSources: World Steel Dynamics, CRU monitor, Annual reports, Bloomberg and ArcelorMittal estimates

Annual average HRC production cost with overhead

Cumulative capacity, m tonnes

Cash cost USD/tonne

0

200

400

600

800

1000

1200

0 50 100 150 200 250 300 350 400 450

Cost leadership has been maintained due in particul ar to active industrial optimisation, allowing positive operating cash-flow throughout the crisis

2008

2009e

ArcelorMittal weighted average target

ArcelorMittal cost leadership

100% output

60% output

Fixed cost per tonne base 100

Fixed cost base 100 *

Increase in fixed cost per tonne

Concept of optimisation

Full

Single unit steelmaker Multi-unit steelmaker

100 100

95 100 100 100 25** 25**

100 100

Average 70

+58% +17%

Hot-Idle

Full Full Full Full Full

Full Full Full

100 100

60%

8

Despite running at less than 50% of capacity utilis ation and facing a decline of more than 60% in steel spot price*, cash-flow from opera tion has remained positive

ArcelorMittal financial flexibility and strength

ArcelorMittal fixed costs annualised (in billion USD)

15

20

25

30

2008 Q4 2008 Q1 2009 Q2 2009

Sustainable SG&A and fixed cost reduction

Temporary fixed cost reduction

Actual Fixed cost

ArcelorMittal cash-flow from operation (in billion USD)

More than USD 10 billion of fixed cost

reduction

0

1

2

3

4

5

6

7

1Q 2

006

2Q 2

006

3Q 2

006

4Q 2

006

1Q 2

007

2Q 2

007

3Q 2

007

4Q 2

007

1Q 2

008

2Q 2

008

3Q 2

008

4Q 2

008

1Q 2

009

2Q 2

009

* From peak to trough

9

The steel market post crisis

10

Markets are not expected to normalise in Europe and the US in 2010*US and EU-15Sources: WSA and ArcelorMittal estimates

A slow and uncertain recovery in developed world…

Annual apparent steel demand in western world* (in Mt)

Monthly apparent steel demand in western world* (in Mt)

10

15

20

25

30

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

150

170

190

210

230

250

270

290

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

e20

12e

11*US, Canada, EU-15 and JapanSources: WSA and ArcelorMittal estimates

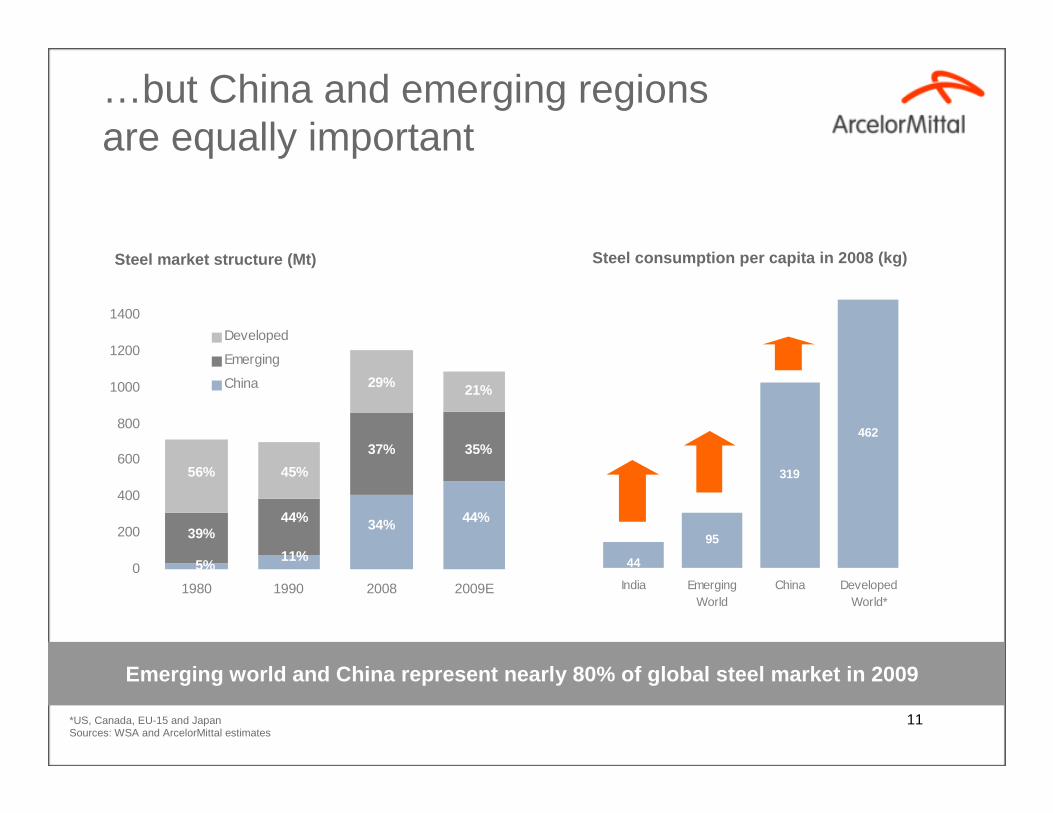

…but China and emerging regions are equally important

Steel market structure (Mt) Steel consumption per capita in 2008 (kg)

0

200

400

600

800

1000

1200

1400

1980 1990 2008 2009E

Developed

Emerging

China

56% 45%

29%

39%44%

37%

5%11%

34%

21%

35%

44%

95

319

462

44

India EmergingWorld

China DevelopedWorld*

Emerging world and China represent nearly 80% of gl obal steel market in 2009

12

Chinese domestic demand expected to increase by mor e than 15% in 2009

*Since crisis troughSources: WSA and ArcelorMittal

China is booming again and emerging markets are recovering rapidly

Chinese steel apparent demand (y-o-y) Crude steel production in South America (000’t)

Crude steel production in CIS (000’t)

5,000

7,000

9,000

11,000

13,000

Jan 05 Jan 06 Jan 07 Jan 08 Jan 09

2,000

3,000

4,000

5,000

Jan 05 Jan 06 Jan 07 Jan 08 Jan 09

+45%*

+43%*

-30%

-20%

-10%

0%

10%

20%

30%

40%

Jan-0

2Ja

n-03

Jan-0

4Ja

n-05

Jan-0

6Ja

n-07

Jan-0

8Ja

n-09

+31% in July

13

Chinese steel demand expected to slowdown in 2010 b ut to continue to growSources: WSA, SBB and ArcelorMittal estimates

Steel consumption per capita in 2008e (kg)

Western China

(160 kg)Coastal

China

(525kg)

Central China

(215 kg)

Development and growth potential

Population migration

Steel consumption per capita in 2008 (kg)

Chinese steel apparent demand (mt)

319597 717

1210

0

200

400

600800

10001200

1400

China Japan Taiw an Korea

Chinese growth is driven by stimulus plan and solid fundamentals

0

100

200

300

400

500

600

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

P20

12P

14

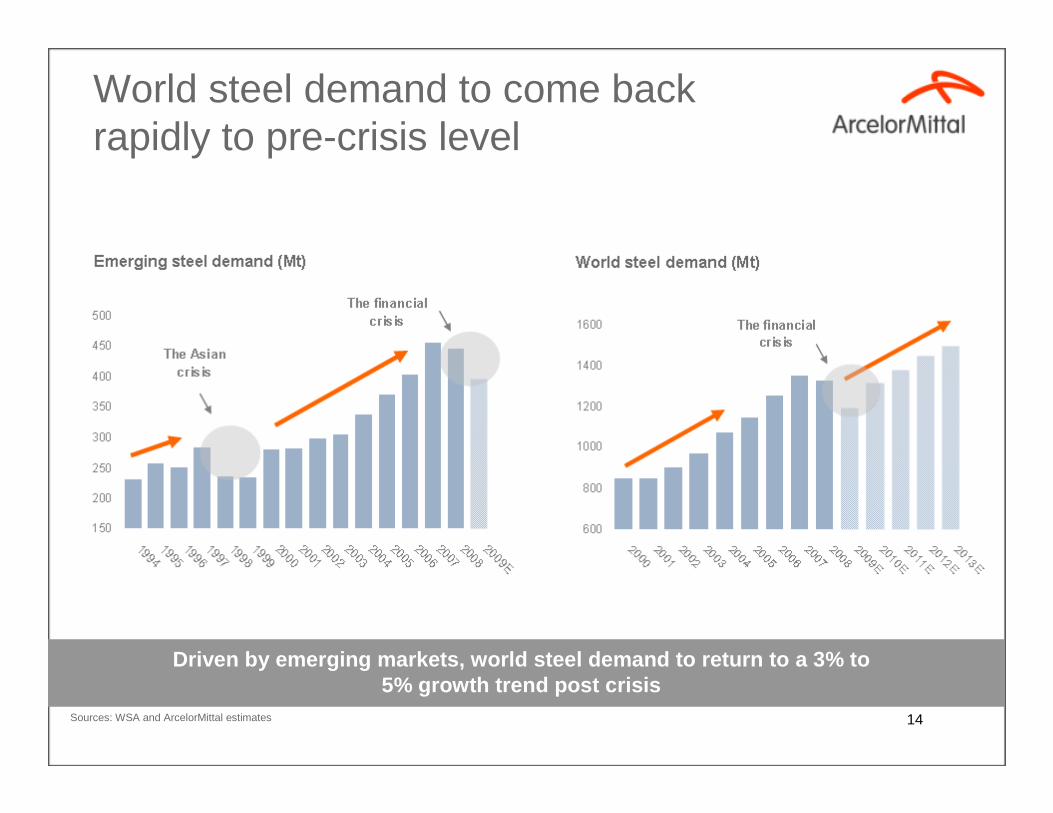

Driven by emerging markets, world steel demand to r eturn to a 3% to 5% growth trend post crisis

Sources: WSA and ArcelorMittal estimates

World steel demand to come back rapidly to pre-crisis level

Emerging steel demand (Mt) World steel demand (Mt)

15

ArcelorMittal post crisis

16* Finished steel

Capturing market recovery while controlling invento ry and cost

A more flexible industrial network and cautious production restarts

ArcelorMittal HRC cost curve average 2006-2008 (USD /t)ArcelorMittal steel production and shipments (Mt)

0

5

10

15

20

25

30

35

Q3 20

07Q4

2007

Q1 20

08Q2

2008

Q3 20

08Q4

2008

Q1 20

09Q2

2009

Q3 20

09E

Steel production* Steel shipments

200

300

400

500

600

700

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

ArcelorMittal capacity

Plants and units to be progressively restarted according to cost and market position

Production in line with demand

17

Maintaining focus on sustainable management gains

0.41.2

1.72.0

3.0

0

1

2

3

4

Q2 2008 Q1 2009 Q2 2009 Q4 2009 Q4 2010

Captured Target

Management gains 2010

20%

Management gains plan

beyond 201040%

Fixed cost and SG&A cost

reduction 200940%

USD 5 billion of sustainable management gains target by 2012, of which USD 3 billion by 2010

5 years management gains plan breakdownManagement gains progress (USD billion annualised)

18

Optimizing supply chain and working capital

Significant improvement in working capital and supp ly chain is possible

ArcelorMittal steel shipments and inventory Working capital (rotation days)

50

100

150

Q12007

Q22007

Q32007

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009E

Steel shipments (base 100) Steel inventory (base 100)

Under inventory

ArcelorMittal iron ore consumption and inventory

0

20

40

60

80

100

120

140

2Q2006

3Q2006

4Q2006

1Q2007

2Q2007

3Q2007

4Q2007

1Q2008

2Q2008

3Q2008

4Q2008

1Q2009

2Q2009

Target

50

100

150

Q12007

Q22007

Q32007

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009E

Iron ore consumption* (base 100) Iron ore inventory (base 100)

Over inventory

* Total group consumption based on crude steel production

19

ArcelorMittal sales breakdown in Q2 2009

ArcelorMittal key emerging markets currently target ed for growth

ArcelorMittal’s leading position in emerging market s offers high growth potential

Reinitiating some projects to capture growth in key emerging markets

US & Canada

14%

EU-1538%

Emerging48%

20

Managing mining assets for an optimum level of self-sufficiency

Iron ore

Key mining assets and projectsArcelorMittal steel and iron ore production

Mining expansion to continue and internal raw materi al flow to be adjusted to new flexible industrial model

50

60

70

80

90

100

110

120

130

Q12007

Q22007

Q32007

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Crude steel production (base 100) Iron ore production (base 100)

Self-sufficiency increased

Coal

21