THE COST LANDSCAPE OF SOLAR AND WIND - …€¦ · · 2016-06-08THE COST LANDSCAPE OF SOLAR AND...

29

THE COST LANDSCAPE OF SOLAR AND WIND Nicholas Culver January 2015 Americas Insight

Transcript of THE COST LANDSCAPE OF SOLAR AND WIND - …€¦ · · 2016-06-08THE COST LANDSCAPE OF SOLAR AND...

THE COST LANDSCAPE OF SOLAR AND WIND

Nicholas Culver

January 2015

Americas Insight

1

AGENDA

PREFACE: RENEWABLES IN CONTEXT

SOLAR

WIND

ROUND UP

2

● Clean energy investment in the US since 2007 has been $386bn

● Investment in 2014 rebounded by 7% from 2013 levels, and is 5x higher than a decade ago

US CLEAN ENERGY INVESTMENT – TOTAL NEW INVESTMENT, ALL ASSET CLASSES ($BN)

Source: Bloomberg New Energy Finance

Notes: Shows total clean energy investment in the US across all asset classes (asset finance, public markets, venture capital / private equity) as well as corporate and government R&D, and small

distributed capacity (rooftop PV). The definition of ‘clean energy’ used here is: renewable energy, energy smart technologies (digital energy, energy storage, electrified transportation), and other low-carbon

technologies and activities (carbon markets value chain, companies providing services to the clean energy industry). Values in both charts include estimates for undisclosed deals and are adjusted to

account for re-invested equity. Values are in nominal dollars.

$10.3

$16.7

$34.6

$41.3$43.8

$35.4

$48.0

$65.2

$52.4$48.1

$51.8

0

10

20

30

40

50

60

70

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

3

● Wind and solar both saw increased levels of build in 2014, relative to 2013 levels, but for different reasons:

● Solar build increased by 40%. The utility-scale side of the industry brought online projects that have been driven by state

renewable energy mandates and by the long-standing federal Investment Tax Credit (ITC). (The ITC is due to drop in value at

the end of 2016.) The small-scale side capitalized on economics that increasingly make solar an attractive alternative to retail

rates in much of the US

● Wind build bounced back due to policy swings. The Production Tax Credit expired at the end of 2012, dampening build in

2013. The incentive was renewed at the beginning of 2013, and it took the industry a year to reconstruct pipelines and bring

projects to completion, hence the uptick in 2014. The pipelines show strong years in 2015-16.

● Other sectors – biomass, biogas, waste-to-energy, geothermal, hydro – are languishing without long-term policy certainty

Source: Bloomberg New Energy Finance, EIA

Notes: Numbers include utility-scale (>1MW) projects of all types, rooftop solar, and small- and medium-sized wind.

US POWER OVERVIEW: RENEWABLE ENERGY CAPACITY BUILD BY TECHNOLOGY (GW)

9.210.5

4.56.6

14.0

0.5

4.7

0.3

0.4

0.9

2.0

3.3

4.9

7.2

10.0

11.6

5.8

9.0

18.1

6.5

12.2

2

4

6

8

10

12

14

16

18

20

2008 2009 2010 2011 2012 2013 2014

Hydro

Geothermal

Biomass, biogas,waste

Solar

Wind

4

US cumulative renewable capacity by technology

(including hydropower) (GW)

US cumulative non-hydropower renewable

capacity by technology (GW)

● Power-generating capacity of non-hydropower renewables surpassed hydropower capacity for the first time

● US non-hydropower renewable capacity has increased by 2.5x since 2008, mostly due to new wind and solar

US POWER OVERVIEW: CUMULATIVE RENEWABLE ENERGY CAPACITY BY TECHNOLOGY

Source: Bloomberg New Energy Finance, EIA

Notes: Hydropower capacity includes pumped hydropower storage facilities.

25.836.1 40.7

47.2

61.2 61.7 66.4

1.2

1.92.8

4.9

8.113.0

20.3

11.1

11.511.8

12.0

12.313.0

13.0

3.1

3.23.3

3.3

3.43.5

3.5

41

5359

67

8591

103

20

40

60

80

100

120

2008 2009 2010 2011 2012 2013 2014

Geothermal

Biomass, biogas,waste

Solar

Wind

100 101 101 101 101 101 101

41 53 59 6785 91 103

141153 160

168

186 193 205

50

100

150

200

2008 2009 2010 2011 2012 2013 2014

Otherrenewables

Hydropower

5

US electricity generation by fuel type (%) US electricity generation by fuel type (TWh)

● The US electricity mix in 2014 was nearly identical to 2013 levels. Natural gas’s contribution is off of the record high achieved

in 2012, when the fuel’s prices sank to historic lows. This up-and-down in natural gas’s market share is a cyclical effect

● Longer term, though, larger structural trends are afoot: the US power sector is gradually decarbonizing. Coal plants are being

retired, and natural gas and renewables are gaining ground: from 2007 to 2014, natural gas increased from 22% to 27% of

the mix, and renewables climbed from 8% to 13%

US POWER OVERVIEW: ELECTRICITY GENERATION MIX

Source: EIA

Notes: Values for 2014 are projected, accounting for seasonality, based on latest monthly values from EIA (data available through September 2013). In chart at left, contribution from ‘Other’ is not shown;

the amount is minimal and consists of miscellaneous technologies including hydrogen and non-renewable waste. In chart at right, contribution from CHP is indicated by a shaded bar in each of the columns.

The hydropower portion of ‘Renewables’ includes negative generation from pumped storage.

49% 48% 44% 45% 42%37% 39% 39%

19.4%19.6%20.2%19.6%

19.3%19.0%19.4%19.4%

22% 22%24% 24%

25%31% 28% 27%

8% 9% 10% 10% 12% 12% 13% 13%

0%

20%

40%

60%

80%

100%

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Renewables(including hydro)

Natural gas

Nuclear

Oil

Coal0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

CHP

Renewables(including hydro)

Natural gas

Nuclear

Oil

Coal

6

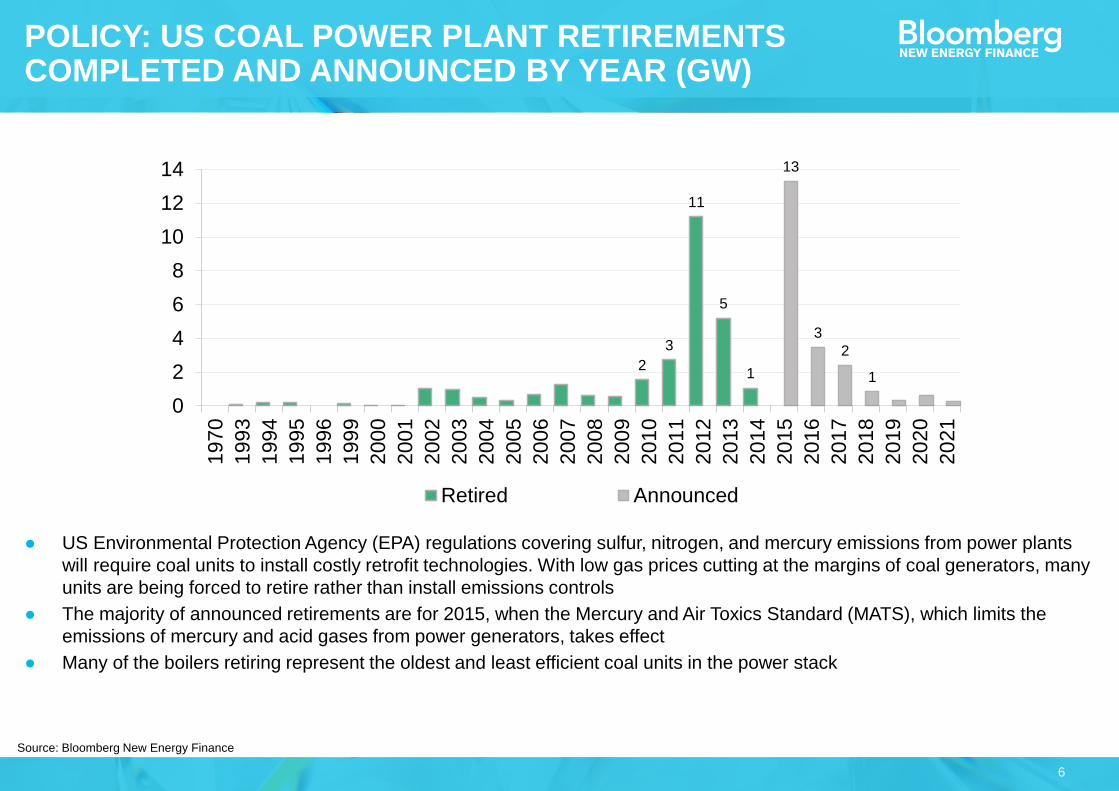

POLICY: US COAL POWER PLANT RETIREMENTS COMPLETED AND ANNOUNCED BY YEAR (GW)

● US Environmental Protection Agency (EPA) regulations covering sulfur, nitrogen, and mercury emissions from power plants

will require coal units to install costly retrofit technologies. With low gas prices cutting at the margins of coal generators, many

units are being forced to retire rather than install emissions controls

● The majority of announced retirements are for 2015, when the Mercury and Air Toxics Standard (MATS), which limits the

emissions of mercury and acid gases from power generators, takes effect

● Many of the boilers retiring represent the oldest and least efficient coal units in the power stack

2

3

11

5

1

13

3

2

1

0

2

4

6

8

10

12

14

1970

1993

1994

1995

1996

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Retired Announced

Source: Bloomberg New Energy Finance

7

ECONOMICS: COST OF GENERATING ELECTRICITY IN THE US FROM NATURAL GAS VS COAL ($/MWH)

● Power has served as the swing demand source for natural gas: when prices fall too low, gas burn rises until the differential (in

$/MWh) between the two fuels closes.

● In 2014, the cold winter drove gas prices to regional highs, giving coal a comparative advantage across the US

● The differential was particularly high in the northeast, where pipeline constraints resulted in especially high winter prices

0

10

20

30

40

50

Apr 2010 Apr 2011 Apr 2012 Apr 2013 Apr 2014

Coal

Gas(CCGT)

Source: Bloomberg New Energy Finance

Notes: Assumes heat rates of 7,410Btu/kWh for CCGT and 10,360Btu/kWh for coal (both are fleet-wide generation-weighted medians); variable O&M of $3.15/MWh for CCGT and $4.25/MWh for coal.

8

Source: Bloomberg New Energy Finance

HENRY HUB PRICE FORECAST ($/MMBTU NOMINAL)

0

2

4

6

8

10

12

2011 2013 2015 2017 2019 2021 2023 2025 2027 2029

Actual

Back to Black ($90 oil, high LNG exports)

Lean Times ($70 oil, lower LNG exports)

● Natural gas prices are historically cheap and there appears to be about a decade of cheap gas available. Gas prices

fluctuated between $6 and $14 per Mmbtu during 2004-2008.

9

0

10

20

30

40

50

60

70

1 2 3 4 5 6 7

$2.40/MMBtu = $60/ton Appalachian

$1.15/MMBtu = $20/ton PRB (delivered)

ECONOMICS: LCOE COMPARISON FOR US NATURAL GAS VS. COAL ($/MWH) AS A FUNCTION OF FUEL PRICE ($/MMBTU)

● With gas prices below $4.50/MMBtu, new natural gas plants have a lower levelised cost of electricity than new coal power

plants anywhere in the country

● The EPA’s New Source Performance Standards for carbon indicates that no new coal units could be built without carbon

capture and sequestration (CCS); that technology would push coal LCOEs even higher

● At 2014 prices, economics favored new natural gas plants new coal plants (even without accounting for CCS)

● With futures prices suggesting gas may rise above $5/MMBtu, LCOEs for natural gas and non-CCS coal will be close in value

LCOE ($/MWh)

Fuel price ($/MMBtu)

Eastern coal LCOEWestern coal

LCOEGas LCOE

Source: Bloomberg New Energy Finance

Notes: Assumes heat rates of 7,410Btu/kWh for CCGT and 10,360Btu/kWh for coal (both are fleet-wide generation-weighted medians); variable O&M of $3.15/MWh for CCGT and $4.25/MWh for coal.

10

AGENDA

PREFACE: RENEWABLES IN CONTEXT

SOLAR

WIND

ROUND UP

11

DEPLOYMENT: GLOBAL PV SUPPLY AND DEMAND

Global PV module production by country (GW) Global PV demand by country (GW)

● Bolstered by strong uptake in China and Japan, PV demand rose strongly, as the global market again reduced its reliance on

European demand centers

● Trade disputes raged on, as the US took steps to applying tariffs on Chinese and Taiwanese solar products (which still

account for much of the market). The US tariff regime to date has increased modules prices by roughly ~$0.15, but so far low-

cost Chinese producers have largely held onto market share in the US by accepting slimmer margins

Source: Bloomberg New Energy Finance

Notes: In chart at right, 2014 values represent an average of optimistic and conservative analyst estimates.

3.612.9 13.5

7.111.1

3.3

4.7

6.3

5.15.8

5.4

5.4

3.8

7.2

7.57.6

3.3

7.93.64.4

5.0

9.7

7.7

18.2

28.330.7

40.3

48.7

10

20

30

40

50

60

2009 2010 2011 2012 2013 2014

Rest of world

Italy

Germany

Rest of EU

US

Japan

China

3.19.9

19.1 21.326.9

2.3

2.72.2

7.0

1.8

2.3

3.3 3.3

2.7

7.7

18.1

29.7 30.1

38.7

5

10

15

20

25

30

35

40

45

2009 2010 2011 2012 2013

Other

US

Norway

Germany

Japan

China

12

ECONOMICS: PRICE OF SOLAR MODULES AND EXPERIENCE CURVE ($/W AS FUNCTION OF GLOBAL CUMULATIVE CAPACITY)

● Module pricing has broadly followed the experience curve for costs for the past few decades. Prices dropped in 2012 due to

manufacturing overcapacity, but then ticked back up in 2013 as oversupply began to ease

● Module prices are down by more than 80% relative to 2007 levels

Source: Bloomberg New Energy Finance, Paul Maycock, company filings

Notes: Prices in 2013 USD.

0.1

1

10

100

1 10 100 1,000 10,000 100,000 1,000,000

Experience curve (c-Si)Module prices (Maycock)Module prices (Chinese c-Si) (BNEF)Experience curve (thin-film)Module prices (thin-film) (First Solar)

2003

2006

2012

1976

1985

Q4 2013

2012

Cumulative capacity (MW)

2013

Cost ($/W)

(in 2013

dollars)

13

Source: Bloomberg New Energy Finance,

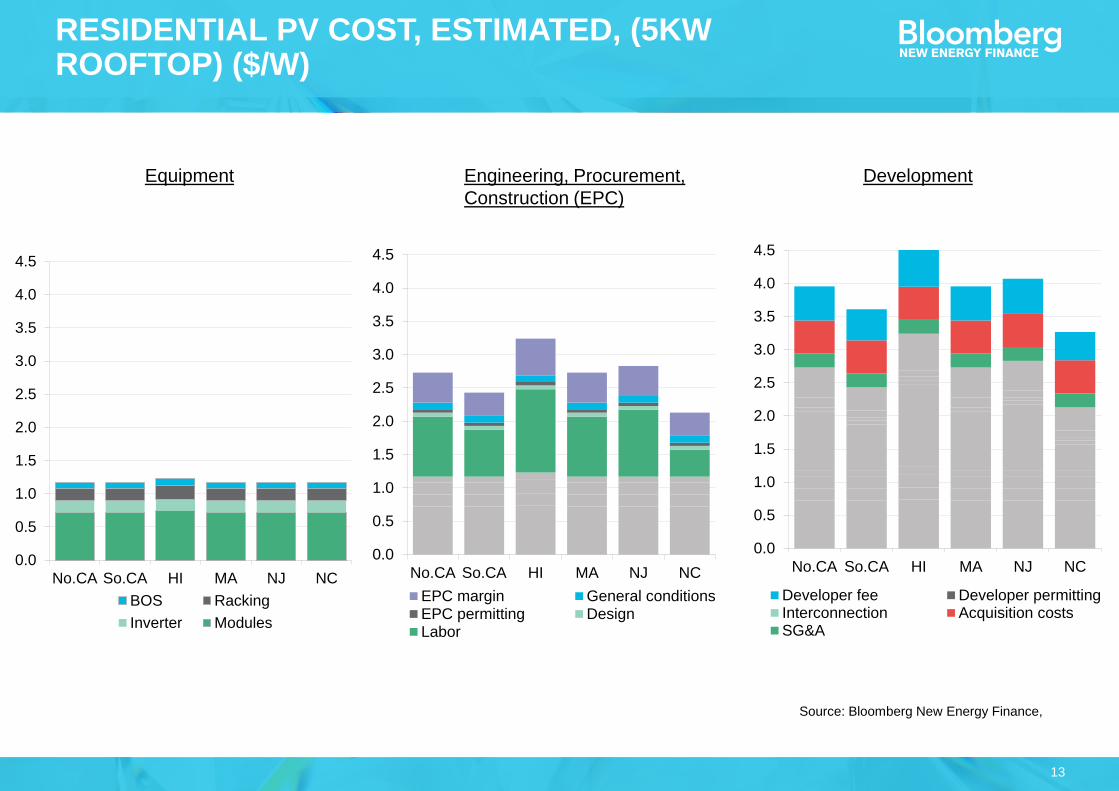

RESIDENTIAL PV COST, ESTIMATED, (5KW ROOFTOP) ($/W)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

No.CA So.CA HI MA NJ NC

BOS Racking

Inverter Modules

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

No.CA So.CA HI MA NJ NC

EPC margin General conditionsEPC permitting DesignLabor

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

No.CA So.CA HI MA NJ NC

Developer fee Developer permittingInterconnection Acquisition costsSG&A

Equipment Engineering, Procurement,

Construction (EPC)

Development

14

Source: Bloomberg New Energy Finance,

RESIDENTIAL PV COST – SO. CALIFORNIA, ESTIMATED HISTORICAL AND FORECAST ($/W)

0

1

2

3

4

5

6

7

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

202

3

202

4

202

5

202

6

202

7

202

8

202

9

203

0

Development

Engineering,Procurement,Construction

Equipment

15

Source: Bloomberg New Energy Finance,

CALIFORNIA RESIDENTIAL PV: SUBSIDISED VERSUS UNSUBSIDISED

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014

No state subsidy CSI-funded

16

Source: Bloomberg New Energy Finance,

UTILITY-SCALE PV COST, ESTIMATED, (10MW GROUND-MOUNT) ($/W)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

No.CA So.CA HI MA NJ NC

BOS Racking

Inverter Modules

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

No.CA So.CA HI MA NJ NC

EPC margin General conditions

EPC permitting Design

Labor

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

No.CA So.CA HI MA NJ NC

Developer fee Developer permitting

Interconnection SG&A

Equipment Engineering, Procurement,

Construction (EPC)

Development

17

Source: Bloomberg New Energy Finance,

UTILITY-SCALE PV COST – NORTH CAROLINA, ESTIMATED HISTORICAL AND FORECAST ($/W)

0

1

2

3

4

5

6

7

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

202

3

202

4

202

5

202

6

202

7

202

8

202

9

203

0

Development

Engineering,Procurement,Construction

Equipment

18

Source: Bloomberg New Energy Finance,

UNITED STATES SOLAR PV FORECAST, 2010-17 (GW)

0.5 0.9 1.3 1.9 2.5 2.61.0 1.0 1.21.6

2.0 2.01.7

2.73.8

4.9

6.3

1.1

0.91.9

3.34.6

6.3

8.4

10.8

5.8

0

2

4

6

8

10

12

14

2010 2011 2012 2013 2014 2015 2016 2017

Residential Nonresidential Utility

2 47

12

18

27

38

43

0

10

20

30

40

50

2010 2011 2012 2013 2014 2015 2016 2017

Residential Nonresidential Utility

Annual Cumulative

19

Source: Bloomberg New Energy Finance,

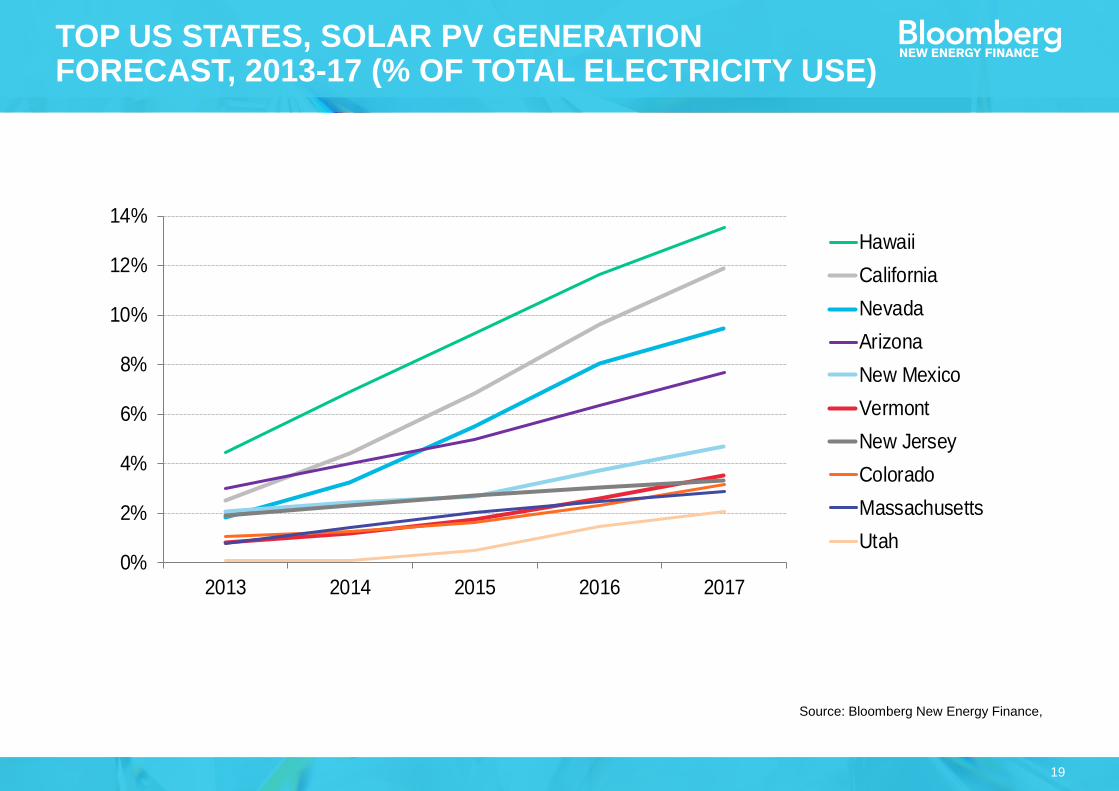

TOP US STATES, SOLAR PV GENERATION FORECAST, 2013-17 (% OF TOTAL ELECTRICITY USE)

0%

2%

4%

6%

8%

10%

12%

14%

2013 2014 2015 2016 2017

Hawaii

California

Nevada

Arizona

New Mexico

Vermont

New Jersey

Colorado

Massachusetts

Utah

20

Source: Bloomberg New Energy Finance,

ESTIMATED COST OF SOLAR PV IN NORTH CAROLINA, 2012-30

0

50

100

150

200

250

300

201

2

201

4

201

6

201

8

202

0

202

2

202

4

202

6

202

8

203

0

UtilityNonresidential

Residential

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

201

2

201

4

201

6

201

8

202

0

202

2

202

4

202

6

202

8

203

0

Capex ($/W) Levelised cost of electricity

($/MWh)

21

AGENDA

PREFACE: RENEWABLES IN CONTEXT

SOLAR

WIND

ROUND UP

22

DEPLOYMENT: US LARGE-SCALE WIND BUILD (GW)

● New build in 2014 rebounded six-fold from 2013 levels, from 0.8GW to 4.7GW

● The increase was driven by the one-year extension of the Production Tax Credit (PTC) in 2013, the key federal incentive for

wind in the US. The PTC expired at the end of December 2012, was renewed January 2013, expired December 2013 (but

wind projects qualified for the incentive by starting construction in 2013), was ‘retroactively’ renewed in December 2014 and

expired again two weeks later, at the end of 2014. The current pipeline suggests healthy build for 2015-16

● A majority of the build is occurring in Texas. The state recently completed a $7bn transmission build-out to connect windy

regions in the Panhandle and West Texas to demand centers. Wind in Texas is among the cheapest in the country, with an

unsubsidized levelized cost of electricity of around $50/MWh, due to high capacity factors (>50%) and low cost to build

Incremental Cumulative

Source: Bloomberg New Energy Finance

0.3

1.72.7

4.8

8.5

10.4

4.5

6.6

13.8

0.8

4.7

0

15

30

45

60

75

0

3

6

9

12

15

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Cumulative capacity

23

COST OF WIND, SELECTED US STATES, ($/W)

Source: Bloomberg New Energy Finance

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0H

aw

aii

Ala

ska

Verm

on

t

Ma

ssachu

se

tts

West V

irgin

ia

Ne

bra

ska

Ma

ine

Uta

h

Mic

hig

an

Ne

w Y

ork

Mis

so

uri

Wis

consin

Gra

nd

Tota

l

Puert

o R

ico

Ca

liforn

ia

Illin

ois

Mo

nta

na

Penn

sylv

an

ia

Washin

gto

n

Min

nesota

Ore

go

n

Texas

Ne

w H

am

pshire

Ma

ryla

nd

Idaho

Arizona

Okla

hom

a

India

na

Ne

w M

exic

o

Co

lora

do

South

Dakota

Ohio

Iow

a

No

rth

Dakota

Wyo

min

g

Kansas

24

LEVELISED COST OF ENERGY (LCOE) OF WIND SELECTED US STATES ($/MWH)

Source: Bloomberg New Energy Finance

0

20

40

60

80

100

120A

laba

ma

Ark

ansa

s

Geo

rgia

Ken

tucky

Lou

isia

na

Mis

sis

sip

pi

Sou

th C

aro

lina

Te

nn

essee

Arizo

na

Ne

vad

a

Ne

w M

exic

o

Flo

rid

a

Co

nn

ecticut

Ma

ssa

chu

sett

s

Ne

w H

am

pshir

e

Rh

od

e Isla

nd

Verm

ont

Ne

w Y

ork

Ma

ine

Wash

ing

ton

De

law

are

Ma

ryla

nd

Ne

w J

ers

ey

No

rth

Caro

lina

Ohio

Pen

nsylv

an

ia

Virg

inia

Uta

h

Ind

ian

a

Ore

go

n

Illin

ois

Co

lora

do

Ida

ho

Mo

nta

na

Mic

hig

an

Wis

con

sin

Mis

souri

Wyo

min

g

Ca

lifo

rnia

Iow

a

Kan

sa

s

Min

neso

ta

Ne

bra

ska

No

rth

Dako

ta

Okla

ho

ma

Sou

th D

ako

ta

Te

xas

Subsidised Unsubsidised

25

Note: Grey numbers represent our previous forecast, available here. Specifically, they correspond to a forecast based on

a scenario that assumes no PTC extension. Source: Bloomberg New Energy Finance

US NEW BUILD WIND FORECAST WITH 2014 PTC EXTENSION VS PRIOR EXPECTATIONS, 2008-2020 (GW)

9.110.4

4.56.6

13.6

0.72.3

1.6 6.2

1.0

2.5

4.6

2.3

2.54.3 3.7 3.3

9.1

10.4

4.5

6.6

13.6

0.7

4.0

9.1

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Total Yet to be announced

Announced / planning begun Permitted

Financing secured / under construction

Previous forecast

9.7

5.3

4.35.0

4.2

3.33.6

9.4

26

AGENDA

PREFACE: RENEWABLES IN CONTEXT

SOLAR

WIND

ROUND UP

27

This publication is the copyright of Bloomberg New Energy Finance. No portion of this document may be photocopied,

reproduced, scanned into an electronic system or transmitted, forwarded or distributed in any way without prior consent of

Bloomberg New Energy Finance.

The information contained in this publication is derived from carefully selected sources we believe are reasonable. We do

not guarantee its accuracy or completeness and nothing in this document shall be construed to be a representation of such

a guarantee. Any opinions expressed reflect the current judgment of the author of the relevant article or features, and does

not necessarily reflect the opinion of Bloomberg New Energy Finance, Bloomberg Finance L.P., Bloomberg L.P. or any of

their affiliates ("Bloomberg"). The opinions presented are subject to change without notice. Bloomberg accepts no

responsibility for any liability arising from use of this document or its contents. Nothing herein shall constitute or be

construed as an offering of financial instruments, or as investment advice or recommendations by Bloomberg of an

investment strategy or whether or not to "buy," "sell" or "hold" an investment.

COPYRIGHT AND DISCLAIMER

Unique analysis, tools and data for decision-makers

driving change in the energy system

MARKETS Renewable Energy

Energy Smart Technologies

Advanced Transport

Gas

Carbon and RECs

SERVICESAmericas Service

Asia Pacific Service

EMEA Service

Applied Research

Events and Workshops

Nicholas Culver