The cost is hyper-inf lation down the road

40

Monday, September 24, 2012 | www.brecorder.com/fr2012

Transcript of The cost is hyper-inf lation down the road

Monday, September 24, 2012 | www.brecorder.com/fr2012

Cont

ents

04

05

07

08

10

12

14

15

16

17

20

22

24

26

28

30

32

34

36

37

38

39

Country’s hope lies hidden in the next setupBy Ali Khizar

The cost is hyper-inf lation down the road-Dr. Hafiz A. Pasha

Fiscal Devolution: Still an Unfinished AgendaBy Rao Muhammad Asif Iqbal 7

NFC was no economic awardDr. Ashfaque Hasan Khan

Not a drop to taxSyed Bakhtiyar Kazmi

Government shying away from the bitter pill:Ibrahim Sidat

Targeted subsidies needed to tackle persistent povertyBy Zuhair Abbasi

Blanket subsidies adding to inf lationDr Mohammad Zubair Khan

Inflation sitting on the pedestal of government borrowingBy Sijal Fawad

BUDGET AT A GLANCE

ECONOMY AT A GLANCE

Corporate Tax Rate in Pakistan– Substantially highBy M. Abdul Aleem

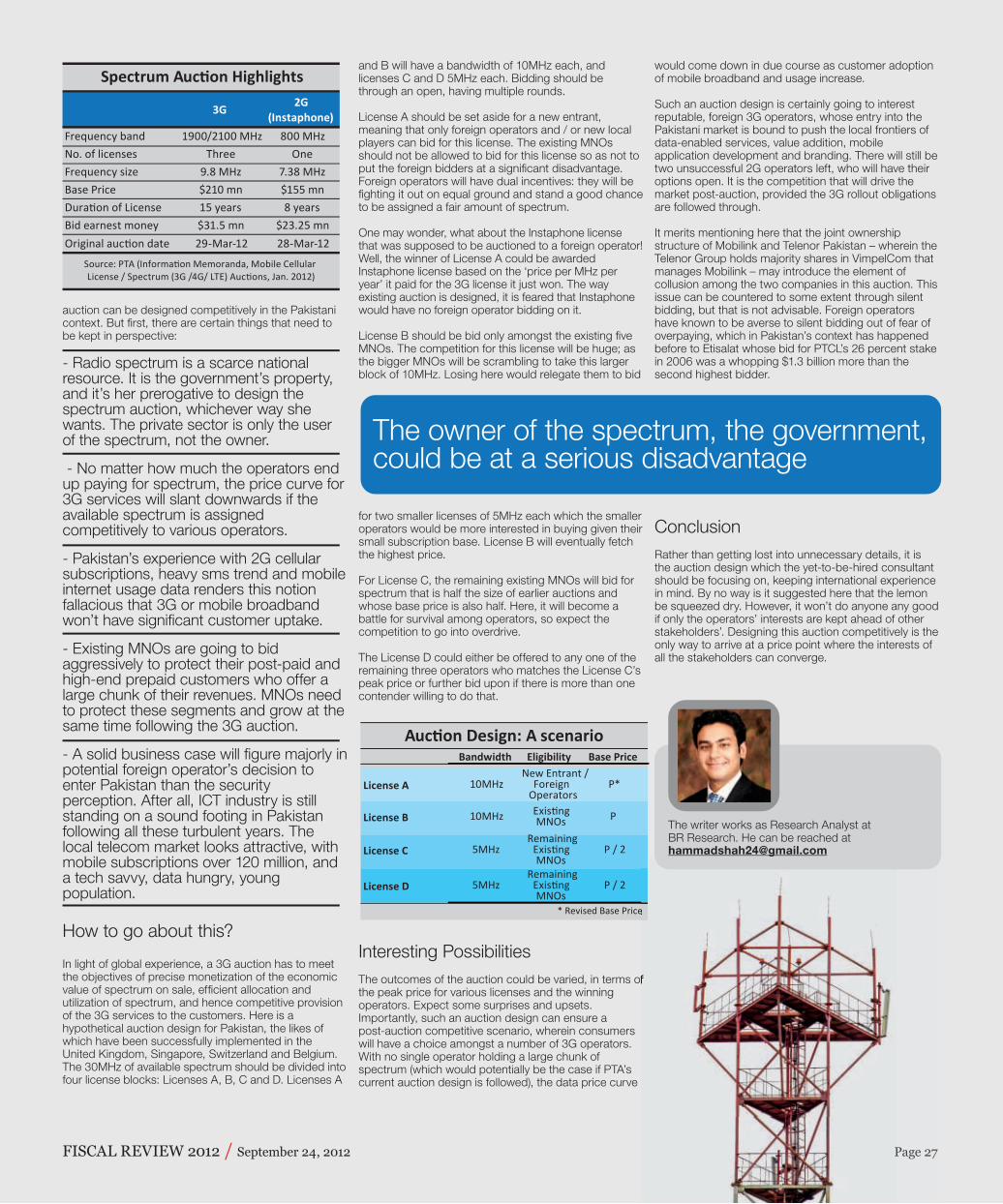

3G Spectrum Auction: Don’t delay- Do it now!By Parvez Iftikhar

Auction for 3G licenses: Faulty reasoning, designBy Hammad Haider

Health of a polio-endemic countryBy Dr. Talib Lashari

Challenges of a largely uneducated societyBy Heman D. Lohano

Youth Unemployment: A Ticking Time BombBy Sidra Farrukh

Separation of commercial interestand regulatory role at KSE is our immediate priorityMuhammad Ali Ghulam Muhammad, Chairman, SECP

Media does not have any space for economic reformsDr. Nadeem ul Haque

Liberlized trade to expand markets, improve livesBy Javeria Ansar

Cyclical Bilateral RelationsBy Salman Zaidi

FY13: Back to the Fund?By Mobin Nasir

In his highly-acclaimed Winesburg, Ohio, celebrated American novelist Sherwood Anderson wrote: “There is the truth of virginity and the truth of passion, the truth of wealth and of poverty, of thrift and profligacy, of careless-ness and abandon.” In our context, however, a wave of gloom, uncertainty, pessimism, and despondency pervades across the country. People are moaning in despair and dismay. The reasons for this state of melan-choly and depression are quite plausible. Two provinces are firmly in the grip of semi-insurgencies as these are in a condition of being in revolt or insurrection while the situation in other provinces is far from satisfactory; pathetically poor governance and massive corruption now represent themselves as more formidable challenges than ever; the economy is going south in the absence of a clear vision as growing macroeconomic imbalances continue to create profound complications, although inflation has softened up only recently while the country has been largely untouched by the financial meltdown that has been shaking up the economies of the US and the EU in particular—the two top trading partners of Pakistan -- since 2008. As far as Pakistan’s foreign policy issues are concerned, the US continues to remain one of the most important countries for a variety of reasons. Unfortunately, however, there has been an unprecedented deterioration in Pakistan-US relations post-May 12 2011. Despite a semi-resolution of Nato supply route issue, there is a sudden surge in acts of terrorism amid reports that the government is contemplating moving into the hitherto no-go territory of North Waziristan to drive out terrorists from their safe havens. The production of a highly sacrile-gious film in the US has only deepened anti-Americanism in the Islamic world, including Pakistan and Afghanistan. As far as Europe is concerned, it is still struggling to come out of recession after almost three years of the sovereign debt crisis. Victor Hugo’s European dream, it seems, is facing profoundly testing times in present-day Europe. In the region, there has been a welcome thaw in Pakistan-

India relations. The bilateral peace efforts have brightened the prospects of increased trade between the two countries in the short-and mid-term, which may ultimately lead to resolution of some core issues, including Kashmir.

That the economy is not the successive governments’ top priority in Pakistan is a perception that hardly needs any elaboration or explaining. The incumbent government, it seems, has also failed to fully understand the message of its voters who catapulted it into power in February 2008. None of its leaders has ever said that they take it on the chin and they have got to learn from what people are saying. What people have been hankering after is government’s focus on issues that really matter such as law and order and economy; and they do not want to distract or burden their leaders with too many other issues, including education and healthcare, because they strongly appreciate the public sector’s lack of capacity to deliver in these areas. While the Benazir Income Support Program and Benazir Stock Option Scheme are its major success stories, the list of its failures in the realm of economy is very long. This newspaper seeks to underscore the need for competitive economy, which includes formulating and implementing such economic policies that provide an enabling framework so that private sector can operate with full efficiency; improve management of enterprises and gain cost effective access to highly specialized economic inputs. We are also a strong advocate for productive employment, which is at the core of market competitive-ness. Policymakers must be able to identify the required technical and managerial skills to expand training programs that hone available technical, managerial and entrepreneurial skills.

Dear readers, although this publication in your hands is no white-paper of the incumbent government’s performance in over four years and its arguably irrational and lopsided budgetary priorities in an election year, it seeks to look at

the state of economy in accordance with the cardinal principle of journalism: objectivity. The issues thus covered range from the 7th NFC Award and provinces’ enhanced financial prowess post-18th Constitutional Amendment to the required tax reforms; from the curse of blind subsidies to a dangerously spiraling circular debt; from energy woes to water shortages; from analyses on federal and provin-cial budgets to challenges to macroeconomic stability; from glaring structural weaknesses in civil bureaucracy to lack of fiscal devolution; from challenges and handicaps bedeviling our exports on account of lack of competitive-ness and costly imports because of a weakened PKR in the external sector; from abysmally low allocations for social sector to burgeoning population growth amid shrinking resources; and from recklessly wasteful and wildly extravagant government spending to alarmingly large fiscal and current account deficits. So on and so forth. We expect from all political stakeholders, particularly PPP, PML-N, PML-Q, PTI, MQM and ANP, the multilateral lending agencies such as the IMF, ADB and the World Bank, and key regulators such as State Bank of Pakistan and Competition Commission of Pakistan to respond to our effort, Fiscal Review 2012-13, which is clearly aimed at providing a firm basis for future planning efforts and creating bridges to emerging economic paradigms. Dear readers, there is something which tells us that the present difficult, unpleasant and painful situation will definitely end. Macroeconomic indicators paint a bleak picture but our abiding trust in the majesty of democracy and constitution-alism assures us there is light at the end of the tunnel.

BR RESEARCHTHE TEAM

CONTENT TEAM

1. Ali Khizar Aslam | Head of Research 2. Mobin Nasir | Assistant Editor3. Zuhair Abbasi | Research Analyst4. Sijal Fawad | Research Analyst5. Hammad Haider | Research Analyst 6. Sidra Farrukh | Research Analyst 7. Javeria Ansar | Research Analyst8. Naseem Waheed | Database Officer

DESIGN TEAM

9. Murtaza Khaliq | Creative Head 10. Abdul Musawer Gulzar | Illustrator

1 2 3 4 5 6

7 8 9 10

FISCAL REVIEW 2012 / September 24, 2012 Page 03

Don’t abandon hopeFrom Editor’s Desk

India relations. The bilateral peace efforts have brightened

countries in the short-and mid-term, which may ultimately lead to resolution of some core issues, including Kashmir.

the state of economy in accordance with the cardinal principle of journalism: objectivity. The issues thus covered range from the 7th NFC Award and provinces’ enhanced financial prowess post-18th Constitutional Amendment to the required tax reforms; from the curse of blind subsidies to a dangerously spiraling circular debt; from energy woes to water shortages; from analyses on federal and provin-cial budgets to challenges to macroeconomic stability; from glaring structural weaknesses in civil bureaucracy to lack of fiscal devolution; from challenges and handicaps bedeviling our exports on account of lack of competitive-ness and costly imports because of a weakened PKR in the external sector; from abysmally low allocations for

Don’t abandon hopeDon’t abandon hope

FISCAL REVIEW 2012 / September 24, 2012Page 04

The democratically elected government presented the fifth budget of its tenure, marking national history in the process. But the Federal Budget 2012-13 is a denial of basic accounting standards. The numbers simply do not add up.

In fact the budget making exercise is expressive of the general apathy of the current political regime on the economic front. The budget was a non-event while the speech delivered by the Federal Finance Minister was unceremonious.

The economic experts interviewed for this publication were more disappointed and disgruntled than ever encountered before. A general consensus has appeared that the government is too busy with daily firefighting and cash management issues, to focus on infrastructure development, job creation and debt management.

Granted, this government inherited a shambling economy with structural imbalances exposed to global crises. Yet in the first year, it had fared relatively better. Shaukat Tarin captained the FinMin successfully into a stan-by arrangement with the IMF and the provinces reached consensus on the 7th NFC Award.

But there were few other blips on the fiscal radar. Debate over tax reform was sparked but extinguished before the time the fourth and the fifth budgets announcements were made.

But the newfound fiscal space being enjoyed by the provinces appears only on paper. The transfer of power has been reluctant and selective. The friction in this process impeded service delivery, at least in the short run. The rift between the Federal Government and Government of Punjab is another irritant compounding the hurdles between public services and the public. Precedence to political expediency is leading to duplicity of resources, especially human resources.

Nonetheless these transitions were long due and they may take their sweet time in acquiring new equilibrium. The next step of fiscal federalism which is not favored by mainstream political parties is the devolution of power to the third-tier of government.

The Federal Government has been expecting budget surpluses from the

provinces for the past two years. But not only has this goal eluded them; the fiscal deficit has actually grown wider over this span of time. With the elections coming up, this tally is headed further south.

There is a dire need to smooth institutional functioning of Council of Common Interest with representation from the provinces and federal government and make it constitutional for the federating units to abide the decisions of the body.

Persistently high fiscal deficits are eroding the purchasing power for consumers. In the last fiscal, the government borrowed over Rs1.2 trillion (almost doubled the amount last regime borrowed in its last year) from the banking system out of which more than half was high powered money creation and a quarter was liquidity injection through reverse open market operations.

Nothing could be more inflationary in nature; according to some internal studies of State Bank, one quarter of inflation in the last year was attributable to this process of monetization. Had it been at zero, inflation would have been at 8-9 percent in FY12.

Given the upcoming elections, the printing presses at SBP will likely be in over drive, so inflation shall persist despite falling international oil prices.

Domestic debt which is much more expensive than external debt increased manifold in the past four years, as did debt servicing. Overall public debt increased from Rs4.8 trillion in 2007 to Rs12.5 trillion by June 2012. A weakening rupee has added another Rs1.5 trillion to public debt with Balance of Payments vulnerabilities looming the pie of foreign debt in rupee terms is going to increase further; every one rupee fall in dollar, public debt soars by Rs35 billion.

The foreign exchange reserves at SBP are low and fragile. IMF payments are going to get heavy in the second half of this fiscal making the job harder at FinMin and SBP.

There is a near consensus amongst the leading economists that going back to the IMF programme is inevitable. However, the timing is critical.

The challenge is not attainability and question is not the legitimacy of what IMF is going to prescribe. The issue is to resolve the structural imbalances which are impeding the economic growth and hindering the macroeconomic stability.

The foremost issue which is deeply felt by every Pakistani is power sector slippages. The core of the fiasco is the wrong choice of fuel – departure from indigenous gas to expensive imported furnace oil. FO is the most expensive fuel choice and its presence in fuel mixies of India, US and China is less than 5 percent; while here it’s at 35 percent.

The resolution of the power crisis lies in short-term as well as medium-term responses. But the government response has come at snail’s pace. The new Power Policy 2012 is a good roadmap but no one has really hit the trail yet. Again all are waiting and hoping for new government to come and kick-start the much-needed power sector reforms.

Then there are issues of tax to GDP ratio. Despite IMF pressure no new sector has come into the tax net. And more importantly nothing concrete is done on tax administration reforms.

Broad based subsidies must go, power tariffs should be rationalized. Social support programmes such as the BISP are great steps but these are not enough. Poverty cannot be combated with hand-outs indefinitely.

On the macroeconomic stability; the need for all economic managers to sit down

and chart-out a plan on how to pull up the investment to GDP ratio from its lowest ebb in national history. The potential for domestic and foreign investment is enormous knowing the favourable demographics of the country and investors are hunting for good assets. Local groups, even in such a tough political and economic environment are grabbing good assets – whether its Tabba Group taking on ICI’s domestic operations, Dawood Group buying Hubco or Mansha bullying on AES Lalpir.

Similarly foreign investors are eyeing telecom expansion, energy sector (both upstream and downstream) and other sectors. But the biggest deterrent for them is the inconsistent economic policies, poor law and order situation and bad governance.

We need to provide policy security to reserve the trend of repatriation of profits and dividends which stand at an alarming level at present.

Country’s hope lies hidden in the next setupBy Ali Khizar

in the next setup

The writer works as Head of Research at Business Recorder. He can be reached at [email protected]

FISCAL REVIEW 2012 / September 24, 2012 Page 05

and bloated development programs, they are going to be under further pressure to borrow.

BRR: Will the development spending not have beneficial spillover effects on the economy?

HP: Development expenditure is pumping money. Look at the composition of the federal PSDP. At this time when power is your biggest constraint, its share in PSDP is barely 20 percent. And the biggest hand goes to highways and roads, which have taken up about 25 percent more than power.

Then there is political programming with special programs managed by the Prime Minister’s secretariat. There is no precedent for the Prime Minister’s Secretariat handling the brunt of development expenses which play to the tune of about Rs29 billion at present.

Another anomaly is the Ministry of Finance having been given 100 projects – related to water supply, by-passes, flyovers, urban development – under the President’s and PM’s directive which have not been approved by the cabinet. FinMin is a controlling ministry; it is not supposed to implement projects. There’s going to be inefficient spending this year. You’ll see borrowings at astounding levels in the first half of the year, particularly from SBP.

BRR: Will we have to go to the IMF again?

HP: It seems likely, but there will be several conditions. In the controversial Article IV constitution of the IMF released in February this year, they have systematically stated many conditions. The first thing they have objected to is the currency being overvalued. So the first thing they’ll ask for is a big devaluation. Then they’ll ask for the withdrawal of all exemptions and reductions in tax rates given over the last two years ever since the Fund walked out.

The third condition from the IMF this time around will be the implementation of Reformed General Sales Tax (RGST). Fourthly the Fund will demand an enhancement in the sales tax rate to 20 percent. Further conditions could be a quantum jump in tariffs, privatization of some sectors like energy distribution, a compulsory budgetary surplus, zero limits on borrowing from the central bank, hike of 3-4 percentage points in the policy rate, etc.

BRR: But the conditions are hardly implemented by the government.

HP: This time, you cannot get away with mere lip service because the country has no credibility anymore. The reforms will be front-loaded since not a single member of the board will be on our side. But the question is which government will want to take these measures in an election year? So you are on the verge of a financial

crisis, because we may need to go to the Fund within this fiscal year.

BRR: What other signs and symptoms of a financial crisis do you see?

HP: The real worry is high inflation, which is very destructive in terms of the effect it has on people. And that will happen if your currency is falling by a multiple, which happens in a crisis. Hyper inflation is defined as a period where the average price level doubles in three years. We are already flirting with that level.

Collapse of saving schemes is also a worrying phenomenon. It has gone down by about 40 percent because of slow erosion of confidence in government papers, and people prefer to save in dollars instead of rupees.

BRR: What is a feasible solution to these quagmires?

HP: It is important to come up with a rational government which initiates serious reforms. Interestingly, if there is a soft bailout, you will never come to a point where some serious reforms will be taken. It seems that only a crisis will bring the tough decisions that have become so necessary for the sustained progress of Pakistan.

BRR: In your opinion, should the power sector be deregulated like the telecommunications sector?

HP: The remarkable leap in technology was a major factor in deregulating the telecommunication sector. We don’t have that dramatic increase in technology as far as the energy sector is concerned. The telecom revolution was lead by MNCs; not Pakistani companies.

Today, sovereign guarantees are not being honored. So the prospect of big money coming into this sector from MNCs or from local private companies is gone because you have destroyed the sector so much. Rental power didn’t help either.

There are many short-term issues that need to be focused on. There must be no tolerance for electricity theft or non-payment of utility bills; gas supply must be prioritized for power production, industries and fertilizer sectors. Unfortunately, the current regime has shown little willingness to even increase CNG rates, let alone sweeping reforms across the power sector.

Dr. Pasha is currently serving as the Chairman of the Advisory Panel of Economists to the Planning Commission and Convener of the Economic Advisory Council of the Prime Minister of Pakistan. He has formerly been Federal Minister for Commerce and Trade, Finance and Economic Affairs, Education and Deputy Chairman, Planning Commission in three different governments.

From 2001 to 2007, Dr. Pasha was UN Assistant Secretary General and Director of the Regional Bureau for Asia and the Pacific of UNDP. Dr. Pasha has an M.A. from Cambridge University, and a Ph.D. from Stanford University. He is currently the Dean of the School of Liberal Arts and Social Sciences at the Beaconhouse National University (BNU), Lahore, Pakistan.

The cost is hyper-inflation down the road -Dr. Hafiz A. Pasha

BR Research: What are your views about the fiscal outcome this year?

Hafiz Pasha: It has busted all possible limits. You’ve crossed the peak level, which was last seen in 2007-08. The way the deficit is being financed is even more worrying. In FY12, borrowing from the banking system was over Rs1200 billion, while about Rs505 billion was from the central bank. Last year, government borrowing from SBP stood at Rs590 billion. So that’s the rate at which high powered money is being pumped into the economy.

The only reason the money supply is not exploding is that the net foreign assets are contracting. Your reserves are cancelling out. The government has to borrow this kind of money from the central bank when they promised the net borrowing would be zero. Even more worrying is the fact that the federal government is now borrowing predominantly for consumption. So if you have an 8 percent deficit and your development program closes at slightly above 1-1.5 percent, it means that government borrowing stands around 6.5 percent of the GDP for consumption.BRR: What will be the economic impact of this?

HP: The cost is hyperinflation down the road. This is a runaway fiscal deficit situation and even the International Monetary Fund must be having nightmares looking at these numbers.

BRR: What about rupee depreciation?

HP: We had managed to keep the debt-to-GDP ratio more or less constant

because, following the big devaluation in 2007-08 the currency had depreciated about Rs5 or so over a four year period. But this year, it depreciated by over Rs9, or about 10 percent. Now consider that every rupee of depreciation adds at least Rs60 billion to the country’s debt burden. I fear that we will soon also exceed the limit of 60 percent debt to GDP that was set in the Fiscal Responsibility and Debt Limitation Act. This year the government will likely be even less prudent given the fact that the elections are coming up.

BRR: Will this have an impact on the upcoming general elections?

HP: The issue is how long this government will carry on without holding elections. The timing issue is important, with regard to two aspects. Firstly, it will probably be cognizant of the frequency and seasonality of load shedding.Secondly, reserves are depleting faster than anticipated. We started the year at $14.8 billion. In May we lost $800 million because of IMF repayments. We came down to $10.1 billion – which is roughly 2-2.5 months of import cover before we got his breather of coalition support fund of $1.1 billion. You can easily go down to 1.5-2 months once you start making lumpy repayments to the IMF later this year.

Financing the current account deficit is becoming a problem because the capital account has died. It was negative last month. Have you ever heard of a financial account being negative? There’s no FDI and no aid. So things could start looking very uncomfortable around September-October.

If they are neck-deep in financial crises and load shedding, there is no way in the world they can win an election. The longer time stretches, the greater is the likelihood of a financial crisis. The rupee may fall another Rs20 by that time. There are risks of capital flight, of export proceeds being held back, speculative opening of LCs, which will precipitate the process. And the worst thing that could happen is the holding back of remittances.

BRR: What about the rupee-dollar exchange rate? What does that show?

HP: The worst indicator is the gap between the interbank rate and the open market rate which is unsustainable. It went up to around Rs1.50 a couple of months back; that’s a huge gap. Historically the gap has been at Rs0.5 at most. This may mean that informal remittances will increase because they get a better rate.

BRR: What about the benefits of decreasing oil prices on the trade side?

HP: Whatever you gain on the imports front due to the decline in oil prices will be countered by a decline in exports, particularly to Europe which is the destination of about a fourth of the country’s total exports. The growth pattern of exports has been progressively in the negative over the past few months.

BRR: Won’t this mellow the effect on inflation?

HP: No, because the rupee is being devalued. If your rupee has devalued by 10 percent and oil prices have gone down

by 17-18 percent, that’s a net benefit of 8 percent in rupee terms. But if the rupee continues to devalue, it cancels out. Besides, the injection of trillions of rupees of liquidity in the system will also have an effect on CPI, which has systematically gone up since December last year; core inflation is also on the rise. Reverse OMO operations are also creating artificial injection of liquidity in the system. The rollover rates of T Bills have also increased and that’s further pressure.

BRR: What are your views on this year’s Federal Budget?

HP: The budget shows an accounting error because development expenditure figures don’t add up. And the speech was very badly drafted. The full, published budget speech ignores underlying realities completely.

The government has reduced tax rates for people earning Rs5 million a year. There is little justification for a tax break to individuals earning a million rupees or more each month. The lowering of presumptive tax rates will not only lower government revenues, it will also rekindle the evil of corruption in the tax administration.

BRR: What about provincial surpluses?

HP: The provinces will not do anything as long as they have surpluses from the NFC, so they cannot be relied upon. Two are already in deficit; Punjab and Sindh. Only Balochistan and KP are in surpluses, but overall the four are facing budget deficits. This year with election spending coming in

FISCAL REVIEW 2012 / September 24, 2012Page 06

BRR Interview by Ali Khizar

and bloated development programs, they are going to be under further pressure to borrow.

BRR: Will the development spending not have beneficial spillover effects on the economy?

HP: Development expenditure is pumping money. Look at the composition of the federal PSDP. At this time when power is your biggest constraint, its share in PSDP is barely 20 percent. And the biggest hand goes to highways and roads, which have taken up about 25 percent more than power.

Then there is political programming with special programs managed by the Prime Minister’s secretariat. There is no precedent for the Prime Minister’s Secretariat handling the brunt of development expenses which play to the tune of about Rs29 billion at present.

Another anomaly is the Ministry of Finance having been given 100 projects – related to water supply, by-passes, flyovers, urban development – under the President’s and PM’s directive which have not been approved by the cabinet. FinMin is a controlling ministry; it is not supposed to implement projects. There’s going to be inefficient spending this year. You’ll see borrowings at astounding levels in the first half of the year, particularly from SBP.

BRR: Will we have to go to the IMF again?

HP: It seems likely, but there will be several conditions. In the controversial Article IV constitution of the IMF released in February this year, they have systematically stated many conditions. The first thing they have objected to is the currency being overvalued. So the first thing they’ll ask for is a big devaluation. Then they’ll ask for the withdrawal of all exemptions and reductions in tax rates given over the last two years ever since the Fund walked out.

The third condition from the IMF this time around will be the implementation of Reformed General Sales Tax (RGST). Fourthly the Fund will demand an enhancement in the sales tax rate to 20 percent. Further conditions could be a quantum jump in tariffs, privatization of some sectors like energy distribution, a compulsory budgetary surplus, zero limits on borrowing from the central bank, hike of 3-4 percentage points in the policy rate, etc.

BRR: But the conditions are hardly implemented by the government.

HP: This time, you cannot get away with mere lip service because the country has no credibility anymore. The reforms will be front-loaded since not a single member of the board will be on our side. But the question is which government will want to take these measures in an election year? So you are on the verge of a financial

crisis, because we may need to go to the Fund within this fiscal year.

BRR: What other signs and symptoms of a financial crisis do you see?

HP: The real worry is high inflation, which is very destructive in terms of the effect it has on people. And that will happen if your currency is falling by a multiple, which happens in a crisis. Hyper inflation is defined as a period where the average price level doubles in three years. We are already flirting with that level.

Collapse of saving schemes is also a worrying phenomenon. It has gone down by about 40 percent because of slow erosion of confidence in government papers, and people prefer to save in dollars instead of rupees.

BRR: What is a feasible solution to these quagmires?

HP: It is important to come up with a rational government which initiates serious reforms. Interestingly, if there is a soft bailout, you will never come to a point where some serious reforms will be taken. It seems that only a crisis will bring the tough decisions that have become so necessary for the sustained progress of Pakistan.

BRR: In your opinion, should the power sector be deregulated like the telecommunications sector?

HP: The remarkable leap in technology was a major factor in deregulating the telecommunication sector. We don’t have that dramatic increase in technology as far as the energy sector is concerned. The telecom revolution was lead by MNCs; not Pakistani companies.

Today, sovereign guarantees are not being honored. So the prospect of big money coming into this sector from MNCs or from local private companies is gone because you have destroyed the sector so much. Rental power didn’t help either.

There are many short-term issues that need to be focused on. There must be no tolerance for electricity theft or non-payment of utility bills; gas supply must be prioritized for power production, industries and fertilizer sectors. Unfortunately, the current regime has shown little willingness to even increase CNG rates, let alone sweeping reforms across the power sector.

BR Research: What are your views about the fiscal outcome this year?

Hafiz Pasha: It has busted all possible limits. You’ve crossed the peak level, which was last seen in 2007-08. The way the deficit is being financed is even more worrying. In FY12, borrowing from the banking system was over Rs1200 billion, while about Rs505 billion was from the central bank. Last year, government borrowing from SBP stood at Rs590 billion. So that’s the rate at which high powered money is being pumped into the economy.

The only reason the money supply is not exploding is that the net foreign assets are contracting. Your reserves are cancelling out. The government has to borrow this kind of money from the central bank when they promised the net borrowing would be zero. Even more worrying is the fact that the federal government is now borrowing predominantly for consumption. So if you have an 8 percent deficit and your development program closes at slightly above 1-1.5 percent, it means that government borrowing stands around 6.5 percent of the GDP for consumption.BRR: What will be the economic impact of this?

HP: The cost is hyperinflation down the road. This is a runaway fiscal deficit situation and even the International Monetary Fund must be having nightmares looking at these numbers.

BRR: What about rupee depreciation?

HP: We had managed to keep the debt-to-GDP ratio more or less constant

because, following the big devaluation in 2007-08 the currency had depreciated about Rs5 or so over a four year period. But this year, it depreciated by over Rs9, or about 10 percent. Now consider that every rupee of depreciation adds at least Rs60 billion to the country’s debt burden. I fear that we will soon also exceed the limit of 60 percent debt to GDP that was set in the Fiscal Responsibility and Debt Limitation Act. This year the government will likely be even less prudent given the fact that the elections are coming up.

BRR: Will this have an impact on the upcoming general elections?

HP: The issue is how long this government will carry on without holding elections. The timing issue is important, with regard to two aspects. Firstly, it will probably be cognizant of the frequency and seasonality of load shedding.Secondly, reserves are depleting faster than anticipated. We started the year at $14.8 billion. In May we lost $800 million because of IMF repayments. We came down to $10.1 billion – which is roughly 2-2.5 months of import cover before we got his breather of coalition support fund of $1.1 billion. You can easily go down to 1.5-2 months once you start making lumpy repayments to the IMF later this year.

Financing the current account deficit is becoming a problem because the capital account has died. It was negative last month. Have you ever heard of a financial account being negative? There’s no FDI and no aid. So things could start looking very uncomfortable around September-October.

If they are neck-deep in financial crises and load shedding, there is no way in the world they can win an election. The longer time stretches, the greater is the likelihood of a financial crisis. The rupee may fall another Rs20 by that time. There are risks of capital flight, of export proceeds being held back, speculative opening of LCs, which will precipitate the process. And the worst thing that could happen is the holding back of remittances.

BRR: What about the rupee-dollar exchange rate? What does that show?

HP: The worst indicator is the gap between the interbank rate and the open market rate which is unsustainable. It went up to around Rs1.50 a couple of months back; that’s a huge gap. Historically the gap has been at Rs0.5 at most. This may mean that informal remittances will increase because they get a better rate.

BRR: What about the benefits of decreasing oil prices on the trade side?

HP: Whatever you gain on the imports front due to the decline in oil prices will be countered by a decline in exports, particularly to Europe which is the destination of about a fourth of the country’s total exports. The growth pattern of exports has been progressively in the negative over the past few months.

BRR: Won’t this mellow the effect on inflation?

HP: No, because the rupee is being devalued. If your rupee has devalued by 10 percent and oil prices have gone down

by 17-18 percent, that’s a net benefit of 8 percent in rupee terms. But if the rupee continues to devalue, it cancels out. Besides, the injection of trillions of rupees of liquidity in the system will also have an effect on CPI, which has systematically gone up since December last year; core inflation is also on the rise. Reverse OMO operations are also creating artificial injection of liquidity in the system. The rollover rates of T Bills have also increased and that’s further pressure.

BRR: What are your views on this year’s Federal Budget?

HP: The budget shows an accounting error because development expenditure figures don’t add up. And the speech was very badly drafted. The full, published budget speech ignores underlying realities completely.

The government has reduced tax rates for people earning Rs5 million a year. There is little justification for a tax break to individuals earning a million rupees or more each month. The lowering of presumptive tax rates will not only lower government revenues, it will also rekindle the evil of corruption in the tax administration.

BRR: What about provincial surpluses?

HP: The provinces will not do anything as long as they have surpluses from the NFC, so they cannot be relied upon. Two are already in deficit; Punjab and Sindh. Only Balochistan and KP are in surpluses, but overall the four are facing budget deficits. This year with election spending coming in

FISCAL REVIEW 2012 / September 24, 2012 Page 07

Fiscal Devolution: Still an Unfinished AgendaBy Rao Muhammad Asif Iqbal

In the context of federalism, Pakistan has witnessed two major developments in the last two years or so. The first of these developments was the 7th National Finance Commission (NFC) Award, which came into effect in July 2010 and resulted in significant changes in revenue sharing arrangements between the federal and provincial governments. The other major development is the 18th Amendment to the Constitution. It contains far reaching stipulations for empowering Pakistan’s four federating units, giving them unprecedented autonomy.

The amendment makes very clear demarcation of legislative authority between federal and provincial governments. With this amendment the Concurrent List of legislation in the Constitution stands abolished, devolving the functions contained in this list to the provincial governments. This significantly enhances the range of legislative and functional responsibilities of provincial governments.

Some changes have also been made in the Federal Legislative List (FLL). Only a provincial assembly will have power to make legislation with respect to any matter not spelled out in the FLL. The only exception is that legislation with respect to criminal law, criminal procedure and evidence can be made both by Parliament and Provincial Assembly.

The erstwhile Concurrent List contained 47 subjects, which now have been transferred to the provinces. However, some subjects such as electricity, legal, medical and other professions and standards in higher education have been added to FLL Part I.

The role of provinces is also enhanced by transferring few subjects from FLL Part I to FLL Part II since the latter comes under the Council of Common Interests (CCI), which is well represented by the provinces. These subjects include major ports, census, national coordination and planning, and inter-provincial jurisdiction of police force. Moreover, all regulatory authorities established under federal law and management of public debt have also been given under the control of CCI.Moreover, some subjects have been omitted from FLL Part I, implying that legislative authority for these subjects will

now be prerogative of provincial government. These include state lotteries, duties in respect of succession to property, sales tax on services and taxes on capital value of immovable property. On the other hand, international treaties, conventions and agreements and international arbitration have been added to FLL.

More autonomy to the federating units also calls for greater coordination between the provincial and federal governments. In this regard, an important and welcome step is revitalisation of the Council of Common Interests (CCI). In the past, the CCI has occasionally played a very important role in reaching agreements on disputed issues. For example, the 1991 Water Accord was agreed upon during a CCI meeting.Under the 18th Amendment, composition of the CCI has been changed. Although the total number of members remains unchanged (four from provinces and four representing federal government), the Prime Minister has been made a permanent member as well as the Chair of the Council.

The council has the power to formulate and regulate policies in relation to matters enumerated in Part II of the Federal Legislative List as well as to exercise supervision and control over related institutions. In order to make the CCI an effective body, the Constitution has provided that CCI would have a permanent secretariat and meet at least once in three months.

Transfer of Functions to the ProvincesThe 18th Amendment resulted in redistribution of functional responsibilities of federal and provincial governments. The federal government dissolved its 18 ministries, which are mostly related to social sectors. On the contrary, eight new ministries have been formed by the federal government though one would have expected much smaller size of federal cabinet after devolution.

A number of departments and institutions related to dissolved ministries were transferred to the provinces while many of them were retained by the federal government. Some issues, however,

emerge regarding retention of various institutions/departments by the federal government and their placement within federal divisions. Foremost, the legal grounds for retaining these institutions are at best, murky.

Several institutions involved in service delivery have been retained by the federal government; the most controversial being Employees’ Old-Age Benefits Institution (EOBI) and Workers Welfare Fund (WWF) which have been transferred to newly formed Ministry of Human Resource Development. Punjab and Sindh have already voiced concerns over this decision.

There appears to be a dichotomy in the policy of federal government where it has transferred some institutions requiring a national approach, such as health and education services to the provinces, while retaining others that are strong contenders for devolution.

For example, two federally run hospitals namely Jinnah Post Graduate Medical Centre Karachi and Sheikh Khalifa Bin Zaid Hospital Quetta were transferred to government of Sindh and Balochistan, respectively. On the other hand, Zayed Post-Graduate Medical Institute Lahore and Shaikha Fatima Institute of Nursing and Health Sciences Lahore have not been transferred to the government of Punjab. Similarly, federal government has retained Tuberculosis Centre and Women and Chest Diseases Hospital (both based Rawalpindi), which should have been handed over to the province. In the same manner, National Colleges of Arts (Lahore and Rawalpindi) and Marine Biological Research Laboratory Karachi have been retained.

In summary, while the 18th Amendment has provided greater autonomy to the provinces, in order to reap the full benefits of this paradigm shift, transfer of functions and responsibilities will have to be made in line with the spirit of the Constitution.

Dissolved Ministries

Population welfare

Education Education Food and Agriculture Special Initiatives Health Sports Labour and manpower Tourism Livestock and dairy Development Woman Development Local Government and Rural Youth Affairs Development Zakat and Ushr

Culture Social Welfare and Special

Newly formed Ministries

Human Resource Development National Heritage and IntegrationProfessional and Technical Training National Harmony

Food Security and Research Climate Change

National Regulation and Services Capital Administration and Development

The author is Principal Economist at the Social Policy Development Centre. His areas of concentration include Governance, Civil Society and Public Finance.

More autonomy to the federating units also calls for greater coordination between the provincial and federal governments.

Page 08 FISCAL REVIEW 2012 / September 24, 2012

BR Research: Do you agree with the current government’s claim that they inherited the power sector crisis from previous regime?

Dr. Ashfaq Hassan Khan: There are many misconceptions about Pakistan’s economy – created either deliberately or are based on ignorance. A little background and history of the power crisis is in order here. Pakistan was facing power shortages prior to the Power Policy of 1994. The Power Policy attracted massive investment from the IPPs, and by 2001, we had surplus of 3,000 megawatts. The government had to pay for electricity produced, not consumed, so there were financial implications of this surplus at that time. The tensions with India following the December 2001 attack on Indian parliament broke down negotiations for the export of electricity.

In 2003, Pakistan was still carrying a surplus of 2,000 megawatts. Several exercises were conducted by the government to determine if the supply would match the demand in coming years. Power demand had been rising at an average rate of three percent per annum prior to 2003, which meant that at that rate the break even would reach in 2010. Assuming a 6 percent GDP growth in the coming years (double the 2003 rate); the breakeven was to be reached in 2007. Hence, it did not make any economic sense to commission new power plants in 2003, since Pakistan was carrying a large power surplus at that time.

Between 2003 and 2007, Pakistan’s economic growth rate averaged 7.3 percent, something beyond the expectations of the government. During the period, power demand grew by 9 percent, against 6 percent we had projected earlier in 2003, due to increased economic growth, commercial activities, infrastructure development, rise in the middle class, etc. The power

supply-demand breakeven, therefore, reached in 2005 instead of 2007. It is fair to ask what power projects the previous government undertook.

Fifty new power projects – totaling 12,141 MW – were launched between February 2004 and June 2007 due to early warning signs. These projects were to become operational between October 2008 and December 2015. These dates have now been removed from the website of the PPIB due to political pressure. The incumbents focused on rental power plants and did not work as much on the already planned projects. The new captive power generation capacity added to the grid is due to the projects commissioned in previous regime. The credit needs to be given where it’s due.

BRR: Coming to the budget affairs, why is Pakistan’s tax-to-GDP ratio going down?

AHK: Firstly, we need to understand the tax-t-GDP ratio in the right perspective. Pakistan did a GDP rebasing in 2000, in which the GDP deflator had increased by 20 percent. That is why the then 12-13 percent tax-to-GDP ratio fell down to 9 percent soon after. Now, coming back to your question, there are many reasons for gradual decline in the ratio.

One, the agricultural lobby is very strong – that is why the agriculture sector contributes around one percent to the tax base. I feel that a more precise measure would be tax-to-(Non-Agriculture) GDP ratio, because the 22 percent of GDP (that is, agriculture) is not being taxed. The services sector is 52 percent of the GDP, but it contributes just 26 percent to the tax pool, and the tax proceeds are mainly coming from the telecom and banking sectors.

There are many services sectors that are not in the tax-net, like. retail, transportation, professional service (e.g. doctors, lawyers, technicians, etc.) So, the GDP is rising, but the contributors to GDP growth are not contributing in enlarging the tax pool. As you can see, the services sector is growing, but its tax contributions are not.

As long as the current political structure and system are intact, the agricultural incomes may not be taxed. Some portions of manufacturing income will also be reported under agriculture income and hence not taxed. Whichever political party comes to govern, this problem will remain. The structure of parliament is such that the issue will remain.

In addition, the capacity of FBR has eroded over the years. The quality of taxmen has eroded in the last 15-20 years. There is a lot of politicization. Every government paid attention towards reforming tax system, but nobody focused on tax administration reforms. The two must go hand in hand, but tax administration remained neglected.

BRR: What are your thoughts on the existing fiscal policy framework?

AHK: In the presence of existing NFC Award, there can never be any meaningful fiscal policy in the country.

Dr. Ashfaque Hasan Khan is currently the Dean and Professor, NUST Business School, National University of Sciences & Technology (NUST), Islamabad. He has been the Special Secretary Finance/Director General, Debt Office of the Ministry of Finance, Islamabad. He is also the Director and Vice Chairman of Saudi Pak Industrial and Agricultural Investment Company Ltd.

NFC was no economic awardDr. Ashfaque Hasan Khan

In the presence of existing NFC Award, there can never be any meaningful fiscal policy in the country.

Publicly, the government claims credit for the passage of this Award, but privately, they realize that they have made a mistake. It was a political award, not an economic one. The fiscal discipline shifted from federal government to provincial governments, since 60 percent of the resource is going to the latter.

This is happening at a time when federal government itself is starving for resources. The government team did not think about future power sector subsidies, or calculate the hundreds of billions doled out to the PSEs.

The IMF has also acknowledged this in their latest Article IV review. The government made a mistake, so they must correct it and move on. But they probably won’t as they want to take credit for it, not the blame.

Resources were transferred to the provinces very quickly – without regard to capacity building and fiscal discipline. Hence, the provinces are running budget deficits. The provincial development expenditures have risen by 90 percent since, and this has bred corruption. If the 18th Amendment had preceded the NFC Award, things would have been different. The federal government was profoundly naïve to think that since the resources had been increased through the 7th NFC Award, the provinces would take up additional responsibilities after the 18th Amendment. On the contrary, provinces demanded more resources for additional assignments.

On another note, the size of the federal government did not shrink, as one would have expected – it actually enlarged after devolution. There is a need to address these issues in the NFC Award, to bring binding constraints. The budget making exercise is made redundant in this scenario. It has become just a piece of paper. Just look at the unrealistic allocations for power sector subsidies. People have lost their interest in the budget.

BRR: Public debt has almost doubled since 2007, with major increase in domestic debt. How alarming is that?

AHK: There was a purpose behind the Fiscal Responsibility and Debt Limitation Act [2005], which was to establish fiscal discipline in the government. The decade of the 1990s taught us this lesson that government borrowings slow down investment and growth, and fuel inflation. The intention was to allow for a prudent fiscal path to be trodden, with a constant check on the government’s fiscal practices. We have been off-track since 2008; hence debt has grown manifold, growing faster than GDP growth rate.

The domestic and external debt components are almost equal. The difference is that external debt is cheap, but domestic debt is very expensive. On an average, the servicing of external debt is 3-3.5 percent, whereas domestic debt’s servicing is at a rate of 13-14 percent.

Hence, almost 90 percent of interest payments are on account of domestic debt, the rest is external debt servicing.

Till 2007, Pakistan’s total public debt was Rs4.8 trillion. The figure reached Rs12.5 trillion in June 2012. It has actually more than doubled. The higher debt accumulation during last five year is due to a variety of reasons. Upto Rs1500 billion of the increase is due to exchange rate depreciation. For every dollar in external borrowing, public debt has increased by Rs35.

BRR: What is your outlook on the exchange rate?

AHK: There is a lot of focus on the current account deficit and its implications on the macro economy. But I think that it is the capital account which is going to create difficulties or be a source of improvement in the balance of payments position. The foreign inflows matter – both debt-creating and non-debt-creating. A current account deficit of $4 billion shouldn’t worry an economy as large a size as Pakistan’s. But due to problems in the capital account, financing even this small current account deficit becomes an issue.

Non-debt-creating inflows are a big question mark, as the traditional sending countries in the North America and Europe are befuddled with their own economic woes. The surplus has shifted to Asia, where unlike the West, there is no tradition to give aid.

The forex reserve position will deteriorate, as the usable reserves with the SBP will be under pressure. The gap in trade and services account balances is also widening. Remittances growth is a mystery, as Pakistan’s growth rate defies the regional and global trends in remittance inflows. This is creating a Dutch Disease, as financing current account deficit with remittance inflows is not sustainable. We have become so much addicted to this that any drop in remittances could spell trouble. I hope these remittance flows are legitimate, but my thinking suggests that there is something wrong with this.

The problems will start in this fiscal year, due to external sector. Pakistan has to pay back to the IMF, it has to finance its trade and services account deficits, and it has to pay off its amortized external debt. This will create difficulties in terms of ability to pay back. We will be depending on the US clout, which is, again, a question mark. Foreign aid is not forthcoming. I see pressure on

exchange rate in next two years, with all its adverse consequences for the economy.

BRR: What is your view on the inflation trend?

AHK: The official figure of 9.5 percent is just because the finance

minister wanted a single digit number. There is no way this target can be

achieved this fiscal year. I think inflation will remain in the vicinity of 12 to 12.5 percent. Pakistan has been a low-inflation country, with occasional double-digit spikes. This is the only regime during which inflation never slipped back in single digits. There is a lot of unrest among people due to high inflation in recent years, because they are not used to this.

BRR: The investment- and savings-to-GDP ratios are at all time low. How can we turn these around?

AHK: Gross domestic saving rate is 5.8 percent, lower than it was in 1947. The root cause is the budget deficit, simple. The government is borrowing from the commercial banks, with the latter earning risk-free returns. The bankers are doing business, not banking, and they are not to blame. The private sector is suffering due to low credit availability. Hence, the investment level is falling down, and I think that the investment-to-GDP ratio has actually fallen below 10 percent. Majority of what businesses have borrowed from the banks is running finance, for working capital needs, and very less is for fixed capital investment. Curtailing the fiscal deficit would free up space for the private sector to take traction. This will help SBP to reduce interest rates. If the private sector cannot come in, the government should establish industries based on the PIDC model. This will bring in investment, create jobs, and enable private sector to take control later.

BR Research: Do you agree with the current government’s claim that they inherited the power sector crisis from previous regime?

Dr. Ashfaq Hassan Khan: There are many misconceptions about Pakistan’s economy – created either deliberately or are based on ignorance. A little background and history of the power crisis is in order here. Pakistan was facing power shortages prior to the Power Policy of 1994. The Power Policy attracted massive investment from the IPPs, and by 2001, we had surplus of 3,000 megawatts. The government had to pay for electricity produced, not consumed, so there were financial implications of this surplus at that time. The tensions with India following the December 2001 attack on Indian parliament broke down negotiations for the export of electricity.

In 2003, Pakistan was still carrying a surplus of 2,000 megawatts. Several exercises were conducted by the government to determine if the supply would match the demand in coming years. Power demand had been rising at an average rate of three percent per annum prior to 2003, which meant that at that rate the break even would reach in 2010. Assuming a 6 percent GDP growth in the coming years (double the 2003 rate); the breakeven was to be reached in 2007. Hence, it did not make any economic sense to commission new power plants in 2003, since Pakistan was carrying a large power surplus at that time.

Between 2003 and 2007, Pakistan’s economic growth rate averaged 7.3 percent, something beyond the expectations of the government. During the period, power demand grew by 9 percent, against 6 percent we had projected earlier in 2003, due to increased economic growth, commercial activities, infrastructure development, rise in the middle class, etc. The power

supply-demand breakeven, therefore, reached in 2005 instead of 2007. It is fair to ask what power projects the previous government undertook.

Fifty new power projects – totaling 12,141 MW – were launched between February 2004 and June 2007 due to early warning signs. These projects were to become operational between October 2008 and December 2015. These dates have now been removed from the website of the PPIB due to political pressure. The incumbents focused on rental power plants and did not work as much on the already planned projects. The new captive power generation capacity added to the grid is due to the projects commissioned in previous regime. The credit needs to be given where it’s due.

BRR: Coming to the budget affairs, why is Pakistan’s tax-to-GDP ratio going down?

AHK: Firstly, we need to understand the tax-t-GDP ratio in the right perspective. Pakistan did a GDP rebasing in 2000, in which the GDP deflator had increased by 20 percent. That is why the then 12-13 percent tax-to-GDP ratio fell down to 9 percent soon after. Now, coming back to your question, there are many reasons for gradual decline in the ratio.

One, the agricultural lobby is very strong – that is why the agriculture sector contributes around one percent to the tax base. I feel that a more precise measure would be tax-to-(Non-Agriculture) GDP ratio, because the 22 percent of GDP (that is, agriculture) is not being taxed. The services sector is 52 percent of the GDP, but it contributes just 26 percent to the tax pool, and the tax proceeds are mainly coming from the telecom and banking sectors.

There are many services sectors that are not in the tax-net, like. retail, transportation, professional service (e.g. doctors, lawyers, technicians, etc.) So, the GDP is rising, but the contributors to GDP growth are not contributing in enlarging the tax pool. As you can see, the services sector is growing, but its tax contributions are not.

As long as the current political structure and system are intact, the agricultural incomes may not be taxed. Some portions of manufacturing income will also be reported under agriculture income and hence not taxed. Whichever political party comes to govern, this problem will remain. The structure of parliament is such that the issue will remain.

In addition, the capacity of FBR has eroded over the years. The quality of taxmen has eroded in the last 15-20 years. There is a lot of politicization. Every government paid attention towards reforming tax system, but nobody focused on tax administration reforms. The two must go hand in hand, but tax administration remained neglected.

BRR: What are your thoughts on the existing fiscal policy framework?

AHK: In the presence of existing NFC Award, there can never be any meaningful fiscal policy in the country.

FISCAL REVIEW 2012 / September 24, 2012 Page 09

Publicly, the government claims credit for the passage of this Award, but privately, they realize that they have made a mistake. It was a political award, not an economic one. The fiscal discipline shifted from federal government to provincial governments, since 60 percent of the resource is going to the latter.

This is happening at a time when federal government itself is starving for resources. The government team did not think about future power sector subsidies, or calculate the hundreds of billions doled out to the PSEs.

The IMF has also acknowledged this in their latest Article IV review. The government made a mistake, so they must correct it and move on. But they probably won’t as they want to take credit for it, not the blame.

Resources were transferred to the provinces very quickly – without regard to capacity building and fiscal discipline. Hence, the provinces are running budget deficits. The provincial development expenditures have risen by 90 percent since, and this has bred corruption. If the 18th Amendment had preceded the NFC Award, things would have been different. The federal government was profoundly naïve to think that since the resources had been increased through the 7th NFC Award, the provinces would take up additional responsibilities after the 18th Amendment. On the contrary, provinces demanded more resources for additional assignments.

On another note, the size of the federal government did not shrink, as one would have expected – it actually enlarged after devolution. There is a need to address these issues in the NFC Award, to bring binding constraints. The budget making exercise is made redundant in this scenario. It has become just a piece of paper. Just look at the unrealistic allocations for power sector subsidies. People have lost their interest in the budget.

BRR: Public debt has almost doubled since 2007, with major increase in domestic debt. How alarming is that?

AHK: There was a purpose behind the Fiscal Responsibility and Debt Limitation Act [2005], which was to establish fiscal discipline in the government. The decade of the 1990s taught us this lesson that government borrowings slow down investment and growth, and fuel inflation. The intention was to allow for a prudent fiscal path to be trodden, with a constant check on the government’s fiscal practices. We have been off-track since 2008; hence debt has grown manifold, growing faster than GDP growth rate.

The domestic and external debt components are almost equal. The difference is that external debt is cheap, but domestic debt is very expensive. On an average, the servicing of external debt is 3-3.5 percent, whereas domestic debt’s servicing is at a rate of 13-14 percent.

Hence, almost 90 percent of interest payments are on account of domestic debt, the rest is external debt servicing.

Till 2007, Pakistan’s total public debt was Rs4.8 trillion. The figure reached Rs12.5 trillion in June 2012. It has actually more than doubled. The higher debt accumulation during last five year is due to a variety of reasons. Upto Rs1500 billion of the increase is due to exchange rate depreciation. For every dollar in external borrowing, public debt has increased by Rs35.

BRR: What is your outlook on the exchange rate?

AHK: There is a lot of focus on the current account deficit and its implications on the macro economy. But I think that it is the capital account which is going to create difficulties or be a source of improvement in the balance of payments position. The foreign inflows matter – both debt-creating and non-debt-creating. A current account deficit of $4 billion shouldn’t worry an economy as large a size as Pakistan’s. But due to problems in the capital account, financing even this small current account deficit becomes an issue.

Non-debt-creating inflows are a big question mark, as the traditional sending countries in the North America and Europe are befuddled with their own economic woes. The surplus has shifted to Asia, where unlike the West, there is no tradition to give aid.

The forex reserve position will deteriorate, as the usable reserves with the SBP will be under pressure. The gap in trade and services account balances is also widening. Remittances growth is a mystery, as Pakistan’s growth rate defies the regional and global trends in remittance inflows. This is creating a Dutch Disease, as financing current account deficit with remittance inflows is not sustainable. We have become so much addicted to this that any drop in remittances could spell trouble. I hope these remittance flows are legitimate, but my thinking suggests that there is something wrong with this.

The problems will start in this fiscal year, due to external sector. Pakistan has to pay back to the IMF, it has to finance its trade and services account deficits, and it has to pay off its amortized external debt. This will create difficulties in terms of ability to pay back. We will be depending on the US clout, which is, again, a question mark. Foreign aid is not forthcoming. I see pressure on

exchange rate in next two years, with all its adverse consequences for the economy.

BRR: What is your view on the inflation trend?

AHK: The official figure of 9.5 percent is just because the finance

minister wanted a single digit number. There is no way this target can be

achieved this fiscal year. I think inflation will remain in the vicinity of 12 to 12.5 percent. Pakistan has been a low-inflation country, with occasional double-digit spikes. This is the only regime during which inflation never slipped back in single digits. There is a lot of unrest among people due to high inflation in recent years, because they are not used to this.

BRR: The investment- and savings-to-GDP ratios are at all time low. How can we turn these around?

AHK: Gross domestic saving rate is 5.8 percent, lower than it was in 1947. The root cause is the budget deficit, simple. The government is borrowing from the commercial banks, with the latter earning risk-free returns. The bankers are doing business, not banking, and they are not to blame. The private sector is suffering due to low credit availability. Hence, the investment level is falling down, and I think that the investment-to-GDP ratio has actually fallen below 10 percent. Majority of what businesses have borrowed from the banks is running finance, for working capital needs, and very less is for fixed capital investment. Curtailing the fiscal deficit would free up space for the private sector to take traction. This will help SBP to reduce interest rates. If the private sector cannot come in, the government should establish industries based on the PIDC model. This will bring in investment, create jobs, and enable private sector to take control later.

BRR Interview by Ali Khizar

Remittances growth is a mystery, as Pakistan’s growth rate defies the regional and global trends in remittance inflows. This is creating a Dutch Disease, as financing current account deficit with remittance inflows is not sustainable.

debt, the rest is external

Till 2007, Pakistan’s total public debt was Rs4.8 trillion. The figure reached Rs12.5 trillion in June 2012. It has actually more than doubled. The higher debt accumulation during last five year is due to a variety of reasons. Upto Rs1500 billion of the increase is due to exchange rate depreciation. For every dollar in external borrowing, public debt has

What is your outlook on the

exchange rate in next two years, with all its adverse consequences for the economy.

BRR: What is your view on the inflation trend?

AHK: The official figure of 9.5 percent is just because the finance

minister wanted a single digit number. There is no way this target can be

achieved this fiscal year. I think inflation will

a Dutch Disease, as financing current account deficit with remittance inflows is not sustainable.

FISCAL REVIEW 2012 / September 24, 2012Page 10

struggled to keep corn prices high, Pakistani landlords are struggling to keep them low!

The fallacy that direct taxation on agriculturists will in isolation only impact their income needs to be absolutely destroyed. That nobody in the world wants to pay tax willingly is an ugly truth. Hence when forced, coerced and cornered into paying tax, any rational person will make all attempts to pass the burden on.

Admittedly, compared with immediate passing on of indirect taxes, the time lag will be longer. Nonetheless, the inherent favorable space between domestic and international prices of produce, will supplement the landed aristocracy’s endeavors to swiftly avoid taxes and make the poor pay.

Another tax on the poor! When will the rich pay? The rich are only willing to pay for their luxuries, so the only solution is to tax them where it hurts! But if the verdict is to be infallible and defendable, we must not jump to conclusions.

Revisiting history, the British industrialist was ferociously against the Corn Laws not because of their love for the poor, but because a higher cost of sustenance meant higher minimum wage and lower profits for the rich. Correspondingly, any agriculture tax will logically increase the cost of business reducing their profits thereby negating any net gain to tax collection. Since higher cost of produce impacts the entire populace, an adverse impact can also not be ignored.

Self sustainability of food at minimum cost is a primary directive of every nation. No wonder even the West ferociously protects its agriculture sector. The sensitivities of landlords are such a credible threat that tampering with individual produce is considered risky, lest the landlords shift to some other produce contrary to national interest. Having a support price for wheat and taxing farmers is synonymous with transferring money from one pocket to the other. Realistically, so is subsidizing power and enhancing indirect taxation across the populace. That the meek will forever subsidize the mighty is an unavoidable absolute truth.

Summarizing the conclusions thus far, if the inhabitants of the corridors of power ever wanted agriculture to be taxed, bread would be dearer today. If the “will to do” is conspicuous by its absence and the presence of any benefit at best is unproven, why so much noise?

Serendipitously, noise is a tool for distracting limelight from fundamental issues. The inability to effectively implement existing tax legislation can be a probable cause for the pandemonium

around agricultural tax. A sector-wise reconciliation between GDP and tax collected can perhaps affirm this conjecture beyond doubt.

The plight of existing taxpayers at the hands of desperate tax collectors is definitely credible circumstantial evidence pointing in this very direction. Trying to squeeze water from a rock is contrary to universal laws. Already taxpayers popularly refer to income tax by a synonym worse than draconian, which for reasons of optics cannot be quoted here.

Take another example. The undocumented economy, which time and again has proved to be the white knight for Pakistan’s economy, is generally invested in the real estate. Fiddling with this sector without taking cognizance of the related overall impact on the economy is a fatal strategy. Attempts to proactively regulate property ownership can have an adverse affect on foreign currency flows.

By now the truth behind the title “Not a drop to tax” should be clearer. The point is that taxation is not the only option in the equation. Governments have generally chosen the much simpler option of printing money to fill coffers. While the gurus have postulated extensive theories for the optimum quantity of money, troubled nations have always chosen to simply relate quantity with the cost of paper and ink. Unfortunately, however, this strategy leaves the populace worse off. Inflation is a hidden tax which has the dual effect of reducing purchasing power and eliminating wealth.

Conceivably, economic growth is the only incontrovertible mechanism to enhance the absolute amount of tax collected, assuming a constant percentage to GDP can be maintained. A small digression, comparing the tax collected to GDP ratios between countries is an exercise in futility since all other factors are not constant between such samples. Growth, however, requires investment which again is only possible through surplus resources.

But all is not lost. Revenue is one side of the picture only; austerity is the other more righteous path. Consider, if workers remittance from fellow Pakistanis have gone up from $5.4 billion to $12 billion in the past five years, why is the country still struggling with its balance of payments? For abundant clarification, note that the increase in inward remittance is a “windfall” outside the control of any government. What if this windfall had not materialized?

The answer to the second question is most likely bankruptcy leading to abject slavery. The answer to the first question is worse; Pakistanis continued to live beyond their means resulting in

uncontrolled imports. Befuddled by economic theories postulating consumer supremacy, the nation lost sight of reality. Recall grandmother’s famous dictum, “Hamesha chadar daikh ker pair phelana” (live within your means)..

So what is the nation importing worth $35 billion other than debt and devaluation? Venturing a guess, a geek’s analysis will identify significant imported wants that can and should be curtailed, which dovetails into our earlier conclusion. Those who desire luxuries should pay a premium. What are luxuries and how are they to be taxed will require “out of the box” brainstorming, which is hardly possible in the current, already abused limited space. Nonetheless, while the path maybe difficult, the objective is achievable. There are nations with a proven track record around import substitution and enhanced export philosophy; Germany, Japan and China, to highlight a few.

The objective behind pinpointing imported uncontrolled wants was simply to highlight the existence of variable problems and solutions for conquering “Everest”. Domestic wants are another dimension that can also be explored.

The key limitation to trailblazing a different path is misguided effort. If policymakers continue to believe their own excuses, a solution to Pakistan’s economic squeeze will remain a fantasy. Struggling with not a drop to tax and at the same time desperate for growth, finance managers will need to rewrite economic theory or perhaps go back to the basics.

Scanning international news interestingly reveals that today the very proponents of free markets are concerned about externalities. Tariffs, currency regulation and protectionism are once again around the corner?

Every problem has a solution; all that is needed is honest hard work!

Not a drop to taxBy Syed Bakhtiyar Kazmi

A problem which has no solution is an undeniable fact ignored only by the vain or the insane.

The chronic antagonists quick to disagree with any other viewpoint are admonished to go no further. The receptive and open minded intelligentsia, in agreement with the above, is invited to deliberate upon the following observation:

Since the past few decades, successive governments have dodged legislating agriculture tax in spite of apparent and persuasive exigencies, which should be sufficient evidence to conclude that eternal status quo is a fact. The question then is, why does not the motif die its natural death? Is it because of the conspiratorial mischief of the vain or the insane?

The proponents of a change culminating through awareness and public or moral pressure created by a vibrant media, who by now should also have joined the ranks of the dissenters to the aforestated hypothesis,

are referred to the history of aristocratic misrule and landlordism prevalent in global governance.

Irrespective of the means by which power is acquired - democracy or dictatorship - the meek have yet to inherit the earth.

The unconventional approach adopted herein, most likely, is already discernible to the readers; nevertheless a further clarification is warranted. Deference to economic or other statistics in this article is kept at the minimal as they are but a distraction only.

Imaginative people have a proven capacity to eventually pull out some boring statistic for justifying any cause or covering up any debacle. Unsurprisingly, statistics are a dime a dozen. And for those having a penchant for details, there are sufficient other sources to whet the appetite.

“Money in the bank” needs no statistical alibi.

Pursuant to expectations, this journey continues with the remaining few curious and adventurous readers.

Responding to the question postulated in the hypothesis above, it would be a gargantuan task, even for the agencies, to keep an outbreak of mass insanity within the political elite under wraps. So, by default, is vanity the culprit? On the other hand, this conclusion is even more illogical since the powerful driven by their vanity would have taxed agriculture ages ago; mere lip service is therefore confusing.

To explore the improbable, the intent behind the controversial inclusion of the provision to exempt agriculture in the Constitution needs exposition. Without beating around the bush, let’s just go with the assumption that feudalism, from an undisputed position of strength, was able to negotiate a better deal when the legislation was being enacted. But herein lies the paradox: while the British landlords, the famous Corn Law saga,

FISCAL REVIEW 2012 / September 24, 2012Page 11

struggled to keep corn prices high, Pakistani landlords are struggling to keep them low!