The Controversies over the Chinese Currency Value : China’s Central Bank’s Responses and the...

41

The Controversies over the Chinese The Controversies over the Chinese Currency Value Currency Value : : China’s Central Bank’s Responses and the China’s Central Bank’s Responses and the Future of Yuan Future of Yuan Gene Hsin Chang 张张 University of Toledo Director of the Asian Studies Institute, Professor of Economics © International Convention of Asia Scholars International Convention of Asia Scholars August 22, 2005

-

Upload

carol-armstrong -

Category

Documents

-

view

215 -

download

0

Transcript of The Controversies over the Chinese Currency Value : China’s Central Bank’s Responses and the...

The Controversies over the Chinese Currency ValueThe Controversies over the Chinese Currency Value::

China’s Central Bank’s Responses and the Future of YuanChina’s Central Bank’s Responses and the Future of Yuan Gene Hsin Chang 张欣

University of ToledoDirector of the Asian Studies Institute, Professor of

Economics

©

International Convention of Asia ScholarsInternational Convention of Asia Scholars

August 22, 2005

The Issue of the Chinese CurrencyThe Issue of the Chinese CurrencyYuan (RMB)Yuan (RMB)

“ “ 2% Solution: 2% Solution: China Lets Yuan Rise vs. China Lets Yuan Rise vs. Dollar, Easing Trade Tensions Slightly”Dollar, Easing Trade Tensions Slightly”

------Title of the Report, Wall Street Journal, July 21, 2005Title of the Report, Wall Street Journal, July 21, 2005

Under the pressure of the market, the Under the pressure of the market, the Chinese authority announced the Chinese authority announced the currency-policy change on July 21, 2005.currency-policy change on July 21, 2005.

The Issue of the Chinese CurrencyThe Issue of the Chinese CurrencyYuan (RMB)Yuan (RMB)

The July 21The July 21stst Policy Change includes: Policy Change includes:

2.1 % one-time revaluation, from $1=8.27yuans 2.1 % one-time revaluation, from $1=8.27yuans to $1=8.11yuansto $1=8.11yuans

Move to “managed floating” exchange rate Move to “managed floating” exchange rate regimeregime

The exchange rate is decided by an undisclosed The exchange rate is decided by an undisclosed basket of currencies.basket of currencies.

The rate will be allowed to float against U.S. The rate will be allowed to float against U.S. dollar by 3 per thousand each day.dollar by 3 per thousand each day.

The value of yuan has not really The value of yuan has not really changed since thenchanged since then

RMB / Dollar Exchange Rate

8.000

8.050

8.100

8.150

8.200

8.250

8.300

Yu

an

s t

o $

1

The yuan has not really changed The yuan has not really changed since thensince then

In the past month, the yuan has changed In the past month, the yuan has changed only 0.065%, from only 0.065%, from

July 21st: $1 = 8.1100 yuans July 21st: $1 = 8.1100 yuans

to to

August 22August 22ndnd: $1=8.1047 yuans: $1=8.1047 yuans

If this pattern continues …If this pattern continues …

In the past month, the yuan has changed In the past month, the yuan has changed only 0.065%. Assume this pattern only 0.065%. Assume this pattern continues, continues, On July 21On July 21stst, 2006: $1 = 8.046 yuans , 2006: $1 = 8.046 yuans

which representswhich representsa total of 0.72% additional revaluationa total of 0.72% additional revaluation

ororCumulatively, 2.8 percent revaluation from Cumulatively, 2.8 percent revaluation from the original rate before the peg policy the original rate before the peg policy changechange

This is far from what the market This is far from what the market expectsexpects

How much does the yuan How much does the yuan undervalued?undervalued?

Has China’s Central Bank (The Has China’s Central Bank (The People’s Bank of China) done a good People’s Bank of China) done a good job in the exchange rate reform?job in the exchange rate reform?

What is the future of yuan?What is the future of yuan?

Background: The U.S. CongressBackground: The U.S. Congress

Senate Bill by Charles Schumer (D., N.Y.) and Senate Bill by Charles Schumer (D., N.Y.) and Lindsey Graham (R., S.C.)Lindsey Graham (R., S.C.)

If no RMB revaluation, imports from China can If no RMB revaluation, imports from China can be subject to 27.5% tariff. be subject to 27.5% tariff.

House China Currency Act by Congressmen DuHouse China Currency Act by Congressmen Duncan Hunter (R., Calif.) and Tim Ryan (D., Ohio)ncan Hunter (R., Calif.) and Tim Ryan (D., Ohio)

If no RMB revaluation, trigger an antidumping or If no RMB revaluation, trigger an antidumping or countervailing duty. countervailing duty.

Top trade partners of the U.S.Top trade partners of the U.S.(2004)(2004)

Total Trade Total Trade VolumeVolume

Trade DeficitTrade Deficit

11 CanadaCanada ChinaChina

22 MexicoMexico JapanJapan

33 ChinaChina CanadaCanada

44 JapanJapan MexicoMexico

55 GermanyGermany GermanyGermany

US Trade with China US Trade with China (million dollars)(million dollars)

0

50,000

100,000

150,000

200,000

250,000

TotalDeficit

The Bush administrationThe Bush administration-- ambivalence-- ambivalence

•2003: US Treasury Secretary John Snow told a House of Representatives panel. "China has pegged its currency to the dollar for 10 years. This administration has stressed that China needs to move to float its currency as soon as possible”

•The U.S. Treasury angered Congress by stopping short of issuing a formal finding that the Chinese government manipulated the exchange value of the yuan. It concluded that such a policy by itself does not meet the statutory definition of currency manipulation.

•May 26, 2005: The Bush administration stopped demanding that China let its currency, the yuan, float freely against other major currencies. "I don't think it is in our interest or in their interest in going immediately to a full float," Treasury Secretary John Snow told the Senate Banking Committee on Thursday. " Snow refused to say by how much he wanted China to revalue the yuan.

Federal Reserve:Federal Reserve:--- --- reservationreservation

•March 2005: Federal Reserve Chairman Alan Greenspan warned if China were to let its currency float immediately, as many in the US want, it could weaken that country’s banking system and threaten the world economy

•May 20, 2005 – Greenspan: “American shoppers will pay higher prices but the U.S. trade deficit with the rest of the world won't fall if China revalues its yuan currency as the Bush administration wants”.

Debate in the U.S.Debate in the U.S.

Reducing trade deficit Reducing trade deficit with Chinawith ChinaPreserving more jobs Preserving more jobs in the U.S.in the U.S.

Increasing trade deficit in terms Increasing trade deficit in terms of dollarsof dollarsSpeculative sell of dollarsSpeculative sell of dollarsPressure on the global dollar Pressure on the global dollar system, dollar and T bondssystem, dollar and T bondsU.S. bonds down, interest rate U.S. bonds down, interest rate upupWidening financial resource gapWidening financial resource gapInflationInflationDeterioration of terms of tradeDeterioration of terms of tradeConsumer surplus lossConsumer surplus loss

Pro Con

Debates in ChinaDebates in China

Reduce competitivenessReduce competitiveness

Adversely affect exportsAdversely affect exports

Adversely affect Adversely affect employmentemployment

DeflationDeflation

Improve terms of tradeImprove terms of trade

Reduces debt service Reduces debt service burdenburden

Reduces the cost of the Reduces the cost of the huge foreign reservehuge foreign reserve

Upgrading economic Upgrading economic structurestructure

ProCon

Debates among Asian countriesDebates among Asian countries

China is the largest export destination for China is the largest export destination for many Asian regions including Korea and many Asian regions including Korea and TaiwanTaiwanChina and Hong Kong imports more China and Hong Kong imports more goods from rest of Asia than Japangoods from rest of Asia than JapanThe benefits of revaluation of yuan are The benefits of revaluation of yuan are ambivalent for Asian countriesambivalent for Asian countriesConcern over a floating RMB that may Concern over a floating RMB that may cause regional economic instability.cause regional economic instability.

Responses by various countries to Responses by various countries to the yuan revaluationthe yuan revaluation

The U.S. The U.S.

JapanJapan

European UnionEuropean Union

Rest of AsiaRest of Asia

Developing countriesDeveloping countries

China itselfChina itself

Summary of the ResponsesSummary of the Responsesin the Worldin the World

Welcome the changeWelcome the changeMany are unsatisfied: the change is Many are unsatisfied: the change is symbolic and not enough to respond to the symbolic and not enough to respond to the market conditionmarket conditionThe world is evaluating the policy: what The world is evaluating the policy: what the implication are impactthe implication are impactThe world is wondering: what the future of The world is wondering: what the future of yuan will be.yuan will be.

Understanding the Yuan ValueUnderstanding the Yuan Value

Jeffrey Frankel: Yuan 42% undervaluedJeffrey Frankel: Yuan 42% undervalued

Lardy and Goldstein: 15%-25% Lardy and Goldstein: 15%-25% undervaluedundervalued

Gene Chang: 19.2% undervaluedGene Chang: 19.2% undervalued

Steve Hanke and Michael Connoly: No unSteve Hanke and Michael Connoly: No undervaluation dervaluation

Ronald McKinnonRonald McKinnon

Robert MundellRobert Mundell

Estimation of Equilibrium Value Estimation of Equilibrium Value of Yuanof Yuan

Determination in the short-runDetermination in the short-runDetermination in the long-runDetermination in the long-runPurchasing power parityPurchasing power parity

E = PE = PU.S.U.S. / P / PChinaChina

Relative purchasing power parityRelative purchasing power parity% depreciation in E% depreciation in E

= inflation U.S. – inflation China= inflation U.S. – inflation ChinaProblems with using relative PPP to estimate Problems with using relative PPP to estimate equilibrium value of yuanequilibrium value of yuan

Estimation of Equilibrium Value Estimation of Equilibrium Value of Yuanof Yuan

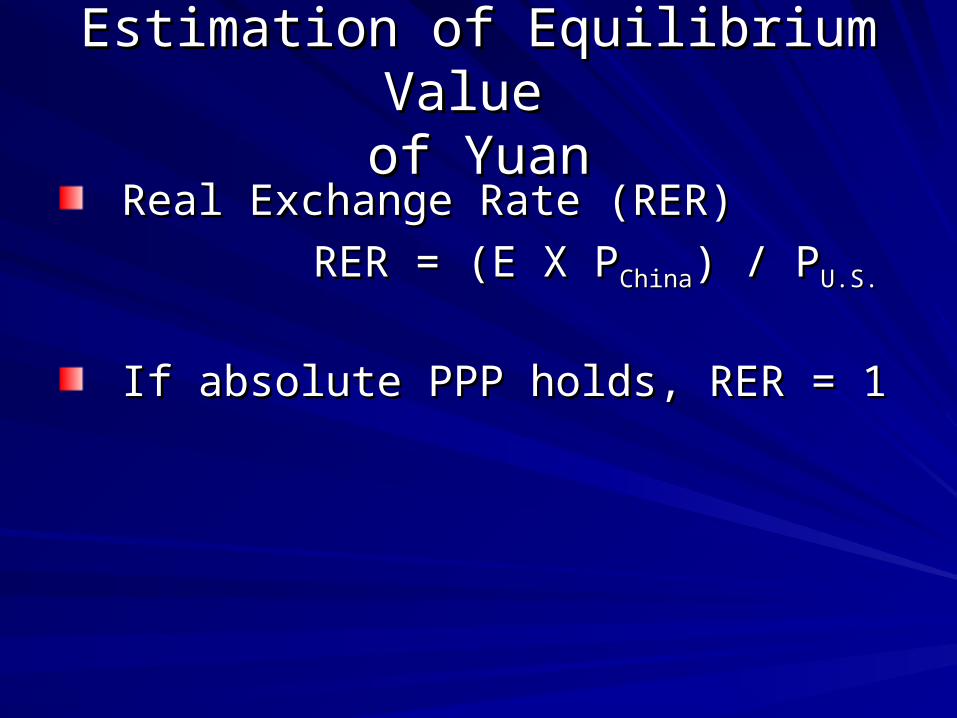

Real Exchange Rate (RER)Real Exchange Rate (RER)

RER = (E X PRER = (E X PChinaChina) / P) / PU.S.U.S.

If absolute PPP holds, RER = 1If absolute PPP holds, RER = 1

Fig 1. Relative Pruchasing Power (RPP) of Currencies of Various Countries

-4

-2

0

2

4

6

8

10

0 10000 20000 30000 40000 50000

GDP per capita

Re

lati

ve

Pu

rch

as

ing

Po

we

r

RPP

Fitted line

Linear (Fitted line)

Estimation of Equilibrium Value Estimation of Equilibrium Value of Yuanof Yuan

Why is RER greater than 1 for poor Why is RER greater than 1 for poor countries?countries?

The Balassa-Samuelson hypothesisThe Balassa-Samuelson hypothesis

The Bhagwati-Kravis-Lipsey hypothesisThe Bhagwati-Kravis-Lipsey hypothesis

Estimation of Equilibrium Value Estimation of Equilibrium Value of Yuanof Yuan

Model with control of the income level:Model with control of the income level:

RER = f (GDP per capita)RER = f (GDP per capita)

Data for RERData for RER

Linear or log linearLinear or log linear

(ln) RER = a + b X (ln) GDP per (ln) RER = a + b X (ln) GDP per capitacapita

Control heteroskedasticityControl heteroskedasticity

Estimation of Equilibrium Value Estimation of Equilibrium Value of Yuanof Yuan

Using the world sample to obtain the Using the world sample to obtain the estimates and the prediction equationestimates and the prediction equation

CoefficientsCoefficients Standard Standard errorerror

t -statisticst -statistics

InterceptIntercept 4.28039 4.28039 0.15922 0.15922 26.88387 26.88387

GDP p.c.GDP p.c. -0.13386 -0.13386 0.01320 0.01320 -10.14495 -10.14495

RMB exchange rateRMB exchange rate

0123456789

10

RER actual

Exchange rate (yuan per $)

RMB Undervaluation EstimationRMB Undervaluation Estimation

YearYear GDP pc GDP pc 20012001

RER RER actualactual

RER RER predictedpredicted

ValuationValuation P-valueP-value

19781978 703703 1.981.98 4.074.07 51.3%51.3% 0.0840.084

19851985 11581158 2.682.68 4.024.02 33.3%33.3% 0.1870.187

19861986 12931293 3.213.21 4.004.00 19.7%19.7% 0.2990.299

19871987 15091509 4.334.33 3.973.97 -8.9%-8.9% 0.4060.406

19911991 17571757 4.394.39 3.943.94 -11.2%-11.2% 0.3840.384

19941994 24842484 4.794.79 3.863.86 -24.3%-24.3% 0.2630.263

19951995 27882788 4.304.30 3.823.82 -12.6%-12.6% 0.3720.372

19961996 29872987 4.084.08 3.803.80 -7.4%-7.4% 0.4240.424

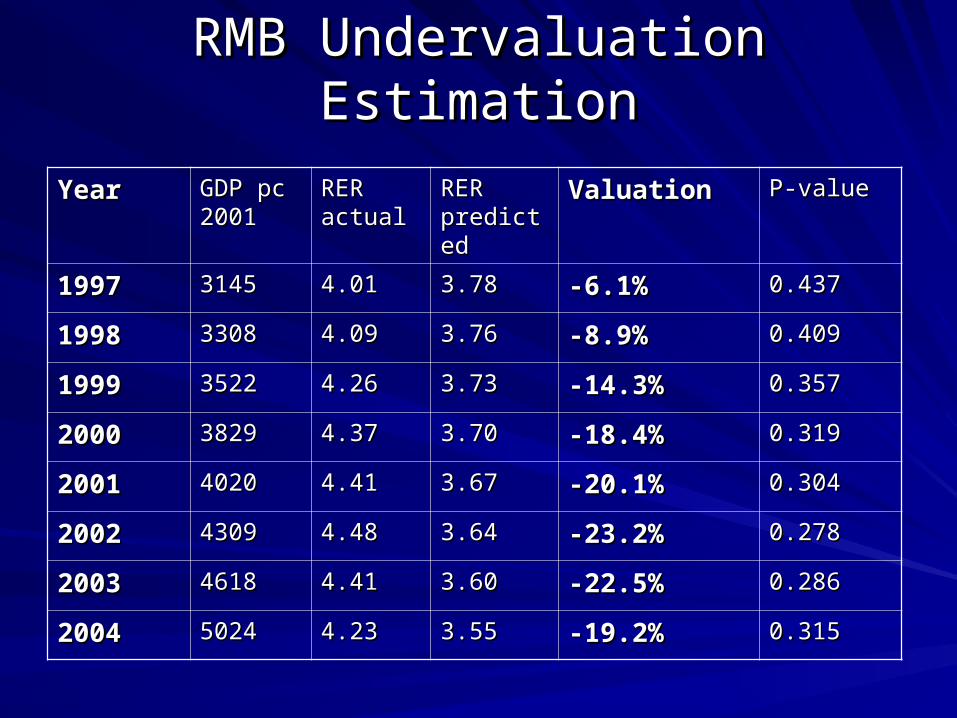

RMB Undervaluation EstimationRMB Undervaluation Estimation

YearYear GDP pc GDP pc 20012001

RER RER actualactual

RER RER predictedpredicted

ValuationValuation P-valueP-value

19971997 31453145 4.014.01 3.783.78 -6.1%-6.1% 0.4370.437

19981998 33083308 4.094.09 3.763.76 -8.9%-8.9% 0.4090.409

19991999 35223522 4.264.26 3.733.73 -14.3%-14.3% 0.3570.357

20002000 38293829 4.374.37 3.703.70 -18.4%-18.4% 0.3190.319

20012001 40204020 4.414.41 3.673.67 -20.1%-20.1% 0.3040.304

20022002 43094309 4.484.48 3.643.64 -23.2%-23.2% 0.2780.278

20032003 46184618 4.414.41 3.603.60 -22.5%-22.5% 0.2860.286

20042004 50245024 4.234.23 3.553.55 -19.2%-19.2% 0.3150.315

Under / Over –valued currenciesUnder / Over –valued currencies

-1.5

-1

-0.5

0

0.5

1

China’s Choice of China’s Choice of exchange rate regimeexchange rate regime

It is claimed to be “Managed floating”It is claimed to be “Managed floating”

Definition for managed floating– floating with Definition for managed floating– floating with government intervention, normally allowing government intervention, normally allowing for change within the range of 3-5%. for change within the range of 3-5%.

China’s policy is not a conventional MF China’s policy is not a conventional MF regime.regime.

China’s ChoiceChina’s ChoiceIt is also claimed to be fluctuate around a central rate It is also claimed to be fluctuate around a central rate

set by the previous transaction day, and using an uset by the previous transaction day, and using an undisclosed basket currencies as a “reference”, but ndisclosed basket currencies as a “reference”, but not stick to this basket.not stick to this basket.

Definition:Definition:Target zone, or band – a margin of fluctuation arouTarget zone, or band – a margin of fluctuation around some central ratend some central rateBasket peg – fixing not to a single foreign currency Basket peg – fixing not to a single foreign currency but to a weighted average of other currenciesbut to a weighted average of other currencies

China’s policy is not a conventional regime as defined China’s policy is not a conventional regime as defined above.above.

China’s ChoiceChina’s Choice

Definition of various FEX regimesDefinition of various FEX regimes

Crawling peg – a preannounced policy of Crawling peg – a preannounced policy of devaluing a bit each weekdevaluing a bit each week

Adjustable peg – fixing the exchange rate,Adjustable peg – fixing the exchange rate, but without any open-ended commitment t but without any open-ended commitment to resist devaluation or revaluation in the pro resist devaluation or revaluation in the presence of a large balance of payments defesence of a large balance of payments deficit or surplusicit or surplus

China’s ChoiceChina’s Choice

The real nature of China’s Foreign Exchange rate rThe real nature of China’s Foreign Exchange rate regime is:egime is:Basically still using the U.S. dollar as a major anBasically still using the U.S. dollar as a major anchor rather than a basket of currencies.chor rather than a basket of currencies.In practice allowing changes within only a very nIn practice allowing changes within only a very narrow band, much smaller than the announced 0.arrow band, much smaller than the announced 0.3% band.3% band.

In theory, China’s policy and practice is close to: In theory, China’s policy and practice is close to:

“crawling adjustable peg”“crawling adjustable peg”

Achievements of Achievements of China’s New FEX PolicyChina’s New FEX Policy

Diplomatic gainDiplomatic gain

Right direction to achieve the long Right direction to achieve the long term equilibrium valueterm equilibrium value

Cautious step, move and see.Cautious step, move and see.

More flexibility for future changesMore flexibility for future changes

Merits of Pegging to dollarMerits of Pegging to dollar

Lower transaction costs includingLower transaction costs includingcost of gaining informationcost of gaining informationcost of hedging exchange rate fluctuationcost of hedging exchange rate fluctuationcost of negotiationcost of negotiation

More than 90% of international transaction is More than 90% of international transaction is in dollars. This is extremely true for the in dollars. This is extremely true for the small and medium size Chinese firmssmall and medium size Chinese firms

Problems with China’s PolicyProblems with China’s PolicyContradiction between what is claimed and Contradiction between what is claimed and what is actually practiced.what is actually practiced.

The 2.1% revaluation is too small to ease the The 2.1% revaluation is too small to ease the market pressure.market pressure.

Ambiguous statement of “initial adjustment” , Ambiguous statement of “initial adjustment” , and the allowed floating band, leaving too and the allowed floating band, leaving too much room for speculators to guessmuch room for speculators to guess

Inviting more speculation and more capital Inviting more speculation and more capital flow.flow.

Problems with China’s PolicyProblems with China’s Policy

As a result,As a result,

The huge capital inflow continues and The huge capital inflow continues and show no sign of slow downshow no sign of slow down

2 billion dollars inflow on the first day 2 billion dollars inflow on the first day after the policy changeafter the policy change

Future of the YuanFuture of the Yuan

The 2.1 percent revaluation is too little to The 2.1 percent revaluation is too little to ease market pressure.ease market pressure.

If China’s inflation is under control, yuan is If China’s inflation is under control, yuan is going to revalue by 20% in coming five going to revalue by 20% in coming five years.years.

In the coming future …In the coming future …The current adjustment pace is certainly not The current adjustment pace is certainly not enough.enough.Hence the foreign capital flow will continue and Hence the foreign capital flow will continue and even accelerate. By the end of 2005, China’s even accelerate. By the end of 2005, China’s foreign reserve will exceed 800 billion U.S. foreign reserve will exceed 800 billion U.S. dollars.dollars.The central bank has to issue more and more The central bank has to issue more and more bank notes to sterilize the explosion of the bank notes to sterilize the explosion of the money base.money base.It adds tremendous pressure on the money It adds tremendous pressure on the money supply control and price level.supply control and price level.

Future of the YuanFuture of the Yuan

The central bank has to accelerate the The central bank has to accelerate the revaluation in the late period of the yearrevaluation in the late period of the year

Or, it has to make another one-time Or, it has to make another one-time adjustment at a certain stage.adjustment at a certain stage.

Internationalizing yuanInternationalizing yuanAdvantagesAdvantages

1. More flexibility for an independent 1. More flexibility for an independent monetary policymonetary policy

2. Low transaction cost2. Low transaction cost3. Seigniorage income3. Seigniorage income

But must meet the conditionsBut must meet the conditions1. Good macro fundamentals1. Good macro fundamentals

2. Greater role in the global market2. Greater role in the global market

Feasible only in the long runFeasible only in the long run

ConclusionConclusion

China’s change in FEX policy is a China’s change in FEX policy is a welcome step and in a right directionwelcome step and in a right direction

But it is too little to correct the But it is too little to correct the disequilibriumdisequilibrium

We expect that China is going to and has We expect that China is going to and has to take more actions to address this to take more actions to address this equilibrium issue in near futureequilibrium issue in near future