The Chinese model: Towards the end of producer-biased … · The Chinese model: Towards the end of...

41

The Chinese model: Towards the end of The Chinese model: Towards the end of producer producer - - biased and export biased and export - - led growth? led growth? Ettore Dorrucci European Central Bank (Deputy Head, International Policy Analysis Division) Workshop “The Chinese Economy”, co Workshop “The Chinese Economy”, co - - organised by organised by Banca Banca d’Italia d’Italia and Venice International University and Venice International University (Venice, 25 (Venice, 25 - - 27 November 2010) 27 November 2010)

Transcript of The Chinese model: Towards the end of producer-biased … · The Chinese model: Towards the end of...

The Chinese model: Towards the end of The Chinese model: Towards the end of producerproducer--biased and exportbiased and export--led growth?led growth?

Ettore DorrucciEuropean Central Bank (Deputy Head, International Policy Analysis Division)

Workshop “The Chinese Economy”, coWorkshop “The Chinese Economy”, co--organised by organised by BancaBanca

d’Italiad’Italia

and Venice International Universityand Venice International University

(Venice, 25(Venice, 25--27 November 2010)27 November 2010)

Outline

1

Part 1 – The current Chinese model:

Sustained growth Sustained growth cumcum imbalancesimbalances

Part 2 – Longer-term sustainability of the current model:

Are the longAre the long--term factors supporting China’s model running out? term factors supporting China’s model running out? Will this “force” adjustment towards more sustainable growth?Will this “force” adjustment towards more sustainable growth?

Part 3 – What is being done do adjust the model:

The thorny way to rebalancingThe thorny way to rebalancing

Part 4 – Current contradictions in the adjustment of the model:

Tensions between shortTensions between short--term growth objectives and rebalancing needsterm growth objectives and rebalancing needs

Part 1 – The current Chinese model:

Sustained growth Sustained growth cumcum imbalancesimbalances

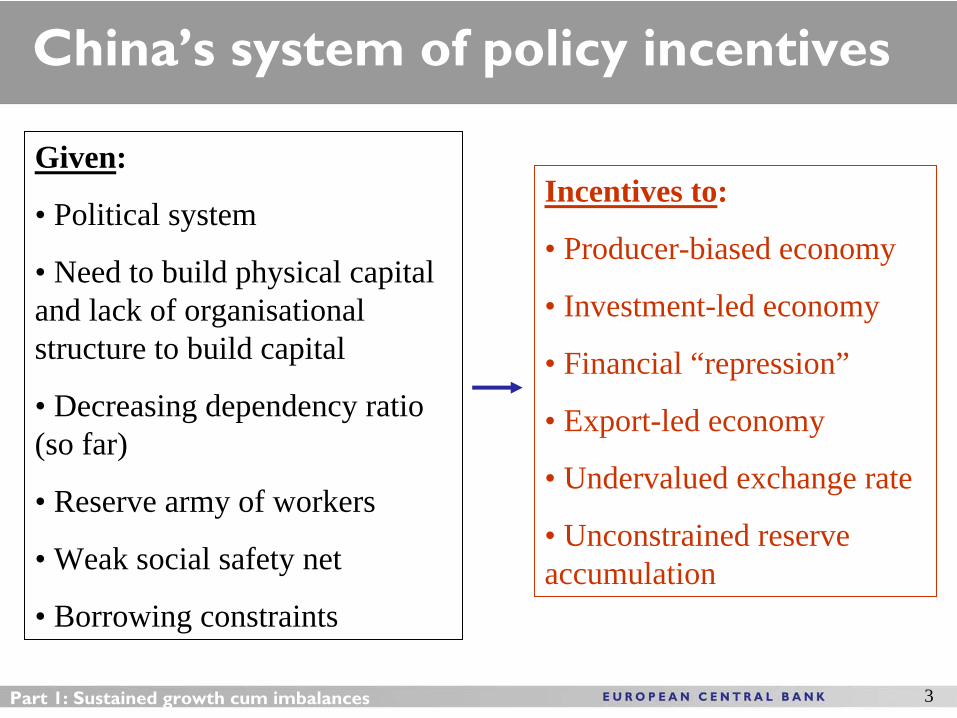

Key proposition:In the past three decades, China’s policy-makers have had incentives to maximise growth while postponing any fundamental adjustment in the associated economic model.

This has led to the accumulation of serious imbalances.

Part 1: Sustained growth cum imbalances 2

China’s system of policy incentives

Incentives to:

• Producer-biased economy

• Investment-led economy

• Financial “repression”

• Export-led economy

• Undervalued exchange rate

• Unconstrained reserve accumulation

Given:

• Political system

• Need to build physical capital and lack of organisational structure to build capital

• Decreasing dependency ratio (so far)

• Reserve army of workers

• Weak social safety net

• Borrowing constraints

Part 1: Sustained growth cum imbalances 3

Part 1: Sustained growth cum imbalances 4

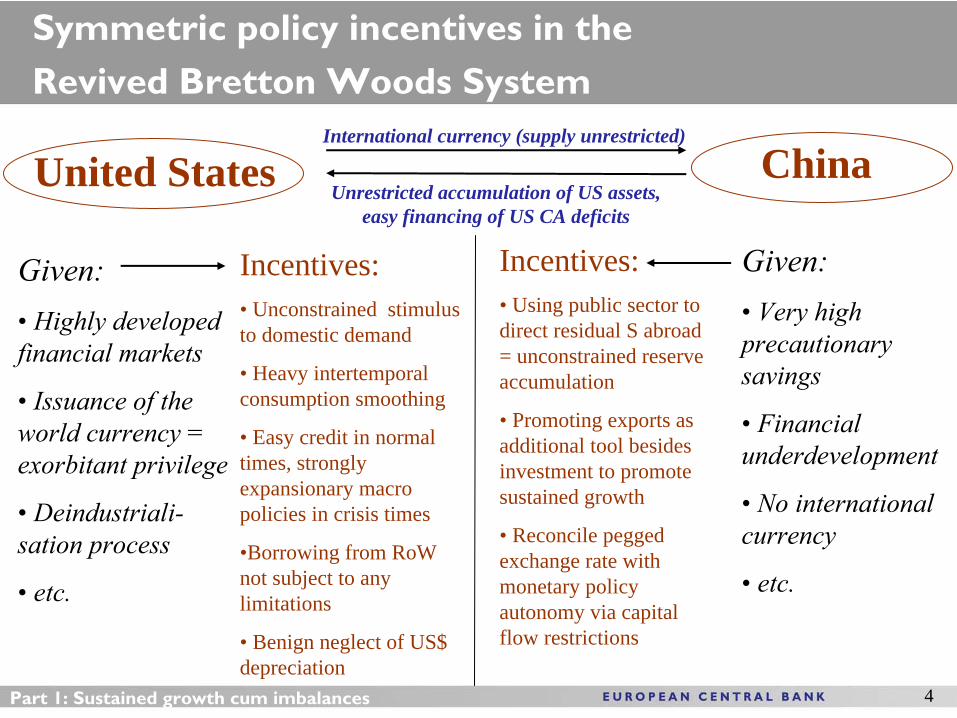

Symmetric policy incentives in the Revived Bretton

Woods System

United States ChinaInternational currency (supply unrestricted)

Given:• Highly developed financial markets

• Issuance of the world currency = exorbitant privilege

• Deindustriali- sation

process

• etc.

Incentives:• Unconstrained stimulus to domestic demand

• Heavy intertemporal consumption smoothing

• Easy credit in normal times, strongly expansionary macro policies in crisis times

•Borrowing from RoW not subject to any limitations

• Benign neglect of US$ depreciation

Given:• Very high precautionary savings

• Financial underdevelopment

• No international currency

• etc.

Incentives:• Using public sector to direct residual S abroad = unconstrained reserve accumulation

• Promoting exports as additional tool besides investment to promote sustained growth

• Reconcile pegged exchange rate with monetary policy autonomy via capital flow restrictions

Unrestricted accumulation of US assets, easy financing of US CA deficits

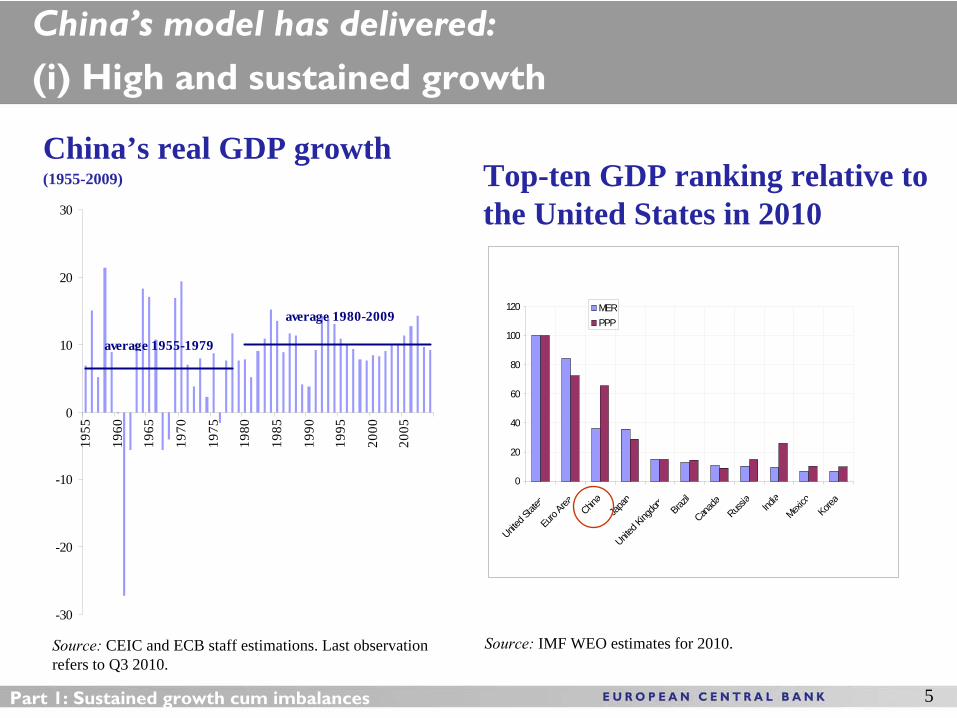

China’s model has delivered:

(i) High and sustained growth

5Part 1: Sustained growth cum imbalances

China’s real GDP growth(1955-2009)

Source: CEIC and ECB staff estimations. Last observation refers to Q3 2010.

0

20

40

60

80

100

120

United S

tates

Euro

Area China

Japan

United K

ingdom Braz

ilCana

daRuss

ia

India

Mexico

Korea

MERPPP

Top-ten GDP ranking relative to the United States in 2010

Source: IMF WEO estimates for 2010.

-30

-20

-10

0

10

20

30

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

average 1955-1979

average 1980-2009

6Part 1: Sustained growth cum imbalances

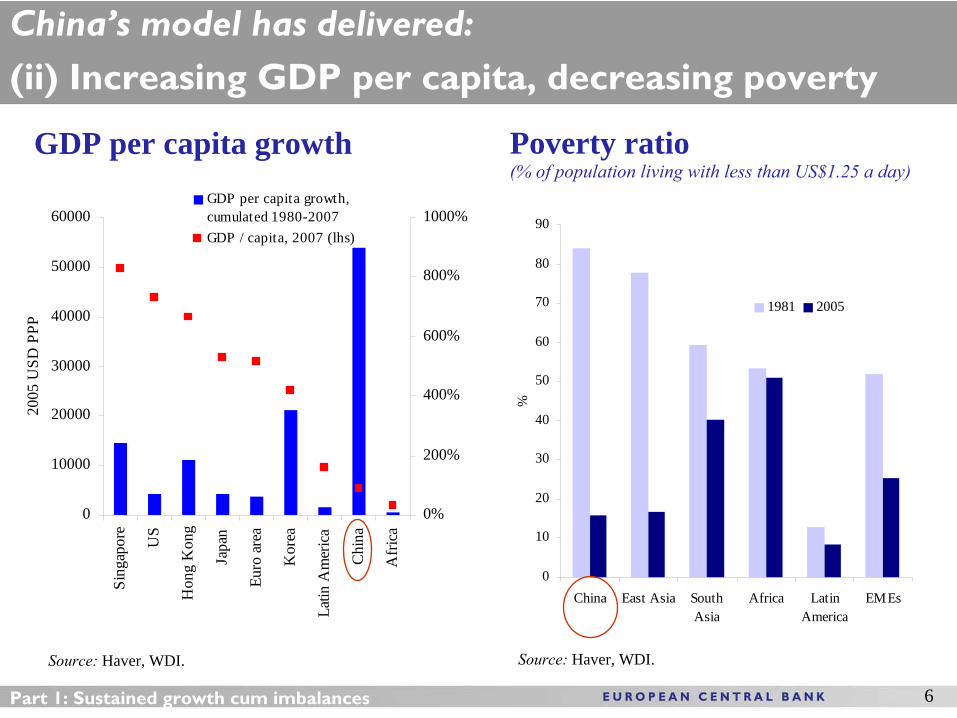

GDP per capita growth

Source: Haver, WDI.

Poverty ratio (% of population living with less than US$1.25 a day)

Source: Haver, WDI.

China’s model has delivered:

(ii) Increasing GDP per capita, decreasing poverty

0

10000

20000

30000

40000

50000

60000

Sing

apor

e

US

Hon

g K

ong

Japa

n

Euro

are

a

Kor

ea

Latin

Am

eric

a

Chi

na

Afr

ica

2005

USD

PPP

0%

200%

400%

600%

800%

1000%GDP per capita growth,cumulated 1980-2007GDP / capita, 2007 (lhs)

0

10

20

30

40

50

60

70

80

90

China East Asia SouthAsia

Africa LatinAmerica

EMEs

%

1981 2005

7Part 1: Sustained growth cum imbalances

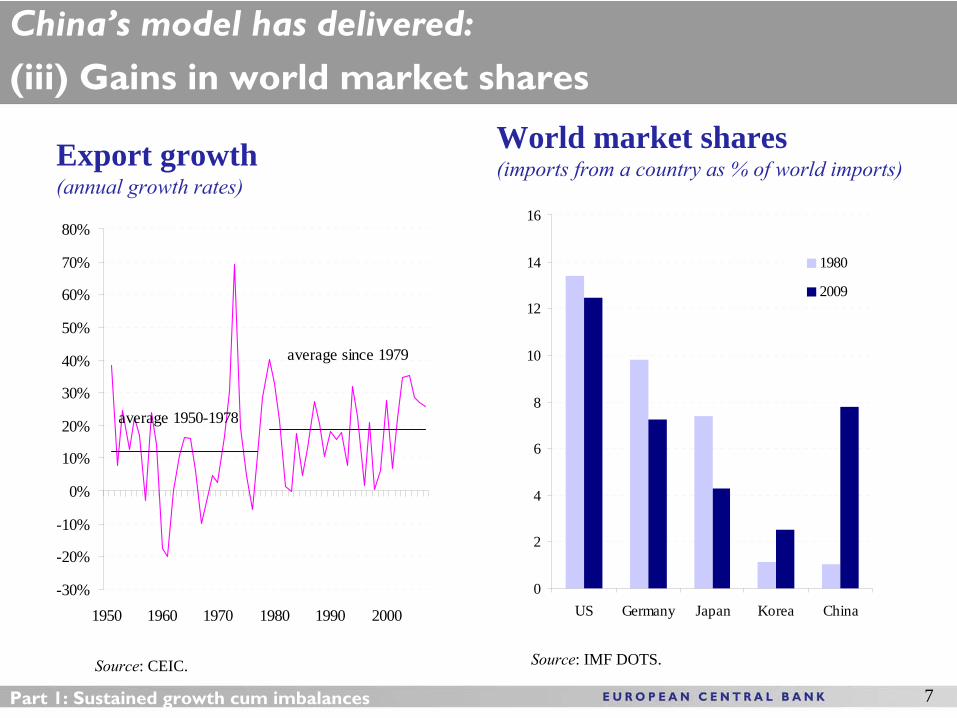

Export growth(annual growth rates)

Source: CEIC.

World market shares(imports from a country as % of world imports)

Source: IMF DOTS.

China’s model has delivered:

(iii) Gains in world market shares

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

1950 1960 1970 1980 1990 2000

average 1950-1978

average since 1979

0

2

4

6

8

10

12

14

16

US Germany Japan Korea China

1980

2009

8Part 1: Sustained growth cum imbalances

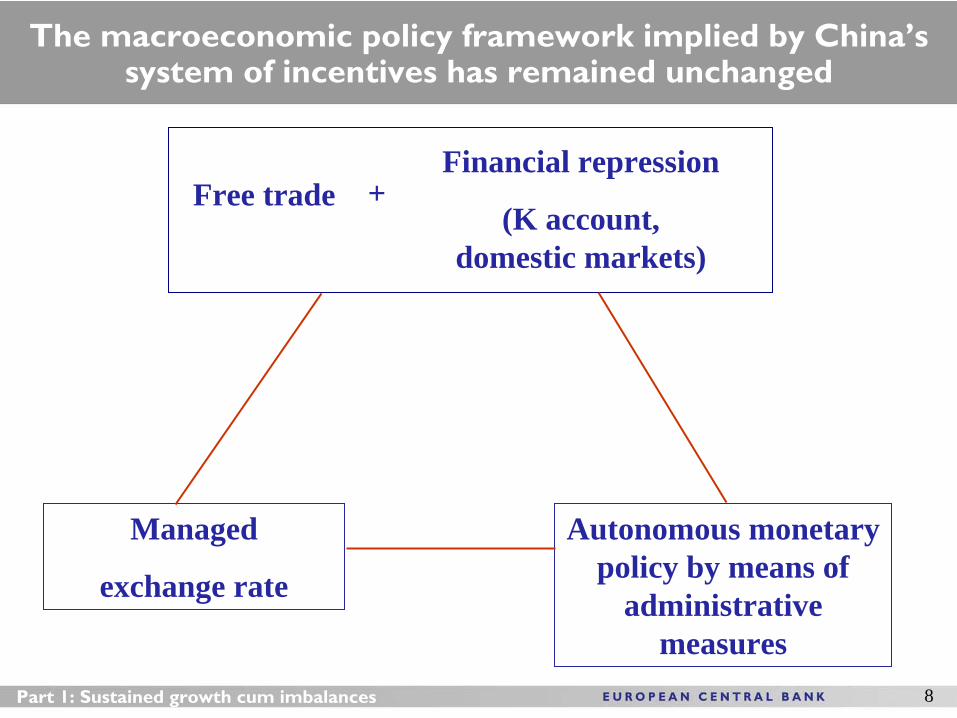

Managed

exchange rate

Free tradeFinancial repression

(K account, domestic markets)

Autonomous monetary policy by means of

administrative measures

+

The macroeconomic policy framework implied by China’s system of incentives has remained unchanged

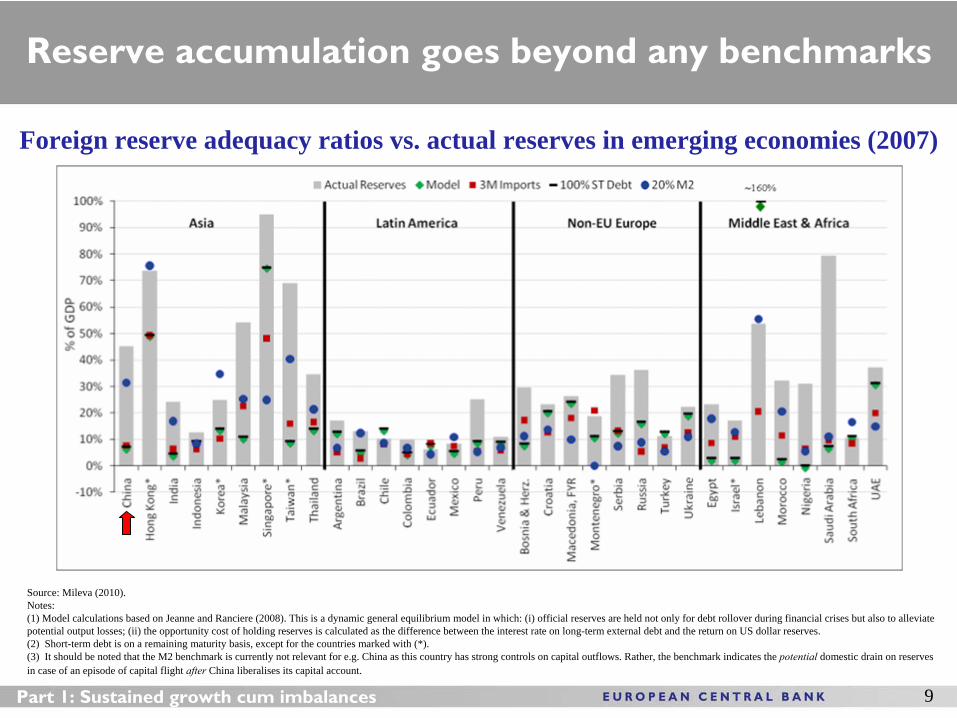

Reserve accumulation goes beyond any benchmarks

9

Foreign reserve adequacy ratios vs. actual reserves in emerging economies (2007)

Source: Mileva (2010).Notes: (1) Model calculations based on Jeanne and Ranciere (2008). This is a dynamic general equilibrium model in which: (i) official reserves are held not only for debt rollover during financial crises but also to alleviate potential output losses; (ii) the opportunity cost of holding reserves is calculated as the difference between the interest rate on long-term external debt and the return on US dollar reserves. (2) Short-term debt is on a remaining maturity basis, except for the countries marked with (*).(3) It should be noted that the M2 benchmark is currently not relevant for e.g. China as this country has strong controls on capital outflows. Rather, the benchmark indicates the potential

domestic drain on reserves in case of an episode of capital flight after

China liberalises its capital account.

Part 1: Sustained growth cum imbalances

10Part 1: Sustained growth cum imbalances

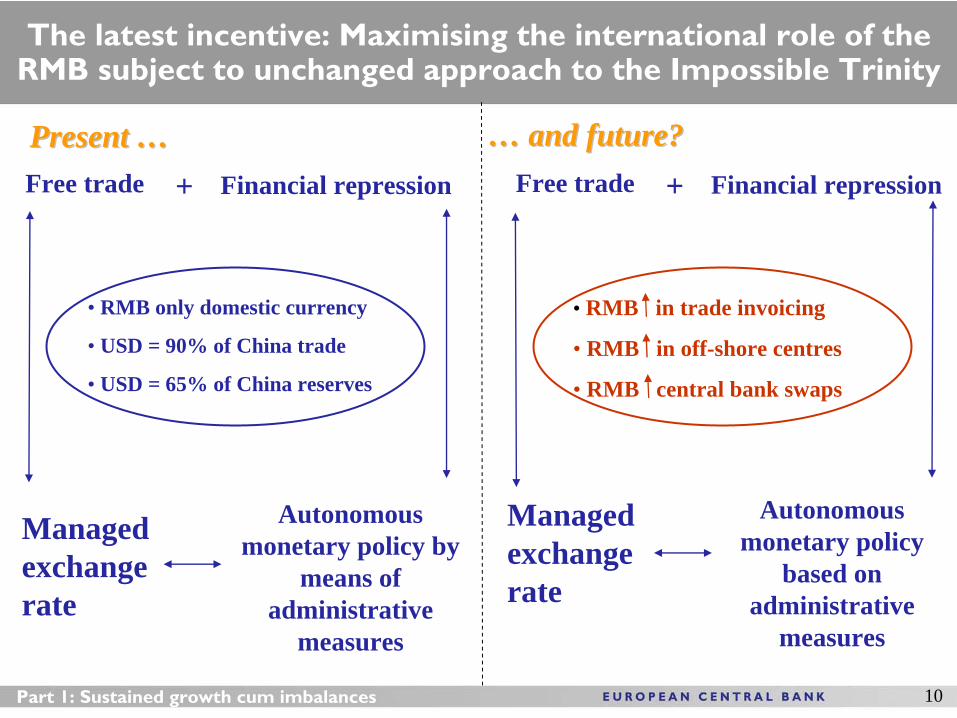

Managed exchange rate

Free trade Financial repression

Autonomous monetary policy by

means of administrative

measures

+

• RMB only domestic currency

• USD = 90% of China trade

• USD = 65% of China reserves

Autonomous monetary policy

based on administrative

measures

• RMB in trade invoicing

• RMB in off-shore centres

• RMB central bank swaps

The latest incentive: Maximising the international role of the RMB subject to unchanged approach to the Impossible Trinity

Managed exchange rate

Present …Present … …… and future?and future?Free trade Financial repression+

China’s imbalanced growth: C vs.

I + (X-M) (1)

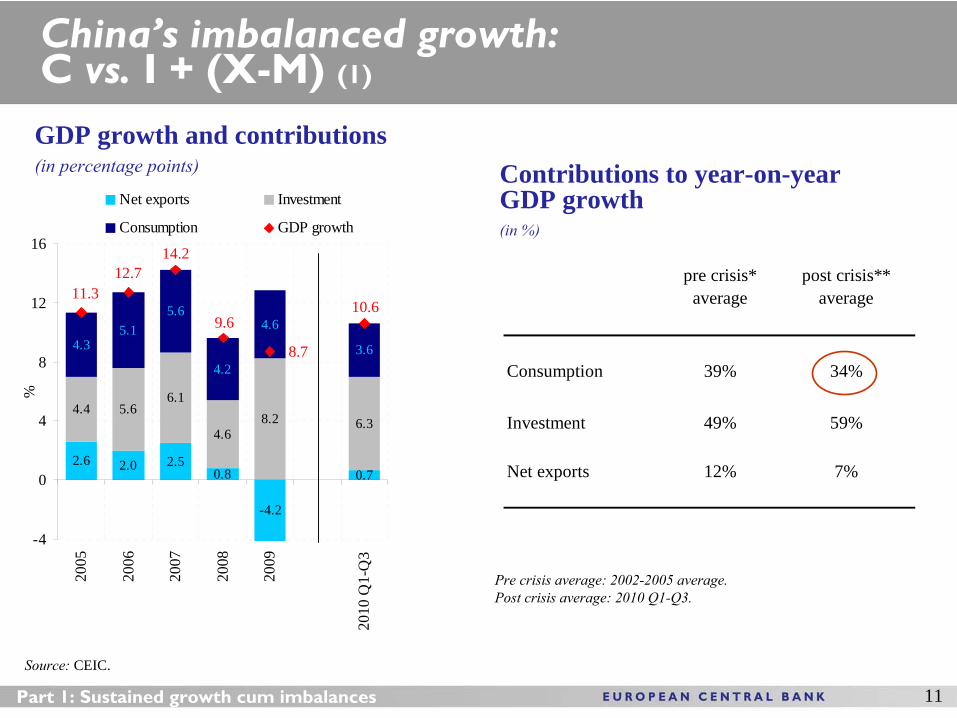

11Part 1: Sustained growth cum imbalances

GDP growth and contributions(in percentage points)

Source: CEIC.

2.6 2.0 2.50.8

-4.2

0.7

4.4 5.66.1

4.68.2 6.3

4.35.1

5.6

4.2

4.6

3.6

10.6

8.7

9.6

14.212.7

11.3

-4

0

4

8

12

16

2005

2006

2007

2008

2009

2010

Q1-

Q3

%

Net exports Investment

Consumption GDP growth

Contributions to year-on-year GDP growth (in %)

pre crisis* average

post crisis** average

Consumption 39% 34%

Investment 49% 59%

Net exports 12% 7%

Pre crisis average: 2002-2005 average.Post crisis average: 2010 Q1-Q3.

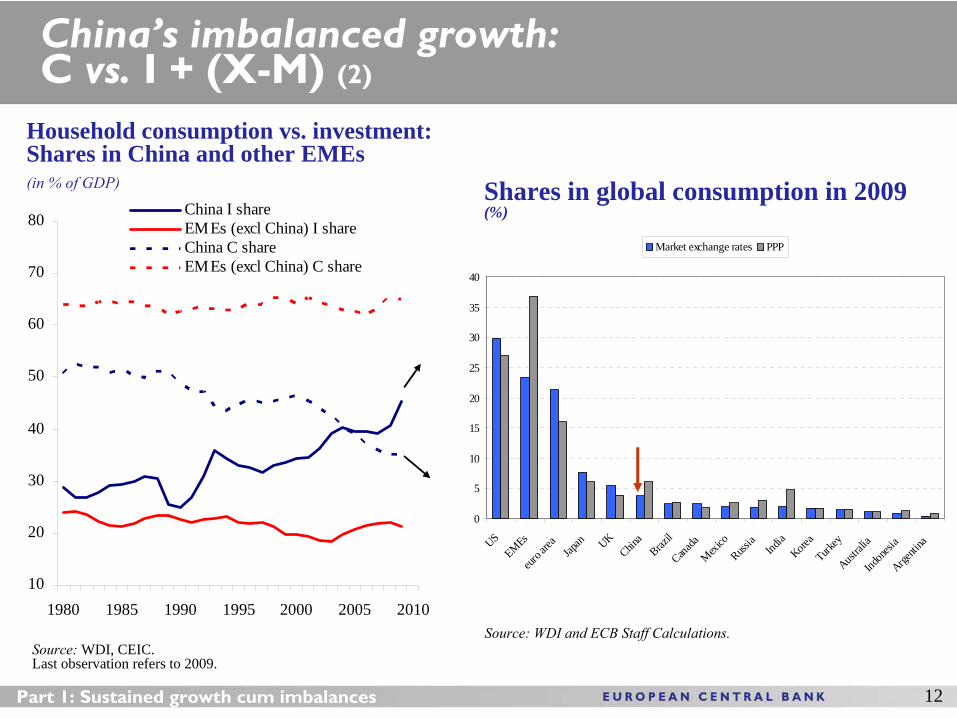

China’s imbalanced growth: C vs.

I + (X-M) (2)

12Part 1: Sustained growth cum imbalances

Household consumption vs. investment: Shares in China and other EMEs(in % of GDP)

Source: WDI, CEIC.Last observation refers to 2009.

10

20

30

40

50

60

70

80

1980 1985 1990 1995 2000 2005 2010

China I shareEMEs (excl China) I shareChina C shareEMEs (excl China) C share

Shares in global consumption in 2009 (%)

Source: WDI and ECB Staff Calculations.

0

5

10

15

20

25

30

35

40

USEMEs

euro a

rea Japan UK

China

Brazil

Canada

Mexico

Russia

India

Korea

Turkey

Austral

iaInd

onesi

aArge

ntina

Market exchange rates PPP

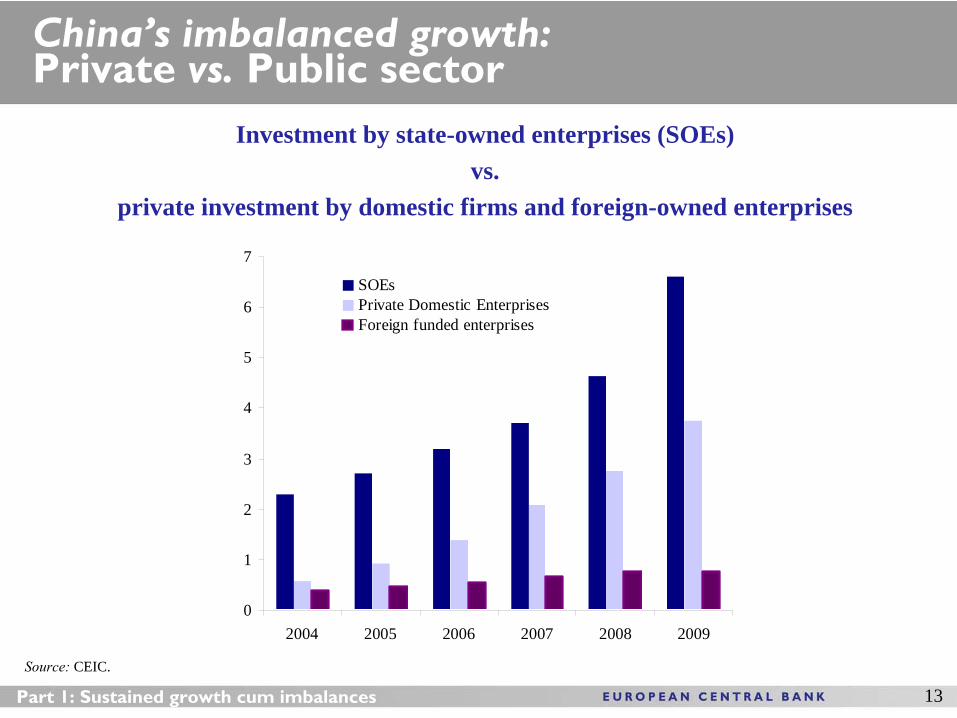

China’s imbalanced growth: Private vs.

Public sector

13Part 1: Sustained growth cum imbalances

Investment by state-owned enterprises (SOEs) vs.

private investment by domestic firms and foreign-owned enterprises(RMB trn)

Source: CEIC.

0

1

2

3

4

5

6

7

2004 2005 2006 2007 2008 2009

SOEsPrivate Domestic EnterprisesForeign funded enterprises

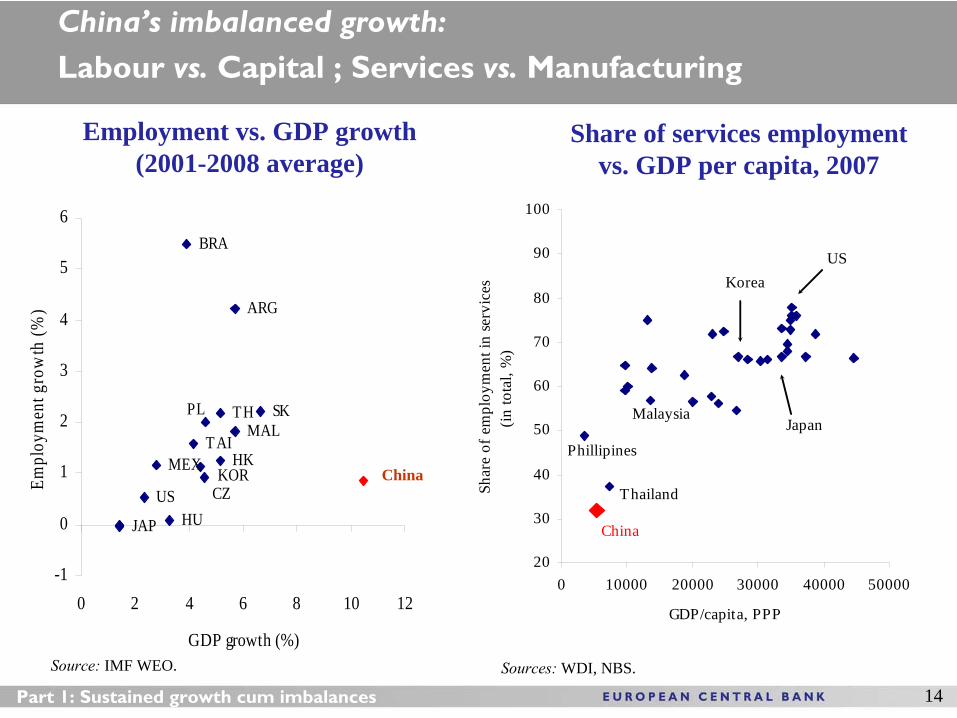

China’s imbalanced growth:

Labour vs.

Capital ; Services vs. Manufacturing

14

Employment vs. GDP growth (2001-2008 average)

CH

TH

HKKOR

MALTAI

ARG

BRA

MEX

JAP

CZHU

PL SK

US

-1

0

1

2

3

4

5

6

0 2 4 6 8 10 12

GDP growth (%)

Empl

oym

ent g

row

th (%

)

Source: IMF WEO.

China

20

30

40

50

60

70

80

90

100

0 10000 20000 30000 40000 50000

GDP/capita, PPP

Shar

e of

em

ploy

men

t in

serv

ices

(in

tota

l, %

)China

Korea

Japan

US

Thailand

Phillipines

Malaysia

Sources: WDI, NBS.

Share of services employment vs. GDP per capita, 2007

Part 1: Sustained growth cum imbalances

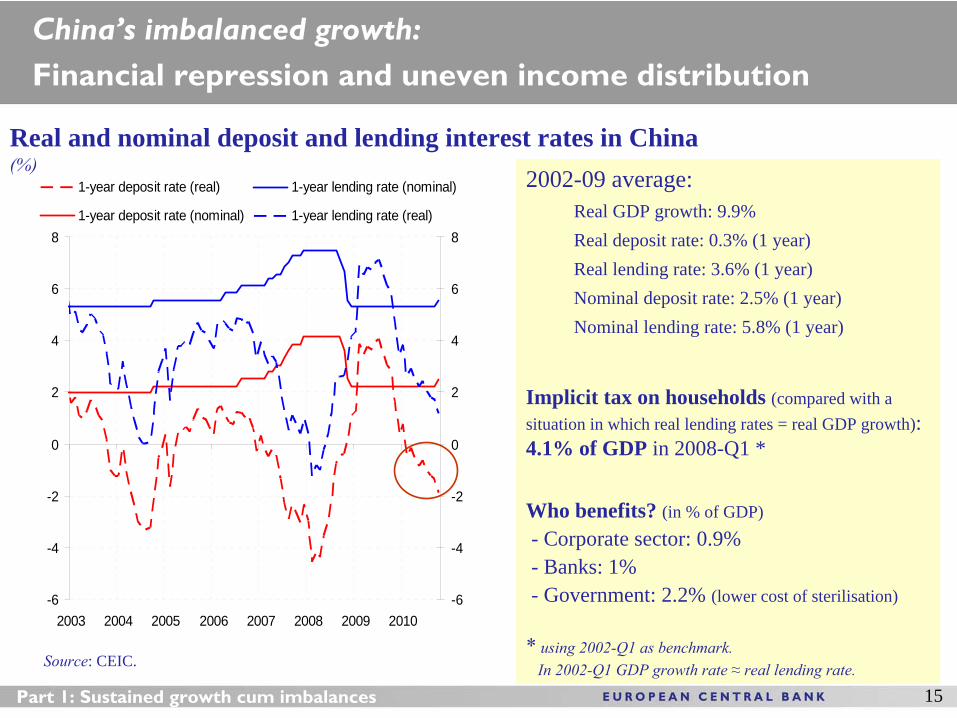

15

Real and nominal deposit and lending interest rates in China (%)

Source: CEIC.

2002-09 average: Real GDP growth: 9.9%Real deposit rate: 0.3% (1 year)Real lending rate: 3.6% (1 year)Nominal deposit rate: 2.5% (1 year)Nominal lending rate: 5.8% (1 year)

Implicit tax on households (compared with a situation in which real lending rates = real GDP growth): 4.1% of GDP in 2008-Q1 *

Who benefits? (in % of GDP)- Corporate sector: 0.9%- Banks: 1% - Government: 2.2% (lower cost of sterilisation)

*

using 2002-Q1 as benchmark. In 2002-Q1 GDP growth rate ≈

real lending rate.

China’s imbalanced growth:

Financial repression and uneven income distribution

Part 1: Sustained growth cum imbalances

-6

-4

-2

0

2

4

6

8

2003 2004 2005 2006 2007 2008 2009 2010-6

-4

-2

0

2

4

6

8

1-year deposit rate (real) 1-year lending rate (nominal)

1-year deposit rate (nominal) 1-year lending rate (real)

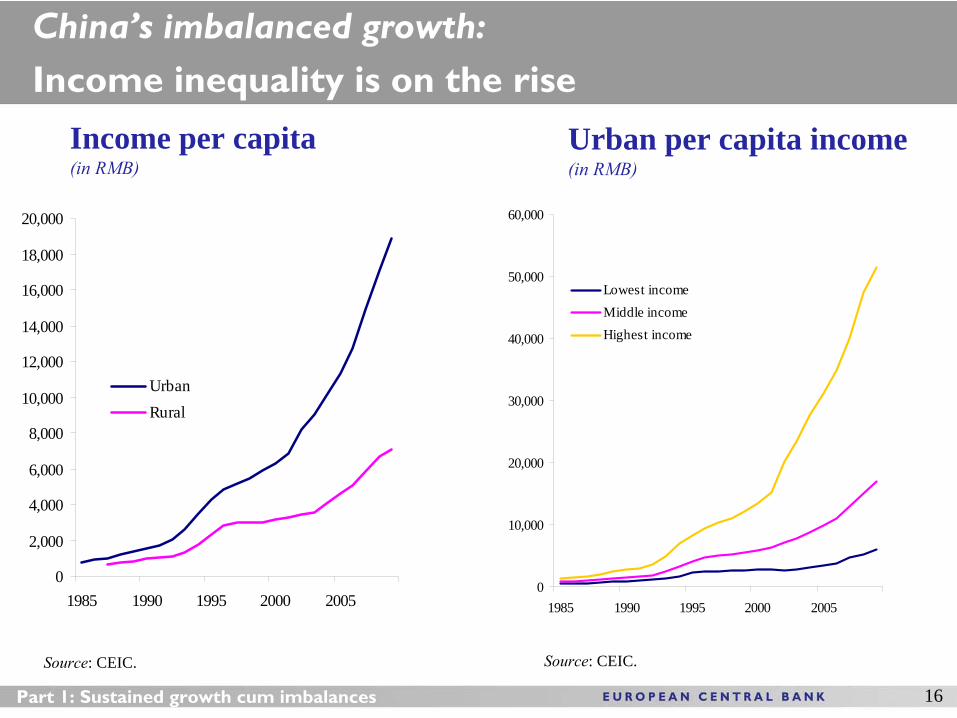

16

Urban per capita income(in RMB)

Source: CEIC.

China’s imbalanced growth:

Income inequality is on the rise

Part 1: Sustained growth cum imbalances

0

10,000

20,000

30,000

40,000

50,000

60,000

1985 1990 1995 2000 2005

Lowest incomeMiddle incomeHighest income

Income per capita(in RMB)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

1985 1990 1995 2000 2005

UrbanRural

Source: CEIC.

Part 2 Part 2 –– LongerLonger--term sustainability of the current model:term sustainability of the current model:

Are the longAre the long--term factors supporting China’s model running out? term factors supporting China’s model running out? Will this “force” adjustment towards more sustainable growth?Will this “force” adjustment towards more sustainable growth?

Key proposition:

The main long-term factors making China’s growth model possible have been: (1) export demand; (2) demographic factors coupled with labour surplus in the primary sector; and (3) capital accumulation.

These factors have started running out, thus forcing adjustment.17Part 2: What longer-term developments could “force” adjustment?

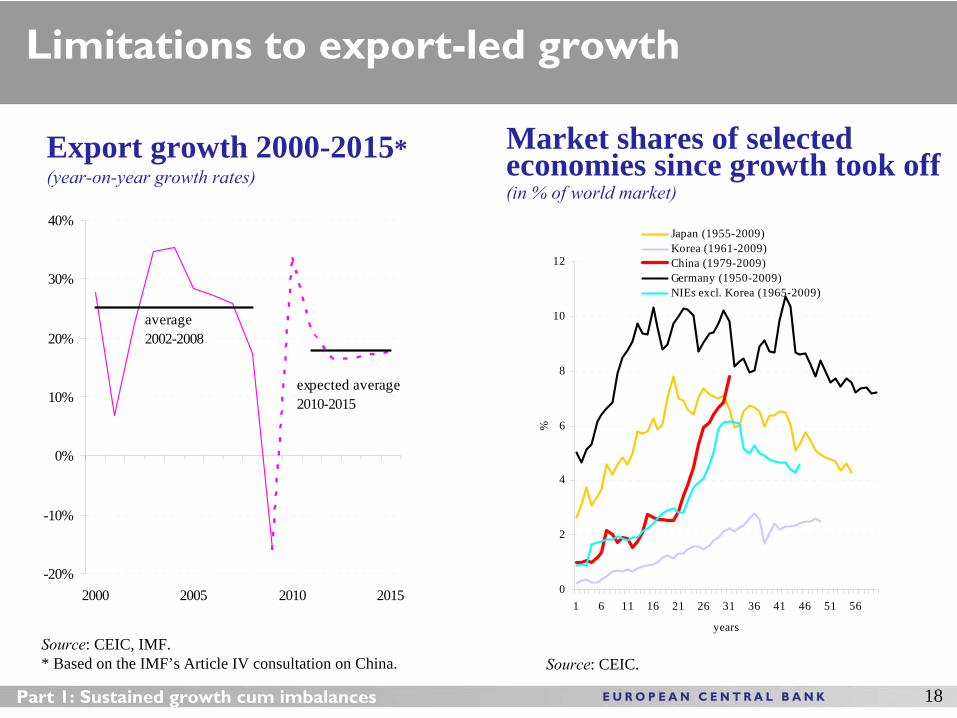

18

Export growth 2000-2015*(year-on-year growth rates)

Source: CEIC, IMF. * Based on the IMF’s Article IV consultation on China.

Limitations to export-led growth

Part 1: Sustained growth cum imbalances

Market shares of selected economies since growth took off(in % of world market)

Source: CEIC.

0

2

4

6

8

10

12

1 6 11 16 21 26 31 36 41 46 51 56

years

%

Japan (1955-2009)Korea (1961-2009)China (1979-2009)Germany (1950-2009)NIEs excl. Korea (1965-2009)

-20%

-10%

0%

10%

20%

30%

40%

2000 2005 2010 2015

average 2002-2008

expected average 2010-2015

19

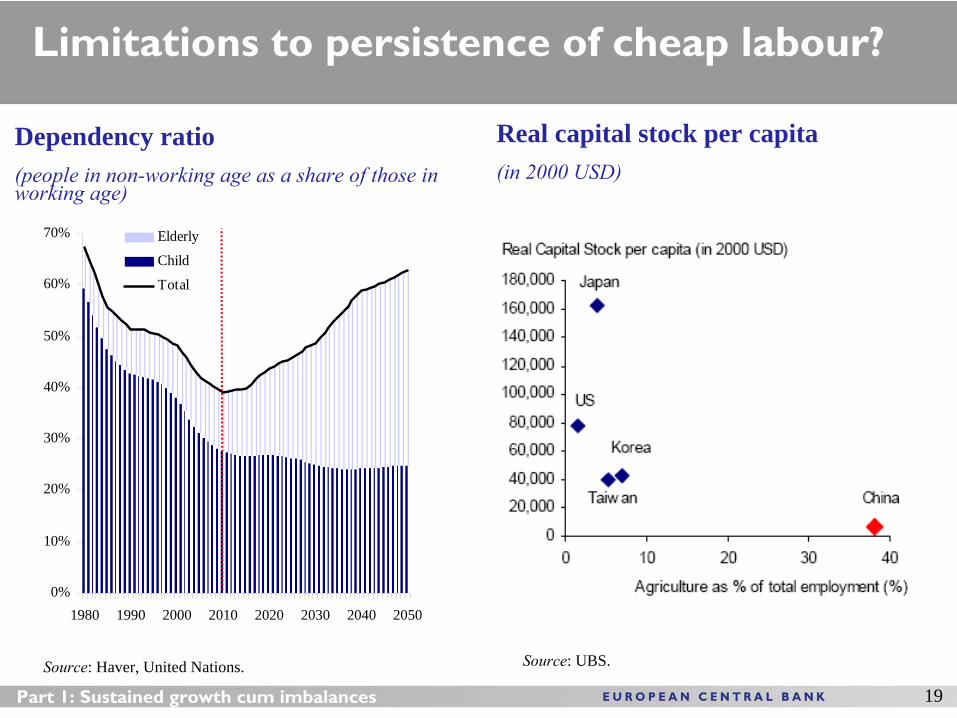

Real capital stock per capita (in 2000 USD)

Source: UBS.

Limitations to persistence of cheap labour?

Part 1: Sustained growth cum imbalances

Dependency ratio(people in non-working age as a share of those in working age)

Source: Haver, United Nations.

0%

10%

20%

30%

40%

50%

60%

70%

1980 1990 2000 2010 2020 2030 2040 2050

Elderly

Child

Total

20

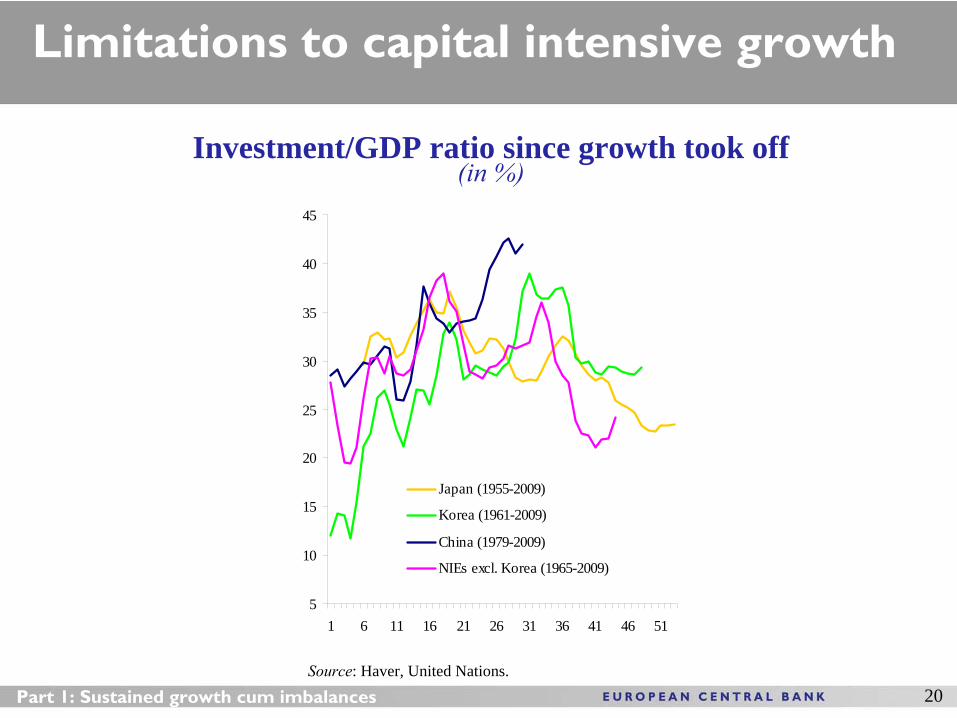

Limitations to capital intensive growth

Part 1: Sustained growth cum imbalances

Investment/GDP ratio since growth took off (in %)

Source: Haver, United Nations.

5

10

15

20

25

30

35

40

45

1 6 11 16 21 26 31 36 41 46 51

Japan (1955-2009)

Korea (1961-2009)

China (1979-2009)

NIEs excl. Korea (1965-2009)

21

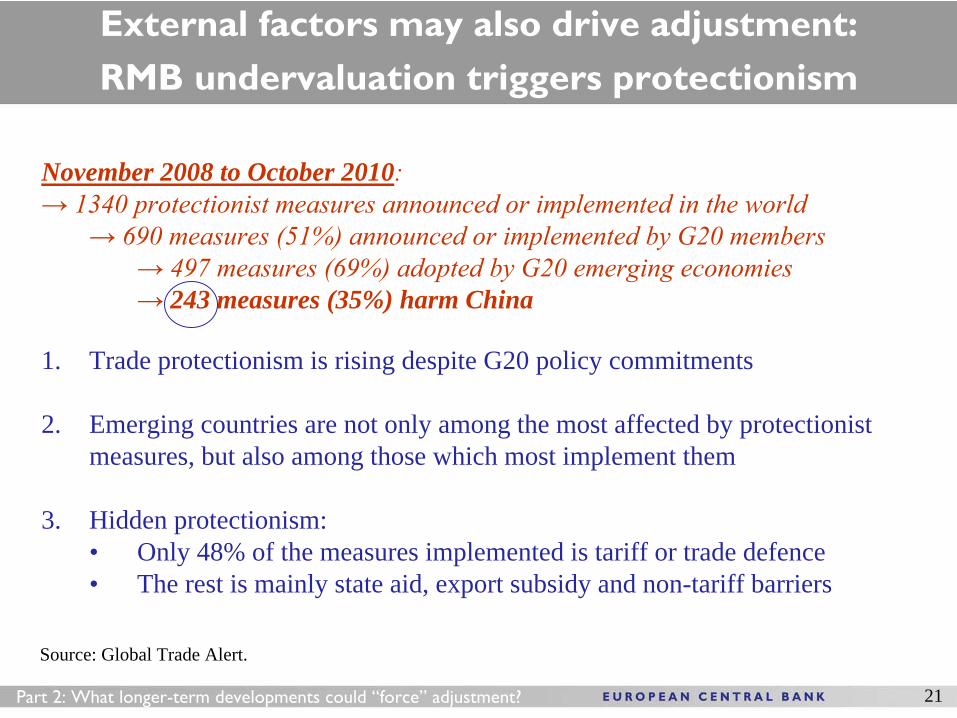

External factors may also drive adjustment:

RMB undervaluation triggers protectionism

November 2008 to October 2010: → 1340 protectionist measures announced or implemented in the world

→ 690 measures (51%) announced or implemented by G20 members→ 497 measures (69%) adopted by G20 emerging economies→ 243 measures (35%) harm China

1. Trade protectionism is rising despite G20 policy commitments

2. Emerging countries are not only among the most affected by protectionist measures, but also among those which most implement them

3. Hidden protectionism:• Only 48% of the measures implemented is tariff or trade defence• The rest is mainly state aid, export subsidy and non-tariff barriers

Source: Global Trade Alert.

Part 2: What longer-term developments could “force” adjustment?

Part 3 – What is being done do adjust the model:

The thorny way to rebalancingThe thorny way to rebalancing

Key proposition:Rebalancing is proceeding slowly, also because of policy resistance to change a model of growth that delivered for 30 years.

This may imply short-term advantages, but also longer-term risks given the fading away of longer-run supporting factors.

22

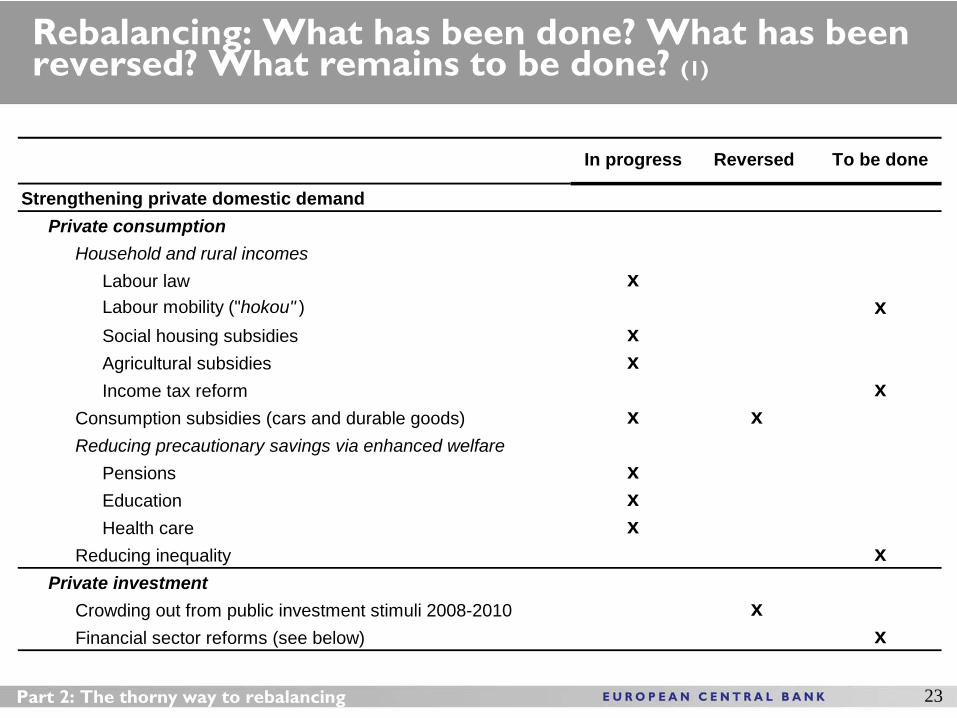

Rebalancing: What has been done? What has been reversed? What remains to be done? (1)

23Part 2: The thorny way to rebalancing

Strengthening private domestic demandPrivate consumption

Household and rural incomesLabour law xLabour mobility ("hokou" ) xSocial housing subsidies xAgricultural subsidies xIncome tax reform x

Consumption subsidies (cars and durable goods) x xReducing precautionary savings via enhanced welfare

Pensions xEducation xHealth care x

Reducing inequality xPrivate investment

Crowding out from public investment stimuli 2008-2010 xFinancial sector reforms (see below) x

In progress Reversed To be done

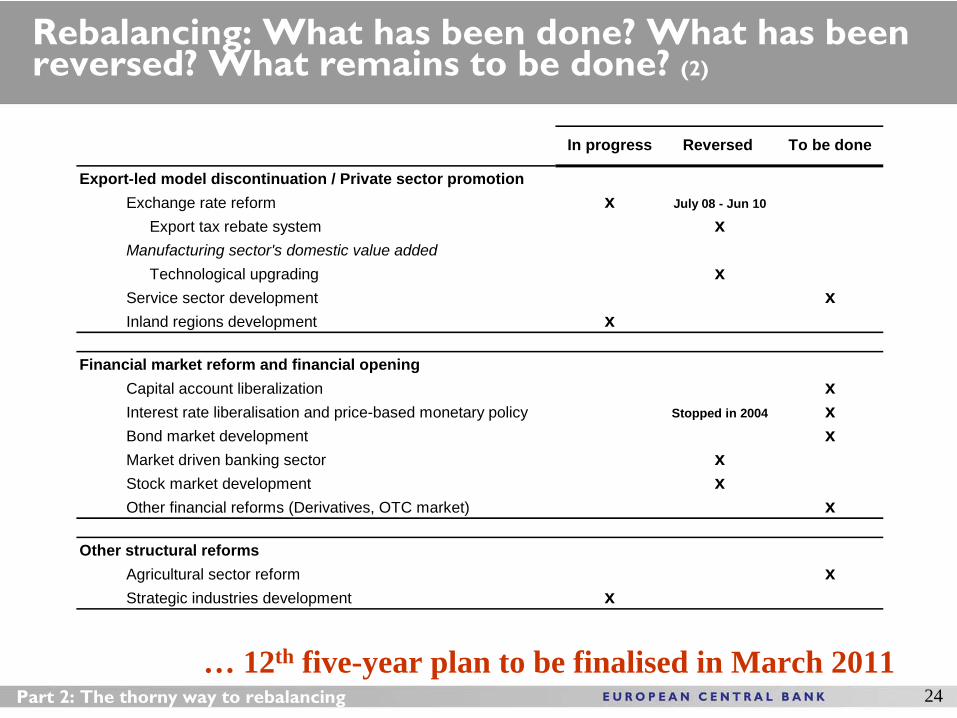

Rebalancing: What has been done? What has been reversed? What remains to be done? (2)

24Part 2: The thorny way to rebalancing

… 12th five-year plan to be finalised in March 2011

Export-led model discontinuation / Private sector promotionExchange rate reform x July 08 - Jun 10

Export tax rebate system xManufacturing sector's domestic value added

Technological upgrading xService sector development xInland regions development x

Financial market reform and financial openingCapital account liberalization xInterest rate liberalisation and price-based monetary policy Stopped in 2004 xBond market development xMarket driven banking sector xStock market development xOther financial reforms (Derivatives, OTC market) x

Other structural reformsAgricultural sector reform xStrategic industries development x

In progress Reversed To be done

Part 4 – Current contradictions in the adjustment of the model:

Tensions between Tensions between shortshort--term growth objectives and term growth objectives and

longerlonger--term rebalancing needsterm rebalancing needs

Key proposition:

Yes, there are tensions and contradictions, both on Yes, there are tensions and contradictions, both on (1) the external and (2) the domestic front.(1) the external and (2) the domestic front.

25

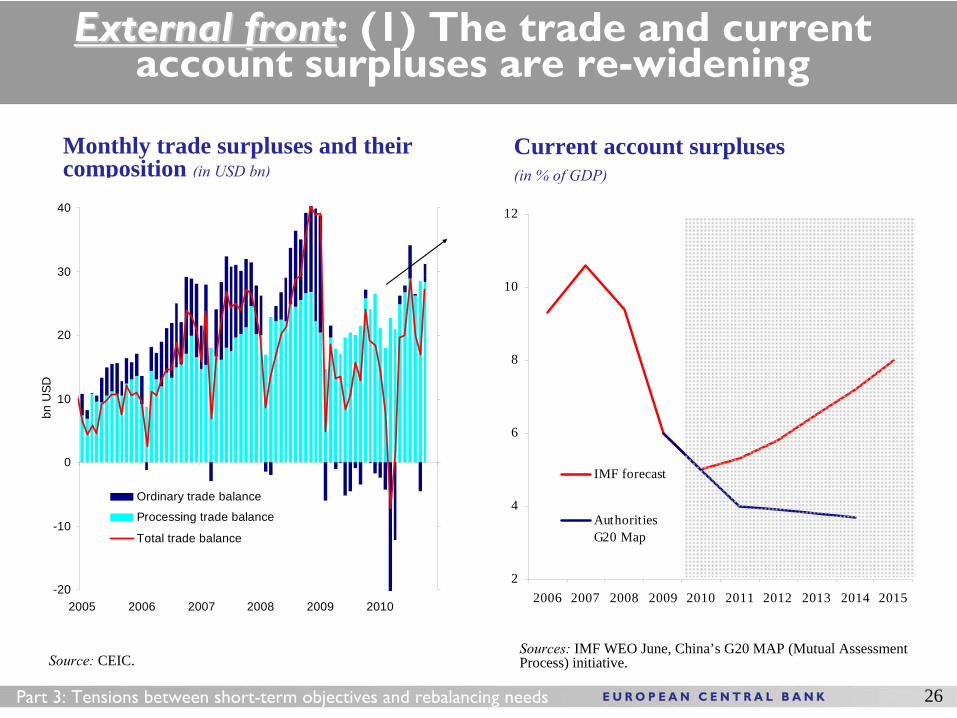

26Part 3: Tensions between short-term objectives and rebalancing needs

External frontExternal front: (1) The trade and current account surpluses are re-widening

Current account surpluses(in % of GDP)

Monthly trade surpluses and their composition (in USD bn)

Source: CEIC.

-20

-10

0

10

20

30

40

2005 2006 2007 2008 2009 2010

bn U

SD

-20

-10

0

10

20

30

40

Ordinary trade balance

Processing trade balance

Total trade balance

2

4

6

8

10

12

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

IMF forecast

AuthoritiesG20 Map

Sources:

IMF WEO June, China’s G20 MAP (Mutual Assessment Process) initiative.

27Part 3: Tensions between short-term objectives and rebalancing needs

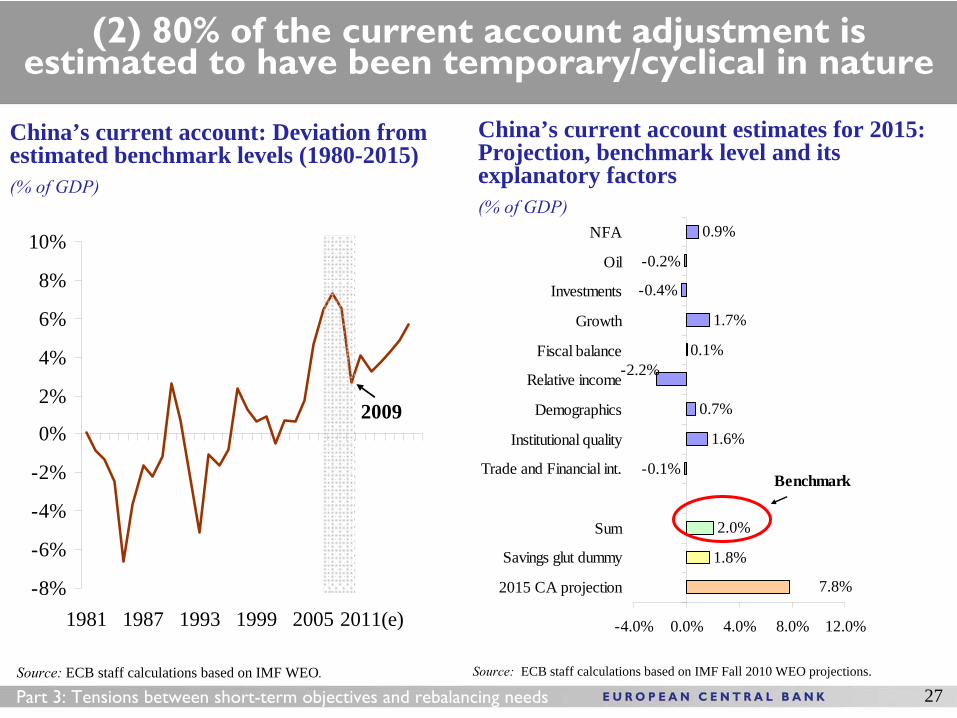

(2) 80% of the current account adjustment is estimated to have been temporary/cyclical in nature

China’s current account: Deviation from estimated benchmark levels (1980-2015) (% of GDP)

China’s current account estimates for 2015: Projection, benchmark level and its explanatory factors(% of GDP)

Source: ECB staff calculations based on IMF WEO. Source: ECB staff calculations based on IMF Fall 2010 WEO projections.

0.9%

-0.2%

-0.4%

1.7%

0.1%

0.7%

1.6%

-0.1%

2.0%

-2.2%

1.8%

7.8%

-4.0% 0.0% 4.0% 8.0% 12.0%

NFA

Oil

Investments

Growth

Fiscal balance

Relative income

Demographics

Institutional quality

Trade and Financial int.

Sum

Savings glut dummy

2015 CA projection

Benchmark

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

1981 1987 1993 1999 2005 2011(e)

2009

28

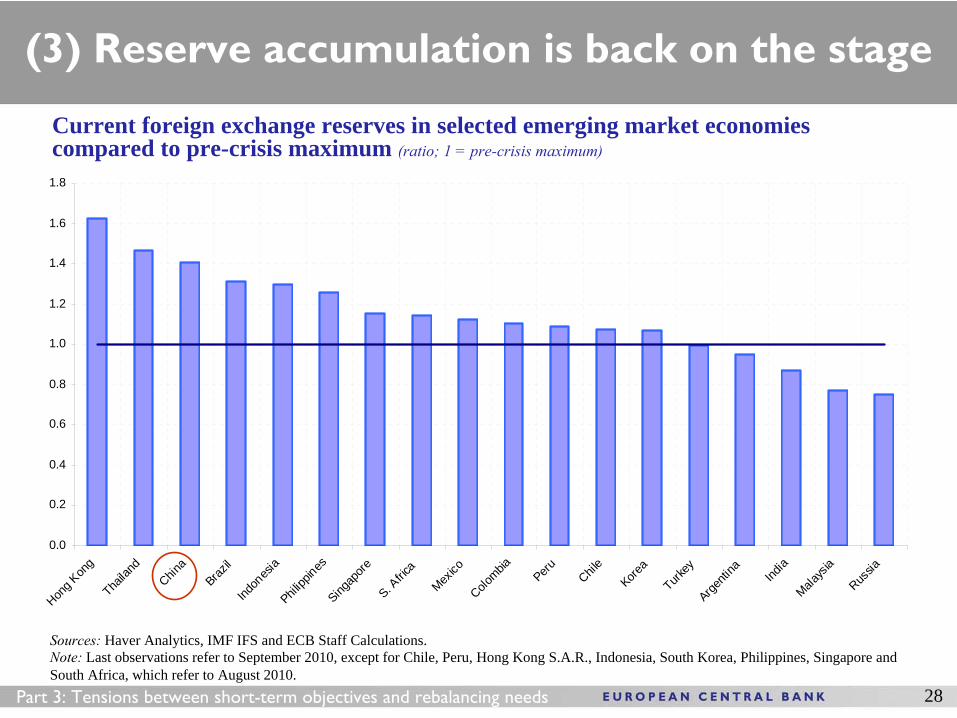

(3) Reserve accumulation is back on the stage

Current foreign exchange reserves in selected emerging market economies compared to pre-crisis maximum (ratio; 1 = pre-crisis maximum)

Sources: Haver Analytics, IMF IFS and ECB Staff Calculations.Note: Last observations refer to September 2010, except for Chile, Peru, Hong Kong S.A.R., Indonesia, South Korea, Philippines, Singapore and South Africa, which refer to August 2010.

Part 3: Tensions between short-term objectives and rebalancing needs

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Hong K

ong

Thaila

nd

China

Brazil

Indon

esia

Philipp

inesSing

apore

S. Afric

a

Mexico

Colombia

Peru Chile

Korea

Turkey

Argenti

na India

Malays

ia

Russia

29Part 3: Tensions between short-term objectives and rebalancing needs

Source: BloombergNote: Last observation refers to 17 November 2010.

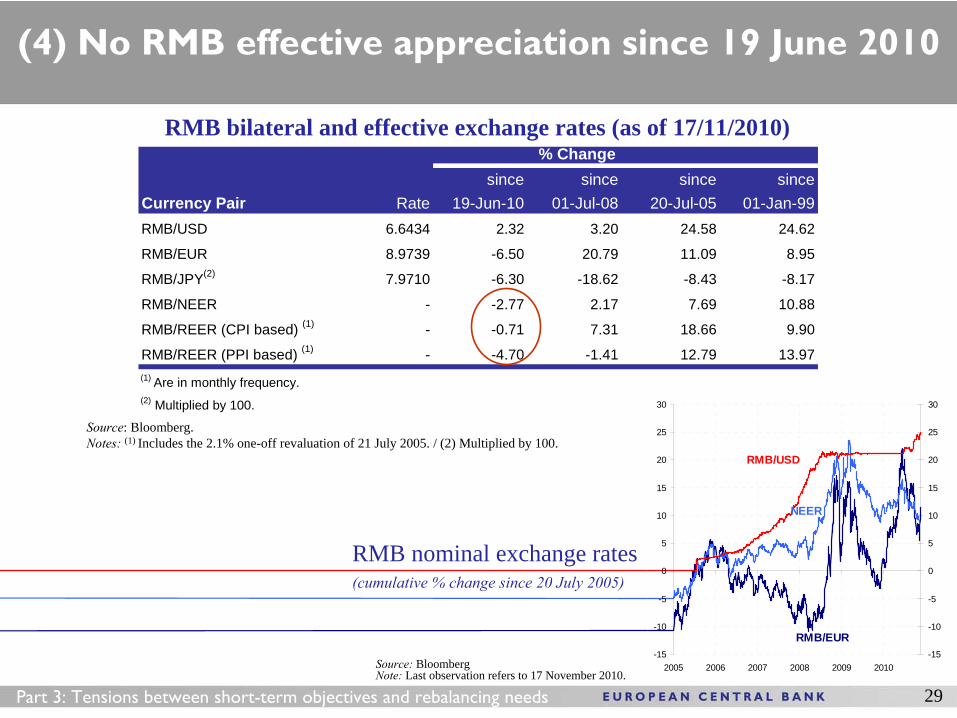

(4) No RMB effective appreciation since 19 June 2010

RMB nominal exchange rates (cumulative % change since 20 July 2005)

RMB bilateral and effective exchange rates (as of 17/11/2010)

Source: Bloomberg.Notes: (1) Includes the 2.1% one-off revaluation of 21 July 2005. / (2) Multiplied by 100.

(1)

7.31

-1.41

since01-Jan-99

24.62

8.95

-8.17

10.88

9.90

13.97

since19-Jun-10

since20-Jul-05

since01-Jul-08

24.58

RMB/NEER

RMB/EUR

-6.30

12.79

- -2.77

-0.71

-4.70

2.17

11.09

-8.43

7.69

18.66

RMB/USD

RMB/JPY(2)

RMB/REER (CPI based) (1)

RMB/REER (PPI based) (1)

-

-(1) Are in monthly frequency.(2) Multiplied by 100.

20.79

6.6434

8.9739

7.9710

2.32

-6.50

3.20

-18.62

RateCurrency Pair

% Change

-15

-10

-5

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010-15

-10

-5

0

5

10

15

20

25

30

RMB/USD

RMB/EUR

NEER

30Part 3: Tensions between short-term objectives and rebalancing needs

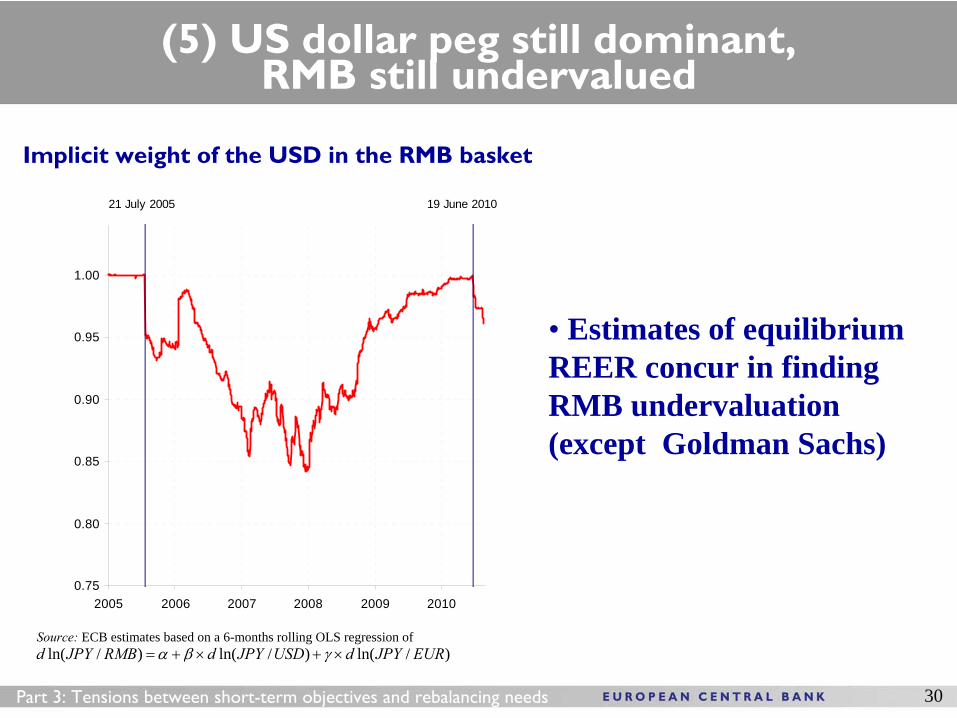

(5) US dollar peg still dominant, RMB still undervalued

Source:

ECB estimates based on a 6-months rolling OLS regression of

Implicit weight of the USD in the RMB basket

0.75

0.80

0.85

0.90

0.95

1.00

2005 2006 2007 2008 2009 2010

21 July 2005 19 June 2010

)/ln()/ln()/ln( EURJPYdUSDJPYdRMBJPYd

• Estimates of equilibrium REER concur in finding RMB undervaluation (except Goldman Sachs)

31Part 3: Tensions between short-term objectives and rebalancing needs

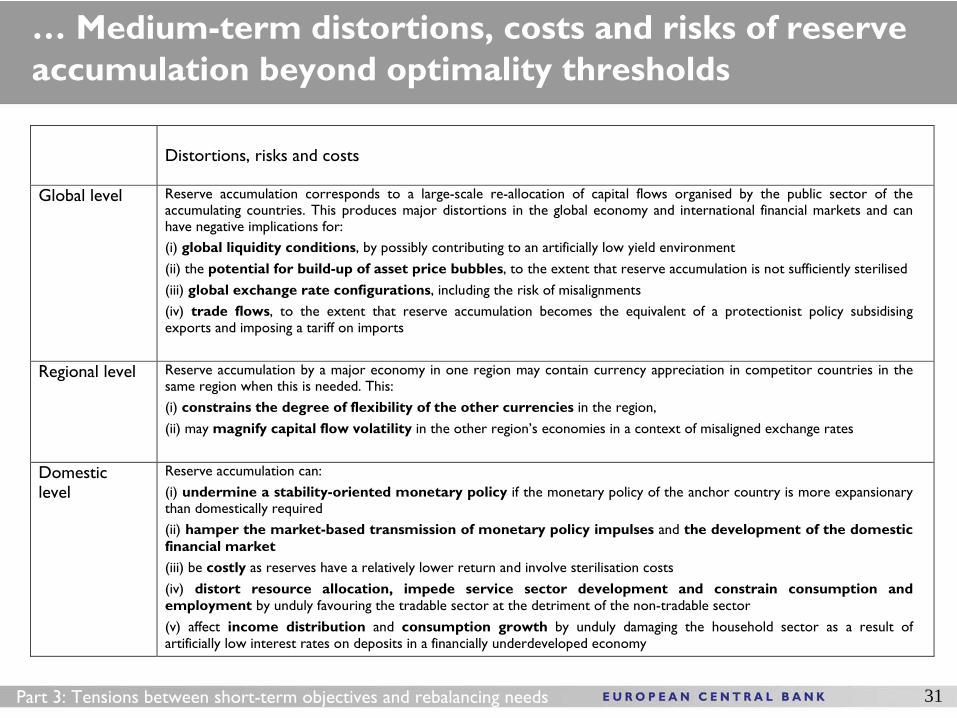

Distortions, risks and costs

Global level Reserve accumulation corresponds to a large-scale re-allocation of capital flows organised by the public sector of the accumulating countries. This produces major distortions in the global economy and international financial markets and can have negative implications for: (i) global liquidity conditions, by possibly contributing to an artificially low yield environment (ii) the potential for build-up of asset price bubbles, to the extent that reserve accumulation is not sufficiently sterilised (iii) global exchange rate configurations, including the risk of misalignments (iv) trade flows, to the extent that reserve accumulation becomes the equivalent of a protectionist policy subsidising exports and imposing a tariff on imports

Regional level Reserve accumulation by a major economy in one region may contain currency appreciation in competitor countries in the same region when this is needed. This: (i) constrains the degree of flexibility of the other currencies in the region, (ii) may magnify capital flow volatility in the other region’s economies in a context of misaligned exchange rates

Domestic level

Reserve accumulation can: (i) undermine a stability-oriented monetary policy if the monetary policy of the anchor country is more expansionary than domestically required (ii) hamper the market-based transmission of monetary policy impulses and the development of the domestic financial market (iii) be costly as reserves have a relatively lower return and involve sterilisation costs (iv) distort resource allocation, impede service sector development and constrain consumption and employment by unduly favouring the tradable sector at the detriment of the non-tradable sector (v) affect income distribution and consumption growth by unduly damaging the household sector as a result of artificially low interest rates on deposits in a financially underdeveloped economy

… Medium-term distortions, costs and risks of reserve accumulation beyond optimality thresholds

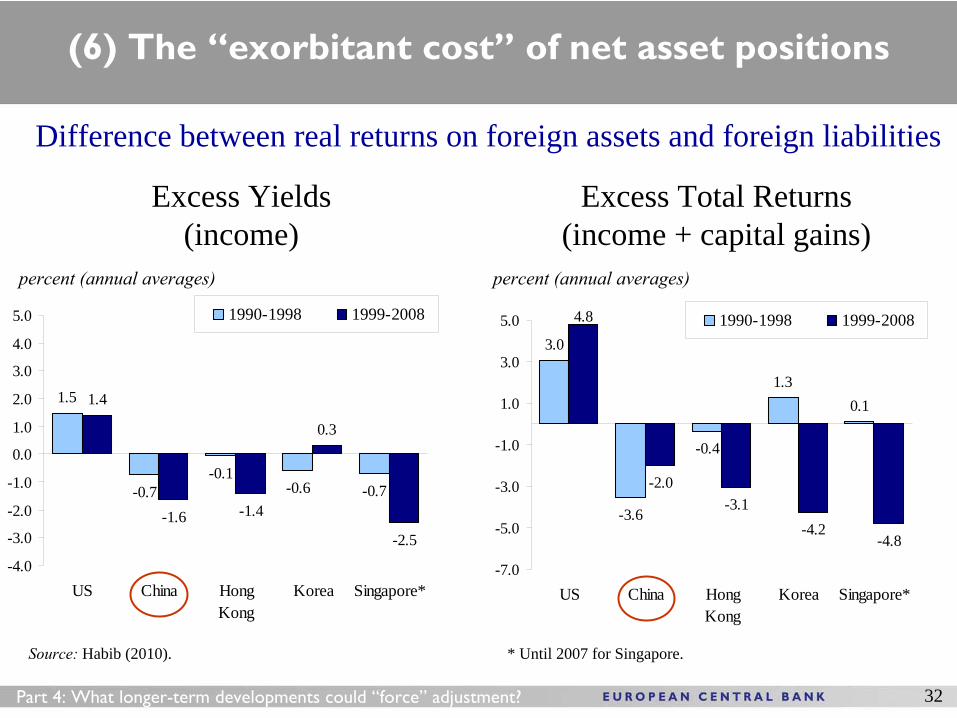

(6) The “exorbitant cost” of net asset positions

Source:

Habib (2010). * Until 2007 for Singapore.

Difference between real returns on foreign assets and foreign liabilities

Excess Yields (income)

Excess Total Returns (income + capital gains)

percent (annual averages) percent (annual averages)

32

3.0

-3.6

-0.4

1.30.1

4.8

-2.0-3.1

-4.2-4.8

-7.0

-5.0

-3.0

-1.0

1.0

3.0

5.0

US China HongKong

Korea Singapore*

1990-1998 1999-2008

1.5

-0.7-0.1

-0.6 -0.7

1.4

-1.6 -1.4

0.3

-2.5

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

US China HongKong

Korea Singapore*

1990-1998 1999-2008

Part 4: What longer-term developments could “force” adjustment?

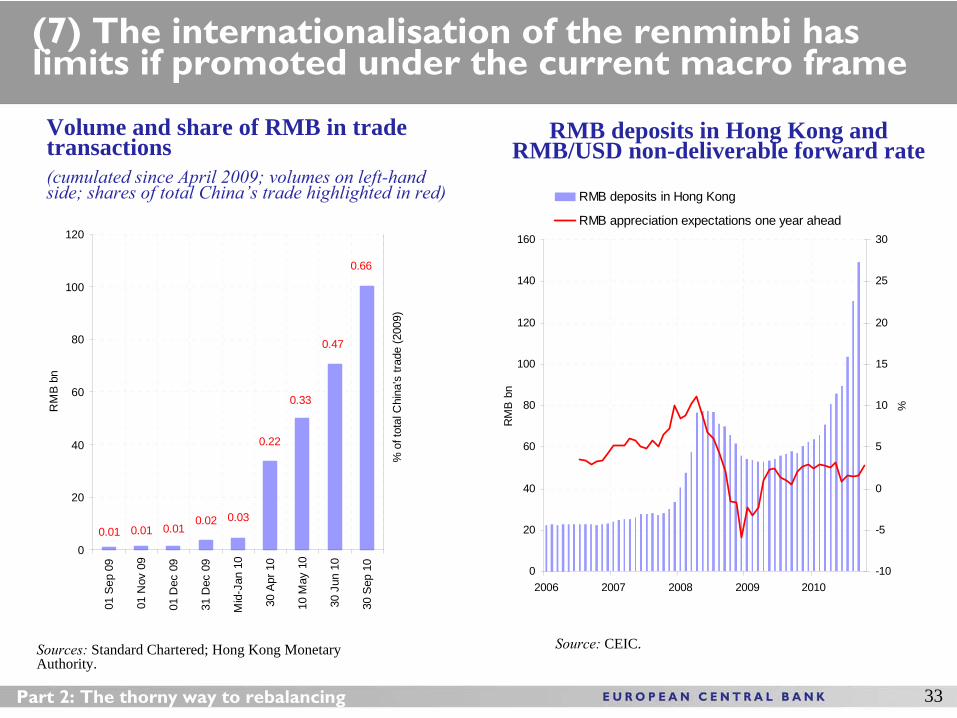

(7) The internationalisation of the renminbi has limits if promoted under the current macro frame

33Part 2: The thorny way to rebalancing

Volume and share of RMB in trade transactions(cumulated since April 2009; volumes on left-hand side; shares of total China’s trade highlighted in red)

Sources: Standard Chartered; Hong Kong Monetary Authority.

RMB deposits in Hong Kong and RMB/USD non-deliverable forward rate

Source: CEIC.

0

20

40

60

80

100

120

140

160

2006 2007 2008 2009 2010

RM

B b

n

-10

-5

0

5

10

15

20

25

30

%

RMB deposits in Hong Kong

RMB appreciation expectations one year ahead

0.47

0.01 0.01 0.010.02 0.03

0.22

0.33

0

20

40

60

80

100

120

01 S

ep 0

9

01 N

ov 0

9

01 D

ec 0

9

31 D

ec 0

9

Mid

-Jan

10

30 A

pr 1

0

10 M

ay 1

0

30 J

un 1

0

30 S

ep 1

0

RM

B b

n

% o

f tot

al C

hina

's tr

ade

(200

9)

0.66

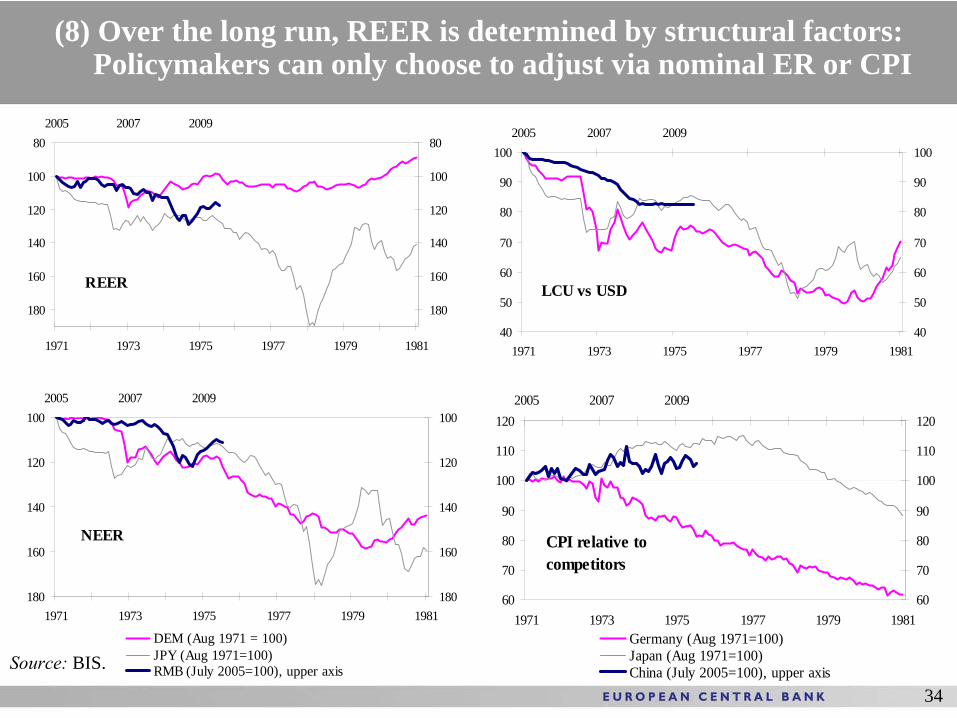

(8) Over the long run, REER is determined by structural factors: Policymakers can only choose to adjust via nominal ER or CPI

34

80

100

120

140

160

180

1971 1973 1975 1977 1979 1981

80

100

120

140

160

180

2005 2007 2009

REER

100

120

140

160

1801971 1973 1975 1977 1979 1981

100

120

140

160

180

2005 2007 2009

DEM (Aug 1971 = 100)JPY (Aug 1971=100)RMB (July 2005=100), upper axis

NEER

40

50

60

70

80

90

100

1971 1973 1975 1977 1979 198140

50

60

70

80

90

1002005 2007 2009

LCU vs USD

60

70

80

90

100

110

120

1971 1973 1975 1977 1979 198160

70

80

90

100

110

1202005 2007 2009

Germany (Aug 1971=100)Japan (Aug 1971=100)China (July 2005=100), upper axis

CPI relative to competitors

Source: BIS.

35

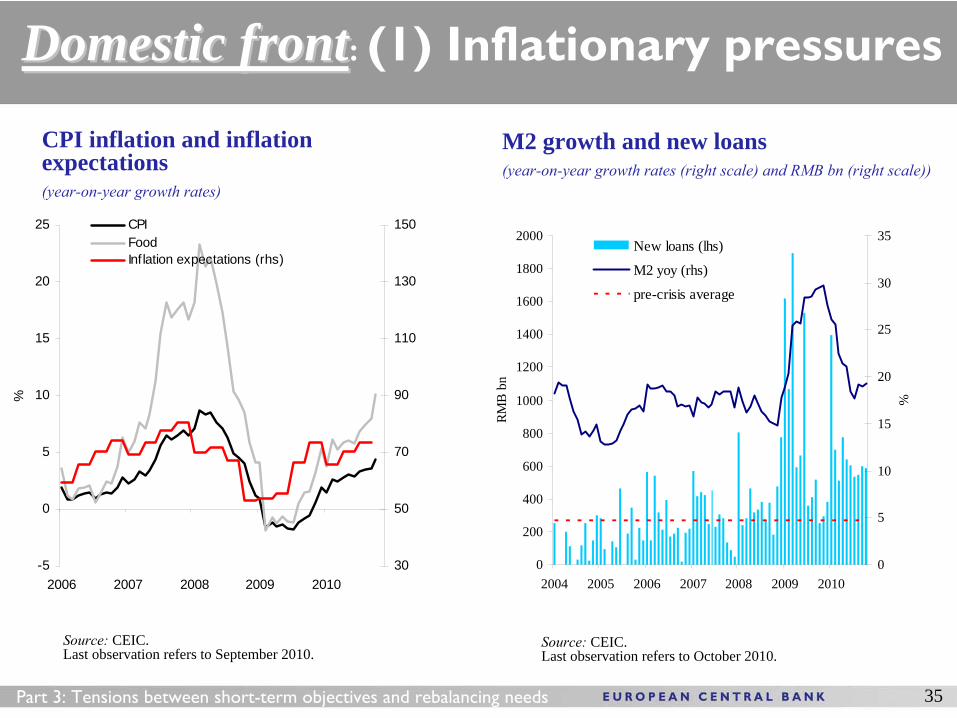

Domestic frontDomestic front: (1) Inflationary pressures

Part 3: Tensions between short-term objectives and rebalancing needs

CPI inflation and inflation expectations(year-on-year growth rates)

Source: CEIC.Last observation refers to September 2010.

Source: CEIC.Last observation refers to October 2010.

-5

0

5

10

15

20

25

2006 2007 2008 2009 2010

%

30

50

70

90

110

130

150CPIFoodInflation expectations (rhs)

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2004 2005 2006 2007 2008 2009 2010

RMB

bn

0

5

10

15

20

25

30

35

%

New loans (lhs)

M2 yoy (rhs)

pre-crisis average

M2 growth and new loans(year-on-year growth rates (right scale) and RMB bn

(right scale))

36

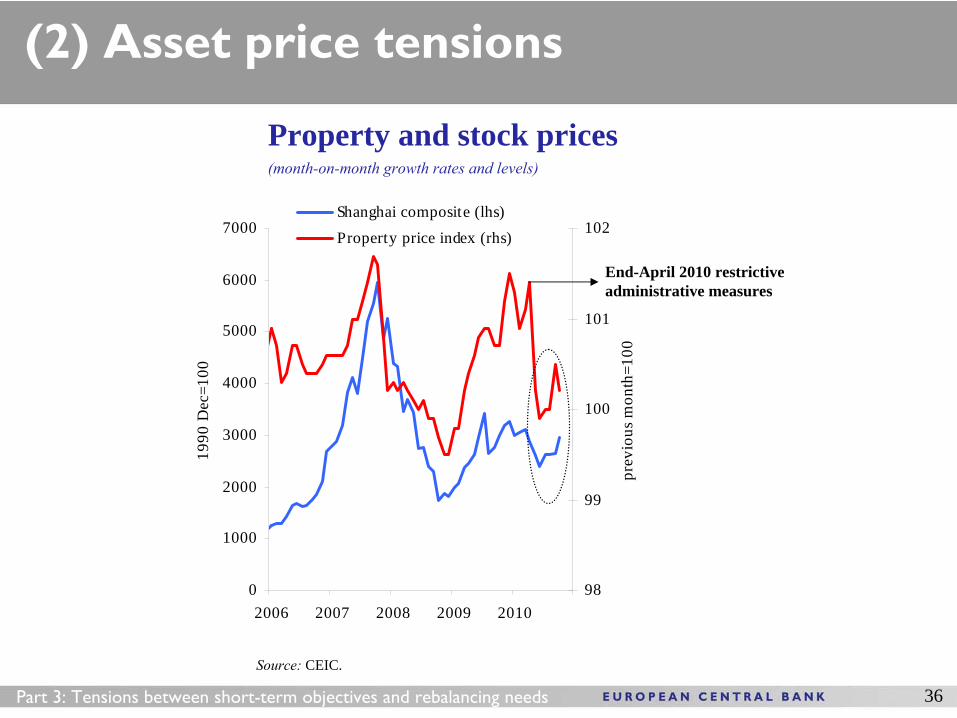

(2) Asset price tensions

Source: CEIC.

Part 3: Tensions between short-term objectives and rebalancing needs

0

1000

2000

3000

4000

5000

6000

7000

2006 2007 2008 2009 2010

1990

Dec

=100

98

99

100

101

102

prev

ious

mon

th=1

00

Shanghai composite (lhs)Property price index (rhs)

Property and stock prices(month-on-month growth rates and levels)

End-April 2010 restrictive administrative measures

37

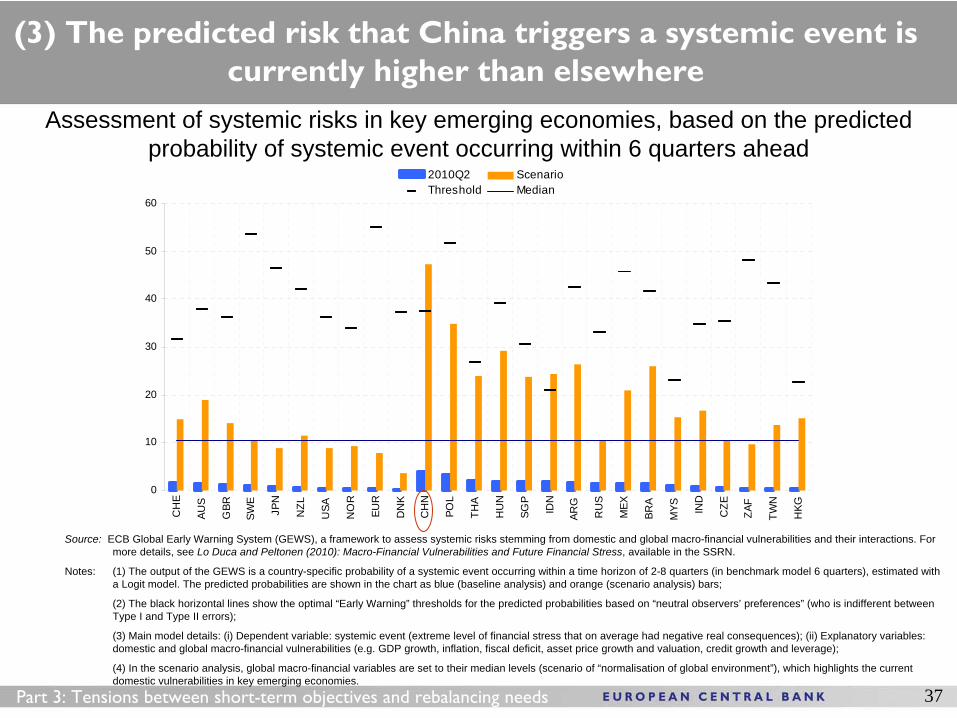

(3) The predicted risk that China triggers a systemic event is currently higher than elsewhere

Part 3: Tensions between short-term objectives and rebalancing needs

Assessment of systemic risks in key emerging economies, based on the predicted probability of systemic event occurring within 6 quarters ahead

0

10

20

30

40

50

60

CH

E

AUS

GBR

SWE

JPN

NZL

USA

NO

R

EUR

DN

K

CH

N

POL

THA

HU

N

SGP

IDN

ARG

RU

S

MEX

BRA

MYS IN

D

CZE

ZAF

TWN

HKG

2010Q2 ScenarioThreshold Median

Source: ECB Global Early Warning System (GEWS), a framework to assess systemic risks stemming from domestic and global macro-financial vulnerabilities and their interactions. For more details, see Lo Duca and Peltonen (2010): Macro-Financial Vulnerabilities and Future Financial Stress, available in the SSRN.

Notes: (1) The output of the GEWS is a country-specific probability of a systemic event occurring within a time horizon of 2-8 quarters (in benchmark model 6 quarters), estimated with a Logit model. The predicted probabilities are shown in the chart as blue (baseline analysis) and orange (scenario analysis) bars;

(2) The black horizontal lines show the optimal “Early Warning” thresholds for the predicted probabilities based on “neutral observers’ preferences” (who is indifferent between Type I and Type II errors);

(3) Main model details: (i) Dependent variable: systemic event (extreme level of financial stress that on average had negative real consequences); (ii) Explanatory variables: domestic and global macro-financial vulnerabilities (e.g. GDP growth, inflation, fiscal deficit, asset price growth and valuation, credit growth and leverage);

(4) In the scenario analysis, global macro-financial variables are set to their median levels (scenario of “normalisation of global environment”), which highlights the current domestic vulnerabilities in key emerging economies.

38

Source: CEIC.

Loans issued broken down by recipients (RMB trn)

(4) Will the surge in loans result in higher NPLs?

Official and “true” NPL ratios (% of total loans)

0

5

10

15

20

25

30

2002 2003 2004 2005 2006 2007 2008 2009 2013

% o

f tot

al lo

ans

'True' NPL ratio (AMCs adjusted)Official NPL ratioECB estimatesOfficial LGFV loss estimates

Source: ECB estimates based on CEIC and CBRC.

Official estimates

Part 3: Tensions between short-term objectives and rebalancing needs

3.6

4.9

6.3

9.6

0

2

4

6

8

10

2007 2008 2009 Jan-Sep 2010

HouseholdsOther loans in domestic currencyEnterprises: short term and bill financingEnterprises: long term

1. China’s model may not be sustainable going ahead

2. Reforms are needed to rebalance the economy. This is both in the domestic and global interest

3. Reforms agreed thus far might prove too gradual given the running out of long-term supporting factors; importance of upcoming 12th five-year plan

4. Multilateral cooperation (G20, IMF) can help set the right aligned incentives to rebalancing both in China and in its key global partners

CONCLUSIONS

39

Thanks!

Grazie!

Xiè xiè!