Opportunities for Chartered Accountants in International taxation

Page 1 of 36

THE CHARTERED INSTITUTE OF TAXATION OF NIGERIA

(Chartered Institute by Act No. 76 of 1992)

STUDENTS’ DELIGHT APRIL 2012 TAXATION

TECHNICIAN SCHEME EXAMINATION TTS II

QUESTION AND SUGGESTED SOLUTIONS

Page 2 of 36

THE CHARTERED INSTITUTE OF TAXATION OF NIGERIA

APRIL 2012: TAXATION TECHNICIAN SCHEME

PART 2: BUSINESS MANAGEMENT

ATTEMPT ALL QUESTIONS. TIME: 3 HOURS

1. a. One of the functions of management in an organization is control. Briefly discuss the three types of inventory in a manufacturing company on which management maintains effective

control. (12 marks)

b. Quality control is a common unit in a production oriented company. Enumerate the benefits of

quality control to a manufacturing company. (8 marks)

(20 marks)

Assessor’s Comment

There was no serious preparation by all candidates as shown in the poor mark obtained. It means the use

of syllabus is no longer relevant to do a serious preparation.

Solution to question 1:

1 a. The management of a manufacturing company will maintain effective control on the following items of inventory:

i. Raw Materials ii. Work – In – Progress iii. Finished Goods.

i. Raw Materials Stock: In order to take advantage of bulk – buying and also reduce the

wastage of materials needed for production, management will always install effective control

measures in the process of processing raw materials, storage and usage. It is important to note that

production process is continuous hence raw materials must always be available so that workers

can be kept busy at all times.

ii. Work – In – Progress: This is the buffer between production processes.

iii. Finished Goods Stock: Goods that are transferred from the production floor are

Page 3 of 36

normally documented while issuance from the warehouse is effectively monitored to ensure that

goods are normally available to meet customers‟ demands.

In all these types of inventory costs are always a concern to management.

b. The concept of quality depends on the perspective of those concerned. Quality control is an

important function in a product producing organization because it provides the following

benefits:

i. Reduction in cost occasioned by scraps or re-working.

ii. Reduction in complaints from customers.

iii. Enhances the reputation of the company.

iv. Provides a feedback to product designers and engineering staff about product

performance and the machines required to produce them.

2. a. What do you understand by the term Paperless Office? (5 marks)

b. Briefly identify three components of information technology. (5 marks)

c. The term telecommunication means communicating over a distance. State five means of

telecommunication. (5 marks)

d. Discuss the benefits derivable by a business organization from the use of email communication. (5 marks)

(20 marks)

Assessor’s Comment

Most of the students/candidates are not focused and lost steam. They answered questions as if they were

in lecture room. They have to realize that there is difference between lecture room and examinations.

This bow to unseriousness on the part of the students.

Solution to question 2:

2. a. A paperless office is an office driven by the use of electronic devices like computers,

telecommunication gadgets. It makes use of micro - electronic application for:

i. Data storage, retrieval and processing.

Page 4 of 36

ii. Industrial process control

iii. Electronic Funds Transfer

All these applications are integrated to avoid office routine activities

b. The three components of Information Technology are:

i. Computers

ii. Telecommunication

iii. The internet

c. Five means of telecommunication are:

i. Global system of Telecommunication /GSM

ii. Electronic –mail

iii. Radio phones

iv. Facsimile

d. Benefits derivable from e-mail communication

i. E-mails provide immediate exchange of information between the sender and the receiver.

ii. E-mails assist manpower in prompt decision making

iii. Documents can be sent as attachments through an e-mail.

iv. It can be used as tools for promoting business.

v. It provides a very cheap means of communicating.

vi. It is easy to use and simple to send to many people at the same time.

3. a. What do you understand by Market Research? (5 marks)

b. Outline the steps that a Research Officer would take in conducting a Marketing Research

(10 marks) c. Identify five roles of a Marketing Manager. (5 marks)

(20 marks)

Assessor’s Comment

Page 5 of 36

The performance was very poor. Candidates are not well prepared for the question. They cannot define

what is Market Research, the role of a Marketing Manager with the steps a research officer would take in

conducting Marketing Manager. They should watch out for such question in future.

Solution to question 3:

3. a. Market Research is any organized effort to gather information about markets or customers. It is a

very important component of business strategy.

Market Research which includes social and opinion research is the systematic gathering and

interpretation of information about individuals or organizations using techniques, statistical analytical

methods and techniques to gain insight or support decision making.

b. Steps to Marketing Research

Every company which hopes to compete in the market must consider conducting market research.

The following are the steps to take in Market Research.

i. Defining the problem

− Taking the product and service to the market.

− Find out how the product or service fits into the market place.

− Set the objectives of the research

ii. Developing the Research plan

− Identify the data that would be needed.

iii. Collect information

iv. The final report.

c. The Roles of a Marketing Manager

i. Research and reporting on external opportunities.

ii. Understand current and potential customers.

iii. Manage the customer journey (customer relationship management)

iv. Develop the market strategy for management

v. Ensure timely delivery of goods to customers.

vi. Assisting customers to remain focused in taking decision.

vii. Manage the marketing budget.

Page 6 of 36

4 a. Manpower planning is an essential part of a Human Resources Manager‟s work. Briefly state the

four major activities involved in Manpower Planning. (8 marks)

b. Job Satisfaction is aimed at productivity improvement through motivation.

What are the ways in which productivity can be enhanced in an organization? (6 marks)

c. Briefly discuss the followings:

i. Authority ii. Responsibility iii. Delegation (6 marks)

(20 marks)

Assessor’s Comment

This is generally a below average performance by all candidates. Majority of the candidates did not go

straight to the points relevant to the questions asked and answers given were mostly guessed and

irrelevant.

Solution to question 4:

4. a. The four major activities in Human Resources Planning (Manpower Planning) are:

i. Analyzing the existing common resources situation

ii. Forecasting future demands for people

iii. Assessing the external labour market and forecasting the supply situations.

iv. Establishing and implementing human resources plans.

b. Ways of Productivity Enhancement

1. Effective delegation of authority.

2. Assigning responsibility

3. Job enrichment

4. Efficient reward system

5. Improved consultation between management and staff.

Page 7 of 36

6. Job Enlargement

c i. Authority is the right conferred on some members of an organization to act in a certain way over

others. Authority is rarely as arbitrary. Authority can be regarded as a defined amount of power

granted by an organization to selected members. etc.

ii. Responsibility is a concept that refers to the legitimate expectation of a level of performance that

a senior person has over his or her subordinates or team members. Another word for

responsibility is accountability which in some respects is a more helpful term since it implies that

one person is accountable to another on a given task.

iii. Delegation is essentially a power sharing process in which individual managers transfer part of

their legitimate authority to subordinate/team members but without passing on ultimate

responsibility for the completion of the overall task which has been entrusted to them by their

superiors.

5 a. Identify the relevant tax authority for the collection of the followings taxes: i. Property Tax

ii. Partnership Tax iii. Value Added Tax iv. Petroleum Profit Tax

v. Education Tax (10 marks) b. What is Tax Avoidance? (5 marks)

c. How can a taxing authority minimize the incidence of Tax Avoidance? (5 marks)

(Total: 20 marks)

Assessor’s Comment

I am not impressed with the candidates‟ way of answering questions. They always mix up the questions.

For example question (5) contains a, b, c, d, e, property tax, partnership tax, value added tax. They could

not differentiate the answers.

Solution to question 5:

5. a. Relevant taxing authority for the followings:

Page 8 of 36

i. Property Tax - State Internal Revenue Board

ii. Partnership Income - State Internal Revenue Board

iii. Value Added Tax - Federal Inland Revenue Service

iv. Petroleum Profit Tax - Federal Inland Revenue Service

v. Education Tax - Federal Inland Revenue Service

b. Tax Avoidance: This arises in situation where the tax payer arranges his financial affairs in

a form that would make him pay least possible amount of tax

c. A taxing authority will minimise the incidence of tax avoidance through the following ways:

i. Carrying out prompt examination of self -assessment returns.

ii. Sending tax queries to tax payers as soon as desk examination of returns has been

concluded.

iii. Carrying out back duty audit from time to time.

Page 9 of 36

THE CHARTERED INSTITUTE OF TAXATION OF NIGERIA

APRIL 2012: TAXATION TECHNICIANS SCHEME PART 2: BUSINESS TAXATION

ATTEMPT ALL QUESTIONS. SHOW ALL WORKINGS TIME: 3 HOURS

1. Mr Owolowo established Tilapia Fisheries Limited in 2000 for the purpose of commercial fish

production. The company commenced business on 1st January 2001. Its accounting date is 31st

December each year while its adjusted profits for the first ten years are the following:

Trading Period Adjusted

Profits/(Losses) ₦ Year ended 31/12/2001 (100,000)

Year ended 31/12/2002 30,000 Year ended 31/12/2003 25,000

Year ended 31/12/2004 20,000 Year ended 31/12/2005 15,000 Year ended 31/12/2006 35,000

Year ended 31/12/2007 50,000 Year ended 31/12/2008 (40,000)

Year ended 31/12/2009 35,000 Year ended 31/12/2010 30,000

You are required to compute the assessable profits for the relevant years of assessment.

(Total: 20 Marks)

Assessor’s Comment

The questions were very okay at this level of examination, but the students lack the knowledge of basis

period in determining the relevant Assessable period for relevant years. Also, the students were not fully

prepared for the examination which led to bad failure in that particular paper.

Solution to question 1:

1.

TILAPIA FISHERIES LIMITED

YOA BASIS PERIOD ASSESSABLE ASSESSABLE PROFITS

2001 (1/1/2001 – 31/12/2001) – Actual Loss for year

ended 31/12/2001

(100,000)

NIL

Page 10 of 36

Loss c/f to 2002

(100,000)

2002 1st 12 Months – 1/1/2001 – 31/12/2001

Loss b/f from 2001 Loss c/f to 2003 restricted to actual loss sustained

(100,000)

(100,000) (100,000)

NIL

2003 Preceding year basis (1/1/2002 – 31/12/2002) Profit for year ended 31/12/2002

Loss b/f from 2002 Loss c/f to 2004

30,000

(100,000) (70,000)

NIL

2004 Preceding year basis (1/1/2003 – 31/12/2003)

Profit for year ended 31/12/2003 Loss b/f from 2003 Loss c/f to 2005

25,000 (70,000) (45,000)

NIL

2005 Preceding year basis Profit for year ended 31/12/2004 Loss b/f from 2004

Loss c/f to 2006

20,000 (45,000)

(25,000)

NIL

2006 Preceding year basis Profit for year ended 31/12/2005

Loss b/f from 2005 Loss c/f to 2007

15,000

(25,000) (10,000)

NIL

2007 Preceding year basis Profit for year ended 31/12/2006

Loss b/f from 2006

35,000

(10,000)

25,000

2008 Preceding year basis Profit for year ended 31/12/2007

50,000

50,000

2009 Preceding year basis

Loss for year ended 31/12/2008 Loss c/f to 2010

(40,000) (40,000)

NIL

2010 Preceding year basis

Profit for year ended 31/12/2009 Loss b/f from 2009 Loss c/f to 2011

35,000 (40,000) (5,000)

NIL

2011 Preceding year basis

Profit for year ended 31/12/2010 Loss b/f from 2010

30,000 (5,000)

25,000

Note

Since Tilapia Fisheries Limited is engaged in Commercial Fish Production, it qualifies to be regarded as

an Agro-Allied Business, and losses incurred by an Agro-Allied Business can be carried forward

indefinitely, that is, not restricted to four years.

2. Aanu John & Co. makes up accounts to 30th September every year acquired the following assets:

Page 11 of 36

₦ 1/11/2008 Plant 2,500,000

4/2/2009 Motor Vehicle 800,000 21/7/2009 Non-Industrial Building 5,000,000

The following additions were made during the year ending 30th September 2010.

₦

Plant 1,500,000 Motor Vehicle 1,000,000 Non-industrial Building 500,000

You are required to compute the Capital Allowances for the relevant years of assessment.

(Total: 20 Marks)

Assessor’s Comment

The question tests the computation of Capital Allowances for the relevant years for existing assets and

additions during the specific years.

Candidate performance was poor.

Candidate did not understand how to determine the capital allowances due.

This topic should be studied in depth because of its importance in Tax Computation.

Solution to question 2:

2.

AANU JOHN & CO. CAPITAL ALLOWANCE COMPUTATION

RATES PLANTS MOTOR

VEHICLES

NON-

INDUSTRIAL BUILDING

ALLOWA

NCE

I.A 50% 50% 15%

A.A 25% 25% 10%

₦ ₦ ₦ ₦

2010 Year of Assessment Cost 2,500,000 800,000 5,000,000

I.A. (1,250,00

0)

(400,000) (750, 000) 2,400, 000

A.A. (W1) (312,500) (100,000) (425,000) 837,500

TWDV 937,500 300,000 3,825,000 323,750

2011 Year of Assessment Additions

1,500,000 1,000,000 500,000 3,561,250

Page 12 of 36

2,437,500 1,300,000 4,325,000

I.A. (750,000) (500,000) (75,000) 1,325,000

A.A.(W2) (500,000) (225,000) (467,500) 1,192,500

TWDV 1,187,500 575,000 3,782,500 2,517,500

2012 Year of Assessment A.A.

(500,000) (225,000) (467,500) 1,192,500

687,500 350,000 3,315,000

Workings

Calculation of Initial and Annual Allowances

With effect from 1985 Year of Assessment, Annual Allowances were computed on a straight line basis as

follows:

W1 Plant Cost = ₦250,000

I.A. = 50% X ₦250,000

=₦125,000

A.A. = Cost – I.A. = 250,000 – 125,000 = ₦31,250 Useful life 4

Since the A.A. is 25%, then the useful life of the asset must be 4 years.

Motor Vehicle Cost = ₦80, 0000 I.A. = 50% X ₦80, 0000

= ₦40, 0000

A.A. = Cost – I.A. = 80, 0000– 40, 0000 = ₦10,000 Useful life 4

Since the A.A. is 25%, then the useful life of the asset must be 4 years.

Non-industrial Building Cost = ₦500,000

I.A. = 15% of ₦500, 0000 = ₦75,000

A.A. = Cost – I.A. = 500, 0000 – 75, 0000 = ₦42, 5000 Useful life 10

(W2) Plant Cost = 150, 0000

I.A. = 50% of ₦150, 0000 = ₦75, 0000

Page 13 of 36

A.A. = 150,000 – 75, 0000 = ₦18, 7500 4

Motor vehicle cost = ₦100, 0000 I.A. = 50% X ₦100, 0000 = ₦50, 0000

A.A. = 100, 0000 – 50, 0000 = ₦50, 0000 4 4 = ₦12, 5000.

Non-industrial Building Cost = ₦50,000

I.A. = 15% X ₦50,000 = ₦7,500

A.A. = ₦50, 0000 – 7, 5000 = ₦42, 5000 10 10 = ₦4, 2500.

3. a. In relation to the assessment procedures in Nigerian Taxation Administration, discuss the

following:

i. Types of assessment available to companies

ii. Time limit within which tax is to be paid

iii. Terms of payment

iv. Penalty for late pay (8 marks)

b. The Self-assessment system was introduced with effect from 1st January 1996 to run parallel

and in conjunction with the existing government assessment for both individual and corporate

tax payers.

How does it operate and what are the benefits? (6 marks)

c. In compliance with the provision of the Act, discuss the following with respect to filing of tax

returns by companies:

i. Content

ii. Timing

iii. Failure and Penalty (6 marks)

(Total: 20 Marks)

Assessor’s Comment

The question tests various topics viz:

Page 14 of 36

(a) Types of Assessment

(b) Self-Assessment

(c) Filing of Tax Returns.

About 40% of the students performed fairly, however, about 60% performed poorly.

The major pitfall is that some candidates could not remember these basic topics, hence were short of what

to write.

Candidates should not neglect any part of the syllabus, a thorough study of all areas is strongly

recommended.

Solution to question 3:

3. a. (i) Types of Assessment - Provisional Tax Assessment: This is a tax of an amount equal to what was paid in the

preceding year. (2/3 Mark) - Assessed Tax by Government: A Company‟s tax liability for the year is conveyed through

a notice of assessment in case of the existing government assessment(that is BOJ

assessment) (2/3 Mark)

- Self-Assessment System : This tax is assessed by the tax payers themselves

ii. Time of payment

- Provisional Tax – it must be paid before the end of March of any given year. It is due from

Corporate Tax payers within three months of each year of assessment

- Government Assessment: Is payable within two months from the date on the notice , and

the tax liability is after the payment of Provisional Tax credit for withholding taxes and

possible adjustments for overpayments.

- Self- Assessment system: same applies as for government assessment. Disputed

Assessment must be settled within one month from the date of Amended Assessment

Notice.

iii. Terms of Payment

Provisional or Government Assessment tax is payable in one lump sum. However, a tax

payer has the right of taxes under provisional, government and self- assessed tax.

Page 15 of 36

This arrangement is subject to Revenue Authority‟s approval and will be granted in cases

where there are reasonable grounds to believe that all avenues to obtain necessary funds to

pay the tax have been exhausted.

iv. Penalty for Rate payment

Failure to comply with the payment timetable will attract a penalty (1 Mark) at

Commercial rate of interest. The penalty (1 Mark) is in addition to the tax in default.

3b. OPERATION OF SELF ASSESSMENT SYSTEM

With effect from 1996 year of assessment, all companies with turnover of one million

naira and above must file their returns under self-assessment scheme. The choice of a

company within this turnover (2 Marks) range to file its return under government of Self-

assessment scheme has been removed.

Companies in this category should file their returns within 6 months of the accounting year-

end (1 Mark). Incentives enjoyed by companies under self- assessment scheme include:

- 1% tax rebate

- The right to pay current tax on instalmental basis will be granted – 6 equal monthly

instalments

- Provisional Tax will not be paid

Small Companies with turnover below 1 million naira are given 2 years (from 1996 year of

assessment) of grace during which period they have a choice, but thereafter, no more choice they

will be expected to file their returns under self-assessment.

3c. FILING OF TAX RETURNS BY COMPANIES

Every Company is required to file a tax return in a prescribed form with the Federal Inland

Revenue Service once every fiscal year.

(i) Content – The tax returns for the tax payers include the following:

- Completed tax IR3C, which is a declaration of income and other relevant information by

the tax payer.

- The audited accounts of the business for the relevant year of assessment which must

meet the statutory requirements of the Companies and Allied Matters Decree 1990. The

Statement of Accounting Standards issued by NASB and other relevant Acts/Decrees

governing the operation of that particular line of trade.

The Capital allowance computations and tax liability.

Page 16 of 36

(ii) Timing: Tax returns must be filed with the appropriate Area Office of the Revenue

Authority;

- Within 3 months of every year of assessment, failing which provisional tax becomes

applicable, especially for tax payers who are not filing self-assessment returns.

- Not later than six months after the close of the companies‟ accounting year, for all

corporate tax payers, including those that becomes liable to provisional tax.

- In the case of newly incorporated company, within 18 months from the date of

commencement of business.

(iii) Failure and Penalty: It is a serious offence for a tax payer not to file tax return

annually under the Nigerian tax laws.

- Besides viewing the failure when discovered, as a serious case of tax fraud and

evasion, the board will determine the appropriate assessment for all years on its best of

judgement (BOJ) and penalize the offender severely in accordance with the tax laws.

- A company which fails to file tax return is liable to a penalty of ₦2,500 for the first

month and ₦5,000 for every additional month of default.

- The previous concession of waiving this penalty by the Authorities on the grounds of

special appeals will be exercised only in special cases by the Chairman FIRS.

- Pre-operational levy: Every company which is yet to commence business is liable

to a pre-operational levy of ₦25,000 for the first year and ₦20,000 for every subsequent

year such company comes forward to obtain Tax Clearance Certificate on the grounds

that it has not commenced business.

4. a. What do you understand by the term Capital Allowances? (4 marks)

b. List five categories of Capital expenditure that qualify for grant of Capital Allowances.

(3 marks)

c. Enumerate the various categories of fixed assets classified as Industrial Building or Structure

for Capital allowances purposes as contained in Companies Income Tax Act, 2004.

(3 marks)

d. Jungle Nigeria Limited has been in business for several years making up account to 31st March each

year. For the year ended 31st March, 2009 the company failed to file annual tax returns and a best of

judgement assessment was raised as follows:

N Turnover 36,000,000 Assessable Profit 7,800,000 Income tax at 30% 2,340,000 Education Tax at 2% 156,000

Page 17 of 36

As the Company‟s Tax Consultant, you were informed that during the year the company

acquired assets worth 2.6 million on which Capital Allowance should be granted. You are

required to advise the company on what to do, particularly on the failure to grant Capital

allowances? (10 marks)

(Total: 20 Marks)

Assessor’s Comment

Part c of this question (industrial buildings) was a major challenge for the candidates. There was a

general display of lack of knowledge in this area. Also, the candidates did not know that the advice to

Jungle Nigeria Limited should be communicated in the form of a letter properly addressed to the

Managing Director.

Solution to question 4:

4. (a) Capital Allowance is a form of relief that is granted to any person who incurred

qualifying capital expenditure during a basic period in respect of assets in use for the

purpose of a trade or business at the end of the basis period.

The term Capital allowances covers initial, annual, investment and balancing

allowance.

- Initial allowance is a relief that is granted in the year assessment in the basic period of

which the qualifying capital expenditure was incurred.

- It is granted in full irrespective of when the asset was acquired.

- Annual allowance on the other hand is granted every year on the residue of

expenditure of an asset until fully written off.

- Balancing allowance is the excess of TWDV over and above the sale proceeds on

eventual disposal of an asset.

- Investment allowance: is an additional allowance which is granted on plant and

equipment used for a business at the rate of 10% of the cost Investment allowance is

also available to businesses located in areas that are more than 20km away from normal

facilities such as: electricity, tarred road, pipe borne water and telephone.

(b) Categories of qualifying Capital Expenditure.

Five (5) categories of Capital expenditure that qualify for granting of capital

allowance are as follows:

- Qualifying industrial and non- industrial building expenditure

- Qualifying mining expenditure

- Qualifying plant expenditure

- Qualifying furniture and fittings expenditure

- Qualifying Motor vehicle expenditure

Page 18 of 36

(c) Industrial Building: An industrial building or structure as categorised under

paragraph 5 of schedule 2 of CITA 1979 as amended is any building or structure in

regular use.

(i) as a mill, factory, mechanical workshop or other similar building or as a structure

used in connection with any such buildings.

(ii) as a dock, port, wharf, pies, jetty or other similar building structure.

(iii) for the operation of a railway for public use of water or electricity undertaking

for the supply of water or electricity for public consumption.

4d. The Managing Director

Jega Limited APO Avenue

Tundunwada Abuja.

Dear Sir,

RE: BEST OF JUDGEMENT ASSESSMENT

We refer to your letter on the above subject matter and like to comment and

advice on the best of judgement assessment raised by the Federal Inland

Revenue Services as follows:

(a) All companies are required to file tax returns at the tax office within

six months after the year end. The returns should include the

following information:

- The audited financial statements

- The computation of Capital Allowance

- The computation of Income and Education taxes

- Claim for capital allowances and schedule of assets

acquisition and disposal during the year

- Properly completed Self-assessment form and evidence of

payment of the tax.

(b) Failure to file the tax returns gives the tax authority the right to assess the

company on best of judgement basis.

(c) Since Capital allowance is not granted automatically, that is, a claim must

be made by the company, it is usually not considered when raising best of

judgement assessment.

(d) The company is advised to immediately file the tax returns without further

delay so as to have a basis of objection to the best of judgement

assessment raised.

Page 19 of 36

(e) A notice of objection to the BOJ assessment must be made within 30 days

of the date of services of the notice of assessment otherwise, the

assessment shall become final and conclusive. Failure to pay will attract

penalty at 10% and interest rate at the ruling rate.

In conclusion, if you require further explanation or clarification on the

above, please contact the undersigned

Thank you and best regards.

Yours faithfully,

OMA Global Consultants

5. Write short notes on the following:

a. The Composition of the Federal Inland Revenue Service Board. (5 marks)

b. Capital Allowance as it relates to second hand building. (3 marks)

c. Duties of the Joint Tax Board. (6 marks)

d. Power of Distrain by the Tax authority. (6 Marks)

(Total:20 Marks)

Assessor’s Comment

The question is okay, but the students misunderstood the composition of Federal Inland Revenue Board

to Federal Inland Revenue Service, while capital allowance on second hand building was not understood

by the students. Also, the power of detrain by the Tax Authority was not understood by the students.

Solution to question 5:

5. (a) Federal Inland Revenue Service (Establishment) Act, 2007, Section 3(1) established the

Federal Inland Revenue Service Board and composed as follows:

(i) An Executive Chairman ,who shall be experienced in taxation matters, appointed by the

President and subject to the confirmation of Senate

(ii) Six members with relevant qualifications and expertise who shall be appointed by the

President to represent each of the six geo-political zones

(iii) A representative of the Attorney-General of the Federation

(iv) The Governor of the CBN or his representative

(v) A representative of the Minister of Finance not below the rank of a Director

(vi) The Chairman of the Revenue Mobilization Allocation and Fiscal Commission or his

representative who shall be any of the Commissioners representing the 36 State of the

Federation

Page 20 of 36

(vii)The Group Managing Director of NNPC or his representative who shall not be below the

rank of a Group Executive Director of the Corporation or its equivalent

(viii) The Comptroller-General of the Nigerian Custom Service or his representative not

below the rank of Deputy Comptroller-General

(ix) The Registrar-General of CAC or his representative not below the rank of a Director; and

(x) The Chief Executive Officer of the National Planning Commission or his representative not

below the rank of a Director.

. 5(b) Capital Allowance as it relates to second hand building.

(i) Where a building is acquired second-hand, both initial and annual allowances may be claimed on such a building if the original owner did not previously use it for business.

(ii) On the other hand, if the original owner has used it for business and has hence claimed Capital allowance on it, no initial allowance may be claimed. The annual allowance to be claimed must be based on the lower of the original cost and the new purchase price.

5(c) Duties of Joint Tax Board

(i) This body is more or less a platform that allows the Federal and the State tax authorities to meet. Essentially, it can be posited that the Joint Tax Board is an avenue that ensures uniformity in the taxation law and practice in Nigeria.

(ii) Exercising the powers and duties conferred on it by the express provisions of the law (Decree) and any other powers and duties arising from the law which may be agreed by the

Government of each of the territories exercised by the Board. (iii)Exercising powers and perform duties conferred on it by any enactment of the Federal

Government imposing tax on the income and profits of companies

(iv) Advising the Federal Government on request, in respect of double taxation arrangement concluded or under consideration with any other country, and in respect of rates of Capital

allowances and other taxation matters having effect throughout Nigeria. (v) Using its best endeavour to promote uniformity both in the application of the decree and in the

incidence of tax on individuals throughout Nigeria.

(vi) Imposing its decisions on matters of procedures and interpretation of this decree on any state for the purposes of conforming to agreed procedure or interpretation.

5 (d) Power to Distrian by the Tax Authority.

(i) Where an assessment has become final and conclusive, and a demand note has been served on the

tax payer, then if payment is not effected within the time given by the demand note, the tax authority may in the prescribed form, for the purpose of enforcing payment of the tax due

distrain the tax payer by his goods or other chattels, bonds or securities, land, premises or places owned by the tax payers.

(ii) For the purpose of levying any distress, an officer of the tax authority, authorised in writing may

execute any warrant or distress and if necessary break open any building or place in the day time for the purpose of levying the distress and he may call for his assistance any police

officer and it shall be the duty of that police officer when so required to aid and assist in the execution of the warrant of distress and in levying the distress.

Page 21 of 36

(iii)The goods distrained upon will be kept for 14 days at a cost to the tax payer after which the items may be sold. Out of the proceeds of sale, the cost or charges of and incidental expenses to the

sale and keeping of the distress and disposal will be settled, next the tax due will be settled while the balance, if any shall be payable to the tax payer upon demand being made by him or

on his behalf within one year of the date of sale.

THE CHARTERED INSTITUTE OF TAXATION OF NIGERIA APRIL 2012: TAXATION TECHNICIANS SCHEME

PART 2: MANGEMENT INFORMATION SYSTEM ATTEMPT ALL QUESTIONS. TIME: 3 HOURS

1. As an information technology student who has acquired considerable knowledge of the subject,

discuss the following :

i. e- tax card

ii. ALU

iii. Flash Disk

iv. ROM

v. Data base (Total: 20 marks)

Solution to question 1:

1 i. e-tax Card- A computer plastic card containing tax holder information that can be read

Page 22 of 36

by a card reader and display on the system.

ii. ALU- Stands for arithmetic and logic unit and is a part of the CPU of the computer where

all processing in the system take place.

iii. Flash Disc- A mobile, small auxiliary storage device used to store data, programmes and

other files. Usually use USB ports for connection to the computer.

iv. Rom- Rom stands for Read Only Memory, which means Information stored in it can only

be read and not modified. It is a type of computer memory

vi. Database- An organized collection of data. Data base may be network, mechanical, or

relational. Relational data bases are more popular. Example includes, Microsoft Access,

Oracle etc.

2. a. How would you define a system under the general systems theory? (2 marks)

b. What are the three components of general systems theory? (3 marks)

c. What do you understand by „Open‟ and „closed‟ system? (5 marks)

d. Explain five systems that are classified by behaviour. (10 marks)

(Total: 20 marks)

Solution to question 2:

2. a.

A system is an organized method for accomplishing a business functions or task.

A system is combination of interrelated elements or sub-systems organized in such a way

to ensure the efficient functioning of the system as a whole, necessitating a high degree of

co-ordination with the sub-systems each of which is designed to achieve a specified

purpose e.g. business organization.

A system consists of components or parts which possess the following elements:

b. Inputs, process, outputs, control, feedback and constraints or limitations.

General Systems Theory and long term planning

General Systems Theory and policy making

General Systems Theory and principles of management.

c.

An open system is a system connected to and interacting with its environment. It takes in

energy or influences from its environment and also influences this environment by its

behavior.

Page 23 of 36

A closed system is a system which is isolated from its environment and independent of it,

so that no environmental influence affects the behavior of the system.

d.

Planning System: This is a system that plans for the operations of other systems e.g.

budget unit

Mechanistic or Organic system: This is a system that is very rigid in structure. It observes

standard rules and regulations e.g. machines

Deterministic system: This is a system that possesses no difference in behavior. Output

from the system can be predicted without error based on an input.

Probabilistic system: This is a system that operates on chances from the internal and

external environment. Output from the system may be 0 or 1, positive or negative, good or

bad. They are stochastic in nature.

Adaptive or Self Organising System: This is a system that adapts to a changing

environment by adjusting itself on a self-organizing basis. The system changes as a result

of measuring its output e.g. animals, human beings.

3. a. State the rules used for naming files in DOS/Windows. (5 marks)

b. Write short notes on index files, sequential files and direct access files. (9 marks)

c. Give the advantages and disadvantages of each of the files in (b) above. (6 marks)

(Total: 20 marks)

Solution to question 3:

3. (a)

It must not use special characters such as,

Can be a mixture of characters, numerals

It is made up of two parts: first part is the file name and second part associates it to an

application.

In DOS the maximum length of the filename is 8 characters and in WINDOWS 128

characters

(b) Index files: A file which stores keys and an index into another file. The inde x file may

have additional structure. An index file is helpful if record are large; the keys and indexes can be

extracted, sorted, and the original file accessed faster than the original file could be re-arranged

into sorted order. Also if the file needs to be accessed by different keys at the same time, it cannot

be sorted by all of them. An index file is maintained for each different key.

Page 24 of 36

Sequential file: it contains records written in a defined sequence according to the record

keys.

Direct access files: These are file which provide fast and efficient direct access. These

files can be accessed without accessing physically previous files stored on a device. They

are normally random file with one of a number of appropriate addressing methods.

(c) Index files:

Reduces time to locate a file.

Information can be obtained without accessing the main file

Each changes to the index requires a recompilation of the index file

Requires additional space when accessing the files.

Sequential file:

Ability to access the “next” record quickly

Simplicity of design

Useful for sorting and searching large volumes

Performance becomes bad when file searched for is not “next” record

Retrieval may be low

Transaction must be sorted in a particular sequence

Direct access files:

Mapping is very simple to implement

No processing time is required to determine the records location on a device

User must know how the records are stored physically

It is device dependent

Reorganization means new addresses thus it is address-space dependent

4. a. Draw and state the functions of five program flowchart symbols. (10 marks)

b. Draw a program flowchart to calculate the total daily sales of a salesman who sold 200 items.

(10 marks) (Total: 20 marks)

Solution to question 4:

4. 13 (a)

Symbol Name Function

Page 25 of 36

Terminator Used to START, or STOP, or to INTERRUPT a procedure

Process To show the process of calculation

Input/output

To READ a file or WRITE a record

Decision box To choose between two options

Connector To show the continuation of a flow chart

(b)

READ SALES

TOTAL=TOTAL + SALES

COUNT = COUNT + 1

IS

COUNT

= 200?

START

TOTAL= 0

COUNT = 0

Page 26 of 36

5. a. Describe in brief, the generation of computers. (10 marks)

b. Differentiate between the following types of direct input methods

i. OCR

ii. OMR

iii. MICR

iv. Bar codes (10 marks)

(Total: 20 marks)

Solution to question 5:

5. (a)

Zeroth Generation- Mechanical Computers (1642 – 1945): A calculating machine was

built by Blaise Pascal that could only add and subtract. Baron Gottfried Wilhelm built a

machine that could add, subtract, multiply, and divide. Then Charles Babbage attempted

to mechanize sequences of calculations, eliminating the operator and designing a machine

that would perform all the necessary operations in a predetermined sequence. He built the

difference engine and designed the analytical engine.

First Generation – Vacuum Tubes(1945-1955): In 1943 S. P. Eckert and J.W. Mauchly, of

the Moore school of Engineering of the University of Pennsylvania, started the Eniac,

PRINT TOTAL

STOP

Page 27 of 36

which used electric components (primarily vacuum tubes) and therefore faster, but which

also used switches and a wired plug board to implement the programming of operations.

Later Eckert Mauchly built the Edvac, which has its program stored in the computer

memory, not depending on external sequencing. This was an important innovation, and a

computer that stores its list of operations, or program, internally is called a stored –

program computer.

Second Generation- Transistors (1955-1965): Quite a few vacuum-tube electronic

computers were available and in use by the late 1950s, but an important innovation in

electronics appeared –the transistor. The replacement of large, expensive (hot) vacuum

tubes with small, inexpensive, reliable, comparatively low heat-dissipating transistors led

to what are called second generation computers. The size and importance of the computer

industry grew at amazing rates, while the costs of individual‟s computers drops

substantially.

Third Generation: - Integrated Circuits (1965-1980): by 1965 a third generation of

computer was introduced. The IBM corporation, in introducing the 360 series, used the

term third generation as a key phrase in their advertising, and it remains a catchword in

describing all machines of this era. The machines of this period began making heavy use

of integrated circuit in which many transistors and other components are fabricated and

packaged together in a single container. The low prices and high parking densities of this

circuits plus lessons learned from previous machines led to some differences in computer

system design, and these machines proliferated and expanded the computer industry to its

present multibillion-dollar size.

Fourth Generation:- personal computers and VLSI (1980-?): The manufacture of

integrated circuits has become so advanced as to incorporate hundreds of thousands of

active components in volumes of fraction of an inch, leading to what is called large scale-

integration (LSI) and very large scale integration (VLSI). This has led to small- size,

lower cost, large memory, ultra- fast computers called personal computers.

b.

OCR (Optical Character Reader): OCR devises can read printed or typed characters

directly into a computer system by recognizing the shape of different characters. They

work by scanning the text and measuring the amount of light reflected from each

character.

OMR (Optical Mark Reader): this technics is used when information is given as marks on

paper such as those in questionnaires and multiple choice tests. Some OMR device rely on

the conductivity of graphite to recognize a mark, thus marks are made in pencil. Other

Page 28 of 36

works by recognizing the amount of light reflected from the surface of the surface and can

thus accept marks made by pen as well as pencil.

MICR (Magnetic Ink Character Readers): These devices can read characters which are

printed in special typeface and with a special magnetic ink. They work by recognizing the

magnetic pattern produced by each character. The codes across the bottoms of cheque are

printed in magnetic ink and it is expensive.

Bar codes: The bar code consists of a number of vertical black stripes on a white

background. Special bar code readers in the form of light pens are able to interpret the

stripes and convert them into character codes. Bar codes provides a relatively cheap and

reliable method of capturing data.

THE CHARTERED INSTITUTE OF TAXATION OF NIGERIA APRIL 2012: TAXATION TECHNICIANS SCHEME

PART 2: PERSONAL TAXATION ATTEMPT ALL QUESTIONS. SHOW ALL WORKINGS TIME: 3 HOURS

1. a) What is balancing allowance as it relates to capital allowance? (3 marks)

b) The following data relate to Sadiq Enterprises for three years of assessment

2008 2009 2010

N N N

Adjusted profit 1,287,500 7,141,000 8,648,000 Capital allowances 4,337,500 4,337,500 4,337,500

Loss brought forward 3,471,000 - - Balancing allowance 271,000 - - Balancing charge 1,624,500 - -

Required: Compute the chargeable income of the business for the relevant years of

assessment (17 marks)

(Total: 20 marks)

Solution to question 1:

1 a. Balancing allowance is the excess of tax written down value over and above the sale proceeds

on disposal of fixed asset which had enjoyed Capital Allowance. The implication of

Page 29 of 36

balancing allowance is that the total capital allowances already granted to the taxpayer is less

than the value of fixed asset used up in the production of income for the taxpayer.

b. SADIQ ENTERPRISE

COMPUTATION OF CHARGEABLE INCOME FOR 2008, 2009 AND 2010 YEARS OF

ASSESSMENT.

2008 Year of Assessment N N

Assessable Profit 1,287,500

Balancing Charge 1,624,500

2,912,000

Loss Brought Forward 3,471,000

Loss Absorbed 1,287,500 (1,287,500)

Loss Carried Forward 2,183,500

Chargeable Profit (1,624,500)

Capital Allowance 4,337,500

Balancing Allowance 271,000

Capital Allowance c/fwd 4,608,500

2009 Year of Assessment N N

Assessable Profit 7,141,000

Loss Brought Forward 2,183,500

Loss Absorbed 2,183,500 (2,183,500)

4,957,500

Capital Allowance b/fwd 4,608,500

Capital Allowance for the

year

4,337,500

8,946,000

Capital Allowance Utilized 4,957,500 (4,957,500)

Chargeable Profit NIL

2010 Year of Assessment N N

Assessable Profit 8,648,000

Capital Allowance b/fwd 3,988,500

Capital Allowance for the

year

4,337,500

8,326,000

Capital Allowance Utilized (8,326,000)

322,000

Page 30 of 36

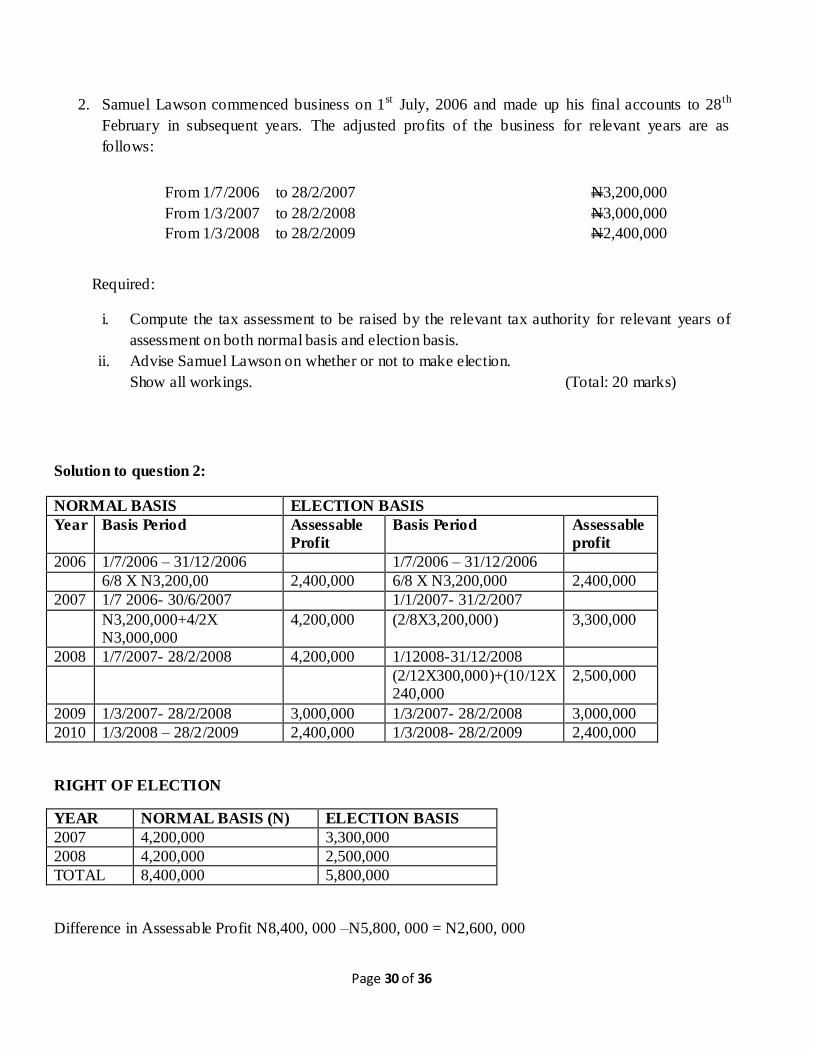

2. Samuel Lawson commenced business on 1st July, 2006 and made up his final accounts to 28th

February in subsequent years. The adjusted profits of the business for relevant years are as

follows:

Required:

i. Compute the tax assessment to be raised by the relevant tax authority for relevant years of

assessment on both normal basis and election basis.

ii. Advise Samuel Lawson on whether or not to make election.

Show all workings. (Total: 20 marks)

Solution to question 2:

NORMAL BASIS ELECTION BASIS

Year Basis Period Assessable

Profit

Basis Period Assessable

profit

2006 1/7/2006 – 31/12/2006 1/7/2006 – 31/12/2006

6/8 X N3,200,00 2,400,000 6/8 X N3,200,000 2,400,000

2007 1/7 2006- 30/6/2007 1/1/2007- 31/2/2007

N3,200,000+4/2X N3,000,000

4,200,000 (2/8X3,200,000) 3,300,000

2008 1/7/2007- 28/2/2008 4,200,000 1/12008-31/12/2008

(2/12X300,000)+(10/12X 240,000

2,500,000

2009 1/3/2007- 28/2/2008 3,000,000 1/3/2007- 28/2/2008 3,000,000

2010 1/3/2008 – 28/2/2009 2,400,000 1/3/2008- 28/2/2009 2,400,000

RIGHT OF ELECTION

YEAR NORMAL BASIS (N) ELECTION BASIS

2007 4,200,000 3,300,000

2008 4,200,000 2,500,000

TOTAL 8,400,000 5,800,000

Difference in Assessable Profit N8,400, 000 –N5,800, 000 = N2,600, 000

From 1/7/2006 to 28/2/2007 N3,200,000

From 1/3/2007 to 28/2/2008 N3,000,000

From 1/3/2008 to 28/2/2009 N2,400,000

Page 31 of 36

Comment: It is advisable for Samuel Lawson to apply for election, because by doing so he will have a

tax savings of N2,600, 000

3. a) Indicate, with reasons, the relevant tax authority in Nigeria to which the following taxes

should be remitted when deducted

i. PAYE tax on salaries (3 marks)

ii. Withholding tax on rent paid to a resident individual by a corporate body

(3 marks)

iii. Partnership income (3 marks)

iv. Withholding tax on rent paid to a corporate body by a corporate body.

(2 marks)

v. Withholding tax on bank saving interest due to a limited liability company

(2 marks)

b.) List the required information to be submitted to the relevant tax authority when remitting

withholding tax deducted from rent. (5 marks)

c) Mrs. Jemila Adamu rented an apartment from Gains Properties Limited. In paying her annual

rent to the company in January 2011, she deducted withholding tax and paid the net to the

company. Justify her action. (2 marks)

(Total: 20 marks)

Solution to question 3:

3 a

(i) PAYE Tax on Salaries and Wages, the relevant tax authority is the Internal Revenue

Authority of the State in which the recipient is deemed to be resident in the year of

assessment. For tax purposes, a person is deemed to be resident in a state where he has his

residence on the 1st January of the year of assessment.

(ii) Withholding tax on rent paid to a resident individual by a corporate body, the relevant tax

authority is the Internal Revenue Authority of the state in which the recipient is deemed to be

resident in the year of assessment. For the purposes, a person is deemed to be resident in a

state where he has his residence on the 1st January of the year of assessment.

(iii) Partnership Income, the relevant tax authority is the tax authority of the territory or Internal

Revenue Authority of the State in which the principal office or place of business of the

partnership in Nigeria situated on the first day of the year of assessment or is first established

during that year of assessment.

(iv) Withhold tax on rent paid to corporate body by a corporate organization, the relevant tax

authority shall be the Federal Inland Revenue Service.

(v) Withholding tax on banks savings interest due to a limited liability company, the relevant tax

authority shall be the federal Inland Revenue Service.

Page 32 of 36

(b). Relevant information to be submitted to the relevant tax authority when withholding taxes on rent

are:

i. The gross amount of the payment;

ii. The name and address of the recipients;

iii. The amount to tax withheld; (i.e. Gross amount)

iv. The address or accurate description of the location of the property;

v. The period which the rent covers.

(c). The amount of the withholding tax deducted by Mrs, Jemila Adamu when paying her rent to

Gains Properties Ltd will be paid to the Federal Inland Revenue Service. She will obtain

necessary withholding tax receipt and form and send to Gains Properties Ltd.

4. Chigozie Maijangali has been in business for many years in the name of Maijangali Enterprise and

made up accounts to 30th September each year, but decided to change to 30th June as follows:

N

Year to 30/9/2005 2,520,000 Year to 30/9/2006 5,040,000 Year to 30/0/2007 4,200,000

9 months to 30/6/2008 5,880,000 Year to 30/6/2009 8,400,000

Required

i. Compute the assessable profits for 2006 to 2010 years of assessment

ii. Prepare a summary of assessments and briefly comment on it (20 marks)

Solution to question 4:

CHIGOZIE MAIJANGALI

COMPUTATION OF ASSESSABLE PROFITS

Old Accounting Date New Accounting Date

Year Basis Period Assessable

Profit (N)

Basis period N Assessable profit

N

2006 1/10/2004 – 30/9/2005 2,520,000 1/10/2004 – 30/9/2005 2,520,000

2007 1/10/2005 – 30/9/2006 5,040,000 1/7/2005 – 30/6/2006 4,410,000

Page 33 of 36

(3/12 X 2,520,000) +(9/12X5,040,000)

2008 1/10/2006 – 30/9/2007 1/7/2006- 30/6/2007

M420,000+(3/12X588,000) 5,670,000 (3/12X504,000)+420,000 5,460,000

2009 1/10/2007 – 30/9/2008 1/7/2007 – 30/6/2008

(9/12X588,000)

+(3/12X840,000

6,510,000 5,880,000

2010 1/102008 – 30/9/2009 8,400,000 1/7/2008- 30/6/2009 8,400,000

SUMMARY OF ASSESSMENT

YEAR Old Accounting Date(N) New Accounting Date

(N)

2007 5,040,000 4,410,000

2008 5,670,000 5,460,000

2009 6,510,000 5,880,000

TOTAL 17,220,000 15,750,000

Comment: The tax authority will raise assessments based on the old accounting date for 2007, 2008, and

2009 years of assessment as a result of higher tax payable by Chigozie Manjangali.

5. Akpabio Love Modern Beauty and Barbing Salon owned by Madam Okoleyanmijemo has traded

for many years in Oshogbo, Osun State. The results of the business for the year ended 31 st October

2010 are as follows:

N N

Income derived from hair dressing business 2,250000 Income derived from hair barbing business 750,000 3,000,000

Less: Cost of Goods sold - 1,875,000 1,125,000

Deduct Administrative Expenses Salaries and wages 153,750 Rent and Rates 75,000

Security 66,000 Transport 93,750

Cleaning 42,000 Miscellaneous Expenses 152,700 Telephone 15,300

Repairs and Maintenance 64,500 Entertainment 36,000

Insurance 30,000 Electricity 24,000 753,000

Net profit for the year 372,000

Additional information:-

Page 34 of 36

i. One fifth of the amount indicated as Salaries and Wages was paid to the Domestic workers of

madam Okoleyanmijemo.

ii. The sum of N15,000 spent in transporting the children of the Properties was included in

Transport and Travelling Expenses.

iii. Fifty per cent of the Telephone Bill was consumed by the Proprieties‟ Husband.

iv. Part of the Entertainment Expenses included a sum of N21,000 spent on the domestic food

consumed.

v. Capital Allowances of N18,750 was agreed with the Tax office.

vi. Madam Okoleyanmijemo is married to a Chartered Accountant who is currently on paid

employment and the marriage is blessed with seven children. All the children are under 16

years of age and attending full tie educational institutions in England.

vii. Madam Okoleyanmijemo is responsible for the up keep of her aged parents – in law who

reside at the village.

viii. She has a life policy that is on a premium of N24,000 per annum.

You are required to compute the personal tax liabilities of madam Okoleyanmijemo for the relevant

year of assessment.

(20 marks)

Page 35 of 36

Solution to question 5:

AKPEBIO LOVE MODERN BEAUTY AND BARBING SALON

COMPUTATION OF INCOME TAX LIABILITY OF OKOLEYANMIJEMO FOR 2010 YEAR

OF ASSESSMENT

N N

Net profit per accounts 372,000

Add: Disallowed Expenses

Salaries and Wages 30,750

Transport and Travelling 15,000

Telephone 7,650

Entertainment 21,000 74,400

Adjusted Profit 297,600

Capital Allowance for the year 18,750

Capital Allowance Relieved (18,750) (18,750)

Statutory Total Income 278,850

Deduct:

Personal Allowance 60,770

Dependant Relative Allowance 4000

Life Assurance Policy Premium 24000 88,770

TAXABLE INCOME 190,080

Tax Payable

1st N30,000 5% 1,500

2nd N30,000 10% 3,000

3rd N50,000 15% 7,500

4th N50,000 20% 10,000

5th N30,000 25% 7,520

TOTAL 29,520

WORKINGS

1. Personal Allowance

i.e. ₦5,000 +20% of E.I

= ₦5,000 + 20/100 X ₦278,850 = ₦60,770

2. Disallowed Salaries & Wages:

1/3 X ₦153,750 = ₦30,750

3. Telephone (Disallowed)

Page 36 of 36

50% of ₦15,300 = N7,650

4 Insurance Assurance Policy

Total Premium paid in both self and spouse is allowed in year 2010

![CAP. C10 Chartered Institute of Taxation of Nigeria Act ...Chartered Institute of Taxation of Nigeria Act CAP. C10 C10 _ 3 [Issue 1] (b) securing, in accordance with the provisions](https://static.fdocuments.us/doc/165x107/5e79099f7c653b451834eaee/cap-c10-chartered-institute-of-taxation-of-nigeria-act-chartered-institute.jpg)