THE CHARTERED INSTITUTE OF TAXATION OF … 2 - OLD...salary increment (12 marks) b The basic steps...

31

Page 1 of 32 THE CHARTERED INSTITUTE OF TAXATION OF NIGERIA (Chartered Institute by Act No. 76 of 1992) STUDENTS’ DELIGHT APRIL 2013 TAXATION TECHNICIAN SCHEME EXAMINATION TTS II OLD SYLLABUS QUESTION AND SUGGESTED SOLUTIONS

Transcript of THE CHARTERED INSTITUTE OF TAXATION OF … 2 - OLD...salary increment (12 marks) b The basic steps...

Page 1 of 32

THE CHARTERED INSTITUTE OF TAXATION OF NIGERIA

(Chartered Institute by Act No. 76 of 1992)

STUDENTS’ DELIGHT APRIL 2013 TAXATION

TECHNICIAN SCHEME EXAMINATION TTS II

OLD SYLLABUS

QUESTION AND SUGGESTED SOLUTIONS

Page 2 of 31

THE CHARTERED INSTITUTE OF TAXATION OF

NIGERIA APRIL 2013: TAXATION TECHNICIAN

SCHEME

PART 2: BUSINESS MANAGEMENT

ATTEMPT ALL QUESTIONS. TIME: 3

HOURS

TAXATION TECHNICIAN’S SCHEME (TTS 2) – OLD SYLLABUS

TTS 2 BUSINESS MANAGEMENT

1 Business communication is one of the dynamic processes that enable the organization to

remain an open system as opposed to the closed system.

Required:

a. List the most common external information which a business organization requires.

(10 marks)

b. What are the steps needed towards the designing of an effective communication

system? (5 marks)

c. What are the effects of a breakdown in communication? (5 marks)

(Total: 20 marks)

SOLUTION

1 a The following are the most common external information required by a business

organization.

(i) Sources and prices of plants and machinery

(ii) Sources and prices of raw materials

(iii) Sources and pricing of fund (Information on Capital and Money Market).

(iv) Customers’ needs, wants and specifications

(v) Competitors’ activities with respect to price, product, promotion, distribution,

internal operation, remuneration to staff etc.

(vi) Sources of and remuneration for skilled, semi-skilled and unskilled labour.

(vii) Government legislation is likely to affect the business e. g. environmental

pollution Act, price control, foreign exchange control, embargo on importation

on specific commodities, taxation rate, minimum wage laws etc.

(viii) General economic, political and social situation in the firm’s immediate

environment.

(ix) Global economic, political and social conditions e.g. global recession, changes in

price of petroleum, raw materials, foreign exchange fluctuations, etc.

(x) Dealer specifications relating to product size, etc. (10 marks)

b The steps required towards the designing of an effective communication systems are:-

Page 3 of 31

(i) Analysis of the decision making system.

(ii) Analysis of information required

(iii) Designing appropriate organization structure

(iv) Designing information processing

(v) Design of control system

c Effects of poor or breakdown in communication are:

Poor decision making by management

It precipitates conflict in organization

Poor communication can lead to organizational unhealthiness symptomized by

poor sales, poor activity level, absenteeism, poor profit and overall

performance.

Complete breakdown in communication will result in the collapse of the

business organization. (5 marks)

2. a. As a Manager in your organization, what motivational incentives would you give in

order to retain your staff? (12 marks)

b. List the basic procedures in a recruitment exercise. (8 marks)

(Total: 20 marks)

SOLUTION

2 a As a manager, the following incentives will be put in place in order to retain staff:-

(i) Review remuneration packages upwards to industry standard or slightly above standard.

(ii) Establish good training policy to improve employees’ skills

(iii) Establish good medical welfare incentives to staff.

(iv) Grant generous fringe benefits to staff e. g. transport allowance, Christmas bonus, leave allowance, retirement benefit schemes

(v) Staff should be given opportunities to attend seminars, workshops, conferences

(vi) Devise measures aimed at rewarding employees performance e.g. promotion

salary increment (12 marks)

b The basic steps in a recruitment exercise are:-

Screening of applicants (1 mark)

Selection of applicants (1 mark)

Testing (1mark)

Interview (1 mark)

Background verification (1 mark)

Page 4 of 31

Decision to hire (1 mark)

Offer letter and medical examination (1 mark)

Induction (1 mark)

(8 marks)

(20 marks)

3. a. List the importance of organizational objectives. (5 marks)

b. Well-defined and integrated organizational objectives or goals have numerous

advantages.

Discuss, at least, three of the advantages of a well-defined and integrated objective in

the management of organization. (15 marks)

(Total: 20 marks)

SOLUTION

3 a The importance of organizational objectives are:-

i. Objectives serve as reference points for the efforts of the organization

ii. Objectives are necessary for coordinating the efforts of the organization. In

coordinating the effort of the organization, the first step is to state the

objectives the organization desires to achieve.

iii. It is important that the organization renews its objectives so as to compete

effectively and grow in the face of stiff competition in the global environment.

iv. Organizational objectives are also the end towards which all organizational

action is directed.

v. Objectives are prerequisite to determine effective policy procedures, methods,

strategies and rules.

vi. Organizational objectives define the destination of the organization; they move

forwards as rapidly as they are approached or attained.

vii. Clearly defined objective is a good navigation aid comparable to a star which

can be used for navigation by ships and airplanes. (5 marks)

b The advantages of a well-defined objectives or goals include:-

Effective objectives encourage all members to work toward the same

organizational objectives. In contrast, there will likely be many different ideas

among members as to what the objectives of the organization are or should be.

Each person under such circumstances work toward his own ideas of the

organizational objectives.

Much of such work will apparently be in conflicting direction or may be

otherwise ineffective. This good objective make behavior in organization more

Page 5 of 31

rational, more coordinated, and thus more effective, because everyone knows

the accepted goals to work towards.

A person can justify doing anything if any objective is as good as the other-

Effective goals give objective yardsticks for measuring, comparing, and

evaluating performance. They provide objective, rational basis for settling

dispute in organization.

Effective objective also can be good motivators because they make it easier for

a member to relate the accomplishment of his personal goals to the work of the

organization. He knows what is expected of him and is thereby more secure in

what he needs to do to be successful in the organization. In setting effective

objectives, managers help members at all levels of the organization to

understand how they can “best achieve their own goals by directing their

behavior towards the goals of the organization. (15 marks)

4. Training and development are key functions of personnel management. The Personnel

Manager is therefore expected to apply his/her technical skills in dealing with conflicts that

arise in these areas among other personnel management functions.

Required:

a Briefly list and explain the training/development process. (10 marks)

b In the design of training programmes, what specific method will you consider in the

training of junior employees? (5 marks)

c Will there be any differences when designing training programmes for managers?

(5 marks)

(Total: 20 marks)

SOLUTION

4 a The training and development process embraces the following steps:-

Identification of training needs

Design of training programmes

Implementation of training programme

Evaluation of training programme (4 marks)

The training and development process can be explained as illustrated here

under.

Page 6 of 31

1½ mark

1½ mark

1½ mark

1½ mark

b The following are the methods for the training of Junior employees.

On -the –job training

Vestibule training:- Where training takes place under classroom conditions for a

large number of staff who must learn the same kind of work techniques at the

same time. An attempt is also made to use as nearly as possible the actual

materials, equipment and work conditions that will actually be found in the real

work place.

Classroom Method:- This is similar to vestibule training except that here

concepts and attitudes are taught to employees rather than specific work

techniques.

This may be in form of lectures, conferences, case studies, role playing and

programmed instruction.

Identification of training / Development needs a. Organization Analysis b. b. Job Analysis c. Individual Analysis

Design of Training / Development Program a. Establishing Training and Development Objectives b. Determine Content of Training and Development

Process c. Choosing Training / Development Methods d. Choosing Location and Instructions.

Implementation of Training / Development a. Releasing of staff, facilities and locations b. Ensuring that Training / Development, meets

Training / Development objectives

Evaluation of Training / Development Program. A general assessment of the training program on the basis of:- a. Objective Criteria e.g. costs, turnover rates, absentism,

productivity, etc. b. Behavioural Criteria – e. g. training reaction, changes

in morales, attitudes, behaviours, etc.

Page 7 of 31

Training through demonstration. A demonstration is one in which an expert or

an instructor show employees how to do certain things. An example is how to

assemble a machine. Demonstration is widely used in the Army in the training of

soldiers. It is particularly effective because it depends upon the visual display of

the method or techniques that is been taught to employees. (5 marks)

c Some of the methods mentioned above particularly those of classroom and

demonstration are also used in the development of managers. The additional methods

used in the development of managers are:-

Job rotation

Coaching

Understudy

Multiple management

Management games (5 marks)

5 a. What are the basic tasks that the marketing manager must perform in order to manage

his operations effectively? (15 marks)

b. Mention five objectives of business organizations. (5 marks)

(Total: 20 marks)

SOLUTION

5 a The following tasks must be performed by the marketing manager to enhance maximum

efficiency.

i MARKET ANALYSIS

This involves the marketing manager to gain an understanding about the

market. This involves obtaining quantitative and behavioural data on buyers and

competitors. (2 marks)

ii SETTING GOALS

This involves the setting of goals and objectives to be pursued from the outset.

Marketing goals are naturally derived from the overall or the ultimate goal of

the organization. The goals set should be challenging and yet attainable and

should be clearly communicated down the organization. (2 marks)

iii PLANNING THE MARKETING EFFORT

To develop a marketing strategy and specific decision regarding the product, the

price, the distribution and the promotion in order to satisfy the needs of the

target market and provide the best channels of achieving the goals

(3 marks)

iv ORGANISATION

Page 8 of 31

This involves designing and establishing position and lines of authority, assigning

personnel and motivating them to do their best. (2 marks)

v EXECUTION

This involves implementing marketing plan. Task must be assigned to individuals

and groups, resources provided and time schedule set for accomplishing

specified objectives or results. (2 marks)

vi CO -ORDINATION

Marketing activities must be coordinated with advertising agencies,

transportation companies and other outside company facilitating the marketer’s

effort. (2 marks)

vii CONTROL

This involves monitoring results in order to identify deviation from planned

objective and to take corrective measures. (2 marks)

(Total 15 marks)

b THE OBJECTIVE OF BUSINESS ORGANIZATIONS ARE:-

i. Maximization of profit (1 mark)

ii. Maximization of revenue (1 mark)

iii. Maximization of shareholders’ wealth (1 mark)

iv. Cost minimization (1 mark)

v. Increase market share (1 mark)

(5 marks)

TTS2 BUSINESS TAXATION

1 a Mention ten (10) bodies to which donation made are allowable in accordance to

the 5th

Schedule of CITA. (10 marks)

b State the steps you will take to register a company with the Federal Inland Revenue

Service (FIRS), and list what you will need to complete the registration. (10 marks)

(Total: 20 marks)

SOLUTION

1 a Bodies to who donation may be made to according to the 5TH schedule of CITA.

1. The Boys Brigade of Nigeria

2. The Boys Scout of Nigeria

3. The Christian Council of Nigeria

4. The Cocoa Research Institute of Nigeria

5. The Girls Guide Of Nigeria

Page 9 of 31

6. The National Library

7. The National Council Of Medical Research

8. The Nigeria Museum

9. The Nigeria Red Cross

10. The National Youth of Nigeria

11. The Society for the Blind

12. The Nigeria Institute of International for the Affairs

13. The National Commission For Rehabilitation

14. The Nigeria Youth Trust

15. Islamic Education Trust

16. Nigeria Accounting Standard Board

17. Nigeria Conservation Foundation

18. National Science Technology Fund

19. The Nigeria Society For The Deaf And Dumb

20. The Nigeria National Advisory Council for the Blind

21. The Chartered Institute of Taxation of Nigeria

22. The Institute Of Charted Accountants of Nigeria

b In oder to register a company as a corporate tax payer with the Federal Inland Revenue

Service (FIRS), the following steps must be taken.

1. A formal letter on the company letter headed paper would be written to FIRS

informing her of his intention to register.

The letter will provide the following information:-

i. The date of incorporation of the company.

ii. The registered address of the company

iii. Date of commencement of business (If it has commenced business)

iv. Names and addresses of shareholders and their shareholding structure.

v. Names and addresses of Bankers.

vi. Names and addresses of tax representative.

vii. Names and addresses of auditors.

viii. Date to which the account of the company will be made i.e. The

accounting year end.

ix. The principal activity of the company.

x. Whether the company is starting a new trade or it is taking over another

business.

xi. Any other directorship/shareholders of the directorship

- The company will need to register as VAT able person.

Page 10 of 31

- A copy of the certificate of incorporation and memorandum and

Articles of Association of the company will be taken along for

sighting at the time of submission.

2 Surulere Limited commenced business on 1st October, 2008 as a manufacturer of baby

wears. You are required to determine the basis on which the company would be subjected

to taxation for the first three tax years given the following results:

Year ended 30th

September, 2009 N480,000

Year ended 30th

September, 2010 N670,000

Year ended 30th

September, 2011 N550,000

(20 marks)

SOLUTION

2 SURULERE LIMITED

DETERMINATION OF THE BASIS PERIOD FOR ASSESSABLE PROFIT FOR THE RELEVANT TAX YEARS.

NORMAL RIGHT

Tax Year Basis Period Assessable Profit Basis Period Assessable Profit

N’000 N’000

2008 1/10/08-31/12/08 120,000

2009 1/10/08-30/09/09 480,000 1/1/09-31/12/09 527,500

2010 1/10/08-30/09/09 480,000 1/1/10-31/12/10 640,000

Conclusion: Surulere limited should not exercise the right of election.

Workings

Normal

2008 = 1/10/08 – 31/12/08

3/12 x 480,000 = N120,000

Right

N

2009 1/1/09 – 30/09/09 = 9/12 x 480,000 = 360,000

1/10/09 – 31/12/09 = 3/12 x 670,000 = 167,500

527,500

2010 1/1/10 – 30/09/10 = 9/12 x 670,000 = 502,500

1/10/10 – 31/12/10 = 3/12 x 550,000 = 137,500

640,000

3 Premier Limited is a company incorporated with a nominal capital of N8.5 million.

Page 11 of 31

The paid up capital of the company is N6,250,000 divided into shares of N1.00 each. The

company which has been trading for many years makes up its account to 31 May every

year. The following is an extract of the company‟s Profit and Loss Account for the year

ended 31st May, 2010. N N

Gross Profit 12,200,000

Directors salaries 650,000

Erection of new sign post 65,000

Depreciation 4,250,000

Income Tax – 2008 1,450,000

Plant replacement reserve 720,000

Other expenses 1,630,000 8,765,000

Net Profit 3,435,000

The capital allowances were agreed to be N4,104,800. It was also agreed that there were no

disallowable expenses included in “other expenses”.

You are required to :

a. Compute the total assessable profit for the relevant year of assessment. (5 marks)

b. Compute the income tax payable for the year of assessment (5 marks)

c. Compute the total tax liability for the relevant year of assessment. (5 marks)

d Under the companies income Tax Act, mention the types of dividends that are

exempted from Tax. (5 marks)

(Total: 20 marks)

SOLUTION

3 PREMIER LIMITED

a COMPUTATION OF TOTAL ASSESSABLE PROFIT FOR 2011 TAX YEAR

N N

Net profit per amount 3,435,000

Add:

Erection of new Sign Post 65,000

Depreciation 4,250,000

Income Tax – 2008 1,450,000

Plant Replacement Reserve 720,000 6,485,000

Adjusted Profit 9,920,000

Capital Allowance (4,104,800)

Total assessable Profit 5,815,200

Page 12 of 31

b Income Tax payable @ 30% 1,744,560

Add

Education Tax @ 2% (2% x 5,815,200) 116,304

c Total Tax Liability 1,860,864

d i Dividends distributed by Unit Trust in Nigeria

ii Dividends derived by a company from a country outside Nigeria and brought

into Nigeria through government approved channels.

Iii Dividends received from investment in wholly export oriented business

Iv Dividends paid by a pioneer company to the extent that they are paid out of

income exempted from tax under CAP179 LFN 1990

v Dividends received from small companies in the manufacturing sector in the

first five years of their operations.

vi Dividends received from a foreign investment provided such dividend are

received through a domiciliary account.

4 a Outline the practice of Revenue where changes in accounting dates are made.

(5 marks)

b Explain the conditions available for granting Capital Allowance (5 marks)

c List and explain five types of relief available to Corporate Tax Payers. (5 marks)

d Explain what you understand by Original Assessment and Additional Assessment.

(5 marks)

(Total: 20 marks)

SOLUTION

4 a The practice of revenue for change in accounting date

i. The date when the business first failed to prepare accounts to the old

accounting year end is identified. This becomes the first tax year.

ii. Two subsequent tax years are identified and chosen

iii. The basis period for asessable profit is determined on the preceeding year basis

for three tax years using the old date.

iv. Step (iii) is repeated using the new date.

v. The sums of the assessable profit in step (iii) and (iv) are determined and

compared.

vi. The assessment for the three tax years is based on the higher of the two.

b The conditions available for capital allowance are:-

i. The qualifying capital expenditures must be owned by the tax payer making the

claim as at the end of the basis period.

ii. The tax payer must be making use of the capital expenditure for the purpose of

its trade or business.

Page 13 of 31

iii. The qualifying capital expenditure must be “in-use” as at the end the basis

period.

iv. Where the value of the qualifying capital expenditure is not less than N500,000

(Five Hundred Thousand Naira), an acceptance certificate must be obtained

from the Inspectorate Division of the Federal Ministry of Industry.

Note that (iv) is not strictly a condition for granting CA but for additional CA.

v A claim must be made by a tax payer before allowances can be granted.

vi For land and buildings, capital allowances are not claimable on the cost of the

land. The cost of the land must be separated from the total cost of land and

buildings and the allowances should be granted only on the cost of a building.

vii Not all assets qualify for capital allowances. e. g. Assets which do not qualify for

allowances include company formation costs, goodwill, patents, stock and

shares.

c Reliefs available to a corporate tax payer.

i. Capital allowance may be claimed on qualifying capital expenditure with the aim

of reducing tax liability.

ii. Investment allowance may be claimed on plant and machinery, in addition to

the normal annual and initial allowance.

iii. Losses may be carried forward for a maximum period of four years after which it

lapses. The exception to this rule is the agricultural business where losses might

be carried forward indefinitely.

iv. Company operating in the export – processing zone are to enjoy tax free period

of up to five years.

v. For pioneer business, pioneer certificate may be issued with the implication

that such a business will enjoy a tax holiday period of between three to five

years.

Others reliefs available to corporate tax payers include:-

vi Small Companies Relief

vii Roll Over Relief

viii Rural Investment Relief

ix Investment Allowance

x Pioneer Companies Relief

xi Reconstruction Investment Relief

xii The profit of the company established within an export processing zone or free

Page 14 of 31

trade zone are exempted provided that 100% production of such company is for

export otherwise tax shall accrue proportionately on the profit of the company

(as amended by CITA 2007)

d Original Assessment . This is the first assessment raised on a tax payer in a particular

year of assessment. An Original assessment may be the subject of an objection and

appeal procedures.

Additional Assessment. An additional assessment will usually arise from a back duty

assessment. The additional assessment is cover a short fall in tax that was previously

paid.

5 a What are the rules governing cessation of business? (5 marks)

b Chief Lamidi Limited has been in business for many years. As a result of

economic meltdown, he ceased trading permanently on 30th

September 2010. The

adjusted profits were as follows:

Year ended 30th

June 2007 N160,500

Year ended 30th

June 2008 N96,000

Year ended 30th

June 2009 N125,000

Year ended 30th

June 2010 N95,000

3 months to 30th

September 2010 N25,000

i Compute the assessable profit of Chief Lamidi Limited for the last three

years of assessment. (9 marks)

ii Justify the option open to the Federal Inland Revenue Service and

comment. (6 marks)

(Total: 20 marks) SOLUTION

5 a Under the cessation rule, it is required that the basis period for assessable profit for the

last two years of assessment should be determined. The assessable profit determined

for this two tax years form the basis of final assessment.

In the penultimate tax year, the basis of assessment shall be on the preceeding tax year.

In the ultimate tax year, the basis of assessment shall be from the beginning of the

government tax year i.e. 1ST January of the year up to date of cessation. It must however

be noted that under this cessation rule, the tax authority has the right to exercise an

option. This is to determine whether the basis of assessing the tax payer in the pen

ultimate tax year should be on actual year basis. This right is exercised if it will increase

the tax payable by the tax payer.

Finally, in the event that a tax payer whose business has ceased derives or receives

income after the date of cessation, such income would be deemed to have been made

on the last day of business. Consequently, such an income will be subjected to tax.

Page 15 of 31

b (i) CHIEF LAMIDI LIMITED

COMPUTATIONS OF ASSESSABLE PROFIT FOR THE LAST THREE TAX YEARS

Tax year Basis Year Assessable Profit

2008 1/7/2006-30/6/2007 N160,500

2009 1/7/2007-30/6/2008 N96,000

2010 1/1/2010-30/9/2010 N72,500

2010 Computation

1/1/2010-30/6/2010 6/12 x 95,000 = 47,500

1/7/2010-30/09/2010 = 25,000 72,500

(ii) CHIEF LAMIDI LIMITED

COMPUTATIONS OF OPTION OPEN TO THE FEDERAL INLAND REVENUE SERVICE

Tax year Basis Year Assessable Profit

2008 1/7/2006-30/6/2007 N160,500

2009 1/1/2009-31/12/2009 N110,000

2010 1/1/2010-30/9/2010 N72,500

2009 OPTION COMPUTATION

1/1/2009-30/06/2009 = 6/12 x 125,000 = 62,500

1/7/2009-31/12/2009 = 6/12 x 95,000 = 47,500

110,000

Note:

The option open to the Federal Inland Revenue Service is the penultimate tax

year where it can be decided to assess the tax payer on actual year basis. It is

apparent from the above that this option would be exercised because the

associate profit of N110,000 is higher than N96,000 on the original basis.

TTS 2 PERSONAL TAXATION SOLUTION

1 a i Distinguish between Tax Avoidance and Tax Evasion. (5 marks)

ii Give four examples of Tax Avoidance (4 marks)

iii Give four instances where tax can be said to have been evaded

(4 marks)

b Mention clearly the penalties payable by a person or company that is

required by law to deduct withholding Tax in a situation where the person or

company:

i Fails to deduct the withholding tax. (2 marks)

Page 16 of 31

ii Fails to pay the tax to the relevant tax authority within the stipulated 30

days. (2 marks)

c State the income exempted from withholding tax under the relevant tax laws.

(3 marks)

(Total: 20 marks)

SOLUTION

1 a Distinguish between Tax Avoidance and Tax Evasion

i. Tax Avoidance is a device by which a tax-payer legally reduces tax payable while

tax evasion on the other hand, is a deliberate act on the part of the tax payer

not to pay the tax due.

In the case of tax avoidance, the tax payer identifies loop-holes in the tax law

and takes advantage of them to reduce tax liability. Tax Evasion is a

contravention of the tax laws whereby a taxpayer reduces the tax liability or

pays no tax by deliberate omission of revenue, concealment of materials fact

etc.

ii. Examples of Tax Avoidance

Incurring capital expenditure with the purpose of claiming capital

allowance;

Where foreign investment is made with the aim that income therefrom

will be exempted from tax;

Investments in certain sectors of the economy which enjoy special

reliefs e.g. agriculture, mining and manufacturing. These sectors are

also amenable to specific tax incentives; and

Another example of tax avoidance is where some expenses, which are

allowable expenses are incurred – which have the tendency of reducing

profit computed for tax purposes.

iii. Four instances of tax evasion are as follows:

Understatement of incomes;

Inclusion of personal expenses in company’s accounts;

Overstatement of expenses/ Fraudulent claiming of expenses or

allowances

Manipulation of figures in the manufacturing or trading accounts/

Dishonest tax reporting;

Deliberate omission of incomes from some sources;

Concealment of profits from illegal or other sources;

Page 17 of 31

Fictitious claim of capital or tax incentive and allowances.

b. For a person or company who is required by law to deduct withholding tax but fails to

do so and also fails to remit it to a tax authority

i) Prior to the amendment of the Personal Income Tax Act in 2011, the penalty

was the higher of 10% of the tax due or N5,000 while interest was at the

prevailing commercial rate.

However, the amendment to PITA prescribes new penalties as follows:-

10% of tax not deducted or remitted;

Addition to tax not deducted or remitted;

Plus interest at the prevailing monetary policy rate of the CBN; and

Power of the Accountant General of the Federation to deduct at source.

ii) Failure to deduct and pay the tax to the Relevant Tax Authority within the

stipulated 30days, the penalty under the Companies Income Tax Act- is 10% of

the tax due plus the interest at the prevailing commercial interest rate, in

addition to the principal tax due (old section 74 of PITA).

c. Under the Personal Income Tax Law, the following incomes shall be exempted from

Withholding Tax:-

i) Interest on deposit accounts of a foreign non-resident company; is exempted

provided the deposits in the accounts are transfers wholly of foreign currencies

to Nigeria or after 1st January, 1990 through Government approved channels

(see section 23, CITA).

ii) Dividends received from small companies in the manufacturing sector in the

first 5years of their operations (see section 23, CITA).

iii) Dividends received from investments in wholly export oriented businesses (see

section 23, CITA).

iv) Any interest received on a passbook saving account of less than N50,000.00;

v) Any dividend, interest, rent and royalty received from outside Nigeria and

brought into Nigeria through a Government approved channel.

2 Wazobia Motors PLC is a leader in the luxurious bus business. It has, altogether 50

luxurious buses in its fleets which as a matter of company policy, must be disposed off

after four years of use. On 1st January,2008, it enters into a hire - purchase agreement

with Qua – Iboe International Merchant Bank Limited for the purchase of six buses. An

initial deposit was paid on 1st of August,2008 in the sum of N3,000,000. This was to be

followed by ten (10) equal quarterly installments of N500,000 each. The financial

Page 18 of 31

director had reported that N6,900,000 would have been needed to purchase the buses

for cash.

The first installment was paid on 30th

November,2008. Wasobia Motors Plc adopts 31st

December as its accounting year end. There would be no change in accounting date in

the next four (4) years.

You are required to:

a Compute the Capital Allowances claimable for all the years. (10 marks)

b Compute relevant tax payable. (10 marks)

(Total: 20 marks)

SOLUTION

2 WAZOBIA MOTOR INCORPORATED PLC.

COMPUTATION OF CAPITAL ALLOWANCE FOR 2009 – 2012 TAX YEARS

TAX YEAR I II III IV CAPITAL ALLOWANCE 2009 N N N N N

COST 3,390,000

IA (1,695,000) 1,695,000

AA (423,750) 423,750

2,118,750

2010 TWDV 1,271,250

COST - 1,560,000

IA - (780,000) 780,000

AA - (260,000) 683,750

1,463,750

2011 TWDV 847,500 520,000

COST - - 1,560,000

IA - - (780,000) 780,000

AA (423,750 (260,000) (390,000) 1,073,750

1,853,750

2012 TWDV 423,750 260,000 390,000

COST - - - 390,000

IA - - - (195,000) 195,000

AA 423,750 (200,000) (390,000) (194,940) 1,268,690

1,463,690

Working Notes.

Page 19 of 31

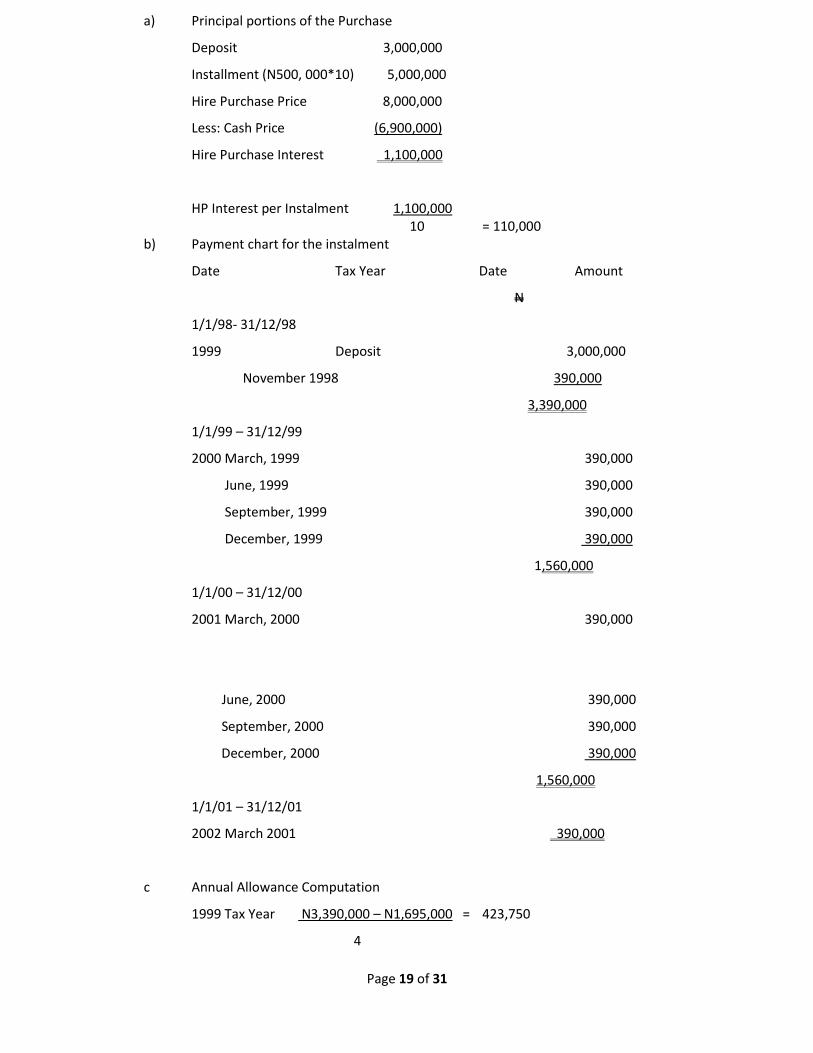

a) Principal portions of the Purchase

Deposit 3,000,000

Installment (N500, 000*10) 5,000,000

Hire Purchase Price 8,000,000

Less: Cash Price (6,900,000)

Hire Purchase Interest 1,100,000

HP Interest per Instalment 1,100,000 10 = 110,000

b) Payment chart for the instalment

Date Tax Year Date Amount

N

1/1/98- 31/12/98

1999 Deposit 3,000,000

November 1998 390,000

3,390,000

1/1/99 – 31/12/99

2000 March, 1999 390,000

June, 1999 390,000

September, 1999 390,000

December, 1999 390,000

1,560,000

1/1/00 – 31/12/00

2001 March, 2000 390,000

June, 2000 390,000

September, 2000 390,000

December, 2000 390,000

1,560,000

1/1/01 – 31/12/01

2002 March 2001 390,000

c Annual Allowance Computation

1999 Tax Year N3,390,000 – N1,695,000 = 423,750

4

Page 20 of 31

2000 Tax Year N1,560,000 – N780,000 = 260,000

4-1

2001 Tax Year N1, 560,000 – N780,000 = 390,000

4-2

2002 Tax Year N390,000 – 195,000 = 195,000

4-3

Less: Residual Value (N10 x 6) = 60

194,940

40 ticks x ½ = (20 marks)

3 a Explain the meaning of the following teams under the Personal Income Taxation:

i Place of Residence (2 marks)

ii Principal place of Residence (2 marks)

iii Itinerant Worker (2 marks)

b Discuss the Relevant Tax Authorities in relation to the following:

i An Individual (1 mark)

ii An officer of the Nigerian Foreign Service (1 mark)

iii A trustee of a trust or settlement (1 mark)

iv A partnership (1 mark)

c i What is „Earned Income‟? (2 marks)

ii Provide a list of six incomes that are chargeable to tax under the Personal

Income Tax Act. (6 marks)

iii Give two examples of Unearned Income. (2 marks)

(Total: 20 marks)

SOLUTION

3 a. i. Place of Residence in relation to an individual means a place available for his

domestic use in Nigeria on a relevant day, and does not include any hotel rest-

house or other place at which he is temporally lodging unless no more

permanent place is available for his use on that day.

ii. Principal Place of Residence in relation to an individual with two or more places

of residence on a relevant day not being within any one territory means:

In the case of an individual with source of income other than a person in

Nigeria, that place of those places in which he usually resides

In the case of an individual who has a source of earned income other

than pension in Nigeria that place of those places which on a relevant

day is nearest to his usual place of work.

Page 21 of 31

For an individual who has a source(s) of unearned income in Nigeria,

that place of those places in which he usually resides

iii. Itinerant Worker – Prior to the amendment to PITA in 2011, an individual who

works at any time during a year of assessment ( other than as a member of the

Armed Forces) for a daily wage or customarily earns a livelihood in more than

one place in Nigeria and whose total income does not exceed N600. (Section

108 of PITA).

“Itinerant worker”, according to the PITA 2011 Amendment includes an

individual irrespective of his status who works at any time in any State during a

year of assessment (other than as a member of the Armed Forces) for wages,

salaries or livelihood by working in more than one State and work for a

minimum of twenty (20) days in at least three (3) months of every assessment

year.

b. Relevant Tax Authority in respect of the following :

For individual – for a year of assessment , the tax authority of the territory in

which the individual is deemed to be resident that year;

An officer of the Nigeria Foreign Service has the Federal Inland Revenue Service

as his relevant tax authority;

For a trustee of a trust or settlement- where all incomes of the settlement or a

trust for a year of an assessment arises in one territory, is the tax authority of

that territory.

But where the income of the settlement or trust for a year of assessment arises in more

than one territory,, or in any other case where the relevant tax authority cannot be

determined, the tax authority would be the Federal Board of inland Revenue.

Relevant tax authority for a partnership, for a year of assessment, in which the

principal office or place of business of the partnership in Nigeria, is situated on

the first day of that year or where it is first established that year.

c. i) Earned Income is income from personal services that you earn by work or effort

as distinguished from incomes generated by property or other investment

incomes. Earned incomes include all amounts received as wages, tips, bonuses,

salaries, professional fees, gains or profit of a trade, business, vocation,

compensation, bonuses, premiums, pension, benefits and other perquisites.

ii) Various sources of income on which tax is payable are:

Gains or profit of any trade, business, profession or vocation;

Remuneration of an employment excluding sums paid to the employee

as reimbursements;

Page 22 of 31

Gains or profit including premiums arising from the grant of the right of

use or occupation of property;

Dividends;

Interest;

Discounts;

Pension, charge or annuity;

Employment incomes such as salaries, wages, fees, allowance or other

gains or profit from employment including compensations, bonuses,

premiums, benefits or other perquisites allowed.

iii) Unearned incomes under the Personal Income Tax Act are mostly limited to

investment incomes such as dividends, rents, Royalties and interest. They are

received net of withholding tax.

4 Mr. Owoori retired from Federal government employment on 31st January, 2008. He took

up an employment with a private company on 1st April, 2008. The following information

related to Mr. Owoori:

N

i. Salary per annum (2007) 60,000

January salary (2008) 5,000

Salary for new employment per month 12,000

ii. Pension payable from February, 2008 45,000

iii Dividend received (Gross)

Paid 3/4/07 10,000

“ 3/12/07 3,000

“ 30/06/08 4,500

“ 31/12/08 8,000

iv Christmas bonus (December 2008) 8,500

v Rent collected (1/9/07 to 30/4/09) 84,000

vi Transport Allowance (new employment) 9,600

vii Housing Allowance “ “ 12,000

viii Expenses on property:

Water rate - 50% paid in 2007 2,250

„‟ „‟ „‟ paid in 2008 2,250

Insurance per annum 3,500

ix Mr. Owoori is married with five (5) children whose profiles are:

Child Date of Birth Employment

Page 23 of 31

Bonus 5/7/97 Attending School

Sunday 29/3/04 Out of School but

unemployed

Ekunwo 4/2/03

Idanwo 21/8/00

Adura 21/1/09

x Mr. Owoori settles an alimony of N13,000 per annum to a legally-

divorced wife

xi Capital Allowances on the building amount to N5,000

xii He has two life assurance policies on:

-- Self - Capital Sum N200,000

-- Annual Premium N22,000

-- Bonus, his eldest - Capital Sum N100,000

Annual Premium N3,000

xiii Mr. Owoori pays monthly N1,000, as settlement of loan which he took to

build the house yielding the rent.

xiv. He has an aged Uncle on whom he spends only N5,000 per annum.

The Uncle has a rental income of N6,100 per annum

You are required to compute the income tax payable by Mr. Owoori for

the 2008 year of assessment. (20 marks)

SOLUTION

4. MR. OWOORI

COMPUTATION OF TAX LIABILITY FOR 2008 TAX YEAR

Earned Income N N

Salary (1) 137,000

Housing (2)

Transport (3)

Gratuity (4)

Christmas Bonus 8,500

Pension (5) 41,250 186,750

Unearned Income

Dividend (Gross) (6) 13,000

Rent 9,100 22,100

208,500

Page 24 of 31

Less: Personal Allowance (8) 42,350

Children Allowance 10,000

Dependent Allowance (9)

Life Policy Allowance (7) 22,000 (74,350)

134,500

Tax Payable

1st N30,000 @ 5% 1,500

Next N30,000 @ 10% 3,000

Next N50,000 @ 15% 7,500

Next N24,500 @ 20% 4,900

Tax Borne 16,900

Deduct:

Withholding Tax deducted at source:

Dividend (N13,000 x 10%) (1,300)

Net Tax Payable 15,600

Notes:

1) Salary

Federal Ministry (1/1/08 – 31/1/08) 5,000

New employment (1/2/08 – 31/12/08) (12,000 x 11) 132,000

137,000

2) Housing Allowance

Since the housing allowance does not exceed N100,000 it will be exempted from tax.

3) Transport Allowance

The transport allowance received of N9,600 per annum is less than N20, 000 which is

exempted from tax.

4) Pension (5) (1/2/08 – 31/12/08) = N45,000 x 11/12 N41,250

5) Rental Income 1/09/07 – 31/12/07 N N

Income received (4/20 x N840,000) 16,800

Deduct:

Water rate (4/12 x N4,500) 1,500

Insurance (4/12 x N3,600) 1,200 2,700

Net Income 14,100

Capital Allowance (5,000)

Chargeable Income 9,100

6) Dividend

Page 25 of 31

Since Dividend is charged to tax on the proceeding year basis, the relevant data for 2008

year of assessment are the 2007 receipts.

Received 3/04/07 N10,000

Received 3/12/07 N 3,000

N13,000

7) Life Assurance Policy Allowance

Actual premium N22,000

8) Personal Allowance is N5,000 + 20% of Earned Income

=5,000 + (20% of N186,750)

=5,000 + N37,350 N42,350

9) No dependant relative allowance is available to Mr. Owoori as the dependant earns an

income that exceeds N600 per annum

10) The N1,000 paid by him for the settlement of loan is not available for him as an

allowance. Only the interest is available

5 Mrs. Emulewu is the Chief Accountant of Ogogoro Holdings. She is married with six

children, all of school age. She also maintains her aged parents both of whom earn no

income. She indeed shares their maintenance equally with her junior brother.

The following is the summary of her remuneration:

Basic Salary: N150,000 per annum up to July, 2009 and N180,000 per annum from

August,2009

House Allowance of N90,000 per annum up to July, 2009

Transport Allowance of N60,000 per annum up to July, 2009 Perquisite from August,

2009

- Company‟s house which was completed with N350,000 in 2004

- Company‟s car costing N450,000

- Furniture, air conditioner and others costing N300,000

- Bonus: one month basic pay as at the end of the year.

- Leave Allowance: One month basic pay as at the time of the leave. She normally

takes her leave in July. She has a personal house which was completed in 2002.

She collected a total sum of N350,000 being a seven years rent in 2002. She also

regularly receives dividend from 2000 ordinary shares in Nestle Plc and during

2006, 2007, 2008, dividend

She receives 30 kobo, 30 kobo and 50 kobo per share respectively.

Page 26 of 31

You are required to compute her income tax liability for 2009 year of assessment.

(20 marks)

SOLUTION

5 a. The term “place of residence” in relation to an individual means a place that is available

for domestic use of the individual in Nigeria on the day in a relevant tax year except an

hotel, rest house or other place which is a temporary residence unless no permanent

place is available.

b. Working of Employment Income of Mrs. Emulewu

Jan – July Aug – Dec Total

N N N

Salary 87,500 75,000 162,500

Allowances:

Housing 52,500 - 52,500

Trans port 35,000 35,000

Leave allowance 12,500 12,500

Perquisites

Accommodation 7,292 7,292

Car 9,375 9,375

Furniture 6,250 6,250

Bonus 15,000 15,000

300,417

Less: Restrictions

Housing (52,500)

Transport (20,000)

Leave (12,500)

215,417

MRS. EMULEWU

COMPUTATION OF INCOME TAX LIABILITY FOR 2009 TAX YEAR

N N

Earned Income

Employment Income 215,417

Unearned Income

a - Dividend 10,000

b - Rent 5,000

Page 27 of 31

Total Statutory Income 230,417

Less: Relief

Personal Allowance (5,000 + (20% x N215, 417) 48,083

Children Allowance (N2,500 x 4) 10,000

Dependant Relative (N2,000 x 1) 2,000

Taxable Income 206,334

Tax Liability

1st N30,000 @ 5% 1,500

Next N30,000 @ 10% 3,000

Next N50,000 @ 15% 7,500

Next N50,000 @ 20% 10,000

Above N46,334 @ 25% 11,584

33,584

TTS 2 MANAGEMENT INFORMATION SYSTEM

1 Explain the following terms:

a. Object Program (4 marks)

b. Multi-Programming (4 marks)

c. LAN (4 marks)

d. E-Commerce (4 marks)

e. Data Security (4 marks)

(Total: 20 marks)

SOLUTION

1 a OBJECT PROGRAM

These are programmes that have been converted to machine codes from the source

Programme. The programmer writes in his language that the computer did not

understand. This programme has to be converted to the language of the computer

which is machine codes.

b MULTIPROGRAMMING

This is a data processing technique that permits multiple or more than one programme

to share a computer system’s resources at the same time. The CPU is used concurrently.

Many users can access different application programme at the same time.

c LAN

This means “Local Area Network”. This is network that is confined into small area. i. e.

geographic are such as office, building e.t.c. One system will be designated as a server

while others system (workstations) is connected to it by cables.

Page 28 of 31

d E-COMMERCE

Electronic commerce is an act of carrying out business over the internet with the aid of

computers. This is buying and selling of goods and services electronically. It allows

business to be carried out without barriers of time and distance.

e DATA SECURITY

This is the act of protecting data from corruption, destruction and removal. It shields

data from unauthorized access and damage.

2 a. What is flowchart? (2 marks)

b. List 5 characteristics of a good program. (10 marks)

c. Mention any 5 areas where computer can be used. (5 marks)

d Mention 3 features/characteristics of computer that makes it better than manual

operations. (3 Marks)

(Total: 20 marks)

SOLUTION

2 a FLOW CHART

This is a diagrammatical representation of the processing of information system. It

shows the sequence of events with use of symbols.

b CHARACTERISTICS OF A GOOD PROGRAMME

(i) Accuracy:- it must be precise and produce correct result always.

(ii) Reliability:- it must be reliable

(iii) Maintainability:- it must be easy to modify

(iv) Portability:- ability to transfer the programme to other system.

(v) Readability:- ability to read and understand the programme

(vi) Performance:- ability to achieve required task effectively

(vii) Optimal Storage:- The programme should not occupy much storage space.

c APPLICATION AREA OF COMPUTER

(i) Offices

(ii) Hospitals

(iii) Schools

(iv) Hotels

(v) Telecommunication Industries

(vi) Airport

(vii) Banks

d FEATURES OF COMPUTER THAT MAKES IT BETTER THAN MANUAL OPERATION

(i) Fast:- faster than manual method

Page 29 of 31

(ii) Accuracy:- data supply to computer is always accurate and correctly processed

(iii) Improved output

(iv) Easy retrieval of information

(v) Ability to solve complex operation

(vi) Ability to process large volume of data

(vii) Versatility

3 Computer can process data into information with 99% accuracy and reliance.

a. Identify errors inherent in data processed through computer. (7 marks)

b. What are control measures required to eliminate errors associated with the computer

processes? (8 marks)

c. What are the advantages and limitations of human processes over computer processes

in generating information? (5 marks)

(Total: 20 marks)

SOLUTION

3 a IDENTIFY ERRORS INHERENT IN DATA PROCESSED THROUGH COMPUTER

(i) Software/Programme errors/Semantic and syntax software being set of

programme used in executing application, if wrong or faulty, outcome will also

be faulty.

(ii) Garbage in- garbage out/ input error. If wrong data is inputted into the

computer output will be wrong

(iii) Technical/ Hardware Errors: If the hardwire is having factory fault. It will affect

the efficiency.

(iv) Human error

(v) Power failure can cause error in computer

b WHAT ARE THE CONTROL MEASURES REQUIRED TO ELIMINATE ERRORS

ASSOCIATED WITH THE COMPUTER PROCESSES.

(i) Softwares / Programs must be well tested on debugged by programmer before

being put to use.

(ii) Data must be properly checked before being inputted to computer – data

validation

(iii) Hardware: Manufacturer’s, standards regulations must be followed

(iv) Regular power supply e. g. generating set or Uninterrupted power supply (ups)

(v) Adequate training for users and administrators.

Page 30 of 31

c WHAT ARE THE ADVANTAGES AND LIMITATION OF HUMAN PROCESSES OVER

COMPUTER PROCESSES IN GENERATING INFORMATION

Advantages:-

(i) It is cost effective i.e. does not involve the purchase of computer

(ii) Processing an output is not dependent on electricity

(iii) It does not required technical skill

(iv) It is simple to process

LIMITATIONS

(i) The input might not be accurate

(ii) Processing is slow

(iii) It kills workers morale and reduces job satisfaction

(iv) Security:- This might be difficult to effect

(v) Human process might not be able to process complex operations

(vi) Large volume of operation might be difficult handle

4 a. Describe e-Taxation. (2 marks)

b. State 3 advantages and 2 disadvantages of e-Tax system. (10 marks)

c. List 3 members of a Steering Committee. (6 marks)

d. State 2 functions of a Steering Committee . (2 marks)

(Total: 20 marks)

SOLUTION

4 a E- TAXATION

This means electronic taxation which allows all tax related issues to be carried out with

the aid of internet

b ADVANTAGES

(i) Tax payers have assess to tax information faster

(ii) Accuracy in tax matters

(iii) It reduce touting or intermediaries

(iv) It prevent queuing in tax office

(v) It saves filling effort.

DISADVANTAGES

(i) There might be delay in accessing tax information due to system breakdown

(ii) There is high cost of getting connected to the soft wares

(iii) There is need for tax payers to have skill in operating tax programme

c STEERING COMMITTEE

(i) A senior manager has chairman

(ii) Managers of user department

(iv) Senior officers of data processing department

Page 31 of 31

(v) External representative e.g. consultant

(vi) A certified Accountant

d FUNCTION OF STEERING COMMITTEE

(i) They decide to allocate it resources of the organization

(ii) They plan for the future system development of the organization

(iii) They ensure that all it activities is in in line with the strategic plan of the

organization

(iv) They create terms of reference for the project teams

(v) They monitor the progress of the projects

(vi) They make recommendation to Board and Management

(vii) To evaluate feasibility reports

5 Information technology through the use of computer is taking the place of human resources

astronomically and could soon render human (physical labour) valueless. Discuss.

(Total: 20 marks)

SOLUTION

5 The use of computer cannot take the place of human resources in an organization. Computer is

meant to be a tool that aids the accurate and fast processing of data to provide management

with information necessary for decision making process. It adds value to human labour in the

following ways:-

(i) Information technology reduces paper work

(ii) Cost effectiveness

(iii) Accuracy of processing

(iv) Minimizes errors

(v) Saves time

(vi) Availability of information at any required time

(vii) Create employment for IT professionals

(viii) Reliability and accuracy of information

(ix) Accessibility to global information

(x) Enhances good record keeping

(xi) Real time information for management decisions

Hence, the use of computer will not render human valueless.

This is expected with technology development for improve work efficiency.

Computer and other IT equipment were designed to improve data processing efficiency. Only

routine manual job capable of been programmed can be handled by computer.

Most logical job requiring high level personnel skill like managerial skill may not be handled by

computer.