The case of HSBC’s Climate Partnership Programme · The case of HSBC’s Climate Partnership...

29

1 Talent management and effect of sustainability training The case of HSBC’s Climate Partnership Programme Maria Laura Franco-Garcia Senior research in environmental policy, CSTM Twente Centre of Studies in Technology and Sustainable Development at the University of Twente, The Netherlands. Former director of academic department and master's programme of sustainable development sciences in Tec de Monterrey, Mexico. PhD obtained in France on Environmental Sciences and Environmental Engineer from Mexico City. University of Twente Postbus 217; 7500 AE; Enschede, Netherland Tel : +31.53.4893203; Fax : +31.53.4894850; Email: [email protected] http://www.utwente.nl/cstm/ Matthew Gitsham Director of ACBAS, the Ashridge Centre for Business and Sustainability. Lecturer on Ashridge programmes (MBA and MSc in Sustainability) and Programme Director for the Integrating Corporate Responsibility programme. Elected member of the academic board of the European Academy of Business and Society. Member of the stakeholder advisory panel of Nexen, the Canadian Energy company. Frequent contributor to industry and academic conferences. Ashridge Berkhamsted Hertfordshire HP4 1NS United Kingdom [email protected] Tel. +44 1442843491 Fax. +44 1442841209 www.ashridge.org.uk Carla C.J.M. Millar Professor of International Marketing & Management at the School of Management & Governance of the University of Twente, and a Fellow of Ashridge Business School in the UK. Previously, she was Dean of TSM Business School and professor at the University of Groningen, and spent 10 years with major MNC's, followed by >15 years at the University of Greenwich and City University Business School, London, UK. Her research and consultancy interests are in culture and values, business ethics, tacit knowledge transfer, the HE sector, branding and reputation, governance, international business. Her publications include the Journal of Management Studies, British Journal of Management, Journal of Business Ethics, Management International Review, Journal of Knowledge Management, IJTM and the Journal of Public Affairs.. University of Twente School of Management and Governance PO Box 217 7500AE Enschede, The Netherlands e-mail: [email protected] and Ashridge Business School, ACBAS Berkhamsted, Herts HP4 1NS, UK e-mail: [email protected]

Transcript of The case of HSBC’s Climate Partnership Programme · The case of HSBC’s Climate Partnership...

1

Talent management and effect of sustainability training

The case of HSBC’s Climate Partnership Programme

Maria Laura Franco-Garcia Senior research in environmental policy, CSTM Twente Centre of Studies in Technology and Sustainable Development at the University of Twente, The Netherlands. Former director of academic department and master's programme of sustainable development sciences in Tec de Monterrey, Mexico. PhD obtained in France on Environmental Sciences and Environmental Engineer from Mexico City. University of Twente Postbus 217; 7500 AE; Enschede, Netherland Tel : +31.53.4893203; Fax : +31.53.4894850; Email: [email protected] http://www.utwente.nl/cstm/ Matthew Gitsham Director of ACBAS, the Ashridge Centre for Business and Sustainability. Lecturer on Ashridge programmes (MBA and MSc in Sustainability) and Programme Director for the Integrating Corporate Responsibility programme. Elected member of the academic board of the European Academy of Business and Society. Member of the stakeholder advisory panel of Nexen, the Canadian Energy company. Frequent contributor to industry and academic conferences. Ashridge Berkhamsted Hertfordshire HP4 1NS United Kingdom [email protected] Tel. +44 1442843491 Fax. +44 1442841209 www.ashridge.org.uk Carla C.J.M. Millar Professor of International Marketing & Management at the School of Management & Governance of the University of Twente, and a Fellow of Ashridge Business School in the UK. Previously, she was Dean of TSM Business School and professor at the University of Groningen, and spent 10 years with major MNC's, followed by >15 years at the University of Greenwich and City University Business School, London, UK. Her research and consultancy interests are in culture and values, business ethics, tacit knowledge transfer, the HE sector, branding and reputation, governance, international business. Her publications include the Journal of Management Studies, British Journal of Management, Journal of Business Ethics, Management International Review, Journal of Knowledge Management, IJTM and the Journal of Public Affairs.. University of Twente School of Management and Governance PO Box 217 7500AE Enschede, The Netherlands e-mail: [email protected] and Ashridge Business School, ACBAS Berkhamsted, Herts HP4 1NS, UK e-mail: [email protected]

2

Talent management and effect of sustainability training

The case of HSBC’s Climate Partnership Programme

Abstract:

The objective of this paper is to link ‘talent development ’ with ‘sustainability’, and to do

this we have analysed empirically the unique dataset of 2608 learning evaluations of

HSBC’s global Climate Partnership programme (HCP). Europe was represented by 685

respondents and was our baseline for comparing the impact of the HCP with that for the

Global results. The HCP is part of HSBC’s business strategy aimed at embedding

sustainability and social responsibility across the corporation. Our quantitative data

analysis shows a positive impact of the sustainability training in terms of participants’

further commitment to the organisation and the development of leadership skills. We

developed our ‘Management sustainability training model’, and used Dunphy’s model

of Organisational change for corporate sustainability, ranking the HCP in phase 5

because of its effect on the development of talented people with a long‐term vision and

improvement in well being at work as well as with the communities involved. The link

between “talent development” and “corporate sustainability” provided a number of

important lessons, e.g. training programmes addressing societal problems in a project

applied approach enhance the employee’s commitment to the organisation, in particular,

if employees’ develop their leadership skills and count with managerial support for

application of knowledge post‐training.

Keywords: sustainability; talent development; social responsibility; Europe.

Bibliographical notes: are on the previous page

3

Talent management and effect of sustainability training The case of HSBC’s Climate Partnership Programme

1.Introduction

In the literature review, much research has been carried out in the area of talent

management. Currently however, it seems clear that some people give sustainability

training a special place in the development of talent, as much as saying that if one does

not acquire the ‚sustainability “bug” then one is not really ʺtalentʺ, and that training is a

way to acquire it. Unfortunately, at this particular regard, there is few evidence in

literature looking at the organisational effects of holding training programmes on

sustainability. Therefore the purpose of this paper was to explain the linkages between

talent management and sustainability training programmes by using the HSBC’s

training on Climate Partnership (HCP) programme.

Due to the growing need for human capital with the knowledge, abilities and behaviour

to lead the type of organisational change that answers the needs posed by the corporate

sustainability and corporate social responsibility principles, training in sustainability is a

‘must’ for future talent. This was also argued by Waddock (2007) based on her analysis

of the different corporate initiatives proposed or undertaken to face the social and

environment issues of sustainability inside business. She also stressed that market

pressure is driving the incorporation of sustainability in business strategy and that it is

foreseen that sustainability will take an even more crucial role in the future

The process and impact of developing talent were our ʺdrivingʺ issues and a

contribution of this paper is identifying indicators and components that are important in

the implementation of the training / coaching programme . These indicators are relevant

for talent investment, namely on what, how and where to invest in talent, especially at a

time when the economic crisis pushes managers to make short term decisions and for

some organisations talent development is put on the back burner.

However, the development of talent related to sustainability always pays back in the

long run (Lacy et al., 2009) , e.g. Hewlett‐ Packard has saved $25 million annually by

introducing energy saving programmes, through training and information.

Therefore, from an investment point of view, ʺsustainable talent developmentʺ needs a

clear set of criteria, indicators in order to be assessed. We identified some variables

which can be used as the set of criteria and put them together (section 4) in our model of

“management sustainability training model”.

4

The research question driving the elaboration of this paper was : What are the linkages

between talent management and training/learning programmes about sustainability

within organisations such as HSBC ?

Being HSBC our case study for this paper, we described in the following section the

programme “HSBC’s global Climate Partnership” (HCP) programme.

2. HSBC’s HCP programme as case study

The “green” reputation of HSBC has given it a haul of awards as well as much

recognition for their environmental and social achievements. Among them in 2009,

HSBC received the following recognitions: Number 1 financial institution for climate

strategy and carbon data disclosure and the British business awards 2009.

HSBC is a corporation headquartered in London, United Kingdom. They have 8000

offices across 88 countries and territories in Europe, The Asian‐Pacific region, North

America, Latin America and Middle East. They serve around 100 million individuals

and business consumers around the world. HSBC has used throughout its history

several policies and programmes for embedding social responsibility issues in the

corporation. They adopted the Equator principles in 2004 and each year HSBC issues

their sustainability report in which social and environmental indicators are collected to

show achievements to the shareholders and stakeholders groups.

As corporation, they have some 300,000 employees worldwide and according to Group

chairman, Stephen Green, “the institutional aim is to reward employees appropriately in

order to meet the long‐term goals of the business and in particular create an

environment where financial reward is not the only motivating factor” (Stephen Green,

2010). He also pointed out that one way to do it is through employees engaging in the

HSBC Climate Partnership (HCP) programme. The HCP programme forms part of a

corporate strategy to embed climate change and sustainability inside the HSBC

Corporation. Their report emphasizes their Corporate sustainability activities, and we

notice that in practice the concepts of Corporate sustainability and corporate social

responsibility are often used interchangeably (Waddock and Bodwell, 2007).

The HCP programme is executed through collaboration between HSBC, the Earthwatch

Institute, the Climate Group (international NGO), the Smithsonian Tropical Research

Institute and the World Wildlife Fund (WWF). The HCP was conceptually designed and

implemented to have an impact on the awareness level of HSBC employees towards

sustainability but also to enhance the talent development aspects which were the main

focus of our research. The HCP programme involved nearly 1000 HSBC employees and

has 3 learning formats: the Climate Change programme, 12 days with field work in a

remote area with only HSBC employees; the Local Volunteering Project (LVP), a 1 day

course in a regular location with mixed population of HSBC employees and

5

volunteering local participants; and The Online Programme, an any time, self‐

instruction programme using virtual educational systems and interaction platforms to

receive feedback.

In the particular case of the Climate Champion (CC) project, in 2009 484 HSBC

employees were trained as Climate Champions at 5 Regional Climate Centres in 40

countries. CC participants consider field work a way to put their knowledge into

practice through being involved in projects.

In their 2009 Sustainability report Sandy Flockhart stated: “77 per cent of HSBC’s people

feel actively encouraged to take part in employee volunteering initiatives, and those

who do are more engaged with HSBC” (HSBC, 2009). This evidence on perception inside

HSBC about the HCP programme was one of our reasons to link “talent management”

and “corporate sustainability” in our study.

While the programme was global in scope, the data available on Europe is most

complete and reliableReflecting the objectives set for the training and the availability of

data, our hypotheses are as follows:

Hypothesis 1: The HCP programme is an effective tool to link talent development

(leadership and influencing skills), organisational support and organisational

commitment with corporate sustainability in the European context.

Hypothesis 2: HCP managers’ stakeholders see an improvement in leadership skills in

the area of sustainability as an advantage in the labour market.

Hypothesis 3: HCP participants’ perceptions can be used to rank organisations in terms

of corporate sustainability by using the “Human Sustainability” indicators of Dunphy’s

model.

Our hypotheses were tested and confirmed through a statistical analysis of the empirical

data. Our model to address hypotheses 1 and 2 is described in the methodology section.

HCP participants’ and stakeholders’ perceptions were gathered by means of surveys.

The surveys were part of the instruments used during the training evaluation report

carried out by Malnick and Gitsham (2010). We focused our analyses on Europe, but in

the Findings section, we also covered the global perceptions.

3. Theoretical Framework

Our research interest was to embrace “talent” and “corporate sustainability and social

responsibility”, and for this we used Chowdhury’s (2002) definition, i.e. “talented

individuals are those being considered the spirits of an enterprise, being creative, rule

breakers and change initiators”. Four years later, Gitsham et al (2006) defined the

concept of leadership in their report of the “Developing the Global Leader of Tomorrow

6

project” which shows important similarities with Chowdhury’s concept. Gitsham et al

took the (United Nations Global Compact Principles for Responsible Management

Education (PRME) as a reference to frame their own concept of leadership, which is:

“leadership requires a range of discrete skills with the ability to be flexible and

responsive to change, the ability to find creative, innovative and original ways of solving

problems, the ability to balance shorter and longer term considerations”. The

characteristics shared between Chowdhury and Gitsham on – on the one hand – the

important business values as talent and leadership skills, and – on the other hand ‐ the

flexibility of the “talent” criteria to be adapted to the particular situation drove us to the

conclusion that in the context of “corporate sustainability and social responsibility”,

leadership skills can be considered as part of the abilities needed to develop talented

people in the HCP case.

As one of the components of the leadership skills‐set, it has been documented that for

the organisational change implicit in the initiatives of corporate sustainability and social

responsibility, leaders require to have outstanding influencing skills (Angus‐Leppan et

al., 2010). This is because they have the mission to embed sustainability principles

through the organisation (corporation) in different directions: vertical (upper and lower

positions); across organisational departments; at local or international scale; etcetera.

They have to deal in different stages with diversity of mindsets and remain assertive

and flexible to turn their colleagues perceptions ‘on message’ towards the sustainability

agenda.

Developing talented people to meet expectations about organisational change derived

from corporate sustainability initiatives calls for substantial investments from both sides,

employees and employers. Businesses have been investing in developing knowledge,

skills and attitudes (Lacy et al, 2009) through training and/or coaching programmes. This

has been explored widely within corporations (Waddock and Bodwell, 2007). Impact

evaluation of training to enhance talent and embed corporate sustainability has its

measures in different organisational criteria, like commitment and engagement

(Dunphy, 2003)

An increase in organisational commitment was introduced as one of the sustainability

programme’s intended impacts, in accordance with Dunphy (2003) whose explanation

was that the ethical component in the sustainability programmes raised the participants’

perceptions about their professional relationships within the organisation. Trevino et al

. (2000) showed this effect in a broader scenario and related it to ethical leadership; he

stated that people acting with ethical principles increased their reputation inside the

organisation, which improves to some extent the inter‐relationship and impact of the

employee commitment to the business. Moreover, Howard (2010) argued in his research

that “leaders who align personal purpose with organisational mission and societal need

can have a positive impact on the world and foster a new global ethics”. Therefore, we

7

take it as our assumption that both elements, the ethical content of the sustainability

programme and leaders pursuing and implementing ethical goals, can positively

influence the organisational commitment level.

D’Amato and Herzfeldt (2007) researched the influence of learning programmes and

organisational commitment on talent retention. They gathered empirical data by means

of a survey which was responded to across different generations of European managers.

They have shown that age can be an important factor when comparing organisational

commitment and talent retention because they found a lower commitment level within

the younger groups. Nevertheless that effect can be diminished if the young group has

access to individual development programmes. Hence, in the European context,

organisational commitment can be increased by facilitating individual development.

The main influential concepts in the connection between “talent management” and

“corporate sustainability” were researched individually in the literature and described

in next sub‐sections.

Corporate Sustainability and Corporate Social Responsibility

Due to the emerging issues in both corporate sustainability and CSR, interpretations

tend to be different. Therefore we have attempted to include the most common

definitions according to recognized sources. “Sustainable development seeks to draw

attention to ways of meeting needs of people without compromising the ability of future

generations to meet their own needs” (Burdtland, 1980). Corporate Sustainability has a

direct link to the business which promotes and embraces the “sustainability” aspects

inside the companies. When talking about “Corporate Social Responsibility”, the wider

impacts that companies have in society (Gitsham, 2008) are covered. Other terms used in

this context are “Corporate governance”, “corporate citizenship”, “Business ethics”,

“corporate accountability”, but all of these include social and environmental aspects to a

greater or lesser extent.

Corporate sustainability and corporate social responsibility initiatives increasingly call

for human capital with the knowledge, abilities and behaviour to lead organisational

change and this highlights the need for research on the links amongst talent

development, leadership skills and organisational commitment as these impact on

corporate sustainability initiatives. Most corporations use training/coaching

programmes to cope with the demand for “talented” human capital. As said before,

hence we try to provide a relevant framework to link training / coaching programmes

with talent development; in particular for training on sustainability.

Sandra Waddock’s (2008) defined “Corporate Responsibility” as “the ways in which

companies’ vision, values, and business models (ways of adding value) affect societies,

stakeholders, and the natural environment” and “corporate social responsibility” as the

ways in which companies act to explicitly benefit society.

8

In the broader definition of corporate citizenship/responsibility many large corporations

have begun implementing significant programmes. Some of these initiatives are still tied

to narrowly defined criteria of corporate social responsibility (CSR). However there are

other companies which initiatives are aligned beyond (Waddock, 2008) CSR because

they engage in managing their corporate (citizenship) responsibilities, i.e. including

stakeholder management, governance and ecological responsibilities’. This view is

supported by De Bruijn and Tukker (2002).

Why reporting sustainability issues or CSR?

The power of reporting and its tendencies in business are of growing corporate concern.

From the 1990’s (KPMG, 2005) corporations took on wider societal responsibilities. A

positive trend of the number of firms reporting on corporate sustainability was recorded

in 2005 with more than the half of the top 250 Fortune 500 companies, and 33% of the

top 100 companies in 16 countries having issued such reports (Waddock, 2008).

In the case of CSR, almost 3000 of the best known corporate brands have signed the UN

Global Compact (Berger et al., 2007). Furthermore, the number of companies using

reports in accordance with the global reporting initiative guidelines increased from

merely 20 in 1999 to over 1000 companies in 2006 (Nijhof, 2008). This evidence confirms

how relevant it is for businesses to disseminate their good practices in favour of

environmental and social aspects both inside and outside the business borders. Some

organisations want to make a real difference but there are also those whose main drivers

for reporting on sustainability activities are purely related to improving business

branding and reputation rather than authentic altruistic reasons.

The other relevant field to review in the literature is concept of talent management and

its components, some relevant works have been analysed in the following section.

Talent management

The subject of “Talent management” has been tackled from many different angles to

better understand the critical elements associated with the complex processes involved.

There are many definitions, and that by Blass (2007) refers to “additional processes or

opportunities that are made available to people in the organisation considered as

‘talent”.

The argument for talent management was put by Dunphy (2007) who saw it as a vital

element of business capital and as incorporating basic elements of: recruitment,

development and retention. In particular, retention has lately become very complex due

to the mobility potential of talented people. This, notwithstanding his argument that

when talented people have meaningful work, autonomy and are in professional

development, they do not want to leave their job. We see “meaningful” as, for many

people, encompassing an appreciation of the ethical corporate position of the company

9

and its interaction with stakeholders. Bringing about such an appreciation is therefore a

critical element of talent management.

]Bhatnagar (2008) argued that for organisational purposes “talent development” and

“leadership development” have similar supportive arguments and both are seen as

mechanisms for talent management. Additionally, looking at the latest empirical

developments, he refers to mentoring/coaching and training as the most popular

activities to address talent development. Leadership development as a concept emerging

from this talent development description is further developed in this section.

Due to the use of similar terms for the processes involved in “talent development” and

“human resources development”, it is relevant to mention that they can be different in

approach, goal and content. Furthermore, since “talent” inside business has been seen

as an adaptable term in the organisation for which it was meant, the concept becomes an

internal definition process per se, which is framed for a specific business at a particular

point in time. Because of the relevance of the concept some researchers tried to introduce

a locality bound concept. This was Blass’ research purpose (Blass, 2007) when surveying

1500 managers in 2002 across the UK where the output focus was “talent”, and was

defined by this UK managers group in terms of capability for “more pressure”,

“enhancing development opportunities” and “better promotion”. The concept reflected

the circumstances as valid for managers interviewed in the UK at that particular time.

Leadership development

For the purpose of this study, leadership skills were considered part of a number of

“talent” components HCP participants were asked to give their views about. Hence we

need to define “leadership” and “leadership development” from the literature. Berger

and Berger (2004) in their book on talent management gave an unique definition of

leader, and associate the term ‘leader’ with various levels of leader development They

described three types of leader development: emerging leader, developing leader and

strategic leader and we focused in the latter two because of their connection with our

analysis. Berger and Berger described the developing leader as “he/she is a great thinker

but may not be adept at mobilizing others or addressing practical consequences”. The

way to enhance his/her leadership is by a coaching process with involvement only of the

executive group facilitating bonds within the higher organisational levels. Another

relevant category is the “strategic leader” who should learn to think in a strategic way in

order to improve senior‐level bench strength and to retain valued talent. The

development approach, also named as “coaching” should be focused on providing a

sounding board and be building specific skills.

Another approach for framing leadership development is the one explained by Hannum

and Martineau (2008) who identified three different stages of development in terms of

expectations: improvement in skills or changes in behaviour of individual leaders;

10

improvement in the group or team effectiveness; and an enhanced ability to meet

organizational, community, system, government, or other broad goals. Each of these

expectations for the leaders requires specific coaching process. For our particular HCP

case, the ability to gain vision towards a broader goal suits the leader profile on

sustainability (Climate Change) projects.

Leadership development must be related to the improvement of leadership capability

and an improved organisational performance. Increasing leadership on the work floor

positively impacts (Alimo‐Metcalfe, 2001), the organisational situation.

Most companies do not find it easy to evaluate their leadership development’s impacts,

relationship and effectiveness, and commonly assess two or three categories of

subjective measures or behaviour indicators, e.g. allowing employees to give their own

perception about their change in behaviour. Hayward and Voller (2010) indicated that

few studies refer to theoretical models of evaluation. Instead, many studies focused on a

specific research approach, such as appreciative enquiry or a case study approach.

Next to a self identification as someone with leadership characteristics or in

development, it is important to measure the influencing ability mentioned by Berber

(2004) as someone being able to mobilize people and the more explicit leadership

definition which is an influence process, also related to Yukl (2001). Angus‐Leppan T. et

al (2010) added to this concept that when leadership is framed as a process of influence,

leadership become broader than management; this is because influence can come from

outside or inside the organization. This moves the concept from leadership to

relationships (Baker 2001) and some other authors define leadership as a dynamic

collaboration. This definition gives the concept in a more social meaning. Angus‐Leppan

and others discussed (2010) leadership in the CSR context and cited theoretical concepts

of Waldman and Siegel (2008) without empirical analysis; they assumed that the

personal values of a CSR leader are indicative of ethical and moral leadership styles. As

a consequence Angus‐Leppan framed and analysed the ethical and moral leadership

models for CSR context focused in the personal ethics of the denominated leader while

other researchers (Crossan and Hulland, 2002) have proposed that the new key

responsibility of leadership must help the organization stay aware of and adapt to the

rapid changes in its industry and answer to new stakeholder demands. At the end of

Augus‐Leppan narrative it was clear that there was a lack of research around CSR and

leadership, and that such lack of evidence to some extent also exists between corporate

sustainability and leadership.

As a consequence our research model will use some of the parameters described as self‐

perception of leadership, the influencing process and stakeholder’s involvement to

identify how a training programme with a high ethical content can increase leadership

skills as well as organizational commitment in participants. Furthermore we will relate

personal development and talent development where ethical values and leadership are

11

part of the programme; finally, our model will cover the implementation of

sustainability in corporations, through using Dunphy’s Model which is described next.

Dunphy’s model as theoretical framework

Dunphy’s model (2003) consists of two lists of criteria divided on the basis of ecological

and human indicators. Based on such criteria, organizations can be ranked from 1 to 6,

using phases of development. The “Rejection” Phase forms the first phase, and is

followed by the “Non‐responsiveness” phase. The third is the Compliance phase, and

Phase 4 is called Efficiency. Phase 5 is called “Strategic Proactivity” and the highest

phase (number 6) has the title “The sustaining Corporation”. This model has been used

to assess corporate sustainability policies and can allow further comparisons and

developments among organizations. In some cases, the model has to be adapted to the

particular needs and expectations of managers.

As previously mentioned there are two general criteria in this model: Ecological and

Human sustainability. We used the latter as our framework of analysis in terms of

management of the social performance, in the perception of HCP participants and

stakeholders. Those form the headings to follow and to be translated according to the

particular conditions of the organization. In our Findings and Discussion section we will

use Dunphy’s model to anchor and measure aspects related to organizational

commitment and engagement with the corporation, and personal satisfaction with the

ethical orientation of the organisation – in the perception of the HCP groups. We will

also elaborate on Dunphy’s characteristics for phases 5 and 6 related to our findings.

Bhatnagar’s (2008) model has some similarities with Dunphy’s. Bhatnagar used some of

the terms used by Dunphy but also added more emotional components like

“deployment of their engagement in “head and heart”, and “connecting with the people

who will help them to achieve their objectives”.

4. Methodology

Research design

As previously outlined, the aim of this study is to examine the link between “talent

development” and sustainability awareness/education programmes – in this case

through evaluating the effect of the HCP programme. We focused on the HCP

programme, as we had access to the data, and hence this provided an opportunity to test

the relationship quantitatively, next to carrying out literature research.

We looked at the HCP programme by first examining the analysis of the quantitative

research instruments (surveys) used to evaluate the training effects from the HCP

12

programme (Malnick and Gitsham, 2010) and the theoretical framework used in Malnick

and Gitsham’s report, i.e.: Dunphy’s Ecology Sustainability Criteria.

We carried out a further literature survey on theories and models interconnecting the

variables in the HCP surveys with our object of study in terms of the “linkage” between

“talent development” and the effect of programmes on sustainability.

We then decided to use Dunphy’s Human Development criteria set as a further research

framework for our study. The reason is that the HCP’s impacts can be directly related to

both Dunphy’s Human and Ecology indicators. Furthermore, the Human indicators

present a direct relationship with aspects of the “talent development”. Additionally, it is

relevant to mention that in his book (Dunphy, 2003) the author presented several case

studies which, like the HCP aim to embed corporate sustainability as organisational

change, and from which he developed his model.

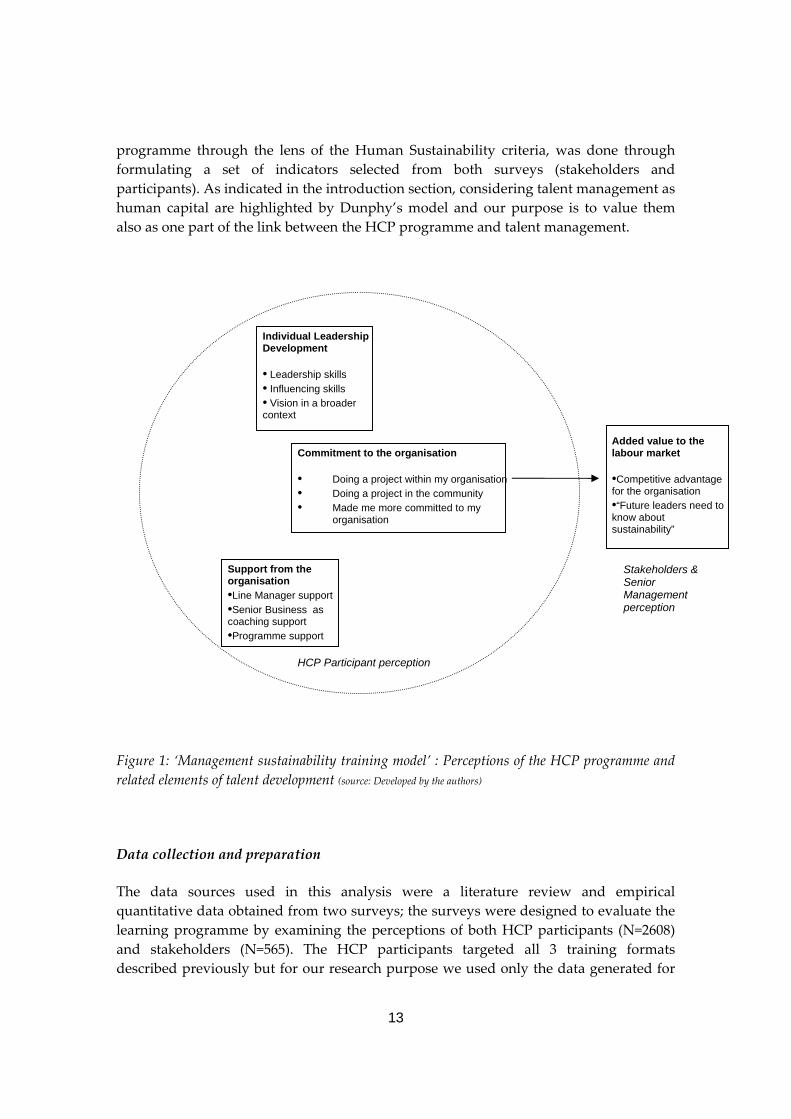

As part of our research we designed a model which is set out in Figure 1. This model is

used to test our two first hypotheses, mentioned in section 2: case HSBC description. The

model involves 3 main categories of the data set in relation to the HCP participants’

perception: individual development (a development or improvement in leadership

skills, influencing skills and obtaining a wider vision in a broader context); HSBC’s

organisational support (e.g. from line management, from senior business, from the

coach) to the participants for implementation of skills learnt; and commitment to the

organisation (doing a project within my organisation, doing a project in the community

and HCP made me more committed to my organisation) as a “recipient cell” of the 2

first categories. The variables used for the statistical analysis are listed with bullet points

below the title of each category.

For hypothesis 1, “The HCP programme is an effective tool to link talent development

(leadership and influencing skills), organisational support and organisational

commitment with corporate sustainability in the European context”, the statistical

analysis was limited to the categories inside the oval and the variables correlated per

category. Their inter‐connections were not the object of this study.

For hypothesis 2 “HCP managers’ stakeholders see an improvement in leadership skills

in the area of sustainability as an advantage on the labour market”, we used the

stakeholders’ data set (a result of the quantitative survey) and looked for numerical

evidence. The variables used for correlation were those outlining a competitive

advantage for the organisation and the one phrased as “Future leaders need to know

about sustainability”.

Tackling the third and last hypothesis, “HCP participants’ perceptions can be used to

rank organisations in terms of corporate sustainability by using the “Human

Sustainability” indicators of Dunphy’s model” which intends to generate

complementary information about Dunphy’s criteria and implications for the HCP

13

programme through the lens of the Human Sustainability criteria, was done through

formulating a set of indicators selected from both surveys (stakeholders and

participants). As indicated in the introduction section, considering talent management as

human capital are highlighted by Dunphy’s model and our purpose is to value them

also as one part of the link between the HCP programme and talent management.

Figure 1: ‘Management sustainability training model’ : Perceptions of the HCP programme and

related elements of talent development (source: Developed by the authors)

Data collection and preparation

The data sources used in this analysis were a literature review and empirical

quantitative data obtained from two surveys; the surveys were designed to evaluate the

learning programme by examining the perceptions of both HCP participants (N=2608)

and stakeholders (N=565). The HCP participants targeted all 3 training formats

described previously but for our research purpose we used only the data generated for

Added value to the labour market •Competitive advantage for the organisation •“Future leaders need to know about sustainability”

Commitment to the organisation • Doing a project within my organisation • Doing a project in the community • Made me more committed to my

organisation

Support from the organisation •Line Manager support •Senior Business as coaching support •Programme support

Individual Leadership Development • Leadership skills • Influencing skills • Vision in a broader context

HCP Participant perception

Stakeholders & Senior Management perception

14

the Climate Champion project group (N=325), as the other two groups also contained

non‐HSBC participants.

Our stakeholder perceptions survey addressed the management group inside HSBC and

the survey gathered opinions from Line managers of participants on the Climate

Champion programme, HSBC Climate Partnership senior business sponsors , HSBC

Partnership regional or country coordinators, the group or regional sustainability team

and other managerial groups inside HSBC.

Another criterion for breaking down the databases was to limit our analysis to the

European region only – although for reasons of completeness and comparison we also

included some ”global” values , reported according to statistical significance values.

Data Analysis

In order to find significant differences between the groups (regions), crosstabs and one

way ANOVA were applied to the participants and stakeholders databases. The

correlations of our variables (see our model in figure 1) were obtained by Pearson’s

coefficient values and verified by Spearman’s rho test. All statistical analyses were ran

by SPSS version 15 and procedures were kept in accordance with Pallant, J. 2008.

5. Findings

Europe and global, preliminary tests

Although as mentioned the regional focus of this study was Europe, given the HCP

global implementation, we report here the findings for both the European and the global

regions. We applied two tests to assess the significance values of our participants’

answers: one way ANOVA and crosstabs. The results obtained by crosstabs are in table

1. The “one way ANOVA” outputs shown for all the variables used in our model give a

significance of between 0.06 and 0.504. The threshold on the lower limit is 0.05. The

comparison of significance within regions by variable was also measured under Pos hoc

and the significance values were above the limit of >0.05.

In contrast, when testing the data set for stakeholder’s perceptions of our model’s

variables under the same conditions, the significance values were below the 0.05 limit

when comparing the two groups. The crosstabs outputs for the same data however gave

higher significance values by variable, in particular when the analysis was done

individually by region. But when analysing the data only for Europe, the Pearson sign 2

sided test lay between 0.63 and 0.265.

15

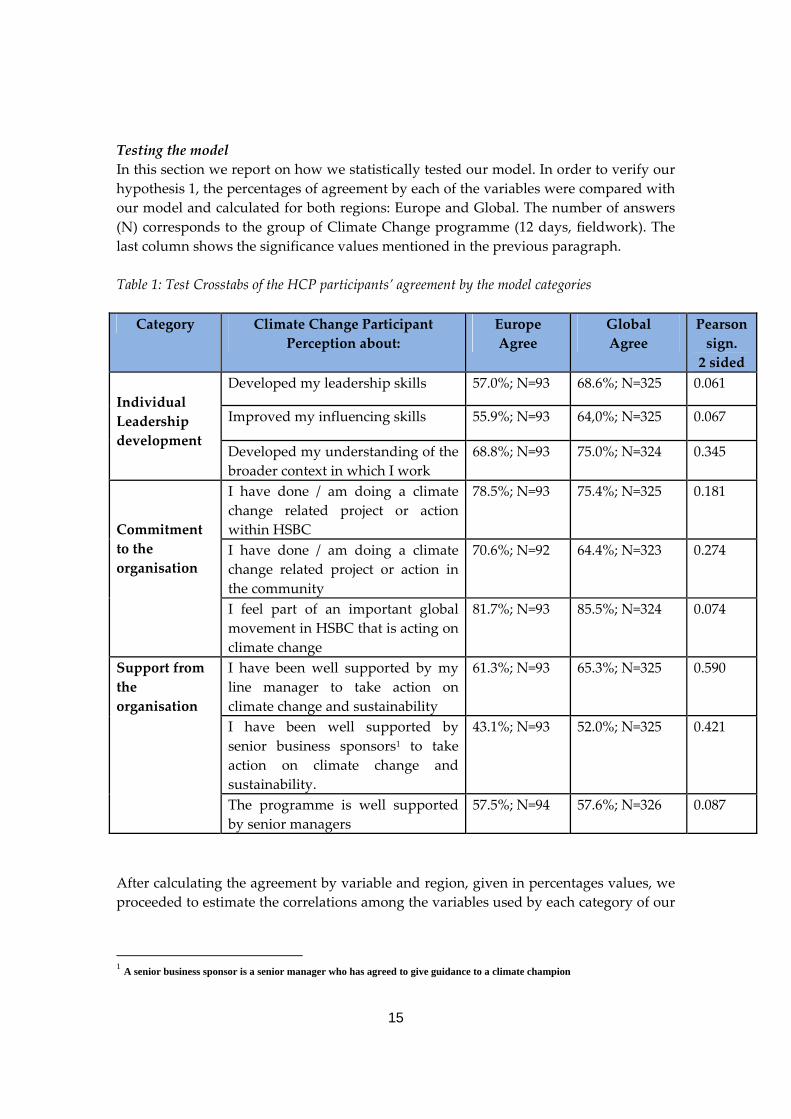

Testing the model

In this section we report on how we statistically tested our model. In order to verify our

hypothesis 1, the percentages of agreement by each of the variables were compared with

our model and calculated for both regions: Europe and Global. The number of answers

(N) corresponds to the group of Climate Change programme (12 days, fieldwork). The

last column shows the significance values mentioned in the previous paragraph.

Table 1: Test Crosstabs of the HCP participants’ agreement by the model categories

Category Climate Change Participant

Perception about:

Europe

Agree

Global

Agree

Pearson

sign.

2 sided

Individual

Leadership

development

Developed my leadership skills 57.0%; N=93 68.6%; N=325 0.061

Improved my influencing skills 55.9%; N=93 64,0%; N=325 0.067

Developed my understanding of the

broader context in which I work

68.8%; N=93 75.0%; N=324 0.345

Commitment

to the

organisation

I have done / am doing a climate

change related project or action

within HSBC

78.5%; N=93 75.4%; N=325 0.181

I have done / am doing a climate

change related project or action in

the community

70.6%; N=92 64.4%; N=323 0.274

I feel part of an important global

movement in HSBC that is acting on

climate change

81.7%; N=93 85.5%; N=324 0.074

Support from

the

organisation

I have been well supported by my

line manager to take action on

climate change and sustainability

61.3%; N=93 65.3%; N=325 0.590

I have been well supported by

senior business sponsors1 to take

action on climate change and

sustainability.

43.1%; N=93 52.0%; N=325 0.421

The programme is well supported

by senior managers

57.5%; N=94 57.6%; N=326 0.087

After calculating the agreement by variable and region, given in percentages values, we

proceeded to estimate the correlations among the variables used by each category of our

1 A senior business sponsor is a senior manager who has agreed to give guidance to a climate champion

16

model. The variables of the “Individual Leadership Development” category were

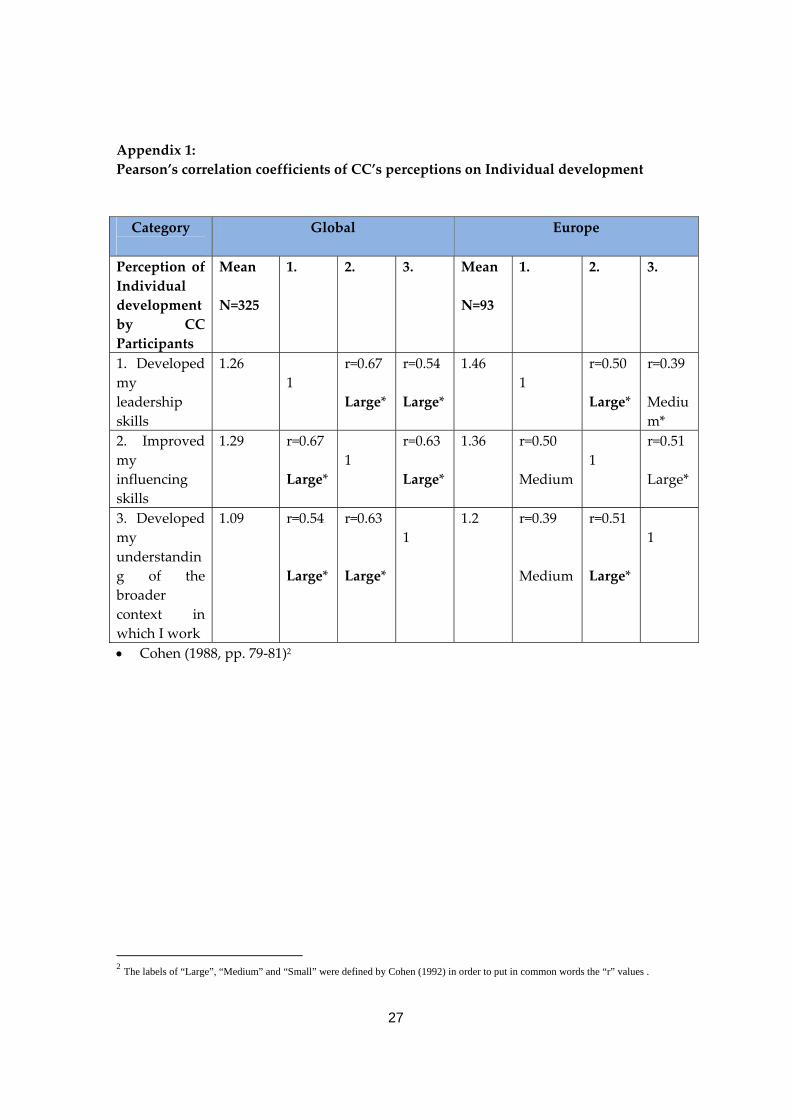

correlated “Bivariate” by Pearson and the results are shown in Appendix 1.

The same procedure was carried out to analyse the correlational relationship between

the variables chosen as indications of commitment to the organisation according to the

CC participants’ perceptions. Values for both, Global and Europe are displayed in

Appendix 2. The same analysis was done for the variables considered in our model as

“support” category and the results are presented in Appendix 3.

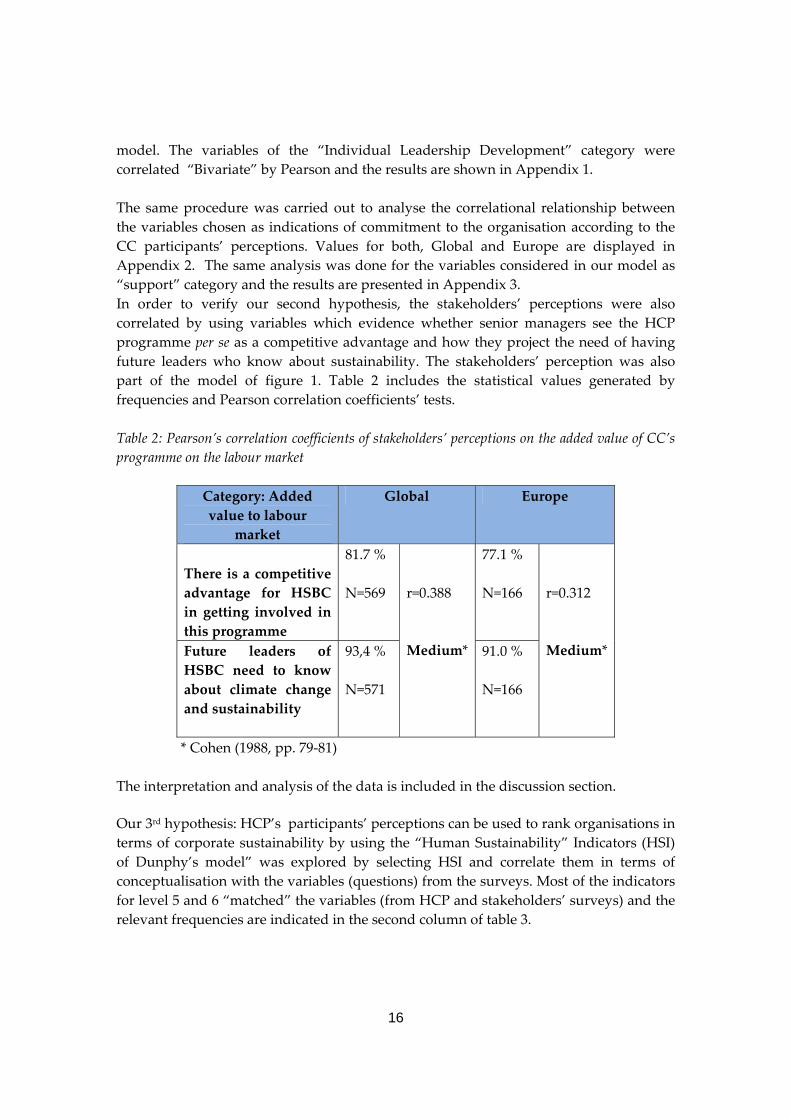

In order to verify our second hypothesis, the stakeholders’ perceptions were also

correlated by using variables which evidence whether senior managers see the HCP

programme per se as a competitive advantage and how they project the need of having

future leaders who know about sustainability. The stakeholders’ perception was also

part of the model of figure 1. Table 2 includes the statistical values generated by

frequencies and Pearson correlation coefficients’ tests.

Table 2: Pearson’s correlation coefficients of stakeholders’ perceptions on the added value of CC’s

programme on the labour market

Category: Added

value to labour

market

Global Europe

There is a competitive

advantage for HSBC

in getting involved in

this programme

81.7 %

N=569

r=0.388

Medium*

77.1 %

N=166

r=0.312

Medium* Future leaders of

HSBC need to know

about climate change

and sustainability

93,4 %

N=571

91.0 %

N=166

* Cohen (1988, pp. 79‐81)

The interpretation and analysis of the data is included in the discussion section.

Our 3rd hypothesis: HCP’s participants’ perceptions can be used to rank organisations in

terms of corporate sustainability by using the “Human Sustainability” Indicators (HSI)

of Dunphy’s model” was explored by selecting HSI and correlate them in terms of

conceptualisation with the variables (questions) from the surveys. Most of the indicators

for level 5 and 6 “matched” the variables (from HCP and stakeholders’ surveys) and the

relevant frequencies are indicated in the second column of table 3.

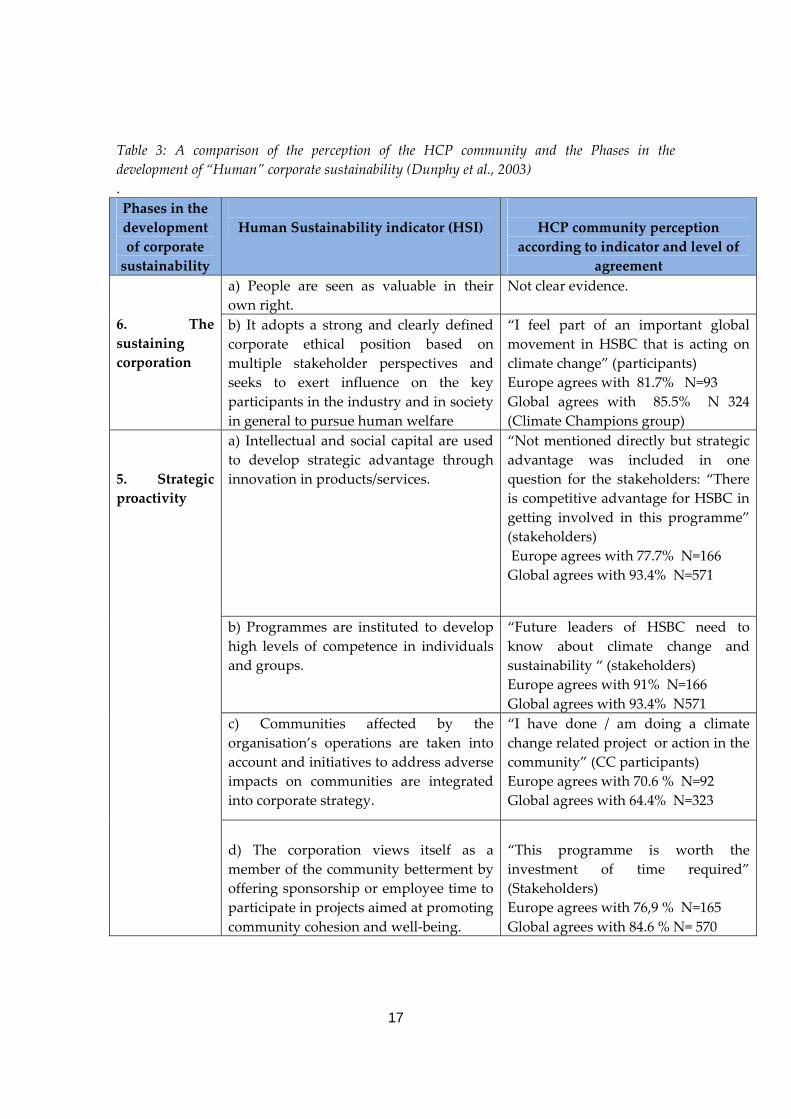

17

Table 3: A comparison of the perception of the HCP community and the Phases in the

development of “Human” corporate sustainability (Dunphy et al., 2003)

.

Phases in the

development

of corporate

sustainability

Human Sustainability indicator (HSI)

HCP community perception

according to indicator and level of

agreement

6. The

sustaining

corporation

a) People are seen as valuable in their

own right.

Not clear evidence.

b) It adopts a strong and clearly defined

corporate ethical position based on

multiple stakeholder perspectives and

seeks to exert influence on the key

participants in the industry and in society

in general to pursue human welfare

“I feel part of an important global

movement in HSBC that is acting on

climate change” (participants)

Europe agrees with 81.7% N=93

Global agrees with 85.5% N 324

(Climate Champions group)

5. Strategic

proactivity

a) Intellectual and social capital are used

to develop strategic advantage through

innovation in products/services.

“Not mentioned directly but strategic

advantage was included in one

question for the stakeholders: “There

is competitive advantage for HSBC in

getting involved in this programme”

(stakeholders)

Europe agrees with 77.7% N=166

Global agrees with 93.4% N=571

b) Programmes are instituted to develop

high levels of competence in individuals

and groups.

“Future leaders of HSBC need to

know about climate change and

sustainability “ (stakeholders)

Europe agrees with 91% N=166

Global agrees with 93.4% N571

c) Communities affected by the

organisation’s operations are taken into

account and initiatives to address adverse

impacts on communities are integrated

into corporate strategy.

“I have done / am doing a climate

change related project or action in the

community” (CC participants)

Europe agrees with 70.6 % N=92

Global agrees with 64.4% N=323

d) The corporation views itself as a

member of the community betterment by

offering sponsorship or employee time to

participate in projects aimed at promoting

community cohesion and well‐being.

“This programme is worth the

investment of time required”

(Stakeholders)

Europe agrees with 76,9 % N=165

Global agrees with 84.6 % N= 570

18

6. Discussion

The use of statistical tests like crosstabs and one way ANOVA did not indicate any

significant differences between ‘Europe’ and the ‘global region’ when analysing the

participant’s perceptions, see table 1 in findings section. The two tests gave values of

significance for all our model’s variables in the range of 0.06 – 0.504.

As far as the data set on the stakeholders perception is concerned, the significance value

was not larger than 0.05 for all the variables, when comparing Europe and the global

region. However, crosstabs outputs for the same data gave higher significance values by

variable, in particular when the analysis was done individually by region. Furthermore,

by analysing the data only for Europe, the Pearson result lay between 0.63 and 0.265.

In table 1 which shows our analysis regarding hypothesis 1, the level of agreement by

CC participants for Europe and the Global region was presented to illustrate how the

variables were ranked globally and to find relevant differences by variable in the

European region.

It was interesting to see the influence of the sample size on most of the percentages.

Leaving the sample effect aside, the data on the global scale indicated a higher level of

agreement than those in the European context. There were few exceptions to this

observation. Only for the variable (question) related to “I have done / am doing a climate

change related project or action in the community” the European perception was higher

than the global one, by 6%.

For Europe and Global, the highest percentage corresponded to the variable of “I feel

part of an important global movement in HSBC that is acting on climate change” with

81.7% of agreement by the CC programme participants. This reflects one of the most

important impacts of the CC programme (HCP in general) which is perceived by the

participants and can be interpreted as an indication of “commitment to the

organisation”.

Regarding the lowest degree of perception, it was for the variable related to the

“support” category (I have been well supported by senior business sponsors to take

action on climate change and sustainability (mentorship)) with correspondent

agreements for Europe and Global of 43.1% and 52% respectively. This highlighted one

of the potential improvements perceived by the participants in terms of support.

Actions at this regard should be taken by the HCP programme managers’ group.

19

OUR MODEL (hypothesis 1 and 2)

A) the Category of individual development

By using a Pearson correlation (see Appendix 1) for the CC group (training length of 12

days, fieldwork) the correlation of 3 variables related to the leadership development for

global (N=325) were scored as “Large” while for the European region (N=93) the value

of “r” for some of the correlations was between “Medium” and “Large” levels, “r” was

spread between 0.393 and 0.514. This indicates that we have made the right selection of

variables, in accordance with our model in figure 1, to assess individual development as

part of the HCP programme’s impacts.

The results above proved that the perceptions of the CC participants allow the

identification and matching of characteristics denoted in our literature discussion section

and bibliography as part of the individual development as the variables proved a

significant (r>0.507) correlations for Global region and for Europe (r>0.393) with the

improvement of leadership skills.

The HCP programme has been described by some of their senior managers as a

“supplementary opportunity for employees to deploy their abilities and develop a set of

skills on sustainability issues and apply them in projects which are socially responsible”.

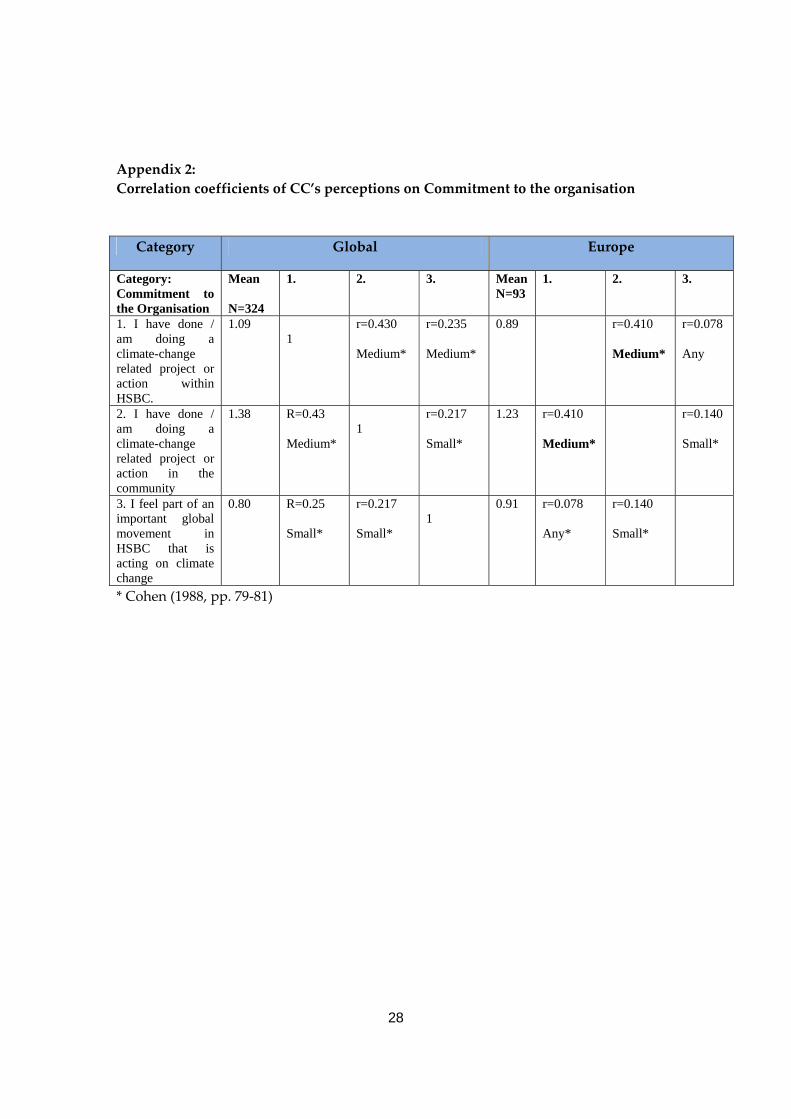

B) the category of commitment to the organisation

In the category of commitment to the organisation, we analysed the relationship

between 3 variables by using Pearson’s technique, see Appendix 2 for results. The

results gave both regions (global; N = 326 and Europe; N=94) rankings at “Medium” and

“Small” levels (Cohen, 1988). For the global region, the maximum value of “r” was 0.430

(N=326) and for Europe it was r=0.41 (N= 93). This result was for the correlation between

the variables: “I have done/am doing a climate change related project or action in the

community” and “I have done/am doing a climate change related project or action

within HSBC”. The rest of combinations for Europe and global had ‘Small’ level (r>0.1).

Only for the variable “I feel part of an important global movement” the correlation was

“any”, which means that the value of ʺrʺ was lower than 0.1. One way to explain this

result is to assume that the variables selection was not suitable for this category.

However, we can still argue that although the correlation between variables was not

highly enough ranked its representation in this category can be justified given its level of

agreement among participants with 81.7 % (N=93) in Europe and 85.5% (N=324) global.

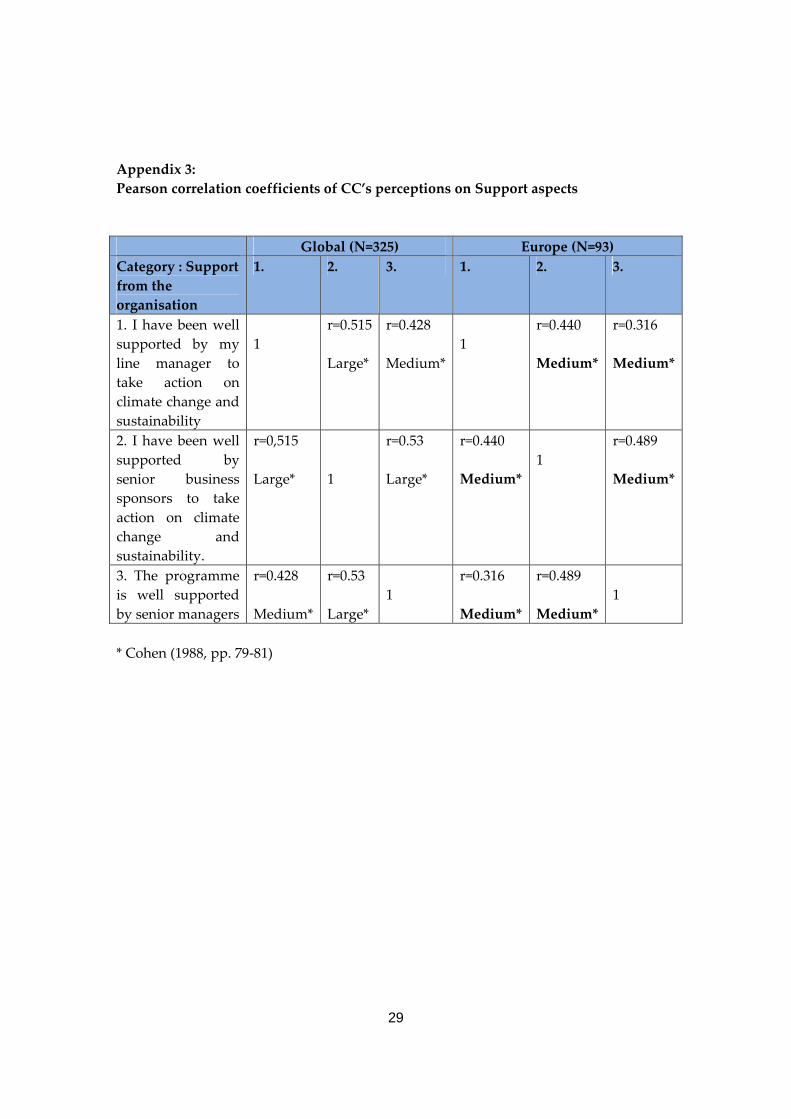

C) the Category of organisational support

The labels of “Large”, “Medium” and “Small” were defined by Cohen’s (1992) in order to put in common words the “r” values .

20

In the category of support provided for the implementation of the CC programme, the

levels of correlations fluctuated between “Medium” and “Large”, which means that

participants perceived the support in general at the same level for the 3 variables,

although the values in percentage (table 1) highlight low percentage of agreement

(43.1%; N=93; Europe) for the variable “I have been well supported by senior business

sponsors to take action on climate change and sustainability”. The low percentage value

gives us an indication of how some participants perceive mentorship as one of the

inconveniences during implementation – something that can be related to the answers

given in one of the open questions in the survey in which suggestions were asked for

improvements and it was indicated that in order to have a better understanding between

participants and mentors, the mentors should also take part in the CC programme

(Malnick and Gitsham (2010).

Some participants believe that in spite of developing their talent towards understanding

sustainability and increase their commitment to the organisation, they are facing

institutional barriers like not receiving enough support to implement what they learnt in

particular aspects. These include further support e.g. regarding access to resources (time,

budget and power) to engage in new projects in Climate Change or sustainability. This

indicates HSBC is maintaining a normal reality check.

Hence it will be a real challenge for the organisation to facilitate the complex process of

talent development, provide the conditions required and especially to marry individual

expectations with corporate reality and there are no guarantees that after developing

this special talent (and their skills set) the business will be ready and prepared to

welcome the “new” experience, expertise and skills, and be able to keep them on board.

Therefore, post training actions should accommodate the talent prepared for dealing

with sustainability issues, and improvement issues should be detected and dealt with.

This leads to one further question for further research: What are the barriers faced

during the implementation of training programmes on sustainability which represent

risks for talent retention?

THE LABOUR MARKET

As reported in the literature, one of the benefits that HSBC receives by making

sustainability issues part of their business strategy is “branding”. The organisation is

recognized as one of the leading banking groups due to its initiatives in embedding

sustainability issues in the business. This external, client, perception may also impact the

perception the employee has of his/her employer. And subsequently may lead to a

higher commitment of the employee to the organisation (Malnick & Gitsham, 2010). A

number of issues may contribute to this, such as the ethical motivation at CEO level to

have this vision and to engage in sustainability, market pressure, business responsibility

and the effect on branding and reputation. Working for a well branded company with

this sustainability label and being part of the leaders group in this respect give an

21

employee’s profile added value. Moreover, the HCP training/coaching also has value on

the labour market and as a consequence will bring more opportunities for the employee.

Bearing this in mind, in relation to our hypothesis 2, we reported in table 2 the

correlation of 2 variables which showed the stakeholders’ perception (mainly HSBC

senior managers) about the effect of the CC programme in the organisation.

Independently of the correlation values (r), which were “Medium” for both Europe and

the global regions regarding “Competitive advantage” and for “Future leaders need to

know about sustainability”, there was a high percentage of agreement among the

respondents for each variable (see table 2). This indicates that the perceptions of the

stakeholders gave an extra value to the CC programme which can be related to the

labour market.

DUNPHY’S MODEL (hypothesis 3)

As mentioned in the finding section, we made a selection of the Human Sustainability

Indicators (HSI) (table 3) which were connected with the HCP components. This was

done by choosing those variables which matched in terms of words used and context

with the HSI. And the purpose of the comparison was to give a general picture of to

what extend Dunphy’s HSI can be a framework to discuss the impact of

training/coaching programmes like HCP. In spite of the matches between HSI and our

study variables, there was no evidence that this was the case e.g. for “People are seen as

valuable in their own right”. This was reported in table 3 as ”No clear evidence”.

In a previous work (Malnik and Gitsham, 2010) Dunphy’s model was compared for the

Ecological component based in the interviews to HCP community members which were

related to Dunphy’s model. They reported two main conclusions after Dunphy’s

application:

“Within any group of Climate Champions, Senior Managers or other internal

stakeholders, there is evidence of a variety of different stages of response to

sustainability issues in HSBC. Many approaches and perspectives focus entirely on

efficiency and cost saving (phase 4), others on reputation, regulation and compliance

(phase 3) and a few on innovating new products and services (phase 5).”

“There is much to be gained from considering the different types of learning,

interventions and support that each stage of response may require, and reflecting on

what level response(s) the programme is aiming for”.

In our analysis, the perceptions of the HCP participants, senior managers and other

internal stakeholders were used as evidence. There were different stages of response to

HSI criteria as showed in figure 6. For each of the rows it can be seen what was used

from the HCP programme to “evaluate” the HSI in particular. The CC participants’

agreement (Europe (N=93) and Global (N=323)) and stakeholders’ ones (Europe (N=166)

and Global (N=571)) varied between 75% and 93%.

22

Although the level of agreement for such variables was high, we want to raise the point

here that Dunphy’s model remains as no more than a conceptual indication due to the

fact that there are no “acceptance” scales associated by indicator saying that effectively

the organisation fulfilled the conditions or not. Therefore, we have decided that

thresholds and procedures to be able to quantify the HSI are missing. For instance, what

does it mean, what ‘value’ should we put on the fact that the indicator of “c)

“Communities affected by the organisation’s operations are taken into account and

initiatives to address adverse impacts on communities are integrated into corporate

strategy” has an agreement of 64.4% in Europe and 70% in Global? Although there is a

clearer case for the rest of the HSI, in that their acceptance level was more in evidence as

the values are higher than 77%, representing indeed the majority of perceptions by

group, we still believe that further research is needed in this respect. For the moment the

only conclusion we can draw here is that as a whole and from the results analysis, we

rank the CC (HCP programme) in phase 5 under Dunphy’s HSI criteria.

Conclusions

Managing and developing talent is a hard task at the best of times. Currently however,

managers and leaders not only need to demostrate the required managerial knowledge

and skills required, but also to understand the requirements of sustainability.

We have been in the unique position of having access to the data of a survey in which

the perception of participants in the HSBC Climate Partnership (HCP) programmme and

their managers and other stakeholders in HSBC was researched. The survey focused on

three issues: personal development of the participants; their further commitment, or not,

to the organisation; and the support, or not, of the organisation for the implementation

of what was learnt during the programme. A fourth issue investigated whether

stakeholders perceived that the labour market would value talent that was

knowledgeable about sustainability.

Our analysis led to the following conclusions:

1. Participants felt that through the HCP programme they have developed the special

skills that are needed to master sustainability. For example, participants responded

positively to questions related to leadership, influencing skills, and a broader vision,

independent of the region in which they were based.

2. Climate Change training has led to an increase in HCP participants’ organisational

commitment to HSBC, as verified through internal as well as community variables.

23

3. Participants felt that the organisational efforts by their HSBC managers to support

implementation of what was learnt in the HCP programme was acceptable, but not

always as easily forthcoming as is suggested, and felt this was an issue that could be

improved.

4. Stakeholders in the labour market saw participation in HCP as valuable.

5. The Dunphy model is a useful vehicle to rank the HCP programme in terms of human

sustainability indicators, on the basis of the variables used in the participants’ and

stakeholders’ surveys. Most indicators proved to be measurable for our case study by

using the perceptions of HCPʹs participants and managers.

The literature reviewed provided insight into the factors that play a role in talent

management and talent development theories which can be adapted to the specific

organisation’s requirements and conditions. The model that we (t) developed (Figure 1:

‘Management sustainability training model’) can help organisations to create the

awareness for embedding sustainability within the organisation. This is because the

the organisation requires for people with knowledge, skills and behaviour for

implementing action on sustainability issues.

The link between talent development and sustainability corporate programmes has

proved to be a relevant research area where many questions have been raised and

further empirical research would prove valuable.

We trust that our findings may inspire organisations to invest in talent development

through training programmes on sustainability and projects associated with social

responsibility. Employees’ increased commitment to the organisation, enhanced by

sustainability training programmes, can improve the retention of these talented people

whom the organisation has (1) invested in, provided the organisational commitment (2)

and conditions are also favorable to facilitate (3) employees’ action on sustainability

projects.

Limitations of this research and further research

Our research was focused on the perceptional analysis of the employees who

participated in the HCP programme, such analysis gave us indications to validate the

variables used in our “Management sustainability training model”. Nevertheless, we

foresee, in one hand, that the model requires complementary validation by including

participants’ perceptions about their level of individual skills, prior to the HCP

programme. In another hand, we also consider that the same research is necessary to

carry out with a sample of HCP non‐participants (control group). By doing time series

analysis for both groups ‐HCP participants (experiment group) and control group‐ we

can elaborate stronger arguments about the linkage(s) between the HCP programme and

24

individual skills development. Certainly, the variables of the categories “Support from

the organisation” and “Commitment to the organisation” need to be considered in such

research design as contextual components of the category “individual leadership

development”.

Another potential niche for further research is the external dimension of the

“Management sustainability training model”, i.e. how organisations are ‐or should‐ be

prepared to accommodate the ”added value of skilled leaders in sustainability” into the

labour market and use it as a competitive advantage. Questions associated to identify

barriers and drivers of the external dimension of our model need further attention for

better understanding.

References

Alimo‐Metcalfe, B. and Lawler, J. (2001) “Leadership development in UK companies at

the beginning of the 21st Century; lessons for the NHS?”, Journal of Management Medicine,

London, MCB University Press, Vol. 3, No. 5, pp. 387‐404.

Angus‐Leppan, T., Metcalf, L. and Benn, S. (2010) “Leadership Styles and CSR Practice:

An Examination of Sensemaking, Institutional Drivers and CSR Leadership”, Journal of

Business Ethics, Vol. 93, pp. 189‐213.

Barker, R.A. (2001) “The nature of leadership”, Human Relations, Vol. 54, No.4, pp. 469‐

494.

Berger, L.A. and Berger, D.R. (2004) “The Talent Management Handbook”, Mc Graw

Hill, USA, pp. 314‐317.

Bhatnagar, J. (2008) “Managing capabilities for talent engagement and pipeline

development”, Industrial and commercial training, Vol. 40, No. 1, pp. 19‐28.

Blackman, D. and Kennedy, M. (2008) “Talent management: Developing or preventing

knowledge and capability”, Conference proceedings of the Organisational Learning,

Knowledge, and Capabilities Conference (OLKC 3) Retrieved 25th May 2008 from

http://www2.warwick.ac.uk/fac/soc/wbs/conf/olk/archive/olkc3/papers/contribution113.

pfg

Blass, E. (Ed.) (2007) “Talent management”, Chartered Management Institute and

Ashridge Consulting, UK, pp. 7‐10.

25

Chowdhury, S. (2002) “The talent Era: Achieving a High Return on Talent”, New Yersey:

FT/Prentice Hall, USA.

Crossan, M. and Hulland, J. (Ed) (2002) “Leveraging Knowledge Through Leadership of

Organisational Learning”, Oxford, New York.

Cohen, J.W. (1988) “Statistical power analysis for the behavioral sciences” (2nd ed),

Hillsdale, NJ: Lawrence Erlbaum Associates.

D’Amato, A. and Herzfeldt, R. (2003) “Learning orientation, organisational commitment

and talent retention across generations”, Journal of Managerial Psychology, Vol. 23, No. 8,

pp. 929‐953.

De Bruijn, T. and Tukker, A. (2002) “Partnership and Leadership”, Kluwer Academic

Publishers, Dordrect.

Dunphy, D., Griffiths, A. and Benn, S. (2003) “Organizational Change for Corporate

Sustainability: a guide for leaders and change agents of the future”, Rutledge Taylor and

Francis Group, UK.

Groves, K.S. (2007) “Integrating leadership development and succession planning best

practices”, Journal of Management Development, Vol. 26, No. 3, pp. 239‐260.

Hannum, K.M., Martineau, J.W. and Reinelt, C.(Ed) (2007) “The Handbook of

Leadership Development Evaluation”, Published by Jossey Bass, USA, pp. 228‐260

Hannum, K.M. and Martineau, J.W. (2008) “Evaluating the Impact of Leadership

Development”, Pfeiffer, USA, pp. 16‐18.

Haywards, I. and Voller, S. (2010) “How effective is leadership development? The

evidence examined”, The Ashridge Journal, summer 2010, pp. 8‐13.

Howard, A. (2010) Perspectives on practice: A new global ethic, Journal of Management

Development, Vol. 29, No. 5, pp506‐517.

HSBC Holding plc (2010) “Sustainability Report 2009”, Retrieved 15th August 2010 from

http://www.hsbc.com/1/PA_1_1_S5/content/assets/sustainability/100528_sustainability_r

eport_2009.pdf.

Gitsham, M.(Ed), Lenssen, G., Quinn, L., Bettingnies, H.C., Gomez, J., Oliver‐Evans, C,

Zhexembayeva, N., Fontrodona, J., Garcia Lombardia, P., Pillsbury, M., Van

Wassenhove, L., Roper, J., Glavas, A. and Cooperrider, D. (2006) “Developing the Global

Leader of Tomorrow”, Ashridge & EABIS, UK.

26

Lacy, P., Arnott J. and Lowitt, E. (2009) “The challenge of integrating sustainability into

talent and organisation, strategies: investing in the knowledge, skills, and attitudes to

achieve high performance”, Corporate Governance, Vol. 9., No. 4., pp 484‐494.

Lance, A. and Berger, D.R. (Ed) (2004) “The Talent Management Handbook”, Mc Graw

Hill, USA.

Malnick, T. and Gitsham, M. (2010) “External HCP Earthwatch Learning Evaluation‐Final

Report”, Ashridge Consulting, UK.

Nijhof, A., De Bruijn, T. and Honders, H. (2008) “Partnerships for corporate social

responsibility: a review of concepts and strategic options”, Management Decision, Vol. 46,

No. 1, 2008.

Pallant, J. (2008) “SPSS Survival Manual”, Mc Graw Hill, 3rd Edition.

Trevino, L. K., Hartman, L.P. and Brown., M. (2000) “Moral Person and Moral Manager:

How Executives Develop a Reputation for Ethical Leadership”, California Management

Review , Vol. 42, 128‐142.

Waddock, S. and Bodwell, C. (2007) “Total Responsibility Management: The Manual”,

Greeleaf Publishing, Sheffield, UK.

Waddock, S. (2008) “The difference makers, how social and institutional entrepreneurs

created the corporate responsibility movement”, Greenleaf Publishing Ltd, UK, pp.30‐

31.

Yukl, G. (2001) “Leadership in Organisations”, Prentice, Hall.

27

Appendix 1:

Pearson’s correlation coefficients of CC’s perceptions on Individual development

Category

Global Europe

Perception of

Individual

development

by CC

Participants

Mean

N=325

1. 2. 3. Mean

N=93

1. 2. 3.

1. Developed

my

leadership

skills

1.26

1

r=0.67

Large*

r=0.54

Large*

1.46

1

r=0.50

Large*

r=0.39

Mediu

m*

2. Improved

my

influencing

skills

1.29 r=0.67

Large*

1

r=0.63

Large*

1.36 r=0.50

Medium

1

r=0.51

Large*

3. Developed

my

understandin

g of the

broader

context in

which I work

1.09 r=0.54

Large*

r=0.63

Large*

1

1.2 r=0.39

Medium

r=0.51

Large*

1

Cohen (1988, pp. 79‐81)2

2 The labels of “Large”, “Medium” and “Small” were defined by Cohen (1992) in order to put in common words the “r” values .

28

Appendix 2:

Correlation coefficients of CC’s perceptions on Commitment to the organisation

Category Global Europe

Category: Commitment to the Organisation

Mean N=324

1. 2. 3. Mean N=93

1. 2. 3.

1. I have done / am doing a climate-change related project or action within HSBC.

1.09 1

r=0.430 Medium*

r=0.235 Medium*

0.89 r=0.410 Medium*

r=0.078 Any

2. I have done / am doing a climate-change related project or action in the community

1.38 R=0.43 Medium*

1

r=0.217 Small*

1.23 r=0.410 Medium*

r=0.140 Small*

3. I feel part of an important global movement in HSBC that is acting on climate change

0.80 R=0.25 Small*

r=0.217 Small*

1

0.91 r=0.078 Any*

r=0.140 Small*

* Cohen (1988, pp. 79‐81)

29

Appendix 3:

Pearson correlation coefficients of CC’s perceptions on Support aspects

Global (N=325) Europe (N=93)

Category : Support

from the

organisation

1. 2. 3. 1. 2. 3.

1. I have been well

supported by my

line manager to

take action on

climate change and

sustainability

1

r=0.515

Large*

r=0.428

Medium*

1

r=0.440

Medium*

r=0.316

Medium*

2. I have been well

supported by

senior business

sponsors to take

action on climate

change and

sustainability.

r=0,515

Large*

1

r=0.53

Large*

r=0.440

Medium*

1

r=0.489

Medium*

3. The programme

is well supported

by senior managers

r=0.428

Medium*

r=0.53

Large*

1

r=0.316

Medium*

r=0.489

Medium*

1

* Cohen (1988, pp. 79‐81)