The CAPM Strikes Back? An Investment Model with...

38

Transcript of The CAPM Strikes Back? An Investment Model with...

The CAPM Strikes Back?

An Investment Model with Disasters

Hang Bai1 Kewei Hou1 Howard Kung2 Lu Zhang3

1The Ohio State University

2London Business School

3The Ohio State University

and NBER

Federal Reserve Bank of New York

September 17, 2015

IntroductionInsight

An investment model with disasters replicates:

The failure of the CAPM in capturing the value premium in

�nite samples in which disasters are not materialized;

The relative success of the CAPM in samples in which

disasters are materialized

IntroductionLiterature

Early quantitative theories of cross-sectional asset pricing rely on

single-factor models:

Gomes, Kogan, and Zhang (2003); Carlson, Fisher, and

Giammarino (2004); Zhang (2005); Cooper (2006)

Recent quantitative theories introduce two-shock models:

Ai and Kiku (2013); Kogan and Papanikolaou (2013); Belo,

Lin, and Bazdresch (2014); Koh (2014)

Prior disaster models:

Rietz (1988); Barro (2006, 2009); Barro and Ursua (2008);

Gourio (2012); Gabaix (2012); Wachter (2013)

Outline

1 Stylized Facts

2 The Model

3 Failing the CAPM

4 The Beta Anomaly

Outline

1 Stylized Facts

2 The Model

3 Failing the CAPM

4 The Beta Anomaly

Stylized FactsThe CAPM regressions for the b/m deciles, July 1963�June 2014

Fama and French (1992, 1993)

L 2 3 4 5 6 7 8 9 H H−Lm 0.42 0.52 0.55 0.55 0.54 0.59 0.68 0.71 0.79 0.93 0.51tm 2.00 2.72 2.95 2.89 2.97 3.25 3.81 3.88 4.07 3.91 2.75α −0.12 0.01 0.06 0.06 0.08 0.13 0.24 0.27 0.32 0.39 0.51tα −1.28 0.15 0.92 0.57 0.83 1.45 2.27 2.28 2.92 2.50 2.26β 1.06 1.01 0.98 0.99 0.91 0.93 0.88 0.88 0.94 1.07 0.01tβ 40.79 46.28 34.55 29.35 27.50 28.34 22.89 17.53 20.85 15.44 0.07R2 0.86 0.92 0.90 0.87 0.83 0.85 0.78 0.76 0.76 0.66 0.00

Stylized FactsThe CAPM regressions for the b/m deciles, July 1926�June 2014

Ang and Chen (2007)

L 2 3 4 5 6 7 8 9 H H−Lm 0.57 0.68 0.68 0.68 0.73 0.76 0.77 0.92 1.03 1.09 0.52tm 3.24 4.09 4.05 3.67 4.12 4.04 3.86 4.43 4.36 3.82 2.60α −0.09 0.06 0.05 −0.01 0.08 0.07 0.05 0.18 0.21 0.14 0.23tα −1.27 1.20 0.89 −0.13 1.02 0.93 0.58 1.93 1.83 0.94 1.18β 1.00 0.95 0.97 1.06 1.00 1.05 1.09 1.14 1.27 1.45 0.45tβ 47.76 28.52 59.63 20.06 27.74 16.04 16.14 15.40 13.46 13.38 3.52R2 0.90 0.92 0.92 0.90 0.89 0.87 0.84 0.82 0.79 0.72 0.14

Stylized FactsThe value premium vs. MKT, July 1926�June 2014

−40 −20 0 20 40−40

−20

0

20

40

60

80

28Nov

29Oct

30Jun31May

31Jun

31Sep

31Dec

32Apr

32May

32Jul

32Aug

32Oct33Feb

33Apr

33May

33Jun33Aug

34Jan

37Sep

38Mar

38Apr

38Jun

39Sep

40May 74Oct

75Jan76Jan

80Mar87Jan87Oct

98Aug

08Oct

The market excess return

The v

alu

e p

rem

ium

−40 −20 0 20 40−40

−20

0

20

40

60

80

The market excess return

The v

alu

e p

rem

ium

Stylized FactsLarge swings in the stock market and the value premium

MKT H−L MKT H−L

November 1928 11.79 −0.41 August 1933 12.03 4.92October 1929 −20.07 7.57 January 1934 12.63 34.10June 1930 −16.25 −3.54 September 1937 −13.57 −10.90May 1931 −13.16 −3.09 March 1938 −23.80 −22.67June 1931 13.75 14.80 April 1938 14.49 8.76September 1931 −29.07 −5.03 June 1938 23.77 15.22December 1931 −13.42 −16.73 September 1939 16.94 56.61April 1932 −17.98 −2.85 May 1940 −21.93 −15.49May 1932 −20.44 3.61 October 1974 16.10 −13.58July 1932 33.47 45.73 January 1975 13.66 19.70August 1932 36.41 69.99 January 1976 12.16 15.04October 1932 −13.09 −12.97 March 1980 −12.90 −9.02February 1933 −15.06 −7.45 January 1987 12.47 −2.98April 1933 37.93 22.41 October 1987 −23.24 −1.21May 1933 21.36 45.01 August 1998 −16.08 6.33June 1933 13.05 10.29 October 2008 −17.23 −11.93

Stylized FactsThe CAPM's general problem, the beta anomaly,July 1963�June 2014, Fama and French (2006)

L 2 3 4 5 6 7 8 9 H H−Lm 0.51 0.52 0.52 0.56 0.66 0.54 0.68 0.53 0.62 0.63 0.12tm 3.64 3.46 3.11 3.15 3.46 2.67 3.06 2.25 2.33 1.92 0.43α 0.22 0.17 0.11 0.12 0.17 0.02 0.10 −0.08 −0.06 −0.18 −0.40tα 2.03 1.75 1.32 1.39 1.89 0.22 1.17 −0.83 −0.47 −0.90 −1.48β 0.57 0.68 0.81 0.87 0.98 1.03 1.14 1.22 1.35 1.61 1.04tβ 12.29 16.79 19.13 20.74 27.23 30.22 46.72 41.42 34.60 30.04 11.41R2 0.54 0.68 0.77 0.79 0.86 0.86 0.88 0.86 0.84 0.78 0.43

Stylized FactsThe CAPM's general problem, the beta anomaly,July 1928�June 2014, Fama and French (2006)

L 2 3 4 5 6 7 8 9 H H−Lm 0.57 0.63 0.64 0.73 0.82 0.71 0.80 0.72 0.82 0.81 0.24tm 4.80 4.51 4.23 4.33 4.36 3.55 3.69 2.99 3.04 2.59 0.94α 0.21 0.17 0.12 0.14 0.16 0.01 0.04 −0.13 −0.11 −0.26 −0.47tα 2.68 2.18 2.04 2.37 2.29 0.11 0.54 −1.53 −1.09 −1.80 −2.40β 0.57 0.74 0.82 0.93 1.05 1.12 1.22 1.36 1.49 1.70 1.12tβ 22.94 29.62 35.56 40.62 41.07 40.12 46.51 36.08 26.55 40.59 18.46R2 0.67 0.81 0.85 0.88 0.90 0.90 0.91 0.90 0.88 0.85 0.58

Outline

1 Stylized Facts

2 The Model

3 Failing the CAPM

4 The Beta Anomaly

The ModelHighlights

Embedding disasters into a standard investment model:

Rare disasters in consumption (productivity) growth

Asymmetric adjustment costs: Value �rms are more exposed

to disaster risk than growth �rms

Recursive preferences

In a sample without disasters, estimated betas only re�ect risk in

normal times, but the value premium is driven by disaster risk

The ModelRecursive utility

The pricing kernel:

Mt+1 = ι

(Ct+1

Ct

)− 1

ψ

U1−γt+1

Et

[U1−γt+1

]

1/ψ−γ1−γ

The ModelConsumption dynamics

Log consumption growth:

gct = g + gt

Normal states follow a discretized autoregressive process:

Five states: {g1, g2, g3, g4, g5}Transition matrix: pij ≡ Prob(gt+1 = gi |gt = gj):

P =

p11 p12 . . . p15p21 p22 . . . p25

......

. . ....

p51 p52 . . . p55

The ModelConsumption dynamics

Insert the disaster state, g0 = λD (disaster size < 0), and the

recovery state, g6 = λR (recovery size > 0)

Modify transition matrix:

P =

θ 0 0 . . . 0 1− θη p11 − η p12 . . . p15 0

η p21 p22 − η . . . p25 0...

......

. . ....

...

η p51 p52 . . . p55 − η 0

0 (1− ν)/5 (1− ν)/5 . . . (1− ν)/5 ν

η: disaster probability; θ: disaster persistence; ν: recoverypersistence

The ModelFirms, technology

Operating pro�ts:

Πit = (XtZit)1−ξK ξ

it − fKit

Aggregate productivity growth:

gxt = g + φgt

Firm-speci�c productivity:

zit+1 = (1− ρz)z + ρzzit + σzeit+1

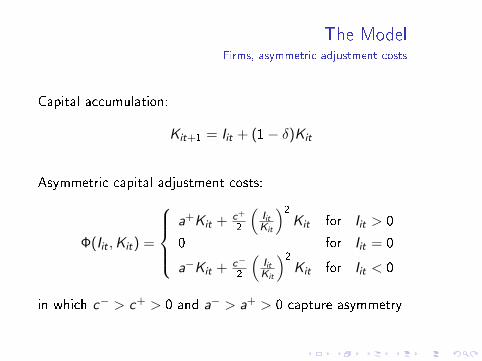

The ModelFirms, asymmetric adjustment costs

Capital accumulation:

Kit+1 = Iit + (1− δ)Kit

Asymmetric capital adjustment costs:

Φ(Iit ,Kit) =

a+Kit + c+

2

(IitKit

)2Kit for Iit > 0

0 for Iit = 0

a−Kit + c−

2

(IitKit

)2Kit for Iit < 0

in which c− > c+ > 0 and a− > a+ > 0 capture asymmetry

The ModelFirms, value maximization

Source of funds constraint:

Dit = Πit − Iit − Φ(Iit ,Kit)

Value maximization:

Vit = max{χit}

(max{Iit}

Dit + Et [Mt+1V (Kit+1,Xt+1,Zit+1)] , sKit

),

in which s ≥ 0 is the liquidation value parameter

Entry and exit, delisting return, reorganizational costs

Outline

1 Stylized Facts

2 The Model

3 Failing the CAPM

4 The Beta Anomaly

Failing the CAPMCalibration, preferences

Parameters Value Description

ι 0.99035 Time discount factorγ 5 The relative risk aversionψ 1.5 The elasticity of intertemporal substitution

Failing the CAPMCalibration, consumption dynamics

Parameters Value Description

g 0.019/12 The average consumption growthρg 0.6 The persistence of consumption growthσg 0.0025 The conditional volatility of consumption growth

η 0.028/12 The disaster probabilityλD −0.0275 The disaster sizeθ 0.9141/3 The disaster persistenceλR 0.0325 The recovery sizeν 0.95 The recovery persistence

Failing the CAPMThe impulse response of log consumption to a disaster shock

mimics that in Nakamura, Steinsson, Barro, and Ursua (2013)

0 5 10 15 20 25−0.25

−0.2

−0.15

−0.1

−0.05

0

Failing the CAPMCalibration, technology

Parameters Value Description

ξ 0.65 The curvature parameter in the production functionδ 0.01 The capital depreciation ratef 0.005 Fixed costs of productionφ 1 The leverage of productivity growth

z −9.75 The long-run mean of log �rm-speci�c productivityρz 0.985 The persistence of log �rm-speci�c productivityσz 0.5 The conditional volatility of log �rm-speci�c productivity

a+ 0.035 Upward nonconvex adjustment costsa− 0.05 Downward nonconvex adjustment costsc+ 75 Upward convex adjustment costsc− 150 Downward convex adjustment costs

s 0 The liquidation value parameterκ 0.25 The reorganizational cost parameter

R −0.425 The delisting return

Failing the CAPMThe CAPM regressions for the b/m deciles, no-disaster samples

G 2 3 4 5 6 7 8 9 V V−Gm 0.77 0.76 0.75 0.75 0.75 0.77 0.80 0.85 0.95 1.21 0.45tm 18.58 18.43 18.09 17.98 18.11 18.57 19.32 20.52 22.55 24.99 7.10α −0.01 −0.02 −0.06 −0.11 −0.10 −0.08 −0.02 0.08 0.23 0.46 0.47tα −0.07 −0.24 −0.73 −1.26 −1.24 −0.95 −0.18 0.99 2.83 5.02 3.71β 0.95 0.96 1.00 1.05 1.05 1.05 1.00 0.95 0.89 0.92 −0.03tβ 11.07 10.87 11.32 11.98 11.89 11.88 11.47 10.95 9.85 9.00 −0.24R2 0.11 0.12 0.12 0.14 0.14 0.13 0.13 0.11 0.10 0.08 0.00

Failing the CAPMThe CAPM regressions for the b/m deciles, disaster samples

G 2 3 4 5 6 7 8 9 V V−Gm 0.74 0.74 0.73 0.74 0.75 0.77 0.81 0.86 0.96 1.19 0.45tm 13.83 13.61 13.43 13.24 13.15 13.07 13.10 13.07 13.17 13.61 5.83α 0.08 0.06 0.04 0.01 −0.00 −0.03 −0.05 −0.09 −0.13 −0.13 −0.21tα 1.38 1.09 0.76 0.32 −0.08 −0.53 −0.82 −1.15 −1.40 −1.38 −1.72β 0.82 0.85 0.87 0.90 0.94 1.00 1.08 1.19 1.37 1.64 0.82tβ 18.82 23.74 28.64 33.03 33.72 30.60 26.47 20.63 16.00 18.05 6.82R2 0.45 0.47 0.49 0.50 0.52 0.55 0.57 0.60 0.64 0.65 0.24

Failing the CAPMValue is more exposed to disaster risk than growth

−20−10

0

0

10

20

0

10

20

30

zCapital −20−10

0

0

10

20

0

10

20

30

zCapital

Failing the CAPMImpulse responses of risk and risk premiums for value and

growth deciles to a disaster shock

0 5 10 15 20 250

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0 5 10 15 20 25−1

0

1

2

3

4

5

Failing the CAPMNonlinearity in the CAPM regressions

−20 0 20 40 60−40

−20

0

20

40

60

The v

alu

e p

rem

ium

The market excess return

Failing the CAPMNonlinearity in the pricing kernel

−20 0 20 40 600

5

10

15

20

25

The p

ricin

g k

ern

el

The market excess return

Failing the CAPMComparative statics

λD θ η ν λR

−0.025 −0.03 0.955 0.985 0.13% 0.33% 0.935 0.965 2.75% 3.75%Disaster samples

m 0.34 0.55 0.29 0.47 0.42 0.46 0.46 0.43 0.45 0.44tm 4.78 6.75 4.49 5.62 5.72 5.78 5.94 5.61 5.83 5.70α −0.22 −0.20 −0.21 −0.16 −0.21 −0.21 −0.20 −0.22 −0.21 −0.21tα −1.98 −1.51 −2.08 −1.33 −1.60 −1.89 −1.66 −1.80 −1.75 −1.78β 0.77 0.86 0.74 0.77 0.79 0.86 0.85 0.78 0.85 0.81tβ 6.65 7.11 6.56 7.39 6.01 7.80 6.74 6.75 6.74 7.04

No-disaster samples

m 0.33 0.54 0.28 0.55 0.42 0.46 0.45 0.43 0.44 0.45tm 5.63 8.08 5.24 7.89 6.74 7.29 7.09 6.90 6.99 7.06α 0.24 0.71 0.07 0.86 0.43 0.50 0.49 0.45 0.47 0.47tα 2.14 4.96 0.67 5.66 3.38 3.97 3.88 3.52 3.72 3.77β 0.12 −0.19 0.32 −0.33 −0.02 −0.05 −0.05 −0.02 −0.04 −0.04tβ 0.89 −1.35 2.56 −2.32 −0.13 −0.35 −0.41 −0.19 −0.31 −0.34

Failing the CAPMComparative statics

a+ a− c+ c− f

0.025 0.045 0.035 0.065 50 100 100 200 0 0.015Disaster samples

m 0.48 0.29 0.25 0.47 0.37 0.49 0.39 0.46 0.47 0.40tm 6.57 3.75 3.73 5.97 4.64 6.59 5.25 5.90 6.30 4.86α −0.25 −0.23 −0.21 −0.23 −0.24 −0.20 −0.21 −0.22 −0.21 −0.22tα −1.91 −2.05 −1.66 −1.82 −2.04 −1.61 −1.82 −1.80 −1.71 −1.89β 0.96 0.64 0.61 0.89 0.73 0.90 0.76 0.85 0.87 0.75tβ 6.42 6.19 4.32 6.77 7.23 6.57 6.57 6.85 6.61 7.25

No-disaster samples

m 0.45 0.28 0.22 0.46 0.38 0.49 0.39 0.46 0.45 0.40tm 8.48 4.24 3.84 7.32 5.54 8.42 6.35 7.29 7.78 5.81α 0.63 0.14 0.26 0.49 0.27 0.62 0.41 0.49 0.54 0.31tα 5.39 1.10 2.16 3.83 1.98 5.12 3.27 3.89 4.42 2.31β −0.23 0.16 −0.04 −0.04 0.13 −0.17 −0.02 −0.04 −0.10 0.11tβ −1.71 1.20 −0.32 −0.31 0.96 −1.25 −0.15 −0.36 −0.77 0.76

Failing the CAPMComparative statics

s κ R γ ψ

0.15 0.3 0 0.5 −0.3 −0.55 3.5 6.5 1 2Disaster samples

m 0.20 −0.03 0.45 0.45 0.47 0.44 0.18 0.57 −0.06 0.51tm 2.95 −0.28 5.79 5.87 6.08 5.64 2.61 7.19 −2.67 5.74α −0.27 −0.35 −0.21 −0.21 −0.19 −0.23 −0.23 −0.11 −0.29 −0.18tα −2.72 −3.80 −1.72 −1.73 −1.58 −1.89 −2.48 −0.81 −10.00 −1.60β 0.63 0.48 0.82 0.83 0.83 0.83 0.75 0.67 1.74 0.67tβ 7.06 6.57 6.84 6.80 6.75 6.85 6.24 5.29 10.34 8.43

No-disaster samples

m 0.27 0.10 0.44 0.45 0.46 0.44 0.15 0.60 −0.07 0.50tm 4.37 1.68 7.07 7.11 7.27 7.03 3.18 8.47 −3.15 7.10α 0.34 0.20 0.47 0.47 0.48 0.47 −0.12 0.96 −0.31 0.82tα 2.78 1.74 3.68 3.69 3.76 3.65 −1.64 5.87 −11.70 5.23β −0.09 −0.13 −0.03 −0.03 −0.03 −0.03 0.51 −0.34 1.98 −0.30tβ −0.66 −1.01 −0.22 −0.23 −0.22 −0.25 4.35 −2.45 17.67 −2.27

Outline

1 Stylized Facts

2 The Model

3 Failing the CAPM

4 The Beta Anomaly

The Beta AnomalyDeciles formed on rolling market betas, disaster samples

L 2 3 4 5 6 7 8 9 H H−Lm 0.76 0.78 0.81 0.83 0.85 0.86 0.86 0.85 0.83 0.79 0.04tm 13.72 14.09 14.04 13.89 13.55 13.41 13.08 12.65 11.79 11.50 0.53α 0.04 0.06 0.06 0.04 0.01 −0.01 −0.04 −0.08 −0.16 −0.17 −0.21tα 0.69 1.29 1.17 0.82 0.29 −0.05 −0.49 −0.89 −1.45 −2.10 −1.73β 0.90 0.90 0.95 0.99 1.04 1.08 1.12 1.16 1.23 1.20 0.30tβ 19.75 25.57 33.62 34.40 31.60 25.92 21.23 18.56 15.11 17.35 2.49R2 0.53 0.53 0.54 0.55 0.56 0.57 0.58 0.59 0.60 0.61 0.06

The Beta AnomalyDeciles formed on rolling market betas, no-disaster samples

L 2 3 4 5 6 7 8 9 H H−Lm 0.80 0.82 0.84 0.85 0.85 0.86 0.84 0.82 0.79 0.74 −0.06tm 20.12 20.36 20.48 20.45 19.82 20.00 19.58 18.98 18.24 16.65 −0.93α 0.01 0.12 0.17 0.19 0.15 0.16 0.11 0.03 −0.09 −0.42 −0.44tα 0.16 1.55 2.15 2.28 1.75 1.88 1.30 0.39 −1.06 −4.98 −3.49β 0.97 0.86 0.82 0.82 0.86 0.86 0.90 0.97 1.08 1.43 0.47tβ 11.79 10.20 9.50 9.27 9.30 9.15 9.72 10.37 11.67 15.74 3.49R2 0.13 0.10 0.09 0.09 0.09 0.09 0.10 0.11 0.14 0.23 0.01

The Beta AnomalyMeasurement errors in rolling market betas

ConclusionSummary

An investment model with disasters replicates the failure of the

CAPM in capturing the value premium in no-disaster samples, and

its relative success in disaster samples

The beta anomaly largely due to measurement errors in pre-ranking

rolling betas

A �rst step in integrating the disaster literature with

investment-based asset pricing