The Brazilian water transportation sector Regulation...

55

24/10/11 The Brazilian water transportation sector Regulation overview SEP Mission – Shanghai Fernando Antonio Brito Fialho Director-General of ANTAQ

Transcript of The Brazilian water transportation sector Regulation...

24/10/11

The Brazilian water transportation sectorRegulation overview

SEP Mission – Shanghai

Fernando Antonio Brito FialhoDirector-General of ANTAQ

24/10/11

Area total 8.514.876 Km²

Estados 27

Litoral 8.511 Km

População 192 milhões

PIB 2010 US$ 2.194Fonte: MDIC MilhõesAnuário Estatístico-2010

Cobertura vegetal = 28,3%

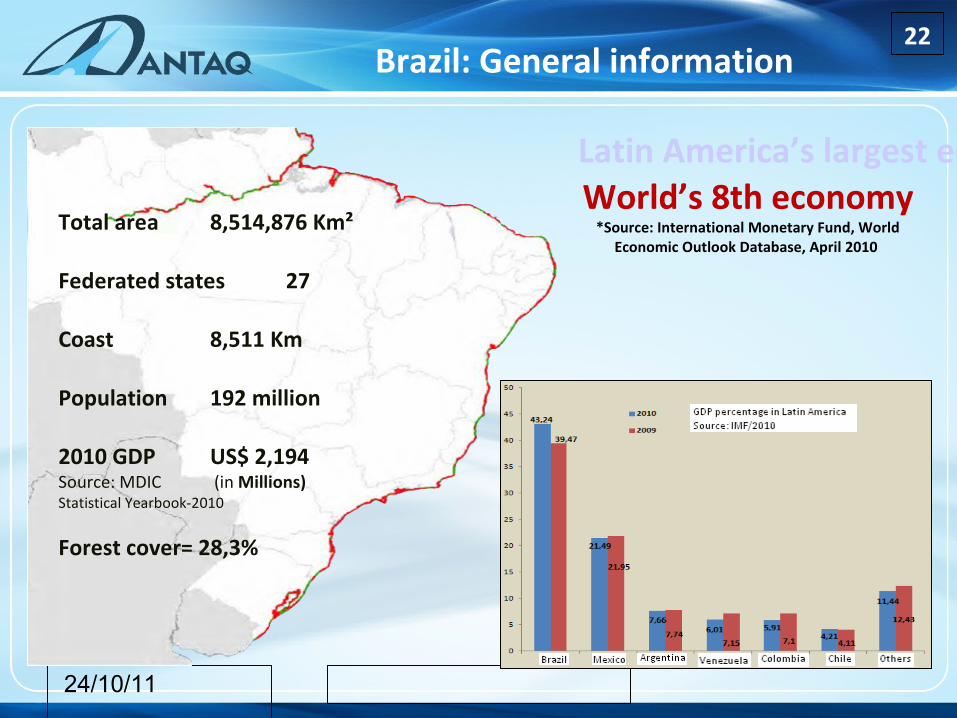

Brazil: General information

Total area 8,514,876 Km²

Federated states 27

Coast 8,511 Km

Population 192 million

2010 GDP US$ 2,194Source: MDIC (in Millions)Statistical Yearbook-2010

Forest cover= 28,3%

22

Latin America’s largest economyWorld’s 8th economy

*Source: International Monetary Fund, World Economic Outlook Database, April 2010

24/10/11

• Created by Act No. 10,233 of June 5th, 2001.

• Act 10,233/01: • Re-structures water and land transportation• creates CONIT, ANTAQ, ANTT and DNIT

• Connected to the Ministry of Transports – MT – and the Ports Secretariat – SEP.

• Regulation, inspection and harmonization of port and water transportation activities

ANTAQ: institutional aspects33

24/10/11

PortAuthority

(concession)

BrazilianWater

TransportInfrastructure

PrivateTerminals

(authorization)

ShippingCompanies

(authorization)

RegulationInspection

RegulationInspectionAuthorization

AdministrativeDelegation

Leases(sub-concession)

Federal Government

State Structure44

24/10/11

Role of the regulator55

24/10/11

BRAZILLease

(sub-concession)

Authorization

Exclusive private ports

Mixed private ports

Small Public Port Installation

Tourist private ports

Cargo Transshipment Station

Organized Port – delegated to a Port Authority by the Union

Port facilities – Act 8,630/9366

24/10/11

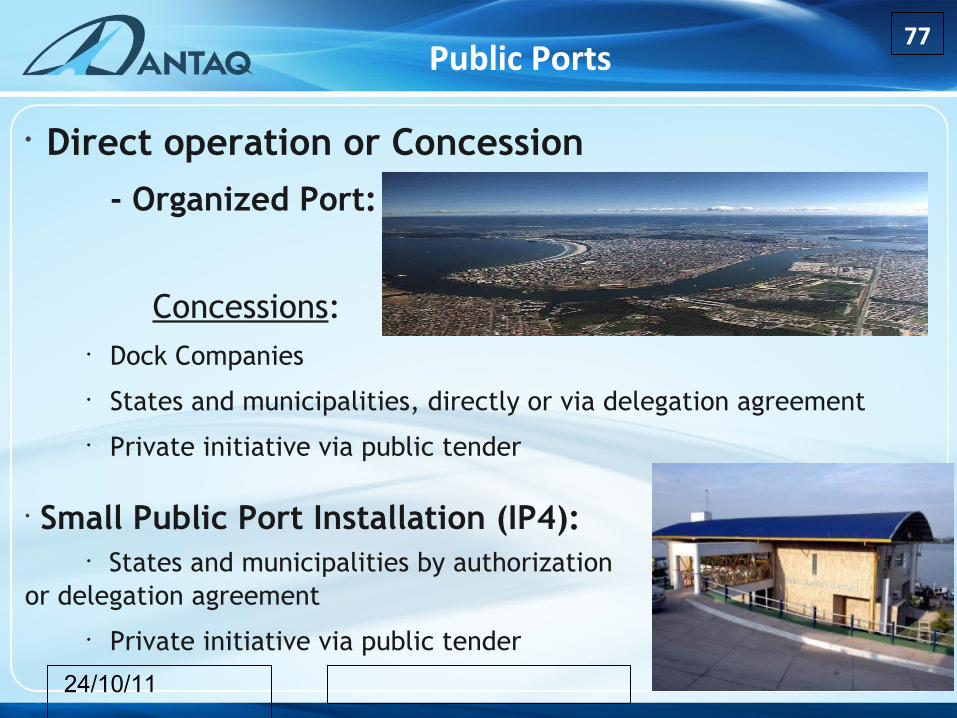

• Direct operation or Concession- Organized Port:

Concessions:• Dock Companies• States and municipalities, directly or via delegation agreement• Private initiative via public tender

• Small Public Port Installation (IP4): • States and municipalities by authorization

or delegation agreement• Private initiative via public tender

Public Ports77

24/10/11

• To Private Companies Legal Basis:

• Act 8,630/93 and Act 8,666/93• Decree 4,391/02 and Decree 6,413/08 (out of National

Development Plan: CDRJ, CDC, CODESP, CDP, CODOMAR, CODERN and CODESA)

• ANTAQ Resolution 55 (under review) and Brazilian Court of Audit Normative Instruction 27/98

• Decree 6,620/08

Peculiarities:

Assignment of use of public asset Appraisal of the undertaking Period of up to 50 years Reversibility of assets to the Union Labor provided by OGMO (port labor management body)

Leasing (sub-concession) of Areas within the Organized Port

88

24/10/11

Legal Basis:

Act 8,630/93; Resolution 1,660/10; and Decree 6,620/08

Peculiarities:

- Types of Facilities

- Period of up to 50 years (Resolution 1,660/10) - Possibility to operate in consortium - Authorization for shipyard and offshore support bases

Exclusive Use – to handle own cargo

Mixed Use – to handle third party and own cargo

By Authorization to the Private Initiative

99

24/10/11

Tender for the private initiative

Granted use of organized ports to public or private companies through public tender

Concession period of 25 years, renewable for an equal period of time

ANTAQ in charge of tender, following the guidelines in General Concessions Plan (PGO)

Study of modeling of intended use in course

Legal Basis:

• Decree 6,620/08• Acts 8,630/93 and 8,987/95• Administrative Decree SEP 108/10

Peculiarities:

1010

Concession of organized ports to the private sector

10

24/10/11

Direct Concession

Delegation Agreement (Ministry of Transports – Government of

Maranhão/EMAP)

Concession to the State of Santa Catarina (state)

Concession of Organized Port through tender ?

Authorization by Contract of Adherence

Private Concession

Types of port operation – Act 8,630/931111

24/10/11

Planning Appreciation

• PNLT – National Transport Logistics Plan• PGO – General Port Concession Plan• Update of Public Ports Development and Zoning Plans• Water Transport General Concession Plan – Ports and Waterways• PNLP – National Port Logistics Plan• PNIH – National Water Transport Integration Plan• Updated Reliable Statistics

Investments to Improve Port Management

• Port Without Paper• Vessel Traffic Management System

Appreciation of Multi-Modal Integration

• Incentive to Cabotage• Investment in Waterways

Change of Behavior Regarding the Environment

• Port Licensing• Shift in Waterways

Improvement of Regulatory Framework

• Modernization of Resolutions

Chief advancements in water transport sector1212

24/10/11

AMAZONASPARÁ

AMAPÁRORAIMA

RODÔNIA

MATO GROSSO

TOCANTINS

GOIÁS

MATO GROSSODO SUL

MARANHÃO

PIAUÍ

CEARÁRIO GRANDEDO NORTE

PARAÍBA

PERNAMBUCO

ALAGOAS

BAHIA

MINAS GERAIS

SÃO PAULO

ESPÍ

RITO

SA

NTO

PARANÁ

SANTACATARINA

RIO GRANDEDO SUL

SERGIPE

RIO DE

JANEIRO

ACRE

MANAUSSANTARÉM

BELÉMVILA DO CONDE

ITAQUI

FORTALEZA

AREIA BRANCA

NATAL

CABEDELO

SUAPE

MACEIÓ

SALVADOR

ARATU

ILHÉUSBARRA DO RIACHO

VITÓRIA

RIO DE JANEIROITAGUAÍ (Sepetiba)

SÃO SEBASTIÃOSANTOS

PARANAGUÁSÃO FRANCISCO DO SUL

ITAJAÍIMBITUBA

PELOTASRIO GRANDE

MACAPÁ

RECIFE

NITERÓIFORNO

ANTONINA

ANGRA DOS REIS

PORTO ALEGRELAGUNA

PUBLIC SEA PORTS

34

1313

24/10/11

AMAZONASPARÁ

AMAPÁ

RORAIMA

RODÔNIA

MATO GROSSO

TOCANTINS

GOIÁS

MATO GROSSODO SUL

MARANHÃO

PIAUÍ

CEARÁRIO GRANDEDO NORTE

PARAÍBA

PERNAMBUCO

ALAGOAS

BAHIA

MINAS GERAIS

SÃO PAULO

ESPÍ

RITO

SAN

TO

PARANÁ

SANTACATARINA

RIO GRANDEDO SUL

SERGIPE

RIO DE JANEIRO

ACRE

MANAUSSANTARÉM

BELÉM

VILA DO CONDE

ITAQUI

FORTALEZA

AREIA BRANCA

NATAL

CABEDELO

SUAPE

MACEIÓ

SALVADOR

ARATU

ILHÉUS

BARRA DO RIACHO

VITÓRIA

RIO DE JANEIROITAGUAÍ (Sepetiba)

SÃO SEBASTIÃOSANTOS

PARANAGUÁSÃO FRANCISCO DO SUL

ITAJAÍ

IMBITUBA

PELOTASRIO GRANDE

MACAPÁ

RECIFE

NITERÓIFORNO

ANTONINA

ANGRA DOS REIS

PORTO ALEGRELAGUNA

14 TUP

13 TUP

Rio de Janeiro = 22 TUP

Rio Grande do Sul= 16 TUP

Santa Catarina= 11 TUP

PRIVATE PORT TERMINALS (TUP)

129

ETC

Espírito Santo = 9 TUP

Bahia = 8 TUP

1414

24/10/11

PUBLIC BY LEASE (TENDER)

PRIVATE BYAUTHORIZATION

ORGANIZED PORT BY CONCESSION (TENDER)

• Acts 8,630/93 and 8,666/93• Decrees 6,620/08, ,.391/02

and 6,413/08• ANTAQ Resolution 55/02 (under review)• Normative Instruction TCU

27/08

• Act 8,630/93• Decree 6,620/08• ANTAQ Resolution 1,660/10

• Acts 8,630/93 and 8,987/95

• Decree 6,620/08• Administrative Decree SEP

108/10

• Assignment of use of public asset

• Appraisal of the undertaking• Period of up to 50 years• Reversibility of assets to the

Union• Use of OGMO (port labor

management body)

• Period of up to 50 years• Possibility to operate in

consortium• Authorization for shipyards

and offshore support bases• Exclusive use – own cargo

only• Mixed use – third party and

own cargo

• Tender for private initiative• Granted use of organized

ports to public or private companies through public tender

• ANTAQ in charge of tender, following guidelines in General Concessions Plan (PGO)

Water transport legislation – Regulations1515

24/10/11 1616

IMAGINARY LINE WITH SMOOTHNAVIGATION AREAS

DRAFT NO REEFS

AWAY FROM PORT AREAS

NO OVERLAPPING CONSERVATION UNITS

FACTORS CONSIDERED

The General Concessions Plan – PGO 16

24/10/11 Source: ANTAQ – Statistical Yearbook 2010 and MDIC, Alice System (http://aliceweb.desenvolvimento.gov.br/)

Brazil: exports and imports (by sea, in tons and US$ FOB)

1717

24/10/11 0

2

4

6

8

10

12

0

2

4

6

8

10

12

Trade Chain and Port Handling - Brazil, 2001- 2010

US$ FOB (billions)

Millions of ton s

Trade chain vs. handling in Brazilian ports

1818

24/10/11

833,882,797 t

CABOTAGE188,011,104 t

22.55%LONG

DISTANCE616,397,721 t

73.92%

INLAND WATERWAYS29,473,972 t

3.53%

EXPORTS489,594,125 t

79.43%IMPORTS

126,803,596 t20.57%

Brazilian ports: handling in 20101919

24/10/11

1

THE 15 GROUPS OF GOODS MOST HANDLEDIN 2010 (millions of t)

Brazilian ports:goods most handled

91% OF TOTAL CARGO HANDLING

IN 2010

2020

24/10/11

NORTH NORTHEAST

SOUTHEAST SOUTH

Brazilian regions: participation in handling goods

2121

Solid BulksSolid Bulks

Solid BulksSolid Bulks

Liquid Bulks

Liquid Bulks Liquid Bulks

Liquid BulksGeneral Cargo

General Cargo General Cargo

General CargoContainers

Containers Containers

Containers

24/10/11

0

2

4

6

8

10

12

Statistics: ANTAQ quarterly bulletinHandling1st and 2nd semester 2011

2222

24/10/11

CONTAINER(TEU)

1st trimester 2011 compared to1st trimester 2010

CONTAINER(TEU)

2nd trimester 2011 compared to2nd trimester 2010

1st semester 2011 compared to1st semester 2010

Fuel Only All Products Fuel not consideredPeriod

Port statistics:1st sem/10 vs. 1st sem/11

2323

CABOTAGE

Accum. 2011 / Accum. 2010

24/10/11

• Oil prospection and extraction: offshore support

• Shipyards: inductor of Transpetro demands

• Establishment of clusters of chemical and oil industries

Opportunities:Oil prospection and extraction

2424

24/10/11

Rio de Janeiro

Pernambuco

Pará

São PauloSanta Catarina

Rio Grande do Sul

Ceará

Bahia

Amazonas

North

Alagoas

In Operation Improvement New Plant

Area (m²)

Northeast

SoutheastSouth

Source: SINAVAL – National Shipbuilding and Repair Industry and Offshore Union

New oil tankers, support vessels, platforms and drilling ships stimulated the construction of 18 shipyards

Pre-Salt: shipyards2525

24/10/11

Opportunities: North Region2626

24/10/11

Opportunities : Northeast Region2727

24/10/11

Opportunities: Southeast2828

24/10/11

Opportunities: South Region2929

24/10/11

R$ 15 BILLION

Opportunities- Private Terminals3030

R$ 7 BILLION

AUTHORIZED – IMPLEMENTATION UNDER WAY

CONCESSION REQUIREMENTS UNDER EXAMINATION

COMPANY

COMPANY

MUNICIPALITY

MUNICIPALITY

AUTHORIZATION

AUTHORIZATION

MODALITY

MODALITY

STATE

STATE

MIXED

MIXED

MIXED

MIXED

MIXED

MIXED

MIXED

MIXED

MIXED

EXCLUSIVE

EXCLUSIVE

EXCLUSIVE

EXCLUSIVE

EXCLUSIVE

EXCLUSIVE

EXCLUSIVE

24/10/11

Leasing opportunities - North3131

R$ 1,5 BILLION

Container Handling and Storage

PORT STATE OBJECTIVE AREA (m²) TIME PERIOD

Implementation of 2nd Plant-Based Solid Bulks Terminal

24/10/11

Leasing opportunities - Northeast

R$ 2 bilLION

3232

TIMEPERIO

D

24/10/11

Leasing opportunities - Southeast

R$ 5,4 bilLION

3333

24/10/11

Leasing opportunities - South3434

R$ 552 MILLION

24/10/11

• Need to equip ports for offshore support

• Investments in specialized terminals

• New businesses

• Stimulation of maritime support companies

Pre-Salt: Maritime support navigation 3535

24/10/11

TODAY, October 2011: 118 authorized companies – Source: ANTAQ website

• Authorization granted by ANTAQ to Brazilian navigation company

• Strong trend of grants increase due to the perspectives of pre-salt extraction and offshore operations

Pre-Salt: Maritime support navigation36

24/10/11

• PROMEF Construction of 49 new tankers

• PROMEF Included in PAC – Acceleration Growth Program

• 2010 – 3 new ships (1 in Pernambuco and 2 in Rio de Janeiro)

• 2011 – delivery of another 5 (five) ships and launching of another 6 for final touches

• PROMEF – can create up to 40 thousand direct and 160 thousand indirect jobs

• Stimulus to other areas: ship parts and equipment, ironworks and metallurgy

• 23 ships = capacity of up to 2.7 million GT

Sea transportationTranspetro Demands

3737

24/10/11

0 2 4 6 8 10 12

1

0 2 4 6 8 10 12

1

0 2 4 6 8 10 12

1

0 2 4 6 8 10 12

1

Drilling rigs in depths over 2,000 m Support and special vessels

SS and FPSO Production platforms Others (Jacket and TLWP)

+48 +250

+43 +6

Maritime support navigation: Pre-salt: Petrobras Demands

3838

up to

up to

up to

up to

up to

up to

up to

up to

up to

24/10/11

• The volume in Tupi, Carioca and the other recently discovered fields in the pre-salt area may increase the country’s oil and gas reserves by more than 50%. Today they amount to 14 billion barrels.• Petrobras target: to commence production at Tupi in 2010, with a pilot project of 100 thousand barrels a day (5% of national production), arriving at 500 thousand barrels per day between 2015 and 2020.

Discovery of new oil fields

Source: Petrobras

*Fonte: ABEAM

• Opportunities to provide for Petrobras needs;

• Renovation of national fleet and maintenance of platforms and vessels

• Port facilities such as building or repair shipyards and provision of logistics supplies

Maritime support navigation – biggest evolution

3939

24/10/11

• Provision of support services• Reserved to Brazilian companies• Brazilian flag vessels• Main services:

• port towage, passenger and cargo transportation, transportation of pilots,

• towing maneuvers• collection of garbage and residues from holds• provision of fuel, drinking water, food

Port support navigation4040

24/10/11

Waterway navigation (Inland navigation)Change in mode: Reduction of CO2 and freight cost 41

41

24/10/11

• Integration with the electricity sector in decisions involving projects with locks

• General Waterway Concession Plan• Social aspects in passenger

transportation in regions with little infrastructure

• Multimodality

• Production flow

• Carbon Credits

Waterways– Emphasis in using inland navigation

4242

24/10/11 4343

*Fonte: Ministério dos Transportes

Waterway Corridors – planning routes43

Grain Production

Area

Mercosur Corridor

Madeira Corridor

Tapajós Teles-Pires Corridor Tocantins Corridor

Parnaíba Corridor

São Francisco CorridorParaguai Corridor

Tietê / Paraná Corridor

24/10/11

Soy corridors – agribusiness4444

Soy Complex Export Corridors

Key:Cerrado Macro RegionSouth Macro RegionNon-operating WaterwayWaterwayProjected WaterwayExporting PortPortPresent FlowsAdditional Flows

Waterways:Place Production Access to Ports

WaterwayRailwayHighway

24/10/11

TocantinsPotential Extension: 1,580 km

AraguaiaPotential Extension : 2,060 km

Multimodal PotentialTocantins-Araguaia Waterway Navigation potential

4545

Navigable StretchLittle NavigabilityDamsBarrages

24/10/11

• The Tietê river is an example of multiple uses of water, as it is a source of energy and a logistic waterway mode of transportation of cargoes

• It is part of a multimodal utilization to suppress bottlenecks in the accesses to the Port of Santos, São Paulo

•Salto

Multimodality – Port of Santos –Tietê River 4646

24/10/11

The Tietê-Paraná waterway will have three sets of multimodal junctions:1 - Pederneiras-Jaú connected to railway (São Paulo and Santos)2 - Conchas-Anhembi3 - Santa Maria da Serra-Artemis (Piracicaba) connected to railway (São Paulo and Santos)

Railway interconnection

Railway connection to

Santos

Multimodality – Tietê River – Intermodal cargo terminals

4747

Source: São Paulo Road Map

24/10/11 0

2

4

6

8

10

12

1 1 1

Transport matrixModes of transportation throughout the world – Comparative chart

4848

Highways

Railways

Waterways

United States Canada Russia Germany Brazil

24/10/11 0

2

4

6

8

10

12

1 1

Transport matrix according to PNLTCurrent and projected for 2025 – Planning demands

4949

Cost Competitiveness

24/10/11

Example from agribusinessReduced CO2 emission by changing mode

5050

Current and Potential Handling of Grains in Brazil

Brazilian Grains Production

Production Transported by Waterway

Handling of Grains in Waterways

Current Potential

million t

million tmillion t

million t(2018/19 harvest)

Source

24/10/11

Example from agribusinessReduced CO2 emission by changing mode

5151

Reduced CO2 emissions to transport 2018/19 grains harvest

Harvest Handling by Waterway

No Investments

Difference – Cargo attracted by waterway

With Investments

million t

million t

million t

Source

24/10/11

Example from agribusinessReduced CO2 emission by changing mode

5252

Reduced CO2 emissions to transport 2018/19 grains harvest

CO2 Emissions Highway Mode

Waterway Mode

Cargo Absorbed

by Waterway

Highway Mode Waterway Mode ReducedEmission

million t

Highway(km)

CO2 Emission(kg)

Waterway (km)

Highway(km)

CO2 Emission(kg)

Source

24/10/11

• Multimode integration of highways, railways and waterways

• Establishment of transshipment terminals at riparian cities along waterways

• Possible better flow of local production

• Development of industries and services along the multimodal matrix

• Attraction of investments

Multimodal potential Potential for waterways usage

5353

24/10/11

“Many have ideas and are creative. Some turn their ideas into dreams, and are persistent. Rarely do they turn their dreams into reality, and these are the ones who change the world.” Steve Jobs

5454

24/10/11

Fernando Antonio Brito FialhoDirector-General

0800-6445001www.antaq.gov.br