THE BERMAN VALUE FOLIO - Forbes · 02/04/2015 · THE BERMAN VALUE FOLIO ... Buffett continue to be...

10

Malcolm Gladwell says it takes 10,000 hours to achieve mastery at something. With 50 years at Berkshire, Buffett has logged those hours ten times over. In this year's annual report, Buffett includes the market return of Berkshire's stock for the first time, showing that the per-share price has appreciated an astonishing 1,826,163% since inception. No that's not a typo: $50,000 invested with Buffett in 1965 is worth nearly $1 billion today. Kicking yourself? Me too. At this pinnacle of achievement, having also increased Berkshire's book value by 751,113% (vs. 11,196% for the S& P 500), Buffett is facing questions about his underperformance on that measure over the last five years. The recent returns for Berkshire's per share book value vs the S& P 500 are as follows: James Berman THE BERMAN VALUE FOLIO A TREFIS INTERACTIVE PORTFOLIO TABLE OF CONTENTS ACCESS INTERACTIVE TREFIS ANALYSIS TO GET THE MOST FROM THE FOLIO James Berman , the president and founder of JBGlobal.com LLC, a registered investment advisory firm (SEC registered), specializes in asset management for high-net-worth individuals and trusts. Mr. Berman is a faculty member in the Finance Department of the NYU School of Professional Studies. He has appeared on CNBC and the Fox Business Channel and has been quoted and published in a variety of publications, including Barron's, Bloomberg, The Huffington Post and CNN Money. Mr. Berman holds a B.A., Magna Cum Laude, Phi Beta Kappa, in English & American Literature from Harvard and a J.D. from Harvard Law School. BUFFETT & BERKSHIRE: TOGETHER 50 YEARS APR 2015 BUFFETT & BERKSHIRE 1 HAS BUFFETT LOST HIS EDGE? 2 UNDER THE HOOD: BRK STOCKS 3 DEERE: INVEST LIKE BUFFETT? 4 EXXONMOBIL 5 ARCELORMITTAL 6 PAYCHEX 7 BUFFETT-STYLE INVESTING 8 THE BERMAN VALUE PORTFOLIO 9 - TEST OUR ASSUMPTIONS - RUN YOUR OWN SCENARIOS - READ FORECAST RATIONALE - ACCESS TREFIS RESEARCH - ANALYZE VALUE DRIVERS Year Berkshire Book Value S& P 500 2010 13.0% 15.1% 2011 4.6% 2.1% 2012 14.4% 16.0% 2013 18.2% 32.4% 2014 8.3% 13.7%

Transcript of THE BERMAN VALUE FOLIO - Forbes · 02/04/2015 · THE BERMAN VALUE FOLIO ... Buffett continue to be...

Malcolm Gladwell says it takes 10,000 hours to achieve mastery at something. With 50 years at Berkshire, Buffett has logged those hours ten times over.

In this year's annual report, Buffett includes the market return of Berkshire's stock for the first time, showing that the per-share price has appreciated an astonishing 1,826,163% since inception. No that's not a typo: $50,000 invested with Buffett in 1965 is worth nearly $1 billion today. Kicking yourself? Me too.

At this pinnacle of achievement, having also increased Berkshire's book value by 751,113% (vs. 11,196% for the S&P 500), Buffett is facing questions about his underperformance on that measure over the last five years.

The recent returns for Berkshire's per share book value vs the S&P 500 are as follows:

James Berman

THE BERMAN VALUE FOLIOA TREFIS INTERACTIVE PORTFOLIO

TABLE OF CONTENTS

ACCESS INTERACTIVE TREFIS ANALYSIS TO GET THE MOST FROM THE FOLIO

James Berman, the president and founder of JBGlobal.com LLC, a registered

investment advisory firm (SEC registered), specializes in asset management for high-net-worth individuals and trusts. Mr. Berman is a faculty member in the Finance Department of the NYU School of Professional Studies. He has appeared on CNBC and the Fox Business Channel and has been quoted and published in a variety of publications, including Barron's, Bloomberg, The Huffington Post and CNN Money. Mr. Berman holds a B.A., Magna Cum Laude, Phi Beta Kappa, in English & American Literature from Harvard and a J.D. from Harvard Law School.

BUFFETT & BERKSHIRE: TOGETHER 50 YEARS

APR 2015

BUFFETT & BERKSHIRE 1

HAS BUFFETT LOST HIS EDGE? 2

UNDER THE HOOD: BRK STOCKS 3

DEERE: INVEST LIKE BUFFETT? 4

EXXONMOBIL 5

ARCELORMITTAL 6

PAYCHEX 7

BUFFETT-STYLE INVESTING 8

THE BERMAN VALUE PORTFOLIO 9

- TEST OUR ASSUMPTIONS

- RUN YOUR OWN SCENARIOS

- READ FORECAST RATIONALE

- ACCESS TREFIS RESEARCH

- ANALYZE VALUE DRIVERS

Year Berkshire Book Value S&P 500

2010 13.0% 15.1%

2011 4.6% 2.1%

2012 14.4% 16.0%

2013 18.2% 32.4%

2014 8.3% 13.7%

So has Buffett lost his edge?

Maybe. It's also possible that the law of large numbers? the inevitable cap on the growth of the hulking and huge? has finally stopped Berkshire in its tracks.

But another explanation bears consideration: the difference in accounting for the purchase of wholly owned operating companies? Buffett's primary strategy over the past few years? versus that of publicly traded stocks, an activity of declining importance to Berkshire's value.

This implicates the bizarre vagaries of accounting, namely the disparate treatment of gains in public securities versus gains in subsidiaries.

Just like the rest of us, Berkshire must mark all publicly traded stock prices to market. So if Coca-Cola goes up or down, the price must be carried on the balance sheet as a component of book value.

But as Buffett has explained, when a subsidiary gains in value, it must still be listed at original cost. It can't be listed at market price, because a private company has no freely available market prices. Just because there are no market prices, doesn't mean that value hasn't increased. Many (if not most) of Berkshire's wholly owned operating companies have intrinsic values which would be valued at significant multiples of the original investment.

If Buffett could carry those at current market prices, book value would explode. Since he can't, book value lags significantly behind intrinsic value.

This is the real reason Berkshire has underperformed the index in recent years. In many ways, Buffett is the victim of his own success. His acquisitions throw off such enormous gobs of cash that the public markets cannot satisfy the beast. Private companies became the outlet for Berkshire's hunger. More private companies (relative to public companies) weigh down book value at times of rising equity prices.

The counterargument is that the subsidiaries throw off their entire net income as cash, which accrues to book value? unlike public companies, whose dividends (if any) are the only cash Berkshire gets to add to book value.

In the end, the only thing that's clear is that Berkshire and Buffett continue to be absolutely unique and unprecedented. Berkshire is like no other company? and Buffett is like no other investor. 2

THE TREFIS DOW

Ticker Trefis Price Market Price

AXP 96.67 81.37

BA 156 152

CAT 85.44 80.48

CSCO 26.38 28

CVX 114 104

DD 70 73.60

DIS 105 107

GE 27.87 25.27

GS 189 191

HD 100 116

IBM 197 163

INTC 34.29 30.79

JNJ 101 102

JPM 65 60.46

KO 41.55 40.47

MCD 96.81 99.36

MMM 153 166

MRK 56.50 58.63

MSFT 44.46 42.90

NKE 85.41 101

PFE 35.10 34.52

PG 82.54 83.92

T 37.58 33.07

TRV 111 109

UNH 105 118

UTX 125 119

V 269 67.10

VZ 55.68 49.41

WMT 80.95 83.05

XOM 96 84.52

DOW 18,259 16,732.28

Undervaluation + 9%

HAS BUFFETT LOST HIS EDGE?

Fortunately, Buffett still does invest in some public securities, aided by co-managers Ted Weschler and Todd Combs. It's always fun to look under the hood and see which stocks constitute Berkshire's largest holdings. Of course, this doesn't change very much, given that Buffett's ideal holding period is "forever."

You'll find everything from the old stalwarts like American Express (AXP)? now worth more than 10 times initial cost? to more recent buys like IBM (IBM), trading at a 6% loss since purchase a few years ago. In the past year, Buffett added to IBM in a vote of confidence to the flailing tech services firm. I own IBM in the Folio and think it continues to be undervalued. Another Buffett stock I own in the Folio is Procter & Gamble (PG), which I recently downgraded to hold on valuation concerns.

One holding that has always puzzled me is DIRECTV (DTV), which appears very far from the Buffett criterion of "I know what this company will look like in a decade." DTV is reportedly a Ted/Todd selection that Buffett must have signed off on, given it's large size ($2.1 billion).

3

UNDER THE HOOD: Berkshire's Stock Portfolio

A new star in the Buffett constellation is Deere & Company (DE), which Buffett purchased in 2014. Unlike DTV, the DE purchase looks like classic Buffett: a company that's been around forever and looks to be around forever more. With origins as a blacksmith's forge in 1837, DE is now a leading manufacturer of agricultural equipment. We'll take a closer look at DE on the next page.

Deere & Co. has many resounding competitive advantages. DE's leading brand, ranked in the top 100 by Forbes, inspires tremendous loyalty among customers.

According to Morningstar, DE enjoys a strong network effect? the virtuous cycle by which buyers go there because the sellers do and vice versa. DE has over 1,500 agricultural dealers, a much stronger network than leading competitors AGCO and CNH Industrial.

DE's moat is confirmed by its high returns on equity, which have averaged 25% over the past decade vs. Morningstar's 9.2% cost of capital estimate.

While DE has reasonable growth, with a trailing 6% 10-yr annualized rate, it's clearly no highflier. Buffett is famous for buying companies that have low growth rates and even low margins, that nevertheless have high returns on capital.

Buffett has often made the point that many businesses can increase revenues at a fast clip, while doing so atop a bloated capital base that doesn't help shareholders.

By way of example, I can set up a website tomorrow that will have the fastest revenue growth ever achieved. My business plan is simple: I exchange $100 bills for $20 bills. That's right: you give me a Benjamin and I give you a Jackson in return. This business will have revenues to the moon but its negative profits and returns on capital will sink it quickly.

In many ways, DE is really the prototypical Buffett purchase: a wonderful business at a fair price.

Trefis thinks the stock is worth $89, just north of the market price. Despite the miniature discount, I'll happily steal this idea from the Oracle of Omaha, and I suggest you do too.

4

DEERE: Invest Like Buffett?

ExxonMobil (XOM) has been hit hard by declining oil prices. At $84.95, XOM is 3% below our $87.42 purchase price. I think XOM is worth over $100 per share, above the Trefis estimate of $96. XOM is the

best-of-breed integrated oil company. If anyone can weather an environment of permanently lower oil prices, it's XOM, with its truly ironclad balance sheet and diversified portfolio of crude oil, refined products, natural gas and chemicals. Trefis feels XOM is worth $96, 13% above the current market price. Trefis assumes high 70s crude oil prices for the next few years, an estimate that may prove too optimistic. Due to XOM's upstream and downstream exposure, however, XOM is less leveraged to oil prices than many monoline energy companies. I like XOM as a long-term holding, not just as a way to profit from increasing oil prices.

Market Capitalization Annual Revenues Dividend/Yield 52 Week Range

$357 B $369 B $2.76/ 3.3% $82.68 - 104.76

COMPANY HIGHLIGHTS

TREFIS KEY DRIVERS

Lower oil prices are likely to have a significant impact on Exxon's upstream earnings this year. According to the company, a $1 per barrel decline in the weighted-average realized price of crude oil results in a $350 million negative impact on its upstream net earnings. This means that - depending on the lag between price fluctuations and their impact on Exxon's earnings - if oil prices (Brent) remain around the current $59 per barrel level, Exxon's upstream earnings could decline by as much as $14 billion, or 50%, compared to last year.

5

With steel & iron ore prices in freefall, ArcelorMittal (MT) is having no easy time of it. At $10.38, MT has lost 90% of its value since its high of $102 back in 2008. I've only owned it in the Folio since 2012. but having purchased at $16.06, that 's been painful enough, thank you. In tandem with falling steel prices, Trefis has reduced their

estimate of fair value dramatically in recent months, pegging intrinsic value at $10.46, while Morningstar maintains theirs at $16. There's no doubt that MT is among the riskier of Folio holdings, leveraged both financially and to industrial commodity prices. Yet, Trefis puts MT's cost of capital at 13%, which seems too high, given that MT is financed mainly through bonds paying a pre-tax average of 7%. I estimate the cost of capital to be closer to 11% which puts fair value above $15. I would buy MT here.

Market Capitalization Annual Revenues Dividend/Yield 52 Week Range

$15.6 B $79.3 B $0.20 / 2.1% $9.21 - 16.80

COMPANY HIGHLIGHTS

TREFIS KEY DRIVERS

Weak iron ore prices have negatively impacted ArcelorMittal's mining division. As a result of the fall in iron ore prices, the division reported a 35% year-over-year fall in revenues to $1.06 billion in Q4 2014, while the division's earnings before interest, taxes, depreciation and amortization (EBITDA) fell by around 60% in the quarter. The Mining segment's performance was a major drag on the company's Q4 results, offsetting improvements in its steelmaking operations.

6

My perennial favorite Paychex (PAYX) is the protypical Buffett holding in one sense: it can be held forever. With recurring revenues, low capex, high switching costs and incredible returns on invested capital, PAYX is clearly a

wonderful business. With a one-year return of 20%, is it now overvalued? On a multiple basis it sure seems so, trading at a lofty trailing P/E ratio of 27. But PAYX's free cash flow generation is consistently higher than its net income, with $763 million in trailing FCF vs. only $660 million in net income over the past year. PAYX is much cheaper than it appears on a P/E basis. The multiple of market cap to FCF is a more reasonable 24 times. For those not fond of multiple analysis, Trefis estimates PAYX's value at $45.15, 9% below the market price. By any measure then, PAYX looks a little rich, but I think it deserves the premium.

Market Capitalization Annual Revenues Dividend/Yield 52 Week Range

$18.0 B $2.7 B $1.52/ 3.1% $39.80 - 51.72

COMPANY HIGHLIGHTS

TREFIS KEY DRIVERS

In its recent earnings release, Paychex reported 8% year-on-year growth in service revenue driven by strong growth in its Human Resource Services (HRS) segment. Rising demand for healthcare reform products and HR outsourcing led to double-digit growth in the HRS segment, while the Payroll segment was sluggish as a result of a shift in the timing of revenues. As businesses continue to work to comply with the PPACA, Paychex?s insurance offering should continue to drive growth in the HRS segment.

7

8

SNEAK PEAK: BRK

I'll be teaching an online class on Buffett-Style Investing at NYU starting April 2, with a live blog from the annual meeting in Omaha: Enroll now at this link!

The Fundamentals of Buffett-Style Investing

Online class in the Finance Dept at NYU-SPS

April 4th - April 25: Self-paced online case studies

May 2: Follow James to Omaha via live blogging for the Berkshire Hathaway's Annual Shareholders Meeting

For more information and to register click here.

Learn the investment techniques of Warren Buffett, the world?s most legendary investor. By examining case studies of Buffett?s acquisitions, students will explore the real-world principles that the ?Oracle of Omaha? uses to pick companies. Then follow James to Omaha via live blog and participate in the "Woodstock of Capitalism"? Berkshire Hathaway's Annual Shareholders Meeting with Warren Buffett himself.

No finance background or experience required.

Featuring the following case studies:

- Coca-Cola- American Express- BNSF- GEICO- Blue Chip Stamps- Nebraska Furniture Mart- And some of his newest acquisitions...

Total return is calculated since inception date of 12/21/2011 and includes reinvested dividends. When a stock is bought in the portfolio, it is added on an equal cash-weighted basis at the time of purchase.

9

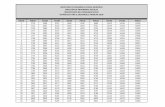

THE BERMAN VALUE FOLIO

Symbol Company Name Buy, Hold, Sell

Purchase Date

Basic Materials

MT Arcelor-Mittal Buy 9/21/2012

RIO Rio Tinto Buy 1/31/2014

Purchase Price

Market Price

Total Return Since Purchase

Trefis Estimate

$16.06 $9.42 (39.3%) $10.46

$53.15 $41.40 (19.2%) $43.04

Consumer

PG Procter & Gamble Hold 12/21/2011 $65.84 $81.94 37.2% $82.54

Energy

SLB Schlumberger Buy 9/30/2014 $98.66 $83.44 (15.0%) $95.26

BP BP Buy 12/21/2011 $41.33 $39.11 8.9% $39.00

PBR Petrobras Buy 12/31/2014 $7.30 $6.01 (17.7%) $13.00

XOM Exxon Mobil Buy 1/30/2015 $87.42 $85.00 (2.0%) $96.00

Financial Services

BK BNY Mellon Buy 12/21/2011 $19.43 $40.24 120.5% $40.00

BLK BlackRock Buy 8/29/2014 $330.53 $365.84 12.6% $360

C Citigroup Hold 12/21/2011 $25.74 $51.52 100.8% $56.00

JPM JPMorgan Chase Buy 12/21/2011 $32.12 $60.58 105.7% $65.00

Tech, Media, Telecom

ADP ADP Hold 12/21/2011 $53.21 $85.64 74.7% $76.30

EBAY eBay Hold 12/21/2011 $30.18 $57.68 91.1% $60.39

IBM IBM Buy 2/28/2014 $185.17 $160.50 (10.7%) $197

PAYX Paychex Hold 12/21/2011 $29.14 $49.62 90.9% $46.11

Industrials & Transportation

UPS UPS Buy 12/21/2011 $72.40 $96.94 46.2% $110

UTX United Tech. Hold 4/21/2012 $80.40 $117.20 54.7% $125

DE Deere New Buy 3/31/2015 $87.69 $87.69 --- $89.26

Total 81.3%

Portfolio Changes:I bought Berkshire holding Deere (DE)

See p. 4.

The Berman Value Folio

DISCLAIMER

The Berman Value Folio (TBVF) is published monthly and provides information and investment ideas on stocks. All material in TBVF is copyright, 2011 through the present, by Trefis and JBGlobal.com LLC and may not be reproduced in whole or in part in any form without written consent. TBVF is written by James Berman with assistance from Trefis staff. TBVF is distributed by both Trefis and Forbes. Forbes acts only as distributor and is not responsible for, nor does it endorse, any TBVF content or investment ideas. All stock buys and sells are the sole decision of James Berman. In the TBVF portfolio, James Berman is restricted to buying only stocks that are covered by Trefis. TBVF is intended for experienced investors, who understand the risks, costs, mechanics and consequences of investing. None of the content in this newsletter is intended to be, nor should be interpreted as, a solicitation to buy or sell securities. The selection of portfolio stocks is based on fundamental analysis. There is, however, no assurance that these securities will produce profits. They may instead produce serious losses. It should not be assumed that the recommendations made in the future will be profitable or will equal the performance of any prior securities mentioned in the TBVF. All investing involves risk of serious loss. No graph, chart, formula or other device offered or portrayed in TBVF can in and of itself be used to make trading or investment decisions. Any graph, chart, formula or other device is inherently unreliable in making a trading or investment decision due to the intrinsically misleading nature of such items.

Performance results are based on model portfolios and do not reflect actual trading. Actual performance will vary based on a variety of factors, including market conditions and trading costs. TBVF results may not reflect the impact that material economic and market factors might have had on the adviser's decision-making if the adviser were actually managing clients' money in this portfolio. TBVF contains stocks that are managed with a view towards capital appreciation. James Berman and JBGlobal.com may manage other portfolios with different strategies and returns that may materially differ from TBVF results with substantially higher or lower performance. TBVF model results do not reflect the deduction of any management fees, advisory fees, brokerage or other commissions, bid-ask spreads, tax consequences, and any other expenses that a client would have to actually pay or would have actually paid in a real portfolio. All return figures assume the reinvestment of all dividends. When a stock is bought in the portfolio, it is added on an equal cash-weighted basis at the time of purchase. Past performance does not guarantee future results. Any forward-looking statement is inherently uncertain and cannot be relied upon as a statement of actual performance. If you would like a spreadsheet furnishing a list of all recommendations made by TBVF since inception on 12/21/2011, please send an email request to: [email protected].

Although all content is derived from data believed to be reliable, accuracy cannot be guaranteed. James Berman, JBGlobal.com LLC, Insight Guru Inc., Trefis, TBVF?s publisher and distributor(s) and their employees assume no liability whatsoever for any investment losses as a result of securities purchased on TBVF recommendations. TBVF is not intended to provide personalized investment advice. Readers and subscribers should consult their financial adviser before investment. James Berman is an investor in Insight Guru Inc., the parent company of Trefis, both personally and through the venture fund he subadvises. James Berman, therefore, has a financial interest in Trefis aside from his interest in TBVF.

James Berman, JBGlobal.com LLC and employees of TBVF, Insight Guru Inc., JBGlobal.com L.L.C. and Trefis may hold positions in some or all of the stocks mentioned here, both personally and in the accounts and funds they manage for others. No compensation for recommending particular securities, services, or financial advisors is solicited or accepted. If you are unwilling or unable to abide by any conditions of this disclaimer, then you may obtain a refund for the unused portion of your subscription at any time.

10