The automobile industry by Sumit Jaiswal

37

-

Upload

sumeet-jayswaal -

Category

Documents

-

view

169 -

download

0

Transcript of The automobile industry by Sumit Jaiswal

The Automobile Industry

Presented By:-

Sumit Jaiswal

Sushil Powar

Sabir Siddhique

Kunal Sarkar

Mayur Avhad Presented By:- batch

29

Top To Bottom Approach

Global Economy Overview

Global economic growth is still weak, its underlying dynamics are changing, and the

risks to the forecast remain to the downside. As a result, new policy challenges are

arising and policy spillovers may pose greater concern. In particular, markets are

increasingly convinced that U.S. monetary policy is reaching a turning point, and

this has led to an unexpectedly large increase in long-term yields in the United States

and many other economies. Also, growth in China is slowing, which will affect many

other economies, notably the commodity exporters among the emerging market and

developing economies. The major economies must urgently adopt policies that improve

their prospects; otherwise the global economy may well settle into a subdued medium

term growth trajectory. The United States and Japan must develop and implement

strong plans with concrete measures for medium-term fiscal adjustment and entitlement

reform, and the euro area must develop a stronger currency union and clean up its

financial systems. China should provide a permanent boost to private consumption

spending to rebalance the growth of demand away from exports and investment.

In Many emerging market economies need a new round of structural reforms.

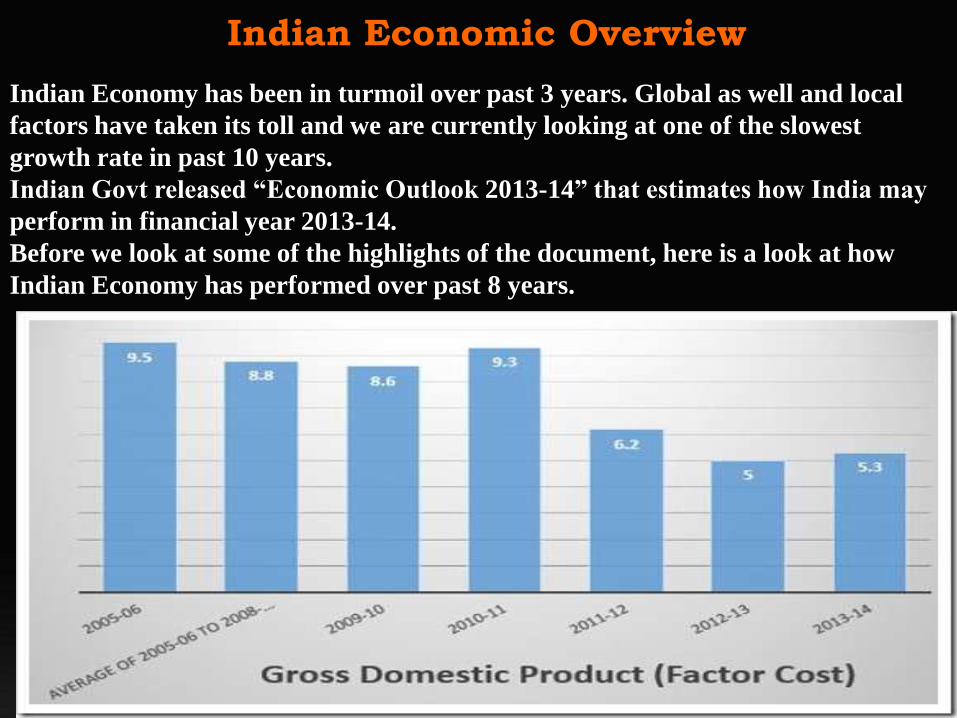

Indian Economic Overview

Indian Economy has been in turmoil over past 3 years. Global as well and local

factors have taken its toll and we are currently looking at one of the slowest

growth rate in past 10 years.

Indian Govt released “Economic Outlook 2013-14” that estimates how India may

perform in financial year 2013-14.

Before we look at some of the highlights of the document, here is a look at how

Indian Economy has performed over past 8 years.

Indian Economic Overview-Current Standing

Investment rate projected at 34.7% of GDP in 2013-14 as against the estimated 35% in

2012-13.

Domestic savings rate projected at 31% of GDP as against the estimated 30.2 % of GDP

2012-13.

Inflation by end March 2014 is expected to be around 5.5 percent as against the average of

7.4% in 2012-13 and 5.7% at end March 2013.

Current Account Deficit is expected to reduce to USD 70 billion (3.8% of GDP) in 2013-14

against an USD 88.2 billion (4.8% of GDP) in 2012-13. The center also expects that The

Current Account Deficit may go even below USD 70 billion, if the recent trends in exports

and imports are maintained through the year.

Net FDI inflows in 2013-14 projected at $21.7 billion against an estimated $19.8 billion in

2012-13.

FII inflows are estimated to reduce drastically to USD 2.7 billion in 2013-14, as against USD

17 billion in 2011-12 and USD 27 billion in 2012-13.

Net Capital flows projected at $ 61.4 billion (3.4% of GDP) in 2013-14 against an estimated

$ 89.4 billion in 2012-13, the second highest level to date.

Budgeted fiscal deficit is estimated at 4.8% of GDP in 2013-14, as against an estimated

4.9% in 2012-13.

In the whole, Indian economy is expected to do better than last year, but it is still much

lower than average growth rate of previous 5 years.

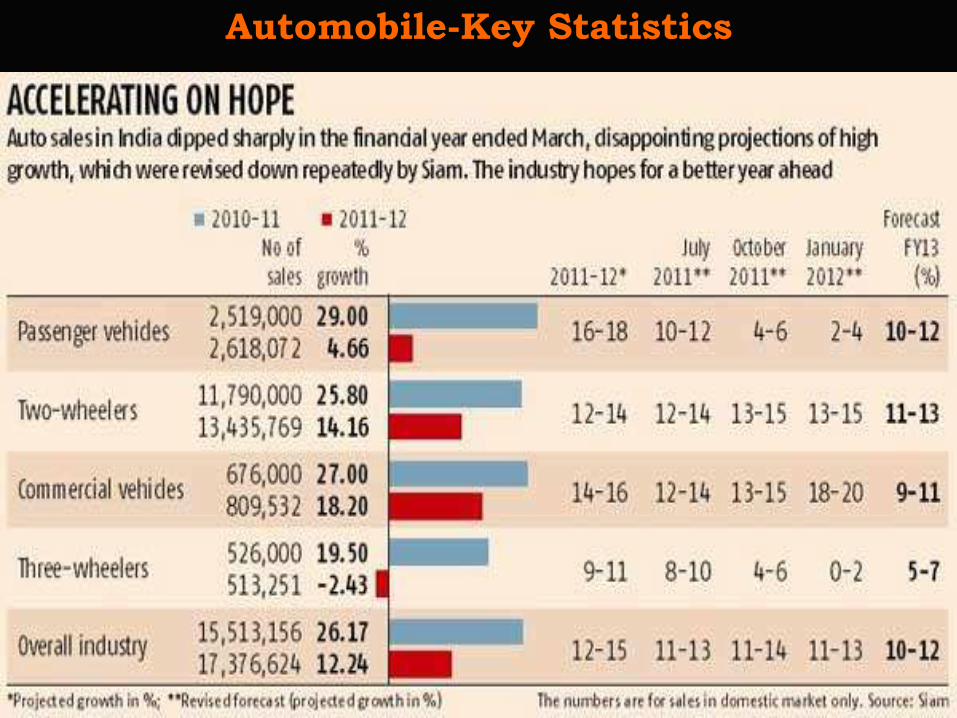

Automobile Industry-Growth Avenue

In terms of the Auto industry, India is the sixth largest market after China, US, Germany,

Japan and Brazil.

Overall the market includes cars, two wheelers, trucks & auto parts and India is expected

to become #3 in the automobile market by 2015 as defined by sales volume growth.

The auto sector reported a robust growth rate of 26% in the last two years (2010-2012)

although this year the growth has slowed down significantly.

The BSE AUTO Index outperformed the benchmark Nifty by 79%, 12% and 19% in FY10,

FY11 and FY12, respectively.

The world standings for the Indian automobile sector, as per the Confederation of Indian

Industry in FY 2012, was as follows:

Largest three-wheeler market

Second largest two-wheeler market

Tenth largest passenger car market

Fourth largest tractor market

Fifth largest commercial vehicle market

Fifth largest bus and truck segment

Since the de-licensing of the sector in 1991 and the subsequent opening up of 100% FDI

through the automatic route, the industry is one of the key drivers of economic growth of

the nation.

Government Support To The Automobile Industry

The Industrial Policy of 1991 de-licensed the Automobile Industry in India, but passenger

cars were de-licensed in 1993.

Now, no license is required for setting up any unit for manufacturing of Automobiles except

in some special cases. Further, 100% Foreign Direct Investment (FDI) is permissible.

Removal of Quantitative Restrictions (QRs) from April 1, 2001 has allowed the import of

vehicles, including in the passenger car segment where one can freely import subject to

certain conditions notified by Directorate General of Foreign Trade (DGFT).

To protect India from becoming a dumping ground for old and used vehicles produced

abroad, the custom duty on the import of second hand vehicles including passenger cars

has been raised to 111%.

Custom duty on Completely Built Units (CBU‟s) of large cars/ MUV‟s/ SUV‟s permitted for

import without any type approval (value exceeding US$40,000 and Engine Capacity

exceeding 3000 cc of Petrol and 2500 cc for Diesel) is being increased from 60% to 75%,

which might force foreign brands to set up manufacturing facilities in India.

Automobile Industry-Future Prospects

“By 2016, India will emerge as the destination of choice in Asia for the design &

manufacturing of automobiles and automotive components.

The output of the India‟s automotive sector will be $145bn by 2016,(from $34bn

in 2006) contributing to 10% of India‟s Gross Domestic Product and providing

employment to 25 mm people.

According to Draft Automotive Mission Plan 2006-2016 by the Ministry of Heavy

Industries & Public Enterprises.

Vision 2016

Automobile-Key Statistics

Structure Of The Auto Industry In India

• Automobiles

Passenger Vehicles

The Indian Passenger vehicle market is the 7th largest market in Asia and 10th largest

market in the world in terms of volume.

As per SIAM, passenger vehicles held a 15.07% domestic market share in the year

2012-12.

India sold 2.6mm passenger vehicles in the domestic market and exported 0.5mm

passenger vehicles in the year 2012-13 and grew at a 7 year CAGR of 14%.

The passenger Vehicle industry is likely to grow at a CAGR of 10-11% till FY 2017.

Small car segment to grow at a CAGR of 6-7% in next five years.

Mid size segment to record a rise of 17-18% by FY 2017.

Asian markets are expected to fuel the growth in the short term as demand drops in the

European markets, and growing demand for mid-size cars and preference for diesel

variants to further boost the realization over the medium term.

Automobile production in India is expected to grow by a modest 9% in 2013-14 as per

current industry forecasts.

Indian Passenger Vehicle Industry

Top Automobiles (Passenger Vehicle) Companies In India

Maruti Suzuki: Maruti Suzuki India Limited (MSIL, formerly Maruti Udyog Limited) is a

subsidiary of Suzuki Motor Corporation of Japan. Maruti Suzuki is a leading manufacturer

of passenger vehicles in India. Lovingly referred to as the people‟s car maker; over the past

three decades Maruti Suzuki has changed the way people in India commute and travel.

Mahindra & Mahindra : In 1947, Mahindra & Mahindra introduced India to the utility

vehicle. More than 65 years later, It is still India‟s premier utility vehicle (UV) company. In

addition to making groundbreaking UVs like the Scorpio and Bolero, Mahindra offers

cars, pickups, and commercial vehicles that are rugged, reliable, environmentally

friendly, and fuel-efficient.

Tata Motors: Tata Motors Limited is India‟s largest automobile company, with consolidated

revenues of INR 1,65,654 crores (USD 32.5 billion) in 2011-12. It is the leader in commercial

vehicles in each segment, and among the top three in passenger vehicles with winning

products in the compact, midsize car and utility vehicle segments. It is the world‟s fourth

largest truck and bus manufacturer.

Source : Economics Times

Company Overview

Maruti Suzuki India Limited has been the leading manufacturer of passenger vehicles in

India over the past 3 decades.

It accounts for 60% of the total Indian passenger car market with respect to Volumes.

It has 15 brands and over 150 variants in all the vehicle segments.

The company has service centers in 1,400 in cities and over 200 driving schools across the

country, which make it one of the most well recognized brands in the country.

The Tragedy that happened at their Manesar plant as a result of labor unrest in

July 2012 has shaken up the auto industry & the entire Manesar belt.

Maruti Suzuki India Limited

Scrip Details

ISIN INE585B01010

Industry Cars & Utility Vehicles

Impact Cost 0.07%

BC/RD BC 16/08/2013-27/08/2013

Market lot 1

Listing Date 9/7/2003

Management

Name Designation

R C Bhargava Chairman

S Ravi Aiyar Company Secretary & Compliance Officer & Chief Legal Officer

Kenichi Ayukawa Managing Director & Chief Executive Officer

Toshihiro Suzuki Director

Kazuhiko Ayabe Director & Managing Executive Officer ( Marketing & Sales)

Masayuki Kamiya Director (Production)

Toshiaki Hasuike Joint Managing Director

Income Statement

(in Cr.) 2013 2012 2011 2010 2009

Income Statement

Revenue 43,587.93 35,587.09 37,040.09 29,623.01 20,852.52

Other Income 812.37 826.86 482.31 496.76 601.34

Total Income 44,400.30 36,413.95 37,522.40 30,119.77 21,453.86

Expenditure -39,358.25 -33,074.20 -33,375.74 -25,668.72 -19,020.46

Interest -189.82 -55.21 -24.41 -33.5 -50.98

PBDT 4,852.23 3,284.54 4,122.25 4,417.55 2,382.42

Depreciation -1,861.17 -1,138.35 -1,013.50 -825.02 -706.54

PBT 2,991.06 2,146.19 3,108.75 3,592.53 1,675.88

Tax -598.93 -511.05 -820.11 -1,094.91 -457.14

Net Profit 2,392.13 1,635.14 2,288.64 2,497.62 1,218.74

Equity 151.04 144.46 144.46 144.46 144.46

EPS 79.19 56.6 79.22 86.45 42.18

CEPS 140.8 96 114.29 115 66.64

OPM % 11.57 9.38 11.2 15.03 11.67

NPM % 5.49 4.59 6.18 8.43 5.84

Dec-13 Sep-13 Jun-13 Mar-13 Dec-12

Promoter and

Promoter Group 56.21% 56.21% 56.21% 56.21% 54.21%

Indian -- -- -- -- --

Foreign 56.21% 56.21% 56.21% 56.21% 54.21%

Public 43.79% 43.79% 43.79% 43.79% 45.79%

Institutions 35.45% 35.01% 35.10% 34.96% 37.48%

FII 21.47% 19.66% 22.03% 22.36% 23.13%

DII 13.98% 15.35% 13.07% 12.60% 14.35%

Non Institutions 8.34% 8.78% 8.69% 8.83% 8.31%

Bodies Corporate 6.08% 6.38% 6.43% 6.31% 5.88%

Custodians -- -- -- -- --

Total 30,20,80,060 30,20,80,060 30,20,80,060 30,20,80,060 28,89,10,060

Shareholding Pattern As On

Mahindra & Mahindra: In 1947, Mahindra & Mahindra introduced India to

the utility vehicle. More than 65 years later, It is still India‟s premier utility

vehicle (UV) company. In addition to making groundbreaking UVs like the

Scorpio and Bolero, Mahindra offers cars, pickups, and commercial vehicles

that are rugged, reliable, environmentally friendly, and fuel-efficient.

Company Overview

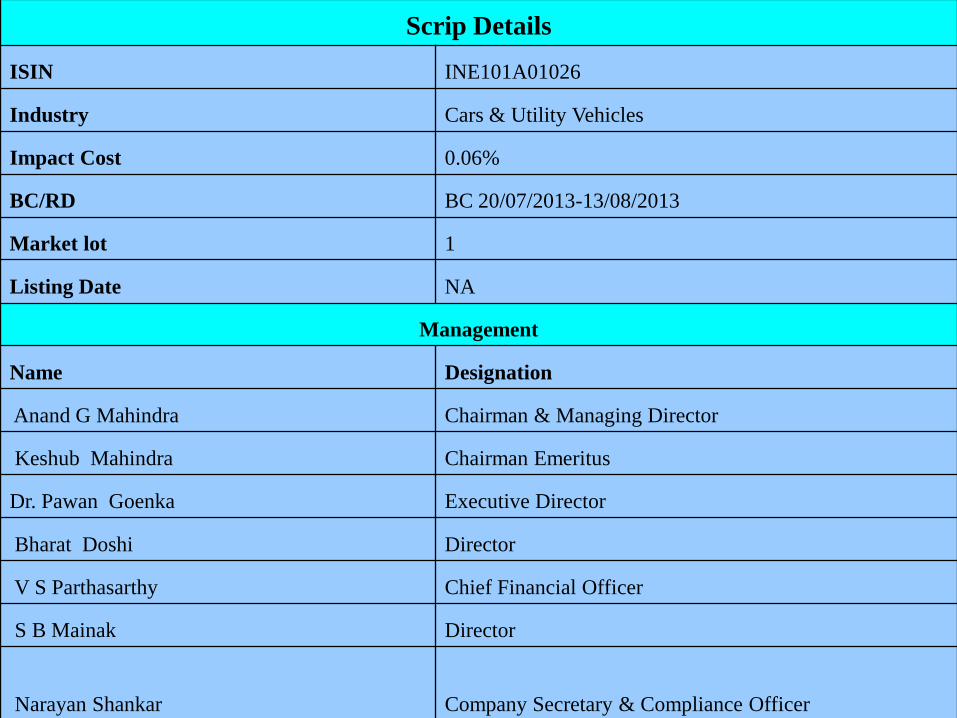

Scrip Details

ISIN INE101A01026

Industry Cars & Utility Vehicles

Impact Cost 0.06%

BC/RD BC 20/07/2013-13/08/2013

Market lot 1

Listing Date NA

Management

Name Designation

Anand G Mahindra Chairman & Managing Director

Keshub Mahindra Chairman Emeritus

Dr. Pawan Goenka Executive Director

Bharat Doshi Director

V S Parthasarthy Chief Financial Officer

S B Mainak Director

Narayan Shankar Company Secretary & Compliance Officer

Income Statement

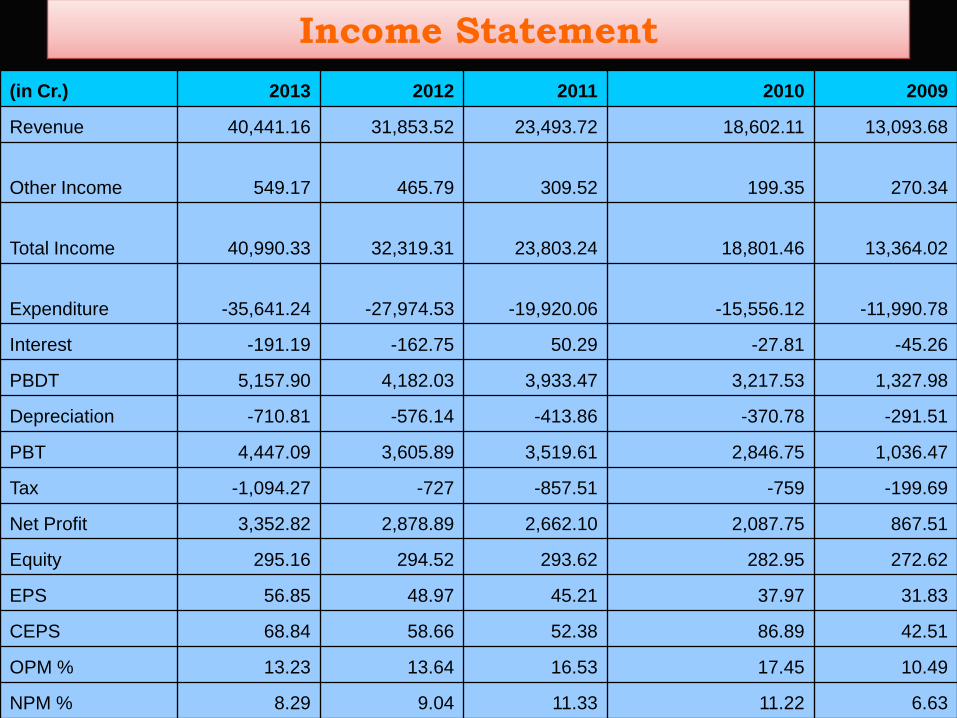

(in Cr.) 2013 2012 2011 2010 2009

Revenue 40,441.16 31,853.52 23,493.72 18,602.11 13,093.68

Other Income 549.17 465.79 309.52 199.35 270.34

Total Income 40,990.33 32,319.31 23,803.24 18,801.46 13,364.02

Expenditure -35,641.24 -27,974.53 -19,920.06 -15,556.12 -11,990.78

Interest -191.19 -162.75 50.29 -27.81 -45.26

PBDT 5,157.90 4,182.03 3,933.47 3,217.53 1,327.98

Depreciation -710.81 -576.14 -413.86 -370.78 -291.51

PBT 4,447.09 3,605.89 3,519.61 2,846.75 1,036.47

Tax -1,094.27 -727 -857.51 -759 -199.69

Net Profit 3,352.82 2,878.89 2,662.10 2,087.75 867.51

Equity 295.16 294.52 293.62 282.95 272.62

EPS 56.85 48.97 45.21 37.97 31.83

CEPS 68.84 58.66 52.38 86.89 42.51

OPM % 13.23 13.64 16.53 17.45 10.49

NPM % 8.29 9.04 11.33 11.22 6.63

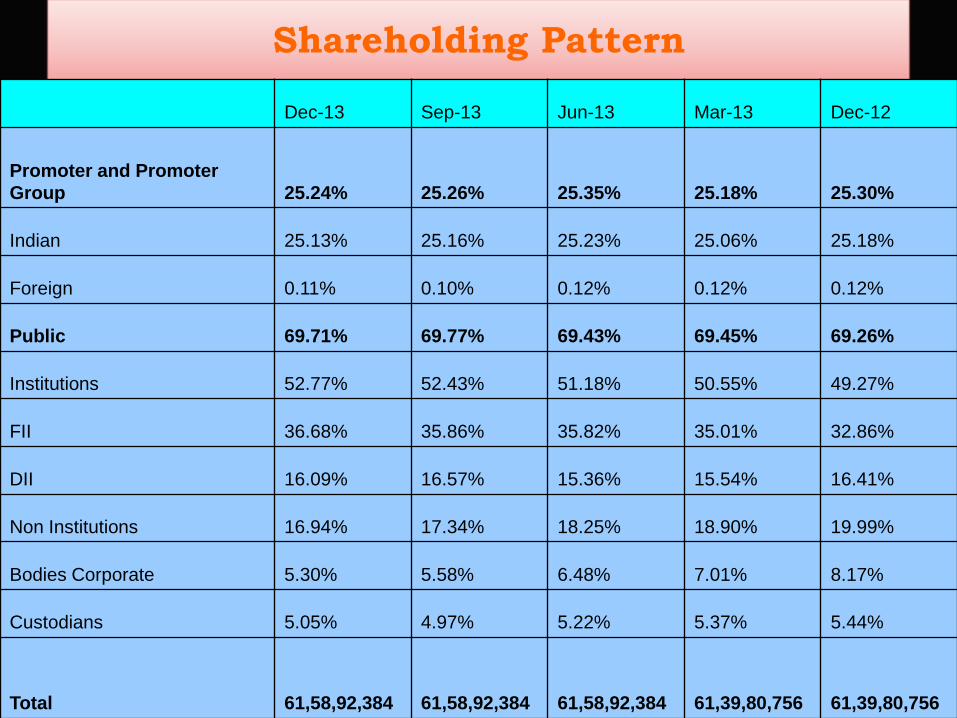

Shareholding Pattern

Dec-13 Sep-13 Jun-13 Mar-13 Dec-12

Promoter and Promoter

Group 25.24% 25.26% 25.35% 25.18% 25.30%

Indian 25.13% 25.16% 25.23% 25.06% 25.18%

Foreign 0.11% 0.10% 0.12% 0.12% 0.12%

Public 69.71% 69.77% 69.43% 69.45% 69.26%

Institutions 52.77% 52.43% 51.18% 50.55% 49.27%

FII 36.68% 35.86% 35.82% 35.01% 32.86%

DII 16.09% 16.57% 15.36% 15.54% 16.41%

Non Institutions 16.94% 17.34% 18.25% 18.90% 19.99%

Bodies Corporate 5.30% 5.58% 6.48% 7.01% 8.17%

Custodians 5.05% 4.97% 5.22% 5.37% 5.44%

Total 61,58,92,384 61,58,92,384 61,58,92,384 61,39,80,756 61,39,80,756

Tata Motors Limited is India's largest automobile company.

It is the leader in the commercial vehicles space in each segment, and among the

top three in passenger vehicles with winning products in the compact, midsize car

and utility vehicle segments.

It is the world's fourth largest truck and bus manufacturer in India.

The Company has over 3,500 touch points in terms of dealerships, sales, service

stations and a widespread spare parts network across the country.

The Tata Motors Group‟s over 55,000 employees are guided by the vision to be„

best in the manner in which we operate, best in the products we deliver.

Company Overview

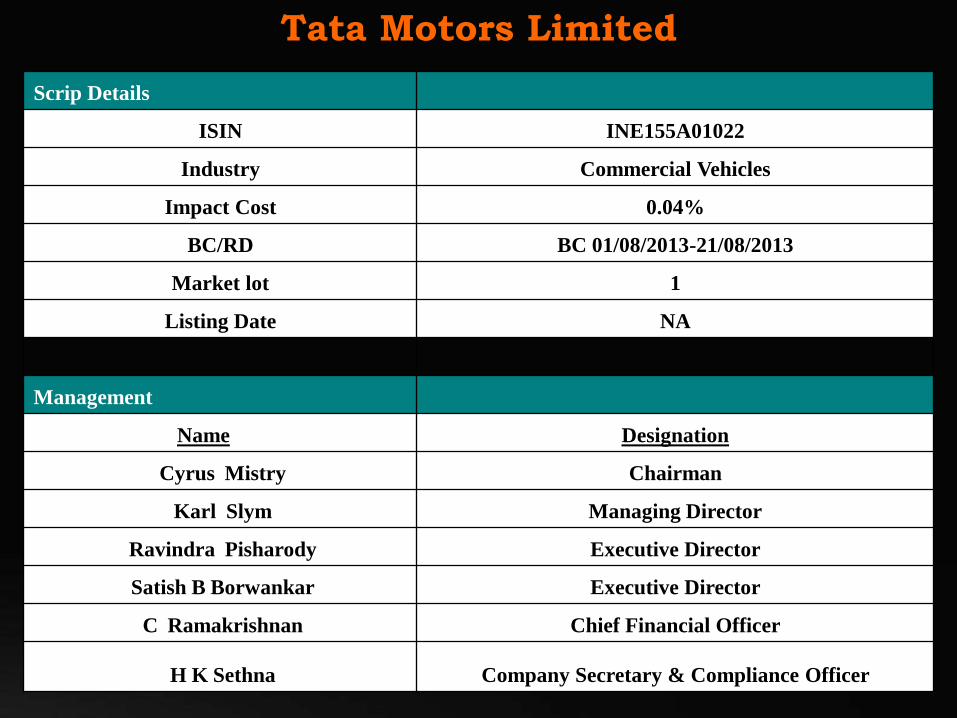

Tata Motors Limited

Scrip Details

ISIN INE155A01022

Industry Commercial Vehicles

Impact Cost 0.04%

BC/RD BC 01/08/2013-21/08/2013

Market lot 1

Listing Date NA

Management

Name Designation

Cyrus Mistry Chairman

Karl Slym Managing Director

Ravindra Pisharody Executive Director

Satish B Borwankar Executive Director

C Ramakrishnan Chief Financial Officer

H K Sethna Company Secretary & Compliance Officer

Income Statement

(in Cr.) 2013 2012 2011 2010 2009

Revenue 44,765.72 54,306.56 48,040.46 35,593.05 25,660.79

Other Income 2,088.20 574.08 183.26 1,853.45 925.97

Total Income 46,853.92 54,880.64 48,223.72 37,446.50 26,586.76

Expenditure -43,473.61 -50,714.25 -43,522.44 -32,479.25 -24,024.78

Interest -1,387.76 -1,218.62 -1,143.99 -1,103.84 -673.68

PBDT 1,992.55 2,947.77 3,557.29 3,863.41 1,888.30

Depreciation -1,817.62 -1,606.74 -1,360.77 -1,033.87 -874.54

PBT 174.93 1,341.03 2,196.52 2,829.54 1,013.76

Tax 126.88 -98.8 -384.7 -589.46 -12.5

Net Profit 301.81 1,242.23 1,811.82 2,240.08 1,001.26

Equity 638.07 634.75 637.71 570.6 514.05

EPS 0.93 3.9 30.28 42.37 22.7

CEPS 6.64 8.98 49.75 57.38 36.49

OPM % 7.55 7.67 9.79 13.96 9.98

NPM % 0.67 2.29 3.77 6.29 3.9

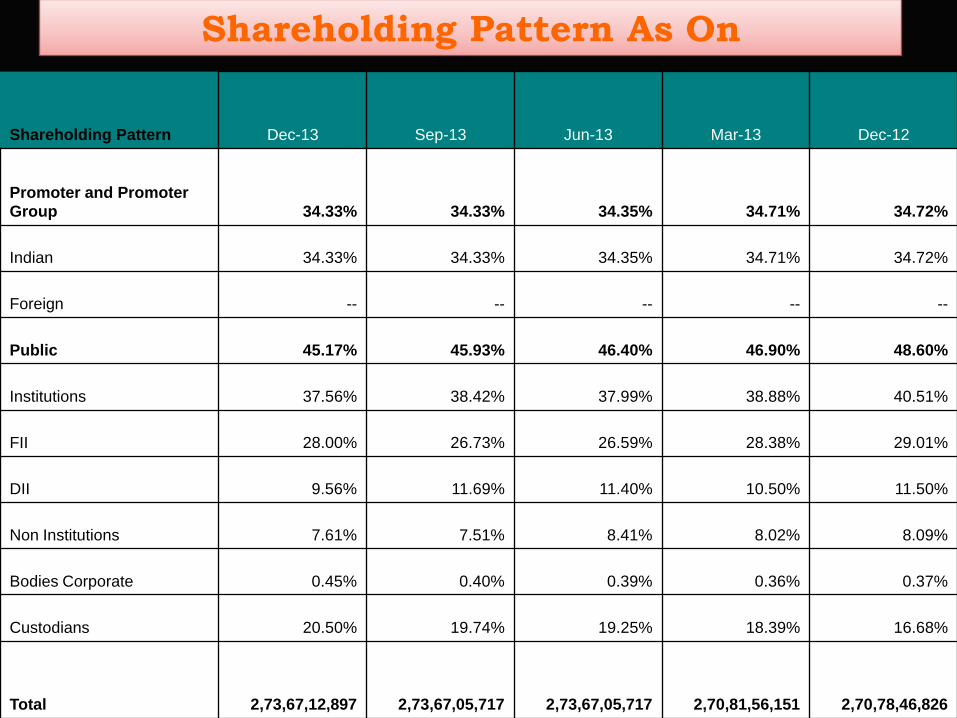

Shareholding Pattern As On

Shareholding Pattern Dec-13 Sep-13 Jun-13 Mar-13 Dec-12

Promoter and Promoter

Group 34.33% 34.33% 34.35% 34.71% 34.72%

Indian 34.33% 34.33% 34.35% 34.71% 34.72%

Foreign -- -- -- -- --

Public 45.17% 45.93% 46.40% 46.90% 48.60%

Institutions 37.56% 38.42% 37.99% 38.88% 40.51%

FII 28.00% 26.73% 26.59% 28.38% 29.01%

DII 9.56% 11.69% 11.40% 10.50% 11.50%

Non Institutions 7.61% 7.51% 8.41% 8.02% 8.09%

Bodies Corporate 0.45% 0.40% 0.39% 0.36% 0.37%

Custodians 20.50% 19.74% 19.25% 18.39% 16.68%

Total 2,73,67,12,897 2,73,67,05,717 2,73,67,05,717 2,70,81,56,151 2,70,78,46,826

Key Ratio

I. ACTIVITY RATIO M & M TATAMOT Maruti

1) Inventory Turnover 9.50% 9.88% 26.78%

2) Receivables Turnover 14.29 Times 17,25 Times 33.50 Times

3) Payable Turnover 2.76 Times 2.16 Times 6.04 Times

II.PROFITABILITY RATIO M & M TATAMOT Maruti

1) Gross Profit Margin 11.00% 11.22% 11.19%

2) Operating Profit Margin 14.00% 13.11% 10.30%

3) Pre - Tax Margin 8.12% 7.22% 6.15%

4) Return on Assets 7.18% 5.77% 1.47%

5) Return on Capital Employed 14.78% 17.93% 16.00%

6) Return on Equity 18.26% 26.04% 15.02%

III. SOLVENCY RATIO M & M TATAMOT Maruti

1) Debt to Asset 0.74 0.59 o.79

2) Debt to Equity 1.43 1.43 0.09

3) Debt to Capital 1.44 1.4 8.24

4) Interest Coverage 3.43 4.84 14.55

IV. LIQUIDITY RATIO M & M TATAMOT Maruti

1) Current Ratio 1.21 0.82 0.85

2) Quick Ratio 1.56 0.7 0.73

V. VALUATION RATIO M & M TATAMOT Maruti

1) Earning Per Share 67.87 30.66 80.4

2) Dividend Payout 19.15 6.58 9.55

3) Retention 18.15 5.58 8.55

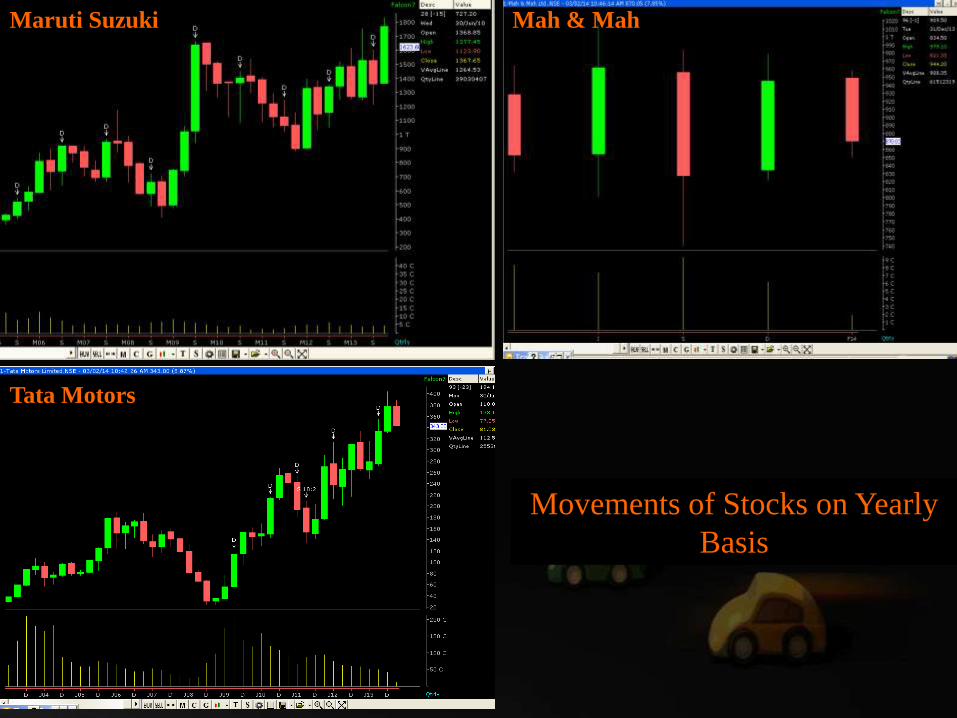

Maruti Suzuki Mah & Mah

Tata Motors

Movements of Stocks on Yearly

Basis

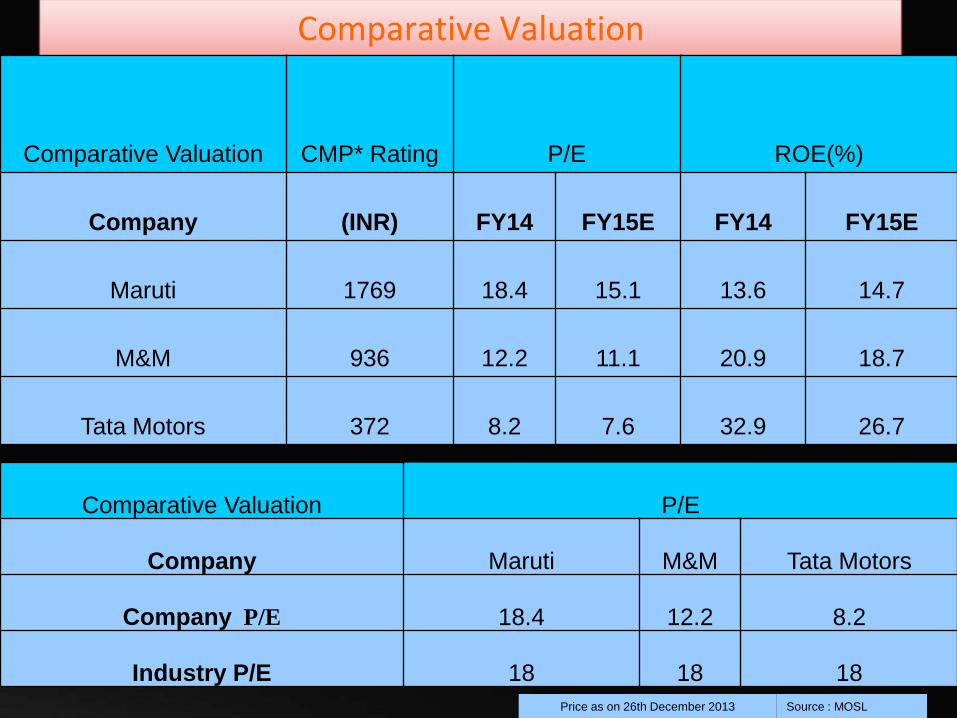

Comparative Valuation

Comparative Valuation CMP* Rating P/E ROE(%)

Company (INR) FY14 FY15E FY14 FY15E

Maruti 1769 18.4 15.1 13.6 14.7

M&M 936 12.2 11.1 20.9 18.7

Tata Motors 372 8.2 7.6 32.9 26.7

Price as on 26th December 2013 Source : MOSL

Comparative Valuation P/E

Company Maruti M&M Tata Motors

Company P/E 18.4 12.2 8.2

Industry P/E 18 18 18

Key Financial Indicators

Key Financial Indicators

EBITDA Margins

(%) EPS (INR) EPS Growth(%)

Company FY14 FY15E FY14 FY15E FY14 FY15E

Maruti Suzuki 12.1 12.8 96.4 117.3 20 23.4

M&M 14.5 14.5 76.5 84.7 25.6 10.6

Tata Motors 16.2 15.5 45.3 48.7 41.2 7.6

Source : BSE

Peer Group Comparison

Quarterly Trends

Mahindra &

Mahindra Maruti Suzuki Tata Motors

LTP 885 1,620.70 336.6

Change % -0.61 -0.9 -3.79

52 W H/L 1,026.45/741.50 1,864.00/1,217.00 405.00/252.10

Results (in Cr.) View in

(Million) 13-Sep 13-Dec 13-Sep

Sales 8,929.57 10,893.84 8,868.45

PAT 989.5 681.15 -803.53

Equity 295.16 151.04 643.78

Face Value 5 5 2

Source : BSE

Peer Group Comparison

Annual TrendsMahindra &

Mahindra Maruti Suzuki Tata Motors

LTP 885 1,620.70 336.6

Change % -0.61 -0.9 -3.79

52 W H/L 1,026.45/741.50 1,864.00/1,217.00 405.00/252.10

Results (in Cr.) View in (Million) 13-Mar 13-Mar 13-Mar

Sales 40,441.16 43,587.93 44,765.72

PAT 3,352.82 2,392.13 301.81

Equity 295.16 151.04 638.07

Face Value 5 5 2

Source : BSE

Maruti Suzuki : We believe the Gujarat facility arrangement through Suzuki 100%

subsidiary is beneficial to MSIL.

MSIL would benefit from similar free cash flows but without any capex for 1st phase of

investment, thus improving overall profits (with treasury income) and return ratios.

Suzuki, Japan intention is not to profit from this investment directly but through MSIL

(given its 56% stake). Moreover, with contract manufacturing through Suzuki, MSIL

can channelize its energy towards more value added activities like marketing/R&D.

Impact on financials of the Gujarat facility though would be seen only in FY17.

Mahindra & Mahindra Ltd.: said, We have achieved a cumulative domestic growth till

January 2014 of 23%. We expect the good run to continue for the rest of the quarter

Tatamotors Car sales stood at 8,663 units (est 8,000 units), a decline of 25% YoY

(+30% MoM). UV sales were at 2,635 units (est 2,900 units), a decline of 36% YoY (-

6% MoM). We have built-in de-growth of 37% for the PV segment for FY14.

The stock trades at 7.2x/5.8x FY15E/16E consol. EPS of INR48.7/60.5 respectively. So

we suggest to buy TATAMOTORS with Target price of % 500/-

Summary