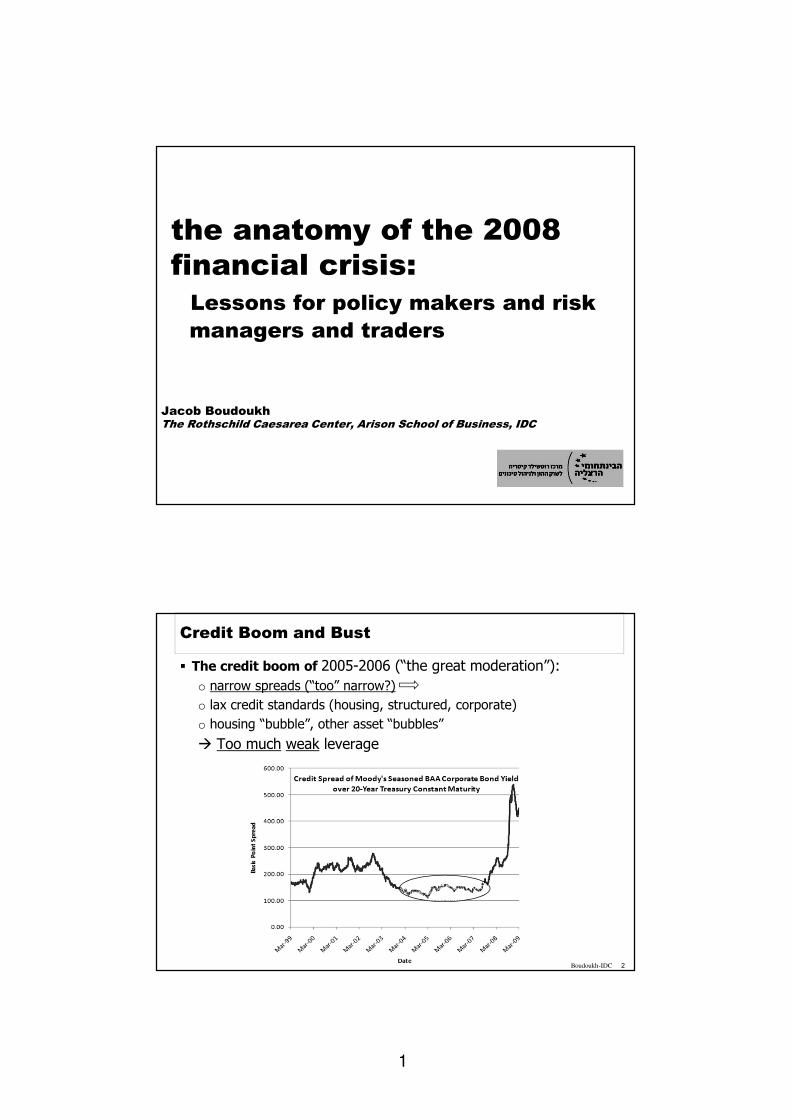

the anatomy of the 2008 financial crisis

37

1 1 the anatomy of the 2008 financial crisis: Lessons for policy makers and risk managers and traders Jacob Boudoukh The Rothschild Caesarea Center, Arison School of Business, IDC 2 Boudoukh-IDC Credit Boom and Bust The credit boom of 2005-2006 (“the great moderation”): o narrow spreads (“too” narrow?) o lax credit standards (housing, structured, corporate) o housing “bubble”, other asset “bubbles” Too much weak leverage

Transcript of the anatomy of the 2008 financial crisis

1

1

the anatomy of the 2008

financial crisis:

Lessons for policy makers and risk

managers and traders

Jacob BoudoukhThe Rothschild Caesarea Center, Arison School of Business, IDC

2Boudoukh-IDC

Credit Boom and Bust

� The credit boom of 2005-2006 (“the great moderation”):

o narrow spreads (“too” narrow?)

o lax credit standards (housing, structured, corporate)

o housing “bubble”, other asset “bubbles”

� Too much weak leverage

2

3Boudoukh-IDC

Credit Boom and Bust (continued)

� A (perhaps severe) recession was, it seems, inevitable

� But how did we get to a global systemic financial crisis comparable only to the great depression:

o widespread failures of FIs,

o near-collapse of the fin system

o freeze of the credit system

o … Resulting in severe real disruptions:

• 3%+ drop in world GDP

• 12%+ drop in global trade

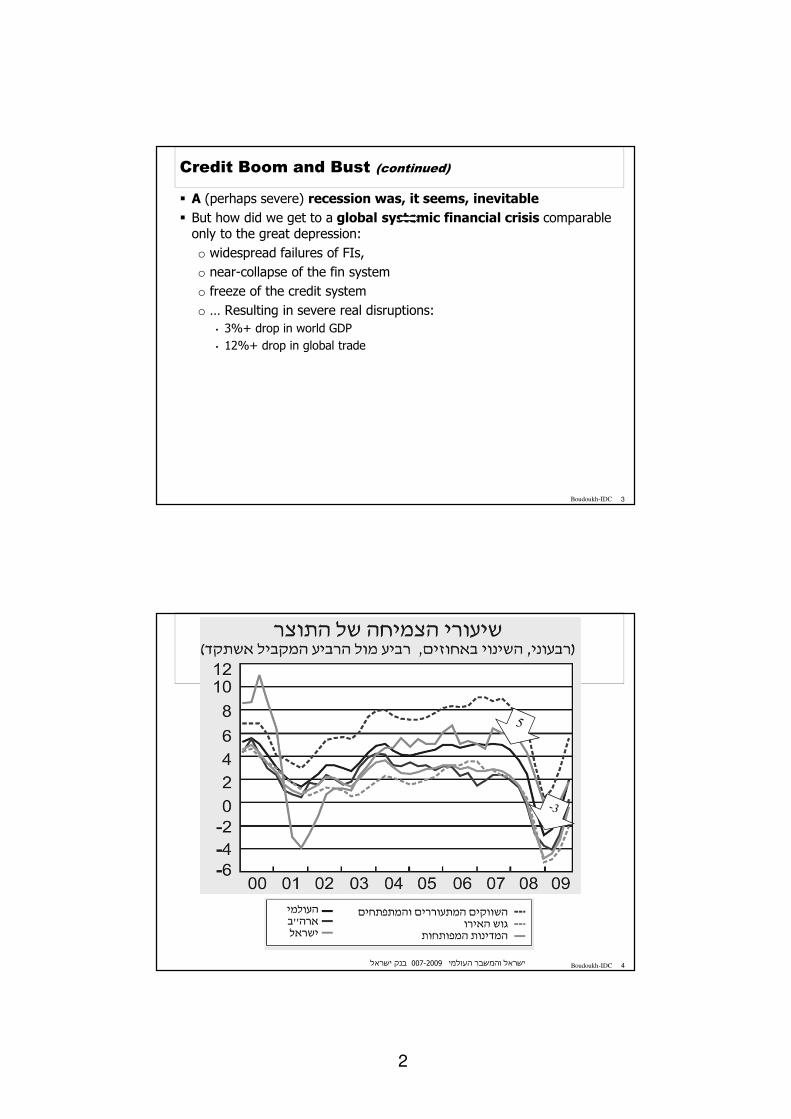

4Boudoukh-IDC בנק ישראל007-2009ישראל והמשבר העולמי

3

5Boudoukh-IDC בנק ישראל007-2009ישראל והמשבר העולמי

6Boudoukh-IDC

My goal today:

explain the underpinnings of the systemic liquidity freeze that propagated through FI’s in late 08

…then, get you thinking about policy, crises, and relevance

4

7Boudoukh-IDCSource: IMF Report, 2008

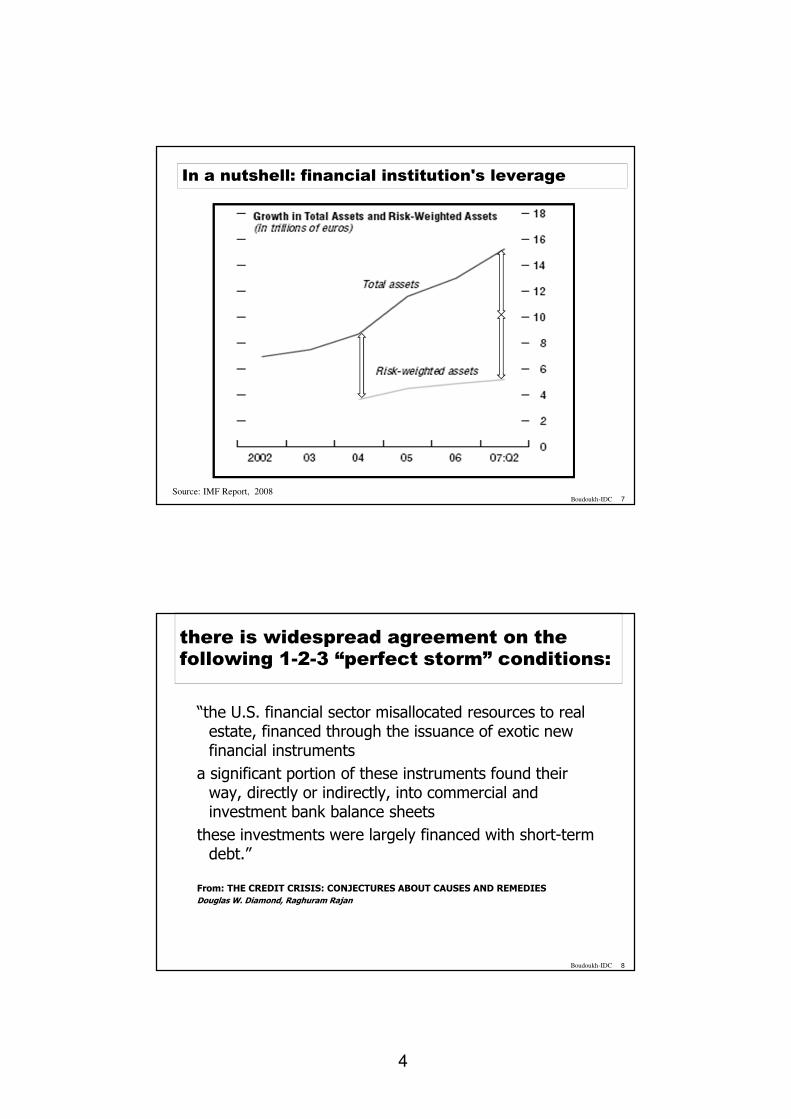

In a nutshell: financial institution's leverage

8Boudoukh-IDC

there is widespread agreement on the following 1-2-3 “perfect storm” conditions:

“the U.S. financial sector misallocated resources to real estate, financed through the issuance of exotic new financial instruments

a significant portion of these instruments found their way, directly or indirectly, into commercial and investment bank balance sheets

these investments were largely financed with short-term debt.”

From: THE CREDIT CRISIS: CONJECTURES ABOUT CAUSES AND REMEDIES Douglas W. Diamond, Raghuram Rajan

5

9Boudoukh-IDC

Outline

� The run-up to the crisis:

how financial institutions manufactured, then warehoused catastrophic risk

� The crisis

� Regulatory Reform & Some Open Questions

� Local lessons

� Literature aspect for sure is incomplete …

10Boudoukh-IDC

The MBS Market

� Political pressure favoring home ownership resulted in regulatory blind eye to deterioration of lending standards

� Low short term rates (the “Greenspan put”) made the all-so-wrong ARMs (2/28, 3/27) the only game in town, setting up the timer on the bomb

� Global imbalances made the search for yield pickup very aggressive

� Then came the banks…

6

11Boudoukh-IDC

Subprime and Alt-A: low FICO, weak documentation (at best), high leverage

Source: Gorton – the Panic of 2007

Non conforming come in many flavors: Low FICO, Thin FICO (XS

spread FICO), No doc, negative amortization, No Debt/Income,…

Here are some stats:

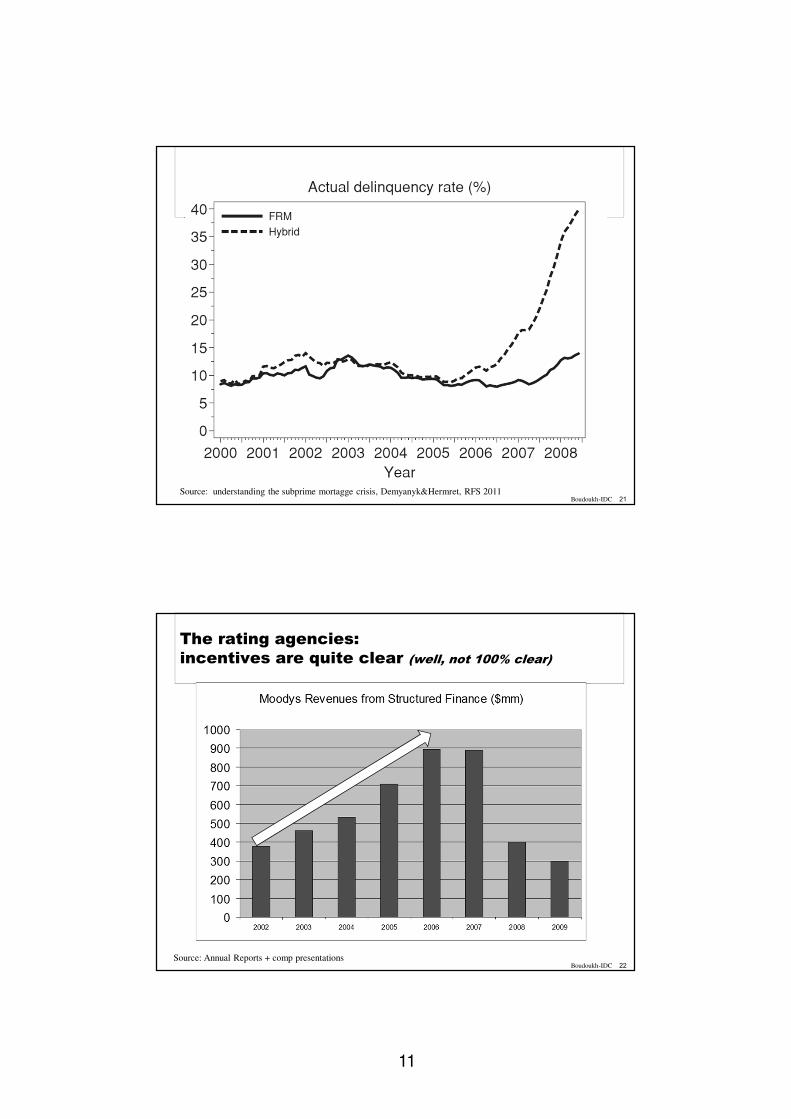

12Boudoukh-IDCSource: understanding the subprime mortagge crisis, Demyanyk&Hermret, RFS 2011

7

13Boudoukh-IDC

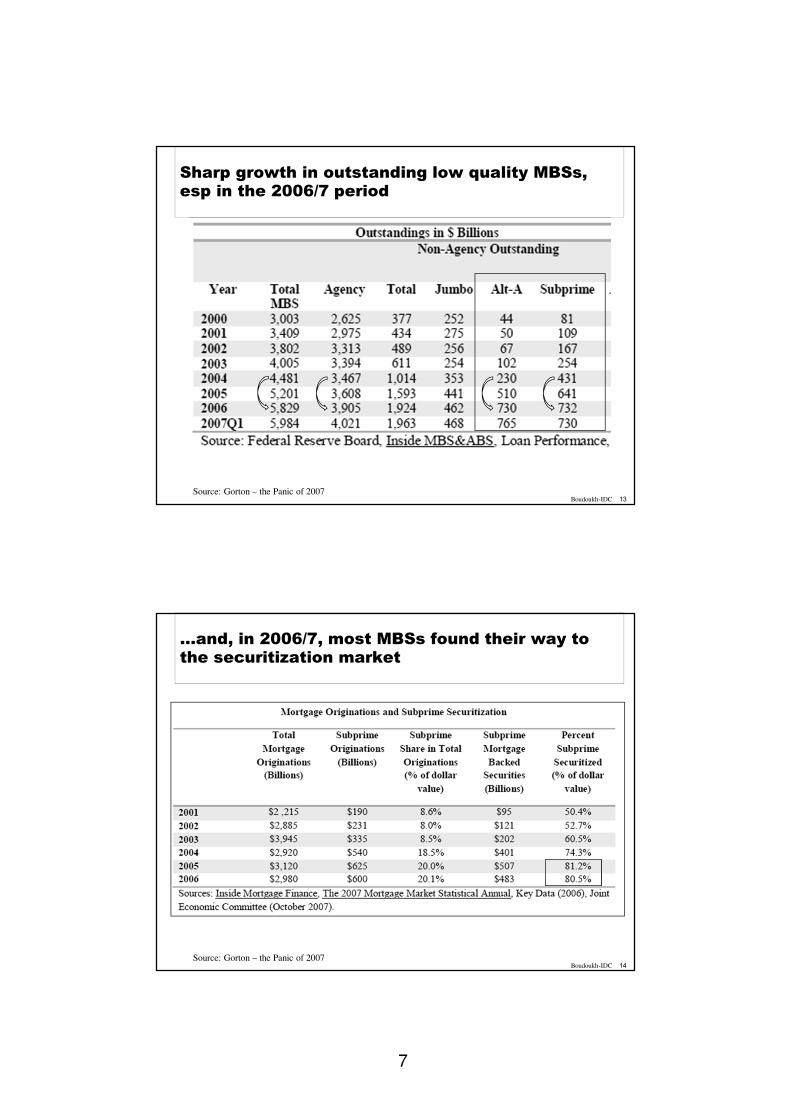

Sharp growth in outstanding low quality MBSs,esp in the 2006/7 period

Source: Gorton – the Panic of 2007

14Boudoukh-IDC

…and, in 2006/7, most MBSs found their way to the securitization market

Source: Gorton – the Panic of 2007

8

15Boudoukh-IDC

Speaking of “securitization”,

where is the mezzanine? A, B, or C?

16Boudoukh-IDC

enter “the optimizers”

Source: Gorton – the Panic of 2007, IMF stability report, 2008

9

17Boudoukh-IDC

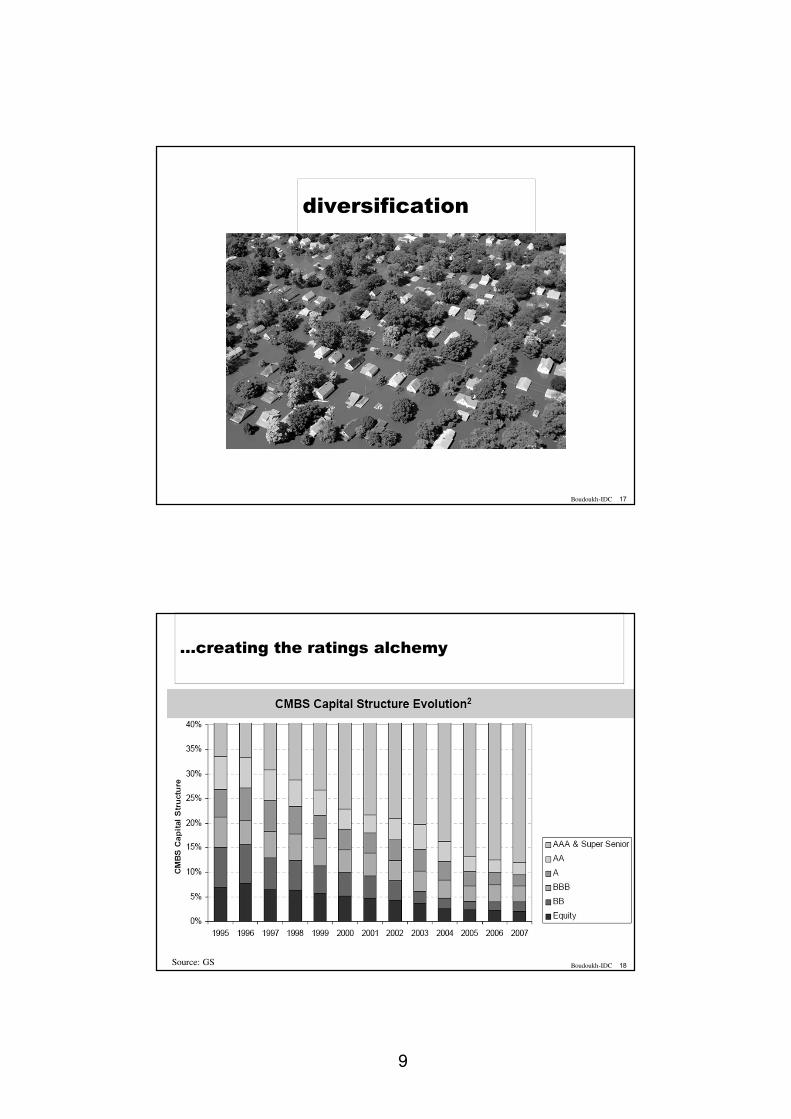

diversification

18Boudoukh-IDC

…creating the ratings alchemy

Source: GS

10

19Boudoukh-IDC

the Binomial Expansion Technique – you BET…

Source: Moodys

20Boudoukh-IDC

…this approach has been, later on, extended to

the triple binomial, with tails still remaining comfortably thin

Source: Moodys

11

21Boudoukh-IDCSource: understanding the subprime mortagge crisis, Demyanyk&Hermret, RFS 2011

22Boudoukh-IDC

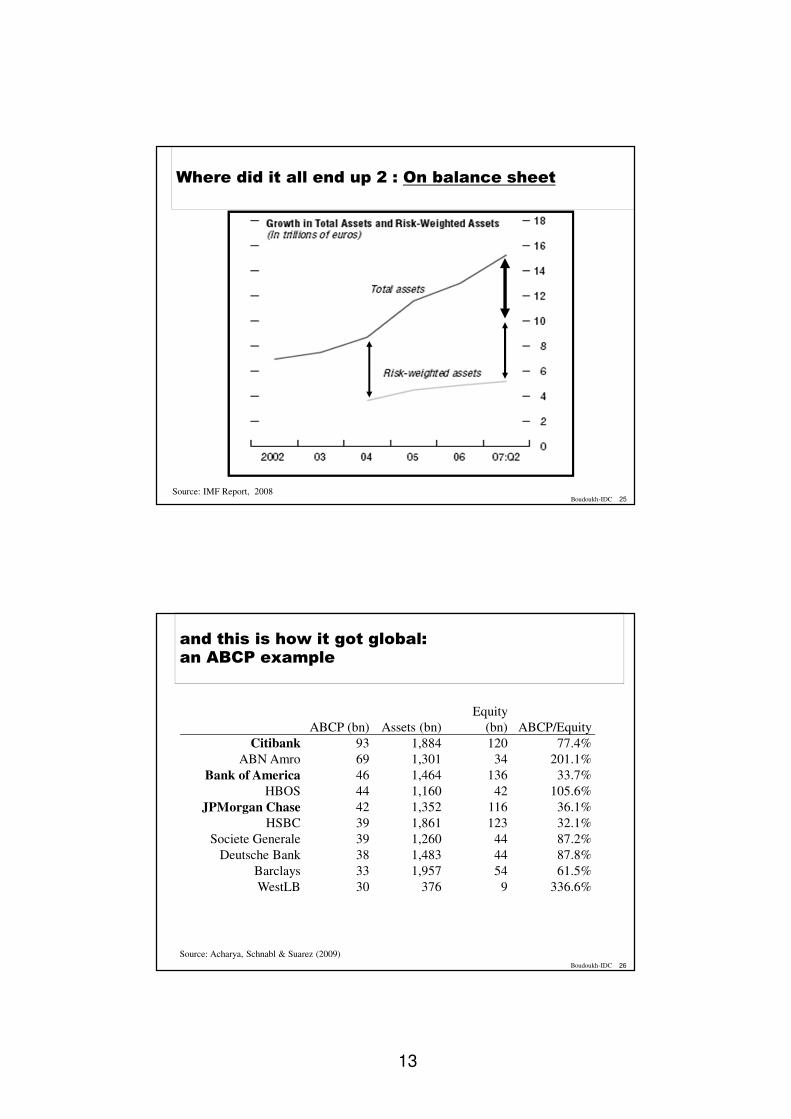

The rating agencies:

incentives are quite clear (well, not 100% clear)

Source: Annual Reports + comp presentations

12

23Boudoukh-IDCSource: IMF stability report, APRIL 2008

24Boudoukh-IDC

Where did it all end up 1 : Off balance sheetABCP Growth: Jan 2001 - June 2007

13

25Boudoukh-IDC

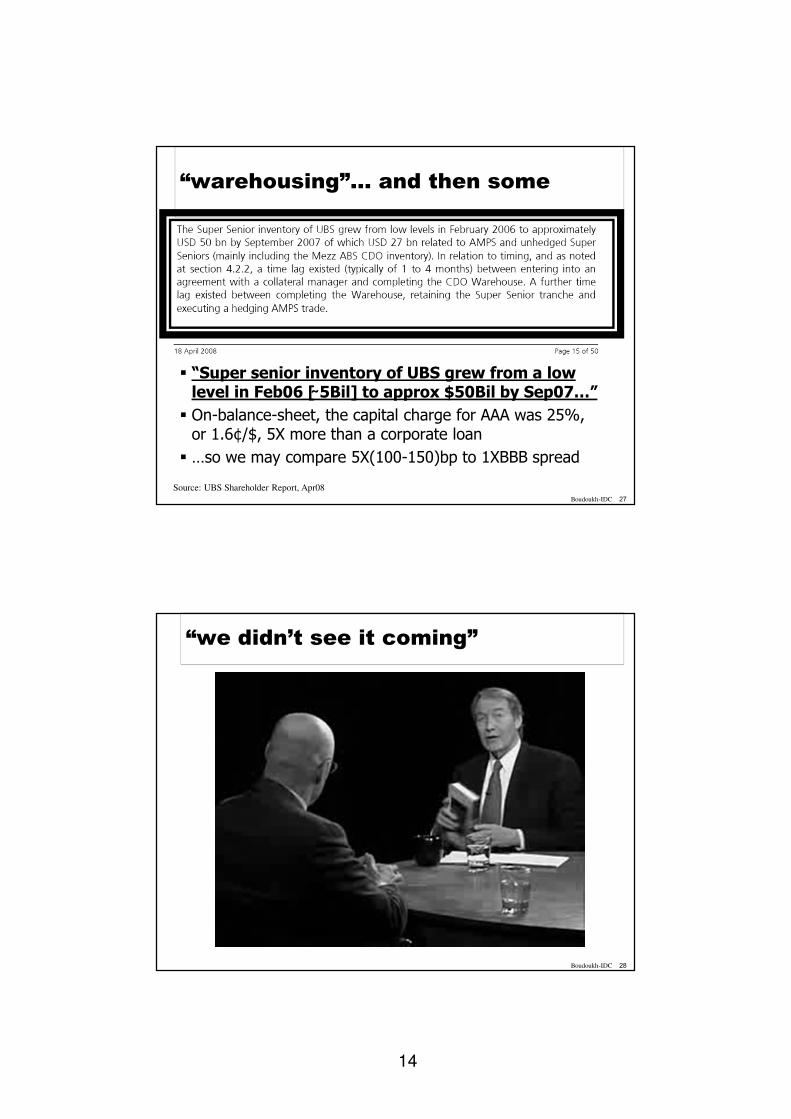

Where did it all end up 2 : On balance sheet

Source: IMF Report, 2008

26Boudoukh-IDC

and this is how it got global:an ABCP example

ABCP (bn) Assets (bn)

Equity

(bn) ABCP/Equity

Citibank 93 1,884 120 77.4%

ABN Amro 69 1,301 34 201.1%

Bank of America 46 1,464 136 33.7%

HBOS 44 1,160 42 105.6%

JPMorgan Chase 42 1,352 116 36.1%

HSBC 39 1,861 123 32.1%

Societe Generale 39 1,260 44 87.2%

Deutsche Bank 38 1,483 44 87.8%

Barclays 33 1,957 54 61.5%

WestLB 30 376 9 336.6%

Source: Acharya, Schnabl & Suarez (2009)

14

27Boudoukh-IDC

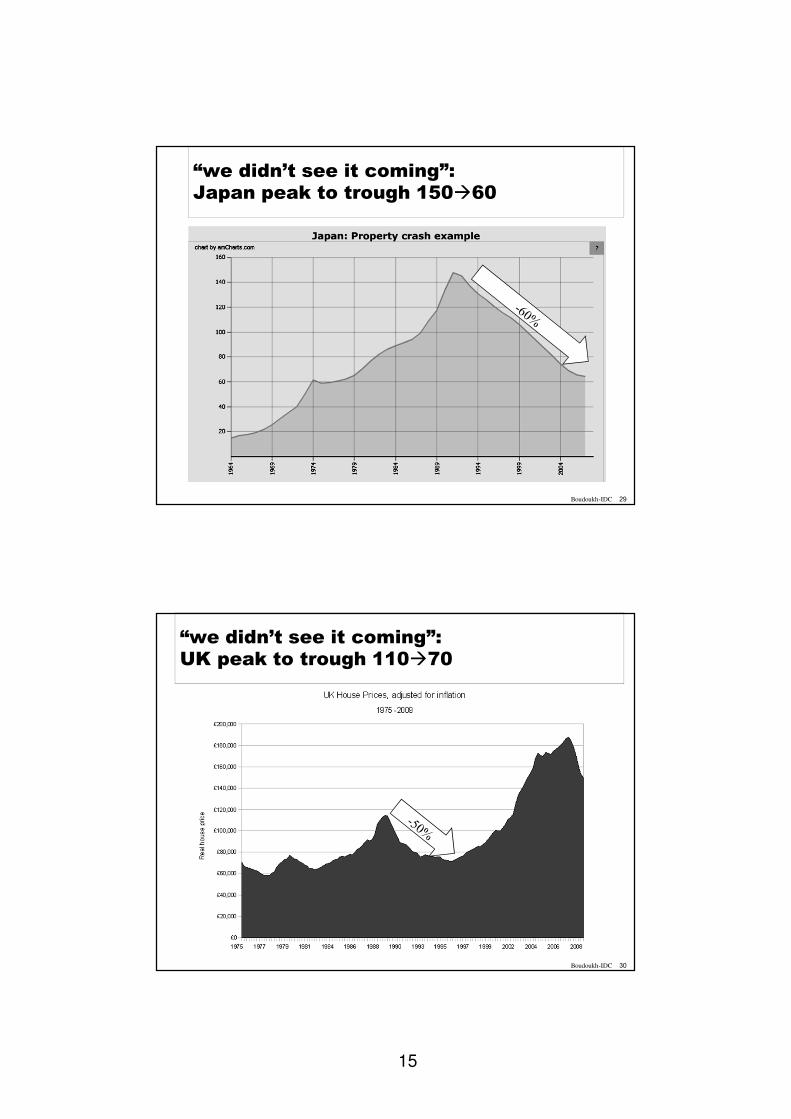

“warehousing”… and then some

� “Super senior inventory of UBS grew from a low level in Feb06 [̴ 5Bil] to approx $50Bil by Sep07…”

� On-balance-sheet, the capital charge for AAA was 25%, or 1.6¢/$, 5X more than a corporate loan

� …so we may compare 5X(100-150)bp to 1XBBB spread

Source: UBS Shareholder Report, Apr08

28Boudoukh-IDC

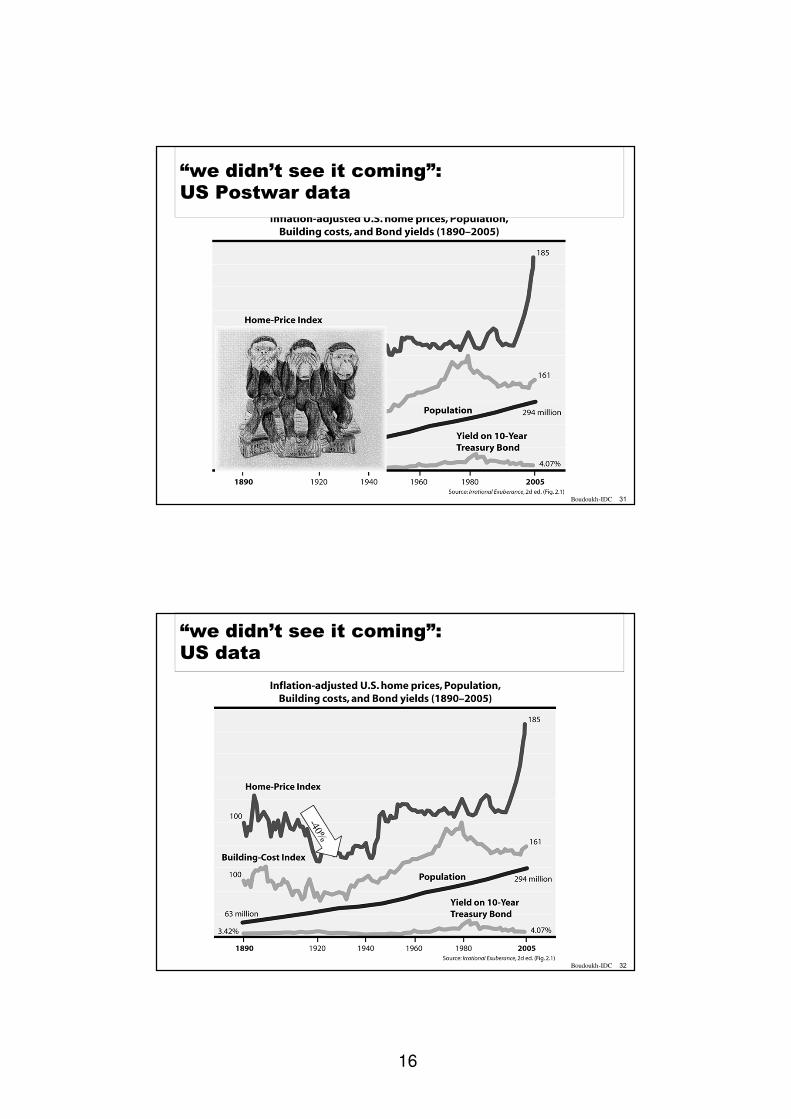

“we didn’t see it coming”

15

29Boudoukh-IDC

“we didn’t see it coming”:Japan peak to trough 150�60

30Boudoukh-IDC

“we didn’t see it coming”:UK peak to trough 110�70

16

31Boudoukh-IDC

“we didn’t see it coming”:US Postwar data

32Boudoukh-IDC

“we didn’t see it coming”:US data

17

33Boudoukh-IDC

Summary of the run-up to the crisis

� We told the story of commercial banks ($11T)

� We could also tell the story of broker dealers ($2.5T)

� We could also tell the story of the GSEs ($3T)

� We could also tell the story of insurance co’s(AIG) ($6T)

� We could also tell the story of hedge funds ($5.5T)

� We could also tell the story of money market funds

� There is a common theme!

34Boudoukh-IDC

RISK TAKING INCENTIVE

� The main offenders were the GSE’s, TBTF-VLCFI’s

including commercial banks, broker dealers & large

insurers

� Common to all was (still is!) that they are

SYSTEMIC and hence

o could raise senior debt and debt capital at slim

margins

o… and use access regulatory loopholes allowing

them to amass AAA risk on- & off-balance sheet

with little to no extra risk capital

18

35Boudoukh-IDC

RISK TAKING INCENTIVE (cont’d)

Observations/claims:

� INCENTIVES of traders, senior mgmt and

shareholders aren't entirely misaligned (case in point: the

GSEs)

� Global imbalances and low short term rates indeed

contributed to excess demand for “safe risk” (AAA) …

but wouldn’t have, in and of themselves, generated

the FINANCIAL meltdown

� Free TBTF status is an ongoing wealth transfer from

the implicit guarantor (���) to the TBTF Fis

(bondholders… stockholders…)

36Boudoukh-IDC

Causes: brief summary

� Incentive misalignment: allowing to book profit and not pay for risk

� The securitization model going awry: credit risk completely removed from risk underwriter

� No/low capital against off- and on-balance sheet risks

� Liquidity gap (short term financing – shadow banking)

� Mispriced risks (eg Subprime linked CDSs)

19

37Boudoukh-IDC

Outline

� The runup to the crisis: how financial institutions manufactured, then warehoused catastrophic risk

� The crisis

� Regulatory Reform

& Some Open

Questions

� Local lessons

38Boudoukh-IDC

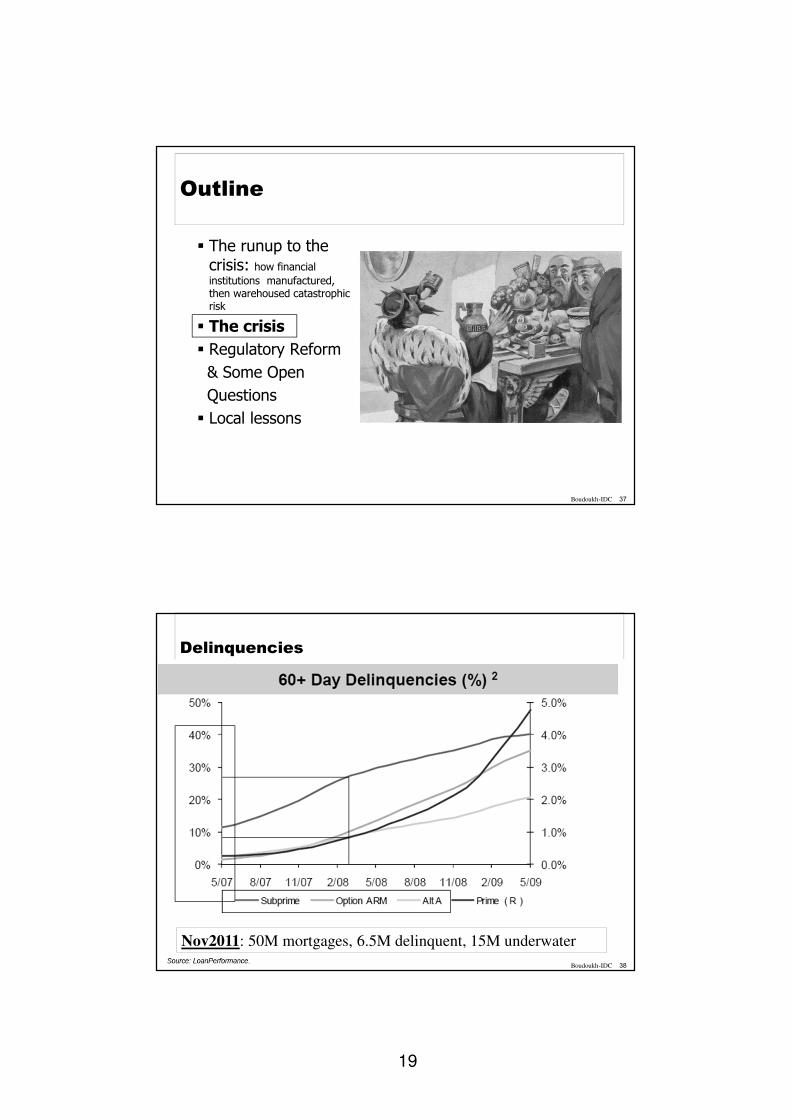

Delinquencies

Nov2011: 50M mortgages, 6.5M delinquent, 15M underwater

20

39Boudoukh-IDC

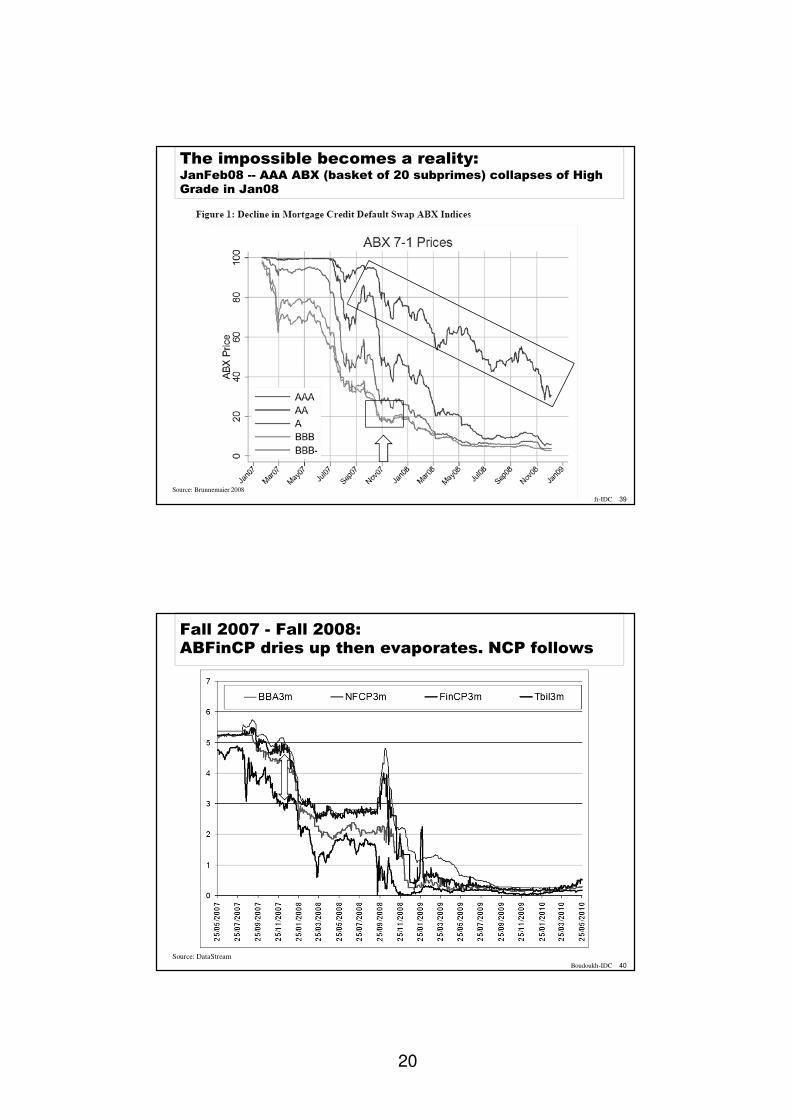

The impossible becomes a reality:JanFeb08 -- AAA ABX (basket of 20 subprimes) collapses of High

Grade in Jan08

Source: Brunnemaier 2008

40Boudoukh-IDC

Fall 2007 - Fall 2008: ABFinCP dries up then evaporates. NCP follows

Source: DataStream

21

41Boudoukh-IDC

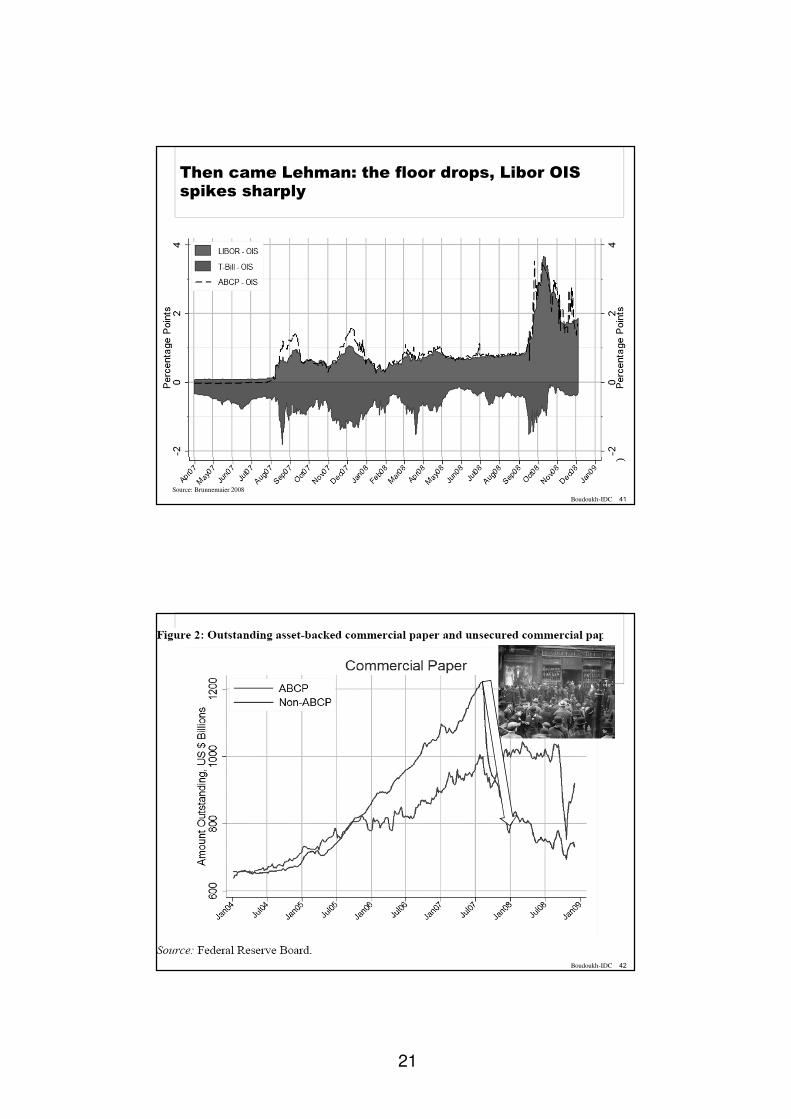

Then came Lehman: the floor drops, Libor OIS spikes sharply

Source: Brunnemaier 2008

42Boudoukh-IDC

22

43Boudoukh-IDC

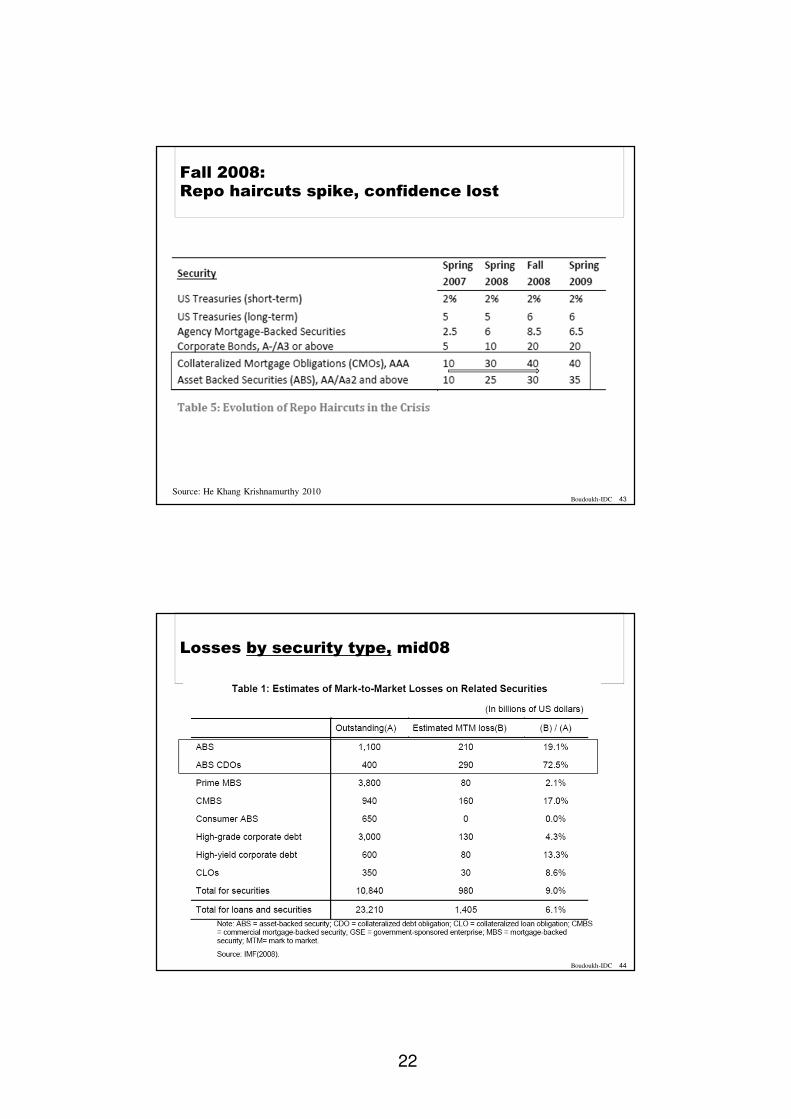

Fall 2008:Repo haircuts spike, confidence lost

Source: He Khang Krishnamurthy 2010

44Boudoukh-IDC

Losses by security type, mid08

23

45Boudoukh-IDC

Losses by type of FI, up to march 2009

Source: He Khang Krishnamurthy 2010

From a risk mgmt perspective: a complete disaster in assessing

PD (tail risk) and LGD (recovery)

46Boudoukh-IDC

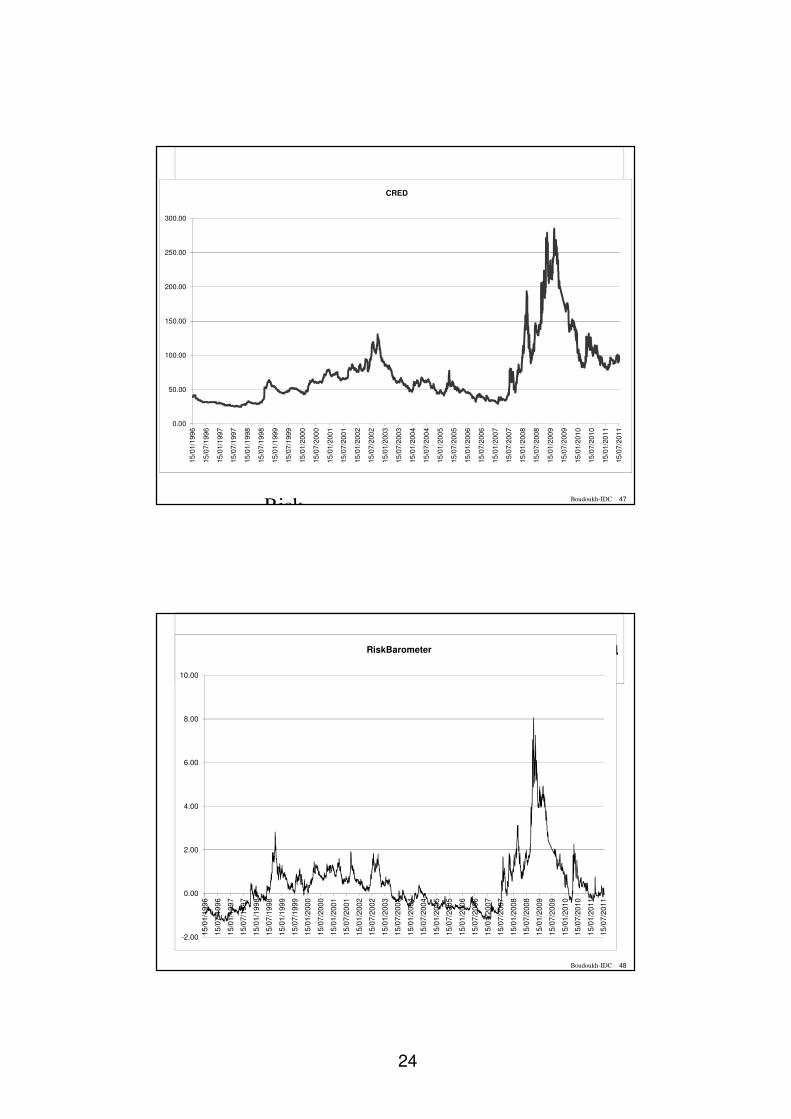

What did a complete outside see?Risk measures: equity, bnk, fx (left) credit (right)

Source: Own calculations

24

47Boudoukh-IDC

Risk

0.00

50.00

100.00

150.00

200.00

250.00

300.00

15

/01/1

99

6

15

/07/1

99

6

15

/01/1

99

7

15

/07/1

99

7

15

/01/1

99

8

15

/07/1

99

8

15

/01/1

99

9

15

/07/1

99

9

15

/01/2

00

0

15

/07/2

00

0

15

/01/2

00

1

15

/07/2

00

1

15

/01/2

00

2

15

/07/2

00

2

15

/01/2

00

3

15

/07/2

00

3

15

/01/2

00

4

15

/07/2

00

4

15

/01/2

00

5

15

/07/2

00

5

15

/01/2

00

6

15

/07/2

00

6

15

/01/2

00

7

15

/07/2

00

7

15

/01/2

00

8

15

/07/2

00

8

15

/01/2

00

9

15

/07/2

00

9

15

/01/2

01

0

15

/07/2

01

0

15

/01/2

01

1

15

/07/2

01

1

CRED

48Boudoukh-IDC

ברומטר סיכו� מנורמל לטרו� המשבר

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

15/0

1/1

996

15/0

7/1

996

15/0

1/1

997

15/0

7/1

997

15/0

1/1

998

15/0

7/1

998

15/0

1/1

999

15/0

7/1

999

15/0

1/2

000

15/0

7/2

000

15/0

1/2

001

15/0

7/2

001

15/0

1/2

002

15/0

7/2

002

15/0

1/2

003

15/0

7/2

003

15/0

1/2

004

15/0

7/2

004

15/0

1/2

005

15/0

7/2

005

15/0

1/2

006

15/0

7/2

006

15/0

1/2

007

15/0

7/2

007

15/0

1/2

008

15/0

7/2

008

15/0

1/2

009

15/0

7/2

009

15/0

1/2

010

15/0

7/2

010

15/0

1/2

011

15/0

7/2

011

RiskBarometer

25

49Boudoukh-IDCSource: Own calculations

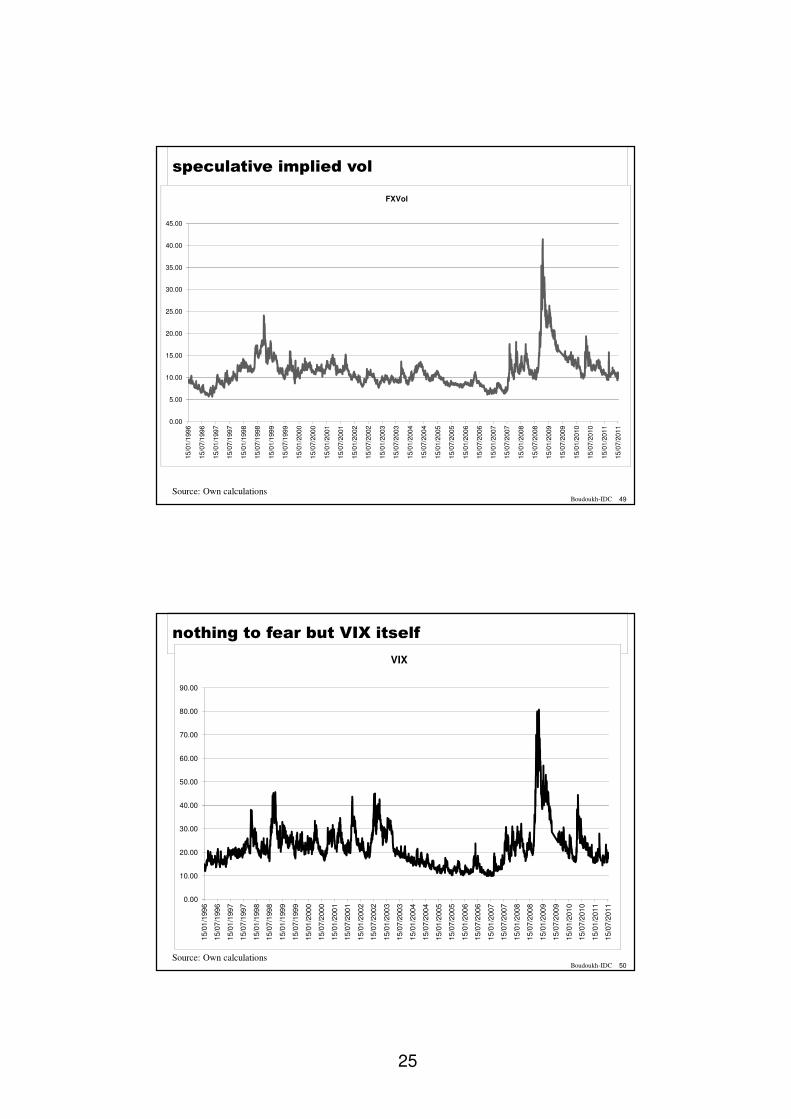

speculative implied vol

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

15/0

1/1

996

15/0

7/1

996

15/0

1/1

997

15/0

7/1

997

15/0

1/1

998

15/0

7/1

998

15/0

1/1

999

15/0

7/1

999

15/0

1/2

000

15/0

7/2

000

15/0

1/2

001

15/0

7/2

001

15/0

1/2

002

15/0

7/2

002

15/0

1/2

003

15/0

7/2

003

15/0

1/2

004

15/0

7/2

004

15/0

1/2

005

15/0

7/2

005

15/0

1/2

006

15/0

7/2

006

15/0

1/2

007

15/0

7/2

007

15/0

1/2

008

15/0

7/2

008

15/0

1/2

009

15/0

7/2

009

15/0

1/2

010

15/0

7/2

010

15/0

1/2

011

15/0

7/2

011

FXVol

50Boudoukh-IDCSource: Own calculations

nothing to fear but VIX itself

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

15/0

1/1

99

6

15/0

7/1

99

6

15/0

1/1

99

7

15/0

7/1

99

7

15/0

1/1

99

8

15/0

7/1

99

8

15/0

1/1

99

9

15/0

7/1

99

9

15/0

1/2

00

0

15/0

7/2

00

0

15/0

1/2

00

1

15/0

7/2

00

1

15/0

1/2

00

2

15/0

7/2

00

2

15/0

1/2

00

3

15/0

7/2

00

3

15/0

1/2

00

4

15/0

7/2

00

4

15/0

1/2

00

5

15/0

7/2

00

5

15/0

1/2

00

6

15/0

7/2

00

6

15/0

1/2

00

7

15/0

7/2

00

7

15/0

1/2

00

8

15/0

7/2

00

8

15/0

1/2

00

9

15/0

7/2

00

9

15/0

1/2

01

0

15/0

7/2

01

0

15/0

1/2

01

1

15/0

7/2

01

1

VIX

26

51Boudoukh-IDCSource: Own calculations

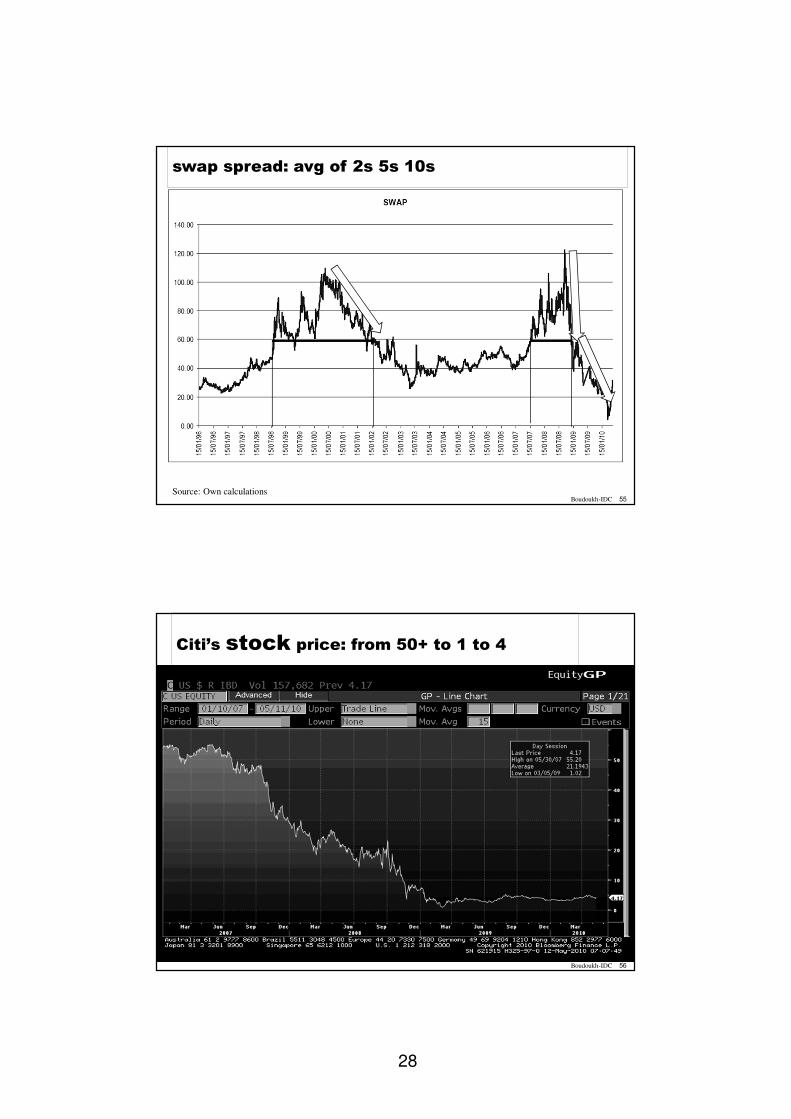

swap spread: avg of 2s 5s 10s

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

15/0

1/1

996

15/0

7/1

996

15/0

1/1

997

15/0

7/1

997

15/0

1/1

998

15/0

7/1

998

15/0

1/1

999

15/0

7/1

999

15/0

1/2

000

15/0

7/2

000

15/0

1/2

001

15/0

7/2

001

15/0

1/2

002

15/0

7/2

002

15/0

1/2

003

15/0

7/2

003

15/0

1/2

004

15/0

7/2

004

15/0

1/2

005

15/0

7/2

005

15/0

1/2

006

15/0

7/2

006

15/0

1/2

007

15/0

7/2

007

15/0

1/2

008

15/0

7/2

008

15/0

1/2

009

15/0

7/2

009

15/0

1/2

010

15/0

7/2

010

15/0

1/2

011

15/0

7/2

011

SWAP

52Boudoukh-IDC

RiskBarometer:combined measure, normalized to pre-crisis distribution

Source: Own calculations

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

15/0

1/1

996

15/0

7/1

996

15/0

1/1

997

15/0

7/1

997

15/0

1/1

998

15/0

7/1

998

15/0

1/1

999

15/0

7/1

999

15/0

1/2

000

15/0

7/2

000

15/0

1/2

001

15/0

7/2

001

15/0

1/2

002

15/0

7/2

002

15/0

1/2

003

15/0

7/2

003

15/0

1/2

004

15/0

7/2

004

15/0

1/2

005

15/0

7/2

005

15/0

1/2

006

15/0

7/2

006

15/0

1/2

007

15/0

7/2

007

15/0

1/2

008

15/0

7/2

008

15/0

1/2

009

15/0

7/2

009

15/0

1/2

010

15/0

7/2

010

15/0

1/2

011

15/0

7/2

011

RiskBarometer

27

53Boudoukh-IDC

54Boudoukh-IDC

Then came the bailout

� lesser of two evils?

� Who was bailed out?

� After Lehman: gvmts and central banks assume role or LOLRso [g] AIG – 85b

o [g] Troubled Asset Relief Fund – TARP – 700b

• Public-Private Investment Program -- PPIP

o [b] Term Asset-Backed Securities Loan Facility – TALF – 200b… 1T

o [g] Financial Stabilization Plan – FSP

o [g] fiscal stimulus – 780b

o [F] Fed’s balance sheet explosion (3T)

and… 12T implicit debt backstop guarantee

28

55Boudoukh-IDCSource: Own calculations

swap spread: avg of 2s 5s 10s

56Boudoukh-IDC

Citi’s stock price: from 50+ to 1 to 4

29

57Boudoukh-IDC

Citi’s 3y CDS rate: from 10bp to 700bp to 100bp

58Boudoukh-IDC

Outline

� The runup to the crisis:

ohow financial institutions manufactured, then warehoused catastrophic risk

� The crisis

� Regulatory Reform & some Open questions

� Local lessons

30

59Boudoukh-IDC

Dodd-Frank: 2700 pages in expansionsome highlights

� Consumer Protections with Authority and Independence: Creates a new independent watchdog, housed at the Federal Reserve, with the authority to ensure American consumers get the clear, accurate information they need to shop for mortgages, credit cards, and other financial products, and protect them from hidden fees, abusive terms, and deceptive practices.

� Ends Too Big to Fail Bailouts: Ends the possibility that taxpayers will be asked to write a check to bail out financial firms that threaten the economy by: creating a safe way to liquidate failed financial firms; imposing tough new capital and leverage requirements that make it undesirable to get too big; updating the Fed’s authority to allow system-wide support but no longer prop up individual firms; and establishing rigorous standards and supervision to protect the economy and American consumers, investors and businesses.

� Advance Warning System: Creates a council to identify and address systemic risks posed by large, complex companies, products, and activities before they threaten the stability of the economy.

� Transparency & Accountability for Exotic Instruments: Eliminates loopholes that allow risky and abusive practices to go on unnoticed and unregulated -- including loopholes for over-the-counter derivatives, asset-backed securities, hedge funds, mortgage brokers and payday lenders.

� Executive Compensation and Corporate Governance: Provides shareholders with a say on pay and corporate affairs with a non-binding vote on executive compensation and golden parachutes.

� Protects Investors: Provides tough new rules for transparency and accountability for credit rating agencies to protect investors and businesses.

60Boudoukh-IDC

Reg reforms

� Consumer protection agency (DF)

� Resolution regime for bank holding companies (DF)

� Compensation (DF)

� Derivatives (“the Volker Rule”)

� Changes in capital structure (BIII)

o IN: Experience strongly favors TierI equity capital – raise required capital to 9%

o OUT: Cycle sensitive capital requirements ?

o OUT: Contingent capital(CoCo) • Why: auto-dilute mechanism reduces s/h risk taking incentive

• Capital replenishment reduces liquidity stress(worked for HFs)

• Bond holders on the hook

31

61Boudoukh-IDC

Some open (practical/research) question:

General

� Banking and shadow banking:

o The role of banking (how big should they be)

o The role and mechanics of securitization

o MUST level the playing field across these two liquidity-risk-taking

forms and bring under the capital adequacy umbrella

o Systemic Risk (see nxt page)

� End of private-public partnerships (agencies)?

� What about the RATING AGENCIES?

o Disassociation or an extra gvmnt agency for prelim rating?

62Boudoukh-IDC

� Systemic freeze only when entire system is weak (counter example: Barings, MF Global)

The cycle:

� Losses � Funding (Capital) problems � Fire Sale at Pmkt<Pecon

� MTM losses � margin calls, higher margins, lower risk appetite

Questions:

� Negative externality, like pollutiono tax it / capitalize it / buy insurance in open mkt [cat bonds] / private-public partnership ?

o How to measure? Liquidity gap, Leverage, Concentration

� Prices fall below economic value ?

� Many small better than few large ?

� Organized exchanges better than netting ?

Some open (practical/research) question

Systemic risk

32

63Boudoukh-IDC

Some open questions:

Accounting & Reporting

Opacity and ambiguity:

� Self fulfilling (eg level3 assets)

� When Hurricane becomes “High Winds”… (who controls ISDA?)

� MFGlobal’s “repo to maturity”

64Boudoukh-IDC

Outline

� The runup to the crisis:

ohow financial institutions manufactured, then warehoused catastrophic risk

� The crisis

� Regulatory Reform & Some Open Questions

� Local lessons

33

65Boudoukh-IDC

what’s relevant for us? a whole lot more than we care to think…

Local economy: many strengths and proven resilience, but

Banking system:

� suffered two sever stress events in <10yrs

� 3-5 TBTF systemically important banks

� guarantees are implicit, hence free and limitless

� prime mortgages with 80-90%LTV exist [no “subprime” reference though!]

� TBTF systemically important borrowers

� Presence of non-bank credit with problematic standards affects banks

Other:

� credit ratings perceived non informative and untimely

� liquidity gap built into the pension system + lagged MTM = risk of “rational runs”

66Boudoukh-IDC

Lessons from the crisis

FIs

� Macroprudential supervision

� Broad-view information

� Early detection

� Identification and treatment of TBTF Fis

� Capital cushion

� Resolution authority

� Unified supervision

� Moral hazard issue

� Compensation

General

� Non-bank credit

� Provision of quality FixIncproducts

� Concentration

� Rating agencies

� Financial education

34

67Boudoukh-IDC

References

The crisis

Acharya, Cooley, Richardson, Walter, 2010 ”Manufacturing tail risk: a Perspective on the financial Crisis of 2007-09”

He Khang Krishnamurthy 2010 “Balance Sheet Adjustments in the 2008 Crisis ”

Krishnamurthy 2009 “How Debt Markets Have Malfunctioned in the Crisis”

Gorton, 2009, “ Slapped in the Face by the Invisible Hand: Banking and the Panic of 2007”

Gorton, Metrick 2009 “Securitized Banking and the Run on Repo”

Khandani, Lo, Merton, 2009, “Systemic Risk and the Refinancing Ratchet Effect”

Systemic Risk

Acharya, Pedersen, Philippon, Richardson, 2010, “Tax on Systemic Risk”

Liquidity

Brunnermeier Pedersen 2009 “Market Liquidity and Funding Liquidity”, RFS

Brunnermeier, 2008, DECIPHERING THE LIQUIDITY AND CREDIT CRUNCH 2007-08

Derivatives

Duffie, 2009, “How Big Banks Fail And What to do About It”

Stulz, 2009, “Credit Default Swaps and the Credit Crisis”

Imbalances

Caballero Krishnamurthy 2009 “Financial Fragility and Global Imbalances”, AER

Rating agencies

Benmelech, Dlugosz, 2009, “The Credit Rating Crisis” NBER Macro Annuals

Coval, Jurek, Stafford, 2009, “the Economics of Structured Finance”

Carry

Brunnermeier Nagel, Pedersen (2008) “Carry Trades and Currency Crashes”,

Sovereign

Reinherdt Rogoff (2009) “This Time is Different”

Macroprudential

BIS (2010) Macroprudential instruments and frameworks: a stocktaking of issues and experiences

Israel

2007-2009ישראל והמשבר העולמי

68Boudoukh-IDC

35

69Boudoukh-IDC

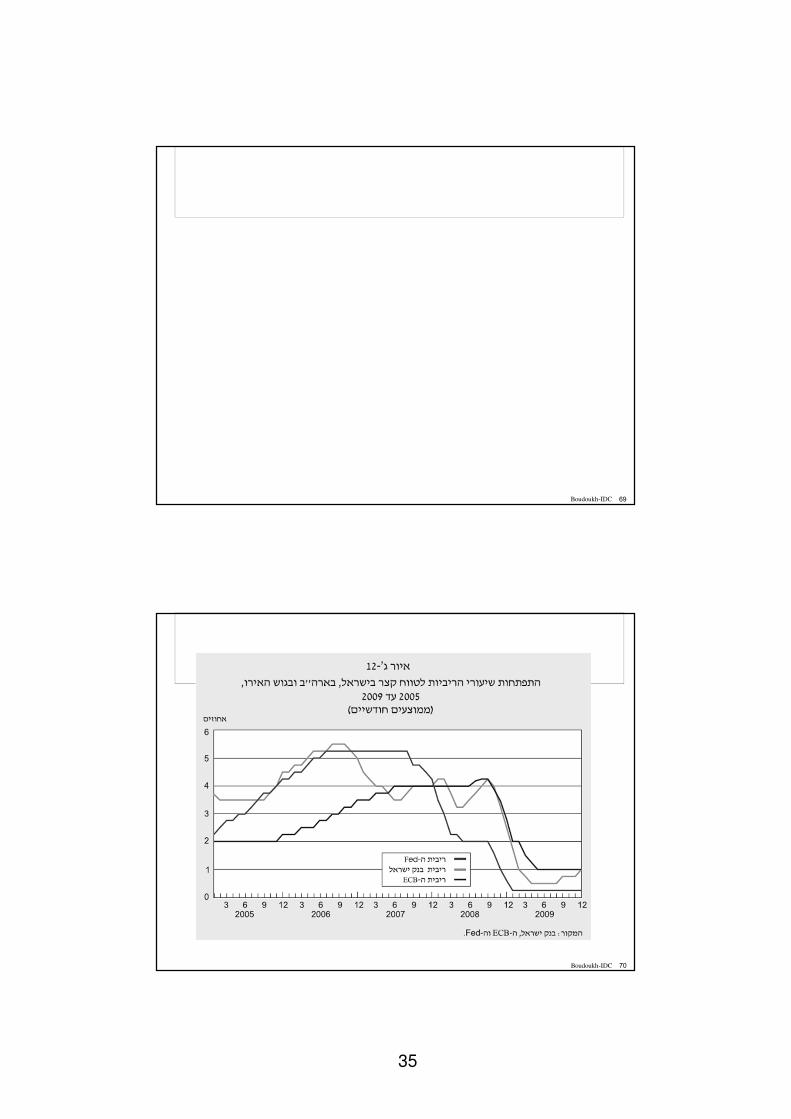

70Boudoukh-IDC

36

71Boudoukh-IDC

Intradaily VIX moves

� Note not only the level, but also the intra-daily variation� Vol-of-vol peaking� What do we make of that?

72Boudoukh-IDCSource: comp presentations

37

73Boudoukh-IDC

The crisis: summary

� Tough to understand instruments

� Separation between credit risk underwriting and credit risk taking:

the “ originate and distribute” model

� Shadow banking system (MM funds) with off balance sheet

spillovers

� Rating agencies

� Lax regulation and oversight

The procss:

� Funding problem � fire sale

� Lending (credit) dries up (and credit worthy weaken)

� Liquid depositors run on FI’s and MM funds (and SPV assets

collapse onto balance sheet)