The 2014 Global Innovation 1000 - Strategy& · IBM Proctor & Gamble ... Sources: Strategy& 2014...

12

The 2014 Global Innovation 1000 Automotive industry findings

-

Upload

truongtruc -

Category

Documents

-

view

217 -

download

1

Transcript of The 2014 Global Innovation 1000 - Strategy& · IBM Proctor & Gamble ... Sources: Strategy& 2014...

The 2014 Global Innovation 1000

Automotive industry findings

Automotive industry findings

From the ground level, three powerful forces are roiling the auto industry: shifts in consumer demand, expanded regulatory requirements for safety and fuel economy, and the increased availability of data and information. Effective innovation will be critical to coping with each of these trends.

Strategy& 2

About the Global Innovation 1000: For the 10th year, Strategy& analyzed R&D investment at the 1,000 biggest-spending public companies in the world. In addition to undertaking our recurring analysis of R&D spending trends, we interviewed and surveyed more than 500 R&D executives and innovation leaders to get their perspectives on changes in innovation at their companies over the last decade and what they expect in the 10 years to come.

Overall, R&D spending by automotive companies has gone up by an average CAGR of 4.6% over the past 10 years. The growth has generally been smooth, with just two years of decline in R&D spending during that time.

70

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

6874

86 89

71

8799 103 105

2005

$70bn2010

2014

$105bn

post-crisis dip

Automotive R&D spending has generally risen over the past decade

Sources: Bloomberg data; Capital IQ data; Strategy& analysis. Results reflect the previous fiscal year, as of June 30 of the respective year shown. More information about our methodology is available on p. 15 of our strategy+business (Issue 77, Winter 2014) article, “Proven Paths to Innovation Success.”

3Strategy&

Increases in automotive R&D spending will likely remain sustained to keep up with the accelerating need for autos to become safer and more efficient yet more technologically advanced. Barry Jaruzelski, Senior Partner, Strategy&

“

In fact, over the past five years, R&D spending by the automotive industry has consistently trended upward, while a number of other sectors, including healthcare, consumer goods and telecommunications, have decreased their R&D spending in the past year.

4Strategy&

Together the Global Innovation 1000 invested US$647 billion last year. Of that, nearly $105 billion was spent by automotive companies. Only computing and electronics and healthcare companies invested more.

Automotive companies rank #3 in innovation spending

Sources: Bloomberg data; Capital IQ data; Strategy& analysis. Results reflect the previous fiscal year, as of June 30 2014.

Want to see more how industries compare over time and across regions? Check out our interactive comparison of R&D spending by regions and industries

When it comes to R&D intensity—how much companies are spending as a proportion of revenues—automotive companies rank third.

4Strategy&

7%

11%

4%2%

13%

3% 4%2%

0.4%2%

1%

Computing & electronics

Other

Healthcare Automotive Software and Internet

ConsumerChemicals Energy

Industrials

Aerospace & defense Telecom

Com

putin

g &

elec

troni

cs

Othe

r

Heal

thca

re

Auto

mot

ive

Softw

are

and

Inte

rnet

Cons

umer

Chem

ical

s

Ener

gy

Indu

stria

ls

Aero

spac

e &

defe

nse

Tele

com

Percentage of the total R&D spend for all sectors

Average % of revenue spent on R&D

26% 21% 16% 11% 9%

4% 3% 3% 3% 2% 2%

Strategy& 5

We asked survey participants which companies they believe are the most innovative to create our 10 Most Innovative companies list. Their responses and our list of Top 10 R&D Spenders match less often than you might expect.

…but being great at innovation requires more than large R&D budgets

Indeed, Toyota has been the only automotive company to ever make both lists—in 2010–12. More recently, in 2013 and 2014, Tesla Motors has been the only automotive company among the 10 Most Innovative, despite investing far less on R&D than the industry’s biggest spenders.

Strategy&

Apple

Amazon

Tesla

3M

GE

Microsoft

IBM

Proctor& Gamble

Volkswagen Intel Roche

Novartis Toyota Johnson& Johnson

MerckGoogle

Samsung

Top 10 R&D spenders

10 most innovative US$10bnUS$5bnUS$1bn

What counts the most isn’t how much you spend. It’s what you get back from your investment. Evan Hirsh, Managing Partner North America Automotive Practice, Strategy&

Want to see who the Top Spenders and Innovators were last year too? Check out our interactive list of the Top 20 R&D Spenders and 10 Most Innovative companies, 2005-2014

“

5Strategy&

Sources: Bloomberg data; Capital IQ data. Results reflect the previous fiscal year, as of June 30. More information about our methdology is available on p.15 of our Strategy + Business (Issue 77, Winter 2014) article, “Proven paths to innovation success.”

Strategy& 6

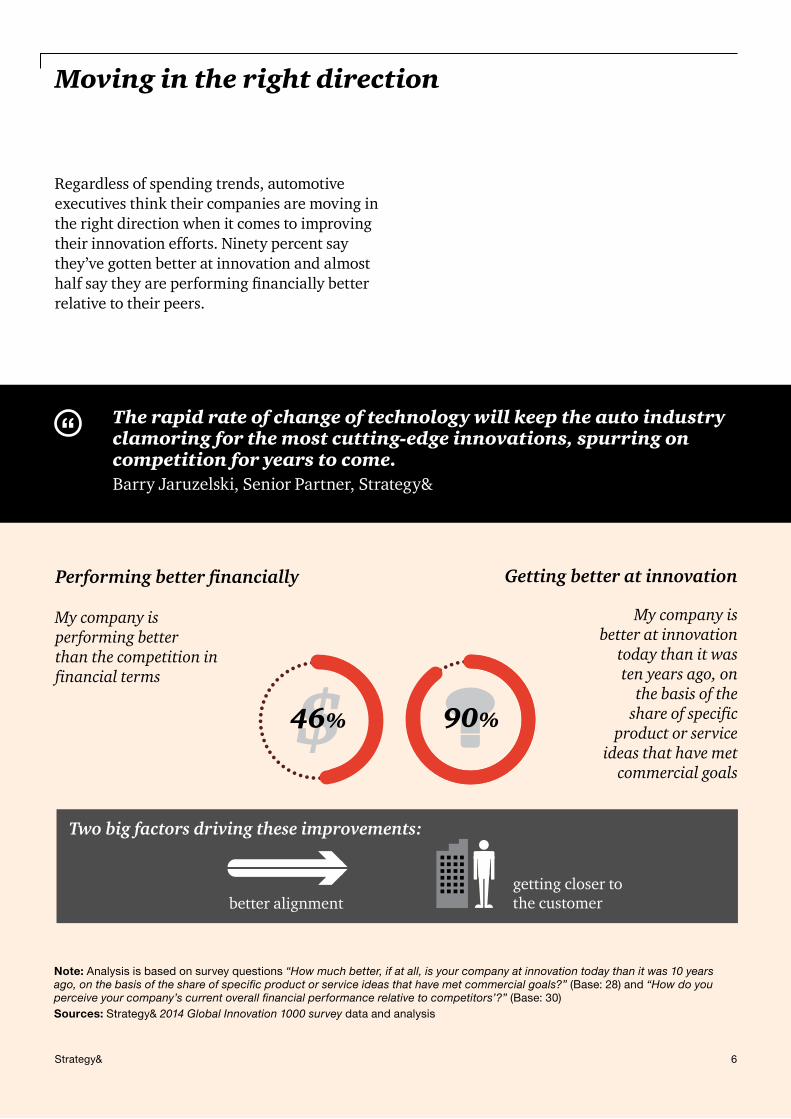

Regardless of spending trends, automotive executives think their companies are moving in the right direction when it comes to improving their innovation efforts. Ninety percent say they’ve gotten better at innovation and almost half say they are performing financially better relative to their peers.

Moving in the right direction

Strategy&

My company is performing better than the competition in financial terms

Two big factors driving these improvements:

better alignmentgetting closer to the customer

46% 90%

Performing better financially

My company is better at innovation

today than it was ten years ago, on

the basis of the share of specific

product or service ideas that have met

commercial goals

Getting better at innovation

Note: Analysis is based on survey questions “How much better, if at all, is your company at innovation today than it was 10 years ago, on the basis of the share of specific product or service ideas that have met commercial goals?” (Base: 28) and “How do you perceive your company’s current overall financial performance relative to competitors’?” (Base: 30)Sources: Strategy& 2014 Global Innovation 1000 survey data and analysis

The rapid rate of change of technology will keep the auto industry clamoring for the most cutting-edge innovations, spurring on competition for years to come. Barry Jaruzelski, Senior Partner, Strategy&

“

6Strategy&

Strategy& 7

Our overall research has shown that companies which closely align their innovation and business strategies perform better than those that don’t. The automotive industry’s performance in this regard mirrors the average across all industries, but there is room for improvement – roughly a third of automotive companies say their innovation and business strategies are not highly aligned.

Aligning innovation with business strategy

In our experience many OEMs have not been able to holistically align their connected car strategy with their overall business strategy. Many players have created parallel organizations tasked with identifying and pursuing incremental service revenue streams which seem relatively elusive in a world where consumers are used to free apps.

Strategy&

innovation strategybusiness strategy

innovation strategy

business strategy

Note: Analysis is based on survey question “How closely aligned is your company’s innovation strategy (or approach to innovation) with its overall business strategy?” (Base: 28) Responses of 1, 2, or 3 were defined as “Not Highly Aligned”, while responses of 4 or 5 were “Highly Aligned”.Sources: Strategy& 2014 Global Innovation 1000 survey data and analysis

7Strategy&

36% 64%My company’s innovation strategy is not highly aligned with its business strategy

My company’s innovation strategy is highly aligned with its business strategy

Being truly innovative – having the know-how to generate ideas and the resources and business acumen to make them a reality – is a part of doing business in the constantly changing automotive industry. The days of simply being a commodity supplier to the world’s OEMs are vanishing rapidly. Evan Hirsh, Managing Partner North America Automotive Practice, Strategy&

“

Strategy& 8

Most automotive executives (86%) believe they understand customer wants and needs better than they did 10 years ago. In fact, one-third of automotive survey respondents say their knowledge of customers has even become much more detailed.

Understanding the customer

Digital advances are of course making it easier to get comprehensive data on customers in all industries. In the automotive industry, social media in particular has improved understanding of the customer as has analyzing data from drivers more directly.

Strategy&

Note: Analysis is based on survey question #18 “How, if at all, has your company’s understanding of your customers’ wants and needs changed over the past 10 years?” (Base: 28)Sources: Strategy& 2014 Global Innovation 1000 survey data and analysis; Strategy& Industry Perspectives: 2015 Auto Industry Trends

8Strategy&

The exponential growth of new and cheaper features in vehicles is substantial today but will become even more significant over time. Innovation at every automotive company has to accelerate to keep pace and they will use customer data to achieve this. Evan Hirsh, Managing Partner North America Automotive Practice, Strategy&

“

My knowledge of customers has become more detailed

My knowledge of customers has

become much more detailed

52%34%

Strategy& 9

The connected car Cars are getting more and more digital, features from internal sensors monitoring critical engine functions to external sensors scanning the roadway for traffic backups and safety hazards are becoming more commonplace. Onboard entertainment and communications interfaces connect with the Internet. Autonomous driving features help with basic functions like parking and keeping a safe distance. And that’s just the beginning.

Keys to success: A strong handle on data security; ability to collaborate with players in other industries.

The next step: The networked mobility market is likely to quadruple in size to more than €115 billion (US$148 billion) globally by 2020. The increase will be driven not only by demand for connected-car components, but also by the rise of entirely new digital business opportunities.

Getting social The connected car

Using technology to drive innovation forward

Getting social Customers, dealers, suppliers, and prospects are discovering, connecting, and sharing their experiences with automotive brands through social media and digital platforms. Brand advocates and detractors now share their purchase and ownership experiences through text, photo, and video postings on their personal networks. That’s having an impact on the cars consumers buy—and driving the need for more innovation in organizational design.

Keys to success: Strong management of all digital touch points, whether they be company-managed, co-owned, or even just loosely affiliated; maintaining a user-centered focus.

The next step: A fully developed and coordinated “digital ecosystem” that pulls together automakers, dealers, and drivers in real time.

Sources: Strategy& Racing Ahead: The Connected C@r 2014 Study; PwC, Social Selling: A Digital Blueprint for the Automotive Industry

9Strategy&

With the accelerating electronic content in vehicles, innovation in the automotive industry is more challenging than ever. Evan Hirsh, Managing Partner North America Automotive Practice, Strategy&

“

Strategy& 10

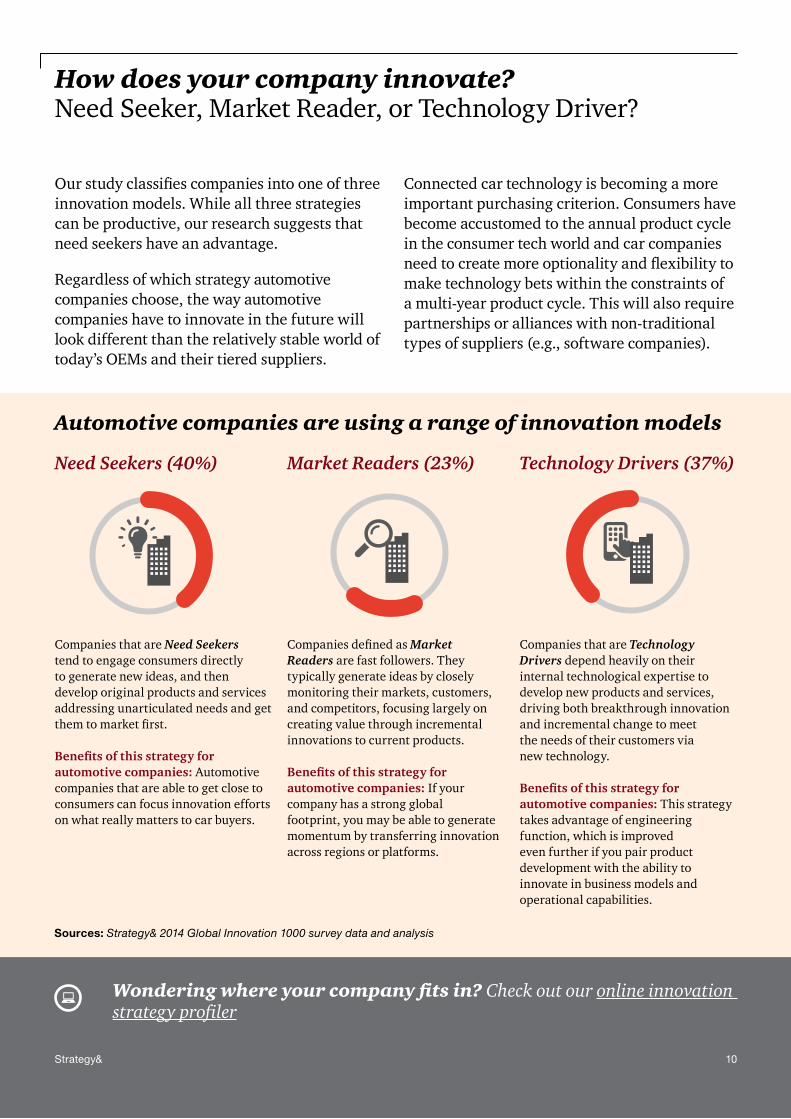

Our study classifies companies into one of three innovation models. While all three strategies can be productive, our research suggests that need seekers have an advantage.

Regardless of which strategy automotive companies choose, the way automotive companies have to innovate in the future will look different than the relatively stable world of today’s OEMs and their tiered suppliers.

How does your company innovate?Need Seeker, Market Reader, or Technology Driver?

Connected car technology is becoming a more important purchasing criterion. Consumers have become accustomed to the annual product cycle in the consumer tech world and car companies need to create more optionality and flexibility to make technology bets within the constraints of a multi-year product cycle. This will also require partnerships or alliances with non-traditional types of suppliers (e.g., software companies).

Strategy&

Wondering where your company fits in? Check out our online innovation strategy profiler

10Strategy&

Companies that are Need Seekers tend to engage consumers directly to generate new ideas, and then develop original products and services addressing unarticulated needs and get them to market first.

Benefits of this strategy for automotive companies: Automotive companies that are able to get close to consumers can focus innovation efforts on what really matters to car buyers.

Companies defined as Market Readers are fast followers. They typically generate ideas by closely monitoring their markets, customers, and competitors, focusing largely on creating value through incremental innovations to current products.

Benefits of this strategy for automotive companies: If your company has a strong global footprint, you may be able to generate momentum by transferring innovation across regions or platforms.

Need Seekers (40%) Market Readers (23%)

Companies that are Need Seekers tend to engage consumers directly to generate new ideas, and then develop original products and services addressing unarticulated needs and get them to market first.

Benefits of this strategy for healthcare companies: Understanding how end consumers are using medications and treatments can help healthcare companies find ways both to improve efficiency and develop new service offerings for patients. It can also help identify the most promising therapeutic areas for research.

Companies defined as Market Readers are fast followers. They typically generate ideas by closely monitoring their markets, customers, and competitors, focusing largely on creating value through incremental innovations to current products.

Benefits of this strategy for healthcare companies: Pharma companies focused on generics and/or biosimilars can use this strategy to increase market share.

Companies that are Technology Drivers depend heavily on their internal technological expertise to develop new products and services, driving both breakthrough innovation and incremental change to meet the needs of their customers via new technology.

Benefits of this strategy for healthcare companies: Taking the lead with emerging technologies like human microbiome therapeutics and RNA-based therapeutics should lead to exciting new advances for pharma companies. And new materials research may change medical devices dramatically.

Need Seekers (43%):

Market Readers (18%):

Technology Drivers (39%):

Companies that are Need Seekers tend to engage consumers directly to generate new ideas, and then develop original products and services addressing unarticulated needs and get them to market first.

Benefits of this strategy for healthcare companies: Understanding how end consumers are using medications and treatments can help healthcare companies find ways both to improve efficiency and develop new service offerings for patients. It can also help identify the most promising therapeutic areas for research.

Companies defined as Market Readers are fast followers. They typically generate ideas by closely monitoring their markets, customers, and competitors, focusing largely on creating value through incremental innovations to current products.

Benefits of this strategy for healthcare companies: Pharma companies focused on generics and/or biosimilars can use this strategy to increase market share.

Companies that are Technology Drivers depend heavily on their internal technological expertise to develop new products and services, driving both breakthrough innovation and incremental change to meet the needs of their customers via new technology.

Benefits of this strategy for healthcare companies: Taking the lead with emerging technologies like human microbiome therapeutics and RNA-based therapeutics should lead to exciting new advances for pharma companies. And new materials research may change medical devices dramatically.

Need Seekers (43%):

Market Readers (18%):

Technology Drivers (39%):

Companies that are Need Seekers tend to engage consumers directly to generate new ideas, and then develop original products and services addressing unarticulated needs and get them to market first.

Benefits of this strategy for healthcare companies: Understanding how end consumers are using medications and treatments can help healthcare companies find ways both to improve efficiency and develop new service offerings for patients. It can also help identify the most promising therapeutic areas for research.

Companies defined as Market Readers are fast followers. They typically generate ideas by closely monitoring their markets, customers, and competitors, focusing largely on creating value through incremental innovations to current products.

Benefits of this strategy for healthcare companies: Pharma companies focused on generics and/or biosimilars can use this strategy to increase market share.

Companies that are Technology Drivers depend heavily on their internal technological expertise to develop new products and services, driving both breakthrough innovation and incremental change to meet the needs of their customers via new technology.

Benefits of this strategy for healthcare companies: Taking the lead with emerging technologies like human microbiome therapeutics and RNA-based therapeutics should lead to exciting new advances for pharma companies. And new materials research may change medical devices dramatically.

Need Seekers (43%):

Market Readers (18%):

Technology Drivers (39%): Technology Drivers (37%)

Companies that are Technology Drivers depend heavily on their internal technological expertise to develop new products and services, driving both breakthrough innovation and incremental change to meet the needs of their customers via new technology.

Benefits of this strategy for automotive companies: This strategy takes advantage of engineering function, which is improved even further if you pair product development with the ability to innovate in business models and operational capabilities.

Sources: Strategy& 2014 Global Innovation 1000 survey data and analysis

Automotive companies are using a range of innovation models

Innovation can be managed

Innovation, although different from operations, sales, and marketing, is nevertheless a function that can be managed: There are principles that are known, capabilities that can be built, and recognized levers that can be pulled to improve the process over time. The stakes for making these efforts are high—the disparities in innovation performance show that there are tremendous opportunities for getting more from your R&D spending, and for improving your competitive position and your financial performance.

To learn more: strategyand.pwc.com/innovation1000

Strategy& 11

Contacts

Strategy& is a global team of practical strategists committed to helping you seize essential advantage. We do that by working alongside you to solve your toughest problems and helping you capture your greatest opportunities. These are complex and high-stakes undertakings — often game-changing transformations. We bring 100 years of strategy consulting experience and the unrivaled industry and functional capabilities of the PwC network to the task. Whether you’re charting your corporate strategy, transforming a function or business unit, or building critical capabilities, we’ll help you create the value you’re looking for with speed, confidence, and impact.

We are a member of the PwC network of firms in 157 countries with more than 195,000 people committed to delivering quality in assurance, tax, and advisory services. Tell us what matters to you and find out more by visiting us at strategyand.pwc.com.

© 2015 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details. Disclaimer: This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

www.strategyand.pwc.com/innovation1000

Evan R. Hirsh Managing Partner, Automotive Practice Mobile: +1-216-287-3723 Email: [email protected]

Barry H. Jaruzelski Senior Partner, Global Leader of Engineered Products and Services Practice Mobile: +1-973-410-7624 Email: [email protected]