The 10 Most Critical Trends that will Shape the Global Power Energy Industry till 2020

22

Annual Global Power and Energy Outlook 2011 Top 10 Market Trends and Their Impact

-

Upload

frost-sullivan -

Category

Education

-

view

3.904 -

download

0

Transcript of The 10 Most Critical Trends that will Shape the Global Power Energy Industry till 2020

Annual Global Power and Energy Outlook 2011

Top 10 Market Trends and Their Impact

2

The 10 Most Critical Trends

that Will Shape the Global Power

Energy Industry till 2020

The 10 Most Critical Trends

that Will Shape the Global Power

Energy Industry till 2020

Source: Frost & Sullivan

Power Demand Growth

Annual Power and Energy Outlook: Top 10 Market Trends (World), 2011

New Age for Natural Gas

Clean Coal Commercial-

isation

Power Plant Decommissioning

Smart Energy

Nuclear Power

Energy Efficiency

Energy Storage

Continued Investment in Renewables

Market Liberalisation

Annual Power and Energy Outlook Top 10 Market Trends for the Decade

3

Annual Power and Energy Outlook Top 10 Trends for the Decade - 1. Power Demand Growth

Power Demand Growth

2010 20202015

Why is this important?Electricity demand growth is one of the key indicators in determining likely power plant investment. Exceptional or high growth leads to a build up in pressure on the power generation infrastructure, as reserve margins fall, and countries can ultimately face electricity shortages or rationing, but more usually in mature regions such as Europe, they become dependent on imports, which are usually expensive.

Why is this important?Electricity demand growth is one of the key indicators in determining likely power plant investment. Exceptional or high growth leads to a build up in pressure on the power generation infrastructure, as reserve margins fall, and countries can ultimately face electricity shortages or rationing, but more usually in mature regions such as Europe, they become dependent on imports, which are usually expensive.

Key Impact/Opportunities

1) The investment focus in Europe and North America is on replacing/retrofitting the existing installed base; capacity expansion will largely be driven by investment in renewables. The demand for retrofits and refurbishments, as well as replacement capacity, means that there are still attractive opportunities in the conventional power sector for established participants.

2) Although European and North American electricity demand will continue to increase at approximately 1% p.a., the industrial demand is likely to be stable overall and will decline in some countries. This is due to the continuing trend for companies to relocate labour-intensive and energy-intensive production to lower cost countries/regions. Once this demand is gone, it is rarely replaced.

3) China and India will be the key markets in terms of volume of power equipment orders, but opportunities for Western manufacturers in both markets will be limited due to the presence of competitive local participants. Joint ventures, licencing and partial acquisition of local participants will continue to be the routes for Western manufacturers to play a role in the market.

Key Impact/Opportunities

1) The investment focus in Europe and North America is on replacing/retrofitting the existing installed base; capacity expansion will largely be driven by investment in renewables. The demand for retrofits and refurbishments, as well as replacement capacity, means that there are still attractive opportunities in the conventional power sector for established participants.

2) Although European and North American electricity demand will continue to increase at approximately 1% p.a., the industrial demand is likely to be stable overall and will decline in some countries. This is due to the continuing trend for companies to relocate labour-intensive and energy-intensive production to lower cost countries/regions. Once this demand is gone, it is rarely replaced.

3) China and India will be the key markets in terms of volume of power equipment orders, but opportunities for Western manufacturers in both markets will be limited due to the presence of competitive local participants. Joint ventures, licencing and partial acquisition of local participants will continue to be the routes for Western manufacturers to play a role in the market.

Annual Power and Energy Outlook: Growth inElectricity Demand (World), 2010-2030

Low demand in West offset by boom in the Middle East

Big expansion of electric/hybrid vehicles

Global electrification reaches 80%

Non-OECD countries surpass OECD China becomes

largest consumer

11

Source: International Energy Agency, Frost & Sullivan

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2010 2015 2020 2025 2030

Ele

ctri

city

Gen

erat

ion

(T

Wh

)

4

Annual Power and Energy Outlook Top 10 Trends for the Decade - 1. Power Demand Growth (Contd…)

Power Demand Growth

2010 20202015

Key Impact/Opportunities (Contd …)

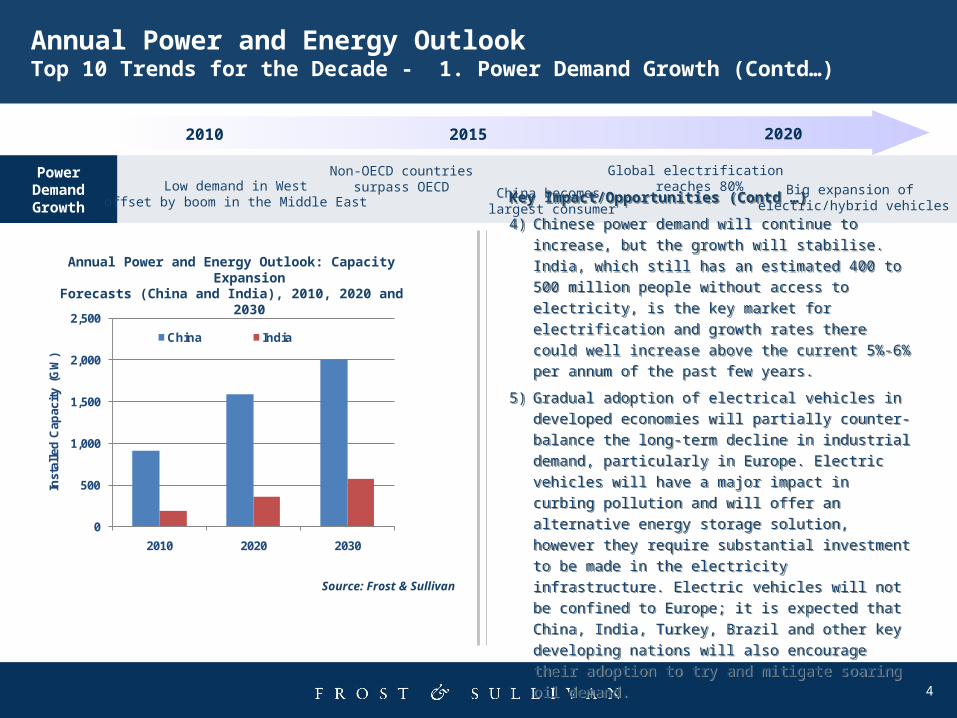

4) Chinese power demand will continue to increase, but the

growth will stabilise. India, which still has an estimated

400 to 500 million people without access to electricity, is

the key market for electrification and growth rates there

could well increase above the current 5%-6% per annum

of the past few years.

5) Gradual adoption of electrical vehicles in developed

economies will partially counter-balance the long-term

decline in industrial demand, particularly in Europe.

Electric vehicles will have a major impact in curbing

pollution and will offer an alternative energy storage

solution, however they require substantial investment to

be made in the electricity infrastructure. Electric vehicles

will not be confined to Europe; it is expected that China,

India, Turkey, Brazil and other key developing nations will

also encourage their adoption to try and mitigate soaring

oil demand.

Key Impact/Opportunities (Contd …)

4) Chinese power demand will continue to increase, but the

growth will stabilise. India, which still has an estimated

400 to 500 million people without access to electricity, is

the key market for electrification and growth rates there

could well increase above the current 5%-6% per annum

of the past few years.

5) Gradual adoption of electrical vehicles in developed

economies will partially counter-balance the long-term

decline in industrial demand, particularly in Europe.

Electric vehicles will have a major impact in curbing

pollution and will offer an alternative energy storage

solution, however they require substantial investment to

be made in the electricity infrastructure. Electric vehicles

will not be confined to Europe; it is expected that China,

India, Turkey, Brazil and other key developing nations will

also encourage their adoption to try and mitigate soaring

oil demand.

Annual Power and Energy Outlook: Capacity ExpansionForecasts (China and India), 2010, 2020 and 2030

Low demand in West offset by boom in the Middle East

Big expansion of electric/hybrid vehicles

Global electrification reaches 80%

Non-OECD countries surpass OECD China becomes

largest consumer

Source: Frost & Sullivan

0

500

1,000

1,500

2,000

2,500

2010 2020 2030

Inst

alle

d C

apac

ity

(GW

)

China India

5

Annual Power and Energy Outlook Top 10 Trends for the Decade - 2. New Age for Natural Gas

New Age for Natural Gas

2010 20202015

Why is this important?

The growth in unconventional gases, particularly shale gas and specifically in the United States, will continue to have a massive impact on the demand and supply balance, driving new investment in gas-fired generation and creating demand for equipment suppliers, exploration companies and project developers.

Why is this important?

The growth in unconventional gases, particularly shale gas and specifically in the United States, will continue to have a massive impact on the demand and supply balance, driving new investment in gas-fired generation and creating demand for equipment suppliers, exploration companies and project developers.

Key Impact/Opportunities

1) The growth in unconventional gas creates interesting

opportunities for exploration equipment companies and, at a

later stage, for infrastructure equipment companies, as the

new gas finds will need to be connected to the existing gas

network. It will also create demand for exploration project

development expertise, which will be a particular boost for

those companies that operate in markets with few new oil &

gas finds, such as the North Sea.

2) Transporting gas through pipelines will continue to be

important, with new investment to link population centres

with gas fields. In Europe, there are several mega pipeline

projects that would generate billions of dollars in orders for

raw material suppliers such as steel pipe manufacturers, as

well as construction workers and project developers.

Smaller-scale projects to link neighbouring countries will

also lead to greater tradability of gas and therefore more

transparency in pricing.

Key Impact/Opportunities

1) The growth in unconventional gas creates interesting

opportunities for exploration equipment companies and, at a

later stage, for infrastructure equipment companies, as the

new gas finds will need to be connected to the existing gas

network. It will also create demand for exploration project

development expertise, which will be a particular boost for

those companies that operate in markets with few new oil &

gas finds, such as the North Sea.

2) Transporting gas through pipelines will continue to be

important, with new investment to link population centres

with gas fields. In Europe, there are several mega pipeline

projects that would generate billions of dollars in orders for

raw material suppliers such as steel pipe manufacturers, as

well as construction workers and project developers.

Smaller-scale projects to link neighbouring countries will

also lead to greater tradability of gas and therefore more

transparency in pricing.

CCGT favourite generation technology

Shale gas boom in the United States

Growth in global pipeline network

Massive boost in LNG availability

Gas demand peaks in OECD but keeps growing elsewhere

22

Annual Power and Energy Outlook: Shale GasReserves (Selected Regions), 2011

Source: Lambert Energy

Country/RegionShale Gas Reserves (Barrels

of Oil Equivalent)

Canda 20

United States 100

Latin America 50-100

Europe 90

China 50-100

6

Annual Power and Energy Outlook Top 10 Trends for the Decade - 2. New Age for Natural Gas (Contd …)

New Age for Natural Gas

2010 20202015

Key Impact/Opportunities (Contd …)

3) A substantial volume of LNG capacity has come online in the past 2 years and significantly boosts global capacity. The current gas glut is deterring investment in new import terminals, but in the longer term, traded volumes of LNG will increase. LNG provides greater energy security and can be utilised as gas storage capacity if there is no immediate demand for the cargo. Opportunities will continue to arise for equipment suppliers and project developers.

4) The low price of gas is likely to drive new investment in gas-fired plant. The Middle East is currently the key market, but Europe and North America will both become attractive markets, as their economies recover, and developing economies will also offer opportunities in the longer term. The continued growth in the use of gas for power generation will boost demand for gas storage equipment such as tanks, degassifiers and compressors.

Key Impact/Opportunities (Contd …)

3) A substantial volume of LNG capacity has come online in the past 2 years and significantly boosts global capacity. The current gas glut is deterring investment in new import terminals, but in the longer term, traded volumes of LNG will increase. LNG provides greater energy security and can be utilised as gas storage capacity if there is no immediate demand for the cargo. Opportunities will continue to arise for equipment suppliers and project developers.

4) The low price of gas is likely to drive new investment in gas-fired plant. The Middle East is currently the key market, but Europe and North America will both become attractive markets, as their economies recover, and developing economies will also offer opportunities in the longer term. The continued growth in the use of gas for power generation will boost demand for gas storage equipment such as tanks, degassifiers and compressors.

CCGT favourite generation technology

Shale gas boom in the United States

Growth in global pipeline network

Massive boost in LNG availability

Gas demand peaks in OECD but keeps growing elsewhere

Annual Power and Energy Outlook: LNGCapacity Expansion (World), 2009-2013

This chart shows the increase in LNG export capacity from 2009 and what is scheduled to come online in the next two years till 2013. Qatar is by far the most important participant; with little domestic demand, the country is keen to export. New participants entering the market are Algeria and Australia, the latter of which will be a key participant in the future.

This chart shows the increase in LNG export capacity from 2009 and what is scheduled to come online in the next two years till 2013. Qatar is by far the most important participant; with little domestic demand, the country is keen to export. New participants entering the market are Algeria and Australia, the latter of which will be a key participant in the future.

Source: OECD

7

Annual Power and Energy Outlook Top 10 Trends for the Decade - 3. Clean Coal Commercialisation

Clean Coal Commercial-

isation

2010 20202015

Key Impact/Opportunities

1) The average efficiency rate of coal-fired plants globally is set

to increase significantly over the next five years, as ultra

supercritical technology becomes the standard, replacing

older sub critical coal-fired units. A large volume of capacity

will also be refurbished and upgraded, with boiler-related

equipment such as economisers, reheaters and

superheaters installed to maximise the potential efficiency,

creating further opportunities for these equipment sub-

suppliers.

2) The commercial viability of carbon capture is yet to be

conclusively determined, but the technology is proven in the

oil & gas sector and there is a general agreement that it is

feasible for the power generation sector. The focus for the

next decade will be on demonstration projects, including

construction of utility-scale projects. Scottish Power, owned

by Iberdrola, remains committed to constructing a 300MW

unit at the Longannet power station.

Key Impact/Opportunities

1) The average efficiency rate of coal-fired plants globally is set

to increase significantly over the next five years, as ultra

supercritical technology becomes the standard, replacing

older sub critical coal-fired units. A large volume of capacity

will also be refurbished and upgraded, with boiler-related

equipment such as economisers, reheaters and

superheaters installed to maximise the potential efficiency,

creating further opportunities for these equipment sub-

suppliers.

2) The commercial viability of carbon capture is yet to be

conclusively determined, but the technology is proven in the

oil & gas sector and there is a general agreement that it is

feasible for the power generation sector. The focus for the

next decade will be on demonstration projects, including

construction of utility-scale projects. Scottish Power, owned

by Iberdrola, remains committed to constructing a 300MW

unit at the Longannet power station.

Annual Power and Energy Outlook: The Developmentof Coal Technology (World), 2010, 2020 and 2030

Time2010 2020

CO

2 E

mis

sio

ns

per

KW

h Average worldwide

EU averageState of the artTechnology

700°C Technology

CCStechnology

Efficiency

32%-35% 38% 45% 50%

CO2 emissions

1,116g CO2/KW 881g CO2/KWh 743g CO2/KWh 669g CO2/KWh

Fuel consumption

480g coal/KWh 379g coal/KWh 320g coal/KWh 288g coal/KWh

Why is this important?

Coal’s long-term future in many global markets depends on reducing the carbon emissions released during the combustion process. Technological advancement will increase the efficiency and cut emissions, but carbon capture and storage is the solution that can have a dramatic impact.

Why is this important?

Coal’s long-term future in many global markets depends on reducing the carbon emissions released during the combustion process. Technological advancement will increase the efficiency and cut emissions, but carbon capture and storage is the solution that can have a dramatic impact.

Commercial CCS viability established and large-scale development commences

Ultra supercritical technologybecomes prevalent globally

Carbon capture and storage pilot plants

33

Source: Frost & Sullivan

2030

8

Annual Power and Energy Outlook Top 10 Trends for the Decade - 3. Clean Coal Commercialisation (Contd …)

Clean Coal Commercial-

isation

2010 20202015

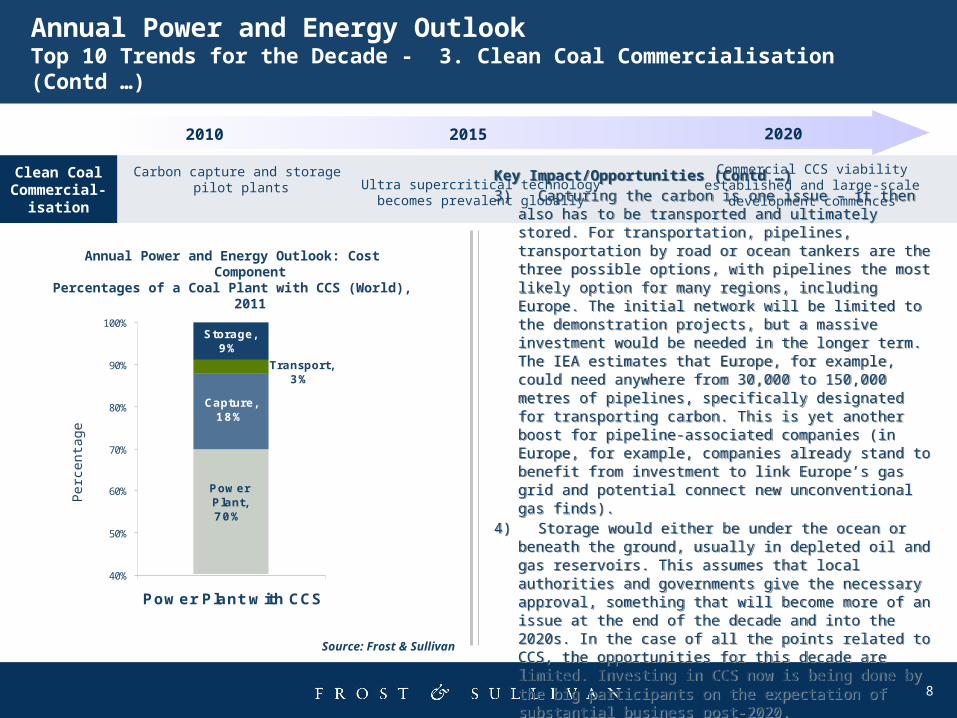

Key Impact/Opportunities (Contd …) 3) Capturing the carbon is one issue – it then also has to be

transported and ultimately stored. For transportation, pipelines, transportation by road or ocean tankers are the three possible options, with pipelines the most likely option for many regions, including Europe. The initial network will be limited to the demonstration projects, but a massive investment would be needed in the longer term. The IEA estimates that Europe, for example, could need anywhere from 30,000 to 150,000 metres of pipelines, specifically designated for transporting carbon. This is yet another boost for pipeline-associated companies (in Europe, for example, companies already stand to benefit from investment to link Europe’s gas grid and potential connect new unconventional gas finds).

4) Storage would either be under the ocean or beneath the ground, usually in depleted oil and gas reservoirs. This assumes that local authorities and governments give the necessary approval, something that will become more of an issue at the end of the decade and into the 2020s. In the case of all the points related to CCS, the opportunities for this decade are limited. Investing in CCS now is being done by the big participants on the expectation of substantial business post-2020.

Key Impact/Opportunities (Contd …) 3) Capturing the carbon is one issue – it then also has to be

transported and ultimately stored. For transportation, pipelines, transportation by road or ocean tankers are the three possible options, with pipelines the most likely option for many regions, including Europe. The initial network will be limited to the demonstration projects, but a massive investment would be needed in the longer term. The IEA estimates that Europe, for example, could need anywhere from 30,000 to 150,000 metres of pipelines, specifically designated for transporting carbon. This is yet another boost for pipeline-associated companies (in Europe, for example, companies already stand to benefit from investment to link Europe’s gas grid and potential connect new unconventional gas finds).

4) Storage would either be under the ocean or beneath the ground, usually in depleted oil and gas reservoirs. This assumes that local authorities and governments give the necessary approval, something that will become more of an issue at the end of the decade and into the 2020s. In the case of all the points related to CCS, the opportunities for this decade are limited. Investing in CCS now is being done by the big participants on the expectation of substantial business post-2020.

Annual Power and Energy Outlook: Cost ComponentPercentages of a Coal Plant with CCS (World), 2011

Source: Frost & Sullivan

Power Plant, 70%

Capture, 18%

Transport, 3%

Storage, 9%

40%

50%

60%

70%

80%

90%

100%

Power Plant with CCS

Commercial CCS viability established and large-scale development commences

Ultra supercritical technologybecomes prevalent globally

Carbon capture and storage pilot plants

Per

cent

age

9

Annual Power and Energy Outlook Top 10 Trends for the Decade - 4. Power Plant Decommissioning

Power Plant Decommissioning

2010 20202015

Key Impact/Opportunities

1) The obvious impact of decommissioning is that it creates a need for new plants. Frost & Sullivan estimates that approximately 200GW of installed plant in Europe, the Middle East and Africa will be closed between 2011 and 2020, and this has to be replaced. In Europe gas-fired plant is expected to account for the largest percentage, given the short-to-medium term challenges faced by coal in relation to carbon emissions and pricing. New nuclear is expected to partially fill the gap left behind by coal station closures and also to replace existing nuclear plants. In light of the events in Japan (occurring as this document is being finalised), the level of new nuclear may be less than anticipated at the start of 2011, but this will become clearer when the full impact of the Fukushima situation is known. If the result is countries scaling back their nuclear investment programmes, this would result in more coal-fired plant equipment sales in Asia and gas-fired plant sales in Europe. For example, if Germany decides to proceed with its 2002 shutdown programme, this will likely provide a boost to gas plant equipment suppliers in particular, as gas accounts for a relatively small percentage of the German installed base (15 %). The key point is that closed thermal and nuclear plants will need replacing with similar plants to guarantee baseload power.

Key Impact/Opportunities

1) The obvious impact of decommissioning is that it creates a need for new plants. Frost & Sullivan estimates that approximately 200GW of installed plant in Europe, the Middle East and Africa will be closed between 2011 and 2020, and this has to be replaced. In Europe gas-fired plant is expected to account for the largest percentage, given the short-to-medium term challenges faced by coal in relation to carbon emissions and pricing. New nuclear is expected to partially fill the gap left behind by coal station closures and also to replace existing nuclear plants. In light of the events in Japan (occurring as this document is being finalised), the level of new nuclear may be less than anticipated at the start of 2011, but this will become clearer when the full impact of the Fukushima situation is known. If the result is countries scaling back their nuclear investment programmes, this would result in more coal-fired plant equipment sales in Asia and gas-fired plant sales in Europe. For example, if Germany decides to proceed with its 2002 shutdown programme, this will likely provide a boost to gas plant equipment suppliers in particular, as gas accounts for a relatively small percentage of the German installed base (15 %). The key point is that closed thermal and nuclear plants will need replacing with similar plants to guarantee baseload power.

Annual Power and Energy Outlook: Likely Decommissioning(Selected Regions), 2010-2020

Why is this important?

A substantial number of plants in Europe and North America will reach the end of their operating lifetime over the next decade, and there will also be closures of some plants in other regions. This creates not only demand for new plants and therefore new equipment sales, but also demand related to safely decommissioning sites in some cases restoring the land or use for other purposes.

Why is this important?

A substantial number of plants in Europe and North America will reach the end of their operating lifetime over the next decade, and there will also be closures of some plants in other regions. This creates not only demand for new plants and therefore new equipment sales, but also demand related to safely decommissioning sites in some cases restoring the land or use for other purposes.

First of substantial wave of gas-fired plant closures

Closure of substantial coal-fired capacity in Europe to comply with the

Large Combustion Plant Directive

Gradual closure of nuclear-fired power stations in Europe

and North America

44

Source: Frost & Sullivan

0 20 40 60 80 100

Europe

Eastern Europe &Russia

Middle East

Africa

Capacity Decommissioned (GW)

10

Annual Power and Energy Outlook Top 10 Trends for the Decade - 4. Power Plant Decommissioning (Contd …)

Power Plant Decommissioning

2010 20202015

Key Impact/Opportunities (Contd …)

2) Decommissioning a plant can be a complex and expensive

process; in the case of coal and gas-fired plants, the plants

would generally be dismantled and then the site would either

be returned to greenfield or more likely be used again for a

new thermal plant. It does depend on country and local

regulations. The most expensive by far for decommissioning is

nuclear; nuclear.info.net estimates that in the United States, it

costs $300 million (€214 million) per reactor. For France and

Sweden, the estimates are 10 to 15 % of the construction cost

(approximately €300 to €450 million). Given the complex

nature of nuclear projects, the reality could be far higher than

both of these. The money to carry out this work is supposed to

be set aside in a fund over the course of the plants lifetime,

but there is concern that these funds will not be sufficient

when the time comes. These decommissioning projects will

create good opportunities for waste disposal firms and EPC

contractors that specialise in plant shutdowns or have the

capabilities to enter this segment of the market.

Key Impact/Opportunities (Contd …)

2) Decommissioning a plant can be a complex and expensive

process; in the case of coal and gas-fired plants, the plants

would generally be dismantled and then the site would either

be returned to greenfield or more likely be used again for a

new thermal plant. It does depend on country and local

regulations. The most expensive by far for decommissioning is

nuclear; nuclear.info.net estimates that in the United States, it

costs $300 million (€214 million) per reactor. For France and

Sweden, the estimates are 10 to 15 % of the construction cost

(approximately €300 to €450 million). Given the complex

nature of nuclear projects, the reality could be far higher than

both of these. The money to carry out this work is supposed to

be set aside in a fund over the course of the plants lifetime,

but there is concern that these funds will not be sufficient

when the time comes. These decommissioning projects will

create good opportunities for waste disposal firms and EPC

contractors that specialise in plant shutdowns or have the

capabilities to enter this segment of the market.

Annual Power and Energy Outlook: EstimatedDecommissioning Costs for Nuclear

Power Plants (Selected Regions), 2011

First of substantial wave of gas-fired plant closures

Closure of substantial coal-fired capacity in Europe to comply with the

Large Combustion Plant Directive

Gradual closure of nuclear-fired power stations in Europe

and North America

Source: nuclearinfo.net

0

50

100

150

200

250

300

350

400

France Sweden United States

Est

imat

ed D

eco

mm

issi

on

ing

Co

st (

€ M

illi

on

)

11

55

Annual Power and Energy Outlook Top 10 Trends for the Decade - 5. Smart Energy

Smart Energy

2010 20202015

Key Impact/Opportunities1) The smart energy concept has re-invigorated mature segments

of the power sector and offers significant opportunities for participants in related sectors. Transmission and distribution was considered a low growth segment five years ago, but smart energy requires substantial upgrades to be carried out on the existing grid infrastructure. Utilities need greater information on the volumes of electricity being transported across the system and this is done through the installation of equipment such Phasor Measurement Units (PMUs). PMUs provide a real time view of a particular part of the grid at any one time. A large number of them, combined with sensors, give a comprehensive, simultaneous view of the grid. This enables faults and outages to be detected quickly and ultimately minimised, as utilities can more accurately implement preventative maintenance. Massive investment in these technologies will take place over the next decade.

2) Another growth area for power equipment companies is sub-station automation. The current system (essentially the way in which the central hub talks to substations) is largely based on conventional serial bus technologies such as SCADA. The future shift is toward IP-based systems that rely on Ethernet switches and intelligent electronic devices (IEDs). This requires substantial investment in new technology.

Key Impact/Opportunities1) The smart energy concept has re-invigorated mature segments

of the power sector and offers significant opportunities for participants in related sectors. Transmission and distribution was considered a low growth segment five years ago, but smart energy requires substantial upgrades to be carried out on the existing grid infrastructure. Utilities need greater information on the volumes of electricity being transported across the system and this is done through the installation of equipment such Phasor Measurement Units (PMUs). PMUs provide a real time view of a particular part of the grid at any one time. A large number of them, combined with sensors, give a comprehensive, simultaneous view of the grid. This enables faults and outages to be detected quickly and ultimately minimised, as utilities can more accurately implement preventative maintenance. Massive investment in these technologies will take place over the next decade.

2) Another growth area for power equipment companies is sub-station automation. The current system (essentially the way in which the central hub talks to substations) is largely based on conventional serial bus technologies such as SCADA. The future shift is toward IP-based systems that rely on Ethernet switches and intelligent electronic devices (IEDs). This requires substantial investment in new technology.

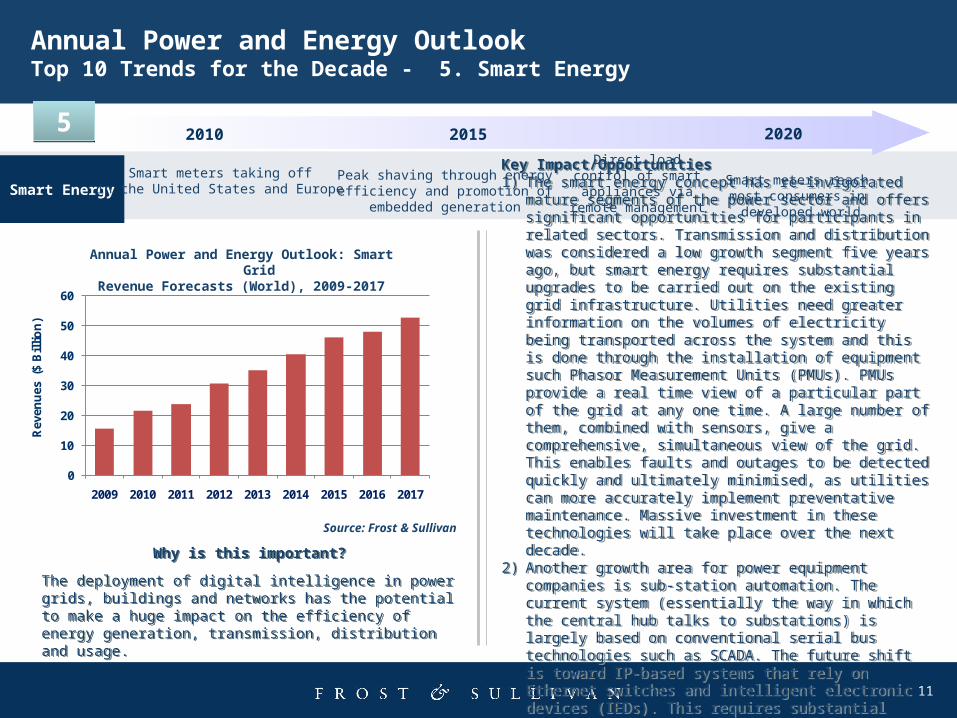

Annual Power and Energy Outlook: Smart GridRevenue Forecasts (World), 2009-2017

Why is this important?

The deployment of digital intelligence in power grids, buildings and networks has the potential to make a huge impact on the efficiency of energy generation, transmission, distribution and usage.

Why is this important?

The deployment of digital intelligence in power grids, buildings and networks has the potential to make a huge impact on the efficiency of energy generation, transmission, distribution and usage.

Smart meters taking off in the United States and Europe

Smart meters reach most consumers in

developed world

Direct load control of smart appliances via remote management

Peak shaving through energy efficiency and promotion of

embedded generation

Source: Frost & Sullivan

0

10

20

30

40

50

60

2009 2010 2011 2012 2013 2014 2015 2016 2017

Rev

enu

es (

$ B

illi

on

)

12

0

5

10

15

20

25

North America Europe Rest of World

Rev

enu

es (

$ B

illi

on

) 2010 2017

Annual Power and Energy Outlook Top 10 Trends for the Decade - 5. Smart Energy (Contd …)

Smart Energy

2010 20202015

Key Impact/Opportunities (Contd …)3) The installation of smart meters over the course of the decade

will enable the creation of Home Area Networks (HANs), where computerised home appliances could be operated remotely by utility companies. A smart system will give home owners detailed data on how much each appliance uses and as the pricing mechanisms that utilities use become more sophisticated, home owners can set parameters for utility companies to enable them to determine when an appliance should be turned on. Home owners could chose to keep control and have remote access instead, probably through a smartphone application). The development of HANs creates a specific opportunity for smartphone application developers/mobile phone companies, but also for appliance manufacturers that could offer products that are HAN ready.

4) The level of data that needs to be transmitted, processed, stored and integrated brings IT companies into the energy space. Companies are investing in smart offerings, trying to understand the requirements and define what applications need to be developed and integrated. Frost & Sullivan expects to see a combination of organic growth by the big participants, along with acquisitions of small specialists by the large equipment manufacturers.

Key Impact/Opportunities (Contd …)3) The installation of smart meters over the course of the decade

will enable the creation of Home Area Networks (HANs), where computerised home appliances could be operated remotely by utility companies. A smart system will give home owners detailed data on how much each appliance uses and as the pricing mechanisms that utilities use become more sophisticated, home owners can set parameters for utility companies to enable them to determine when an appliance should be turned on. Home owners could chose to keep control and have remote access instead, probably through a smartphone application). The development of HANs creates a specific opportunity for smartphone application developers/mobile phone companies, but also for appliance manufacturers that could offer products that are HAN ready.

4) The level of data that needs to be transmitted, processed, stored and integrated brings IT companies into the energy space. Companies are investing in smart offerings, trying to understand the requirements and define what applications need to be developed and integrated. Frost & Sullivan expects to see a combination of organic growth by the big participants, along with acquisitions of small specialists by the large equipment manufacturers.

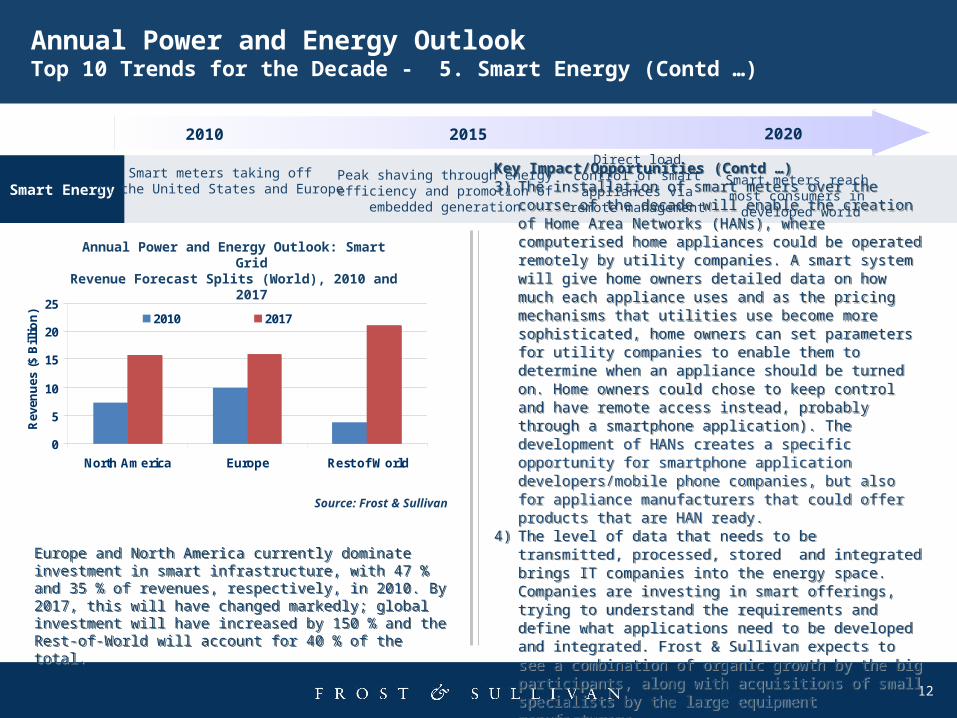

Annual Power and Energy Outlook: Smart GridRevenue Forecast Splits (World), 2010 and 2017

Europe and North America currently dominate investment in smart infrastructure, with 47 % and 35 % of revenues, respectively, in 2010. By 2017, this will have changed markedly; global investment will have increased by 150 % and the Rest-of-World will account for 40 % of the total.

Europe and North America currently dominate investment in smart infrastructure, with 47 % and 35 % of revenues, respectively, in 2010. By 2017, this will have changed markedly; global investment will have increased by 150 % and the Rest-of-World will account for 40 % of the total.

Smart meters taking off in the United States and Europe

Smart meters reach most consumers in

developed world

Direct load control of smart appliances via remote management

Peak shaving through energy efficiency and promotion of

embedded generation

Source: Frost & Sullivan

13

Annual Power and Energy Outlook Top 10 Trends for the Decade - 6. Nuclear Power

Nuclear Power

2010 20202015

Key Impact/Opportunities1) Nuclear reactor safety has always been the priority for all

those involved in the nuclear sector. However, the accident in Fukushima will push governments and nuclear bodies to delay and review existing projects and evaluate any potential flaws in the design approach. Backup systems and fail safe circuits are the prime target of investigations, although the vast majority of reactors are very unlikely to suffer earthquakes of the magnitude seen in Japan. Other risks, however, include tornados, terrorist attacks, cyber hijacking and equipment failure due to abnormal wear. The private sector opportunities here are very limited as this work would be carried out by public sector bodies.

2) Nuclear plant life extensions are a key driver for low electricity prices across the United States, Europe and other nuclear regions. As the operational costs of nuclear power plants are low compared to coal plants, or gas plants per MWh produced, a well-maintained nuclear plant can normally expect a life extension of 10 years beyond its original design life. As cost issues of new reactors continue to impend new construction, an increase in the prevalence of life extensions is highly likely, bringing opportunities for projects to replace key pieces of equipment.

Key Impact/Opportunities1) Nuclear reactor safety has always been the priority for all

those involved in the nuclear sector. However, the accident in Fukushima will push governments and nuclear bodies to delay and review existing projects and evaluate any potential flaws in the design approach. Backup systems and fail safe circuits are the prime target of investigations, although the vast majority of reactors are very unlikely to suffer earthquakes of the magnitude seen in Japan. Other risks, however, include tornados, terrorist attacks, cyber hijacking and equipment failure due to abnormal wear. The private sector opportunities here are very limited as this work would be carried out by public sector bodies.

2) Nuclear plant life extensions are a key driver for low electricity prices across the United States, Europe and other nuclear regions. As the operational costs of nuclear power plants are low compared to coal plants, or gas plants per MWh produced, a well-maintained nuclear plant can normally expect a life extension of 10 years beyond its original design life. As cost issues of new reactors continue to impend new construction, an increase in the prevalence of life extensions is highly likely, bringing opportunities for projects to replace key pieces of equipment.

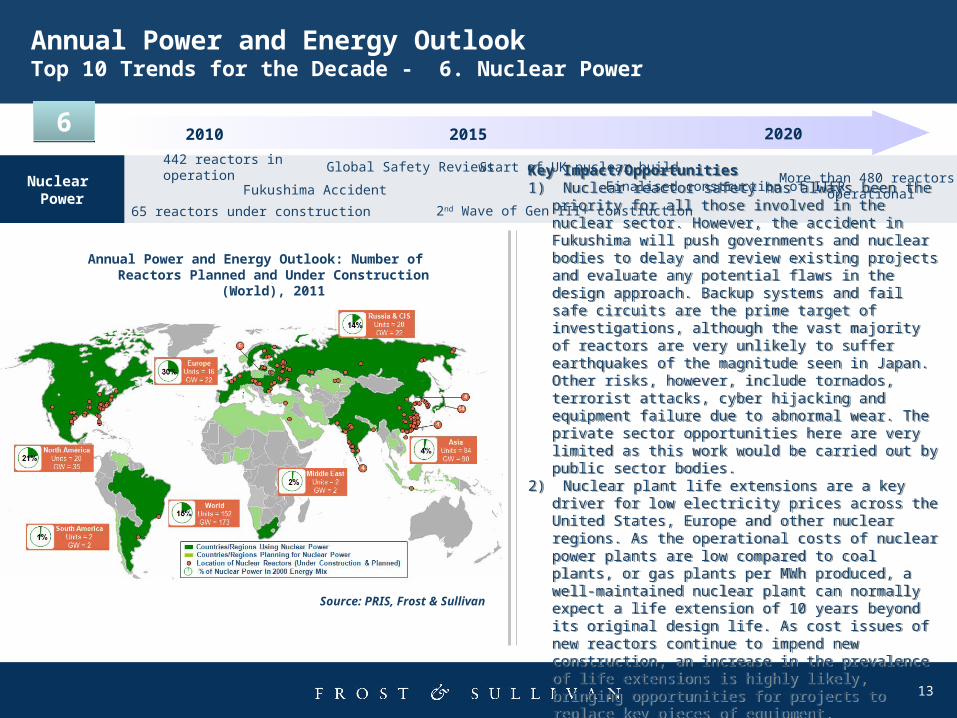

Annual Power and Energy Outlook: Number of Reactors Planned and Under Construction (World), 2011

Fukushima Accident

Start of UK nuclear build

2nd Wave of Gen III+ construction

442 reactors in operationMore than 480 reactors

operational

Source: PRIS, Frost & Sullivan

Global Safety Reviews

65 reactors under construction

Finalised construction of ITER

66

14

Annual Power and Energy Outlook Top 10 Trends for the Decade - 6. Nuclear Power (Contd …)

2010 20202015

Key Impact/Opportunities (Contd …)

3) Reactor pressure vessels (RPVs) are one of the

critical plant equipment elements with a 1:1 ratio to

each reactor. Since 2005, the number of pressure

vessel orders rose from an average of 4 per year

between 2000 and 2006 to over 13 between 2007 and

2010. For an average construction project, RPVs are

ordered 1 year after construction has begun. The

number of orders, therefore, give an accurate view of

the market activity, the likely date of operation for

each reactor and highlight possible constraints along

the supply chain, as only a limited number of

companies can manufacture nuclear RPVs. Despite

Fukushima, and increased scepticism, the average

number of orders per year is likely to continue to grow

until at least 2014.

Key Impact/Opportunities (Contd …)

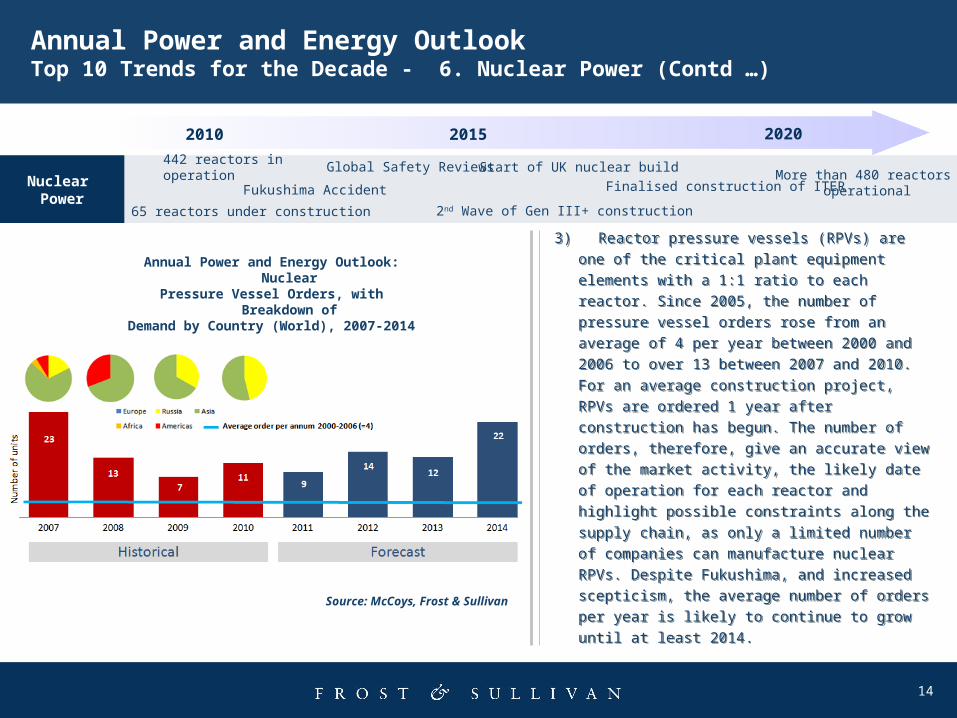

3) Reactor pressure vessels (RPVs) are one of the

critical plant equipment elements with a 1:1 ratio to

each reactor. Since 2005, the number of pressure

vessel orders rose from an average of 4 per year

between 2000 and 2006 to over 13 between 2007 and

2010. For an average construction project, RPVs are

ordered 1 year after construction has begun. The

number of orders, therefore, give an accurate view of

the market activity, the likely date of operation for

each reactor and highlight possible constraints along

the supply chain, as only a limited number of

companies can manufacture nuclear RPVs. Despite

Fukushima, and increased scepticism, the average

number of orders per year is likely to continue to grow

until at least 2014.

Annual Power and Energy Outlook: NuclearPressure Vessel Orders, with Breakdown of

Demand by Country (World), 2007-2014

Source: McCoys, Frost & Sullivan

Nuclear Power

Fukushima Accident

Start of UK nuclear build

2nd Wave of Gen III+ construction

442 reactors in operationMore than 480 reactors

operational

Global Safety Reviews

65 reactors under construction

Finalised construction of ITER

15

Annual Power and Energy Outlook Top 10 Trends for the Decade – 7. Energy Efficiency

Energy Efficiency

2010 20202015

Key Impact/Opportunities1) Green buildings have a vital role to play in the reduction of

carbon emissions and improving the environment. A smart and green building can conserve resources, use energy efficiently and create a healthy occupied environment. Green buildings essential bring together a range of home efficiency concepts, along with a greater use of micro-generation technologies such as solar thermal, photovoltaic cells and heat pumps. There is also better monitoring and control of energy-intensive systems such as HVAC and lighting. Green buildings create opportunities for manufacturers of building automation systems, energy-efficient lighting, green HVAC systems and integrated security solutions. It should be noted that this does not just apply to new buildings; some of these technologies can be incorporated into the existing housing stock.

2) Large-scale deployment of compact fluorescent lights (CFLs) can help reduce peak electricity demand and improve power shortages in developing nations. High-quality CFLs are four to five times more efficient than incandescent bulbs and last substantially longer. Other technologies such as organic light emitting diode (OLED) lighting will further improve energy efficiency in the lighting sector.

Key Impact/Opportunities1) Green buildings have a vital role to play in the reduction of

carbon emissions and improving the environment. A smart and green building can conserve resources, use energy efficiently and create a healthy occupied environment. Green buildings essential bring together a range of home efficiency concepts, along with a greater use of micro-generation technologies such as solar thermal, photovoltaic cells and heat pumps. There is also better monitoring and control of energy-intensive systems such as HVAC and lighting. Green buildings create opportunities for manufacturers of building automation systems, energy-efficient lighting, green HVAC systems and integrated security solutions. It should be noted that this does not just apply to new buildings; some of these technologies can be incorporated into the existing housing stock.

2) Large-scale deployment of compact fluorescent lights (CFLs) can help reduce peak electricity demand and improve power shortages in developing nations. High-quality CFLs are four to five times more efficient than incandescent bulbs and last substantially longer. Other technologies such as organic light emitting diode (OLED) lighting will further improve energy efficiency in the lighting sector.

Annual Power and Energy Outlook: ConceptualDrawing of a Green Building (World), 2011

Why is this important?

Increasing energy efficiency is vital for reducing consumption, because if done well, it enables people to continue acting close to their normal behaviour and yet per capita consumption falls. Government efforts to increase energy efficiency in the past have not always been successful, but the technology now exists to make improvements easier to achieve.

Why is this important?

Increasing energy efficiency is vital for reducing consumption, because if done well, it enables people to continue acting close to their normal behaviour and yet per capita consumption falls. Government efforts to increase energy efficiency in the past have not always been successful, but the technology now exists to make improvements easier to achieve.

77

Global coverage for energy-efficient lighting

Green buildings become norm in developed world Grid investments lay foundations for

supergrids and reduce T&D losses

Global penetration of micro-renewables and micro-CHP

Source: Frost & Sullivan

16

Annual Power and Energy Outlook Top 10 Trends for the Decade – 7. Energy Efficiency (Contd …)

Energy Efficiency

2010 20202015

Key Impact/Opportunities (Contd …)

3) Increased investment in grid infrastructure, as part of the

smart energy concept, will boost the growth of more energy-

efficient distributed generation (DG) technologies such as

micro-generation, micro-combined heat and power (CHP)

plants, biomass boilers, solar thermal panels, geothermal

energy and heat pumps. Micro-CHP is expected to expand

strongly in Europe and Asian countries such as Japan and

South Korea in the near term; however, North America also

holds good opportunities. Besides the increased efficiencies,

DG has the advantage that transmission losses are

minimised, because the electricity is generated close to

where it is ultimately used by the consumer.

Key Impact/Opportunities (Contd …)

3) Increased investment in grid infrastructure, as part of the

smart energy concept, will boost the growth of more energy-

efficient distributed generation (DG) technologies such as

micro-generation, micro-combined heat and power (CHP)

plants, biomass boilers, solar thermal panels, geothermal

energy and heat pumps. Micro-CHP is expected to expand

strongly in Europe and Asian countries such as Japan and

South Korea in the near term; however, North America also

holds good opportunities. Besides the increased efficiencies,

DG has the advantage that transmission losses are

minimised, because the electricity is generated close to

where it is ultimately used by the consumer.

Source: splendidaparna.com

Global coverage for energy-efficient lighting

Green buildings become norm in developed world Grid investments lay foundations for

supergrids and reduce T&D losses

Global penetration of micro-renewables and micro-CHP

Annual Power and Energy Outlook: Energy-efficient Micro-Grid (World), 2011

17

Annual Power and Energy Outlook Top 10 Trends for the Decade – 8. Energy Storage

Energy Storage

2010 20202015

Key Impact/Opportunities

1) With increasing cost reductions in advanced battery

technologies and storage solutions, systems are starting to

provide attractive returns when taking into account the

benefits they bring. Examples include allowing renewable

energy generated off-peak to be sold on-peak, increasing

capacity credit, peak-shaving, increasing T&D asset utilisation,

deferring costs of upgrades and so on. With these monetised

advantages becoming clearer, utility/grid-scale energy

storage deployment is inevitable.

2) New participants will enter the market with new ideas and

new business models. Expect the arrival of spotters of

strategic energy storage locations that will study best locations

for energy storage deployment and develop energy storage

projects in the same way as developers did in the wind and

solar renewable energy markets. New business concepts will

also emerge with storage-as-a-service being offered to utilities

that do not want to invest in their own storage assets.

Key Impact/Opportunities

1) With increasing cost reductions in advanced battery

technologies and storage solutions, systems are starting to

provide attractive returns when taking into account the

benefits they bring. Examples include allowing renewable

energy generated off-peak to be sold on-peak, increasing

capacity credit, peak-shaving, increasing T&D asset utilisation,

deferring costs of upgrades and so on. With these monetised

advantages becoming clearer, utility/grid-scale energy

storage deployment is inevitable.

2) New participants will enter the market with new ideas and

new business models. Expect the arrival of spotters of

strategic energy storage locations that will study best locations

for energy storage deployment and develop energy storage

projects in the same way as developers did in the wind and

solar renewable energy markets. New business concepts will

also emerge with storage-as-a-service being offered to utilities

that do not want to invest in their own storage assets.

Annual Power and Energy Outlook: Forecast RevenueGrowth of the Energy Storage Market (World), 2001-2017

Why is this important?

Energy storage is a rising star in tomorrow’s electricity generation and distribution landscape. It is a key enabling component of the future smart electricity grid as it allows intermittent renewable energy deployment, helps ease bottlenecks on the grid, improves power quality, provides back-up power supply and defers the cost of upgrading or expanding generation capacity and transmission systems.

Why is this important?

Energy storage is a rising star in tomorrow’s electricity generation and distribution landscape. It is a key enabling component of the future smart electricity grid as it allows intermittent renewable energy deployment, helps ease bottlenecks on the grid, improves power quality, provides back-up power supply and defers the cost of upgrading or expanding generation capacity and transmission systems.

88

Grid-scale energy storage such as pumped storage and CAES takes offImproved existing battery technologies emerge

such as Li-ion, Nickel-Zinc and Molten Salt

Energy storage market reaches $50 billion

0

10

20

30

40

50

60

0

100

200

300

400

500

600

2010 2011 2012 2013 2014 2015 2016 2017Gr

owth

Rat

e (%

)

Reve

nue

($ M

illio

n)

Year

Battery Revenue ($ Million) Growth Rate (%)

18

Global Power and Energy Outlook Top 10 Trends for the Decade – 8. Energy Storage (Contd …)

Energy Storage

2010 20202015

Key Impact/Opportunities (Contd …)

3) With alternative vehicles fast increasing penetration of the

automotive market, lithium-ion battery manufacturers will

witness tremendous opportunities arising for their products. By

2016, approximately 50 % of revenues will come from this

application. This will spur accelerated developments in lithium-

based batteries (for example, lithium-manganese) and will

most likely spill and benefit other applications, possibly notably

through battery re-use/recycling schemes.

4) With such impending transformations in store for the battery

markets, the market participants will re-think their strategies,

and lots of momentum is expected in the form of industry

consolidation, alliances, price pressures, shifts in bargaining

power and so on. Exciting times ahead for the energy storage

market!

Key Impact/Opportunities (Contd …)

3) With alternative vehicles fast increasing penetration of the

automotive market, lithium-ion battery manufacturers will

witness tremendous opportunities arising for their products. By

2016, approximately 50 % of revenues will come from this

application. This will spur accelerated developments in lithium-

based batteries (for example, lithium-manganese) and will

most likely spill and benefit other applications, possibly notably

through battery re-use/recycling schemes.

4) With such impending transformations in store for the battery

markets, the market participants will re-think their strategies,

and lots of momentum is expected in the form of industry

consolidation, alliances, price pressures, shifts in bargaining

power and so on. Exciting times ahead for the energy storage

market!

Annual Power and Energy Outlook: Energy StorageMarket Size by Technology (World), 2016

Grid-scale energy storage such as pumped storage and CAES takes offImproved existing battery technologies emerge

such as Li-ion, Nickel-Zinc and Molten Salt

Energy storage market reaches $50 billion

Why is this important?

For the first time in 2016, revenues from lithium-ion batteries will outstrip lead-acid battery revenues leading to profound transformations in the competitive landscape, supply chain, as well as application markets.

Why is this important?

For the first time in 2016, revenues from lithium-ion batteries will outstrip lead-acid battery revenues leading to profound transformations in the competitive landscape, supply chain, as well as application markets.

19

Annual Power and Energy Outlook Top 10 Trends for the Decade – 9. Continued Investment in Renewables

Continued Investment in Renewables

2010 20202015

Key Impact/Opportunities

1) The renewables sector offers a huge range of potentially

attractive opportunities; the challenge for any investor is to

assess and determine which are the best. With different

electricity prices and feed-in tariffs from country to country,

investors need to either develop strong competencies in

monitoring and assessing opportunities or rely on external

help. The investment situation has been made more complex

in the past two years with the unexpected reduction in feed-in

tariffs for some successful schemes (largely due to the

pressure the recession has put on public finances). To ensure

further investment in the future, it is vital that governments

provide clarity and stability for potential investors.

Key Impact/Opportunities

1) The renewables sector offers a huge range of potentially

attractive opportunities; the challenge for any investor is to

assess and determine which are the best. With different

electricity prices and feed-in tariffs from country to country,

investors need to either develop strong competencies in

monitoring and assessing opportunities or rely on external

help. The investment situation has been made more complex

in the past two years with the unexpected reduction in feed-in

tariffs for some successful schemes (largely due to the

pressure the recession has put on public finances). To ensure

further investment in the future, it is vital that governments

provide clarity and stability for potential investors.

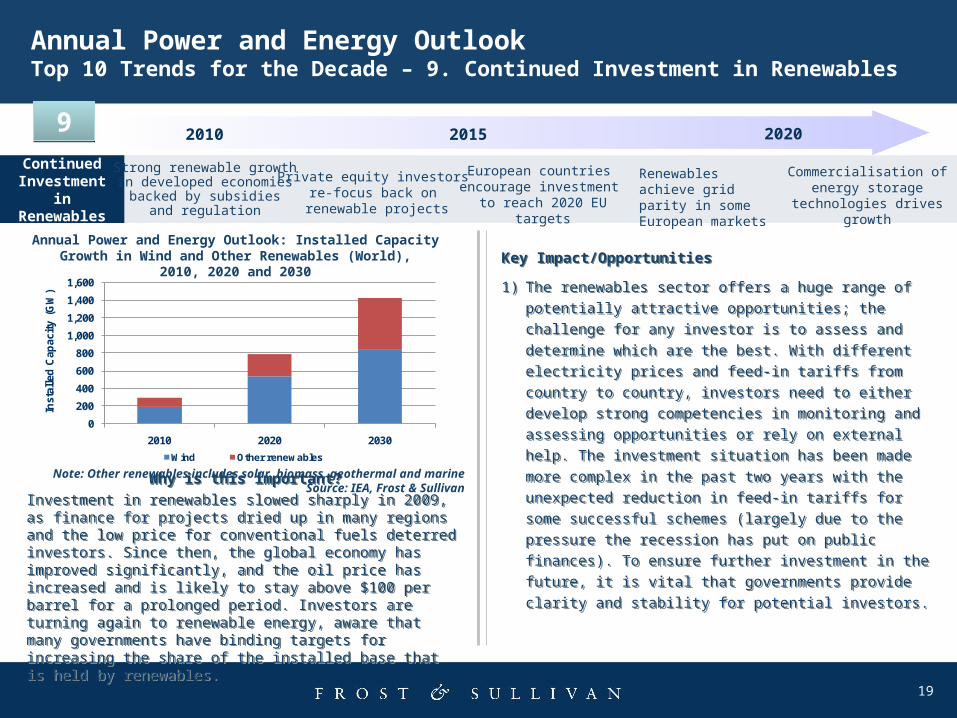

Annual Power and Energy Outlook: Installed CapacityGrowth in Wind and Other Renewables (World),

2010, 2020 and 2030

Why is this important?

Investment in renewables slowed sharply in 2009, as finance for projects dried up in many regions and the low price for conventional fuels deterred investors. Since then, the global economy has improved significantly, and the oil price has increased and is likely to stay above $100 per barrel for a prolonged period. Investors are turning again to renewable energy, aware that many governments have binding targets for increasing the share of the installed base that is held by renewables.

Why is this important?

Investment in renewables slowed sharply in 2009, as finance for projects dried up in many regions and the low price for conventional fuels deterred investors. Since then, the global economy has improved significantly, and the oil price has increased and is likely to stay above $100 per barrel for a prolonged period. Investors are turning again to renewable energy, aware that many governments have binding targets for increasing the share of the installed base that is held by renewables.

99

Renewables achieve grid parity in some European markets

European countries encourage investment

to reach 2020 EU targets

Strong renewable growth in developed economies

backed by subsidies and regulation

Private equity investors re-focus back on

renewable projects

Commercialisation of energy storage

technologies drives growth

Note: Other renewables includes solar, biomass, geothermal and marineSource: IEA, Frost & Sullivan

0

200

400

600

800

1,000

1,200

1,400

1,600

2010 2020 2030

Inst

alle

d C

apac

ity

(GW

)

Wind Other renewables

20

Annual Power and Energy Outlook Top 10 Trends for the Decade – 9. Continued Investment in Renewables (Contd …)

Continued Investment in Renewables

2010 20202015

Key Impact/Opportunities (Contd …)

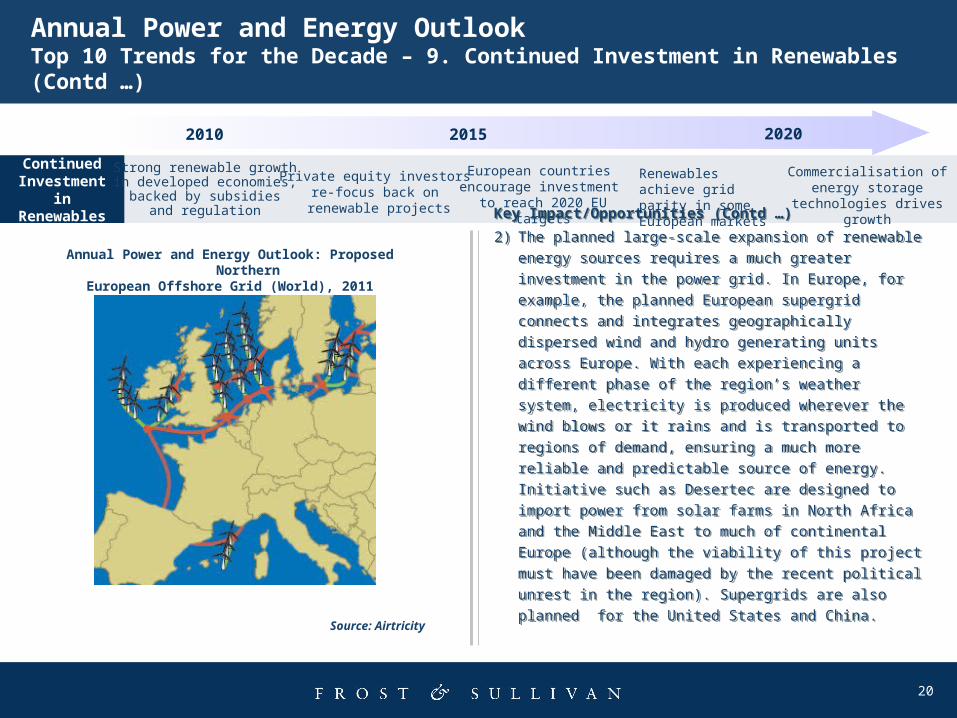

2) The planned large-scale expansion of renewable energy

sources requires a much greater investment in the power grid.

In Europe, for example, the planned European supergrid

connects and integrates geographically dispersed wind and

hydro generating units across Europe. With each experiencing

a different phase of the region’s weather system, electricity is

produced wherever the wind blows or it rains and is

transported to regions of demand, ensuring a much more

reliable and predictable source of energy. Initiative such as

Desertec are designed to import power from solar farms in

North Africa and the Middle East to much of continental

Europe (although the viability of this project must have been

damaged by the recent political unrest in the region).

Supergrids are also planned for the United States and China.

Key Impact/Opportunities (Contd …)

2) The planned large-scale expansion of renewable energy

sources requires a much greater investment in the power grid.

In Europe, for example, the planned European supergrid

connects and integrates geographically dispersed wind and

hydro generating units across Europe. With each experiencing

a different phase of the region’s weather system, electricity is

produced wherever the wind blows or it rains and is

transported to regions of demand, ensuring a much more

reliable and predictable source of energy. Initiative such as

Desertec are designed to import power from solar farms in

North Africa and the Middle East to much of continental

Europe (although the viability of this project must have been

damaged by the recent political unrest in the region).

Supergrids are also planned for the United States and China.

Renewables achieve grid parity in some European markets

European countries encourage investment

to reach 2020 EU targets

Strong renewable growth in developed economies,

backed by subsidies and regulation

Private equity investors re-focus back on

renewable projects

Commercialisation of energy storage

technologies drives growth

Annual Power and Energy Outlook: Proposed NorthernEuropean Offshore Grid (World), 2011

Source: Airtricity

21

Annual Power and Energy Outlook Top 10 Trends for the Decade – 10. Market Liberalisation

Market Liberalisation

2010 20202015

Key Impact/Opportunities

1) Liberalised markets demand flexible power generation

infrastructure capable of responding to electricity price

changes on traded exchanges in the shortest possible time

frame. This will benefit gas turbine technology, which is the

most flexible in terms of its short start-up times and ability to

respond to load changes. There is also a boost for the

service market as equipment suffers greater strain from

flexible generating modes.

2) As the EU completes its liberalised power market and as

market liberalisation expands from the developed countries to

the developing regions, such countries will also develop a

more diverse fuel mix. Electricity market liberalisation tends

to go hand in hand with liberalisation of energy markets in

general, with gas market liberalisation for instance acting as

a driver for lower gas prices and better fuel availability, thus

again spurring the growth of gas-fired power generation.

Key Impact/Opportunities

1) Liberalised markets demand flexible power generation

infrastructure capable of responding to electricity price

changes on traded exchanges in the shortest possible time

frame. This will benefit gas turbine technology, which is the

most flexible in terms of its short start-up times and ability to

respond to load changes. There is also a boost for the

service market as equipment suffers greater strain from

flexible generating modes.

2) As the EU completes its liberalised power market and as

market liberalisation expands from the developed countries to

the developing regions, such countries will also develop a

more diverse fuel mix. Electricity market liberalisation tends

to go hand in hand with liberalisation of energy markets in

general, with gas market liberalisation for instance acting as

a driver for lower gas prices and better fuel availability, thus

again spurring the growth of gas-fired power generation.

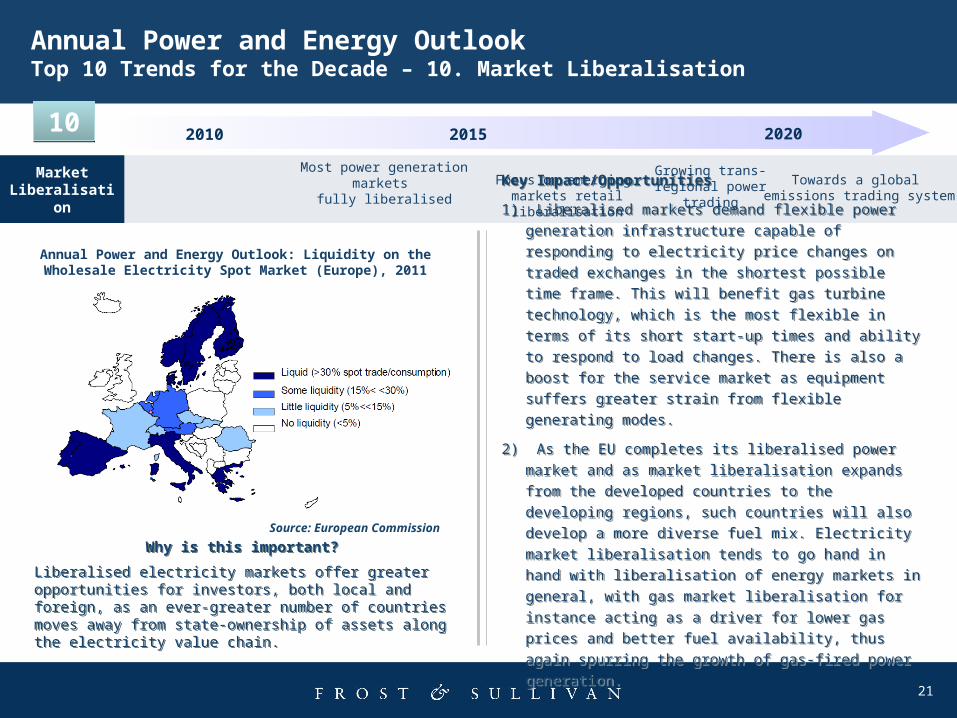

Annual Power and Energy Outlook: Liquidity on theWholesale Electricity Spot Market (Europe), 2011

Why is this important?

Liberalised electricity markets offer greater opportunities for investors, both local and foreign, as an ever-greater number of countries moves away from state-ownership of assets along the electricity value chain.

Why is this important?

Liberalised electricity markets offer greater opportunities for investors, both local and foreign, as an ever-greater number of countries moves away from state-ownership of assets along the electricity value chain.

1010

Focus on emerging markets retail liberalisation

Growing trans-regional power trading

Most power generation markets fully liberalised

Towards a global emissions trading system

Source: European Commission

22

Annual Power and Energy Outlook Top 10 Trends for the Decade – 10. Market Liberalisation (Contd …)

Market Liberalisation

2010 20202015

Key Impact/Opportunities (Contd …)

3) Electricity markets are becoming increasingly interconnected,

with the pioneering development of multi-country power

exchanges such as Nordpool paving the way for other such

exchanges around the world. Over the longer term, the market

liberalisation will also boost interconnection with far-off regions

such as the Sahara desert to export solar-generated power to

Europe.

4) The market liberalisation also boosts a more efficient

operation of emissions trading schemes. The operational

schemes are the Kyoto Protocol, the European Emissions

Trading System (EU ETS) as well as smaller schemes in New

Zealand, parts of the United States and Japan’s capital of

Tokyo. Future schemes are planned for areas such as

Australia, Western United States and South Korea. All these

schemes will become increasingly interlinked and integrated

over time.

Key Impact/Opportunities (Contd …)

3) Electricity markets are becoming increasingly interconnected,

with the pioneering development of multi-country power

exchanges such as Nordpool paving the way for other such

exchanges around the world. Over the longer term, the market

liberalisation will also boost interconnection with far-off regions

such as the Sahara desert to export solar-generated power to

Europe.

4) The market liberalisation also boosts a more efficient

operation of emissions trading schemes. The operational

schemes are the Kyoto Protocol, the European Emissions

Trading System (EU ETS) as well as smaller schemes in New

Zealand, parts of the United States and Japan’s capital of

Tokyo. Future schemes are planned for areas such as

Australia, Western United States and South Korea. All these

schemes will become increasingly interlinked and integrated

over time.

Annual Power and Energy Outlook: Priority Corridorsfor Electricity and Gas (Europe), 2011

Focus on emerging markets retail liberalisation

Growing trans-regional power trading

Most power generation markets fully liberalised

Towards a global emissions trading system

Source: EC DG Energy