Now + New + Next: Rethinking Rewards in the New Engagement Economy

COSO Updates Framework for Technological Advancements; Is Your Company Following Suit? pg 12

Practice Niches Increase Energy and Profitability pg 18

Eight Rules for Effective Technology Management pg 22

The Impact of Presidential Elections on the Stock Market pg 26

The ASSeT is the official publication of the Missouri society of certified public accountants.

Ja n ua r y 2 0 1 7

in this issue:

pg 8

That Was Fun— Now What? The Economy in 2017

2 the Asset | January 2017

With sincere appreciation… Thanks to the generosity of MSCPA members, 33 accounting students were awarded $37,250 in scholarships for the 2015-2016 school year. Your support helps these students to realize their aspirations of working in this rewarding profession. Your contributions are much appreciated!

Leadership GiftsAnders CPAs + AdvisorsBKD CPAs & Advisors

Major GiftsMarksNelson CPARichard Mills III, CPA

speciaL GiftsGrant Thornton LLPSchmersahl Treloar & Co., PCThe Whitlock Company, LLP

partnersDonald Danner, CPA

Kiefer Bonfanti & Co. LLPLopata, Flegel & Company LLPMueller Prost LCRubinBrown LLPSFW Partners LLCTroutt, Beeman & Co., P.C.UHY LLP

advocatesBank of AmericaPatricia Reuter, CPARuth Saphian, CPA

Bronze PArtner CluBbank of americaKenneth a. Moore, cpa, p.c.

BenefACtorbeth boyd, cpa, p.c.h.c. hall, cpaJohn a. hartwig Jr., cpahershewe and company, p.c.John M. hillhouse, cpa, llcMaher & company pctimothy J. Mclaughlin, cpa, pcnemo cpa’s llcnovak birks, p.c.riley, stubbs and cato l.l.c.schroeder & associates, p.c.sommer & associates, cpas, llcuetrecht family fund

Don Breimeier memoriAl CAmPAignGerard Meiners, cpa

SummA Cum lAuDediann Gross, cpaJennifer heim, cpaVenable houts, cpaGary lipscomb, cpapatricia reuter, cpa

mAgnA Cum lAuDeMarkus ahrens, cpadonald danner, cpastephen del Vecchio, cpa

John Gamble, cpalinda hopkins, cpaGary Johnson, cpaJanice Klimek, cpaanalee lanio, cpastanley schmidt, cpapatricia soltys, cparickard tarzwell, cpaJeffrey Ward, cpaJulie Welch, cpa

Cum lAuDedawn anderson, cpaMark barrett, cpaW. robert berg, cpaZack bettis, Jr., cparobert boast, cpaKeith boeller, cpacarol bounds, cparebecca boyer, cparoberta broeker, cpaJohn butler, cparichard capelli, cparex carter, cpapaul chapman, cpab. Wayne clark, cpapenny clayton, cpaMichael croghan, cpalori crump, cpac. Michael dambach, cpasondra depriest, cpaJames devereux, cpalinda ehler, cpasylvia ehrenreich, cpadaniel elder, cpaJohn everest, cpadeborah George, cpaandrew Gingrich, cpaMichael hammond, cpasusan heinsz, cpa

thomas hilton, cpabilly hixon, cpaGregory hodits, cpathomas hornung, cpaeileen hutchinson, cpaaudrey Katcher, cparobert Kaveler, cpadebra Kerby, cpastephen Keyser, cpalisa Klempert, cpabrett lewis, cpaJohn lindbloom, cpadeborah loomis, cpabryan lundstrom, cpaMolly Malone, cpaJohn Mccartney, cpalouis Mcdonald, cpar. douglas McWard, cpaelisabeth Merenda, cpacassandra Meschke, cpadouglas Milford, cpacecil Miller, cpastephen and Jennifer Moehrle, cpasJerry Mogg, cpanoah Moravec, cpaW. david Myers, cpateri newhouse, cpanathan newton, cpaJames o’hallaron, caeWilliam ossie, cpacharles and denise pierce, cpastodd pleimann, cpaMark radetic, cpacharles robb, cpadaniel robinson, cpacharles schutte, cparonald terry, cpaJulie treloar, cpa

catherine turner, cparaymond uetrecht, cpaJennifer Vacha, cpaedwin Vandeven, cpapaul Wentzien, cpabrent Wilson, cpasteven york, cpa

DeAn’S liStJenny bryant, cpacinda chapman, cpasue childers, cpadwayne clark, cpaJoe dwigans, cpachristopher fava, cpaWilliam felty Jr., cpalisa Gioia, cpaKathleen Gray, cpabrooke Grechus, cpaMary lou hamlin, cpaandrew heck, cpaJames huber, cpaterrance Knox, cpabrent Mcclure, cpaJoseph Meek, cpaJerry Mitchell, cpaJenelle MooreJohn pokrefke, cpacindy puettmann, cpapatrick rohrkaste, cpacathy roper, cpaJulie roth, cpaleigh salzsieder, cparita schwager, cpachristopher smith, cpacharles starkey, cparobert tobben, cpaJeremy Varel, cpaWanting Zhou, cpa

Honor rollruth barasa, cpaedith betz, cpaGary boehmer, cpaKaitlin carrier, cpadavid freisner, cpanorman Glaus, cpatimothy hayden, cpaphilip hayes, cpaKenneth henslee, cpaJoan humes, cpaGina James, cpapatrick Miller, cpathomas opich, cpaluke pope, cpaGavin poppen, cpalorri rippelmeyer, cpathomas sims, cpacatherine strauss, cpadebra swiney, cpaGerald Williams, cpaMichael Wilson, cpa

*As of Dec. 7, 2016

BriDge to tHe future CAPitAl CAmPAign

mAke Your mArkhelp ensure the future of your profession. by making a tax- deductible contribution to the Mscpa scholarship campaign, you are enabling students to have the same fulfilling career opportunities you have experienced. Visit mocpa.org/contribute today!

the Asset | January 2017 3

1 17VoluMe 65, no. 1

PUBLISHeD BI-MoNTHLY BY THe MISSoURI SoCIeTY oF CeRTIFIeD PUBLIC ACCoUNTANTS

PublisherJames T. o’Hallaron, CAeEditor Dena HullArt Director Ryan Morris

The ASSET Editorial & Advertising Offices: 540 Maryville Centre Drive, Suite 200 St. Louis, MO 63141 phone: (314) 997-7966 toll free: (800) 264-7966 fax: (314) 997-2592 web: mocpa.org

Editorial Contact Dena Hull [email protected] Advertising Contact Mike Walker [email protected]

2016-2017 oFFICeRSChair John W. Lindbloom, CPAChair-Elect John D. Gamble, CPAVice Chair Sondra J. DePriest, CPATreasurer Jeffrey e. Ward, CPASecretary Rachel Dwiggins, CPA

The ASSET is published as a service to members of the Missouri Society of CPAs. MSCPA members receive the ASSET at no charge. Non-member subscriptions are available for $42 per year.

Views, opinions, advertising, and commentary appearing in the ASSET are not necessarily endorsed by the MSCPA. Information provided in the ASSET requires careful consideration of facts and circumstances before applying to specific situations.

©2017 Missouri society of cpas

268

18

F E A T U R E S

8 ThatWasFun—NowWhat?TheEconomyin2017 With change being mandated, the new year promises to be tumultuous. the economy ended strong in 2016, but what are the determining factors in how long it can be sustained? ByChrisKuehl,Ph.D.

12 COSOUpdatesFrameworkforTechnological Advancements;IsYourCompanyFollowingSuit? use coso’s new guide to develop an effective fraud risk-management program, including conducting risk assessments, designing preventive control processes, and responding to wrongdoing.

ByCatherineturner,CPa,CGMa,Cia,CrMa

18 PracticeNichesIncreaseEnergyandProfitability developing a niche practice area can provide economic advantages without being overly risky. learn the potential benefits of specializing, and determine which area is right for your practice. ByJosePht.eCKelKaMP,CPa

22 EightRulesforEffectiveTechnologyManagement as technology’s rapid advancements create challenges and opportunities, it’s essential to develop a technology plan that integrates with your organization’s overall vision. ByJiMBooMer,CPa,CitP,MBa

26 TheImpactofPresidentialElectionsonthe StockMarket While the future near-term direction of the stock market remains unknown, a historical review of presidential elections can help investors with their long-term strategies. ByDaviDPresson,CFa

S P E C I A L I N T E R E S T N E W S

6 Government Advocacy ByCharlesa.PierCe,CPa,CGMa 10 Taxation ByCathyB.GolDstiCKer,CPa,CGMa

14 Accounting and Auditing ByDeBorahlooMis,CPa

16 Young Professionals ByZaCharyM.MCDowell,CPa

I N E V E R Y I S S U E

4 Chair’s Message5 President’s Message17 New Members20 Society Spotlight 28 MSCPA Snapshots30 Professional Learning31 Classified Advertising

BriDge to tHe future CAPitAl CAmPAign

4 the Asset | January 2017

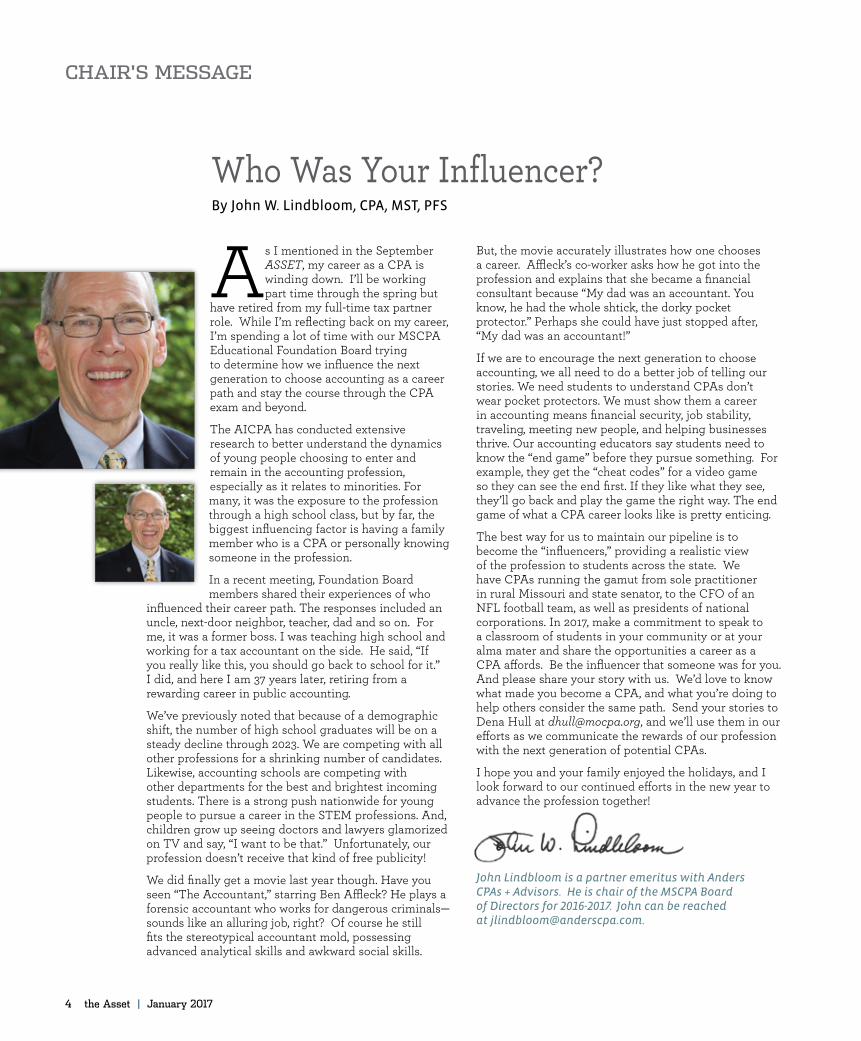

As I mentioned in the September ASSET, my career as a CPA is winding down. I’ll be working part time through the spring but

have retired from my full-time tax partner role. While I’m reflecting back on my career, I’m spending a lot of time with our MSCPA Educational Foundation Board trying to determine how we influence the next generation to choose accounting as a career path and stay the course through the CPA exam and beyond.

The AICPA has conducted extensive research to better understand the dynamics of young people choosing to enter and remain in the accounting profession, especially as it relates to minorities. For many, it was the exposure to the profession through a high school class, but by far, the biggest influencing factor is having a family member who is a CPA or personally knowing someone in the profession.

In a recent meeting, Foundation Board members shared their experiences of who

influenced their career path. The responses included an uncle, next-door neighbor, teacher, dad and so on. For me, it was a former boss. I was teaching high school and working for a tax accountant on the side. He said, “If you really like this, you should go back to school for it.” I did, and here I am 37 years later, retiring from a rewarding career in public accounting.

We’ve previously noted that because of a demographic shift, the number of high school graduates will be on a steady decline through 2023. We are competing with all other professions for a shrinking number of candidates. Likewise, accounting schools are competing with other departments for the best and brightest incoming students. There is a strong push nationwide for young people to pursue a career in the STEM professions. And, children grow up seeing doctors and lawyers glamorized on TV and say, “I want to be that.” Unfortunately, our profession doesn’t receive that kind of free publicity!

We did finally get a movie last year though. Have you seen “The Accountant,” starring Ben Affleck? He plays a forensic accountant who works for dangerous criminals—sounds like an alluring job, right? Of course he still fits the stereotypical accountant mold, possessing advanced analytical skills and awkward social skills.

But, the movie accurately illustrates how one chooses a career. Affleck’s co-worker asks how he got into the profession and explains that she became a financial consultant because “My dad was an accountant. You know, he had the whole shtick, the dorky pocket protector.” Perhaps she could have just stopped after, “My dad was an accountant!”

If we are to encourage the next generation to choose accounting, we all need to do a better job of telling our stories. We need students to understand CPAs don’t wear pocket protectors. We must show them a career in accounting means financial security, job stability, traveling, meeting new people, and helping businesses thrive. Our accounting educators say students need to know the “end game” before they pursue something. For example, they get the “cheat codes” for a video game so they can see the end first. If they like what they see, they’ll go back and play the game the right way. The end game of what a CPA career looks like is pretty enticing.

The best way for us to maintain our pipeline is to become the “influencers,” providing a realistic view of the profession to students across the state. We have CPAs running the gamut from sole practitioner in rural Missouri and state senator, to the CFO of an NFL football team, as well as presidents of national corporations. In 2017, make a commitment to speak to a classroom of students in your community or at your alma mater and share the opportunities a career as a CPA affords. Be the influencer that someone was for you. And please share your story with us. We’d love to know what made you become a CPA, and what you’re doing to help others consider the same path. Send your stories to Dena Hull at [email protected], and we’ll use them in our efforts as we communicate the rewards of our profession with the next generation of potential CPAs.

I hope you and your family enjoyed the holidays, and I look forward to our continued efforts in the new year to advance the profession together!

John Lindbloom is a partner emeritus with Anders CPAs + Advisors. He is chair of the MSCPA Board of Directors for 2016-2017. John can be reached at [email protected].

CHAir'S meSSAge

Who Was your influencer?By John W. Lindbloom, CPA, MST, PFS

the Asset | January 2017 5

PreSiDent'S meSSAge

I hope the new year finds you energized and ready to take on whatever comes your way! With CPAs being planners, I’m sure many of you have set formal resolutions or have given some thought

to what you want to accomplish this year. I’ll borrow a quote from Stephen Covey that member Joe Eckelkamp uses in his article (page 18), “Begin with the end in mind.”

What do you hope to achieve by year’s end? Picture the outcome you plan to attain, and then let the MSCPA help you get there. This edition of the ASSET provides food for thought in many areas to assist you with professional growth in the months ahead, including: expanding your practice with niche specialties (pages 10 and 18); developing management plans for fraud risk or technology (pages 12 and 22); and increasing your network (page 16).

This year, we will continue striving to offer relevant opportunities that will help you fulfill your year-end goals. To ensure we fully understand your preferences and interest areas, we are converting to a new member database that will allow us to capture better data as well as analyze and effectively apply it to resource development. This will be tied to an enhanced website that will be more intuitive and user-friendly for you. We’ll also be rolling out a new logo that matches our MOCPA url. We’ve often been asked “why is the MSCPA at MOCPA.org?” And, when Missouri CPAs search for the MSCPA online, they find four other state CPA societies. We will be the one and only MOCPA! Watch for this changeover soon.

Also in 2017, we’re building on priorities established during our strategic planning process, which include hosting more events for our members to connect with each other, as well as with members of other professions. We’re adding open houses and happy hours with several other professional associations. We’re planning more roundtable discussions for members in private industry, as well as firm administrators. In early January, we’re hosting a gathering of accounting educators and top firm leaders to discuss the outlook for recruiting new CPA candidates into the pipeline and, ultimately, into your firm or company. In addition, we’ve formed a new diversity committee and have been meeting regularly with Steven Harris, MSCPA member and chair of the National Association of Black Accountants, to address the challenges of recruiting and retaining minorities in the profession. As our economist, Chris Kuehl, points out in his article (page 8), most professions will be competing for a shortage of talent in the coming years, and ours is not immune.

We continue to strengthen our efforts to protect the profession through government advocacy in Jefferson City (page 6). The new legislative session convened on Jan. 4., and we’ve been working behind the scenes for months drafting proposed statute revisions that would bring us in line with the Uniform Accountancy Act. We’re fortunate to have an MSCPA member in the state senate this year, Denny Hoskins, CPA. Having relationships with legislators goes a long way in having our issues heard and acted on in the Legislature. As you’re thinking of new ways to get involved in the profession this year, CPA Day on Jan. 18 is a good place to start. It’s not too late to sign up (mocpa.org/cpaday). The event provides you with an overview of legislation that could impact your business or your clients. In addition, we need help delivering Legislator’s Tax Guides to all senators and representatives. If this is a new area for you, don’t be intimidated. We have many “regulars” who are happy to show you around. And because many of our longtime volunteers are beginning to retire, we truly need new member participation.

And finally, as you’ll see on pages 28-29, we wrapped up 2016 with our annual Awards Celebrations. I can’t think of a better way to end the year. Gathering with 400 plus CPAs, family members and friends to honor our colleagues’ milestones from the year gave everyone a sense of pride in the profession and provided a boost of inspiration to continue achieving and setting high standards for the year ahead.

As you set your sights on achieving your end goals in 2017, let us know how we can best help you get there. May the new year bring you much success and prosperity!

Jim O’Hallaron is a certified association executive (CAE) and is the president of the Missouri Society of Certified Public Accountants. He leads the staff and operations for the 8,000-member society. Jim can be reached at [email protected].

Visualize achieving your 2017 GoalsBy James T. O’Hallaron, CAE

6 the Asset | January 2017

help the Mscpa Make an impact this legislative sessionBy Charles A. Pierce, CPA, CGMA

More than 2,000 bills will be filed during the 2017 Missouri legislative session, which convenes on Jan. 4. The MSCPA government relations team has the challenge

of determining which of those bills could impact your business or clients, whether to support or oppose the legislation, and the most effective method for taking action. The driving force behind these decisions is a dedicated group of MSCPA volunteers who serve on the Legislative and Tax Policy Task Force.

A few years ago, MSCPA leaders recognized that legislation impacting the profession and members’ clients was on the increase. At the same time, term limits were impacting the knowledge base of the Legislature. The MSCPA’s time-proven system of working quietly with key legislative leaders and committee chairs was becoming less effective because of legislative turnover. The profession faced a situation of relatively new legislators on various committees trying to understand complex tax legislation. In order to facilitate a more dynamic and pro-active means of dealing with legislation, the MSCPA Board of Directors appointed the Legislative and Tax Policy Task Force.

At first, the task force was made up of various past and current MSCPA Board members. Over time, the task force structure has evolved to consist of the chairs of the MSCPA Taxation, and Government Advocacy and Legislation Committees, as well as various subject matter experts. The task force meets weekly via conference call during session to discuss legislation. The Legislature meets from January to mid-May, so these calls occur during the height of the members’ busy season. In addition to the calls, members take on the responsibility to research specific bills during the week. Because of the Legislature’s fluid environment, task force members are also prepared to respond to ever-changing situations.

The task force serves as a valuable resource for the MSCPA government relations team. During the meetings, the team discusses the professional and practical impact of legislation. For any bills affecting the profession, the group develops strategies for handling. This can range all the way from informally discussing matters with a bill sponsor to testifying on legislation. The strategy may vary on the same bills from week to week as the legislation progresses.

Originally formed to provide input on tax legislation, the task force’s focus has broadened in recent years to include business regulatory measures impacting the profession. The group has had to wrestle with such issues as mandatory leave policies, ban the box, restrictions on overtime, and other employment practices legislation.

The task force does not work in a vacuum. Its policy and decisions are shaped by a combination of MSCPA Board policy, AICPA policy and member input. At all MSCPA Board meetings, legislative issues and policy are discussed. The board’s decisions provide the foundation for the task force’s weekly discussions. Also, the AICPA develops an annual list of legislative priorities for the states. This document offers a valuable guide for how issues in Missouri are viewed in other states. Each week, the MSCPA Government Relations Department emails all members a legislative newsletter highlighting key bills so they have an opportunity to provide input. Member feedback becomes part of the task force’s discussion.

By implementing this process, the MSCPA has significantly increased its effectiveness with the Legislature. Many times, the task force’s input has resulted in improvements to tax legislation. Equally important, concerns they raise have helped stop detrimental legislation from passing.

Every MSCPA member has the opportunity to contribute to the process. There are many ways for you to get involved and make an impact this legislative session, including:

• Serve as a Keyperson for your legislator;

• Attend CPA Day on January 18 in Jefferson City;

• Read the weekly Government Advocacy Update, and share any concerns; and

• Contribute to MO CPA-PAC.

For additional details on the MSCPA’s government advocacy initiatives, visit mocpa.org/government-advocacy or contact Dena Hull at [email protected] or (800) 264-7966, ext 105.

Chuck Pierce is the government relations consultant for the Missouri Society of CPAs. He can be contacted at [email protected].

government ADvoCACY

the Asset | January 2017 7

Experienced.

Professional.Confidential.

Experienced.

Professional.Confidential.

TM

Specializing in the sale of accounting firms and tax practices, our team at Accounting Biz Brokers is committed to providing personalized business brokerage services to our clients and customers. Contact us today to explore the possibility of listing your practice or to receive information about any of our current listings.

Working together, we get deals done.

8 the Asset | January 2017

It is a good thing that nobody really expects too much from an economist when it comes to forecasting. After all, we compete with the weather people for the distinction of being wrong. After this past election, economists can at least assert that we are far better than

the pollsters. This election has also made the task of looking deeply into the economic future that much harder. It’s a whole new ballgame, and one that few were really prepared for.

What can be said about 2017 that will make sense for more than a few days? It will come down to three sets of assertions. There are the economic developments that were going to take place no matter who won the election; the developments that are more likely to take place because the GOP now controls the White House and Congress (as well as the majority of states); and the developments that will only take place if absolutely everything goes strictly according to plan.

The first set of assertions is perhaps the easiest to identify as many of them have started already and are simply expected to continue. Interest rates set by the Fed will rise. They went up in December as expected, and they will continue to increase—probably to between 1.5 and 2 percent by the end of 2017. Along with the rates, there will be a hike in inflation that will be driven mostly by wage pressure but by some commodity price pressure as well. The latter moves will be subtle and halting, but after wages start to rise, they will accelerate. In recent weeks, the first sign has appeared that the oil producing states are willing to start reducing their output enough to impact prices. The shortage of skills plays into the rise in wages as companies are required to pay more to get the people they need and to hang on to those they already have.

In addition, you can count on a higher valued dollar. The gains will accelerate in part due to the hike in interest rates. More and more global investors will take an interest in the U.S. market, and they will need dollars to get in. This boosts demand, and soon the dollar begins a surge that will have a negative impact on any sector in the United States that relies on export demand, including the manufacturing and farm sectors. In point of fact, it will be the dollar rise that creates the most threat to the growth projections for 2017. It’s often forgotten that the United States relies on exports for approximately 14 percent of the national GDP. (In comparison, Japan relies on exports for approximately 14.7 percent of its annual GDP.)

The second set of developments is due to the change in power at the federal level. It’s a given there will be changes, but for the moment it’s not altogether certain what these will look like—precisely. Three important economic targets will be regulation, tax reform and infrastructure development. These have all been discussed for years, but no real progress has been made. This may change in the new administration but not as fast as many had hoped.

Regulations rank as one of the highest priority areas for reform. The top of the priority list is the Bank Reform Act, as this 3,500-page monstrosity has been the bane of the small bank’s existence. The pledge has been to overhaul it and strip away the provisions that have most vexed the small and community banks, which small manufacturers depend on. There will also be efforts to get bureaucracies as varied as the EPA, NLRB, OSHA and many others to back off on regulations that appear to serve no other purpose than to slow growth and expansion. The mood of the Trump team was made clear with the selections of

That Was Fun — Now What? The Economy in 2017By Chris Kuehl, Ph.D.

the Asset | January 2017 9

an EPA head who has sued the agency repeatedly for overstepping its bounds and a labor secretary who has lobbied against everything from a higher minimum wage to various proposals that support unions.

Tax reform is always easier to talk about than to execute, but the idea is to cut taxes on those who will spend and on business so that there is more investment. The tax system now really favors the very rich and those who don’t pay taxes at all. The burden falls on the middle class and the small business community. Tax reform will be the responsibility of Congress, and there is no more agreement now than there was last year. However, there is a strong feeling that now is the time to tackle some of the longer standing issues. Look for lower corporate taxes and an attack on the maze of tax breaks and exemptions that allow major companies to avoid taxes and leave the burden on the small and medium businesses.

The infrastructure boost has been discussed for years, but there is always the same issue—how to fund it. The need is for an investment of more than a trillion dollars but that would be a monumental budget buster. The plans are to somehow engage the private sector investor in this effort but that means prioritizing projects that have revenue connected—toll roads, bridges, and projects where fees can be charged. There is also talk of providing businesses a deal so that they will be encouraged to repatriate their overseas funds. One idea would allow them to bring 75 percent of the money back tax free if they spend the remaining 25 percent on an infrastructure bond that would create a fund that could be drawn upon for these projects.

The third set of developments will rely on many things going just right. New trade deals may be hammered out that are better for the United States, and there may be more cooperation from countries that want to keep working with the United States. It is also possible that trade wars break out, and everybody loses. The most important factor for manufacturing growth is a workforce that is ready to take the sector to the next level, which is not something that can happen overnight. If there is a commitment to filling jobs that are already available, it will advance the economy far more than creating new ones that people can’t be found for.

The workforce development issue is perhaps the most vexing and the real wild card. Throughout the campaign, there was incessant commentary on the need to “create jobs” when the real issue is filling the ones that already exist. Right now, it is estimated there are close to a million jobs available in manufacturing

alone, 300,000 in trucking, and 300,000 in construction. The fast growing medical sector is short of physical therapists, occupational therapists, nurses of all description and even doctors. There are very few sectors that are not seeking new entrants, and once these employees are added, there is a struggle to keep them. Fixing this will be anything but simple as it will require cooperation between businesses, the educational sector and the people who will be expected to train for these new jobs.

This will be a tumultuous year—that much is certain. In my opinion, the verdict on the last eight years was essentially negative, and there will be a mandate to change things. The problem is that few are really certain what needs to be changed and what should be expected to replace it. The economy at the end of 2016 was strong and that provides some momentum for 2017. How long this can be sustained remains the big question.Dr. Chris Kuehl is the co-founder and managing director of Armada Corporate Intelligence in Kansas City. He is the author of the MSCPA’s daily Business Intelligence Brief. Chris can be reached at [email protected].

20%OFF!

30%OFF!

50%OFF!

80%OFF!

Selling on Your Own?For Sale by Owner = Discount to Buyers. Accounting Practice Sales is the largest facilitator in North America for selling accounting and tax practices. Our access to the greatest number of potential buyers provides you the best opportunity of matching not only with the right buyer but also obtaining the optimum price and terms.

Contact us today so we can sell your practice for what it is worth.

Gary L. Holmes1-888-847-1040 x 1

10 the Asset | January 2017

startups as tax clients: risky, but rewarding, Work for cpasBy Cathy B. Goldsticker, CPA, CGMA

The startup ecosystem in Missouri is red hot. From St. Louis, to Mid-Missouri to Kansas City, a multitude of groups throughout the state are investing time and capital to make Missouri

an attractive place to launch and grow a company. Recent data from the Kauffmann Foundation about startup communities across the country yielded some good news for St. Louis. The percentage of startups in business for five years has grown the last three consecutive years. The St. Louis startup community also

made national headlines, most notably being named the fastest-growing startup scene by Business Insider.

BuildingaCaseinYourFirmforaStartupPracticeShould you pursue startup clients, it’s critical to seek opportunities to share the successes you have with your firm leadership. Illustrate that what might begin as a startup relationship can evolve into a broader business opportunity for your firm. Share success stories and the potential for business opportunities, such as valuation services for the startup’s S election, executive tax services as the startup grows, or compliance tax return preparation for the partnership (LLC) startup that might switch to a C corporation. When a company goes public, there are a host of other services that are needed, ultimately leading to an audit of current and perhaps prior years’ financial statements.

While revenue won will certainly help build the case for a startup practice, there are other equally important but less easily quantified reasons why you might want to develop a startup practice, including providing training opportunities for your staff and supporting business growth in your community.

ChallengesofWorkingwithStartupsThere are inherent challenges startup companies tend to face, which become your challenges when working with them, including:

• Entrepreneurs aren’t accountants. Keep reminding yourself of this key point as you build relationships with startup companies. Accounting/tax isn’t their strength, and it’s why they’ve engaged you to help. Be patient, and make time to explain tax and accounting concepts to them. Do this in simple terms, and be prepared to repeat the same concepts a few times. It might be the first time they’ve been exposed to this.

• Entrepreneurs can be hard to pin down. Get ready for follow up, including repeated emails and phone calls.

• Many entrepreneurs have limited resources. Companies that are just starting up tend to have limited cash flow and small teams. Don’t be surprised to see one person handling the critical operational aspects of the business. On the surface, this makes the startup appear disorganized, when the startup is only making its best effort at managing competing priorities. Do your best to encourage advance tax planning and organizational assistance to ensure they meet their tax deadlines. Creating tax templates and checklists for different tax services helps to minimize the cost for many of the repetitive services startups require.

• Cash is king. In a recent survey of St. Louis startups, and the diverse community that supports them, responders said cash flow was their top challenge. The need for funds drives a lot of startups’ decision making, like which advisers to work with. An inconsistent advisory team can lead to reporting omissions, errors and general challenges, which is why it is important to encourage CPA loyalty. To help the startup preserve its funds, think about the services that aren’t economically feasible for you to provide as a CPA. A good example is payroll reporting, where a payroll process services provider can avoid costly tax reporting mistakes at a lower cost than a CPA can, without compromising quality. Another savings opportunity is managing cash to reduce surprise tax liabilities, which often occur with cash basis startups.

• Obtaining a business valuation. Startups have three main challenges with getting a business valuation. First, formal valuations are incredibly expensive. Second, it’s hard to find comparable companies to use in the study. Third, many startups don’t have any earnings history. With these challenges, alternate methods to a formal valuation might provide better options for achieving the same result.

CommunitySupportDespite the challenges, working with startup companies can be incredibly rewarding. Most CPA firms are committed to improving their local communities. There’s no question that supporting startups qualifies as community involvement. Who can argue with the value of and goodwill gained from assisting new businesses that help Missouri retain the best and brightest talent, all while creating jobs and tax revenue? Startups may not be the most profitable clients, but they greatly enrich Missouri’s entrepreneurial landscape.

Cathy Goldsticker, CPA, is a tax partner and startup practice leader with Brown Smith Wallace in St. Louis. She can be contacted at [email protected].

tAxAtion

the Asset | January 2017 11

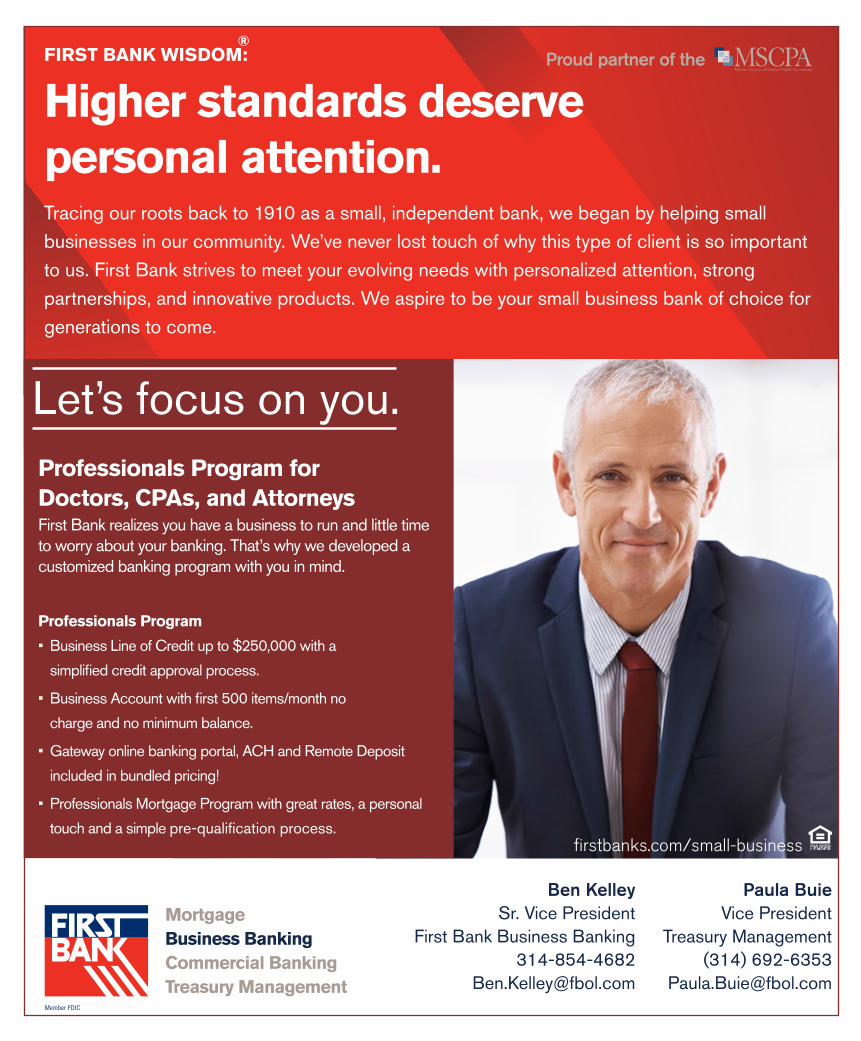

FIRST BANK WISDOM:

Higher standards deserve personal attention.

®

MortgageBusiness BankingCommercial Banking Treasury Management

Ben Kelley Sr. Vice President

First Bank Business Banking 314-854-4682

Paula Buie Vice President

Treasury Management (314) 692-6353

firstbanks.com/small-business

Proud partner of the

Let’s focus on you.

First Bank realizes you have a business to run and little time to worry about your banking. That’s why we developed a customized banking program with you in mind.

Professionals Program for Doctors, CPAs, and Attorneys

Professionals Program

• Business Line of Credit up to $250,000 with a

simplified credit approval process.

• Business Account with first 500 items/month no

charge and no minimum balance.

• Gateway online banking portal, ACH and Remote Deposit

included in bundled pricing!

• Professionals Mortgage Program with great rates, a personal

touch and a simple pre-qualification process.

Tracing our roots back to 1910 as a small, independent bank, we began by helping small businesses in our community. We’ve never lost touch of why this type of client is so important to us. First Bank strives to meet your evolving needs with personalized attention, strong partnerships, and innovative products. We aspire to be your small business bank of choice for generations to come.

12 the Asset | January 2017

Just over three years after updating its Internal Control Framework (Framework), the Committee of Sponsoring Organizations (COSO) released its Fraud Risk Management Guide (Guide). This new report provides organizations a blueprint for establishing

an overall fraud risk-management program. Like most of COSO’s guidance, the Guide’s appendices are filled with examples, templates and tools that can be tailored to each organization’s individual needs. One of the Guide’s unique characteristics is the opportunity to leverage its data analytical recommendations in order to provide value far beyond the perceived boundaries of internal controls by harnessing emerging technological advancements, such as cognitive architecture.

Guide HighlightsTo help organizations obtain best practices and resources focused to their specific needs, the Guide’s resources include considerations for governmental, not-for-profit and smaller organizations. Similar to the Framework, the Guide highlights five core principles and points of focus.

The Guide’s five core principles are mapped to the Framework’s 17 principles. By mapping the Guide’s core principles to the Framework’s principles, auditors and corporate management should consider COSO’s fraud analysis recommendations for each of the Framework’s principles and factor this into their assessment of an organization’s internal control effectiveness. Because the Framework deficiency assessment requires management to assess the identified deficiency’s impact to all other principles and all internal control components, the fraud analysis considerations for each of the 17 principles may further complicate the Framework’s deficiency assessment.

In building upon the Framework’s scope expansion, the Guide states, “…an organization seeking to minimize the adverse impacts of fraud needs to consider fraud risks in all areas of the enterprise and its operations.” Once again, the scope has been explicitly expanded to include significant objectives beyond external financial reporting and even beyond finance in general. Although the Guide’s executive summary makes a brief reference to the potential benefits of future alignment of fraud concepts and terminology with other professional organizations, one can only ponder if the Guide will ever be used in conjunction with the ethics and compliance profession, especially in light of the Federal Sentencing Guidelines’ consideration of effective ethics and compliance programs.

In its executive summary, COSO recognizes that the Guide serves as best practice guidelines for “… this new fraud risk-management principle.” Per the Guide, a best practice fraud risk-management program consists of:

• Fraud risk governance policies—both at the board and management levels;

2013 COSO Framework Principles

COSO Fraud Risk Management Guide Principles

Principles 1-5: Control Environment

Principle 1: Establish and Communicate Fraud Risk Management Program

Principles 6-9: Risk Assessment Principle 2: Risk AssessmentPrinciples 10-12: Control Activities Principle 3: Preventative and

Detective ControlsPrinciples 13-15: Information and Communication

Principle 4: Timely Investigation and Corrective Action

Principles 16-17: Monitoring Activities

Principle 5: Ongoing Evaluations and Deficiency Identification

Source: Fraud Risk Management Guide Executive Summary

COSO Updates Framework for Technological Advancements Is Your Company Following Suit? By Catherine turner, CPa, CGMa, Cia, CrMa

COSO Updates Framework for Technological Advancements Is Your Company Following Suit? By Catherine turner, CPa, CGMa, Cia, CrMa

the Asset | January 2017 13

• Fraud risk assessment;• Design and implement fraud preventative and

detective control activities;• Investigations; and• Monitor and evaluate the program.

Principle Alignment Considerations While principle #8 of the Framework focuses on a fraud risk assessment, the Guide reinforces the need to assess inherent fraud risk (the potential risk itself absent of any internal controls) before assessing residual fraud risk (any remaining risk once current internal controls are considered). The gap between inherent risk and residual risk may be utilized to focus control effectiveness procedures on significant controls and to prevent assumptions about the effectiveness of such controls. Assumed effectiveness of any internal controls should be noted and considered prior to finalizing the organization’s fraud risk-management plan. Oftentimes, accounting and auditing professionals must advocate the importance of assessing inherent risk before considering residual risk.

The correlation outlined between the Guide’s core principles and the Framework’s principles #4 and #5 may lead to more analytical examination of an organization’s demonstrated process for evaluating and timely addressing adherence to its code of conduct. Corporate investigation procedures should be formally documented, which will allow internal audit to test a diverse sample of investigations for compliance to these procedures. This independent review may provide organizational leadership with the insight into consistency and timeliness of investigations.

The Guide defines fraud broadly as, “…any intentional act or omission designed to deceive others, resulting in the victim suffering a loss and/or the perpetrator achieving a gain.” Because this is a broad definition of fraud, best practices include establishing and maintaining a library of fraud scenarios that are relevant to the organization’s specific industry, its operations, its geographical presence, its asset portfolio, its competitive advantage, etc. Oftentimes, these libraries are established through facilitated, collaborative brainstorming discussions that occur with diverse stakeholders. These stakeholders need to embrace thinking like a fraud perpetrator in order to identify what fraud scheme may occur, who may perpetrate the fraud, when and where the fraud is likely to occur. In order to generate valuable discussion, these stakeholders may need support and education on how to take on the perspective of a fraud perpetrator and why it is important to consider a fraudster’s perspective.

Simply establishing a fraud scenario library is not enough; management must commit the time and resources necessary to maintain the relevancy of the library. With the rapid technological advancements and accumulation of data, maintaining effective fraud risk-management programs and relevant fraud scenario libraries can become cumbersome. Luckily, there are some recent technological advances in data analytics that may further facilitate an organization’s fraud risk-management program.

Harnessing the Power of Emerging Technological AdvancesAccording to Deloitte’s 2017 Information Technology (IT) Trends, the operational model of IT departments is predicted to morph so that IT may further engage with the business and harness the power of cognitive architecture, the alignment of technological configuration to human cognitive physiology. In other words, technological advances are now being leveraged in ways that support more effective and efficient human analysis and decision making. By leveraging cognitive architecture, business leaders will be able to enhance dashboard reporting and decision making.

Vince Walden, one of the Guide’s task force members, spoke during an Institute of Internal Auditors’ St. Louis Chapter event last spring and provided insights into some technical tools that may be leveraged in conjunction with the Guide. Walden explained that technological advances are expanding far beyond the concept of business intelligence and are embarking into self-service data visualization, which is software that analyzes multiple data sources while providing data insights that are understandable to most business leaders. Visualization software is taking data mining and big data to a new level by leveraging neuroscience and heuristic models in order to develop visuals that support faster, broader business analysis.

Some visualization software has streamlined user interfaces that allow business leaders to easily analyze real-time data from a variety of sources, including data stored on company networks and in the Cloud. This analysis goes beyond data and numbers by including other forms of media such as photos, videos, audio and text. Just imagine receiving real-time analysis in a rich, visual format that can easily be incorporated into real-time reporting. These technological enhancements free up business leaders from data analysis programming so that they may focus their energies on finding insights faster and speeding up decision making.

In a modernized world where agility and early recognition of market changes is crucial to survival, the Guide may provide organizational leadership with some additional considerations on how to harness technological advancements in order to further innovation and creative disruption. So while incorporating fraud analysis into all 17 Framework principles may at first seem cumbersome, there appears to be an opportunity to leverage the Guide for enhanced business value that goes beyond the traditional boundaries of internal control. Because organizational leadership often views internal control within the parameters of Sarbanes-Oxley, internal and external auditors are in a unique position to advocate for the Guide’s data analysis recommendations.Kate Turner, a Prosci Certified Change Practitioner, is the director of special projects with Spire in St. Louis. She has served on several MSCPA Committees as well as on the MSCPA Board of Directors. Kate can be contacted at [email protected].

COSO Updates Framework for Technological Advancements Is Your Company Following Suit? By Catherine turner, CPa, CGMa, Cia, CrMa

COSO Updates Framework for Technological Advancements Is Your Company Following Suit? By Catherine turner, CPa, CGMa, Cia, CrMa

14 the Asset | January 2017

peer review changes effective January 1, 2017Deborah Loomis, CPA

The AICPA’s Peer Review Board has approved significant changes to the Peer Review standards, interpretations and other guidance that are effective for peer reviews beginning after Jan. 1,

2017. Below is a summary of the more important changes that accounting and auditing firms should be aware.

HeightenedPeerReviewofaFirm’sSystemofQualityControlPeer reviewers will now complete a vigorous review and assessment of a firm’s system of quality control and its compliance with that system, as part of the peer review process. In the past, firms were permitted to document their systems of quality control using the AICPA’s Quality Control Policies and Procedures Documentation Questionnaires (4300 and 4400 checklists), but beginning in January 2017, the AICPA will no longer provide the 4300 and 4400 checklists, and firms must develop quality control documentation tailored specifically for their firm. To aid firms in developing this documentation and to assist them in laying the groundwork for successful peer reviews, the AICPA has developed the following two tools that firms may use free of charge to develop and maintain their individualized systems of quality control. These tools can be found in the peer review section of the AICPA website (aicpa.org).• Invigorate the Focus on Quality Toolkit. This toolkit

contains numerous checklists and templates starting with a Tone at the Top Action Plan to help firms reinforce the importance of quality at their firm, modernize their client evaluation procedures, establish firm-wide agreed-upon pricing considerations and proposal strategies to demonstrate audit quality as a competitive edge, determine firm-wide competence and understanding of the latest independence rules, and pinpoint any risks in the firm’s practice.

• The AICPA Audit and Accounting Practice Aid—Establishing and Maintaining A System of Quality Control for a CPA Firm’s Accounting and Auditing Practice. This practice aid is designed to help practitioners better develop the policies and procedures that comprise their firm’s system of quality control, as required by QC Section 10, A Firm’s System of Quality Control (AICPA Professional Standards). Two versions of the guide are available—one for sole practitioners and another for small- to medium-sized firms—and both versions contain easily customizable policies and procedures documentation that meet the requirements of the quality control standards and is tailored to the facts and circumstances of the practice size.

ChangestothePeerReviewProcess• Documents to be provided in a System Review—Firms

undergoing a System Review will now be required to provide a copy of the inspection reports for each of the three years subsequent to the prior peer review and any relevant communications about those inspections such as consultant review reports.

• Team captain to conduct closing meeting—The peer review team captain will conduct a closing meeting with the reviewed firm to discuss the preliminary results of the peer review (e.g., matters, findings, deficiencies, significant deficiencies, or non-conforming engagements) identified by the review team.

• Team captain to evaluate firm’s responses prior to exit conference—The review team captain will evaluate, prior to the exit conference, the firm’s responses to any MFC forms, FFC forms, deficiencies, significant deficiencies, or non-conforming engagements.

• Firm representation letters—The new standards call for separate firm representation letters for System Reviews and Engagement Reviews. Firm representation letters for Engagement Reviews should now be dated the same day as the peer review report, similar to a System Review. Reviewed firms should not remove any of the required representations from their letters but may include additional information if deemed appropriate. Some of the required representations are new or have changed so firms should ensure they are using the most up-to-date language as representation letters that do not include all of the required representations will not be accepted and may delay acceptance of the firm’s peer review report.

• Reporting changes—There are some clerical changes to the peer review report including a reorganization of information and headings for select paragraphs.

OtherResourcesAdditional information about the peer review changes can be found on the Peer Review section of AICPA website at aicpa.org, including the meeting materials from the May Peer Review Board meeting where the changes were discussed and approved. Included in the meeting materials is an example timeline (page 173 of the PDF) of when certain procedures should be performed in a peer review that commences after Jan. 1, 2017.Firms are encouraged to direct any questions regarding the revised peer review standards to a member of the AICPA Peer Review Technical Team at (919) 402-4502, option 3.

Deborah Loomis is a sole practitioner in Liberty, Mo., specializing in the audits of small companies and local governments. She is a member of the MSCPA Accounting and Auditing Committee.

ACCounting & AuDiting

the Asset | January 2017 15

It’s Time to Get PaidYou’ve earned it.

Thank you for your prompt payment!

Invoice PaymentPayment Detail

Amount to Pay*

Invoice Number

$500.00

Invoice Number

Cardholder Information

Name

Card Number

Name

Card Number

Month Year Pay Invoice

BY 2019, OVER 75% OF BILLS WILLBE PAID ONLINE.

35%47%

55%

75%EST

2010 2013 2016 2019

You work hard for your clients – why not present them with a simple and

secure way to pay for your services? CPACharge provides your firm with

a convenient, affordable solution for managing credit card and ACH

payments, including the option to pass on the cost of processing fees.

Getting paid for your work should be easy – you’ve earned it!

The payment solution for CPAs.

Professionally accept all major cards.

CPACharge is a registered ISO of Merrick Bank, South Jordan UT

CPACharge.com/mocpa | 844.352.4705

Simple online payments No swipe required No equipment needed

16 the Asset | January 2017

stay present by creating professional nexusBy Zachary M. McDowell, CPA

It’s an interesting concept—nexus. You know the principle of nexus in the tax world: identifying a business’s presence for income and sales tax purposes. It is easy to recognize nexus at a local

business, but the farther away a business grows, the more difficult it becomes. As a business’s activities expand regionally, nationally, or even globally, determining and identifying nexus can become a challenge. A few contributing factors to this challenge include: the rise of online and virtual commerce, intangible property considerations, and residency rules. Through it all though, the concept of nexus really aims to answer one simple question: Are you present?

Just as connectivity or presence powers the heart of businesses, it also drives personal relationships. Taking a step back, I asked myself: Where am I present? Where am I creating nexus? Just like a startup business, as a young professional CPA, I recognize that creating relationships and connections starts right in my local community and will expand over time with an entrepreneurial mindset as my career grows. If you are like me, the desire to connect and grow is strong, and it’s a common trait to many young CPAs today.

At the MSCPA Fall Committee Day in Columbia in September, our new Young Professionals Committee held its inaugural meeting and officially kicked off operations. In broad terms, the new Young Professionals Committee will encourage future CPAs to enter the profession and new CPAs to be actively involved; advise MSCPA staff on specific professional learning and growth opportunities

for young professionals; and facilitate sharing perspective and insights of young professionals among society membership and leadership. We are committed to building a diverse, talented and energetic group to help determine the best ways to support new CPAs in the profession.

Consider, for a moment, your professional nexus. There are many different ways to approach building your network, but everyone’s network has a lifecycle that can compare to a business’ nexus lifecycle:

• Inception. Your connections often begin in your local community with coworkers, family, friends, and local businesses and organizations. These connections represent a training ground for you to hone your personal and business skills while diversifying the types of relationships you build. This is your “brick and mortar” nexus.

• Growth. As you transition from establishing early connections, you expand your network to state and regional channels. You add client interaction, business partnerships, and mentor relations. Deepening or pruning early connections, personal branding, specialization, and work history are all particularly impactful. Think of this phase as your “regional” nexus.

• Sustainability. Connections are often cultivated over many years, and these serve as your core. New connections will include profession and business leaders and subject matter experts. Your sustained network guides you throughout the majority of your career and is similar to nexus of a national or global business—sustained and established.

Recognize that the scope of your professional nexus may be relative to the size of the business you own or work for, but the principles apply similarly to a sole proprietor or a CFO. Regardless of what stage of your career you are in, where you are located, or the size of your network, the challenge is to keep that one question in mind: Are you present?

It is an exciting time to be connected and present with the accounting profession and especially right here in Missouri. The profession is growing, and the CPA credential remains the premier professional designation in the business world today. Stay present!

Zach McDowell is a tax associate at Anders CPAs + Advisors in St. Louis. He serves as chair of the MSCPA Young Professionals Committee. Zach can be contacted at [email protected].

Young ProfeSSionAlS

Zach McDowell, Young Professionals Committee chair, meets with Nick Graff and Jen Vacha at MSCPA’s Fall Committee Day.

the Asset | January 2017 17

Welcome! the Mscpa network continues to grow! the following members joined the society in september and october. please take time to welcome them and invite them to participate in events and programs with you.

neW memBerS

Auxiliary membersKristen Albers KpMG llpDawn AllenBronwen AntosewskiNicole BeneMatthew Bey american railcar industries, inc.Anthony Bhasme deloitte & touche llpMark Blechle ernst & young llpAlexis Bowles Daniel Branco Jennifer Brown cerner corporationJarad Bunte ernst & young llpTaylor Burnett bKd, llpNathan Butler ab search

Victoria Bynum bKd llpCrystal Calvert Marksnelson cpaThomas Carpenter spilker McKeone & nelson, pcKevin Cheng pricewaterhousecoopers llpRobert Chesbro Grant thornton llpJohn Clark Marksnelson cpaJoseph Coday bKd, llpDaniel Condra Mark Conrad pricewaterhousecoopers llpPatrick Cullen Marksnelson cpaRyan Dinyer Daniel Dolan Grant thornton llpelyse Douglas bKd, llp

Timothy Downar ernst & young llpPiper earnshaw Grant thornton llpLucy egan pricewaterhousecoopers llpKristen estrada Molly Farrington deloitte & touche llpDevin Feist ernst & young llpTrevor Focht Grant thornton llpMichael Fowler cole & company pcGrant Gash Wassman cpa services llcAlex Goldberg pricewaterhousecoopers llpMarietta Greene Shuhan Gu ethan Harr pricewaterhousecoopers llpCheryl Hawken evers & company, cpasDaniel Hermsmeier anders cpas + advisorsScott Herring Ryan Hoffman ernst & young llpAlicia Hopkins house park dobratz & Wiebler pcJoshua Hsu ernst & young llpAlyssa Huskins ernst & young llpMeigs Jones ernst & young llp

Jessie Kelly cbiZ MhM llcolivia Kimminau Chelsea Kirkpatrick bKd, llpKevin Kolibas Grant thornton llpKatherine Krska ernst & young llp

Philip Kunz anders cpas + advisorsJeremy Lamb ernst & young llpLuke Longfield KpMG llpMatthew Lueken pricewaterhousecoopers llpJoshua Lukens deloitte & touche llpCagney McDonald anders cpas + advisorsRobert McGuinnessBraden McKee Grant thornton llpCaela McMillon Grant thornton llperic Mendelson pricewaterhousecoopers llpBarrett Meyer Grant thornton, llp Aaron Miller Grant thornton llpNathan Miller KpMG llpPaul Moritz rubinbrown llpParker Moss Grant thornton llpRachel Nieters deloitte & touche llpMelinda Nold randy taylor cpa llcJennifer Patt Laura Powderly pricewaterhousecoopers llpJohn Randall ernst & young llpChristina Rowland conner ash, p.c.Andrew Schulz landmark bank, n.a.Stephanie Sheehan Joseph Starke pricewaterhousecoopers llpNicholas Tinoco Marksnelson cpa

Ryan Toarmina rubinbrown llp

Paul Trenhaile Williams-Keepers llcAudrey Van Deraa the Journey fellowship, inc.Zachary Vaninger rubinbrown llpClaire Vaupel pricewaterhousecoopers llpBrandon Visonnavong pricewaterhousecoopers llpMeghan Watt KpMG llpStephen Werth Marksnelson cpaJeremy Winter elizabeth Yannakakis pricewaterhousecoopers llpJusten Yao KpMG llp

fellow memberscentral chapterDoris Brown, CPA doris d. brown, cpaAshley Dodson, CPA Williams-Keepers llcPaul Moen, CPA Marberry & eagle pc cpa’sAshley Watson, CPA bobby Medlin, cpa

Kansas city chapterLisa Alden, CPA Marksnelson cpaJohn Anderson, CPA ernst & young llpLori Creek, CPA Government employees health association, inc.Teresa Garza, CPA Anthony Mueller, CPA bWtp p.c.Daniel Paschang, CPA cbiZ MhM llcChristine Ritchie, CPA cooperative finance associationConnor Scott, CPA pricewaterhousecoopers llp

Kelsey Shireman, CPA cimarron lumber & supply co.

northwest chapterShelby Brown, CPA

southwest chapterDallas Williams, CPAJereme Zook, CPA Kerber eck & braeckel

st. Louis chapterLisa Bushur, CPA Missouri baptist universityJennifer Chickey, CPA bluesummit consultingSandhya Crasta, CPA Kellwood companyJonathan easterling, CPA cummings, ristau & associates, pcJohn ellis, CPA coughlin, donovan, niehaus & scherle, p.c.David Hinners, CPA Milestone equipment holdingsThomas Hoeferlin, CPA purk & associates, pcTaylor Hutson, CPA rubinbrown llpRodney Krieg, CPA olin corporationMason McDonald, CPA brown smith Wallace, llpJane Pagano, CPA Kiefer bonfanti & co. llpRebecca Piel, CPA botz, deal & company, p.c.Mary Piening parkway central high schoolMatthew Pollock, CPASunny Rennier, CPA brown smith Wallace, llpelizabeth Rocco, CPA ernst & young llpBradley Rotermund, CPA opulence llcRhonda Taylor, CPA bdo usa, llp

18 the Asset | January 2017

P ractitioners frequently receive advice to develop practice niches to enhance their business. Yet, many CPAs remain unsure of how to do so. In reality, building and maintaining niches need not be difficult or costly, and most

practitioners already have one or more in place that just need deeper attention.

Firms that properly create niches are often recognized as authorities in that area, and as a result, experience multi-faceted benefits, including:

• Client acquisition costs decrease. Desirable referrals from clients and other CPAs arise without significant extra effort because the opportunity is readily apparent to the referral source.

• Client retention improves while related costs go down. Clients recognize competitors probably lack the unique knowledge, and they understand the CPA is not just another provider like all the others.

• Price sensitivity drops. Clients usually understand and value an expert’s talent and specialized knowledge. Expertise warrants premium pricing.

• Operating costs decrease. Economies of scale not present under a “whatever walks in the door” approach arise, and firms can focus where they operate most efficiently.

• Vulnerability to changing conditions diminishes. Demand within individual niches often is independent of other specialized practice areas and overall conditions.

Important qualitative advantages also arise. Niches allow CPAs to focus on what they enjoy most, to be more selective of whom they serve, and to manage a firm’s client base instead of allowing it to manage the firm. Perhaps most importantly, it allows CPAs to see that their unique knowledge and skills help clients in ways few other providers could.

Developing Your NicheStill, creating niches need not be complex or expensive. While some firms invest aggressively in marketing and special training to develop new niches quickly, that is far more expensive than organically building them. It’s also riskier because it pushes a solution when a need may not exist and when it is not yet clear whether the marketplace views that firm as an optimal solution.

Organically creating and developing niches via the natural expansion and emphasis of current firm activities and client demographics takes more time. But, it is also less risky and more cost effective because the firm’s customers pull it toward areas where it already has core competency, reputation and interest.

Under either approach, certain steps help immensely by reinforcing to clients and others your knowledge and expertise, even though they may not bring in new clients, including:

• Strategic repetition. Mention niches at every opportunity in conversations with referral sources, colleagues, and clients (both in and out of the niche); via the firm’s website; in presentations and speeches;

practice niches increase energy and profitability By JosePh t. eCKelKaMP, CPa

“Begin with the end in mind.”—Stephen Covey

the Asset | January 2017 19

practice niches increase energy and profitability By JosePh t. eCKelKaMP, CPa

and in media interactions. Frequently reinforcing a niche’s importance leads more people to refer prospects to the firm.

• Celebrate even small victories with your team to reinforce staff enthusiasm. For example, track niche client-count milestones and niche revenue. What gets measured gets done!

• Serve as an active resource for other CPAs, particularly for niches in areas most firms don’t see a lot of, or other firms prefer not to handle.

• Be a friend to the media. Press releases establish someone as a “go to” person on a topic.

• Get involved in trade groups related to the niche, and be visible.

Defining Your NicheEach firm, subjectively and in differing ways, must identify its most desirable and impactful niche(s). Definitions also should be specific enough to be understandable and allow differentiation. “Serving non-profit organizations” is likely not specific enough (unless that is all the firm does) while “auditing non-profits not requiring A-133 audits” is. Similarly, “serving small businesses” is likely too broad, but “providing tax and accounting services to privately-owned businesses with fewer than 100 employees” works.

Niche definitions must reflect how the firm views current and desired client populations. As Stephen Covey said, “Begin with the end in mind,” and ask these questions:

• What common attributes do our best clients share, and what groups of similar clients exist? Start by sorting the client list several ways, such as:

- Revenue for several years (descending order);

- Client longevity;

- Industry, ownership, geography;

- Services clients use or may use in the near future; and

- Combinations of these attributes (e.g., audits, but only for non-profit organizations).

• What do we do best? Does that match what we enjoy doing?

• Can we, and how would we, serve clients if we develop those niches further?

• What timeframe is possible, and what tools are needed to make the niches profitable?

• Do we have the right people to lead the effort, and do they have the interest?

This last attribute is perhaps the most important for success. Growing niches organically requires an enthusiastic advocate to continuously seek opportunities, represent the firm publicly, and measure outcomes.

Current and potential competition is another consideration. Does significant competition exist within the defined segment? Is there likely to be? For example, a large regional firm is unlikely to affect a small, local firm. A corollary is: if little competition exists, why? Is it a narrow niche; do most firms not do enough of it to be proficient, or is it unprofitable (or hard to get paid)?

Because definitions often evolve, ongoing re-evaluation and regularly re-assessing long-term viability of niches chosen are essential. For example, will the segment likely grow or contract? When hospital systems are acquiring medical practices, building a broad medical practice niche may be unwise, while an optometrist practice may thrive. However, remember that being the last buggy whip manufacturer or being ready when demand returns (e.g., hospitals begin spinning off medical practices) can be highly profitable.

In ConclusionIn proactively managing CPA firms, periodically evaluating whether to develop current niches further or create new ones and, if so, how to do so, is prudent. Niches provide qualitative and economic advantages and do not need to be expensive or difficult to develop. While niches aren’t the only path to success, they are an important consideration in enhancing profitability, reducing economic risk, or both.Joe Eckelkamp is an MSCPA member and the owner of The E&A CFO Group in St. Louis. He can be reached at [email protected].

20the Asset | January 2017

SOCIETYSPOTlIgHT

Join the Conversation at PubliC PraCtiCe strategiC roundtablesPrepare for tax season and debrief afterward at peer-led, discussion-based roundtables, hosted by the MSCPA’s Firm Leadership Committee. You’ll gather with CPAs from across the state to assess critical challenges and exchange ideas for practical solutions that you can implement at your firm.

upcoming roundtables: Jan. 13 and May 5 8:30 a.m. to 3 p.m. MSCPA St. Louis Learning Center

Register today at mocpa.org/roundtables!

let the MsCPa helP You seleCt the right CYber seCuritY insuranCe Plan to Fit Your needsIt’s nearly impossible to turn on the news without hearing at least one story about cyber hacking. Every system upgrade, remote device, and incoming email can mean a new risk to you and your client’s data. In fact, since 2008, more than 1.1 billion data records from U.S. businesses and organizations of all types and sizes have been compromised, including those containing customers’ private information and companies’ financials.

Given that one system hack can effectively shut down an organization, many firms and companies are taking measures to ensure they are equipped to handle a cyber attack should one occur. The MSCPA has several comprehensive and customizable cyber risk management insurance plans to meet the needs of your organization. Contact Pete Shea at (800) 264-7966, ext. 121, or [email protected] to find the best solution to cover all of your cyber exposures.

utilize the MsCPa legislator’s tax guideThe 2016 Legislator’s Tax Guide will be available at mocpa.org/legislators-tax-guide by mid-January. The guide offers helpful information on unique tax situations for state legislators and also includes examples on claiming meal and travel deductions. If a state legislator is among your clients or potential clients, this guide will help you help them!

need Part-tiMe tax assistanCe? looking For seasonal Work?If your firm needs part-time help during the upcoming busy season, place your opportunities for FREE on the MSCPA Career Center! Your postings will be promoted to MSCPA’s 8,000 members throughout Missouri. Interested applicants will then apply directly to your opening online. To post your complimentary ad today, visit mocpa.org/career-center. Likewise, if you are seeking seasonal employment, be sure to check out these and other great opportunities.

keeP uP With Current tax develoPMentsTune into a weekly video series, featuring Ed Zollars, CPA, with Nichols Patrick CPE, Incorporated, discussing recent federal tax developments. Recent topics have included:

• Farm expenses deducted in two consecutive years— and the Tax Court is fine with it;

• Franchisee group denied tax exempt status;• Early copy of payroll tax withholding tables

released; and• Congress grants some relief for insurance

reimbursement arrangements.Check out the latest video on the MSCPA’s home page at mocpa.org.

the Asset | January 2017 21

Today’s CPA is positioned to offer far more than financial and tax services. As a trusted advisor, you are the first source for most business questions — and that can include HR. Consider delivering strategic and client-valued advice, such as how to:

• Attract and retain talented employees

• Enhance workforce productivity

• Ensure proper classification of workers

Clients crave strategic advice. Together, let’s exceed their expectations.

Be your clients’ first source for

HR SUPPORT.

Participate in the FREE Paychex Partner Program! CPA.com/Contact-Paychex

21249-CAP

Paychex is a proud partner of the MSCPA

22 the Asset | January 2017

Eight Rules for Effective Technology Management By JiM BooMer, CPa, CitP, MBa

The ongoing war for talent, coupled with the rapid advancement of technology, is fueling exponential growth in the importance of technology. It creates a challenge and an opportunity. From the challenge side, you are already

likely forced to do more with less while increasing production to counter the persistent rise in costs. On the flip side, technology allows you to automate many of the manual tasks that would have increased headcount in the past while also providing better client service. Focusing on the right processes and technology to serve the right clients is critical to your company’s success and future readiness.

These eight rules of technology management will help your organization develop a technology strategy that is aligned with overarching company strategy and set you up for success today and into the future.

1. View technology as a strategic assetWhen companies manage technology as overhead, they usually experience frustration as expectations are always greater than the results based upon the resources committed. The better approach is to manage technology strategically, and allocate resources by priorities. Technology is an accelerator for planning, people and processes.

2. Invest in your technology leaderDon’t expect to get extraordinary results if you are not willing to invest in technology leadership. Too often, firms insist on hiring someone who knows accounting to manage their technology and many times they want a CPA. They end up with a person who knows a little about accounting and little about technology but is an expert in neither.

3. Expect technology to change and require ongoing investmentTechnology change is occurring more rapidly than ever before. To keep up, organizations must invest more in process improvement and training. If you simply invest in maintenance projects (keep the lights on) rather than innovation (move the firm forward), you’ll end up spending more to catch up in the long run than you would to stay ahead of the curve. Successful firms spend approximately 6 to 7 percent of net revenue annually for technology and support, including labor and bandwidth.

4. Invest in training at all levelsThe best way to increase your return on investment in technology and people is through training. It is also key to both retention and attraction of top talent. The Boomer Technology Circle™ metrics of member firms show that revenue per full-time equivalent increases considerably in firms with excellent training programs. The attitude and confidence level in those firms also exceeds those of peer firms.

5. Join a peer networkJoining a peer network offers access to experience, expertise and personal development outside of your company. You don’t have to reinvent the wheel. Peer groups provide insight, new perspectives, research and development, benchmarking and confidence that can save your organization time and money. Firms cannot operate in a vacuum, and the value of trusted, vetted peers to call on is priceless. Developing a network of peers and utilizing that network is a professional strength and competitive advantage. After all, it’s what you don’t know you don’t know that costs you a lot of time and money.

22 the Asset | January 2017

the Asset | January 2017 23

6. Commit to a process for managing technologyOther than the cost of labor, technology is the second largest expenditure in most CPA firms. It only makes sense to adopt sound management practices in order to ensure a return on the technology investment. There are several components to an effective management system. It comes down to people, planning and processes with technology acting as the accelerator.

7. Assign a leader to focus on technologyTechnology leadership and vision are an integral part of today’s firm management team. The requirements for a CIO or technology partner are similar to those of a managing partner. The skills include leadership, finance, marketing, human resources, business savvy, project management and technical skills. IT must have a seat at the management table if the firm expects to remain successful and future ready.

8. Operate from a written technology planFollow the planning advice you give clients. Firms should operate from a technology plan that integrates with overall firm vision and strategy. If you don’t have these plans in place, invest the resources and get them in place. Without a plan, it is easy for firms to lose focus on the most important and highest impact projects and strategies.

Value is added when you provide leadership, relationship and creativity. Leadership provides direction, relationship provides confidence and creativity provides new capabilities. All are necessary to effectively manage technology and your business.Jim Boomer is the CEO at Boomer Consulting, Inc. He is also the director of the Boomer Technology Circles and serves as a strategic planning and technology consultant and adviser to CPA firms across the country. Jim can be contacted at [email protected].

Master of Science

FORENSICACCOUNTING

In today’s global landscape, forensic accountants play key roles in tackling foreign and domestic terrorism, fraud and organized crime.

Are you ready to prepare for a career as a professional forensic accountant?

In as little as 18 months, Webster University’s Master of Science in Forensic Accounting can prepare you to do more than simply uncover white-collar crime. A flexible evening format is offered to meet the needs of the working adult.

Classes are forming now! APPLY TODAY!

For more information: webster.edu/forensic-accounting

EC-3080 Web U_1/2 pg Asset.indd 1 12/6/16 3:03 PM

the Asset | January 2017 23

24the Asset | January 2017

100% Mscpa Membership congratulations and thank you to these companies for having 100 percent* of their cpas as Mscpa members! Join these companies that support the cpa profession and Mscpa by enrolling 100 percent of your cpas in Mscpa membership today!

Abacus CPAs LLC Branson, Lee’s Summit & SpringfieldAbbott & Angerer CPAs LLC Jefferson CityAbeles and Hoffman, P.C.St. Louis Advanced Tax Strategies, PC St. LouisAmerican Railcar Industries, Inc.St. CharlesAnders CPAs + AdvisorsSt. Louis Baker, Davis, Roderique CPAsJoplinBates CPAs, P.C.St. CharlesBauers, Hawkins, o’Sadnick & CompanySt. PetersBDo USA, LLPClayton Beard-Boehmer & Associates PCColumbia Becker & Rosen, CPAs, LLCClayton Begley, Young, Unterreiner & White, LLCCape Girardeau Bender & Company CPAs, P.C.St. Louis Beussink, Hey, & Roe, P.C.Cape GirardeauBeyer, Hippe & Michael, P.C.Brentwood BKD, LLPBranson, Joplin, Springfield & St. Louis Botz, Deal & Company, P.C.St. Charles Boyd, Franz & Stephans, LLPSt. LouisBrian G. Toennies & Associates, P.C.St. Louis Brown Smith Wallace, LLPSt. Louis & St. CharlesBuchheit Inc.Perryville