Textile Services in Europe - IndustriALL · Contents Part I: Economic environments of industrial...

43

Final Report November 2016 Study funded with the support of the European Commission Textile Services in Europe

Transcript of Textile Services in Europe - IndustriALL · Contents Part I: Economic environments of industrial...

Final Report

November 2016

Study funded with the support of the European Commission

Textile Services in Europe

Contents

Part I: Economic environments of industrial laundry in Europe 3

Characteristics 4

Industrial laundry: the reasons for success 12

Linen rental market in Europe: state of the sector between 2000 and 2012 16

Part II: Stakes for the sector 26

Part III: Comparison of the various sector stakeholders 39

Textile Services in Europe November 2016 2

Part I: Economic environments of industrial laundry in Europe

Textile Services in Europe November 2016 3

Characteristics

Textile Services in Europe November 2016 4

Customers have two choices when it comes to managing their linen: They can own their linen or rent it from a company

Source: Deloitte study for ETSA, June 2014

Textile services market

Customers

own their linen

Laundry done on the site where

the owner works

Laundry done at home by

the owner

Laundry outsourced to a laundry service

Customers rent their linen from a linen rental

company

Laundry outsourced

to a linen rental company

Linen rental and maintenance is a “full” and “complete” service that takes care of textile-related matters enabling customers to have a disciplined management of their textile budget: the relationship between the company and the customer is formalised by a rental agreement; the customer that rents out linen, invests in a stock of linen and other textile items and undertakes to manage the needs of each customer.

Textile Services in Europe November 2016 5

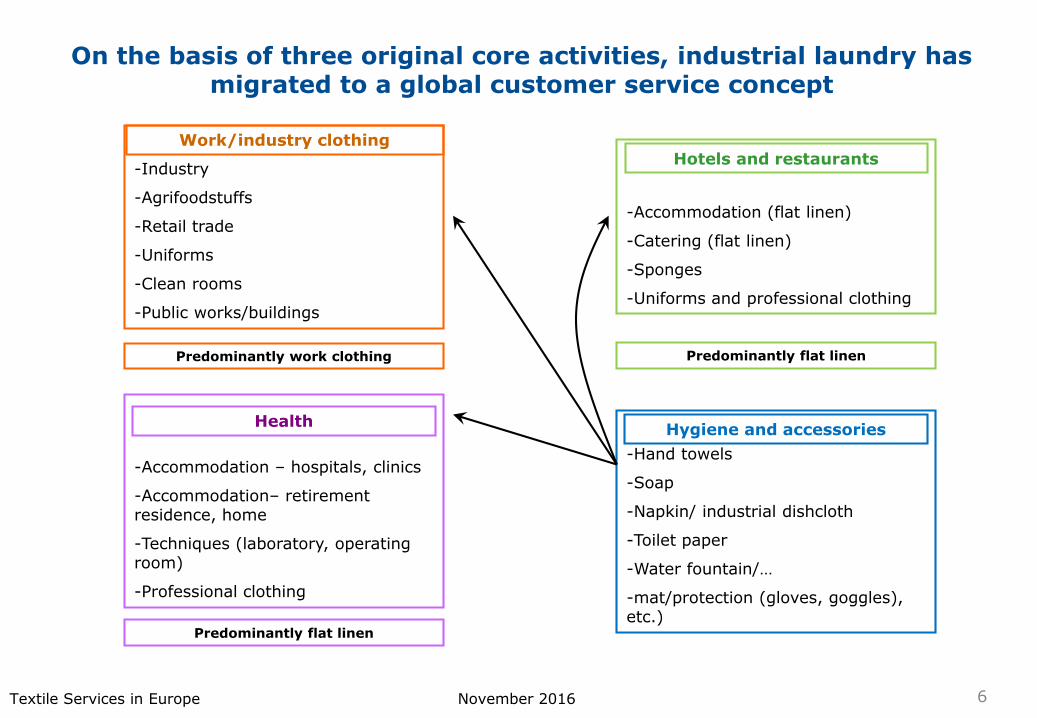

On the basis of three original core activities, industrial laundry has migrated to a global customer service concept

-Industry

-Agrifoodstuffs

-Retail trade

-Uniforms

-Clean rooms

-Public works/buildings

Work/industry clothing

-Accommodation (flat linen)

-Catering (flat linen)

-Sponges

-Uniforms and professional clothing

Hotels and restaurants

-Accommodation – hospitals, clinics

-Accommodation– retirement residence, home

-Techniques (laboratory, operating room)

-Professional clothing

Health

-Hand towels

-Soap

-Napkin/ industrial dishcloth

-Toilet paper

-Water fountain/…

-mat/protection (gloves, goggles), etc.)

Hygiene and accessories

Predominantly work clothing Predominantly flat linen

Predominantly flat linen

Textile Services in Europe November 2016 6

These laundry/dry cleaning segments consist mainly of five “customer” business lines

Healthcare institutions

Hotel industry

Industry Administrative and municipal

authorities

Catering

Clinics, hospitals, retirementhomes; whether for “flatlinen” (sheets, napkins, etc.),clothing for patients andstaff, or the supply ofsterilised linen (operatingroom, for instance), healthinstitutions are significantconsumers of linen rental andmaintenance.

The catering industryconcerns concurrentlythe wholesale laundryand linen rental-maintenance subsectors.Catering also includescollective catering incompanies andeducational institutions(schools, crèches, etc.),collective catering andtraditional catering.

Particularly through theneed for professionalclothing and relatedservices (hand towels,napkins, etc.)

Also constitute a non-negligible outlet(uniforms, etc.)

The hotel industry is aconstant outlet givenguest turnover in hotels,particularly in touristareas (with highseasonal incidence)

Textile Services in Europe November 2016 7

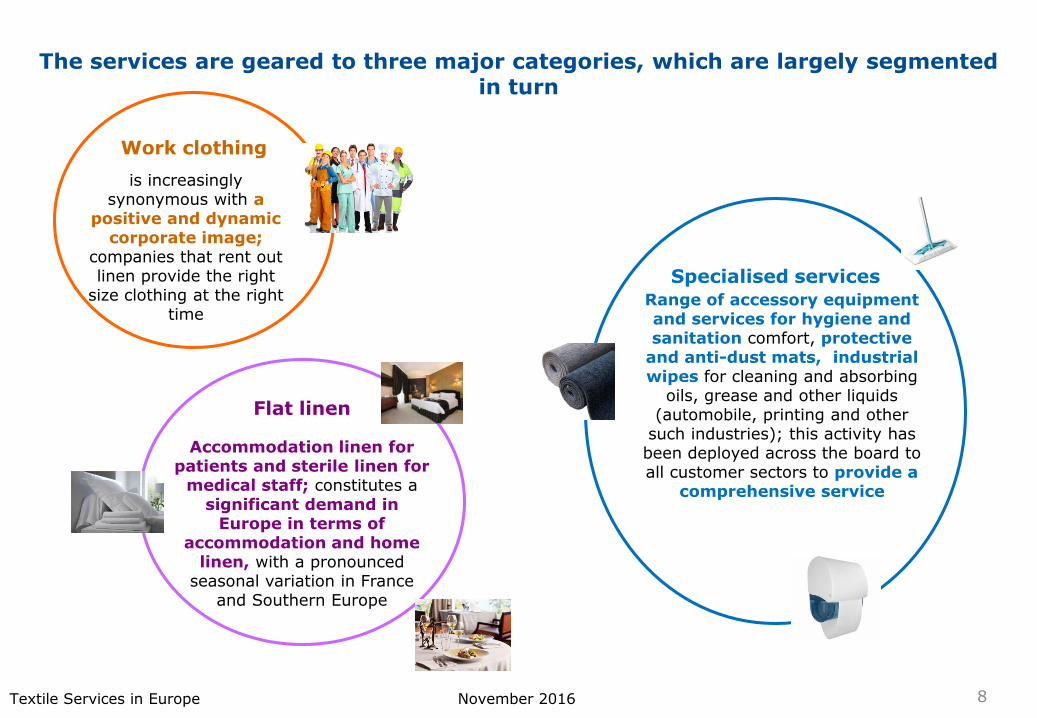

The services are geared to three major categories, which are largely segmented in turn

Work clothing

is increasingly synonymous with a

positive and dynamic corporate image;

companies that rent out linen provide the right

size clothing at the right time

Flat linen

Accommodation linen for patients and sterile linen for

medical staff; constitutes a significant demand in

Europe in terms of accommodation and home

linen, with a pronounced seasonal variation in France

and Southern Europe

Specialised servicesRange of accessory equipment and services for hygiene and sanitation comfort, protective

and anti-dust mats, industrial wipes for cleaning and absorbing

oils, grease and other liquids (automobile, printing and other

such industries); this activity has been deployed across the board to all customer sectors to provide a

comprehensive service

Textile Services in Europe November 2016 8

The services and items provided by a linen rental company are diverse, varied and very complete for a comprehensive service

Linen rental-maintenance companies provide various services to their customers, including:

o Textile articles and accessory items;o Clothing to measure, if necessaryo Industrial cleaning of the items used, ironing, drying or the finishing and appropriate or planned

presentation for each itemo Repairs of articles if necessaryo Automatic replacement of articles that are no longer in an appropriate state for their useo Wrapping and packagingo Transport of articles from the company to the customer’s place of use and collection from the indicated

addresseso Where necessary, distribution of clothes to the workstations at the user and other additional services to

improve overall customer service

Various articles are provided in these companies:

o Clothes that project an institutional image, particularly for service companieso “Ultra-clean” professional clothes for sensitive sectors (fine chemistry, etc.)o High performance Personal Protective Equipment (PPE) for safety and protection against occupational

risks (night visibility, acid projection, protection against fire and heat, etc.)o Traditional work clothing for industrial production siteso Accommodation clothing for patients and clothing for healthcare staffo Sterile linen for surgical operationso Accommodation linen for retirement homeso Accommodation linen for hotels and linen for restaurantso Hygiene services for sanitary facilities: hand towels, soap dispensers, air fresheners, feminine hygiene,

toilet bowl protection, etc.o Anti-dust protective mats for buildings, offices or industrial siteso Resistant industrial wipeso Protective accessories (gloves, shoes, goggles, etc.)

Textile Services in Europe November 2016 9

Industrial laundry services are correlated to the number of inhabitants, economic development and level of industrialisation of the country: Germany dominates the

European market (1)

Some 5 500 industrial laundry production units have been identified in Western Europe and theUnited States: most of them are located in Germany and the United States

18 500 industrial laundry production units have been identified in Eastern Europe and Asia: mostof them are located in China

It seems clear, therefore that the number of industrial laundries is correlated to the number ofinhabitants, to economic development, and the country’s level of industrialisation

There are ca. 24 000 industrial laundry production units in the world– this figure comprises only plants with a production exceeding 15 tonnes per week – which treat ca. 33million tonnes of textiles per year

To this are added 65 000 professionals specialised in cleaning/linen rental that process fewer than15 tonnes per week, which represents ca. 21 million tonnes of textiles per year; there is also a largenumber of very small companies that are not counted.

The concentration phenomenon witnessed in recent years in the sector has resulted in the twobiggest industrial laundry groups in Europe controlling more than 70 production sites, whereasthe 13 other groups of the sector do not exceed more than 10 sites each.

The largest group in the United States has more than 400 production sites, whereas most of theother laundry companies do not have more than 10.

Source: Laundry Operations, Steen Sogaard, Laundry Logics, 2014

Textile Services in Europe November 2016 10

The services provided by industrial laundry are correlated to the number of inhabitants, to economic development and to the industrialisation level

of the countries: Germany dominates the European market (2)

China, with 1.351 billion inhabitants, does not appear in the graph

Textile Services in Europe November 2016 11

32%

30%

10%

8%

7%

6%

2%2% 1%1%

1%

Distribution of sales (in volume) by industrial laundry in Europe

USA

Germany

United

Kingdom

France

Italy

Spain

Netherlands

Sweden

Denmark

Norway

Finland

80%

8%

5%

4%

3%

Distribution of sales (in volume) by industriallaundry in the East and Asia

China

Japan

MiddleEast

FarEast

EasternEurope

317

127

8166 63 61

47

17 9 6 5 5

Number of inhabitants (in million) per country

Industrial laundry: reasons for success

Textile Services in Europe November 2016 12

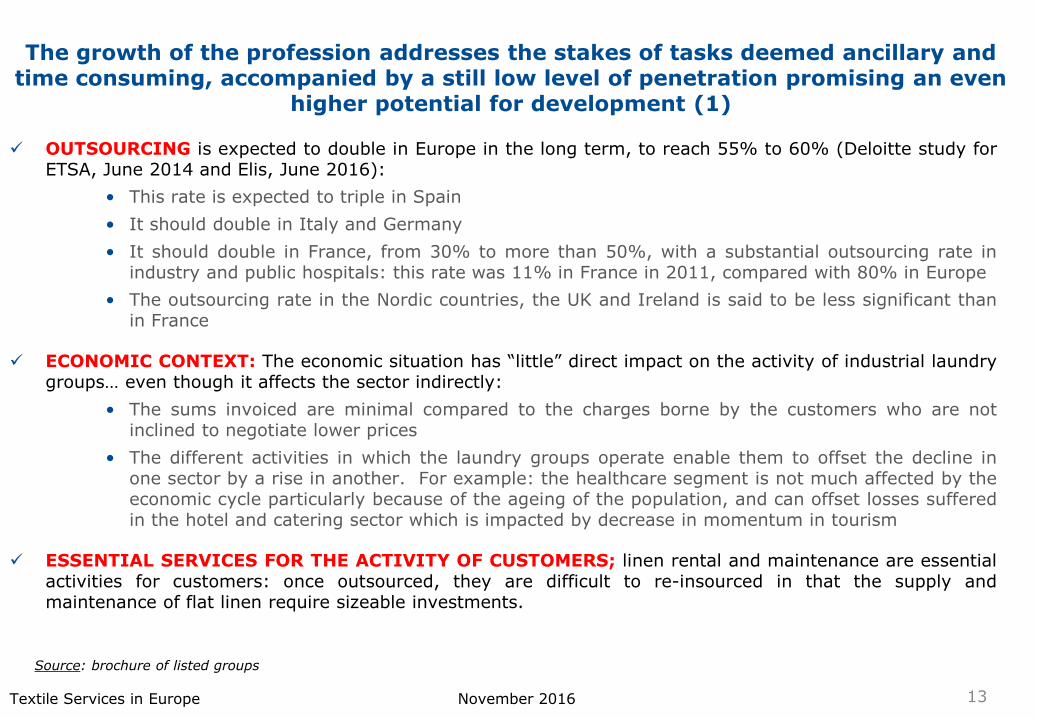

The growth of the profession addresses the stakes of tasks deemed ancillary and time consuming, accompanied by a still low level of penetration promising an even

higher potential for development (1)

OUTSOURCING is expected to double in Europe in the long term, to reach 55% to 60% (Deloitte study forETSA, June 2014 and Elis, June 2016):

• This rate is expected to triple in Spain

• It should double in Italy and Germany

• It should double in France, from 30% to more than 50%, with a substantial outsourcing rate inindustry and public hospitals: this rate was 11% in France in 2011, compared with 80% in Europe

• The outsourcing rate in the Nordic countries, the UK and Ireland is said to be less significant thanin France

ECONOMIC CONTEXT: The economic situation has “little” direct impact on the activity of industrial laundrygroups… even though it affects the sector indirectly:

• The sums invoiced are minimal compared to the charges borne by the customers who are notinclined to negotiate lower prices

• The different activities in which the laundry groups operate enable them to offset the decline inone sector by a rise in another. For example: the healthcare segment is not much affected by theeconomic cycle particularly because of the ageing of the population, and can offset losses sufferedin the hotel and catering sector which is impacted by decrease in momentum in tourism

ESSENTIAL SERVICES FOR THE ACTIVITY OF CUSTOMERS; linen rental and maintenance are essentialactivities for customers: once outsourced, they are difficult to re-insourced in that the supply andmaintenance of flat linen require sizeable investments.

Source: brochure of listed groups

Textile Services in Europe November 2016 13

The growth of the profession addresses the stakes of tasks deemed ancillary and time consuming, accompanied by a still low level of penetration promising an even

higher potential for development (2)

Textile Services in Europe November 2016 14

Source : Elis reference document 2015

35%

30%

15%

80%

50%

35% 50%

Flat linen

Work clothing

Hygiene/Well-being

Outsourcing rate and potential of the rental/maintenance marketfor flat linen, work clothing and hygiene/well-being equipment

in Europe in 2013

Outsourcing rate

Potential

Mat potential

Sanitary potential

Various factors are taken into account by companies when they decide to outsource linen maintenance: these factors seem unquestionably to follow the

“way of the world”

Concentration on the core activity

Reduction of fixed costs and better expenditure management

Simplification of human resources management

Allocation of the occupied space to another activity

Hygiene, cleanliness and safety of work clothing

Better quality textile management

Improvement of the corporate image

Compliance with sustainable development commitments

Traceability of work clothing

Source: brochure of listed groups

Textile Services in Europe November 2016 15

Linen rental market in Europe: state of the sector between 2000 and 2012

Textile Services in Europe November 2016 16

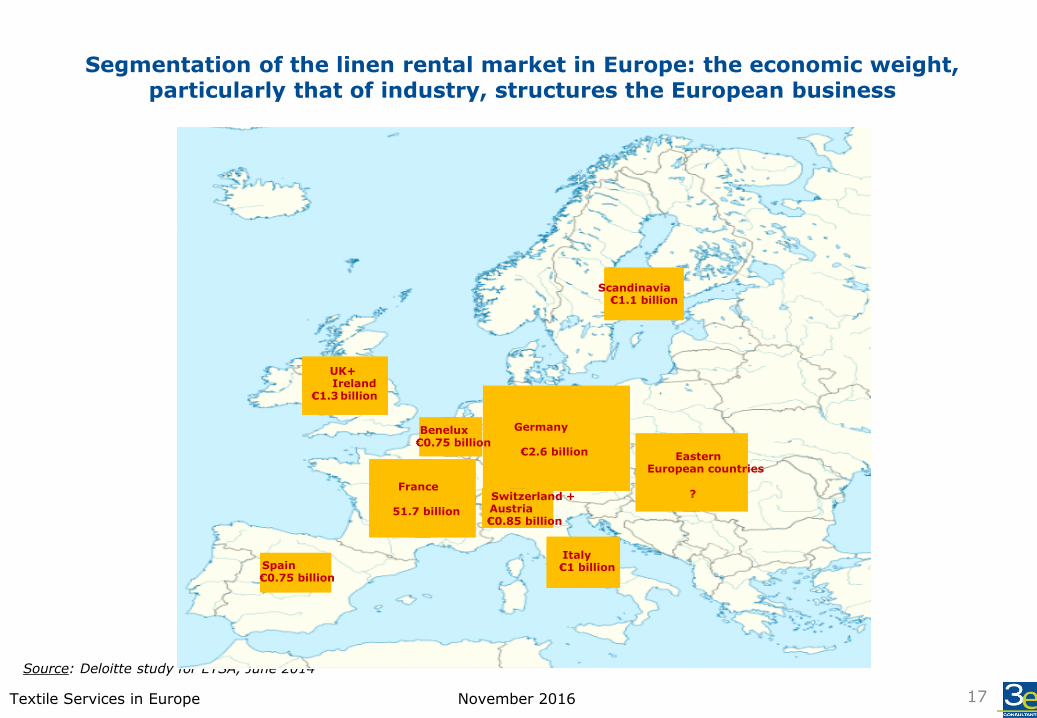

Segmentation of the linen rental market in Europe: the economic weight, particularly that of industry, structures the European business

Source: Deloitte study for ETSA, June 2014

Textile Services in Europe November 2016 17

Scandinavia€1.1 billion

Germany

€2.6 billion

France

51.7 billion

UK+Ireland

€1.3 billion

Switzerland +Austria€0.85 billion

Italy€1 billion

Benelux€0.75 billion

EasternEuropean countries

?

Spain€0.75 billion

The growth rate of the linen rental market in Europe slowed down after the 2009 crisis, but remains positive on the whole: situations vary widely per market,

however (economic cycle, economy of the country, etc.)

Textile Services in Europe November 2016 18

1.92.9

3.6

1.9

3.0

3.5

1.5

2.0

2.1

1.4

1.7

1.3

2000 2007 2012

Development of sales per geographic area in € billion in the linen rental and maintenancesector

Germany/Austria/Switzerland France/Italy/Spain/Portugal/Greece/Cyprus/Malta Sandinavia/Finland/Benelux UK/Ireland

€6.7 billion

€9.9 billion

€11.0 billion

+ 47.8%

+ 11.1%

The activity is dominated by the industry and services per type of customers, whereas flat linen is the 1st product in terms of market shares according to the type

of customers and performance

Source: Deloitte study for ETSA, June 2014

Textile Services in Europe November 2016 19

Development of the linen rental market in Europe

per type of customers

Turnover var. Market shares

2008/2012 2012

ITH* + 4.0% 30%

Healthcare + 1.7% 23%

Hotels + 1.1% 20%

Restaurants + 1.1% 5%

Other nc 22%

*Industry, Trade, Healthcare

Development of the linen rental market in Europe

per type of services

Turnover var Market shares

2008/2012 2012

Flat linen + 2.1% 41%

Work clothing + 3.8% 34%

Hygiene - 0.3% 12%

Anti-dust mat + 3.3% 10%

Clean room + 7.5% 3%

30%

23%

20%

5%

22%

Linen rental

Market in

2012

10.5 billion €

Industry,

Trade,Services

Other

Hotel trade

Catering

Healthcare institutions

41%

34%

12%

10%3%

Linen rental

market in

2012

€10.5 billion

Flat linenHygiene

Mats

Work

Clothing

Clean

Room

Source: Deloitte study for ETSA, June 2014

The different types of customers on the linen rental market in Europe attest to the slowdown in growth after the quite euphoric 2000 decade for

the sector

Textile Services in Europe November 2016 20

Characteristics of products on the linen rental market in Europe

Type of products Market size

Annual

Growth between

2008 and 2012

Growth

PotentialMarket segments

Industry

Trade,

Services

Healthcare

Institutions

Other

Hotel trade

Catering

€3.2 - 3.5

billion

€2.4 - 2.7

billion

€2.3 - 2.5

billion

€2.1 - 2.3

billion

€0.5

billion

4.0 %

1.7 %

nc

1.1 %

1.1 %

Favourable: :The outsourcing of this

service by companies

must continue

There is a great deal ofgrowth potential in France and in Eastern

Europe where the marketis not very developed

at present

Easterne Europe is a abuoyant market:

The hotel industry is growing

there and the linen rentalmarket is not capitalised on

yet

This market is highlycontested in the Southbetween competitors,

particularly concerningpaper products

Flat linen, industrial linen, work clothing, maintenance

linen

Flat linen, work clothingAnd sterilised linen

Toilet linen, mats,Maintenance linen

Flat Linen and workclothing

Flat Linen and workClothing

Source: Deloitte study for ETSA, June 2014c

The different types of services on the linen rental market in Europe: flat linen has greater potential but also remains the least profitable

Textile Services in Europe November 2016 21

Characteristics of services provided by the linen rental market in Europe

Type of customers Market size

Annual growth

between

2008 and 2012

Growth potential

Market segments

7.5 %€0.35

billion

nc

- 0.3 %€1.3 - 1.4

billion

3.8 %€3.5 - 3.8

billion

Bedspreads- ,, , sheets, pillowcases, blankets,

Napkins, curtains, tablecloths,

etc.

nc€4.3 - 4.9

billionFlat linen

Work clothing

Hygiene

Mats

Clean

Room

€1 billion

In recent years, growthin flat linen has beenlimited by

pricing pressure and thethe high rate of

outsourcing in hotels

This type of product isnot considered a premiumservice in the EU.

Strong competition from cheaper alternatives.

Good penetration forimportant customers.

Small markets are

difficult to capture becausethey do not have a largequantity of clothes towash.

The major part of growthfor this type of productsis driven by specialised

companies in this sector

Work clothing, service clothing.

Napkins, Hand towelsfemale hygiene, toilet

paper, dispensers.

Products for washing floors

Dust remover, aerosol sprays

This type of market is highly correlated to the

climate. There is growth

potential in EasternEurope

Linge plat

Vêtements de travail

Hygiène

Tapis

Produits d'entretien

100%

150%

200%

250%

300%

350%

0% 10% 20% 30% 40% 50%

Part du chiffre d'affaires en 2012

Pote

nti

el d

e c

rois

san

ce à

20

17

Growth potential per services and market segmentation

Source: Deloitte study for ETSA, June 2014

Lucrative activity that mobiliseslittle capital

Sizeable potential but less lucrative

than clothing

Lucrative activity,particularly for

technical products

Textile Services in Europe November 2016 22

The linen rental business in Europe is concentrated mainly in Germany, France, the United Kingdom/Iceland and Scandinavia/Finland:

the growth hypothesis at the time appears optimistic because they are based on an opening of the penetration rate that has yet to materialise

The study conducted by the European Textile Services Association (ETSA) made it possible to measure thegrowth potential of the linen rental market in Europe by 2017 per different geographic areas.

Two scenarios were considered:

Conservative scenario: The total turnover generated by linen rental companies in Europe wouldattain €21.5 to €26 billion, i.e. a doubling of sales.

Optimistic scenario: The turnover would register phenomenal growth to attain €36 to €46 billion inthe sector, i.e. x 2.7 compared with 2012.

Source: Deloitte study for ETSA, June 2014

?????Very ambitious, not materialised

Textile Services in Europe November 2016 23

Growth potential in the linen rental market in

Europe by 2017

Conservative Optimistic

scenario scenario

Germany 2.70 5.90 9.50

France 1.75 3.25 6.00

UK/Ireland 1.30 2.15 3.75

Scandinavia/Finland 1.15 1.95 3.45

Italy 1.03 2.50 5.75

Austria/Switzerland 0.85 1.70 3.00

Spain 0.59 1.70 3.00

Benelux 0.98 1.65 2.85

Portugal/Greece/Cyprus/Malta 0.14 0.55 0.75

Other countries 0.53 2.40 3.95

Total 11.00 23.75 42.00

In € billion 2012

25%

16%

12%10%

9%

8%

5%

9%

1%

5%

Distribution, per geographic region, of turnover generatedin 2012 on the linen rental market in Europe

Germany

France

UK/Ireland

Scandinavia / Finland

Italy

Austria/Switzerland

Spain

Benelux

Portugal/Greece/Cyprus Malta

other countries

The turnover generated in the linen rental sector in Europe should have been multiplied by two from 1994 to 2017 according to the scenario deemed

“conservative” by Deloitte; in hindsight, the study commissioned by ETSA appears very optimistic to say the least due to a penetration rate which knows no upward

break in the trend

Source: Deloitte study for ETSA, June 2014

“Enormous” market potential regarding the penetration rate which ultimately remains very stable

establishing the growth conclusions of the study

Textile Services in Europe November 2016 24

119%86%

65% 70%

144%100%

189%

69%

300%

116%

252% 243%

188% 200%

461%

253%

411%

192%

445%

282%

Growth prospects in the linen rental market per country by 2017

Var. 2012/2017 conservative scenario Var. 2012/2017 optimistic scenario

Linge plat

Vêtements de travail

Hygiène

Tapis

Salle blanche

30%

40%

50%

60%

70%

80%

90%

100%

110%

10% 20% 30% 40% 50% 60% 70%

Taux et potentiel d'externalisation du service de blanchiserie en Europe par

produits

La taille des bulles est proportionnelle au chiffre d'affaires réalisé dans chaque produit en Europe en 2012

Taux d'externalisation en 2013

Pote

nti

el d

'exte

rn

alisati

on

The flat linen and clean room services could benefit from higher potential; all “optimistic” hypotheses must at least be projected in the long term (1)

Source: Deloitte study for ETSA - June 2014; Elis AMF basic document – October 2014

Higher potential sustained by the professionalisation of the purchasing

process in hospitals, hotels and restaurants, but there are inter-hospital

regrouping risks

Still has a sizeable margin of manoeuvrability but difficulty in

reaching small companies

Attractive for thegroups by

competition from cleaning companies

Increasingly more stringent regulations militating for nearly total outsourcing

Textile Services in Europe November 2016 25

Part II: Stakes for the sector

Textile Services in Europe November 2016 26

The textile rental and maintenance sector was very dynamic but was hit by the 2009 crisis; whereas the fundamentals and the potential are undeniable and

confirmed by the 2010 recovery, its powerful upswing has been slowed down in the very least

Industrial laundries have adapted their structures to turn more to the customer, and they have thusmanaged to increase the number of potential customers; they used to be more oriented to their internalprocess.

Companies in the sector have made enormous efforts concerning sustainable development; ETSA studieshave compared the consumption of resources linked to the washing of professional clothing over ten years,from 2001 to 2011:o Electricity consumption during this period has gone down by 20%o Water consumption has gone down by 24%o Oil and gas consumption has gone down by 34%

The outsourcing of the laundry service by companies has been generalised in recent years:operators prefer to focus on their core activity to optimise their efficiency;greater reliance on textile services tends to increase with the standard of living; however, thisgrowth market no longer reflects dynamism

Requirements and regulations have been tightened on certain segments, particularly on the medicalmarkets.

Companies that have had recourse to these services are attaching more and more importance totheir image: clean, carefully ironed uniforms, etc.

Conversely, the economic cycle is unquestionably weighing heavily on dynamism, slowing down theprofession – a situation that is more pronounced in countries where growth “is slipping.”

Textile Services in Europe November 2016 27

The market was impacted by the 2009 crisis, less by a downturn, than by a break in the momentum it had until then: the fact remains that it has potential to be reactivated, in

spite of non-negligible pressure factors (1)

Increasing outsourcing of laundry incompanies

More and more ecological and sanitarypressure

More exacting European hygiene andsanitation standards

Technical and technological pressures on theprofessional environment

Demographics (cf. seniors / health)

Productivity / technological leap / reactivity

Competition, dropping of prices, flexibility

Penetration to be improved on the markets

Improvement of the quality of services

Good economic cycle / weak euro

Innovation / PPE / Sophistication of products

Shareholding strategy

Growth or offer development factors

Economic cycle and sensitivity to industrialproduction

Increased competition / less palatable sector

Environmental constraints / logistics /transport / pollution of old sites

Competition from the “disposable” alternative(operating room), paper hand towel, electrichand dryers / cleaning company

Margin safeguarding measures / non-restitution of quality to the customer /perception of deterioration in the quality of theservice

New participants in the world of cleaningcompanies

Digital impact? Direct contact with thecustomer

Health: less lucrative offer / grouping ofhospital centres

Geopolitical tensions (Horeca)

Shareholding strategy: weight of investedcapital

Development of sellers / catalogues

Level of employment

Pressure and demand deterioration factors

Textile Services in Europe November 2016 28

The market was impacted by the 2009 crisis, less by a downturn, than by a break in the momentum it had until then: the fact remains that it has potential to be reactivated, in

spite of non-negligible pressure factors (2)

Relaxation factors Pressure factors

HealthcareRetirement home

Demographics Linen rotation Hygiene and sanitation requirements Care for residents Penetration rate Public sector (France) ----- reactive / financial constraint Clean room

Regrouping of specific, specialised participants Organisation of the healthcare world; outsourcing of

laundry (public health risk, nosocomial diseases) Rise of small structures with appropriate equipment

Hotel and catering

Tourism (Southern Europe) Economic recovery? Change of mentality (penetration rate) Innovation / Differentiation / range / competition

Consumption outside the home « Psychological » breaks of customers Textile costs versus « disposable » solution Geopolitical troubles Digital?

Industry

Penetration rate / increasing outsourcing Tightening up of labour legislation Term of contracts Competition Transfer of responsibility Flexibility / versatility Service Dishcloths

Development of employment in the industrial, agri-food sectors

Disposable, recyclable Cost-killer in the companies Relocation Term of contracts

Hygiene

Penetration rate Low level equipment Expertise Outsourcing of the service Differentiating, original offer

Psychological expenses Rates Strong competition from wholesalers / cleaning

company with captive demand

European

World

Economy

Economic recovery Penetration rate Ecological stakes Group strategy Ecology / sustainable development / recycling

Pressure on industrial activities Strategy of groups Continuation of relocation / employment Waste management Decontamination

Textile Services in Europe November 2016 29

Whereas the sector still has significant sources of growth identified quite early, the 2009 crisis dampened substantially the dynamism of the entire profession and the

recovery has been unequal in the different European countries

Guarantee an original and selective offer

Cultural transgression to be initiated for potential customers

HighG

row

th p

rosp

ects

Weak average

Partnership / adapted local structure

Residents’ linen

Hygiene activityand mats

Hotel trade

Healthcare professional

clothing

Sanitation stakes

Competition fromhealthcare“professionals”

Hyper technical (mechanical/ther

mal) high-performance professional

clothing

Strong development but:

Non-standardised products (logistical and industrial constraint)

“Specialist” and local SMEs (healthcare professional)

Traditional Professional

clothing for industry

Drop in traditional demand/relocation

Migration to more technical clothing with an increasingly stronger component linked to safety (advantage/ ---) particularly for SMEs (new European standards)

----- Product technicityStandard massification

products

Customised “specific" products

Innovation, customisation

Image clothing

Increasingly stronger environmental

constraint

Textile Services in Europe November 2016 30

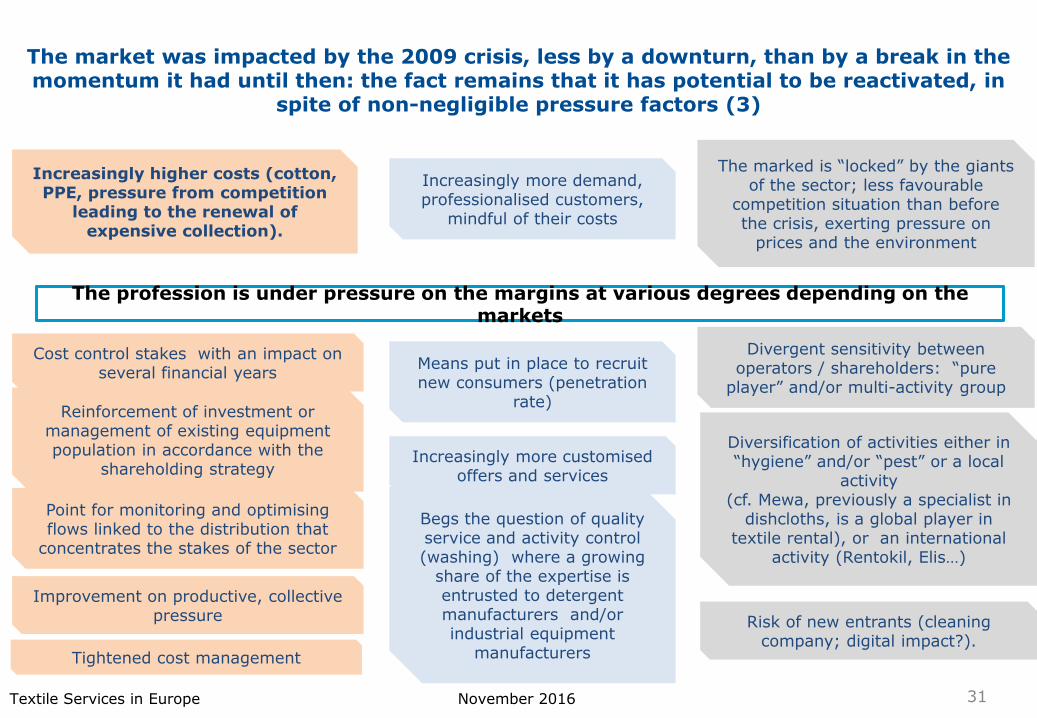

The market was impacted by the 2009 crisis, less by a downturn, than by a break in the momentum it had until then: the fact remains that it has potential to be reactivated, in

spite of non-negligible pressure factors (3)

Increasingly higher costs (cotton, PPE, pressure from competition

leading to the renewal of expensive collection).

Point for monitoring and optimising flows linked to the distribution that

concentrates the stakes of the sector

Increasingly more demand, professionalised customers,

mindful of their costs

The profession is under pressure on the margins at various degrees depending on the markets

Cost control stakes with an impact on several financial years

Means put in place to recruit new consumers (penetration

rate)

Increasingly more customised offers and services

Reinforcement of investment or management of existing equipment population in accordance with the

shareholding strategy

Improvement on productive, collective pressure

Begs the question of quality service and activity control (washing) where a growing

share of the expertise is entrusted to detergent manufacturers and/or industrial equipment

manufacturersTightened cost management

Diversification of activities either in “hygiene” and/or “pest” or a local

activity (cf. Mewa, previously a specialist in

dishcloths, is a global player in textile rental), or an international

activity (Rentokil, Elis…)

The marked is “locked” by the giants of the sector; less favourable

competition situation than before the crisis, exerting pressure on

prices and the environment

Divergent sensitivity between operators / shareholders: “pure

player” and/or multi-activity group

Risk of new entrants (cleaning company; digital impact?).

Textile Services in Europe November 2016 31

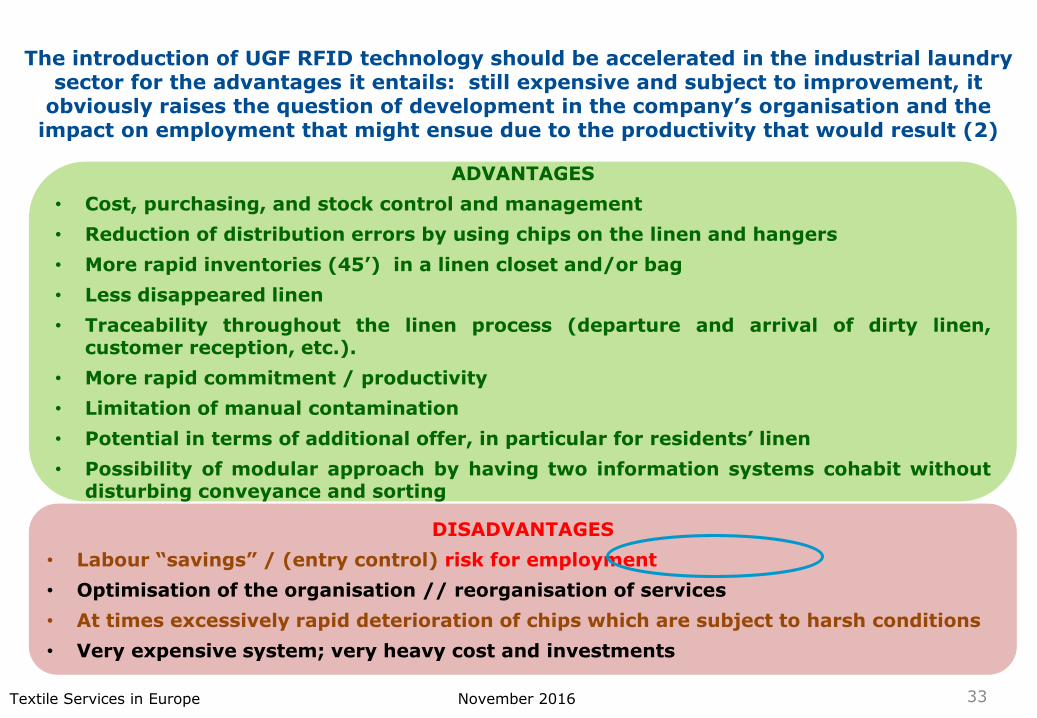

The introduction of UGF RFID technology should be accelerated in the industrial laundry sector for the advantages it entails: still expensive and subject to improvement, it

obviously raises the question of development in the company’s organisation and the impact on employment that might ensue due to the productivity that would result (1)

What is RFID technology

Radio Frequency Identification (RFID) technology is used to trace clothing/linen by installing a chip in thehem of the stitching hems; this technology is available from the manufacturers of this chip,Tagsys, Atlantic, RF, IER.

The detection is made on the basis of contactless identification.

The installation of this technology in the industrial laundry sector was announced some ten yearsago, but, for example, in 2011, the rate of use in France is 2%.

The development of the technology is still facing a number of brakes.

The cost and reliability of the chips, a form of big bang in the organisation and the informationsystem, still constitute serious brakes, even if the deployment is expected to take placegradually by the end of the decade.

Industrial laundries prefer to invest in their own research and development programme, all the more so asthis system still seems to be very expensive for the profession.

Furthermore, by way of reminder, having lived through the inflation of the price of cotton, themultiplication of lines and sophistication of collection, linen weighs increasingly more in theincome statement of the different groups; even though reliability has improved, and with adeclining cost, the question of the balance of constraining opportunities makes the mainoperators cautious still.

Productivity gains of 10% to 20% expected according to Tagsys, probably to the detriment of employment, nonetheless …

Textile Services in Europe November 2016 32

The introduction of UGF RFID technology should be accelerated in the industrial laundry sector for the advantages it entails: still expensive and subject to improvement, it

obviously raises the question of development in the company’s organisation and the impact on employment that might ensue due to the productivity that would result (2)

ADVANTAGES

• Cost, purchasing, and stock control and management

• Reduction of distribution errors by using chips on the linen and hangers

• More rapid inventories (45’) in a linen closet and/or bag

• Less disappeared linen

• Traceability throughout the linen process (departure and arrival of dirty linen,customer reception, etc.).

• More rapid commitment / productivity

• Limitation of manual contamination

• Potential in terms of additional offer, in particular for residents’ linen

• Possibility of modular approach by having two information systems cohabit withoutdisturbing conveyance and sorting

DISADVANTAGES

• Labour “savings” / (entry control) risk for employment

• Optimisation of the organisation // reorganisation of services

• At times excessively rapid deterioration of chips which are subject to harsh conditions

• Very expensive system; very heavy cost and investments

Textile Services in Europe November 2016 33

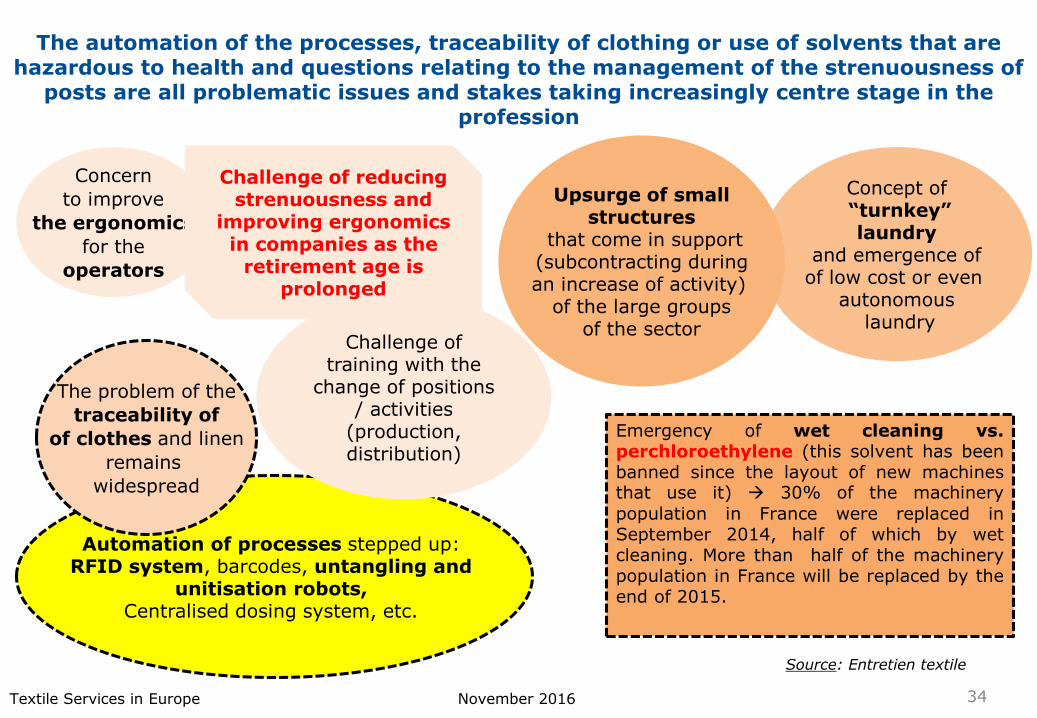

The automation of the processes, traceability of clothing or use of solvents that are hazardous to health and questions relating to the management of the strenuousness of

posts are all problematic issues and stakes taking increasingly centre stage in the profession

Emergency of wet cleaning vs.perchloroethylene (this solvent has beenbanned since the layout of new machinesthat use it) 30% of the machinery

population in France were replaced inSeptember 2014, half of which by wetcleaning. More than half of the machinerypopulation in France will be replaced by theend of 2015.

Concern

to improve

the ergonomics

for the

operators

Concept of“turnkey”laundry

and emergence ofof low cost or even

autonomouslaundry

Upsurge of smallstructures

that come in support(subcontracting during an increase of activity)

of the large groupsof the sector

Automation of processes stepped up: RFID system, barcodes, untangling and

unitisation robots, Centralised dosing system, etc.

Source: Entretien textile

Challenge of reducing strenuousness and

improving ergonomics in companies as the

retirement age is prolonged

The problem of the

traceability of

of clothes and linen

remains

widespread

Challenge of training with the

change of positions / activities

(production, distribution)

Textile Services in Europe November 2016 34

Strenuousness affects nearly all the posts of laundry across the board with diversity and with a variable intensity; the stakes are high in a world where the staff is already subject

to high productivity and constant reorganisations (1)

Physical stress

• Manual handling of loads (lifting, carrying, pushing, pulling, moving with the load)

• Painful posture (arms in the air, crouched and/or kneeling position, extended standing station)

• Mechanical vibrations where necessary (hands / body)

Aggressive environment

• Chemical agents (exposure to a hazardous chemical agent)

• Extreme temperatures (industrial site + station)

• Noise

Work pace

• Night work (?)• Shift work• Repetitive work, with

imposed pace

More generally, risksrelated to the workplace …

Allergic, respiratory and/or skin ailments (detergents) or

infectious diseases (cf. hospital linen), joint injuries in upper limbs, discomfort of

strong odours –input control –high heat emitted by the

washing, drying and folding machines

…and inherent to the equipment

Moving parts of machinery, conveyor belts, arms of untangling and folding machines – hot and/or

burning pipes and machines with risks of leaked steam and

therefore of burns

Textile Services in Europe November 2016 35

Strenuousness affects nearly all the posts of laundry across the board with diversity and with a variable intensity; the stakes are high in a world where the staff is already subject

to high productivity and constant reorganisations (2)

Washer(Noise)

Bag hook Reel unwinding

Sorting on table

Tunnel loading

Mat supply

Honeycomb sorting / platform

Washer loading and unloading (flat

linen, clothing, mats)

Dryer loading and unloading

Engagement and reception (small and large plate calender, reels, folding machine

Distribution(driver, onsite

delivery person)

SewingManual folding

Shipment preparation

platform agent

Inspection

Quality control

Unpacking of chemical products

Warehouseman

Repair

FilmingClothing

shipments

Positions most exposed to physical stress are indicated in red

Textile Services in Europe November 2016 36

Strenuousness at work is acquiring a singular dimension in companies today; it is fought on several fronts through technical, organisational, industrial and other such

solutions

• Acquisition of automated systems with improved ergonomics (cf. increasingly more sophisticated example of untangling robots, conveyor and sorting system)

• Modernising and adapting the facility and trolley / roller tools.

• Reinforcing investments in distribution: more appropriate vehicles, ergonomics of loading platforms, work on delivery points with customers …

Avoiding and combating risks at the source and avoiding of multi-

strenuous situations

Taking account of technical progressTaking collective and/or personal corrective

measures

• Improvements of working conditions on the organisational front (minimising night work, adapting schedules in accordance with seasonality, etc.)

• Versatility and/or mobility of highly strenuous positions: reducing the time of exposure in strenuous position

• the Facilitating the latter years of working career

• Arrangement of posts

• Working the circulation flows

• Training for employees (gestures, postures, risks incurred, production of general safety instructions and sheets, etc).

• Appropriate equipment (PPE, gloves, goggles, mask, etc.)

Textile Services in Europe November 2016 37

QHSE approaches will be increasingly more differentiated and imperative for operators who wish to weigh on the sector: beyond the constraints that they entail,

they constitute powerful commercial mechanisms

Revision of the ISO 14001 – environment –standards

New commitments for the environmententailing proactive approaches(environmental analysis for water, air,noise, visual nuisance, risks, etc.) aimed atthe following aspects:

• Safety

• Energy consumption

• Purchasing/consumption

• Legal matters

Hygiene: RABC certification

Hygiene and linen treatment (linen hygiene control from collection to delivery)

Sensitive challenge for healthcare, the pharmaceutical industry and the foodstuff sector

Quality: ISO 9001 certification

It was revised in 2015 and only the 2015 version will be applicable as of 2018

Social responsibility: ISO 26000 certification

It concerns the following areas:

• Sustainable development and environmental design

• Development and human fulfilment

• Employment development and territorial anchoring

Environment: ISO 50001 certification

It was put in place in 2011 and is aimed at improving energy performance; it is based on the continuous improvement of the energy model which is associated with a management system

model

Textile Services in Europe November 2016 38

Part III: Comparison of the various sector stakeholders

Textile Services in Europe November 2016 39

Salesianer

Mettiex*

Johnson Service

Group

Lindström*

CWS-Boco

Berendsen

Elis

Rentokil Hygiène-

Textile

Alsco**Mewa*

Anett

Malysse

Sterima*

Bardusch*

Elis

France

Rentokil

France

-20%

-15%

-10%

-5%

0%

5%

10%

15%

0 200 400 600 800 1 000 1 200 1 400 1 600 1 800

Chiffre d'affaires 2015 (en M€)

Varia

tion

ch

iffe

d'a

ffair

es 1

5/1

4

La pastille visualise la taille du Chiffre d'affaires de la SociétéSource : Données publiques - Traitement 3E Consultants *CA 2014 ; **CA 2013

Aucune variation du chiffre d'affaires n'est précisée

pour Alsco, Bardusch, Anett et Malysse Sterima car nous ne disposons pas des données N-1

Haniel

(3 808 ; -3.4 %)

Rentokil

(2 423 ; + 1 %)

The growth of industrial laundry groups in Europe is lacklustre in 2015, and continues to be driven by external growth operations: the movement begs the question of the sector’s

state of health in spite of what are still comfortable margins

Rentokil turnover in France deteriorated because of a very

competitive market and an economy that is still in difficulty

Elis organic growth: +2.9

%

Positive impact acquisition of London Linen

RLD

Textile Services in Europe November 2016 40

Most European companies that rent out linen have a profitability of over 10%, except the Johnson Service Group, Haniel and CWS-Boco

Johnson Service Group

Lindström

CWS-Boco

Rentokil - division textiles/hygiène

Berendsen

Elis

Rentokil

Mewa*

Rentokil France

14.6%

4%

6%

8%

10%

12%

14%

16%

18%

20%

200 400 600 800 1 000 1 200 1 400 1 600 1 800 2 000 2 200 2 400 2 600

L'échiquier européen des loueurs de linge : chiffre d'affaires et taux de profitabilité en 2015

Chiffre d'affaires 2015 (en M€)

Tau

x d

e r

ésu

ltat

op

érati

on

nel

La pastille visualise la taille du Chiffre d'affaires de la SociétéSource : Données publiques - Traitement 3E Consultants

Haniel

(5.1 % ; 3 808)

Elis : Après retraitement

des amortissements sur rachat clientèle

*données 2014

Elis : ROC/CA

Profitability sector with highly capitalistic business nonetheless (which drives

linen in particular)

Textile Services in Europe November 2016 41

Operating result/

turnover

Elis

Johnson

Berendsen

Haniel

Mewa

-30

10

50

90

130

170

30 35 40 45 50 55 60 65 70 75

Po

ten

tiel d

e p

ressio

n d

es m

arc

hés f

inan

cie

rs(E

nd

ett

em

en

t n

et

/ f

on

ds p

rop

res)

Indépendance financière(Fonds Propres / Passif du Bilan)La pastille visualise la taille du Chiffre d'affaires de la Société

Source : Données publiques - Traitement 3E Consultants

Rentokil(484; 10)

Following a successful launch on the stock exchange in the beginning of 2015, Elis has cleared the level of debt somewhat, even if it remains high; that of Rentokil

also remains high, albeit lower than in the past; Mewa has “bank” status

Margins of manoeuvrability re-established with the

disposal of Celesio in 2014

Excellent, “bank” status

Fragile, but clearly improved financial

situation for Rentokil

Indebted leading operators: a situation which is strongly reflected

in the pressure extended on the staff and/or the organisation in the search

for margins of manoeuvrability

Textile Services in Europe November 2016 42

Participants

David Mohar: [email protected]

Florie Busca: [email protected]

1 Avenue Foch - BP 9044857008 Metz Cedex 1Tel: 03.87.17.32.60

83 avenue Philippe Auguste75011 Paris

Tel: 01.55.25.77.77

3E Consultants

Textile Services in Europe November 2016 43