TEXTILE MACHINERY MANUFACTURERS’ ASSOCIATION (INDIA ... · textile machinery manufacturers’...

26

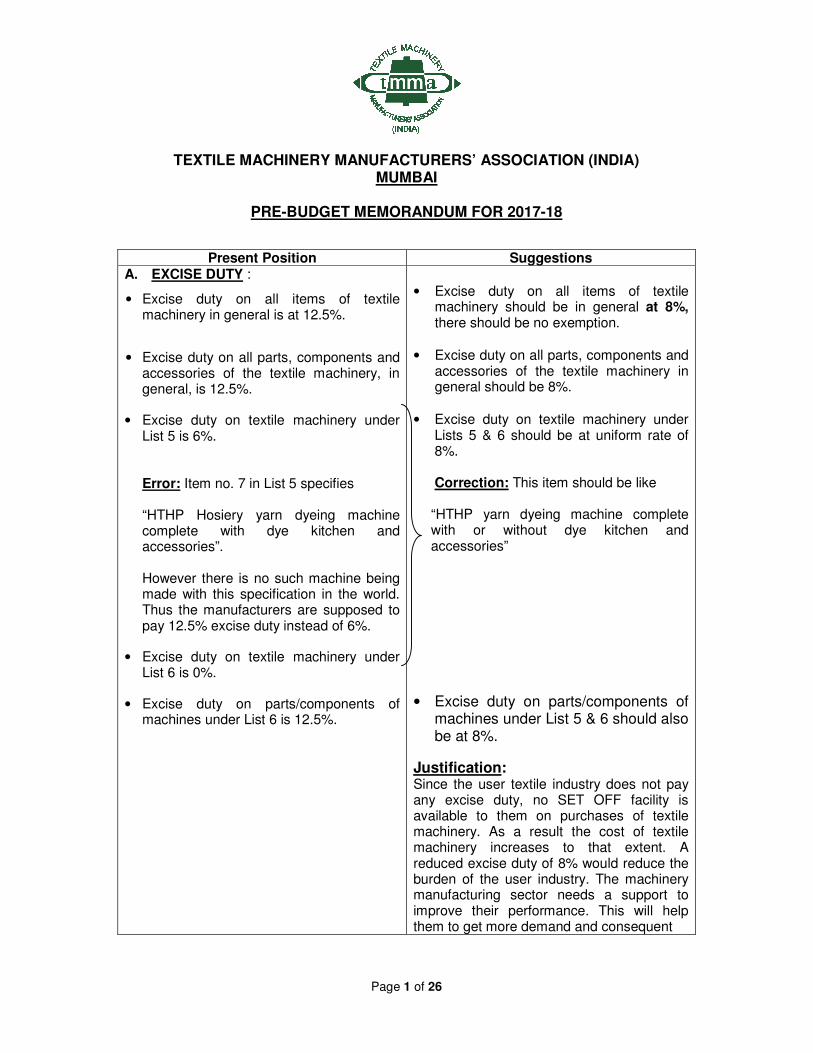

Page 1 of 26 TEXTILE MACHINERY MANUFACTURERS’ ASSOCIATION (INDIA) MUMBAI PRE-BUDGET MEMORANDUM FOR 2017-18 Present Position Suggestions A. EXCISE DUTY : • Excise duty on all items of textile machinery in general is at 12.5%. • Excise duty on all parts, components and accessories of the textile machinery, in general, is 12.5%. • Excise duty on textile machinery under List 5 is 6%. Error: Item no. 7 in List 5 specifies “HTHP Hosiery yarn dyeing machine complete with dye kitchen and accessories”. However there is no such machine being made with this specification in the world. Thus the manufacturers are supposed to pay 12.5% excise duty instead of 6%. • Excise duty on textile machinery under List 6 is 0%. • Excise duty on parts/components of machines under List 6 is 12.5%. • Excise duty on all items of textile machinery should be in general at 8%, there should be no exemption. • Excise duty on all parts, components and accessories of the textile machinery in general should be 8%. • Excise duty on textile machinery under Lists 5 & 6 should be at uniform rate of 8%. Correction: This item should be like “HTHP yarn dyeing machine complete with or without dye kitchen and accessories” • Excise duty on parts/components of machines under List 5 & 6 should also be at 8%. Justification : Since the user textile industry does not pay any excise duty, no SET OFF facility is available to them on purchases of textile machinery. As a result the cost of textile machinery increases to that extent. A reduced excise duty of 8% would reduce the burden of the user industry. The machinery manufacturing sector needs a support to improve their performance. This will help them to get more demand and consequent

Transcript of TEXTILE MACHINERY MANUFACTURERS’ ASSOCIATION (INDIA ... · textile machinery manufacturers’...

Page 1 of 26

TEXTILE MACHINERY MANUFACTURERS’ ASSOCIATION (INDIA)

MUMBAI

PRE-BUDGET MEMORANDUM FOR 2017-18

Present Position Suggestions A. EXCISE DUTY :

• Excise duty on all items of textile machinery in general is at 12.5%.

• Excise duty on all parts, components and accessories of the textile machinery, in general, is 12.5%.

• Excise duty on textile machinery under List 5 is 6%.

Error: Item no. 7 in List 5 specifies “HTHP Hosiery yarn dyeing machine complete with dye kitchen and accessories”. However there is no such machine being made with this specification in the world. Thus the manufacturers are supposed to pay 12.5% excise duty instead of 6%.

• Excise duty on textile machinery under List 6 is 0%.

• Excise duty on parts/components of machines under List 6 is 12.5%.

• Excise duty on all items of textile machinery should be in general at 8%, there should be no exemption.

• Excise duty on all parts, components and accessories of the textile machinery in general should be 8%.

• Excise duty on textile machinery under Lists 5 & 6 should be at uniform rate of 8%. Correction: This item should be like “HTHP yarn dyeing machine complete with or without dye kitchen and accessories”

• Excise duty on parts/components of machines under List 5 & 6 should also be at 8%.

Justification: Since the user textile industry does not pay any excise duty, no SET OFF facility is available to them on purchases of textile machinery. As a result the cost of textile machinery increases to that extent. A reduced excise duty of 8% would reduce the burden of the user industry. The machinery manufacturing sector needs a support to improve their performance. This will help them to get more demand and consequent

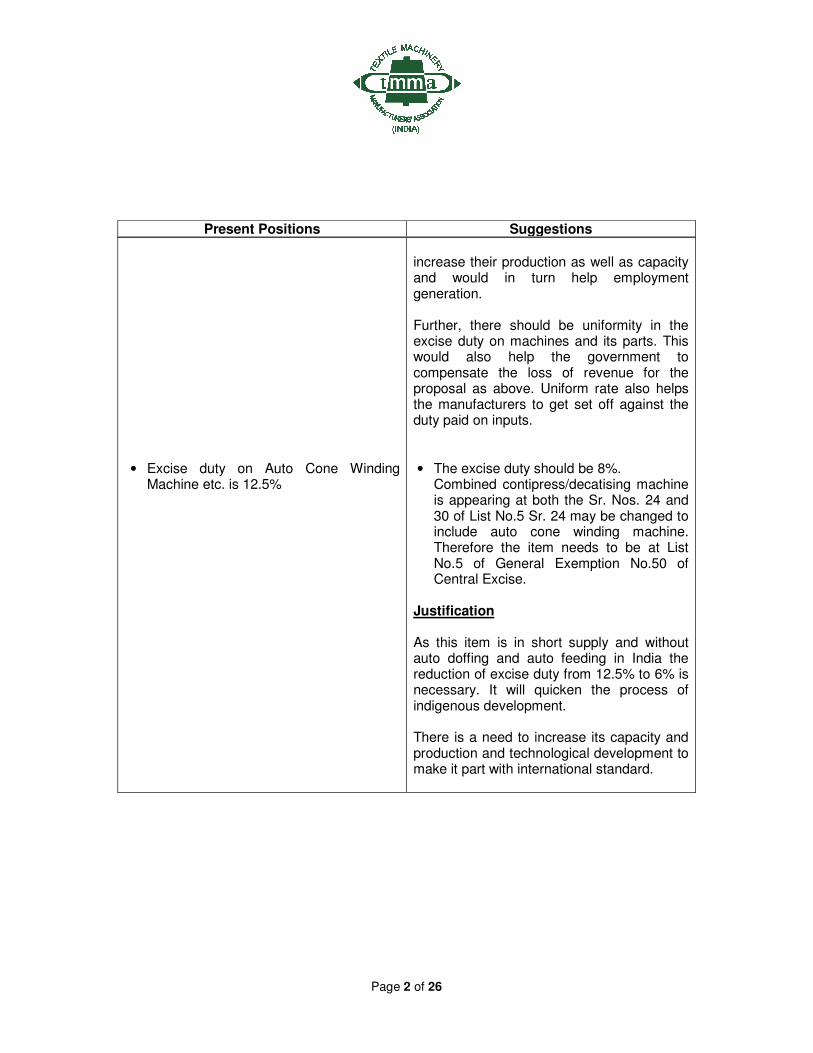

Page 2 of 26

Present Positions Suggestions

• Excise duty on Auto Cone Winding Machine etc. is 12.5%

increase their production as well as capacity and would in turn help employment generation. Further, there should be uniformity in the excise duty on machines and its parts. This would also help the government to compensate the loss of revenue for the proposal as above. Uniform rate also helps the manufacturers to get set off against the duty paid on inputs.

• The excise duty should be 8%. Combined contipress/decatising machine is appearing at both the Sr. Nos. 24 and 30 of List No.5 Sr. 24 may be changed to include auto cone winding machine. Therefore the item needs to be at List No.5 of General Exemption No.50 of Central Excise.

Justification As this item is in short supply and without auto doffing and auto feeding in India the reduction of excise duty from 12.5% to 6% is necessary. It will quicken the process of indigenous development. There is a need to increase its capacity and production and technological development to make it part with international standard.

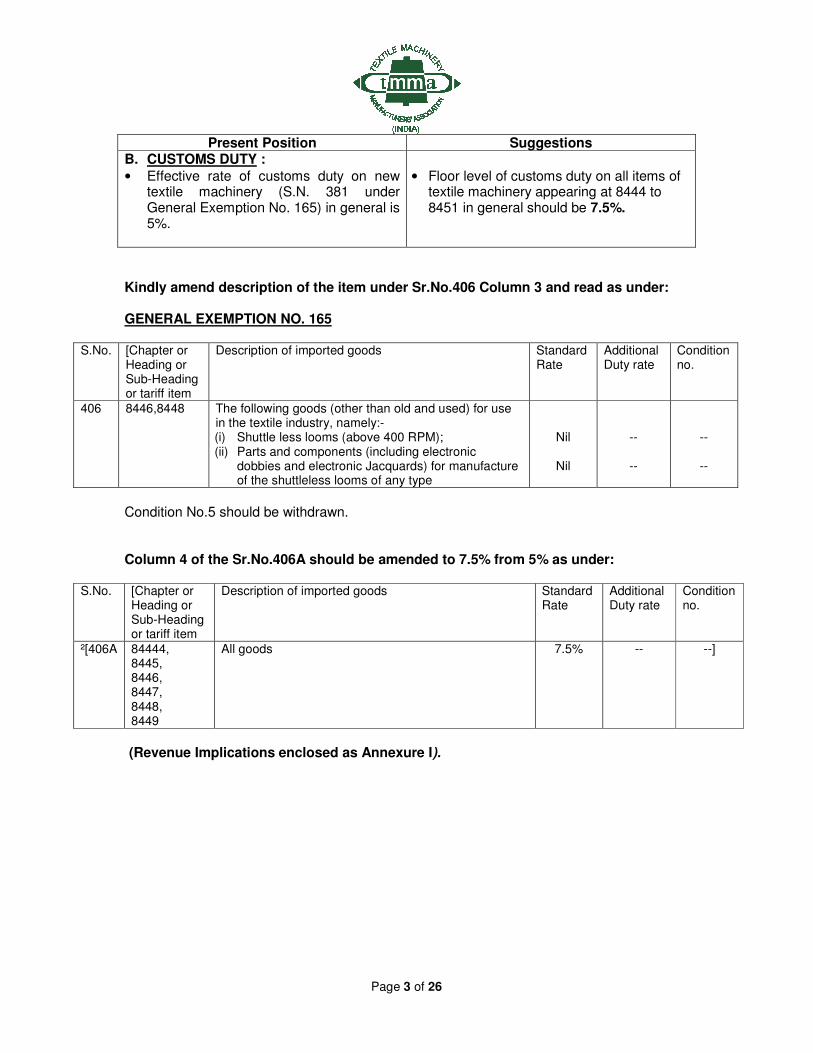

Page 3 of 26

Present Position Suggestions B. CUSTOMS DUTY :

• Effective rate of customs duty on new textile machinery (S.N. 381 under General Exemption No. 165) in general is 5%.

• Floor level of customs duty on all items of textile machinery appearing at 8444 to 8451 in general should be 7.5%.

Kindly amend description of the item under Sr.No.406 Column 3 and read as under: GENERAL EXEMPTION NO. 165

S.No. [Chapter or Heading or Sub-Heading or tariff item

Description of imported goods Standard Rate

Additional Duty rate

Condition no.

406 8446,8448 The following goods (other than old and used) for use in the textile industry, namely:- (i) Shuttle less looms (above 400 RPM); (ii) Parts and components (including electronic

dobbies and electronic Jacquards) for manufacture of the shuttleless looms of any type

Nil

Nil

--

--

--

--

Condition No.5 should be withdrawn. Column 4 of the Sr.No.406A should be amended to 7.5% from 5% as under:

S.No. [Chapter or Heading or Sub-Heading or tariff item

Description of imported goods Standard Rate

Additional Duty rate

Condition no.

²[406A 84444, 8445, 8446, 8447, 8448, 8449

All goods 7.5% -- --]

(Revenue Implications enclosed as Annexure I).

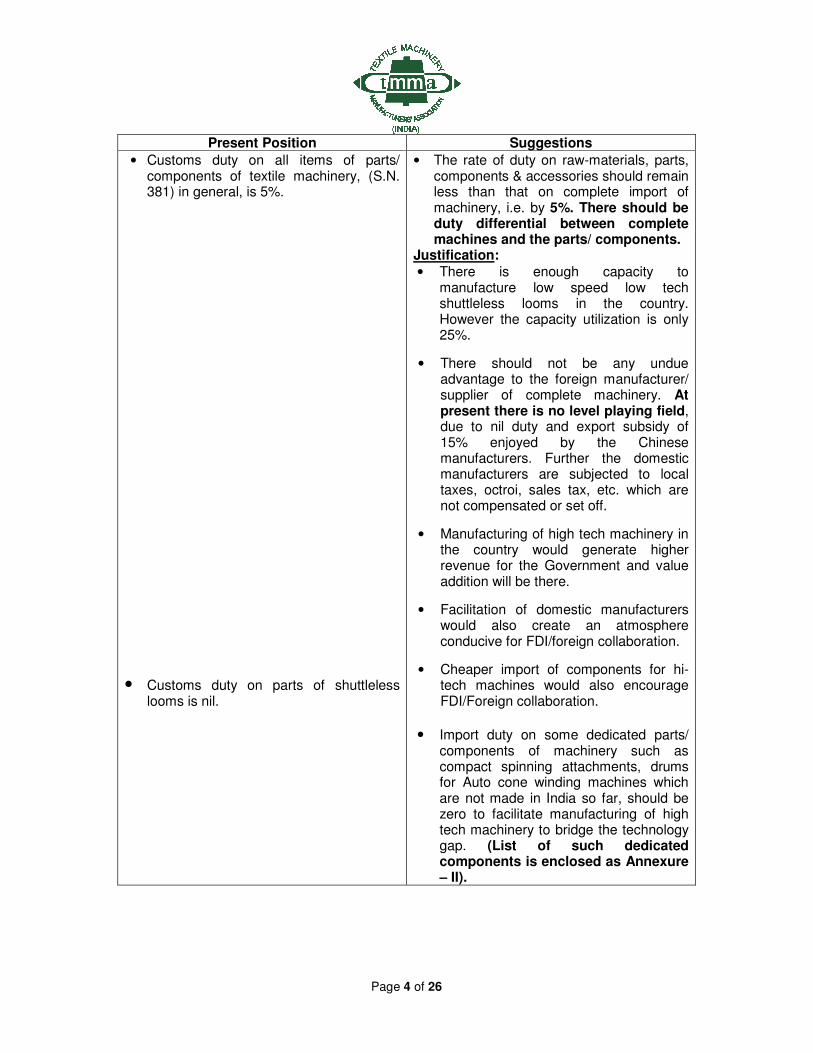

Page 4 of 26

Present Position Suggestions

• Customs duty on all items of parts/ components of textile machinery, (S.N. 381) in general, is 5%.

• Customs duty on parts of shuttleless looms is nil.

• The rate of duty on raw-materials, parts, components & accessories should remain less than that on complete import of machinery, i.e. by 5%. There should be duty differential between complete machines and the parts/ components.

Justification:

• There is enough capacity to manufacture low speed low tech shuttleless looms in the country. However the capacity utilization is only 25%.

• There should not be any undue advantage to the foreign manufacturer/ supplier of complete machinery. At present there is no level playing field, due to nil duty and export subsidy of 15% enjoyed by the Chinese manufacturers. Further the domestic manufacturers are subjected to local taxes, octroi, sales tax, etc. which are not compensated or set off.

• Manufacturing of high tech machinery in the country would generate higher revenue for the Government and value addition will be there.

• Facilitation of domestic manufacturers would also create an atmosphere conducive for FDI/foreign collaboration.

• Cheaper import of components for hi-tech machines would also encourage FDI/Foreign collaboration.

• Import duty on some dedicated parts/ components of machinery such as compact spinning attachments, drums for Auto cone winding machines which are not made in India so far, should be zero to facilitate manufacturing of high tech machinery to bridge the technology gap. (List of such dedicated components is enclosed as Annexure – II).

Page 5 of 26

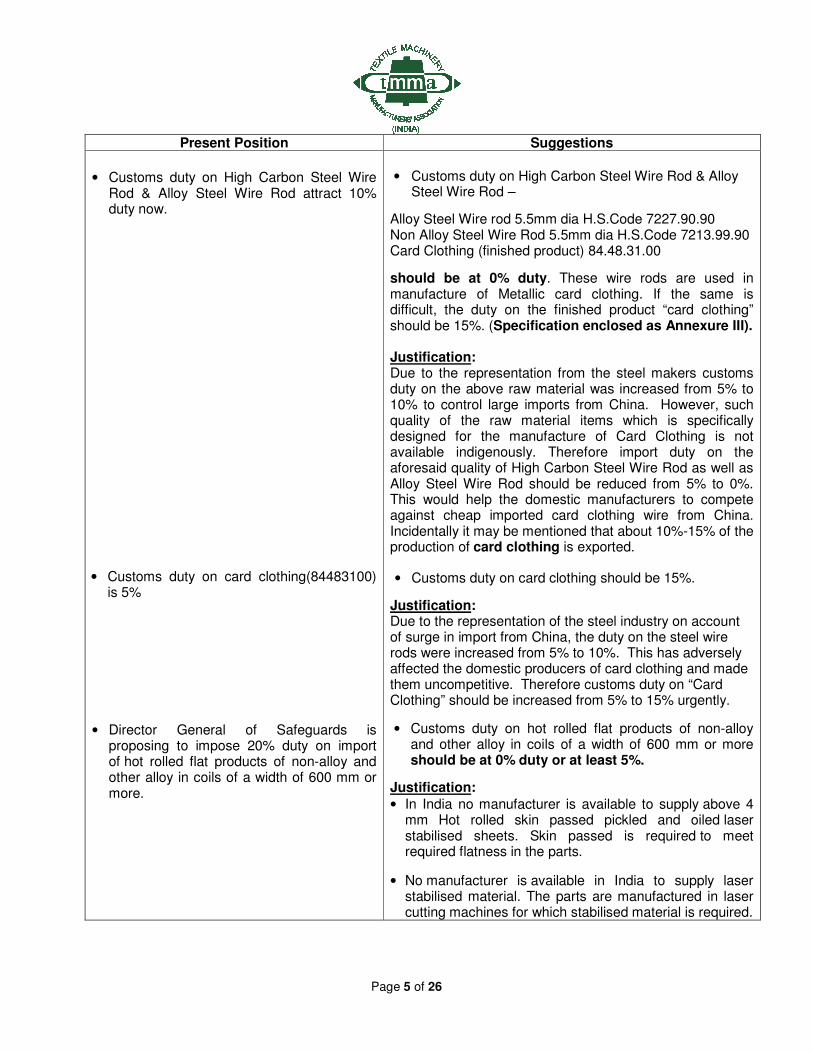

Present Position Suggestions

• Customs duty on High Carbon Steel Wire

Rod & Alloy Steel Wire Rod attract 10% duty now.

• Customs duty on card clothing(84483100) is 5%

• Director General of Safeguards is proposing to impose 20% duty on import of hot rolled flat products of non-alloy and other alloy in coils of a width of 600 mm or more.

• Customs duty on High Carbon Steel Wire Rod & Alloy Steel Wire Rod –

Alloy Steel Wire rod 5.5mm dia H.S.Code 7227.90.90 Non Alloy Steel Wire Rod 5.5mm dia H.S.Code 7213.99.90 Card Clothing (finished product) 84.48.31.00

should be at 0% duty. These wire rods are used in manufacture of Metallic card clothing. If the same is difficult, the duty on the finished product “card clothing” should be 15%. (Specification enclosed as Annexure III). Justification: Due to the representation from the steel makers customs duty on the above raw material was increased from 5% to 10% to control large imports from China. However, such quality of the raw material items which is specifically designed for the manufacture of Card Clothing is not available indigenously. Therefore import duty on the aforesaid quality of High Carbon Steel Wire Rod as well as Alloy Steel Wire Rod should be reduced from 5% to 0%. This would help the domestic manufacturers to compete against cheap imported card clothing wire from China. Incidentally it may be mentioned that about 10%-15% of the production of card clothing is exported.

• Customs duty on card clothing should be 15%.

Justification: Due to the representation of the steel industry on account of surge in import from China, the duty on the steel wire rods were increased from 5% to 10%. This has adversely affected the domestic producers of card clothing and made them uncompetitive. Therefore customs duty on “Card Clothing” should be increased from 5% to 15% urgently.

• Customs duty on hot rolled flat products of non-alloy and other alloy in coils of a width of 600 mm or more should be at 0% duty or at least 5%.

Justification:

• In India no manufacturer is available to supply above 4 mm Hot rolled skin passed pickled and oiled laser stabilised sheets. Skin passed is required to meet required flatness in the parts.

• No manufacturer is available in India to supply laser stabilised material. The parts are manufactured in laser cutting machines for which stabilised material is required.

Page 6 of 26

Present Position Suggestions

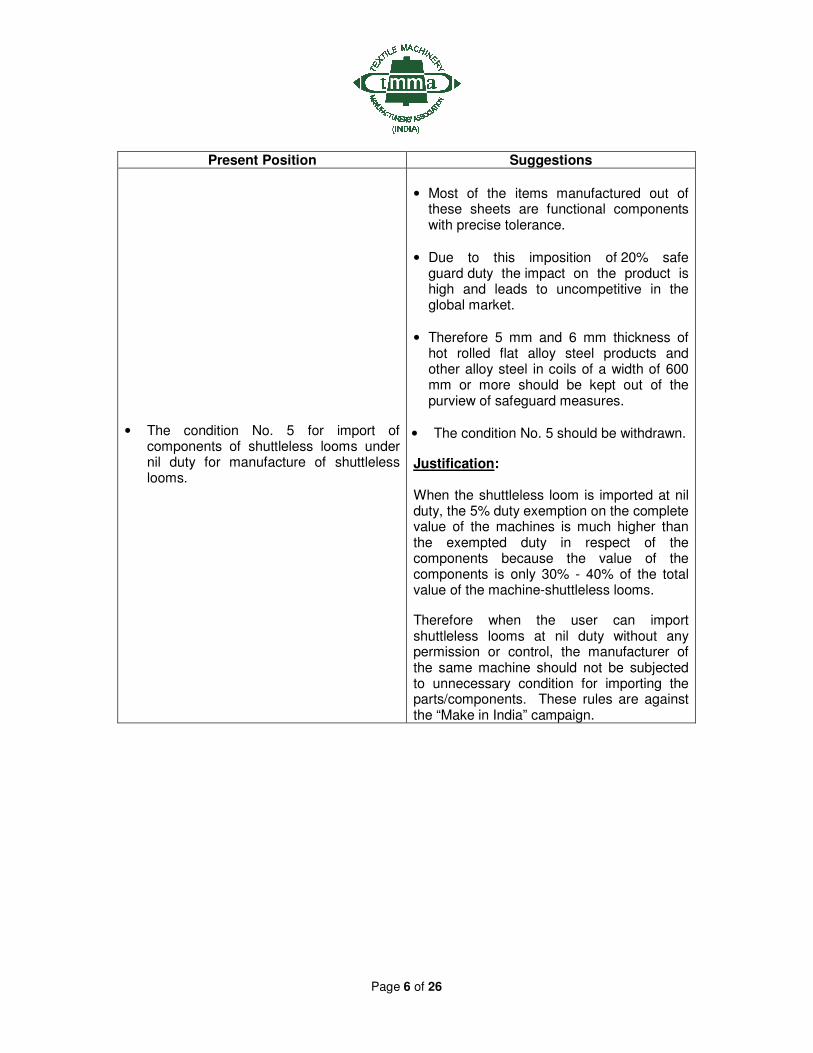

• The condition No. 5 for import of

components of shuttleless looms under nil duty for manufacture of shuttleless looms.

• Most of the items manufactured out of these sheets are functional components with precise tolerance.

• Due to this imposition of 20% safe guard duty the impact on the product is high and leads to uncompetitive in the global market.

• Therefore 5 mm and 6 mm thickness of hot rolled flat alloy steel products and other alloy steel in coils of a width of 600 mm or more should be kept out of the purview of safeguard measures.

• The condition No. 5 should be withdrawn.

Justification: When the shuttleless loom is imported at nil duty, the 5% duty exemption on the complete value of the machines is much higher than the exempted duty in respect of the components because the value of the components is only 30% - 40% of the total value of the machine-shuttleless looms.

Therefore when the user can import shuttleless looms at nil duty without any permission or control, the manufacturer of the same machine should not be subjected to unnecessary condition for importing the parts/components. These rules are against the “Make in India” campaign.

Page 7 of 26

Present Position Suggestions

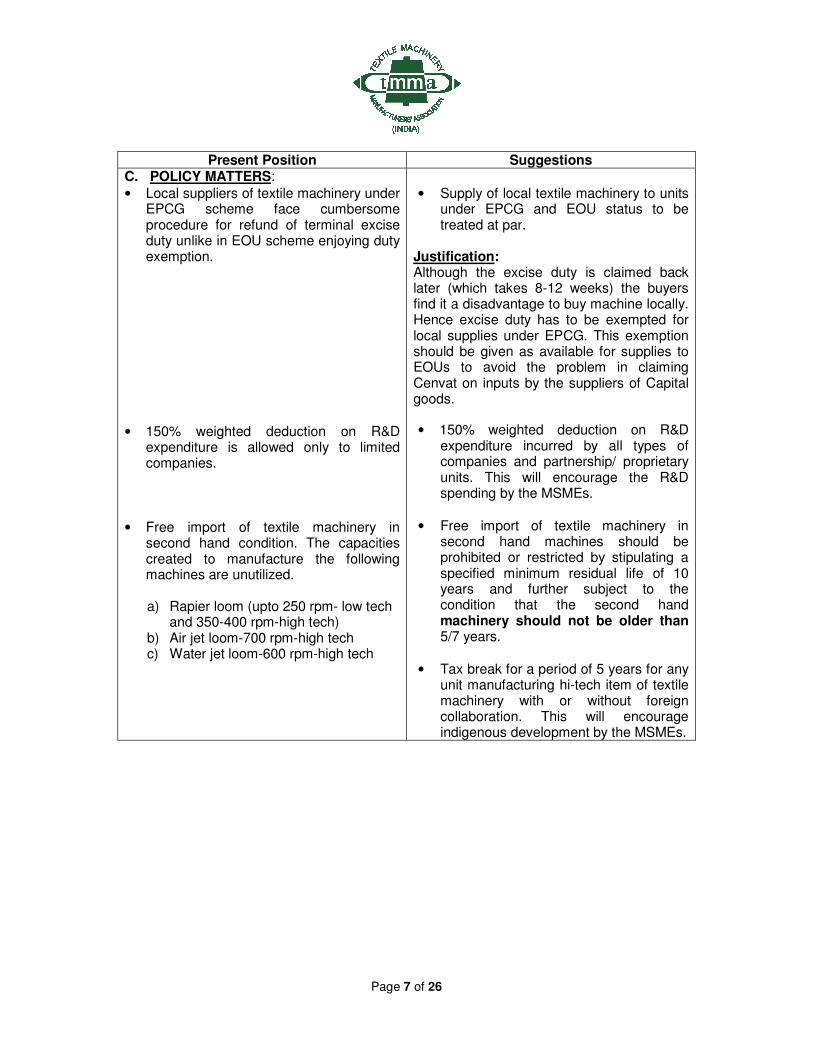

C. POLICY MATTERS:

• Local suppliers of textile machinery under EPCG scheme face cumbersome procedure for refund of terminal excise duty unlike in EOU scheme enjoying duty exemption.

• 150% weighted deduction on R&D expenditure is allowed only to limited companies.

• Free import of textile machinery in second hand condition. The capacities created to manufacture the following machines are unutilized. a) Rapier loom (upto 250 rpm- low tech

and 350-400 rpm-high tech) b) Air jet loom-700 rpm-high tech c) Water jet loom-600 rpm-high tech

• Supply of local textile machinery to units under EPCG and EOU status to be treated at par.

Justification: Although the excise duty is claimed back later (which takes 8-12 weeks) the buyers find it a disadvantage to buy machine locally. Hence excise duty has to be exempted for local supplies under EPCG. This exemption should be given as available for supplies to EOUs to avoid the problem in claiming Cenvat on inputs by the suppliers of Capital goods.

• 150% weighted deduction on R&D expenditure incurred by all types of companies and partnership/ proprietary units. This will encourage the R&D spending by the MSMEs.

• Free import of textile machinery in second hand machines should be prohibited or restricted by stipulating a specified minimum residual life of 10 years and further subject to the condition that the second hand machinery should not be older than 5/7 years.

• Tax break for a period of 5 years for any unit manufacturing hi-tech item of textile machinery with or without foreign collaboration. This will encourage indigenous development by the MSMEs.

Page 8 of 26

Present Position Suggestions D. NECESSARY SCHEMES:

• At present there are some Schemes for product development.

• Scheme for modernization, technology

up-gradation and productivity enhancement of the TEI:

It is recommended to launch a TUF dedicated to the Indian textile machinery Industry. The fund should have an interest reimbursement outlay of Rs.250 crores for XII Plan and based on similar principles as TUFS and over the following areas: � Expansion and modernization of

existing textile machinery manufacturing companies

� Acquisition of technical know-how from overseas

� Industry segments regarded as weak or non-existing (rotors spinning, fully automatic winding, high tech weaving, special purpose processing & finishing, knitting and industrial sewing equipment) should be eligible for upfront 10% capital subsidy in addition to interest reimbursement to upgrade their manufacturing facility.

• Encourage establishment of new TEI units & SEZ for FDI promotion.

Date : 13.9.2016 Sc/Sr:

Page 9 of 26

TEXTILE MACHINERY MANUFACTURERS’ ASSOCIATION (INDIA) SUGGESTIONS RECEIVED FROM MEMBERS

PRE BUDGET MEMORANDUM – DIRECT TAXES –BUDGET 2017 CORPORATE TAXATION :

1. Corporate tax rate should be brought down to 25%

2. Extension of benefit under Section 80-IA for power generation industries

extended till 31st March, 2017 should further be extended till 31st March,

2020 considering solar power projects.

3. Disallowance under Section 40a(ia) of the Act - Section 40(a)(ia) of the Act

allows the taxpayer an extended time upto the due date of filing the return of

income for depositing the tax deducted at source from payments to residents.

Whereas similar benefit of extended time is not available under Section

40(a)(i) of the Act where the payments are made to non-residents. Section

40(a)(ia) of the Act provides that specified payments to residents without

deduction of tax at source will result in disallowance of the related expenditure

and the payer is considered as a taxpayer in default and is liable for interest,

penalty and prosecution (except in certain cases as stipulated). It is

recommended that the discrimination between payments to residents and

non-residents regarding extended time line for deposit of TDS should be

removed and even under Section 40(a)(i) of the Act the taxpayer should be

given the benefit of extended time for depositing the TDS on payments made

to non-residents up to the due date of filing the Return of Income. It is also

recommended that the disallowance should be restricted to the amount of tax

not deductible at source on the payment and not the entire payment.

4. Deputation of employees - Increasing globalisation has resulted in fast

growing mobilization of labour across various countries. Typically, the

company deputing the personnel initially pays the salary and other costs on

behalf of the company to which such personnel are deputed, which are

thereafter reimbursed by the latter company. The issue which had cropped

up before the Indian tax authorities due to the increasing deputation

agreements being entered cross border was whether such reimbursements

made by Indian entity to an overseas entity towards salary and other costs in

relation to the deputed employees should be taxable in India as being

payment in the nature of fees for technical services. It is recommended, since

the employees deputed to the Indian company work under the control and

supervision of the Indian company and hence are essentially 'employees' of

the Indian company, the amounts paid by the Indian company to the foreign

company are merely 'cost reimbursements' for the salaries paid on the Indian

company's behalf. In order to put an end to this litigation, a specific

Page 10 of 26

clarification may be provided by the Government to the effect that as long as

the employee reports and works directly for the Indian company and

operationally works under the 'control and supervision' of the Indian company,

payments made by the Indian company to the foreign company towards

reimbursement of the salary cost would be treated as 'pure reimbursement'

and would not be taxable under the Act.

5. Requirement for non-residents having no place of business in India to comply

with TDS obligations.

The Finance Act, 2012 extended the obligation to withhold taxes to non-residents irrespective of whether the non resident has— (i) a residence or place of business or business connection in India; or (ii) any other presence in any manner whatsoever in India.” The aforesaid amendment was introduced with retrospective effect from 1 April 1962. The amendment will result in a significant expansion in the scope of withholding provisions under the Act and will cover all non-residents, regardless of their presence/connection with India. It is recommended that Applicable rules of statutory interpretation read with Section 1(2) of the Act, indicates that Section 195 of the Act as currently in force should not apply to non-residents.

6. Tax Residency Certificate (TRC) The Finance Act, 2012 had provided that in

order to be eligible to claim relief under the tax treaty, a taxpayer is required to

produce a Tax Residency Certificate (TRC) issued by the Government of the

respective country or the specified territory in which such taxpayer is resident,

containing certain prescribed particulars. Subsequently, the Central Board of

Direct Taxes (CBDT) prescribed the details to be included in the TRC. The

Finance Act, 2013 has done away with the requirement of obtaining

prescribed particulars in the TRC. In other words, the taxpayer can continue

to obtain the TRC as issued by the foreign authorities. The Finance Act, 2013

also introduced a provision to clarify that the taxpayer shall now be required to

furnish such other information or document as may be prescribed. The CBDT

subsequently issued a notification amending the Rules prescribing the

additional information required to be furnished by non-residents along with the

TRC. The details are required to be furnished in Form 10F.

Issues - Even though the requirement to furnish TRC containing prescribed particulars has been dispensed with, however, depending on the jurisdiction, obtaining a TRC certificate may also be a time consuming/difficult process. TRC requirement increases the administrative difficulty for non-residents, especially from the perspective of nonresidents having very few/limited transactions connected to India. The deductor would like to obtain the TRC at the time of the transaction/ depositing the tax (to ensure that the payee is eligible for the tax treaty benefits), the payee would typically be able to obtain

Page 11 of 26

TRC only after the relevant year. As per the new Rule an Indian resident who wishes to obtain TRC from Indian income tax authorities, is required to make an application in Form No. 10FA to the tax officer, containing prescribed details. However, no time limit for issue of TRC is specified from the date of application by the assessee. Furthermore, the issue of TRC in Form No. 10FB has been left to the discretion of satisfaction of the tax officer, without providing a substantive definition for satisfaction in this regard. It has not been specified as to who shall sign Form 10F. Hence, it should be clarified who is authorized to sign the form. Recommendations - The requirement to obtain TRC for a taxpayer to prove that he is a resident of the other state shall be deleted as there may be circumstances wherein the taxpayer who is a bona fide tax resident of the other contracting state is unable to procure a TRC owing to circumstances outside his control. At assessment stage, it is anyway incumbent upon the AO to ascertain complete details before allowing tax treaty benefits. In such a scenario, even though the AO may otherwise be satisfied that the tax treaty benefits must be allowed, only owing to the procedural lapse of not obtaining the TRC which is beyond the tax payer's control, the AO would be compelled to deny tax treaty benefits, which will cause needless hardship. The deductor would like to obtain the TRC at the time of the transaction/deducting the tax (to ensure that the payee is eligible for the tax treaty benefits), it would pose a hardship to the payee to obtain a TRC before the end of the relevant financial year. The procedure so cast would pose onerous responsibility both on the payers/payee resulting in holding of payments by the payer. Without prejudice, even if the requirement to obtain TRC must stay, it is recommended that the TRC shall be made mandatory only for cases where the total payment to a non-resident exceeds Rs. 1 crore in a financial year. This would mitigate hardship in respect of small payments.

7. Income-tax exemption in case of Sale of Carbon Credits Issue Carbon credit

is an incentive available to the industries reducing CO2 emission by investing

in energy efficient technology. Considering the ‘Global Warming’ impacts, it is

a very important initiative on the part of industries. Energy efficient and carbon

emission reduction technologies are substantially costly and results in

additional investment for industries. It is very much likely that the income

generated from sale of Carbon Credits may or may not compensate additional

outflow laid out for earning the same.

Recommendations - Section 10 of the Act should be amended to provide exemption to income from sale of Carbon Credit entitlements. Alternatively, suitable amendment should be made in Section 35 of the Act to allow weighted deduction for expenditure in relation to infrastructure requirement resulting into earning of Carbon Credit.

8. Corporate Social Responsibilty expenditure mandated under Companies Act

2013 should be allowed as deductible expenditure under Income tax act.

Page 12 of 26

9. Concept of tax neutrality should be introduced in domestic transfer pricing

regulations where in if the the Indian Government do not lose any tax, the

disallowance u/s. 92BA should not be made. For example in case of related

party domestic transactions, if the paying and receiving companies are paying

tax @ maximum rates ie 34.67 % for FY 2015-16, the such transactions

should not be subject to disallowance under domestic transfer pricing

regulations.

PERSONAL TAXATION 10. Basic exemption limit and tax rate

Basic exemption limit should be increased to Rs.5,00,000/- and maximum tax rate should be reduced from 30% to 25%

11. Revival of Standard Deduction :

A standard deduction was earlier available to the salaried individuals from their taxable salary income. However the same was abolished with effect from AY 2006-07. On the other hand, business expenses continued to remain as permissible deductions from taxable business income. It has to be appreciated that standard deduction is not a personal allowance and used to be given as a lump sum for meeting employment related expenses. In many countries like Malaysia, Indonesia, Germany, France, Japan, Thailand etc. allowance in the form of standard deduction is available for salaried employees for expenses connected with salary income. To illustrate in Thailand the deduction is as high as 40 percent of income subject to certain limits. Recommendation The standard deduction for salaried employees should be reinstated to at least INR 1,00,000 to ease the tax burden of the employees and keeping in mind the rate of inflation and purchasing power of the salaried individual, which is dependent on salary available for disbursement. This should also reduce the disparity between salaried and business class with only the latter being eligible for deduction for expenses incurred by them for earning their income.

12. Transportation Allowance

The transport allowance granted by the employer to the employee to meet his expenditure for the purpose of commuting between the place of his residence and the place of his duty is currently tax exempt up to INR 1600 per month in terms of Section 10(14) of the Act read with Rule 2BB of the Rules. This exemption limit seems quite nominal considering the ever rising fuel costs and resultant conveyance costs. Recommendation - The exemption limit of INR 1600 per month needs to be considerably raised upwards, say to minimum of INR 5,000 per month to bring it in line with the rising conveyance costs.

13. Education Allowance

Page 13 of 26

The education allowance granted by the employer to the employee to meet the cost of education expenditure upto two children is currently tax exempt up to INR 100 per month per child in terms of Section 10(14) of the Act read with Rule 2BB of the Rules. This exemption limit was fixed in 2000 with retrospective effect from 1 August 1997 and seems quite nominal considering the ever rising cost of education. Recommendation - The exemption limit of INR 100 per month needs to be considerably raised upwards, say to minimum of INR 2,000 per month to bring it in line with the rising inflation and cost of education

14. Reimbursement of Medical Expenditure Issues

Any sum paid by the employer in respect of any expenditure incurred by the employee on the medical treatment of self/ family is currently exempt from tax, to the extent of INR 15,000 per annum. This limit was last revised long back and needs to be revisited in light of the rising medical and hospitalization costs especially for private hospitals. The expenditure incurred by/for retired employees in respect of medical treatment on self/family is currently not exempt from tax. Recommendation The current tax exemption limit of Rs. 15,000 per annum needs to be increased to at least INR 50,000 per annum. This could to some extent help to bring the exemption up to speed with the rising medical costs. Further, the exemption in respect of expenditure on medical reimbursements/hospitalization expenditure in approved hospitals should also be extended to retired employees.

15. Deduction in respect of Health Insurance Premia under Section 80

Currently, a deduction up to INR 55,000 (25,000 for self/ family and 30,000 for parents) is available to an individual under Section 80D of the Act from taxable income, towards health insurance premium paid by him. The limit for parents is increased to INR 30,000 if the parents are senior citizens. Unlike many other countries, India does not have a comprehensive health-care system for its citizens. There are Government hospitals but the facilities available are woefully inadequate while the private hospitals are very expensive. Also, the penetration and awareness of health insurance in India is very slow. Most individuals buy insurance only to save taxes. Recommendation Therefore, there is a need to raise the above limit to achieve two-fold objective of giving a tax incentive while also encouraging people to obtain larger healthcare cover in wake of the rising costs. It will be immensely helpful if, till the Government introduces adequate healthcare systems, the quantum of deduction under Section 80D of the Act is increased. A reference to General Insurance Corporation to find out how much they charge as premium for insurance of a family under a comprehensive hospitalization scheme will give an indication about the reasonable higher limit of the deduction.

16. Tax Exemption in respect of Leave Travel Concession (LTC)

Page 14 of 26

Presently, the economy class air fare for going to anywhere in India is tax exempt (twice in block of four years). However, this exemption is being allowed only for travel within India. Lately, owing to low airfares and package tours, a number of Indians prefer to avail LTC for going abroad particularly to neighbouring countries like Thailand, Malaysia, Sri Lanka, Mauritius, etc., as the fares thereto are at times less than for travelling to some far away destination within India. It is therefore recommended to grant tax exemption for economy class airfare for travel abroad also on holidays so long these are within the overall airfare tax exemption conditions for travelling in India. However, considering the current prevailing trend in respect of foreign travel, there is a need to include overseas travel as well or at least to exempt proportionate expenses pertaining to travel within India in case of joint travel (within India and overseas destination). Further, under Rule 2B of the Rules, the amount exempt in respect of LTC by air is to the extent of the economy fare of National Carrier i.e. Indian Airlines. It is suggested that word “National Carrier” should be deleted from Rule 2B. Moreover, as per the current provisions, Leave Travel Concession/Assistance is eligible for tax relief for 2 calendar years in a block of 4 calendar years. It is suggested that the concept of calendar year should be replaced with financial year (April – March) in line with the other provisions of the Income Tax Law and further exemption should be made available in respect of at least one journey in each financial year

17. Exemption for payment of Leave Encashment to be raised to Rs.10

Lakhs

The exemption limit for leave encashment paid at the time of retirement or otherwise is notified by the CBDT in accordance with the powers given under section 10(10AA) of the Act. The current limit of Rs. 3 lakhs is very old (since 1998) and needs to be raised substantially with immediate effect.

18. Exemption for payment of Gratuity at the time of retirement

Currently exemption limit is Rs.10 lakhs and its already in proposal to raise to Rs. 20 lakhs. It may be noted that on account of absence of social security

schemes in India, the entire amount of gratuity received at the time of retirement may be fully exempt like withdrawal of provident fund at the time of

retirement.

Page 15 of 26

PREBUDGET MEMORANDUM INDIRECT TAX: Export Promotion Schemes. The Government of India has introduced several export promotion schemes to encourage exports. It is really a welcome move and all the exporters are benefited by such schemes. The exporters are further preparing to export more products and earn foreign exchange for the country. However, there are certain areas which require special attention from the government. We would like to bring to your kind notice the following high lights for you to take up before the concerned ministries.

1. Export Incentives:

Presently Export incentives such as Drawback, MEIS (Merchandise Export

From India Scheme), SEIS (Service Exports From India Scheme) are

sanctioned for different categories of clearances like Physical Exports and

Deemed Exports (EOU and EPCG etc.). Drawback for physical exports is

sanctioned by the Finance Ministry and for the remaining schemes Drawback

are allotted by the Commerce Ministry. In the former case the Drawback

amounts are sanctioned immediately where as in the case of Deemed Exports

schemes the Drawback amounts are sanctioned after lapse of more than a

year. The industry expects that equal importance should be given for both

physical exports and deemed exports.

There should be an entirely different system for sanction of Export Incentive.

In the case of physical exports the Drawback /MEIS/SEIS amount can be

sanctioned through respective banks immediately after the export proceeds

are realized in foreign exchange. In the case of deemed exports also the

Drawback can be sanctioned by the respective bankers based on Bank

Realization Certificate. The Government should also consider the interest

subsidies as there will be long gap between the date of export and the date of

realization.

2. EXPORT PROCEDURES Our country is in need of huge foreign exchange reserves. For these more exports have to take place. Therefore exports have to be encouraged and the procedure should me made simple. Though the government has simplified certain procedures, even now the system appears to be complicated. Interaction between the Exporter and the department should be minimised. However, a strict legislation may be introduced to avoid any misuse. The department introduced the system of self sealing but even today that cannot be done without department’s intervention. Genuine exporters should be permitted to have a very simplified procedure. Now every exporter after exporting his product should submit a form called Annexure 19 with the central excise authorities for getting proof of exports. At the time of exports either the central excise officials or the customs officials will be present and they can straight away certify that the export has taken

Page 16 of 26

place. These departments can straight away verify the genuine of export in online through ICE:GATE since most of the exports are cover under EDI.

3. Rebate of Excise Duty:

The conditions and procedure relating to export under claim for rebate are explained in a Central Excise notification. The intention of the government is that the genuine exporters should be benefited and benefits to those who misuse such benefits should not be allowed. However, certain times, the genuine exporters also are subjected to some lengthy procedures. The main verification the government wants to do, is whether the goods are properly exported and corresponding foreign exchange is received or not. When these conditions are fulfilled there shall not be any problem for the exporters to gain the benefits. But, again here, the genuine exporters are subjected to lengthy procedures to claim the rebate of excise duty paid. Firstly, an application for rebate is to be filed at the jurisdictional division office of Central Excise and also the exporters have to submit the same in online (ACES). After the necessary verification is done at division office, the application is sent to jurisdictional Central Excise Range office for further verification. After proper verification is done at the jurisdictional Central Excise Range office the application is sent back to the division office. After the verification is done at the Range office, the officials of the division office send this application to pre-audit department at Commissionerate. After proper verification is done at the audit department, this application is sent back to the division office. Subsequently this application is produced to the jurisdictional Deputy/Assistant Commissioner of Central Excise for writing the cheque and subsequently hand-over the same to the exporters. This procedure is quite time consuming and the exporter has to run to every department to move the file. In the case of duty drawback for physical exports the amount is directly remitted to the bank based on the shipping bill and the Bank Realisation Certificate (BRC). The same procedure similar to drawback on physical exports may be followed in this rebate of excise duty also. This avoids unnecessary wastage of time and also avoids direct contacts with the exporters. However, for misusers the government has already enacted tough law and the genuine exports will reap the legitimate benefits.

4. Benefits under Deemed Exports-EXIM Policy.

We draw your kind attention to Chapter 8 of the erstwhile EXIM Policy for the year 2009-2014. As per this chapter Deemed Export Drawback benefits are available to domestic Capital Goods manufacturers who supply Capital Goods to Export Promotion Capital Goods [EPCG] licence holders. The benefits of Drawback are admissible as per Column ‘B’ of All Industry Rate of Duty Drawback Schedule of the FOB value of exports, as mentioned in the Drawback schedule irrespective of the fact whether Cenvat Credit is availed or not. The new EXIM policy has been introduced during the month of April, 2015. Several changes are made in the new EXIM policy 2015-20.Chapter 8

Page 17 of 26

covering Deemed Exports under the erstwhile EXIM policy is being reintroduced as Chapter 7 in the new EXIM policy 2015-20. The main objective of the new EXIM policy for the period 2015-20 is to provide level playing field to domestic manufacturers in certain specified cases. No All Industry Rates of Drawback is allowed under Column ‘B’ of All Industry Rates of Duty Drawback schedule for deemed exports if Cenvat Credit is availed and implies that the units covered under Deemed Exports have to apply for Brand Rate of Drawback for the Basic Customs Duty portion. A new Para 7.06 is introduced under Chapter 7 -Deemed Exports benefits. ‘Para 7.06 Conditions for refund of deemed export drawback’ reads as under: “Supplies will be eligible for deemed export drawback as per para 7.03 (b) of

FTP, as under:

(a) In case CENVAT credit / rebate has not been availed on the inputs

input services, by the supplier of goods, then, benefit as per Column ‘A’ of All

Industry Rate of Duty Drawback Schedule shall be admissible.

(b) If CENVAT credit / rebate has been availed by the supplier of goods,

on inputs / input services, then, no Drawback shall be admissible as per

Column ‘B’ of All Industry Rate of Duty Drawback Schedule. However, in

such cases, Basic Customs Duty paid can be claimed as Brand Rate of

Duty Drawback based upon submission of documents evidencing actual

payment of duties”

The sub para (b) of para 7.06 of the New EXIM policy states that if Cenvat

facility is availed Column ‘B’ of All Industry Rates of Duty Drawback

schedule implies that no All Industry Rates of Drawback is allowed and the

units covered under Deemed Exports have to apply for Brand Rate of

Drawback for the Basic Customs Duty portion.

This system of filing Brand Rate application is quite complicated not only for

Trade and Industry but also for the DGFT department.

For example, every month, we are raising 300 to 400 invoices and supplying

our machines to different EPCG licence holders throughout India. Every

Machine having different specifications and hundreds of imported

components are used in the manufacturing of these machines. Just imagine,

we have to file around 300 to 400 applications every month for fixation of

Brand Rate of Drawback and thousands of copies of documents are to be

enclosed for each application for evidencing the proof of actual payment of

duties. For this, unnecessarily we have to employ more staffs and the

salaries we pay may exceed the benefits we get.

Page 18 of 26

This is not a healthy amendment. The work at Regional Joint Director

General of Foreign Trade offices also increase tremendously because of

filing these Brand Rate applications.

In order to simplify the procedures and documentation All Industry Rates of duty drawback are fixed by the Government. All Industry Rates of Duty Drawback are fixed and reviewed by the Government annually, taking in to account the budgetary changes. The rates are revised by the government wherever necessary after taking into account the changes in the rates of duty and tax incidence of Customs, Central Excise duties and Service Tax and also variation in the prices of various inputs and rawmaterials used in the manufacture of export products. The All Industry Rates of Drawback specified in the Drawback schedule Column A- CENVAT credit has been availed and Column B- CENVAT credit has not been availed are allowed subject to the notes and conditions stated as per Notification No.110/2014- Cus. (N.T) dated 17-11-2014 issued by the Ministry of Finance, Government of India (Photocopy enclosed for your reference).

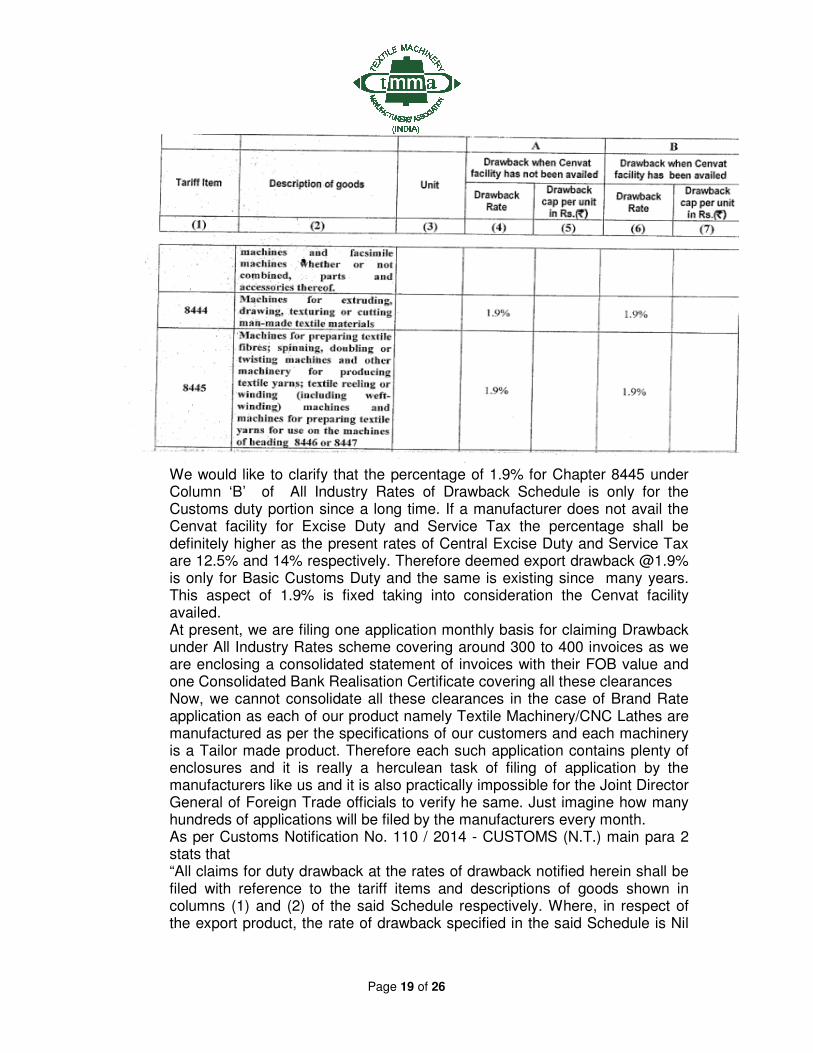

In one of the Notes and Conditions of the above notification, in Condition No.7 it is stated that: “The figures shown under the drawback rate and drawback cap appearing below the column “Drawback when Cenvat facility has not been availed” refer to the total drawback (customs, central excise and service tax component put together) allowable and those appearing under the column “Drawback when Cenvat facility has been availed” refer to the drawback allowable under the customs component. The difference between the two columns refers to the central excise and service tax component of drawback. If the rate indicated is the same in both the columns, it shall mean that the same pertains to only customs component and is available irrespective of whether the exporter has availed of Cenvat or not”. The All Industry Rates of Drawback Schedule has the following columns.

Page 19 of 26

We would like to clarify that the percentage of 1.9% for Chapter 8445 under Column ‘B’ of All Industry Rates of Drawback Schedule is only for the Customs duty portion since a long time. If a manufacturer does not avail the Cenvat facility for Excise Duty and Service Tax the percentage shall be definitely higher as the present rates of Central Excise Duty and Service Tax are 12.5% and 14% respectively. Therefore deemed export drawback @1.9% is only for Basic Customs Duty and the same is existing since many years. This aspect of 1.9% is fixed taking into consideration the Cenvat facility availed. At present, we are filing one application monthly basis for claiming Drawback under All Industry Rates scheme covering around 300 to 400 invoices as we are enclosing a consolidated statement of invoices with their FOB value and one Consolidated Bank Realisation Certificate covering all these clearances Now, we cannot consolidate all these clearances in the case of Brand Rate application as each of our product namely Textile Machinery/CNC Lathes are manufactured as per the specifications of our customers and each machinery is a Tailor made product. Therefore each such application contains plenty of enclosures and it is really a herculean task of filing of application by the manufacturers like us and it is also practically impossible for the Joint Director General of Foreign Trade officials to verify he same. Just imagine how many hundreds of applications will be filed by the manufacturers every month. As per Customs Notification No. 110 / 2014 - CUSTOMS (N.T.) main para 2 stats that “All claims for duty drawback at the rates of drawback notified herein shall be filed with reference to the tariff items and descriptions of goods shown in columns (1) and (2) of the said Schedule respectively. Where, in respect of the export product, the rate of drawback specified in the said Schedule is Nil

Page 20 of 26

or is not applicable, the rate of drawback may be fixed, on an application by an individual manufacturer or exporter in accordance with the said rules…” Therefore, as per he above Customs Notification the drawback applications should be filed as per All Industry Rates of drawback wherever All Industry Rates are available in the Drawback Schedule. Therefore, we shall be glad if you could interfere at this stage and recommend the concerned ministry to make suitable amendments in Para 7.06 (b) of the new EXIM Policy for the period 2015-20 by restoring granting All Industry Rate of Drawback as per column ‘B’ of Drawback Schedule for deemed exports also as like granting All Industry Rate of Drawback for physical exports instead of filing separate applications for Brand Rate fixation.

5. Exhibitions Abroad:

At present majority of Capital Goods manufacturers in India participate in exhibitions conducted in different countries in the world. As you are aware, since these Capital Goods are to be installed at such exhibitions, the Capital Goods manufacturers incur huge expenditure because of such participation. The exporters and such manufacturers have to incur huge expenses such as rent, salary, freight, exhibition expenses etc. Such expenses are quite costly since the amounts are paid in foreign currency. This adds to the cost of manufacture. Moreover Service Tax @ 12.5% is levied on such expenses which further increases the cost. Therefore, under such circumstances wherever the exporters participate in such exhibitions a subsidy, covering such expenses by way of percentage should be given to participants so that more exporters and manufacturers participate in such exhibitions. Moreover global logistic cost increase for participating in the Asia Oceanic region and other regions like Europe, etc. The participation in exhibitions in neighboring countries like Bangladesh, Pakistan, Sri Lanka, Nepal etc. the logistic cost is cheaper when compared to participation in far off countries as the exporters have to bear all these expenses. Such participation requires Government assistance. This will enhance the export capacities of small scale manufactures. Even the large scale exporters can fix a competitive price for their products.

6. New Markets:

In today’s developing economies throughout the world, each country is looking for the sources where they can get their required inputs and Capital Goods. Many of the countries will be looking for imports of Capital Goods. Many of the Capital Goods manufacturers in India, sometimes, will be unaware of the requirements of such countries. Such new markets are to be developed. In order to develop such new markets the exporters have to make study and spend huge amounts to establish such markets and earn good amount of foreign exchange for the country. Under such circumstances the government should come forward in extending its help in identifying such markets and compensate the exporters who incur huge expenses for identifying new markets.

7. Export Profit:

Page 21 of 26

Weighted deduction should be provided while dealing with the export profit

and this should be similar to the provisions given for Research and

Development expenses. Export profits should not be subjected to any tax.

This will help the domestic exporters to compete in the international market

where price is an important factor.

CENTRAL EXCISE

8. Inter Unit Transfers.

Majority of the units have their Units or operate thro their sister Units in the

same city. The Units are located at different geographical positions in the

same city. Every time when the consignments are to be cleared excise duty

has to be paid for such inter unit transfers. The Central Excise department

raises unnecessary disputes with regard to valuation of such inter unit

transfers even though they are revenue neutral as tax paid at one unit can be

availed as Cenvat credit at the other Unit. They issue show cause notices

indiscriminately and it takes several years to come out of it. Therefore inter

Unit transfers any be exempted or as we have in Service tax one licence may

be issued covering all the Units which have 21entralized accounting system

and a common Balance Sheet. This avoids most of the litigation. Cenvat credit

should be availed at one unit just like service tax and from there the debits

can be made in the Cenvat credit towards the clearances at the other units

under this category. Such an amendment helps both the Assessee and the

Revenue and the middlemen like advocates and consultants will be kept at

distance. Even exploitation of small and innocent assessees can be avoided.

This will be a great advantage to the trade. However, we insist that a tough

legislation has to be made for tax evaders when such a system is introduced.

Further, suitable clarifications should be issued in the present rules so that

Show Cause Notices are not served where the cases are revenue neutral. This

aspect has been clearly explained in very many cases by several judiciary.

As there is no impact on revenue the clearances between intern units who

have centralized accounting system and common balance sheet should be

totally exempt. A suitable amendment to this system may be made to avoid

any future complications and litigations.

* * * * *

Page 22 of 26

1. Issue of Imposition of Minimum Import Price on Iron & Steel

Recently Director General of Foreign Trade has imposed minimum import price (MIP) on iron and steel under chapter 72 of ITC (HS), 2012 as USD 560/ MT for sheets of flat rolled products (HS code 72091620).

Here we would like to cite the case of one of our esteemed members, Lakshmi Machine Works Limited, to present how big the impact on their competitiveness in the Global market is? The same is true for others as well.

They approximately import 900 MT of steel sheets monthly @ USD 415/ MT. With the present increase in duty the rate applicable would be @ USD 560/ MT the impact their end product shall be very high in the global market.

Moreover the domestic manufacturers’ also recently increased the steel sheet prices by Rs. 5000/ MT after MIP announcement. Due to this increase the domestic raw materials price is higher than their imported price.

Due to imposition of MIP on iron and steel the impact on their product is very high and leads to un-competitiveness in the global market. It also affects our ambitious national program ‘MAKE IN INDIA’.

Hence we request you to withdraw the minimum import price on iron and steel and decrease in basic customs duty on aluminium products.

2. Issue of mandatory registration under Steel & Steel Products (Quality Control) Order 2015 and Steel and Steel Products (Quality Control) (Amendment) Order, 2016 for import of raw material steel wire rods to manufacture Metallic Card Clothing wire A recent order issued on 17th March 2016 by Ministry of Steel vide “Steel and Steel Products (Quality Control) Order, 2016, is acting to the detriment of one of the important industry segments of textile engineering industry. Here we would like to cite the case of one of our esteemed members, Lakshmi Card Clothing Mfg. Co. Pvt. Ltd. (LCC), who is the largest manufacturer & exporter of Metallic Card Clothing Equipment in India. They import following 5.50mm dia steel wire rods form Europe and Japan for manufacturing metallic card wire used in Carding Machines in the textile mills. 1. Hot Rolled High Carbon Steel wire rods, Grade: C60 (HS Code # 72139990) 2. High Carbon Steel wire rods, Grade: 75Mn4 (HS Code # 72139990) 3. Alloy Steel Wire rods, Grade: 88MnCrW5 (HS Code # 72279090) 4. Alloy Steel Wire rods, Grade: G4 (HS Code # 72279090) These wire rods are critical raw materials for the manufacture of hi quality card clothing wires. As these are not produced by any Indian steel company, LCC needs to import the above wire rods annually. The card clothing is an essential item of component for carding machine important for yarn making process.

Page 23 of 26

However considering the ‘Make in India’ initiative, LCC had approached the following domestic steel companies in June 2015 for supplying above wire rods as raw material to replace the imports. 1. JSW Steel Limited vide letter no. RMP/320/2015 dated 20-06-2015 2. Essar Steel India Limited vide letter no. RMP/322/2015 dated 20-06-2015 3. Mukand Limited vide letter no. RMP/318/2015 dated 20-06-2015 4. Kalyani Carpenter Special Steels Ltd vide letter no. RMP/321/2015 dated 20-06-2015 5. Usha Martin Limited vide letter no. RMP/319/2015 dated 20-06-2015 But there was no response received from these companies so far. Now, as per Ministry of Steel’s order vide “Steel and Steel Products (Quality Control) Order, 2016, fifteen more products are covered under mandatory Bureau of Indian Standards (BIS) certification. Under Serial Number 12 of the above order, it is indicated that Mild Steel Wire Rods for general engineering purpose, IS7887 standard, HS Code Numbers 72139990 and 72279090, now needs mandatory BIS certification for imports from 18th March 2016. This is an unnecessary hurdle for their business. Therefore in this connection LCC took the matter up with BIS, New Delhi office vide LCC’s letter No. RMP/455/2016 dated 3rd February 2016, informing that the wire rod imported by them under HS code # 72139990 and 72279090 are not Mild Steel Wire Rod for general engineering purpose and these products should be exempted from mandatory BIS certification. But we regret to inform you that BIS have not taken any action in this regard. Hence, we request you to take-up the matter with the concerned departments & officials to resolve the matter at the earliest. It will help the industry run the production without interruption.

Page 24 of 26

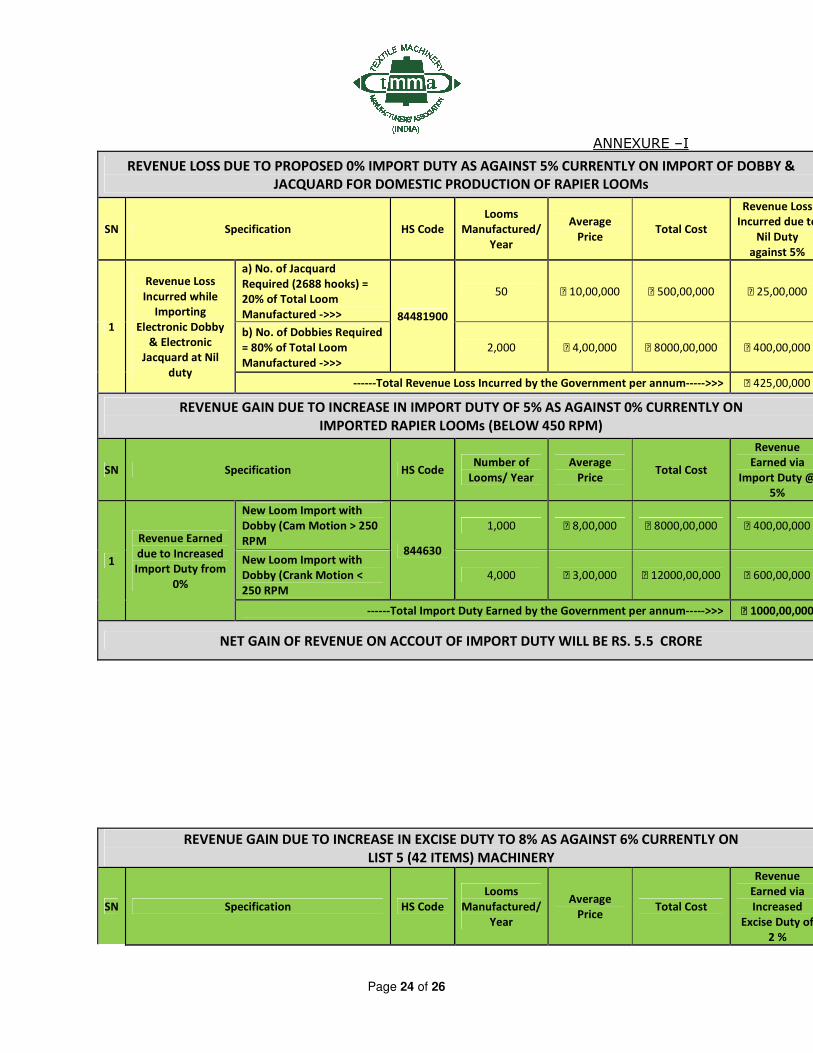

ANNEXURE –I

REVENUE LOSS DUE TO PROPOSED 0% IMPORT DUTY AS AGAINST 5% CURRENTLY ON IMPORT OF DOBBY &

JACQUARD FOR DOMESTIC PRODUCTION OF RAPIER LOOMs

SN Specification HS Code

Looms

Manufactured/

Year

Average

Price Total Cost

Revenue Loss

Incurred due to

Nil Duty

against 5%

1

Revenue Loss

Incurred while

Importing

Electronic Dobby

& Electronic

Jacquard at Nil

duty

a) No. of Jacquard

Required (2688 hooks) =

20% of Total Loom

Manufactured ->>> 84481900

50 ₹ 10,00,000 ₹ 500,00,000 ₹ 25,00,000

b) No. of Dobbies Required

= 80% of Total Loom

Manufactured ->>>

2,000 ₹ 4,00,000 ₹ 8000,00,000 ₹ 400,00,000

------Total Revenue Loss Incurred by the Government per annum----->>> ₹ 425,00,000

REVENUE GAIN DUE TO INCREASE IN IMPORT DUTY OF 5% AS AGAINST 0% CURRENTLY ON

IMPORTED RAPIER LOOMs (BELOW 450 RPM)

SN Specification HS Code Number of

Looms/ Year

Average

Price Total Cost

Revenue

Earned via

Import Duty @

5%

1

Revenue Earned

due to Increased

Import Duty from

0%

New Loom Import with

Dobby (Cam Motion > 250

RPM 844630

1,000 ₹ 8,00,000 ₹ 8000,00,000 ₹ 400,00,000

New Loom Import with

Dobby (Crank Motion <

250 RPM

4,000 ₹ 3,00,000 ₹ 12000,00,000 ₹ 600,00,000

------Total Import Duty Earned by the Government per annum----->>> ₹ 1000,00,000

NET GAIN OF REVENUE ON ACCOUT OF IMPORT DUTY WILL BE RS. 5.5 CRORE

REVENUE GAIN DUE TO INCREASE IN EXCISE DUTY TO 8% AS AGAINST 6% CURRENTLY ON

LIST 5 (42 ITEMS) MACHINERY

SN Specification HS Code

Looms

Manufactured/

Year

Average

Price Total Cost

Revenue

Earned via

Increased

Excise Duty of

2 %

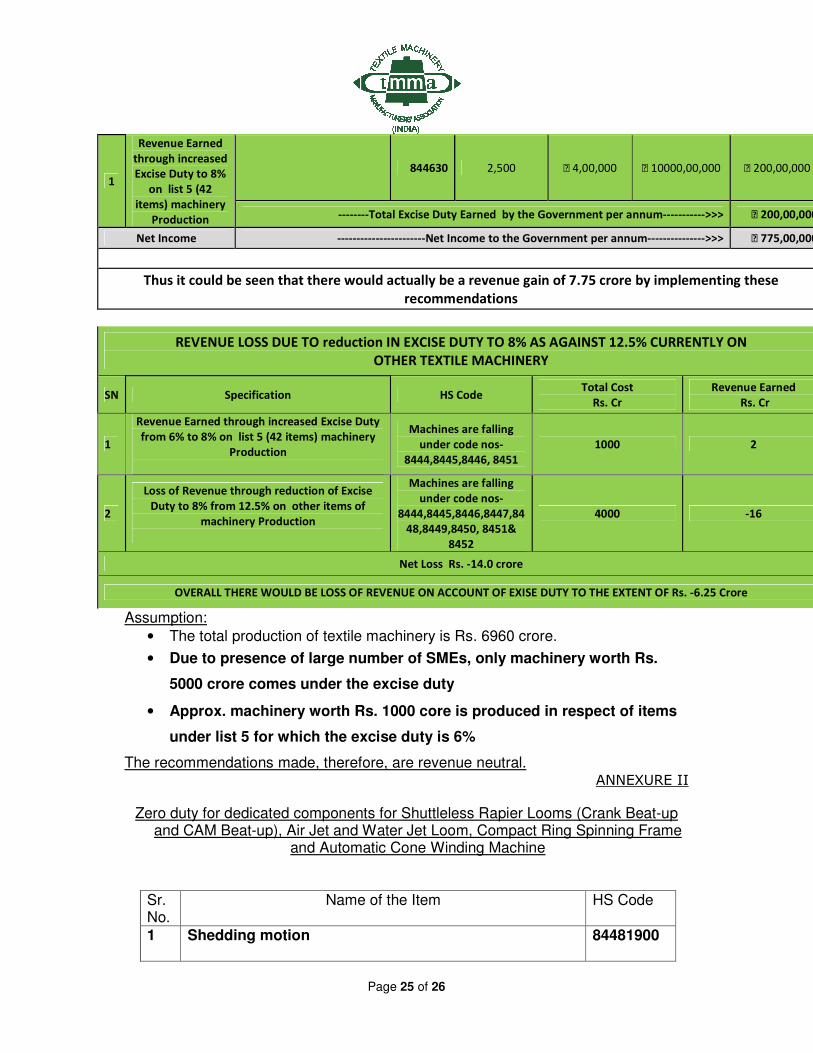

Page 25 of 26

1

Revenue Earned

through increased

Excise Duty to 8%

on list 5 (42

items) machinery

Production

844630 2,500 ₹ 4,00,000 ₹ 10000,00,000 ₹ 200,00,000

--------Total Excise Duty Earned by the Government per annum----------->>> ₹ 200,00,000

Net Income -----------------------Net Income to the Government per annum--------------->>> ₹ 775,00,000

Thus it could be seen that there would actually be a revenue gain of 7.75 crore by implementing these

recommendations

REVENUE LOSS DUE TO reduction IN EXCISE DUTY TO 8% AS AGAINST 12.5% CURRENTLY ON

OTHER TEXTILE MACHINERY

SN Specification HS Code Total Cost

Rs. Cr

Revenue Earned

Rs. Cr

1

Revenue Earned through increased Excise Duty

from 6% to 8% on list 5 (42 items) machinery

Production

Machines are falling

under code nos-

8444,8445,8446, 8451

1000 2

2

Loss of Revenue through reduction of Excise

Duty to 8% from 12.5% on other items of

machinery Production

Machines are falling

under code nos-

8444,8445,8446,8447,84

48,8449,8450, 8451&

8452

4000 -16

Net Loss Rs. -14.0 crore

OVERALL THERE WOULD BE LOSS OF REVENUE ON ACCOUNT OF EXISE DUTY TO THE EXTENT OF Rs. -6.25 Crore

Assumption:

• The total production of textile machinery is Rs. 6960 crore.

• Due to presence of large number of SMEs, only machinery worth Rs.

5000 crore comes under the excise duty

• Approx. machinery worth Rs. 1000 core is produced in respect of items

under list 5 for which the excise duty is 6%

The recommendations made, therefore, are revenue neutral. ANNEXURE II

Zero duty for dedicated components for Shuttleless Rapier Looms (Crank Beat-up and CAM Beat-up), Air Jet and Water Jet Loom, Compact Ring Spinning Frame

and Automatic Cone Winding Machine

Sr. No.

Name of the Item HS Code

1 Shedding motion

84481900

Page 26 of 26

• CAM Dobby, mechanical or electronic

• Jacquard mechanical or electronic (600 hooks and above)

2 Compact Spinning Attachment 84483990

3 Automatic Yarn Splicers for Automatic Cone Winders 84483290 4 Spindle Motor for Automatic Cone Winders 84483290 5 Grooved Winding Drums for Automatic Cone Winders 84483290

Date : 13.9.2016 Sc/Sr/Sa:

---------------------------------------------------------------------------------------------------------------------