Technological Competition and Strategic Alliances · PDF fileTechnological Competition and...

60

Technological Competition and Strategic Alliances * Kai Li Sauder School of Business University of British Columbia 2053 Main Mall, Vancouver, BC V6T 1Z2 604.822.8353 [email protected] Jiaping Qiu DeGroote School of Business McMaster University 1280 Main Street West, Hamilton, ON L8S 4M4 905.525.9140 [email protected] Jin Wang School of Business and Economics Wilfrid Laurier University 75 University Avenue West, Waterloo, ON N2L 3C5 519.884.0710 ext. 2660 [email protected] First version: August, 2014 This version: September, 2014 Abstract Using a large unique patent-strategic alliance dataset over the period 1990 to 2004, we first show that firms faced with greater technological competition are more likely to form alliances. Technological competition is captured by a cosine similarity measure between a firm’s own patent output and the patent output of all other firms in the economy. We further show that alliances lead to more patents afterwards at both client and partner firms, especially for partner firms faced with greater technological competition. Finally, we show that related patents increase significantly at both client and partner firms, whereas innovative efficiency and the productivity of individual inventors increase significantly only at partner firms. Our results are robust to endogeneity concerns. We conclude that technological competition is an important impetus for redrawing the boundaries of the firm in order to accelerate corporate innovation. Keywords: innovation, patents, R&D expenditures, strategic alliances, technological competition, technological overlap JEL classification: G34, O32 * We thank Steve Dimmock, Chuan Yang Hwang, Nengjiu Ju, Roger Loh, Ting Xu, and seminar participants at Carleton University, Nanyang Technological University, Shanghai Advanced Institute of Finance, Singapore Management University, and Wilfrid Laurier University for helpful comments. We also thank Andriy Bodnaruk for providing data on combined reporting and Alice Guo for excellent research assistance. We acknowledge financial support from the Social Sciences and Humanities Research Council of Canada (SSHRC). Li acknowledges financial support from the Sauder exploratory research grant program. All errors are our own.

Transcript of Technological Competition and Strategic Alliances · PDF fileTechnological Competition and...

Technological Competition and Strategic Alliances*

Kai Li Sauder School of Business

University of British Columbia 2053 Main Mall, Vancouver, BC V6T 1Z2

604.822.8353 [email protected]

Jiaping Qiu

DeGroote School of Business McMaster University

1280 Main Street West, Hamilton, ON L8S 4M4 905.525.9140

Jin Wang School of Business and Economics

Wilfrid Laurier University 75 University Avenue West, Waterloo, ON N2L 3C5

519.884.0710 ext. 2660 [email protected]

First version: August, 2014 This version: September, 2014

Abstract

Using a large unique patent-strategic alliance dataset over the period 1990 to 2004, we first show that firms faced with greater technological competition are more likely to form alliances. Technological competition is captured by a cosine similarity measure between a firm’s own patent output and the patent output of all other firms in the economy. We further show that alliances lead to more patents afterwards at both client and partner firms, especially for partner firms faced with greater technological competition. Finally, we show that related patents increase significantly at both client and partner firms, whereas innovative efficiency and the productivity of individual inventors increase significantly only at partner firms. Our results are robust to endogeneity concerns. We conclude that technological competition is an important impetus for redrawing the boundaries of the firm in order to accelerate corporate innovation.

Keywords: innovation, patents, R&D expenditures, strategic alliances, technological competition, technological overlap

JEL classification: G34, O32

* We thank Steve Dimmock, Chuan Yang Hwang, Nengjiu Ju, Roger Loh, Ting Xu, and seminar participants at Carleton University, Nanyang Technological University, Shanghai Advanced Institute of Finance, Singapore Management University, and Wilfrid Laurier University for helpful comments. We also thank Andriy Bodnaruk for providing data on combined reporting and Alice Guo for excellent research assistance. We acknowledge financial support from the Social Sciences and Humanities Research Council of Canada (SSHRC). Li acknowledges financial support from the Sauder exploratory research grant program. All errors are our own.

Technological Competition and Strategic Alliances

Abstract

Using a large unique patent-strategic alliance dataset over the period 1990 to 2004, we first show that firms faced with greater technological competition are more likely to form alliances. Technological competition is captured by a cosine similarity measure between a firm’s own patent output and the patent output of all other firms in the economy. We further show that alliances lead to more patents afterwards at both client and partner firms, especially for partner firms faced with greater technological competition. Finally, we show that related patents increase significantly at both client and partner firms, whereas innovative efficiency and the productivity of individual inventors increase significantly only at partner firms. Our results are robust to endogeneity concerns. We conclude that technological competition is an important impetus for redrawing the boundaries of the firm in order to accelerate corporate innovation.

Keywords: innovation, patents, R&D expenditures, strategic alliances, technological competition, technological overlap

JEL classification: G34, O32

1

1. Introduction

Corporate innovation is a key factor in determining firm comparative advantages, competitiveness, and

long-term productivity growth. In this paper, we examine the relation between one organizational form—

strategic alliances—and corporate innovation in the face of technological competition.

Strategic alliances are long-term contracts between legally distinct organizations, typically a small

entrepreneurial firm (partner) and a large established firm (client), that provide for the sharing of the costs

and benefits of mutually beneficial activities (Robinson, 2008). According to Jensen and Meckling (1992),

alliances are the so-called “network organization” that lies between arm’s length market transactions and

integrated hierarchical organization structures, blurring the boundaries of the firm. Robinson (2008) notes

that since 1985, the number of alliance transactions surpassed that of mergers and acquisitions (M&As).

More importantly, while alliances frequently take place in a broad range of industries, they tend to cluster

in risky, high-R&D settings (Robinson and Stuart, 2007). Given the importance of alliances as an

organizational form to facilitate corporate R&D, it is crucial to understand the role of competition in the

technological space in the formation of alliances and their joint impact on corporate innovation outcome.

This paper fills a void in the literature, providing new empirical evidence on the interplay among

organizational form, technological competition, and corporate innovation.

The following example illustrates some key aspects of the relation between technological

competition and strategic alliances examined in this paper. Incyte Corporation is a biotech company

developing inhibitors for JAK, a causative factor in majority of myeloproliferative disorders that affect the

levels of blood cells in human body. Its JAK inhibitor (INCB18424) entered phase III trial in July 2009. In

October 2009, another biotech company YM BioSciences initiated a phase I/II trial of a new JAK inhibitor

(CTYT387) that had a key potential advantage over INCB18424 in improving patients’ anemia symptoms.

In November 2009, Incyte formed a strategic alliance with the pharmaceutical giant Novartis to jointly

develop INCB18424. Under the terms of the alliance agreement, Novartis was responsible for development

of the drug outside of the US, while Incyte retained rights in the US. In exchange for these rights, Incyte

received an upfront payment of $150 million and was eligible for up to a $60 million milestone payment in

the future. INCB18424 succeeded in its phase III trial and was approved by the US Food and Drug

Administration (FDA) for the treatment of intermediate or high-risk myelofibrosis in November 2011.

2

The above example highlights one important consideration in firms’ decisions to form alliances—

the presence of fierce technological competition faced by both the two small biotech companies and the

large pharmaceutical company. In November 2009 when Incyte and Norvatis formed an alliance, Incyte

faced competition from YM BioSciences Inc. in advancing INCB18424, the first JAK inhibitor that reached

the pivotal phase III trial. In the meantime, many large pharmaceutical companies including Novartis face

fierce competition from biotech companies and the threat of “patent cliff”—a term signifying the sharp

drop-off in revenues from blockbuster drugs that face generic competition once their patents expire. By

joining forces with the pharmaceutical giant Novartis, Incyte was able to accelerate its innovation capacity

and received the FDA approval ahead of its competitor. This example illustrates that alliances are an

important vehicle through which firms gain access to knowledge and capacities outside their own

boundaries in order to accelerate their innovation effort; and most importantly, the alliance decision and its

success hinge on technological threats and opportunities.

In this paper, we argue that strategic alliances, as an organizational form fostering commitment to

long-term risky investments (Robinson, 2008), naturally arise when firms face intensive technological

competition. When faced with technological competition, the speed of innovation is crucial for firms to

succeed in a technological race. Close collaboration via alliances facilitates the transferring of existing

know-how and the pooling of specialized knowledge to generate new knowledge (Gomes-Casseres,

Hagedoorn, and Jaffe, 2006). Further, the flexibility inherent in alliances facilitates experimentation with

new ideas and new combinations of participants in the pursuit of new knowledge (Mody, 1993). Finally,

the presence of technological competition serves as an effective disciplinary device to prevent participant

firms from shirking and self-dealing, leading to better innovation outcome than cases without such

competitive pressure.

To examine whether and how technological considerations drive alliance formation, we first

develop a new measure to capture competition in the technological space and then provide large-sample

analyses on determinants of alliance formation and its impact on corporate innovation outcome. Our

empirical investigation addresses the following two questions: What is the role of technological competition

in affecting a firm’s likelihood of joining alliances? How do alliances and technological competition change

the innovation outcome of alliance participants?

3

We capture technological competition faced by an innovative firm as a cosine similarity measure

between its own patent output, measured by the number of patents across different technological classes,

and the patent output of all other firms in the economy. This cosine measure builds on the firm-to-firm

technological proximity measure of Jaffe (1986). The higher value is this cosine measure, the greater is the

extent of overlap in technological innovation between a firm and all other firms in the economy. Intuitively,

this measure captures two key features of technological competition: threats and opportunities. On the one

hand, greater overlaps between a firm’s patent portfolio and the aggregate patent portfolio of all other firms

in the economy indicate that this firm’s technologies are faced with greater threats from other firms’ similar

technologies and thus have a higher obsolescence risk. On the other hand, greater overlaps with aggregate

innovative activities in the economy suggests that this firm’s technologies attracts interest from other firms

and thus have a higher upside potential. Our cosine similarity measure captures both threats and

opportunities faced by a firm’s technologies (i.e., a greater obsolescence risk as well as a greater

opportunity), which we call technological competition. In a similar vein, Hoberg, Phillips, and Prabhala

(2014) use new product overlaps between a firm and its industry peers to capture product market threats.

Using a large unique patent-strategic alliance dataset over the period 1990 to 2004, we start by

examining whether and how technological considerations are related to alliance formation. Using our new

measure of technological competition and a panel dataset of innovative Compustat firms, we first show that

technological competition faced by a firm is positively associated with the likelihood of that firm joining

an alliance. We further show that more innovative firms, as captured by both patent count and R&D

expenditures, are more likely to form alliances. In terms of the economic significance of these effects, when

increasing the measure of technological competition by one standard deviation, the number of alliances

formed per year increases by 0.12; when increasing the number of patents (in logarithms) by one standard

deviation, the number of alliances formed per year increases by 0.14; and when increasing R&D

expenditures by one standard deviation, the number of alliances formed per year increases by 0.21. Given

that the average number of alliances formed by innovative sample firms is 0.78, these effects on alliance

formation are economically significant. Using either industry- and size-matched or randomly drawn control

firms, we again show that alliance participants are faced with significantly greater technological

competition, have significantly more patents and higher R&D expenditures. Taken together, these results

suggest that technological considerations have a significant bearing on the rising popularity of alliances.

4

Next, we examine the roles of technological competition and alliances in post-alliance innovation

outcome. Following convention, we call the larger firm in a bilateral alliance as a client firm and the smaller

firm as a partner firm. Using both the difference-in-differences specification and the treatment regression

with an instrumental variable, we find that after alliance formation, innovation output of alliance

participants is significantly improved, especially for partner firms faced with greater technological

competition.

Once we establish the positive effects of technological competition and alliance on post-alliance

innovation outcome, we explore possible underlying mechanisms through which these effects take place.

We first find that both client and partner firms significantly increase their R&D expenditures after alliance

formation, supporting the view that strategic alliances provide an effective commitment mechanism for

developing risky long-term projects (Robinson, 2008). Moreover, partner firms significantly increase

innovative efficiency when faced with greater technological competition, consistent with the typical

practice in alliances that clients provide funding while partners focus on developing technologies. We then

find that related patents significantly increase at both client and partner firms after alliance formation,

suggesting effective information flows between alliance participants. We note that unrelated patents also

significantly increase at alliance partner firms (but not at client firms). Finally, using inventor-level data,

we find that the productivity of individual inventors at alliance partner firms improves significantly in the

face of technological competition, consistent with the increased innovative efficiency results. In contrast,

we do not observe any significant improvement in the productivity of individual inventors at client firms

after alliance formation. We conclude that technological competition is an important impetus for redrawing

the boundaries of the firm—forming alliances—in order to accelerate corporate innovation.

In our additional investigation, we find that technological competition does not play the same role

in the formation of joint ventures (JVs) as it does in alliance formation, nor does it have any impact on post-

JV innovation output. We offer a number of explanations for the difference in findings. First, alliances and

JVs are formed for different purposes—the former to developing new ideas while the latter to developing

and marketing new products. Second, alliances are a much more flexible organizational form that is suited

to developing new ideas, while JVs are a relatively more rigid organizational form that is costly to form

and to unwind.

5

Our paper makes a number of important contributions to the literature. First, we develop a novel

firm-level measure of technological competition that captures threats and opportunities faced by innovative

firms in the technological space. Given the crucial role of technology in our knowledge-based economy, it

is important to be able to quantify the amount of technological competition faced by individual firms,

complementing the well-established measure of product market competition (see Hoberg and Phillips, 2010

for the latest development of this measure). Like product market competition, we expect technological

competition to have important implications for corporate policies.

Second, this paper contributes to the long-standing literature on the boundaries of the firm

(Grossman and Hart, 1986; Hart and Moore, 1990; Hart, 1995). A firm can be viewed as the nexus of

contracts (Jensen and Meckling, 1976); alliances are part of the contracts that surround the firm and blur its

boundaries. Although the importance of alliances in facilitating knowledge transfer and technological

innovation has been well recognized (Chan, Kensinger, Keown, and Martin, 1997; Fulghieri and Sevilir,

2003; Gomes-Casseres et al., 2006), there is little large-sample evidence on the role of technological factors

in the formation of alliances. Robinson (2008) finds that the risk of alliance activities outside a client firm

is greater than the risk of activities that are conducted inside the firm. Bodnaruk, Massa, and Simonov

(2013) show that firms with higher quality of governance are more likely to form alliances and also are

better able to reap the benefits of alliances. While strategic alliances are a common phenomenon among

technology firms, prior studies are silent on one important question: How do technological factors affect

firms’ decisions to join alliances? Our paper fills a void in the literature by addressing this question.

Third, our study provides a fresh new perspective on the relation between competition and

innovation. The Schumpeterian theory predicts that intense product market competition deters innovation

of new entrants, as more competition accelerates the obsolescence of new technologies and hence reduces

the monopolistic rents of innovators (Aghion and Howitt, 1992; Caballero and Jaffe, 1993). However,

empirical studies mostly find a positive effect of product market competition on innovative output (Geroski,

1995; Nickell, 1996; Blundell, Griffith, and Van Reenen, 1999). To reconcile theory with empirical

evidence, recent papers emphasize competition faced by incumbent firms (e.g., Aghion, Harris, Howitt, and

Vickers, 2001; Aghion, Bloom, Blundell, Griffith, and Howitt, 2005). In these models, opportunity costs

of innovation failure faced by incumbent firms could be higher when competition is fierce, leading to a

positive relation between competition and innovative output. While most papers in this literature focus on

6

how (product market) competition affects the monopolistic rents of innovators, which in turn affects firms’

incentives to pursue innovation, our study looks at the effect of competition on innovation from a very

different perspective: How does competition affect firms’ choices of organizational forms that foster

commitment to innovation and accelerate innovation? Our findings suggest that competition affects

innovation not only through economic incentives but also through the choice of organizational forms.

Finally, this paper extends Coase’s (1937) original insight that different organizational forms have

important implications for investment performance by focusing on the relation between alliances and

corporate innovation. Prior studies including Allen and Phillips (2000), Lindsay (2008), Robinson (2008),

Hoberg and Phillips (2010), Beshears (2013), Bodnaruk et al. (2013), Bena and Li (2014), and Seru (2014)

have examined whether and how alliances, JVs, and M&As take place to address agency problems and

information asymmetry, reallocate decision rights, and combine firms’ capabilities to create synergies. A

central issue in this strand of the literature is to understand the economic implications of these changes of

firm boundaries. In this paper, our findings that one organizational form—strategic alliances—facilitates

the development of new knowledge (i.e., patents) in the face of fierce technological competition highlight

the complex relation between organizational form, technological competition, and corporate innovation.

Our results suggest that the right organizational form is crucial for firms to succeed in their innovation

effort, especially in the presence of fierce technological competition.

The rest of the paper proceeds as follows. Section 2 develops our hypotheses. Section 3 describes

the sample and key variables used in this study. Section 4 examines whether and how technological

considerations affect alliance formation. Section 5 presents innovation outcome after alliance formation

and examines the underlying mechanisms. Section 6 conducts additional investigation. Section 7 concludes.

2. Hypothesis Development

When there is great technological competition, firms are faced with a great threat of technology

obsolescence as well as a great opportunity. The speed of innovation is thus crucial for firms to succeed in

a technological race. Strategic alliances provide an effective organizational form for otherwise independent

firms to pool resources in accelerating the development of new technology. Forging an alliance enables a

firm to focus resources on its core competencies while acquiring other skills or capabilities from the market

7

place. Chan et al. (1997) note that alliances are becoming increasingly important as competitive pressures

force firms to adopt flexible and more focused organizational structures.

Alliances also offer an effective mechanism for firms to commit to technological innovation that is

characterized by a low likelihood of success but high payoffs (“longshot projects” as modeled in Robinson,

2008). Internal capital markets are prone to the practice of “winner-picking,” whereby headquarters have

incentives to divert resources to short-term projects with a greater likelihood of success but low payoffs

conditional on success. The possibility of reallocating resources ex post dis-incentivizes divisional

managers from undertaking long-term risky investment ex ante. Robinson (2008) suggests that alliances as

enforceable contracts between participant firms help resolve such an incentive problem because they

mitigate winner-picking. Such a commitment is critical when faced with great technological competition

as the consequence of diverging resource from innovation could be dire—obsolete technologies and missed

opportunities.

Finally, compared to other organizational forms such as joint ventures and acquisitions, the

flexibility inherent in alliances facilitates experimentation with new ideas and new combinations of

participants in the pursuit of new knowledge (Mody, 1993). This flexibility of alliances is particularly

valuable when technological competition intensifies and the future of innovation outcome is uncertain (e.g.,

Dixit and Pindyck, 1994; Trigeorgis, 1996; Seth and Chi, 2005).

The above discussions lead to our first hypothesis:

Hypothesis 1: Technological competition increases the likelihood of alliance formation.

Jensen and Meckling (1992) refer alliances as a network organization. They argue that such an

organizational form can add value to participant firms by aligning decision authority with decision

knowledge. In an alliance, such alignment is achieved when each participant has specific decision

responsibility allocated according to its expertise and business objective. The benefits of forming an alliance

are especially high for innovative firms because innovation requires both highly specialized knowledge and

decision authority allocated to experts equipped with such knowledge.

Further, a network organization provides participant firms with organizational flexibility, allowing

them to divest failed investments at relatively low costs. In contrast, Jensen (1993) argues that traditional

8

corporate form destroys value because of its inability to divest assets. The high uncertainty faced by

innovative firms further enhances the value-added from adopting an organizational form whose low

divestiture costs encourage undertaking risky investments.

On the other hand, there are also costs associated with network organizations like alliances that do

not happen in integrated firms or arm’s length transactions. These costs arise out of the potential for

opportunistic behavior by participant firms (Klein, Crawford, and Alchian, 1978; Kranton, 1996).

Innovative projects call for specialized knowledge, then it becomes difficult, if not impossible, to monitor

and control participants’ opportunistic behavior. The costs associated with opportunistic behavior are likely

to be high when alliances involve innovative projects. Ultimately, it is an empirical question whether

alliances enhance corporate innovation.

The above discussions lead to the first part of our second hypothesis:

Hypothesis 2A: Alliances lead to improved post-alliance innovation outcome.

One important advantage of forming an alliance is that participant firms can pool knowledge and

resources for pursuing a common goal. Gomes-Casseres et al. (2006) note that closer collaboration via

alliances than the arm’s length market transaction facilitates not only the transferring of existing know-how

but also the pooling of specialized knowledge to generate new knowledge. Thus, if an alliance does improve

post-alliance innovation outcome of participant firms, we would expect that some of the improved

innovation outcome builds on the shared expertise of participant firms. This conjecture leads to the second

part of our second hypothesis:

Hypothesis 2B: Alliances lead to improved post-alliance innovation outcome that builds on participants’ shared expertise.

To mitigate the costs associated with a network organization, Jensen and Meckling (1992) suggest

establishing an internal control system to provide performance measurement and a reward and punishment

system to reduce opportunistic behavior. Parkhe (1993) recommend alliance participants to commit to

relationship-specific investments that are of little value outside the alliance.

We posit that technological competition provides an external solution to limit alliance participants’

opportunistic behavior. The presence of fierce technological competition, through either the threats of

9

lagging behind or the risk of missed opportunities, as our motivating example demonstrated, could serve as

an effective disciplinary device to prevent alliance participants from shirking and self-dealing and press for

efficiency improvement. Further, given that technological alliances typically have clients as capital

providers and partners as technology owners/developers, we thus expect that partners are likely to benefit

more from the positive effect of technological competition-induced alliances on their innovation outcome.

The above discussions lead to our final hypothesis:

Hypothesis 3: Technological competition strengthens the positive impact of alliances on post-alliance innovation outcome, especially for partners. In our empirical investigation, we test the above hypotheses, and also attempt to control for several

alternative explanations for why alliances take place. In the next section, we describe our sample, define

key innovation variables, and present a sample overview.

3. Sample Formation and Variable Constructions

3.1. Our Sample

We obtain data on Compustat firms’ patenting activity from the National Bureau of Economics

Research (NBER) Patent Citations Data File. This database contains detailed information on patents and

citations for US publicly-listed firms, including patent ID, patent assignee, number of citations made and

the cited patent IDs, number of citations received and the citing patent IDs, patent application year, and

patent award year (see Hall, Jaffe, and Trajtenberg, 2001 for details).

Our alliance sample comes from the Thomson Financial’s SDC database on Joint Ventures and

Strategic Alliances, which covers “agreements where two or more entities have combined resources to form

a new, mutually advantageous business arrangement to achieve predetermined objectives.” The database

contains detailed information on alliance participants and the deal announcement date. It has been used in

recent studies (e.g., Allen and Phillips, 2000; Fee, Hadlock, and Thomas, 2006; Lindsey, 2008; Boone and

Ivanov, 2012; Bodnaruk et al., 2013) given its comprehensive coverage.

Our sample period starts in 1990 because it is the first year when the data quality in the SDC

database became good. Our sample period ends in 2004 because the year 2006 is the last year when the

10

patenting information from the NBER database was available. Due to the well-known patent approval lag

between application and final award of a patent to be two to three years, the data coverage of patents in

2005-2006 was poor. For any bilateral alliance deal in our sample, we define the participant with a larger

(smaller) value of total assets as the client (partner).

Our alliance sample includes all deals where the form of deal is coded as “strategic alliance” by the

SDC. We require that: 1) the alliance involves at least one US public firm or a subsidiary to a US public

firm as covered by Compustat/CRSP; and 2) the US public firm involved is not from the financial sector

(SIC 6000-6999). These filters yield 29,981 alliances for our sample period 1990-2004.

3.2. Measuring Technological Competition

Our central idea is that technological competition-driven alliances enhance corporate innovation

output. The concept of technological competition is new so there is no off-the-shelf measure for our

purpose.

3.2.1. Definition

We capture technological competition faced by an innovative firm at a point in time as a cosine

similarity measure between its own patent output, measured by the number of patents across different

technological classes, and the similarly measured patent output of all other firms in the economy. Innovative

firms are firms with at least one awarded patent over the period 1976-2006 by the US Patent and Trademark

Office (USPTO).1 Our measure of technological competition captures technological threats and uncertainty

that a firm faces, similar to the product market fluidity measure of Hoberg et al. (2014) capturing

competitive threats in the product market.

To construct the variable, we first capture the scope of innovation activity through patent output of

firm i using the technology vector Si,t = (si,t,1, ..., si,t,K), and the scope of innovation activity through patent

output of all other firms in the economy using the aggregate technology vector S-i,t = (s-i,t,1, ..., s-i,t,K). The

subscript k(1,K) is the technology class index.2 The scalar si,t,k (s-i,t,k) is the ratio of the number of awarded

patents to firm i (all other firms in the economy except firm i) in technology class k with application years

1 About half of the Compustat firms over the period 1976-2006 are innovative based on our definition. 2 The US Patent and Trademark Office classifies each patent into 426 technology classes.

11

from t-2 to t (in year t) to the total number of awarded patents to firm i (all other firms in the economy)

applied over the same three-year period (the same year t).

Our technological competition measure is then computed as

,S , S ,

S , S , S , S ,

.

(1)

This cosine measure ranges from zero to one. The higher value is this cosine measure, the more similar of

a particular firm’s innovation output to that of all other firms in the economy.

We believe that our measure is particularly suited to capture technological competition, which by

construction, has two important components—threats and opportunities. On the one hand, a greater overlap

with the aggregate innovative activities in the economy posts threats to the firm’s existing patents,

increasing their obsolescence risk. On the other hand, a firm with patents that have a greater overlap with

the aggregate innovative activities is the one that owns technologies that are of great interest to other firms,

and hence having a higher upside potential but also facing more competitive pressure. As such, our measure

of technological competition captures both threats and opportunities (i.e., greater downside risks as well as

higher upside potentials) for the technologies owned by the firm.

3.2.2. Validation from 10-K Filings

Our measure for technological competition is based on the patent portfolio of a focal firm. Given

that it is a new measure, it is important to check if this measure does capture the threats and opportunities

faced by companies in the technological space.

Firms are required to disclose potential risk factors that might adversely affect future performance

in the Management Discussion & Analysis section (MD&A, typically item 7) or in the risk factor section

(typically item 1 or item 1.A) of their 10-K filings. We examine whether firms faced with greater

technological competition based on our measure in Equation (1) are also more likely to talk about it in their

10-K filings. We employ a machine-based algorithm to search the entire text of 10-K filings for the

following keywords: technology competition, technological competition, technology competitiveness,

technological competitiveness, technology risk, technological risk, technology risks, technological risks,

technology threat, technological threat, technology threats, technological threats, technology uncertainty,

12

technological uncertainty, technology change, technological change, technology changes, technological

changes, changes in technology. We record the number of times any of the above keywords show up in 10-

K filings. As a robustness check, we also search for the above keywords specifically within the MD&A

section, the risk factors section, and the combination of these two sections.

Table 1 provides summary statistics from the above exercise. Panel A presents the mean and median

values of our technological competition measure and the four measures based on text search of the keywords

over different sections of 10-K filings. Panel B presents the correlation matrix between our technological

competition measure and the 10-K based measures. We find that firms faced with high technological

competition are more likely to talk about technological competition in their 10-K filings, not limited to the

MD&A section or the risk factors section. This exercise provides some validating evidence in support of

our measure for technological competition.

To corroborate with the machine-based search results, we randomly pick 300 firms and ask a

research assistant (without any prior knowledge of our technological competition measure) to go over their

10K filings and verify the machine-based count of the number of times any of the 15 keywords show up.

Further, we also ask the research assistant to assign a score of 0 (no competition), 1 (lowest) to 3 (highest)

to each of these 300 firms, based on personal assessment of the degree of technological competition that a

firm is faced with. The correlation between the research assistant’s scores and values of our technological

competition measure is 0.47.

3.2.3. Examples

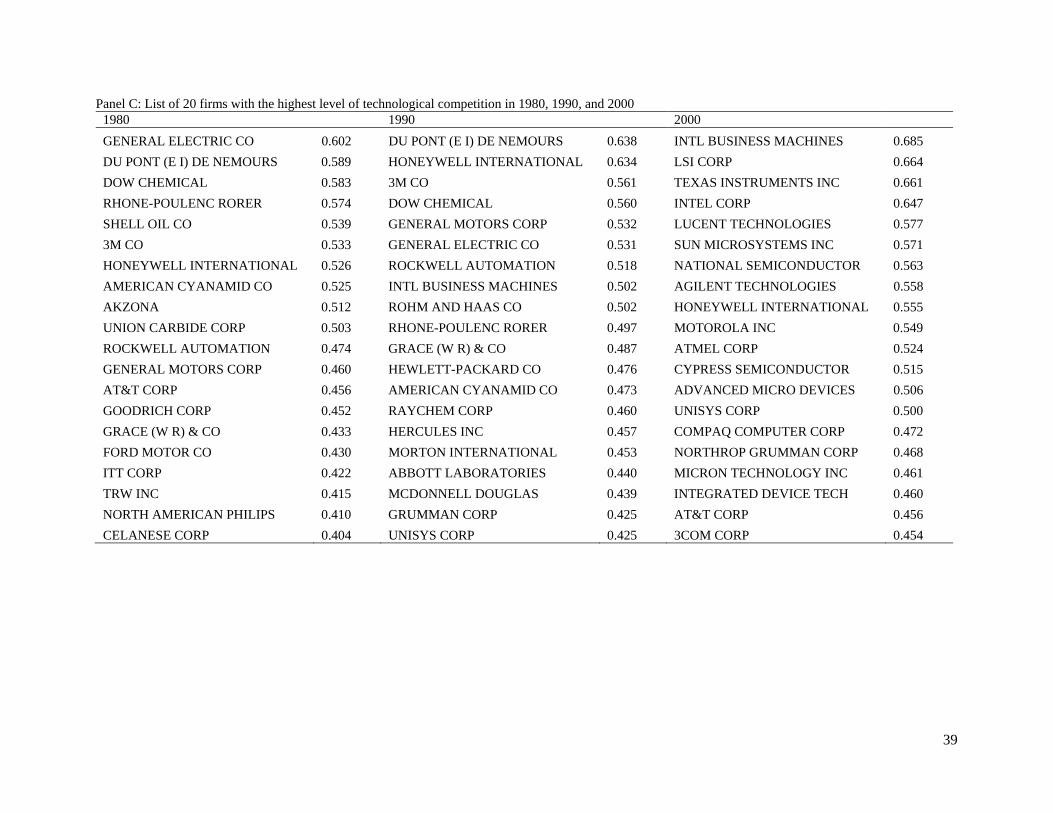

Table 1 Panel C lists the top twenty firms faced with the greatest technological competition in 1980,

1990, and 2000. We find that over the past twenty years, firms faced with the greatest technological

competition shift from manufacturing and resources to IT and computers in the last decade. Figure 1 plots

the time series of our technological competition measure averaged across innovative firms over the sample

period 1990-2004. We observe a gradual rise in the average value of technological competition until the

burst of the Internet bubble and a gradual decline after, likely due to the patent approval lag.

3.3. Summary Statistics

13

Table 2 presents the temporal distribution of alliances over our sample period 1990-2004. Panel A

presents different samples without imposing the requirement that alliance participants have at least one

patent in the NBER patent database. We show that the numbers of alliance deals peaked during the late

1990s and declined after the burst of the Internet bubble in the early 2000s. The evidence that alliances

were most active during the technological golden age around the Internet bubble is consistent with the view

that technological innovation is a key driver. We further show that there were close to 30,000 alliances

involving at least one US public firm. Over 90% of the alliances are bilateral arrangements involving at

least one US public firm or a subsidiary to a US public firm. The sample size drastically drops when we

require both alliance participants to be US public firms.

Panel B presents different samples used in our multivariate analysis after imposing the requirement

that alliance participants have at least one patent over the period 1976-2006. Comparing column (1) across

Panels A and B, we show that close to 80% of the alliances involve innovative US public firms, and over

90% of these alliances are bilateral arrangements involving at least one innovative US public firm. When

we require both alliance participants to be innovative US public firms (not a subsidiary to a US public firm

as covered in column (3)), only a fifth of the full sample (as shown in column (1)) meet the requirement. It

is clear that alliances are a common phenomenon among innovative firms that are publicly listed or

subsidiaries of publicly listed firms. Bilateral alliances with one client and one partner are the prevailing

practice.

To capture innovation output as well as the strength of intellectual property rights, we use patent

count, constructed as the year- and technology-class adjusted number of patents over the three-year period

preceding the formation of an alliance. Patents grant assignees property rights and hence clearly delineate

their contractual rights. Gans, Hsu, and Stern (2002) argue that the presence of patents reduces the

transaction costs associated with collaborative arrangements like alliances. Detailed variable definitions

and constructions can be found in Appendix 1.

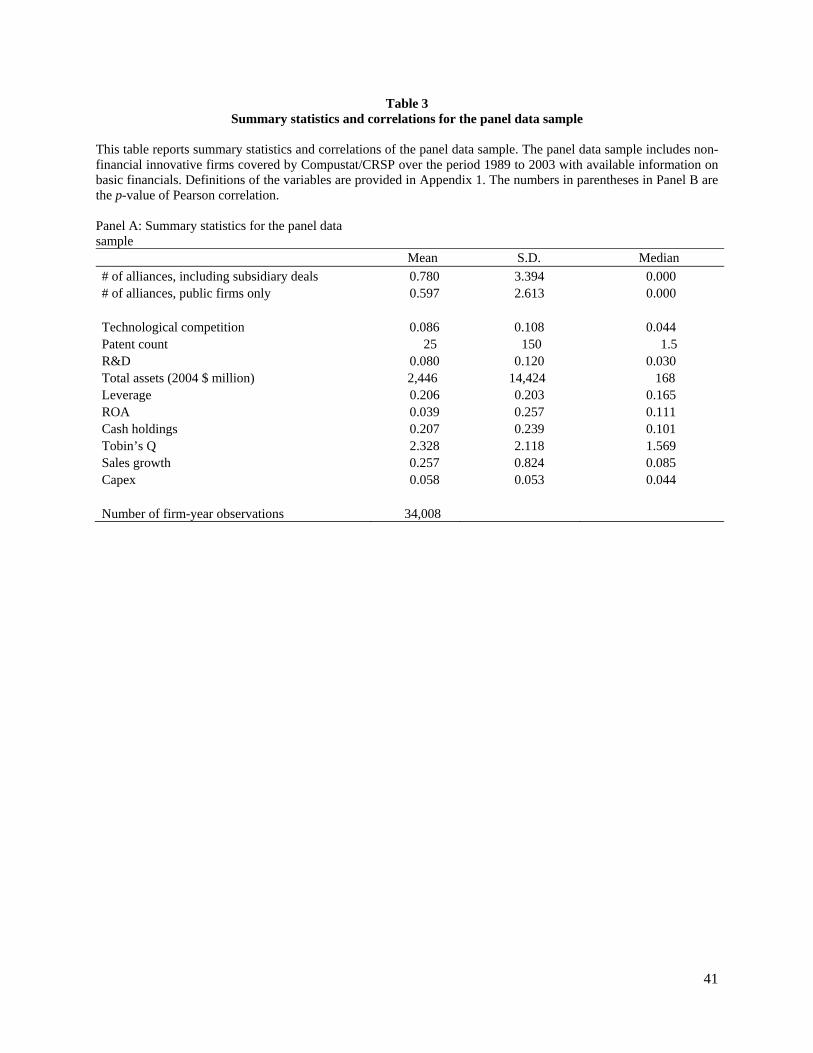

Table 3 presents the summary statistics for the panel data sample that consists of innovative non-

financial firms covered by Compustat/CRSP over the period 1989-2003. All continuous variables are

winsorized at the 1st and 99th percentiles. All dollar values are measured in 2004 dollars.

14

In Panel A, we show that on average an innovative US public firm forms 0.78 alliances every year.

Once we exclude alliances involving subsidiaries of a public firm, the average number of alliances drops to

0.60 per year. The mean (median) value of technological competition is 0.09 (0.04). The mean (median)

number of patents in the three-year period preceding alliance formation is 25 (1.5). The rest of firm

characteristics are typical of Compustat public firms.

In Panel B, we present pair-wise correlation coefficients. We show that there is a positive and

significant correlation between the number of alliances and technological competition. More general

examination of the correlation matrix suggests little problem of multicolinearity. Since biases due to omitted

variables in univariate correlations can mask the true relations between the variables, we rely on

multivariate analysis to examine the factors associated with alliance formation.

4. Technological Competition and Strategic Alliances

Our empirical investigation in this section helps answer the following question: What is the role of

technological competition in affecting a firm’s likelihood of joining alliances?

4.1. Panel Data Evidence

To test our first hypothesis relating alliance formation to technological competition, we look at the

relation between a firm’s measure of technological competition and the number of alliances it enters in the

subsequent year. We estimate a set of Tobit regressions:

1 # , , , & ,

, , . (2)

The dependent variable is the logarithm of one plus the number of alliances a firm enters in year t. The set

of firm innovation characteristics includes technological competition, patent count (in logarithms), and

R&D expenditures. Other firm characteristics to explain alliance formation following prior literature (e.g.,

Gomes-Casseres et al., 2006; Boone and Ivanov, 2012; Bodnaruk et al., 2013) include firm size (the

logarithm of total assets), leverage, ROA, cash holdings, Tobin’s Q, sales growth, and capital expenditures.

To control for industry- and time-clustering in alliances, we include both industry (defined by the two-digit

15

SIC codes) and year fixed effects. For this analysis, we employ the panel data sample (as shown in Table

2) merged with the SDC’s database on Joint Ventures and Strategic Alliances to obtain the number of

alliances formed by these firms or their subsidiaries each year over the sample period 1990-2004. Table 4

presents the results.

We first show that firms faced with greater technological competition are more likely to form

alliances, consistent with our first hypothesis. When a firm’s patent portfolio is under threat, that firm is

more likely to form alliances to fend off the threat and tap into the opportunity. We then show that

innovative firms with more patents are more likely to form alliances, consistent with Gans et al. (2002) who

argue that the strength of intellectual property rights is important for alliances. We further show that firms

with more R&D expenditures are also more likely to form alliances.

In terms of the economic significance of these innovation variables on the number of alliances

formed (based on column (1) estimates), when increasing the measure of technological competition by one

standard deviation, the number of alliances formed per year increases by 0.12; when increasing the number

of patents (in logarithms) by one standard deviation, the number of alliances formed per year increases by

0.14; and when increasing R&D expenditures by one standard deviation, the number of alliances formed

per year increases by 0.21. Given that the sample average number of alliances formed is 0.78, the effects

of these technological factors on alliance formation are economically significant.

Table 4 also provides some other interesting results. We find that large firms, firms with low

leverage, high cash holdings, high Tobin’s Q, and fast sales growth are more likely to form alliances. We

conclude that alliance participants are characterized as large fast-growing innovative firms faced with great

technological competition.

4.2. Matching Firm Evidence

The pros of using the panel data sample is that it provides large sample evidence on the importance

of technological competition in the formation of alliances. The cons is that there are many public firms that

are totally different from alliance participants included in the analysis, raising the hurdle to reject our

hypotheses. For example, firms at different stages of the technological life cycle are included and compared.

Further, the panel data analysis in Table 4 does not differentiate alliance clients and partners.

16

To further examine whether and how technological competition affects a firm’s likelihood of

joining alliances, we follow Bena and Li’s (2014) methodology by identifying matching firms for

participants in alliance deals. For each participant of an alliance deal announced in year t, we find up to five

control firms matched by industry and size, where the industry is defined by the two-digit SIC code. We

move up to the one-digit SIC industry if we cannot identify three valid control firms at the two-digit SIC

industry level. We require a valid control firm to satisfy the following conditions: 1) it is an innovative firm

with at least one awarded patent over the period 1976-2006 (as covered by the NBER Patent Database); 2)

it shares at least one-digit SIC code with the sample firm; 3) its total assets in year t-1 falls between 50%

and 150% of the sample firm’s total assets; and 4) it is not an alliance or JV participant in the three-year

period prior to and one-year period after the alliance deal announcement. As noted by Bena and Li (2014),

the matching creates a pool of potential alliance participants that captures clustering not only in time, but

also by industry. Further, industry-matching controls for product market competition and size-matching

partially controls for technological life cycles. In addition to industry- and size-matching to obtain control

firms for alliance participants, we also obtain random-matched control firms by randomly drawing five

firms for each sample firm that are not an alliance or JV participant in the three-year period prior to and

one-year period after the alliance deal announcement.

Table 5 presents two-sample comparison of alliance clients and partners, alliance clients and their

industry- and size-matched peers, and alliance partners and their industry- and size-matched peers. The

sample is limited to bilateral alliances formed by US public firms (not their subsidiaries) with available

financial information.

Panel A compares alliance clients and partners. We find that alliance clients are faced with

significantly greater technological competition than are alliance partners. In terms of innovative activities,

alliance clients have more patents but a lower R&D to assets ratio as compared to their partners. Further,

we find that alliance clients are much larger than their partners, consistent with the pattern documented in

Lerner and Merges (1998) and Robinson and Stuart (2007). Finally, alliance clients employ higher leverage,

are more profitable, have lower cash holdings (normalized by total assets), lower Tobin’s Q, much slower

sales growth but higher capital expenditures than their partners.

17

Panel B compares alliance clients with their industry- and size-matched peer firms. We find that

alliance clients are faced with greater technological competition, and are significantly more innovative in

terms of patent count and R&D expenditures than their matching firms. Panel C compares alliance partners

with their industry- and size-matched peer firms. Again, we find that alliance partners are faced with greater

technological competition, and are significantly more innovative in terms of patent count and R&D

expenditures than their matching firms. The evidence strongly supports the view that technological factors

are important considerations for joining alliances.

We run a conditional logit regression using cross-sectional data that combines the alliance client

(partner) sample and their industry- and size-matching control sample (or the randomly- drawn control

sample): 3

, , , & ,

, , . (3)

The dependent variable, Event Firmim,t, takes the value of one if firm i is the client (partner) in alliance deal

m, and zero otherwise. All control variables are defined as before and measured at the fiscal year end prior

to the alliance deal announcement. For each alliance deal, there is one observation for the client (partner),

and multiple observations for the client (partner) control firms. Finally, Deal FEm is the fixed effect for

each client (partner) and its control firms.4 Table 6 Panel A presents the results.

Columns (1) and (2) report the results when the dependent variable is the alliance client indicator

variable and the control firms are either industry- and size-matched or randomly drawn as described earlier.

We find that technological competition is positively associated with the likelihood of a firm becoming an

alliance client. We further find that innovative firms with a large number of patents and high R&D

expenditures are more likely to be an alliance client. Finally, we find that large firms with low leverage,

3 See McFadden (1974) for an introduction to the conditional logit regression, and Bena and Li (2014) for a recent application in finance. 4 We do not include industry-level competition measures such as the Herfindahl index based on sales or product market fluidity (Hoberg and Phillips, 2010; Hoberg et al., 2014), for the following reasons. First, our central hypothesis is about the role of technological competition in alliance formation and in improving innovation output, which is quite different from the role of product market competition in improving sales and profitability. Second, we account for industry differences in alliance formation by employing control firms based on industry classifications.

18

good operating performance, high cash holdings, high Tobin’s Q, and high sales growth are more likely to

be an alliance client.

Columns (3) and (4) reports the results when the dependent variable is the alliance partner indicator

variable and the control firms are either industry- and size-matched or randomly drawn. We again find that

technological competition is positively associated with the likelihood of a firm becoming an alliance

partner. We further find that alliance partners tend to possess similar characteristics as alliance clients with

one notable exception. Compared with the industry- and size-matched control firms, a firm’s operating

performance is not significantly associated with the likelihood of it becoming an alliance partner. This is

not surprising, as alliances are typically formed between a client with deep pockets and a partner with

innovative ideas but limited access to financing (Lerner and Merges, 1998).

In summary, the firm-level results in Table 6 Panel A are largely consistent with the panel data

evidence and provide strong support for our first hypothesis (H1) that technological competition is an

important force behind firms’ decisions to form alliances, regardless of their specific role in the alliance.

4.3. Matching Pair Evidence

So far, our multivariate analysis focuses on using (unilateral) firm characteristics to explain alliance

formation, without accounting for the possibility that firms with complementary technologies, or firms in

the same industry may also be more likely to form alliances. For this investigation, we need a sample of

actual alliance pairs and multiple control pairs. We form the client (partner) industry- and size-matched

control (pseudo) pair sample using the actual client (partner) paired with up to five industry- and size-

matched control firms of the actual partner (client). Alternatively, we also form the control pairs using five

randomly drawn control partners (clients) that are not part of an alliance or JV deal in the three-year period

prior to and one-year period after the alliance deal announcement as discussed earlier. Thus, for each

alliance deal, our client (partner) pair sample includes the actual alliance pair and up to five pseudo pairs

where the actual client (partner) is paired with the industry- and size-matched or randomly-drawn control

firms of the actual partner (client).

We introduce three new bilateral measures in this pair-level analysis. Technological proximity from

Jaffe (1986) measures the correlation of alliance participants’ patent portfolios. Same industry is an

19

indicator variable that takes the value of one if the two participants of an alliance operate in the same two-

digit SIC industry, and zero otherwise. Same state is an indicator variable that takes the value of one if the

two participants of an alliance headquarter in the same state, and zero otherwise. Table 5 Panel D compares

these bilateral measures between the alliance pairs and their control pairs. We show that there is significant

difference in all three measures—technological proximity, same industry, and same state—across the two

types of firm pairs: Actual alliance pairs have greater technological overlap, are more likely to be in the

same industry and headquartered in the same state compared to their control pairs.

We then run a conditional logit regression using cross-sectional data of the client (partner) pair

sample, where the control firms are either industry- and size-matched or randomly drawn:

, ,

,

,

, . (4)

The dependent variable, Pairijm,t, takes the value of one if the firm pair ij is the actual pair in alliance deal

m, and zero otherwise. If the client (partner) pair sample is used for the regression, the counterparty is the

partner (client); we do not include characteristics of the actual client (partner) as explanatory variables

because these variables are invariant within a deal and are differenced out by deal fixed effects. In addition

to (unilateral) counterparty characteristics as included in Table 6 Panel A, we control for the three (bilateral)

firm-pair characteristics as defined above. Table 6 Panel B presents the results.

We find that the pair-level evidence is largely consistent with the firm-level results. New in this

analysis, we show that technological proximity between two firms is positively and significantly associated

with the likelihood of them forming an alliance. This finding holds despite the fact that we control for same

industry and same state effects. We further show that two firms from the same industry or in the same state

are also more likely to form alliances.

We conclude that technological competition faced by innovative firms prompts alliance formation.

Next, we examine the innovation outcome after forming alliances.

20

5. Strategic Alliances, Technological Competition, and Post-Alliance Innovation Outcome

In this section we answer the question: How do alliances and technological competition change the

innovation capacity of alliance participants? We posit that alliances foster commitment to long-term risky

projects and allow effective pooling of resources, leading to improved innovation outcome.5 Technological

competition helps rein in opportunistic behavior among alliance participants, further strengthening the

positive effect of alliances on innovation outcome. Due to the patent approval lag noted before, for this

investigation, we limit to alliances formed by 2000.

5.1. The Difference-in-Differences Approach

To test our second set of hypotheses, we estimate the following regression using a panel data set

that contains alliance participants and their industry- and size-matched control firms from three years before

to three years after the formation of alliances:

. (5)

The dependent variable is client (partner) patent count. Samplei takes the value of one if firm i is an actual

client (partner) in deal m, and zero otherwise. Afterit takes the value of one for the alliance participant firm

i and its control firms in the years after alliance formation, and zero otherwise. Samplei Afterit captures

the difference in the change of innovation outcome before and after alliance formation between the alliance

participant firm and its control firms. The difference-in-differences approach allows us to control for

selection (to be in an alliance or not) based on time-invariant unobservable firm characteristics. Table 7

columns (1) and (3) presents the results.

5 The extent to which corporate innovation leads to improvement in operating performance and enhanced firm value has been extensively studied in the literature (Pakes, 1985; Austin, 1993; Hall, Jaffe, and Trajtenberg, 2005; Nicholas, 2008; Kogan, Papanikolaou, Seru, and Stoffman, 2012.). In this paper, we examine innovation outcome rather than operating performance because the focus of our study is on how firms optimally choose organizational form to facilitate innovation. In untabulated analyses, we find that both clients and partners faced with fierce technological competition experience an increase in Tobin’s Q subsequent to alliance formation.

21

We show that the coefficients on the standalone terms Sample and After are positive and significant,

suggesting that alliance clients (partners) are generating significantly more patents compared to their peer

firms or compared to themselves in the pre-alliance period. We further show that the coefficients on the

interaction term Sample After are all positive and significant, suggesting that alliance participants have

significantly larger increases in patents after alliance formation than their control firms. This is strong

evidence in support of our second hypothesis (H2A) on the positive effect of alliances on post-alliance

innovation outcome.

To investigate the heterogeneity in the effect of an alliance on post-alliance innovation outcome

and test our third hypothesis, we employ the difference-in-difference-in-differences approach by estimating

the following regression:

. (6)

Columns (2) and (4) present the results. In column (2), the dependent variable is the client’s patent

count over the period from three years before to three years after alliance formation. We show that the

coefficients on the standalone terms Sample and After are positive and significant, suggesting that alliance

clients are generating more patents compared to their peer firms or compared to themselves in the pre-

alliance period. Further, we show that the coefficient on the two-way interaction term Sample After is

positive and significant, suggesting that alliance clients have significantly larger increases in patents after

alliance formation relative to their peer firms. Interestingly, the rise in patent output is reversed for clients

faced with greater technological competition. The coefficient on the three-way interaction term Sample ×

After × Tech Competition is negative and significant at the 1% level. Our findings, which show significant

improvement in clients’ innovation output post-alliance but less so for those faced with greater

technological competition, might be due to the following reason. Clients, as large established firms in the

partnership, are less nimble to cope with rapidly changing technologies. Such inability is particularly costly

22

when faced with big threats and/or big opportunities. As a result, they choose to form alliance to improve

innovation. While clients’ innovation output does improve after alliance, the negative competitive pressure

on innovation dominates the positive disciplinary role of competition, leading to a negative competition

effect which offsets the positive effect of alliance on clients’ innovation output.

In column (4), the dependent variable is the partner’s patent count over the period from three years

before to three years after alliance formation. We show that the coefficient on the standalone term After is

significantly positive, suggesting that there is an increasing trend in patent output for both alliance partner

firms and their peer firms. Further, we show that the coefficient on the two-way interaction term Sample

After is positive and significant, suggesting that alliance partners have significantly greater increases in

patents post-alliance formation than their peer firms, consistent with our second hypothesis (H2A). The

coefficient on Sample Tech Competition is also positive and significant, suggesting that technological

competition has a stronger positive impact on the innovation output of alliance partners than on their peer

firms. However, the coefficient on After Tech Competition is negative and significant, showing that peers

faced with greater technological competition do worse over time. Put differently, this finding suggests that

firms faced with technological competition but without forming alliances actual do worse on innovation

output over time compared to their alliance peers. Importantly, the coefficient on the three-way interaction

term Sample × After × Tech Competition is positive and significant at the 1% level, indicating that the

positive effect of alliances on the innovation output of partner firms become even stronger in the face of

fierce technological competition. These findings offer strong support for our third hypothesis (H3) that

greater technological competition enhances innovation output in alliance partners.

5.2. The Treatment Regression

So far we have shown that technological competition leads to alliance formation, which in turn

enhances innovation output, especially for alliance partners. However, the above results are subject to

reverse causality concerns, i.e., firms expected to improve patenting output choose to form alliances, so our

findings thus far may be driven by selection, instead of the treatment effect of alliances on innovation

output. To address this concern, we employ the treatment regression framework and for identification, we

23

employ an instrumental variable that clearly drives alliance formation decisions but has nothing to do with

the innovation outcome other than through the channel of forming alliances.6

For this purpose, we use a “natural experiment”—changes to US states requiring combined

reporting of corporate income (Mazerov, 2009) to help pin down the direction of causality (Bodnaruk et

al., 2013). We consider situations where the opportunity costs of forming alliances differ due to exogenous

reasons that are not firm specific, and examine how the differential reaction to this variation is related to

patent outcome. To do so, we rely on the differences in corporate income reporting rules across US states.

There are two types of corporate income reporting for the purpose of state-level taxation: combined

reporting and separate reporting. Under separate reporting rules, a multi-state firm can reduce its taxable

income by isolating highly profitable parts of its business in an affiliate that is not subject to state taxes.

Combined reporting rules, however, require firms to report their overall income generated in the US and

pay state corporate income tax on the basis of the proportion of income attributable to activity in each state

where these firms have business activities. Thus, combined reporting rules reduce the benefits of using non-

arm’s-length transactions between the subsidiaries of a firm located in different states—internal capital

markets—to reduce tax burden. This suggests that combined reporting reduces the opportunity cost of

forming alliances to commit assets. We thus expect that firms form more alliances in states with combined

reporting.

To construct the combined reporting index for each firm that covers all of the states in which it has

business operations, we need to collect data on the location of the firm’s subsidiaries and then aggregate at

the firm level. The detailed information on the construction of the variable is covered in Bodnaruk et al.

(2013) and their Appendix D. The data we have on firm-level combined reporting index is available for

1998, 2000, 2002, and 2004. We use the 1998 data for alliances formed between 1990-1998; the 2000 data

for alliances formed between 1999-2000; the 2002 data for alliances formed between 2001-2002; and

finally the 2004 data for alliances formed between 2003-2004. Our instrumental variable is a firm’s

combined reporting index, where a higher value of the index indicates that more of the firm’s operation is

located in states that require combined reporting.

6 See Li and Prabhala (2007) for an overview of dealing with selection issues versus treatment effects in corporate finance.

24

Table 8 presents the cross-sectional treatment regression results. The sample for columns (1)-(2)

and (5)-(6) contains both the clients and their industry- and size-matched control firms. The sample for

columns (3)-(4) and (7)-(8) contains both the partners and their industry- and size-matched control firms.

Column (1) ((3)) presents the first-stage regression results where the dependent variable is the alliance client

(partner) indicator variable in year t, and the instrumental variable is based on a firm’s headquarter location.

The variable of interest is the firm’s combined reporting index. We show that indeed when a firm has a

higher value of the combined reporting index, that firm is more likely to enter an alliance (either as a client

or a partner). We also show that technological competition faced by a firm is positively associated with the

likelihood of that firm entering an alliance.

Column (2) presents the second-stage regression results where the dependent variable is the patent

count of the client from year t+1 to year t+3. The coefficient on Sample is positive and significant,

supporting our second hypothesis (H2A) that alliances lead to improved innovation outcome. Consistent

with the findings from the difference-in-difference analyses, the coefficient on the interaction term Sample

Tech Competition is negative and significant, suggesting that clients do not generate significantly more

patents in the face of fierce technological competition. Column (4) presents the second-stage regression

results where the dependent variable is the patent count of the partner from year t+1 to year t+3. The

coefficient on Sample is significantly positive, supporting our second hypothesis (H2A) that alliances lead

to improved innovation outcome. Importantly, the coefficient on the interaction term Sample Tech

Competition is positive and significant, suggesting that alliances and technological competition reinforcing

each other in generating more patent output for partners. This finding thus supports our third hypothesis

(H3).

Columns (5)-(8) repeat the analysis in columns (1)-(4) except that the instrumental variable—the

combined reporting index for each firm is based on information on the locations of both its headquarter and

subsidiaries. It is worth noting that our main findings remain unchanged.

In summary, our results in Tables 7 and 8 suggest that technological competition-driven alliances

are associated with improved innovation output, especially for those partners faced with greater

technological competition, consistent with our third hypothesis (H3).

25

5.3. The Underlying Mechanisms

In this section, we explore a number of possible underlying economic mechanisms through which

the improvement in innovation output at alliance participant firms takes place.

5.3.1. Innovative Efficiency

We conjecture that one direct benefit of technological competition-driven alliances is improvement

in innovative efficiency; the competitive pressure may also push alliance participant firms to increase R&D

expenditures.

Following Hirshleifer, Hsu, and Li (2013, p. 637, Equation (1)), innovative efficiency is constructed

as the ratio of the number of patents applied in year t to the R&D capital stock accumulated over year t-6

to year t-2, assuming an annual straight-line depreciation rate of 20%. The two-year gap between the

numerator and the denominator is due to the fact that it takes time to generate patents from R&D

expenditures. Table 9 Panel A presents the results.

Columns (1)-(2) and (5)-(6) present the regression results when the dependent variable is the dollar

amount of R&D expenditures (in logarithm). The coefficients on Sample × After are positive and significant

in both columns (1) and (5), suggesting that alliance participants increase their R&D expenditures after the

formation of alliance. The coefficients on the three-way interaction term Sample × After × Tech competition

is negative and significant in column (2), whereas insignificant in column (6), suggesting that in the face of

fierce technological competition clients reduce their R&D expenditures. The results are consistent with our

findings in Tables 7 and 8 that when faced with fierce technological competition, only partner firms are

associated with improved innovation outcome after alliance formation.

Columns (3)-(4) and (7)-(8) present the regression results when the dependent variable is innovative

efficiency. The coefficients on Sample × After are insignificant in columns (3) and (7), suggesting that

alliance itself does not lead to significant improvement in innovative efficiency. In columns (4) and (8), we

find that in the face of fierce technological competition, there is little change in innovative efficiency of

clients (an insignificant coefficient on Sample × After × Tech competition), but there is significant

improvement in innovative efficiency of partners (a positive and significant coefficient on Sample × After

× Tech competition). The results again are consistent with our prior findings that when faced with fierce

technological competition, partner firms experience significant improvement in post-alliance innovation

26

outcome. More importantly, the results also support our conjecture that technological competition could

play a discipline role and improve innovative efficiency by limiting the opportunistic behaviors of alliance

participants.

In a nutshell, the evidence in Panel A suggests that both clients and partners increase R&D

expenditures post-alliance formation, supporting Robinson’s (2008) view that alliance is an effective

“commitment technology” for developing longshot projects. The evidence that technological competition

improves partner firms’ innovative efficiency further supports our conjecture that competition strengthens

the positive effect of strategic alliances on innovation outcome.

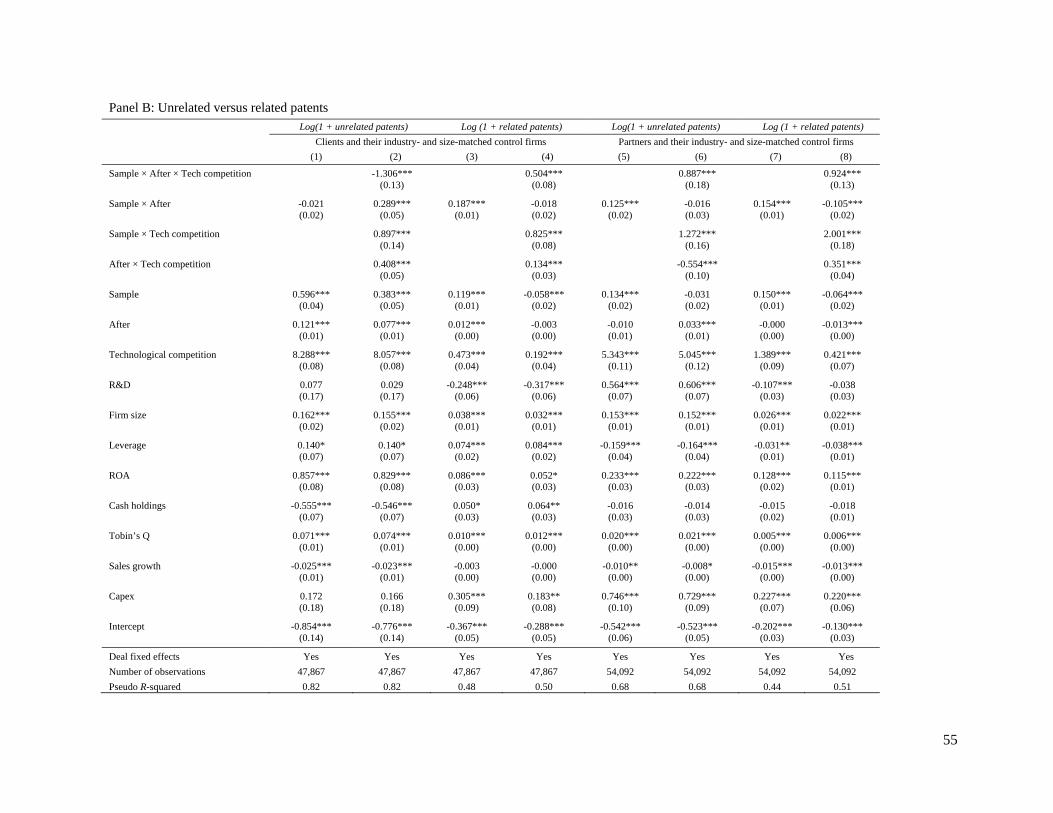

5.3.2. Unrelated and Related Patents

Gomes-Casseres et al. (2006) find that one immediate impact of alliances is enhanced knowledge

flow between participant firms, which might in turn lead to improved patenting output. For a client (partner)

in year t, we define related patents as those patents that are applied in year t and cite patents of the partner

(client) and unrelated patents as those patents that are applied in year t and do not cite patents of the partner

(client). We employ similar model specifications as the difference-in-differences models of Equations (5)

and (6). Table 9 Panel B presents the results.

Columns (1)-(2) and (3)-(4) present the regression results when the dependent variable is the

client’s unrelated and related patent count, respectively. We do not find post-alliance improvement for

unrelated innovation (an insignificant coefficient on Sample × After in column (1)). In contrast, such

improvement occurs for related innovation (a positive and significant coefficient on Sample × After in

column (3)). Further, we find that in the face of fierce technological competition, clients significantly reduce

their unrelated patent output (a negative and significant coefficient on Sample × After × Tech competition

in column (2)), while significantly increase their related patent output (a positive and significant coefficient

on Sample × After × Tech competition in column (4)), suggesting that knowledge flows occur between

alliance participants, consistent with our second hypothesis (H2B). This finding is also consistent with our

earlier observations that clients faced with greater technological competition generate fewer patents; while

enhanced knowledge flow via alliances help those clients to generate significantly more patents that are

related to partners.

27

Columns (5)-(6) and (7)-(8) present the regression results when the dependent variable is the

partner’s unrelated and related patent count, respectively. We find that partners exhibit significant

improvement in both unrelated and related innovation (columns (5) and (7)). Further, we find that the

improvement for both unrelated and related innovation are stronger in the face of fierce technological

competition (columns (6) and (8)), supporting our second hypothesis (H2B) that enhanced knowledge flow

via alliances leads to improved innovation output.

5.3.3. Inventor-Level Evidence

Finally, we examine the productivity of individual investors associated with alliance participant

firms. For this analysis, the sample consists of inventors working either in the alliance firms or their

industry- and size-matched control firms. We obtain information about patent inventors from the Harvard

Business School (HBS) Patent and Inventor Database. For a particular alliance firm (or its matched control

firm), stayers are inventors who apply at least one patent with the firm in the three-year period prior to the

alliance deal and at least one patent with the same firm in the three-year period after the deal and they do

not have any patents outside the firm over these two periods. For a particular alliance firm (or its matched

control firm), new hires are inventors who do not have any patent with the firm in the three-year period

prior to the alliance and at least one patent with the firm in the three-year period after and they do not have

any patents outside the firm over the post-alliance period. Table 9 Panel C presents the results.

The dependent variable is the logarithm of the number of patents an inventor applied, taken at the

end of two three-year periods: year t-3 to t-1 and year t+1 to t+3 relative to the deal announcement in year

t. Firm characteristics are measured at the end of the respective three-year period. We find that both stayers

and new hires in alliance partners exhibit significantly improved productivity post alliance and such

improvement is stronger in the face of fierce technological competition.7 While both stayers and new hires

in alliance clients also exhibit significantly improved productivity, there is no evidence that such

improvement is stronger when clients faced with fierce technological competition. The above findings are

consistent with the evidence in Tables 7 and 8, suggesting that only partners experience significant

improvement in post-alliance patent output when faced with fierce technological competition.

7 In untabulated analyses, we show that both stayers and new hires, respectively, exhibit significant improvement in productivity in alliance partner firms in the face of fierce technological competition.

28

In summary, we conclude that technological competition is positively associated with both the

likelihood of firms joining alliances and the subsequent improved innovation output for alliance partners.

6. Additional Investigation

Robinson and Stuart (2007) note that both alliances and JVs are commonly employed by large firms

to engage in R&D. A joint venture takes place when two or more firms form a new firm to undertake the

activity in common. Like alliances, JVs also involve significant negotiations to divide the income and