Techno-CommercialSimulation · linear or dual sensitivity analysis. How-ever, correlation...

6

© K&F. All rights reserved. / Techno-Commercial Simulation by Kostro&Friedel Pte. Ltd. (K&F) K&F offers a novel asset valuation frame- work with a state of the art techno- commercial simulator at its core. The simulator enables fully probabilistic as- sessments of assets or portfolios in terms of economic performance to facilitate mergers and acquisitions (M&A) activ- ities, improve field development plan- ning and decision making for E&P com- panies. K &F offers due diligence and techno-commercial advisory for the oil and gas industry. The as- set evaluation services provide independent guidance regarding the current and future value of oil and gas fields. This includes the optimisation of field development scenarios to maximise the asset's prof- itability and assistance to decision and risk analysis considering exploration and appraisal activities. K&F has a strong background in the upstream con- sultancy business and works with a team of seasoned associates covering all relevant E&P disciplines with deep technical knowledge, extensive work experience and geographic exposure. Proprietary technologies constitute the basis of K&F's core services. These are summarised in the following figure: Portfolio Management Asset Development and Optimisation Asset (e)Valuation Asset Performance Review © Reservoir – Fluid System © Reservoir Volumetrics © Reservoir Diagnostics © Reservoir Predictive Toolbox Techno- Commercial Simulator K&F's CORE SERVICES K&F's TECHNOLOGIES Insight Insight Services and technologies overview Highlighted ones are invoke techno-commercial simulation. The simulator drives a wide range of K&F services, covering valuation of oil and gas assets, technical and financial risk analysis, financial negotiation support, and decision and risk analysis on a field, block or portfolio level. It supports any application areas where fast and prudent decision making is crucial. This document has been prepared for marketing purposes only. K&F is acting in an advisory capacity only and, to the fullest extent permitted by law, disclaims all liability for actions or losses derived from any actual or purported reliance on this document (or any other statements or opinions of K&F) by the client or by any other person or entity. of

Transcript of Techno-CommercialSimulation · linear or dual sensitivity analysis. How-ever, correlation...

©20

16K&

F.Al

lrig

htsr

eser

ved.

05/2

016

Techno-Commercial Simulationby Kostro&Friedel Pte. Ltd. (K&F)

K&F offers a novel asset valuation frame-work with a state of the art techno-commercial simulator at its core. Thesimulator enables fully probabilistic as-sessments of assets or portfolios in termsof economic performance to facilitatemergers and acquisitions (M&A) activ-ities, improve field development plan-ning and decision making for E&P com-panies.

K&F offers due diligence and techno-commercialadvisory for the oil and gas industry. The as-set evaluation services provide independent

guidance regarding the current and future value of oiland gas fields. This includes the optimisation of fielddevelopment scenarios to maximise the asset's prof-itability and assistance to decision and risk analysisconsidering exploration and appraisal activities.

K&F has a strong background in the upstream con-sultancy business and works with a team of seasonedassociates covering all relevant E&P disciplines withdeep technical knowledge, extensive work experienceand geographic exposure.

Proprietary technologies constitute the basis of K&F's core services. These are summarised in the following figure:

Portfolio Management

Asset Development and Optimisation

Asset (e)Valuation

Asset Performance Review©

Reservoir –Fluid

System©

ReservoirVolumetrics©

ReservoirDiagnostics©

ReservoirPredictiveToolbox

Techno-Commercial

Simulator

K&F's

CORE

SERV

ICES

K&F's TECHNOLOGIES

InsightInsight

Services and technologies overviewHighlighted ones are invoke techno-commercial simulation.

The simulator drives a wide range of K&F services, covering valuation of oil and gas assets, technical and financialrisk analysis, financial negotiation support, and decision and risk analysis on a field, block or portfolio level. Itsupports any application areas where fast and prudent decision making is crucial.

This document has been prepared for marketing purposes only. K&F is acting in an advisory capacity only and, to the fullest extent permitted by law, disclaims all liabilityfor actions or losses derived from any actual or purported reliance on this document (or any other statements or opinions of K&F) by the client or by any other person orentity.

1 of 6

©20

16K&

F.Al

lrig

htsr

eser

ved.

05/2

016

Application Areas

Techno-commercial simulation allows to assess the current and the future value of oil and gas properties. Combin-ing latest proprietary technologies with substantial in-house expertise facilitates a wide range of analysis, cateringfor M&A activities, field development optimisation and portfolio related assessments with multiple assets.

M&A. A primary focus of techno-commercial simulation is to support techni-cal and commercial teams during M&A activities, e.g., in facilitating:

t Oil and gas asset valuations, including producing/developing assetsand exploration blocks/acreage,

t Data-room assessments (screenings/evaluations) and bid preparation,t Technical and financial risk analysis of transaction including techno-

commercial due-diligence,t Financial negotiation support to optimise bid parameters.

Field Development. For asset planning, field development and optimisationit is the tool of choice for:

t Conducting the general framing, concept identification, screening andselection workflow as part of the conventional hydrocarbon resourcematuration process,

t Optimising development concepts in low oil price environments andsupporting field development activities throughout detailed design upto final investment decision (FID),

t Driving area development planning (ADP) and exploration through de-cision and risk analysis (D&RA) to enable performance improvement incomplex integrated development projects,

t Facilitating renegotiation of Production Sharing Contracts (PSC) andother commercial frameworks as part of a D&RA process.

Portfolio Management. It is possible to build models of an entire portfoliocomprising multiple assets, enabling:

t Portfolio assessment in producing and developing fields to (i) bench-mark asset performance based on commercial Key Performance Indi-cators (KPI), (ii) optimise divestment strategies, (iii) enhance capital al-location efficiency, and (iv) to determine the potential impact of com-petitive scoping,

t Decision and risk analysis on portfolio level to, among others, minimiserisk profile and exposure, determine optimum development strategiesacross the portfolio, prioritise exploration commitments and prospectsand maximise utilisation of shared infrastructure.

Asset Valuation

M&A Support

Concept Screening

and Selection

Decision and Risk Analysis

Asset Planning

Area Development

Planning

Portfolio Management

Application areas forTechno-Commercial Simulation

2 of 6

©20

16K&

F.Al

lrig

htsr

eser

ved.

05/2

016

Asset Models & Scenario Analysis

The simulator works on the basis of scenarios. After defining the scheduling, the production and the expenditureload along their uncertainty ranges, it treats the scenarios as discrete asset models with the fully probabilistic as-sessment conducted by an in-house Monte-Carlo solver. A scenario can comprise any number of phases or stages,including conditional actions and decisions, for each asset model.

Production can be defined by means ofdecline assumptions including drillingqueues, various built-in analytical modelsor from external sources such as simulatorresults. Most frequently used types suchas baseline production, production en-hancement activities, infill drilling cam-paigns, IOR/EOR deployment are prede-fined for fast model set-up. An assetmodel can be arbitrarily phased. There isfull flexibility to define complex relation-ships between the individual phases interms of timing and scope, including con-ditional actions and decisions if required.Facilities constraints such as capacity lim-its can be taken into account.

Expenditure loading comprises capital, op-erating or any other miscellaneous expen-diture. Parametrisation for asset screen-ings or evaluations can be kept to a min-imum using high-level cost block esti-mates, distributing those automaticallyover time using pre-defined S-curves. Forprojects closer to FID level, expenditurecan be parametrised alternatively withgreat granularity. This flexibility allows toallocate expenditure accurately accordingto the maturity of the scenario.

Commercial assessment captures the base-line, standalone project, fully incremen-tal and total asset level economics. Thesimulator is designed for a wide rangeof fiscal regimes and terms, from royaltytax, production sharing to risk service con-tracts. An initial and continuous calibra-tion against the operators reference fiscalmodel ensures the consistency and accu-racy of the fiscal arithmetic and the re-sults. Specific data sets can be selected,extracted and modelled in the client's ref-erence model for maximum coherencyand compatibility.

2005 2007 2010 2012 2015 2017 2020 2022 2025 2027 2030 2032

Oil

Pro

duct

ion

Rat

e (M

bopd

)

0

5

10

15

20

25

30Baseline NFAField A(S) ERD Wells Appraisal & DevelopmentField A(S) Phase 1 Development (WHPP)Field A(S) Waterflooding Main ReservoirsField B Appraisal & Development from WHPP Field A (ERD)Field A(S) Phase 2 (Infill Drilling)Field A(N) Phase 1 (Stepout Wells Appraisal & Development)Field B Phase 1 Development (WHP)Field B Phase 2 (Infill Drilling)Field A(N) Infill Drilling

Deterministic production rates,Example Phased Development Scenario

2015 2016 2017 2018 2019 2020 2021 2022 2023

Cap

ital E

xpen

ditu

re C

AP

EX

(M

M$)

0

25

50

75

100

125

150Baseline NFAField A(S) ERD Wells Appraisal & DevelopmentField A(S) Phase 1 Development (WHPP)Field A(S) Waterflooding Main ReservoirsField B Appraisal & Development from WHPP Field A (ERD)Field A(S) Phase 2 (Infill Drilling)Field A(N) Phase 1 (Stepout Wells Appraisal & Development)Field B Phase 1 Development (WHP)Field B Phase 2 (Infill Drilling)Field A(N) Infill Drilling

Annualised Capital Expenditure (CAPEX),Example Scenario

2015 2017 2019 2021 2023 2025 2027 2029 2031

Afte

r T

ax D

isco

unte

dC

umul

ativ

e C

ash

Flo

w (

MM

$)

-150

-100

-50

0

50

100

150

200

250

300

Eco

nom

ic L

imit

Bas

elin

e: 0

1-D

ec-2

019

Total Asset NPV10 (100% WI)Baseline NPV10True Incremental NPV10 (Asset Level)

Baseline and incremental cumulative cashflow NPV10,Example Scenario

3 of 6

©20

16K&

F.Al

lrig

htsr

eser

ved.

05/2

016

Uncertainty assessment can be conductedfor any parameter, including develop-ment scope, production, expenditure,timing or fiscal related ones. A widerange of distribution functions is avail-able. Dependencies can be incorporated,for example as tabular lookups to deter-mine the facility scope as function of theuncertain well number.Conventionally available high, mid,low estimates of production or expen-diture can be readily converted into atime-dependent continuous distributionfunction that is suitable for fully proba-bilistic techno-commercial simulation.Developed in a high performance com-puting environment, the in-house solvertypically runs 5,000 – 10,000 discretetechno-commercial models for eachscenario within minutes.

Probabilistic KPIs are a key deliverable ofthe uncertainty assessment, which yieldsa distribution function for any fiscal orproduction related KPI. It allows to intro-duce new KPIs into the decision makingprocess, such as the 'Probability of Com-merciality’, which captures the probabil-ity of breaking even. The process gen-erates descriptive statistics, such as ex-pected values, percentiles capturing theupside (P10) and downside KPI values(P90) or standard deviation for any KPI.

Risk and uncertainty analysis comprises theconventional techniques of threshold-,linear or dual sensitivity analysis. How-ever, correlation coefficients derived forthe KPI distributions yield a more realis-tic measure describing parameter sensi-tivity. They can be generated for any KPIsuch as NPV, incremental production orCAPEX and allow to identify and focus onkey project risks and mitigation strategies.Several other analytical techniques arebuilt-in to analyse the relationship be-tween uncertain parameters, includingcorrelation matrices, composite scaledsensitivities and principal componentanalysis. Those are specifically tailored forfiscal parameters, e.g., bid parameters, tosupport M&A negotiations.

2008 2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032

Oil

Pro

duct

ion

Rat

e (M

bopd

)

0

5

10

15

20

25

30P10P25P50P75P90Deterministic ModelBaseline

Probabilistic production profiles,Example Scenario

NPV (MM$)-200 0 200 400 600

Cum

ulat

ive

Pro

babi

lity

90

75

50

25

10

Net Present Value NPV

Total Asset NPVTrue Asset Incremental

ME (MM$)-500 -400 -300 -200 -100 0

Cum

ulat

ive

Pro

babi

lity

90

75

50

25

10

Maximum Exposure

Unit Cost ($/STB)10 20 30 40 50 60

Cum

ulat

ive

Pro

babi

lity

90

75

50

25

10

Unit Cost

Incremental UTCIncremental UDC

MY Value (MM$)0 500 1000 1500 2000

Cum

ulat

ive

Pro

babi

lity

90

75

50

25

10

Malaysia Total Value

Total AssetBaseline

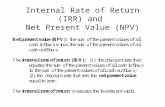

IRR (%)0 20 40 60 80 100

Cum

ulat

ive

Pro

babi

lity

90

75

50

25

10

Internal Rate of Return

Total AssetTrue Asset Incremental

PIR (%)-50 0 50 100 150

Cum

ulat

ive

Pro

babi

lity

90

75

50

25

10

Profit Investment Ratio

Total Asset PIRIncremental PIR - NPV(I)10/ME10

Probabilistic KPI distributions,Example Scenario

-8.0 -12.5 -15.5

NPV (mm$)

CAPEX MULTIPLIER0.5 0.6 0.7 0.8 0.9 1 1.1 1.2 1.3 1.4 1.5

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

1.3

1.4

1.5

1.6 -12.5 -15.5

IRR (%) PROJECT

CAPEX MULTIPLIER0.5 0.6 0.7 0.8 0.9 1 1.1 1.2 1.3 1.4 1.5

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

1.3

1.4

1.5

Dual sensitivities (OPEX vs CAPEX reduction) for project economics NPV10 and IRR,Example Scenario

-0.4 -0.2 0 0.2 0.4 0.6 0.8

Decline ERD well for Field B A&D

Decline infill wells for A(N)Rampup time Field A(S) waterflood

Offtake wells Field B deeper reservoirs

First Oil WHP Field B (Month)

Number injectors WHPP A(S) main reservoirsFirst Oil from WHPP Field A(S) (month)

WHP Field B incremental OPEX

Decline A&D A(S) deeper reservoirs

Baseline production risk

Decline WHP Field B main reservoirsWHPP Field A incremental OPEX

Decline ERD Field A(S)

Decline Field A(S) main reservoirs

General CAPEX contingency

-0.00

-0.01

-0.01

-0.01

-0.02

-0.03

-0.03

-0.04

-0.05

-0.05

-0.07

-0.08

-0.13

-0.17

-0.35

0.00

0.02

0.02

0.03

0.04

0.04

0.05

0.06

0.08

0.09

0.09

0.09

0.09

0.16

0.18

0.18

0.18

0.20

0.28

0.75

Correlation Coefficient

Decline wells A(N) main reservoirs

Offtake ERD well for Field B A&D

Decline wells Field B deeper reservoirs

Number producers Field B deeper reservoirs

Number ERD for A&D A(S) deeper reservoirsIncremental well OPEX

Decline rate Field A(S) waterflood

Offtake infill wells for A(N)

Number infill wells for A(N)Peakoil Field A(S) waterfloodNumber producers Field B main reservoirsNumber wells A(N) main reservoirsOfftake wells A(N) main reservoirs

Number producers WHPP A(S) main reservoirs

Offtake ERD wells Field A(S)Offtake A&D A(S) deeper reservoirsOfftake WHP Field B main reservoirsNumber ERD wellsOfftake Field A(S) main reservoirs

Oil price variability

Significance Boundary

Value Decrease Value Increase

Correlation coefficients for project economics NPV10,Example Scenario

4 of 6

©20

16K&

F.Al

lrig

htsr

eser

ved.

05/2

016

KPI Summary provides a simple mean tosummarise the performance of a poten-tial development scenario, or the value ofan entire asset, in a single 'traffic light’.The colours green, yellow, red are definedas per the operators screening criteria andobjectives.

Scenario Analysis is a powerful tool if mul-tiple development or investment oppor-tunities are benchmarked as part of aconcept screening and selection. KPIs ofthe individual scenarios can be visuallyand statistically benchmarked for specificsanction or decision criteria. Results fromthe techno-commercial simulator can bereadily exported to Microsoft® Excel orother external data analytics packagessuch as Tableau®or Spotfire®.The probabilistic framework introducesthe Performance Index, defined as ra-tio of expected NPV (EMV) and its stan-dard deviation. The KPI allows to screenfor projects that maximise the economicreturn at the lowest uncertainty using'efficient frontier’ based workflows, thuschoosing investments with the lowestamount of risk at any targeted level of re-turn.

Techniques and approaches describedabove for single assets can be readily ex-tended if multiple assets are present forco-development that show some degree ofdependency.

Probabilistic KPI distributions,Example Scenario

-200-160 -120 -80 -40 0 40 80 120 160 200Expected Monetary Value (mm$)

0

20

40

60

80

100

120

140

160

180

200Standard Deviation of EMV (mm$)

Field D

Prospect X1/2

Field A/B

Field A/BField A/B

Field A/B

Prospect X1/2

Prospect X1/2

Prospect X1/2

Prospect X1/2

Prospect X1/2

Prospect X1/2

Prospect X1/2

Field A/B

Field A/B

Field A/B

Field A/B

Field D

Field A/B

Prospect Y

Field A/B

Field A/B

Prospect X1/2

Field A/B

Field A/BField E

Field A/B

Field D

Field D Field D

Reserves (mmstb)82030405056

ThemeStrategy AStrategy BStrategy CStrategy D

Efficient Frontier application (EMV vs. standard deviation),Example Concept Screening

Data Requirements. The level of details required for the parametrisation generally depends on the maturity ofthe hydrocarbon resource and the asset status. The parameter set can be derived as part of conventional as-set screening and evaluation workflows which can be drastically sped-up by K&F 's proprietary technologysuch as the Asset Performance Review©. Scheduling and expenditure estimates typically originates fromcost blocks provided by the development teams. If not available, these can be based on technical input gen-erated through in-house costing software and experience from K&F 's associates. Fiscal parameters such asgeneral contract mechanisms and taxation parameters are publicly available in many cases, and can be fur-ther customised according to actual contracts if available.

Time Line. Designed with a high degree of efficiency and automation of the process, K&F can offer techno-commercial services with fast turnaround time.

The range of analysis techniques and algorithms are continuously expanded and further optimised.Delivering state of the art technological solutions and services is a main business principle of K&F.

5 of 6

©20

16K&

F.Al

lrig

htsr

eser

ved.

05/2

016

Optimisation Capabilities

Unlike spreadsheet applications, the simulator is built around a high-performance computing environment withindustry grade technology and optimisers. Furthermore, the framework utilises techniques developed for historymatching, particularly regarding the risk and uncertainty framework but also for optimisation.

35KOSTRO & FRIEDEL

© 2

014 K

OS

TR

O&

FR

IED

EL P

te L

td.

All

rights

rese

rved.

35

© 2

014 K

OS

TR

O&

FR

IED

EL P

te L

td.

All

rights

rese

rved.

Techno-Commercial Assessment

Predictive and Optimization Capabilities

Linear sensitivities of individual parameters

• Analyse how changes in a single parameter will impact results (one parameter is changed at a time)

Multivariate analysis

• Analyse complex relationships between 2 or more uncertain parameters

Fully probabilistic analysis

• Analyse and improve risk profile by covering full range of possible outcomes (using Monte Carlo on a large number of fully discrete asset models)

Deterministic Optimisation

• Determine the optimum set of parameters under uncertainty to improve single or multiple KPI’s

Fully Probabilistic Optimisation

• Determine the optimum set of parameters thatmaximise the probability of achieving single or multiple KPI’s

Predictive Techno-Commercial Assessment Optimisation Methods

•Tornado Charts and Spider plots

•Advanced 3D/4D visualization

•Advanced statistical presentation incl. PCA, Correlation Matrices, sensitivity index

•Fully probabilistic production, cost and cash flow profiles

•Distribution functions for any KPI

•Tornado & Pareto Charts

•Set of parameters including statistical representation (e.g., confidence intervals)

•Set of parameters including statistical representation (e.g., confidence intervals)

Typical main analysis conducted using common spreadsheet based techno-commercial models

M&A Support FID Support Asset & Portfolio Management

Asset Screening Concept Screening Asset Planning

Asset (E)valuation Concept Selection Performance Benchmarking

Commercial Negotiation Support Performance & Efficiency Improvement

Risk Quantification and Mitigation

FID Support Portfolio Management

Concept Optimization Capital Allocation

Portfolio Optimization

Risk Quantification and MitigationAp

pli

ca

tio

nD

eli

ve

rab

les

Ob

jec

tive

Simulation capability summary.

Benefits

The techno-commercial simulator enables sophisticated, fullyprobabilistic assessment of individual assets or a portfolioof assets in terms of the economic performance to optimiseinvestments (M&A), Field Development Planning and generaldecision making for E&P companies. It is heavily leveraged byparallel computing and allows for running a large number ofdiscrete, yet fully parametrised development scenarios with ashort turn around time. Entire portfolios can be modelled. Thebenefits can be summarised as follows:

t Builds complex field development scenarios with depen-dencies and constraints,

t Models comprehensive fiscal capabilities (including incre-mental economical evaluation),

t Analyses and optimises KPIs fully probabilistically,

t Enables sophisticated risk and statistical analysis,

t Leaves an audit trail and ensures repeatability of results,

t Allows data export/exchange of full data sets into Excel.

Kostro&Friedel Pte. Ltd.Offices inHamburg, GermanyKuala Lumpur, Malaysia

Contact details for Kostro&Friedel Pte. Ltd.Email: [email protected]

www.kostro-friedel.com

6 of 6