Technical barriers to trade for hungarian exports to the ...

30

INSTITUTE FOR WORLD ECONOMICS HUNGARIAN ACADEMY OF SCIENCES W o r k i n g P a p e r s No. 116 June 2001 Kálmán Dezséri, Andrea Éltető and Sándor Meisel TECHNICAL BARRIERS TO TRADE FOR HUNGARIAN EXPORTS TO THE EUROPEAN UNION 1014 Budapest, Orszagház u. 30. Tel.: (36-1) 224-6760 • Fax: (36-1) 224-6761 • E-mail: [email protected]

Transcript of Technical barriers to trade for hungarian exports to the ...

INSTITUTE FOR

WORLD ECONOMICSHUNGARIAN ACADEMY OF SCIENCES

W o r k i n g P a p e r s

No. 116 June 2001

Kálmán Dezséri, Andrea Éltető and Sándor Meisel

TECHNICAL BARRIERS TO TRADE FOR HUNGARIAN EXPORTSTO THE EUROPEAN UNION

1014 Budapest, Orszagház u. 30.Tel.: (36-1) 224-6760 • Fax: (36-1) 224-6761 • E-mail: [email protected]

SUMMARY

The EU was already Hungary’s most important trading partner by the end ofthe 1990s. Hungary managed a rapid increase in its exports to the EU, espe-cially in the second half of the decade. This was accompanied by a consider-able change in the product structure, with the share of high-technologyproducts increasing strongly to a level high by international standards* and arapid fall in the share of low-tech, resource-intensive and unskilled labour-intensive goods. Statistical calculations reveal that Hungary, uniquely amongthe CEE countries, shows clear specialization patterns or revealed compara-tive advantages in high-tech products on the EU market.**

These trends could not have occurred without rapid adaptation of tech-nical standards and upgrading of product quality. The main finding of thesurvey conducted by the authors, therefore, is that TBTs (technical barriers totrade) with the EU were no longer significant for Hungarian firms by 2000.Seventy-three per cent of firms reported no difficulties in exporting to the EU.The expectations of companies were optimistic, with the majority forecastinga positive impact from technical harmonization and the elimination of bor-ders.

The sample was then divided into groups with defined characteristics.One was the sector affiliation of the firm. TBTs proved to be highest in themachinery and textile and clothing sectors. When ownership was examined,it was found that technical requirements presented fewer difficulties to FIEs,which had to invest less in redesigning their products than the domesticgroup. In several cases, FIEs belonged to large multinational networks, whichfacilitated their export activity. The third characteristic examined was the ex-port-intensity of firms. Export-intensive firms in the sample were larger, hada higher average proportion of foreign ownership, and faced fewer difficul-ties in exporting than the non-export-intensive group. However, what diffi-culties they do face are mainly TBTs.

* In 1998, the share of high-tech products in Hungarian exports to the EU was 34.5 per cent,compared with 13.5 per cent in Polish, 16.2 per cent in Portuguese, 17.1 per cent in Czechand 37.9 per cent in Irish exports to the EU (Éltető 2000).** Kaminski (1999) and Éltető (2000).

5

1) THE TECHNICAL BARRIERS TOTRADE WITH THE EU*

Many countries in the world place broad re-liance on standards, technical regulations,and certification systems in their trade.These systems have been developed to en-hance the availability of information and re-duce uncertainties about the quality char-acteristics of goods and services. The EU isno exception. In the areas regulated byCommunity law, manufacturers must applyconformity assessment and inspection pro-cedures in accordance with modules gradedby the risks arising from use of their prod-ucts (as set forth in Council Decision93/465/EEC). The standards and technicalregulations may be considered technicalbarriers to trade (TBTs) for potential export-ers in the outside world.

In the EU (as in any other country),standards are generally defined voluntarilyby commercial associations or other non-governmental organizations. However,technical regulations are legally binding.Certification systems are intended to assurecompliance with existing standards orregulations. The EU had adopted about11,500 such standards by 2000.

Despite the single market, standards,technical regulations, and certificationpractices still differ among member-states inmany respects. In effect, the single marketdoes not fully apply yet. The variety of tech-nical regulations may act as barriers totrade, which the EU is set on overcoming byvarious means, under what are known as theOld Approach and the New Approach.

The harmonization of member-statelegislation began in 1969, according to the * This research was supported by the European Un-ion’s PHARE ACE Project No. 97–8162–R: ‘Accession,Differentiation and Their Impact on Trade and Invest-ment Flows in an Integrated Europe’. The contents ofthis publication are the sole responsibility of theauthors and in no way represent the views of theCommission or its services.

Council’s general programme of May 28that year. The aim was to eliminate technicalbarriers to trade in industrial products. Itcontinued in the framework of a White Pa-per on completing the internal market by1992, according to guidelines approved bythe Council in a resolution of May 7, 1985concerning a New Approach to technicalharmonization and standardization. Progresshas been made in the following sectors:(a) Lifting appliances and lifts.(b) Gas appliances.(c) Pressure vessels.(d) Cosmetics.(e) Motorcycles and mopeds.(f) Fertilizers.(g) Measuring instruments.(h) Pre-packaged goods.(i) Electrical material.(j) Construction plant and equipment.(k) Dangerous substances.(l) Agricultural tractors.(m) Motor vehicles.(n) Construction.(o) Prevention of accidents.(p) Textiles.(q) Road vehicles.(r) Other sectors.

The differences between the standards,technical regulations, and certification pro-cedures of the EU and those of the CentralEuropean countries were significant at thebeginning of 1990s and more pronouncedthan those found between EU member-countries. The aim of acceding to the EUmeant that the Central European associatedcountries have had to adopt new standards,technical regulations, and certificationpractices or harmonize theirs with EU re-quirements. These are areas of major im-portance for access to EU markets. Details ofthe process of adoption and harmonizationof standards are important issues at the ne-gotiations on entry conditions (in the chap-ter on free movement of goods).

6

2) HUNGARY’S POLICY FOR RE-DUCING THE EFFECTS OF EU TBTS

The importance of the technical barriers toHungary’s exports to the EU can be indi-rectly evaluated, by estimating the actualdifferences in standards, technical regula-tions, and certification systems. The greaterthe similarity of the two sets of require-ments, the fewer difficulties Hungary’s ex-ports will encounter in the EU. Analysing theharmonization and evaluating its completionmay reveal the existence or absence of tech-nical barriers to Hungary’s exports to theEU.

Moreover, meeting the harmonizedrequirements of EU technical regulationsand standards can be regarded as a basiccondition for free movement of goods andservices. The White Paper requires the im-plementation of all European Standards asvoluntary national standards. To complywith the internal market and achieve fullmembership of the European standards or-ganizations (CEN and CENELEC), the pace ofadaptation to European Standards has to becontinuous and dynamic. A special means oftransposition is the endorsement notice,which is employed in special fields wherenational standards committees have not beenformed (signalling lack of interest). It is alsoemployed where the circle of users is lim-ited, standards are subject to frequentchange, and use of the English languagecauses no difficulties (e.g. in telecommuni-cations).

Hungary has made steady progresssince the beginning of its accession negotia-tions with adoption of and harmonization toEU standards, technical regulations, andcertification. Screening of the chapter on thefree movement of goods was effected inSeptember 1998. The Position Paper, and asrequested by the Commission, two additionaldocuments containing supplementary in-formation were submitted after the negotia-tions. Guaranteeing the conditions of thefree movement of goods by the date of ac-cession means taking over in full the so-

called horizontal rules on operation of thesingle market, as well as legislation regulat-ing the marketing of individual productgroups and the safety of products. In areasnot regulated by the Community, Hungarymust enforce the principle of the freemovement of goods, in other words, harmo-nize its national legislation with Articles 28,29 and 31 of the Amsterdam Treaty andwith Council Directive 70/50/EEC. Thescreening of the Hungarian legislation iden-tified a range of measures whose amend-ment was found necessary before accession.

2.1. Adopting and harmonizing hori-zontal and procedural measures

With horizontal and procedural measures,Hungary has gradually speeded up its adop-tion of European standards as Hungariannational standards, in line with the Acces-sion Partnership priorities. The governmenthas striven to create conditions that allowthe Hungarian Standards Institution to adoptthe requisite quantity of European standardsby the accession date. The plan was also tojoin CEN and CENELEC before accession.National standards that have remainedmandatory will be replaced by suitable leg-islation and all standards will become vol-untary.

In 1997, the Hungarian governmentstarted negotiations with the EuropeanCommission towards concluding a Protocolon European Conformity Assessment. At thattime, the negotiations covered the followingareas:* Machinery.* Low-voltage equipment.* Electromagnetic compatibility.* Telecommunications terminal equipment.* Electrical equipment for use in potentially

explosive atmospheres (ATEX).* Medical devices, pharmaceutical prod-

ucts (Good Laboratory Practice, GoodManufacturing Practice).

7

These negotiations, which precededthe beginning of the accession negotiationsby about a year, were in themselves evidencethat Hungary had reached a high enoughlevel of harmonization in the cited fields ofthe Single Market to be considered as a po-tential partner. The progress was acknowl-edged positively in 1997 by the EuropeanCommission, in its Opinion on Hungary'sapplication for membership.

Measures implemented in 1998In 1998, the Hungarian government

set itself the aim of continuing and acceler-ating the adoption process and implement-ing more than 1000 European standards. Inthe event, 1398 European standards wereadopted, of which 953 involved an en-dorsement notice. By the end of that year,3266 of the total of about 8500 Europeanstandards had been introduced in Hungary.(See Table 1 on page 16) Accession negotia-tions began in March 1998.

Measures implemented in 1999The process of approximation of laws

required for EU membership involved sev-eral measures being implemented in 1999,which was the first year after the start of theaccession negotiations. The Hungarian Stan-dards Institution (HSI) adopted 3306 Euro-pean standards as Hungarian national stan-dards, by contrast with a planned 2925. Ofthose adopted, 639 were done so in Hun-garian and 2667 with an endorsement no-tice. Thus the HIS had adopted 6581 of thethen 10168 European standards as Hun-garian national standards by December 31,1999, which meant the implemented pro-portion had risen from 37 per cent to 65 percent in one year.

Within this, the implemented propor-tion of CEN standards was 61 per cent andof CELENEC standards 65 per cent. Of theEuropean standards harmonized to the NewApproach Directives the implemented pro-portion reached 81 per cent, from 38 percent in December 1998. Of the standardsimplemented by December 31, 1999, 4065(62 per cent) were adopted with an en-dorsement notice. It could be seen that the

implementation process had speeded upsuccessfully.

Several legal regulations listed in theAppendix were harmonized in 1999. In ad-dition to these, several legal regulations wereamended in line with the preparation for theProtocol on European Conformity Assess-ment (PECA), whose drafting, as a supple-mentary protocol to the Europe Agreement,is at an advanced stage.

Measures implemented in 2000By May 1, 2000, 6884 of the 11,456

European Standards had been adopted asHungarian national standards, which wasan implemented proportion of 60 per cent.With 64 per cent of the implemented stan-dards, endorsement notices had been ap-plied, so that the standards have been im-plemented in English. The proportion ofEuropean standards harmonized to the NewApproach Directives was 82 per cent.

The harmonization process meant thatby September 2000, the HSI had imple-mented 7428 CEN standards as nationalstandards and including 1137 Europeanstandards harmonized to the New ApproachDirectives. This represented 76.6 per cent ofall European standards and 79.7 per cent ofEuropean standards harmonized to the NewApproach Directives (Table 3 on page 17).

It could be said again that the imple-mentation process had been successfullymanaged by the HSI. By the end of 2000,about 3200 European standards were im-plemented, of which 500 were in Hungarianand 2700 implemented with an endorse-ment notice. Thus, the 80 per cent imple-mentation rate (9685 standards and techni-cal regulations implemented in Hungary outof a total of about 11500 European stan-dards and technical regulations) necessaryfor CEN and CENELEC membership had beenachieved and an application for such mem-bership could be made at the beginning of2001.

Measures to be implemented in 2001According to Hungarian Government

Resolution No. 2147/1999. (VI. 23), furthersteps need to be taken to sustain or acceler-ate the Hungarian standardization process in

8

the coming period. In 2001, 2719 Europeanstandards have to be implemented, 2200 ofthem in English. It is expected that almostfull implementation can be attained by theend of the year.

Measures to be implemented in 2002The subsequent task is to ensure con-

tinual adaptation to new European Stan-dards issued. About 1500 new standards areexpected to be implemented in 2002, ofwhich 1000 will be in English. It is govern-ment policy to support further developmentto implement standards and promote activeHungarian involvement as CEN andCENELEC members, with the ability to exe-cute all related functions.

According to the various EU assess-ments, Hungary has made continual prog-ress with horizontal and procedural meas-ures in recent years. Meeting the harmo-nized requirements of the European techni-cal regulations and standards is regarded asbasic to the free movement of goods andservices. The Hungarian system of standardsand technical regulations already complieswith the EU internal market, and Hungaryhas fulfilled the prior conditions for full CENand CENELEC membership. Full implemen-tation of European standards and technicalregulations will be attained by the end of2001. The Hungarian government is par-ticularly concerned to ensure continual ad-aptation to the new European Standards is-sued.

2.2. Sector-specific legislation

Since the beginning of the accession nego-tiations, Hungary has aligned sector-specificlegislation in the following fields:(a) Good manufacturing practice for hu-

man medicines.(b) Good laboratory practice of human

medicines and pesticides.(c) Wholesale distribution of human

medicines.(d) Medical devices for human use.

(e) Colorants for medicines.(f) Residue limits of veterinary medicinal

products in foodstuffs.(g) Novel foods and ingredients.(h) Natural mineral waters.(i) Packaging and labelling of foodstuffs.(j) Migration of plastics coming into

contact with foodstuffs.Further alignment that can be consid-

ered as significant progress occurred inother product areas in the course of 1999and 2000:(a) Motor vehicles.(b) Quality of petrol and diesel fuels.(c) Tyre pressure gauges.(d) Electromagnetic compatibility.(e) Electrical equipment used in poten-

tially explosive atmospheres in mines.(f) Calibration of the tanks of vessels.(g) Good laboratory practice for chemi-

cals.(h) Crystal glass.(i) Recreational crafts.(j) Some pieces of legislation were

adopted in the field of legal metrology.The alignment activity means that a

large part of the sector-specific acquis is alsoin place.

The outstanding legislative issues re-late mainly to:(a) Pharmaceutical products (including

pricing rules and marketing authori-zations).

(b) Cosmetics.(c) Chemical substances.(d) Metrology.(e) Construction-sector products.

The National Programme for Adoptionof the Acquis (NPAA) includes measures oflegislative approximation envisaged beforeaccession, with schedules of implementation.The main product groups are the following:

1. Motor vehiclesTwo items of legislation on legal har-

monization concerning the technical aspectsof motor vehicles were published in May

9

2000: Decree No. 11/2000. (V. 24.) KHVMof the Minister of Transport, Communica-tion and Water Management (amending De-cree No. 5/1990 (IV.12) KöHÉM of theMinister of Transport, Communications andConstruction on the technical testing ofmotor vehicles) and Decree No. 12/2000.(V. 24.) KHVM of the Minister of Transport,Communication and Water Management(amending Decree No. 6/1990 (IV.12)KöHÉM of the Minister of Transport, Com-munication and Construction on the techni-cal conditions of maintaining motor vehiclesin traffic). Most of the harmonized require-ments provided for in these decrees enteredinto force on July 1, 2000. Additional rules––in accordance with the rules governingentry into force within the Community––will become effective gradually, at the latestby the date of accession. The related tasks ofinstitution development and the cost impli-cations of these are presented under Section4.5 Transport of the NPAA.

2. Chemical substancesHarmonization and institutional-

development tasks related to the rules appli-cable to dangerous chemical substances arepresented in Section 5.2 Employment andsocial affairs of the NPAA. Information onfertilizers is provided under Section 4.2 Ag-riculture of the NPAA. Harmonization ofrules applicable to the marketing and super-vision of explosives for civil use will be im-plemented according to the provisions of theprogramme on legal harmonization by theend of 2001, with the Ministry of EconomicAffairs responsible. Council Directive92/109/EEC and Regulation 1485/96/ECregulate the control of drug precursors.Government Decree No. 100/1996. (VII.12.) Korm., on procedural rules for certainchemicals used for illicit manufacture ofdrugs, implements almost full harmoniza-tion. The missing provisions will be intro-duced in an amendment to the decree, butthe current licensing and reporting obliga-tions will be retained until accession forcontrolled substances where Communitydirectives specify less stringent obligationsthan the Hungarian regulations.

3. PharmaceuticalsAbout 25 pieces of legislation con-

cerning medicines for human use set forthprocedures and requirements based on Di-rective 65/65/EEC, as the fundamental di-rective for testing procedures, licensing ofregistration, supervision of manufacturing,and testing, distribution, labelling and ad-vertising. Partial harmonization of 13 legalregulations has been implemented and fullharmonization – excluding fields affected bytransitional measures that Hungary re-quested – will be implemented by the Min-istry of Health in line with the entry intoforce of PECA, but at the latest, by the date ofaccession. The Ministry of Health will alsoperform the preparatory tasks related to theentry into force of the relevant Communityregulations. Tasks of harmonization withCommunity rules applicable to medicines forveterinary use were performed by the Min-istry of Agriculture and Regional Develop-ment by the end of 2000.

4. CosmeticsDirective 76/768/EEC on cosmetics,

with its 30 amendments and 11 supplementspublished, sets forth the fundamental re-quirements, the allowable and prohibitedsubstances, the testing procedures and theinternational nomenclature. Current Hun-garian legislation provides for partial har-monization. Full harmonization will be im-plemented in 2001.

5. MetrologyDirectives on legal metrology are be-

ing taken over in two phases. The regula-tions unaffected by new Community rulesunder preparation such as the MID Direc-tive were harmonized during 2000. So longas it is promulgated by then, the new MIDDirective will be harmonized in 2002. In theabsence of the new legislation, harmoniza-tion will be based on the old directives.

6. Electrical equipmentWith the harmonization of the new

ATEX Directive (94/9/EC), legal harmoni-zation in this field will be fully effected in2001.

10

7. MachineryHere legal harmonization was fully

completed in 1999.8. Crystal GlassThe Ministry of Economic Affairs, in

charge of the legal harmonization in thisarea, effected it in full in 1999.

9. LiftsIncorporation of the related Commu-

nity rules into domestic legislation has be-gun. Full harmonization with Council Di-rective 95/16/EEC will be implemented bythe Ministry of Agriculture and RegionalDevelopment and the Ministry of EconomicAffairs, by the end of 2001. The Europeanstandards in this area were adopted by theend of 2000.

10. Personal Protective EquipmentHere the legislation is partially harmo-

nized in Hungary. To gain full harmoniza-tion, an additional decree was issued in2000 and will be implemented by the end of2001. By February 1, 2000, 190 harmo-nized standards had been issued, 135 ofthem as national standards. Adoption of 35standards is in progress.

11. Medical devicesThe two main directives (93/42/EEC

and 90/385/EEC) related to medical devicesfor human use and the introduction of ap-proximately 120 related standards havebeen implemented, in line with the prepara-tions of the PECA agreement, by Decree No.47/1999. (X. 6.) EüM of the Minister ofHealth on medical devices and Decree No.48/1999. (X. 6.) EüM of the Minister ofHealth on the rules of the designation of theorganizations testing, inspection and certifi-cation the conformity of medical devicesfunctioning under the technical supervisionof the Ministry of Health. Under the direc-tion of the Ministry of Health, harmoniza-tion with Community legislation on medicaldevices used for in vitro diagnostics will beimplemented by the end of 2001. The Min-istry of Agriculture and Regional Develop-ment harmonized the rules on electro-medical equipment used in veterinary medi-cine in 2000.

12. Burning-gas appliancesThe legislation providing for harmoni-

zation with relevant Community legislationwas promulgated and entered into force in1999.

13. Pressure vesselsHarmonization with relevant Commu-

nity directives was carried out by the Minis-try of Economic Affairs in 2000.

14. Construction productsThe Ministry of Economic Affairs and

Ministry of Agriculture and Regional Devel-opment will implement full harmonizationwith Council Directive 89/106/EEC andrelated legislation by the date of accession.

15. Recreational craftsThe Ministry of Transport, Telecom-

munication and Water Management willissue a ministerial decree implementingharmonization with Directive 94/25/EC ofthe European Parliament and the Councilafter the Act on Water Traffic enters intoforce. Parliament passed the act in April2000 and its provisions entered into forceon the first day of 2001, along with desig-nation of the institutes for testing, inspectionand certification.

Where alignment is complete, one im-portant task is to eliminate the previous pre-market controls, in line with the AccessionPartnership priorities. Furthermore, suffi-cient administrative capacity needs to bebuilt up in the field of marketing authoriza-tions for medicines. With foodstuffs, Hun-gary needs to continue to introduce the rele-vant structures for inspection and analysis.

2.3. Non-harmonized areas

Council Directive 98/34/EC provides forexchange of information among member-states on technical regulations and stan-dards. Commission Resolution3052/95/EEC provides for this in non-harmonized areas. The responsible Ministryof Economic Affairs and Ministry of ForeignAffairs plan to implement legal harmoniza-

11

tion in the year leading up to accession, inline with the entry into force of the Protocolon European Conformity Assessment (PECA).

Hungary started internal screening ofits domestic legislation in non-harmonizedareas, to identify legislation that could pre-vent de jure or de facto free movements ofgoods. Internal screening by the Ministry ofEconomic Affairs of measures hindering themovement of goods is to continue andshould lead to the elimination of incompati-ble provisions. The aim is for the principle ofmutual recognition to be well established byaccession.

In December 1999, the modules forthe various phases of the conformity assess-ment procedures and the rules on the use ofthe CE marking of conformity were trans-posed. The CE marking will be used in Hun-gary except in cases requiring third-partycertification, where the 'H' mark will replacethe CE marking until accession, other thanin the sectors covered by the protocol to theEurope Agreement on Conformity Assess-ment and Acceptance of Products, initialledin July 2000. This agreement covers:(a) Machinery.(b) Electrical safety.(c) Electromagnetic compatibility.(d) Hot water boilers.(e) Gas appliances.(f) Medical devices.(g) Good laboratory practice for human

medicines.(h) Good manufacturing practice for hu-

man medicines as regards inspectionand batch certification.The PECA agreement between the EU

and Hungary was signed in February 2001.This accepts the mutual-recognition princi-ple for conformity assessment. Mutual ac-ceptance of quality-control certificates in theeight product groups just mentioned willease trade between the EU and Hungary andsecure conformity with European technicalsystems. The range of product groups cov-ered by this agreement can be extended oncefurther preconditions are met. Negotiationscontinue on four more product groups and

have to be completed by accession. Exceptfor ‘explosive instruments’, the productgroups will cause no significant problems toadopt.

2.4. Accreditation and certification

Legislative conditions were provided by ActXXVIII/1995 on national standardization,which incorporated EU requirements. Theorganizational system is well structured andthe requisite professional level assured.However, the information system of the HSIstill has to be developed.

Approximation of law in itself does notestablish conditions of the free movement ofgoods. In areas regulated by Communitylaw, manufacturers must apply conformityassessment and inspection procedures, inline with the modules for conformity as-sessment, depending on the risk arising fromuse of the product (as set forth in CouncilDecision 93/465/EEC). For this reason, it isnecessary to put in place a set of appropriateinstitutions.

These institutions will cover the activi-ties of the testing and certification bodies,the inspection authorities, the accreditingbodies and the organizations in charge ofdesignation. The comprehensive system to beestablished will have to guarantee the con-ditions for free movement of goods whileproviding a flexible framework for eco-nomic agents. Ministries have issued severalorders under the authorization conferred byGovernment Decree No. 182/1997. (X.17.)Korm., on the designation of the bodiestesting, inspecting and certifying the con-formity of technical products.

In 1999, the Hungarian AccreditationBoard became a full member of the Euro-pean Cooperation for Accreditation (EA).Furthermore, a Notification InformationCentre was set up at the Ministry of Eco-nomic Affairs in September 2000, to preparefor Hungary’s acquis obligations in notifica-tion and information of technical standardsand regulations.

12

Further institutional progress wasmade in 2000, when alignment was com-pleted in nine sectors and market-surveillance bodies were designated. Hun-gary adopted legislation in 1997 authorizingeach ministry in its area of competence todesignate bodies for testing, inspecting andcertifying the conformity of products to theNew Approach Directives.

This authorization has already beenmade for industrial products within thecompetence of the Ministry of EconomicAffairs:(a) Machinery.(b) Toys.(c) Electrical equipment.(d) Gas-burning appliances.(e) Certain construction products.

It has also been done for some othersectors:(a) Telecommunications and information-

technology products.(b) Medical devices.(c) Personal protective equipment.

The technical capacity of several ofthese bodies is being upgraded, as requestedin the short-term Accession Partnership pri-ority.

As the principles of the New andGlobal Approach are introduced, the neces-sary infrastructure for regulation, standardi-zation, accreditation and certification is be-ing established. The HSI is a full member ofthe European Telecommunications Stan-dards Institute and the International Stan-dards Organization.

Efforts to accelerate the adoption ofEuropean standards mean that the require-ments for full membership of the CEN andCENELEC have also been met in the main.The organization and procedures of the HSI,the Hungarian Accreditation Board and theHungarian National Office of Measurementsbroadly appear to meet the needs of the ac-quis.

With safety checks on products, Hun-gary still needs to establish an appropriatecustoms and market surveillance infra-structure and effective administrative coop-

eration among competent authorities. Atpresent, there are only limited or no safetycontrols at the border. The capacities of thetesting and certification bodies need to beenhanced and their independence from theregulator ensured.

The main market-surveillance body,the General Inspectorate for Consumer Pro-tection, also houses the secretariat of theTransitional Rapid Information System onDangerous Products (TRAPEX), an informa-tion-exchange mechanism covering tencandidate countries.

2.5 Conclusion

As the area in which the harmonization re-quirements of European standards and tech-nical regulations are met by the Hungariansystem of standards and technical regula-tions has been spreading gradually, thereshould be progressively fewer cases of con-flict, where EU standards and technicalregulations hinder Hungarian industrial ex-ports. Transfer of EU standards and techni-cal regulations to the Hungarian economyfulfils another basic condition for the freemovement of goods and services.

According to the EU assessment, Hun-gary’s progress in transposing Europeanstandards and technical regulations has beensuccessful and met the requirements forjoining the European standards organiza-tions (CEN and CENELEC). Since the har-monization process has surpassed a level of80 per cent, the Hungarian economy can bebroadly seen as part of the EU single market.The process will be completed in the currentyear, after which the authorities will stillhave to ensure continual adoption of newEuropean standards and technical regula-tions. In Hungary’s case, the European stan-dards and technical regulations can nolonger be considered as technical barriers totrade.

13

3) MEASURING THE EFFECTS OF TBTS

Many experts rate among the hardest toquantify the non-tariff barriers whereregulatory and/non regulatory certificationmechanisms are designed in such a way asto put imports at a disadvantage to domesticgoods. This could be an important issue,since the differences in national technicalregulations can be significant trade barriers.However, it is not the differences that mat-ter, but whether the standards apply differ-ently to imports than to domestic goods.

The question is how costly the differ-ence is for an imported good. These extracosts can be a barrier high enough to hinderthe trade. Although it is very difficult togauge the disadvantage for imports if regu-latory and/non regulatory certificationmechanisms are designed in a way that fa-vours domestic goods, some types of calcu-lation can be made.

3.1 Methods of measuring TBTs

The literature on the subject includes rela-tively few attempts to devise methods ofmeasuring the effects of TBTs. Those thereare belong to four basic types:

1. Price comparisons of domestic andimported goods

Price comparisons of domestic goodsand imports of the same type seem to be thesimplest way to assess inter-country differ-ences in standards. However, simply to useprice comparisons may be of limited use,since the differences may reflect factorsother than TBTs. To extract from affected in-dustries credible assessments of the costs ofthese trade barriers is very uncertain.

2. Foreign-trade statisticsAnother type of simple analysis may be

to compare the shares of export products tothe EU that are exposed to European stan-dards and technical regulations with theshares of the same products exported to

other destinations. Its use can be also limitedby several factors. The differences may notnecessarily reflect technical barriers alone.

3. Evaluations by technical expertsAnother way to evaluate differences in

standards and regulations is to gather in-formation from technical experts. Those fa-miliar with the details of these rules can ap-ply them to particular products and proc-esses. Although this may turn out to be adifficult task, estimates of the added costs in-volved may be possible under the followingconditions:(a) If higher standards are applied to im-

ported goods than to domestic goods.(b) If regulations are enforced more rigor-

ously on imported goods than on do-mestic goods.

(c) If imports are subjected to more cum-bersome and costly certification pro-cedures than domestic goods.4. Questionnaire-based analysisHere producers and traders are asked

various questions about their experienceswith EU standards and technical regulations.The questions focus on the tradability of theproducts, conformity with the standards,and additional tasks (e.g. investment, pro-duction etc.) deriving from the EU regula-tions.

3.2. Analysis of TBT

The applicability of the four methods justlisted to Hungarian exports to the EU israther limited. The practical use of pricecomparisons of domestic and importedgoods is difficult or impossible. There is noinformation, or gathering the information isdifficult and unreliable. Moreover, themethod has endogenous shortcomings, aswas mentioned above.

Analysis of the commodity structure ofHungary’s exports to the EU shows that OldApproach products have a greater sharethan New Approach products. However, theshare of New Approach products in EU im-

14

ports from Hungary has been greater thantheir average share of imports from existingmember-states. Mutual-recognition prod-ucts have had far less importance in Hun-gary’s exports. Products not exposed to sig-nificant technical barriers hold a smallershare, which declined from 34 to 17 percent between 1989 and 1999. Meanwhile,the share of New Approach products in-creased from 9 to 16 per cent and the shareof mutual-recognition products also grew,from 18 to 27 per cent. There has been nosignificant change in the share of Old Ap-proach products. These trends show thatimplementation of EU standards and techni-cal regulations have not caused significantproblems for Hungarian producers. Adapta-tion to the new requirements has been car-ried out quite smoothly.

Methods based on the evaluations oftechnical experts have several practicalproblems that hinder their application. Thegeneral suggestion (see Deardorff and Stern,1998) is to use formulae (I.C.2) for TEEXP or(I.E.3) for TEOWN, based on comparisonswith other export markets or with the do-mestic market of the exporter.1. If imports and domestic goods are sub-

ject to different standards and the costsof satisfying these are known, the tariffequivalent can be calculated by formula(IX.A) for TESTAND1.

2. If imports and domestic goods are sub-ject to a single standard that is enforceddifferently for imports than for domesticgoods, formula (IX.B) for TESTAND2 can beused in terms of fractions of units of thegood that satisfy the standard.

3. If certification requirements are differentfor domestic and imported goods, thecosts of certification can be used as thecosts of the standards themselves, ac-cording to the formula (IX.A) for TES-

TAND1.4. A questionnaire seems to be the most re-

liable method for the time being. It pro-vides sufficiently good results for the ef-fects of technical barriers to trade. Thefindings of such a survey are discussedin the next section.

4. FINDINGS OF A HUNGARIANSURVEY ON TBTS WITH THE EU

Trade with the EU is vital to Hungary, forwhich the EU is the most important tradingpartner. The Europe Agreement (signed inDecember 1991) means that industrial ex-ports are already free of customs duties.However, as with other free-trade areas andwithin the EU, some non-tariff barriers re-main.1 The main ones are technical barriersto trade (TBTs), which occur when a pro-ducer may have to alter his product to com-ply with health, safety, environmental etc.issues imposed by governments or organiza-tions. During the 1990s, the main steps toeliminate non-tariff barriers between the EUand Hungary were these:* From the entry into force of the trade

provisions of the Europe Agreement (inMarch 1992), the EU eliminated allquantitative restrictions on industrial im-ports from Hungary, except for importsof textile and clothing products. For thisgroup, quantitative restrictions wereeliminated on January 1, 1998.

* Voluntary export restraints in industrialtrade were also eliminated with the entryinto force of the trade provisions of theEurope Agreement. There were twoagreements of this type covering indus-trial products (steel and textile products).Restrictions on steel exports ceased on thefirst day of the implementation of theEurope Agreement trade provisions. Thevoluntary export restraints covering tex-tile and clothing products changed inform between 1992 and 1997. They werereplaced by a special protocol under the

1 Apart from the Europe Agreements, there have beenseveral regional trade agreements reached in Europein the last decade, so that the trading architecture is ahub-and-spoke system of bilateral regional tradeagreements. CEE countries are involved in 71 bilat-eral and eight multilateral free-trade agreements(Sapir, 2000). The large number of trade agreementscreates administrative costs and the role of the rulesof origin and non-tariff or technical barriers is in-creasing.

15

Europe Agreement, which existed untilthe first day of 1998.2

* The EU has taken other price-controlmeasures, but they affect agriculturalproducts. The Europe Agreement does notprovide for Hungary adopting the legis-lation and regulations of the single mar-ket. Although Hungary has made stridestowards harmonization of regulation inthis field – partly under the programmeinitiated in 1995 by the Cannes meetingof the European Council and partlyautonomously – some non-tariff barriersremain. One group consists of technicalbarriers such as technical requirements,quality certificates, etc. The research fo-cuses on assessing the impacts of suchbarriers.

4.1. Foreign trade patterns betweenHungary and the EU

In terms of the geographical structure ofHungarian trade, 76.2 per cent of exportsand 64.4 per cent of imports were realizedwith the EU in 1999. During the 1990s, theproduct structure of all Hungarian exportsunderwent major changes (Table 1). The in-dustry classification used here is based onthe OECD (1993) method set out in theISIC.3 The three groups are high-technology, 2 The Europe Agreement allows anti-dumping andcountervailing measures to be applied by either side ifconditions warrant. During implementation of theEurope Agreement, the EU took three anti-dumpingdecisions against Hungarian industrial imports(Meisel, 2000). Such measures became less frequentin the 1990s. The first, formulated in 1993, coveringcertain Hungarian exports of steel tubes, led to aquantitative restrictions on the Hungarian exporter(Csepel Tube). The second came in 1998, againstHungarian exports of polypropylene cords. Two firmswere involved: TVK and a small firm, Partium. As aresult, TVK ceased production of the product, whilethe second firm made a price undertaking. The lastanti-dumping measure was taken in 1999 againststeel wires exported by Diósgy r Wire-Goods. Theoutcome was again a price undertaking by the Hun-garian firm. A fourth anti-dumping complain wasformulated in 1996 against a Hungarian firm ex-porting certain steel products (U and I shapes), butEurofer withdrew the complaint.3 The indicator of technological intensity (weighted

medium-technology and low-technologyproducts.4 All calculations for foreign tradeare made at SITC (Standard InternationalTrade Classification) 5-digit product level(3464 items) given by the Eurostat Comextdatabase.5 Data were later converted to theISIC Rev3 classification, to apply the tech-nology-intensity groupings just mentioned.

The table shows that the share of thehigh-technology industries in manufactur-ing exports rose very rapidly, more than tri-pling to 34 per cent in the seven years to1998. The increase was due to three sub-sectors: electrical machinery, telecommuni-cations equipment, and office machinery.Meanwhile, the traditionally importantpharmaceutical sector lost share. Medium-tech sectors increased share to a much lesserextent, the rise coming almost entirely frommotor vehicles. The share of the low-techsectors fell rapidly, mainly due to the foodand beverage, textile and clothing, and basicmetal branches.6 On the import side (notshown in the table), the share of high-techgroups in Hungary’s imports from the EUwas 23.46 per cent in 1999, while the me-dium-tech and low-tech groups had sharesof 51.26 and 25.28 per cent respectively.

according to sectors and countries) is the share of Rand D expenditures in production or value-added.4 Based on experience, the OECD at the end of the1990s revised the grouping (Hatzichronoglou, 1997),dividing the medium-tech group into two, to createmedium-high and medium-low groups with preci-sion instruments and electrical machinery beingplaced in the former. However, the old grouping isapplied here.5 The EU is reporting here: ‘Hungarian exports to theEU’ means EU imports from Hungary.6 The fall in share masks a rise in the absolute valueof low-tech exports.

16

Table 1Shares of industries in Hungarian manufacturing exports

(%)

ISIC Sectors 1990 1993 1996 1997 1998 1999High-technology: 9.73 16.26 25.84 32.57 34.54 34.142423 Pharmaceuticals 0.37 0.29 0.12 0.11 0.08 0.0830 Office machinery 0.18 0.90 3.22 6.99 9.22 9.3532 Radio, TV sets 1.47 2.02 6.56 9.81 10.97 10.0431 Electrical machinery and appliances 7.05 11.74 14.74 14.48 13.01 13.22353 Aircraft, spacecraft 0.04 0.18 0.03 0.02 0.03 0.0233 Medical, precision, opt. instruments 0.62 1.14 1.17 1.16 1.23 1.43Medium-technology: 23.52 24.62 32.92 34.66 37.12 42.30241 Organic, inorganic basic chemicals 7.55 5.36 4.01 3.50 2.65 2.34251 Manufacture of rubber products 1.42 1.31 1.25 1.17 1.20 1.20252 Manufacture of plastic products 0.45 0.84 0.90 0.95 0.81 0.92272-73 Non-ferrous metals. aluminium 3.74 2.37 2.77 2.68 2.00 1.9229 Machinery and equipment 7.94 7.01 5.92 5.41 5.26 4.97352 Railway and tramway locomotives 0.02 0.14 0.22 0.24 0.37 0.4634 Motor vehicles, trailers 1.25 5.21 16.30 19.51 23.71 29.32354 Manufacture of bicycles, motorcycles 0.01 0.04 0.08 0.05 0.05 0.06355 Manufacture of transport equ. n.e.c. 0.00 0.00 0.01 0.01 0.01 0.0136,37 Other manufacturing industries 0.69 0.89 0.66 0.60 0.52 0.58242-2423 Chemical pr. except pharmaceuticals 0.44 1.44 0.80 0.56 0.54 0.53Low-technology: 66.75 59.12 41.24 32.76 28.34 23.5615,16 Food, beverages, tobacco 19.94 13.96 8.53 6.21 4.77 4.8117-19 Textile, clothing, leather 24.79 27.22 16.42 13.54 11.68 7.2920 Wood and wood products 4.83 4.68 3.89 3.26 3.22 3.0721-22 Paper and printing 1.26 1.18 1.01 1.05 0.96 0.93231 Manufacture of refined petroleum pr. 2.53 1.59 2.50 1.53 1.16 1.36232 Coal and petroleum products 0.51 0.25 0.11 0.07 0.03 0.0326 Other non-metallic minerals 2.37 2.90 1.81 1.51 1.40 1.47271 Manufacture of basic metals 6.88 2.27 2.85 2.02 2.04 1.4428 Fabricated metals 3.48 4.65 4.11 3.54 3.07 3.15351 Building, rep. of pl. and sporting boats 0.16 0.43 0.02 0.03 0.01 0.02D Manufacturing 100.00 100.00 100.00 100.00 100.00 100.00Source: Éltető (2000)

Looking at total Hungarian-EU trade atSITC 5-digit product level, it emerges thatthe top ten product groups were responsiblefor 42.8 per cent of total exports to the EU in1999, which was a considerable increaseover the 13 per cent share in 1990 (Table2). The structure of the top ten changedcompletely in the 1990s. The leading exportproduct in 1990 – footwear – vanished fromthe list, as did agricultural and other non-machinery products. Instead came high-techand medium-tech products produced by asmall number of multinational affiliates,mainly in customs-free zones.7 The structure

7 A salient feature of Hungarian foreign trade today isthe activity of about 100 industrial customs-freezones, mainly in the machinery industry, with in-vestment coming mainly from greenfield, wholly for-eign-owned ventures. Their 1999 trade surplus was

of Hungary’s exports to the EU modernizedconsiderably in the 1990s, which meant atechnological upgrading as well.8 It istherefore interesting to see to what extentthe technical barriers helped to shape Hun-garian-EU trade.

USD 2091 million, from 43 per cent of all exportsand 30 per cent of imports. Their exports rose 30 percent in 1999, against a 3.2 per cent fall in traditionalexports.8 This is confirmed by specialization indices and in-tra-industry trade calculations (Éltető, 2000).

17

Table 2The shares of the top ten SITC 5-digit product groups

in total Hungarian-EU trade in 1999(%)

Product group ShareReciprocating piston engines 13.62Motor vehicle for the transport of persons 7.40Storage units for data processing 5.22Input/output units in data processing 3.15Ignition and other wiring sets 2.87Video recording or reproducing apparatus 2.86Television receivers and video recorders 2.68Parts and accessories for motor vehicles 2.50Compression-ignition engines 1.59Filament lamps 0.94

4.2. Experiences with the survey

The questionnaire survey designed to assessthe significance and costs of the technicalbarriers was prepared in early 2000 andsent to 1000 Hungarian firms active inmanufacturing. The 176 questionnaires re-ceived back (a return rate of 17.6 per cent)is not low by international standards. Ofcourse in some cases, not all questions wereanswered, so that the shares are given in thefollowing analysis as percentages of thevalid answer to each question.

1. Characteristics of the sampleThe respondents were mainly small

and medium-sized firms. Over two-thirds ofthem (68 per cent) employ fewer than 250persons, 14.3 per cent between 250–500persons, and 17.7 per cent over 500 em-ployees. This distribution is very differentfrom the general economic structure (Table3). The sample strongly over-represents big-ger companies and underrepresents small

Table 3Size structure of firms in the sample, the economy

and manufacturing(%)

Number ofemployees Sample

Hungarianeconomy,

1999

Manufac-turing, 1999

Less than 50 18.9 98.3 96.750–250 49.1 1.4 2.4250–500 14.3 0.2 0.5More than 50 17.7 0.1 0.4Data source: Central Statistical Office, Budapest.

ones, since small and micro-firms accountfor an overwhelming proportion of theHungarian economy. (The share of firmswith less than 10 employees was 90 per centin 1999. There are various reasons for thisrather unhealthy structure. Some micro-enterprises function only on paper, con-ducting no real activity, while others areunincorporated one-person businesses withvery restricted functioning. There is astrong difference in the size structures ofHungary and the EU.)

In their ownership structure, 48.8 percent of the respondents are firms in whichthere is foreign investment (FIEs), of which56.1 per cent are majority foreign-owned.9There is no foreign participation in 51.2 percent of the respondent firms. The share ofFIEs in the whole Hungarian economy was11.2 per cent of manufacturing firms in1999, so that these are over-represented inour sample. However, FIEs account for 80per cent of the manufacturing nominalcapital and net sales in the country and havedominated the performance of the Hungar-ian economy since the end of the 1990s.10

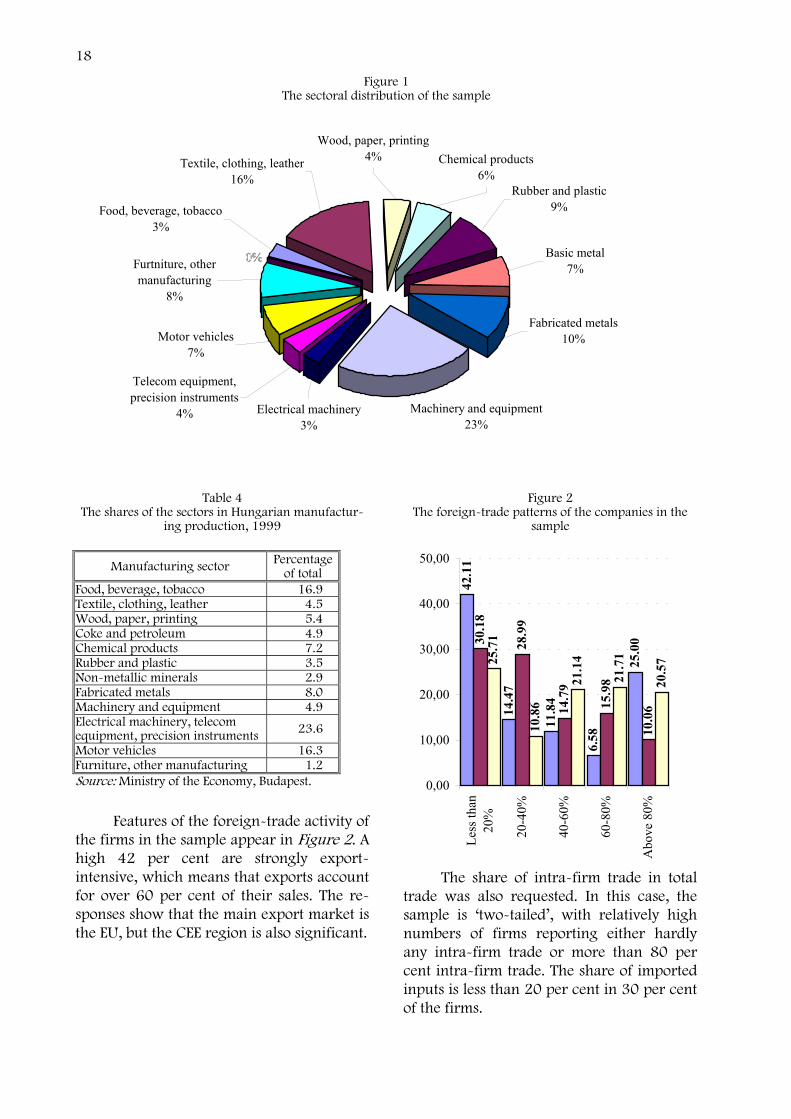

The sectoral distribution of the sampleshows that 88 per cent of respondent firmsbelong to the manufacturing sector. (Othersbelong to the trade, mining, construction,energy or not defined sectors.) The manu-facturing industries most strongly repre-sented are engineering, textile and clothing,motor vehicles and chemicals, but otherbranches such as furniture and metal proc-essing appear. Figure 1 shows the distribu-tion by manufacturing industries. This dis-tribution is based numbers of firms. Ma-chinery, textiles and metal processing arerepresented most strongly. The share in theproduction structure differs from the profileof Hungarian manufacturing, as Table 4shows. Three sectors have outstandinglyhigh shares of national production – electri-cal-precision machinery, motor vehicles,and food-beverages – with fabricated metaland chemicals also important.

9 Majority ownership means more than 50 per centforeign ownership.10 For more on this, see Éltető (2000) and Hunya(2000).

18

Figure 1The sectoral distribution of the sample

0%0%0% Basic metal7%

Rubber and plastic9%

Chemical products6%

Wood, paper, printing4%Textile, clothing, leather

16%

Furtniture, other manufacturing

8%

Motor vehicles7%

Telecom equipment, precision instruments

4% Electrical machinery3%

Machinery and equipment23%

Fabricated metals10%

Food, beverage, tobacco3%

Table 4The shares of the sectors in Hungarian manufactur-

ing production, 1999

Manufacturing sector Percentageof total

Food, beverage, tobacco 16.9Textile, clothing, leather 4.5Wood, paper, printing 5.4Coke and petroleum 4.9Chemical products 7.2Rubber and plastic 3.5Non-metallic minerals 2.9Fabricated metals 8.0Machinery and equipment 4.9Electrical machinery, telecomequipment, precision instruments 23.6

Motor vehicles 16.3Furniture, other manufacturing 1.2Source: Ministry of the Economy, Budapest.

Features of the foreign-trade activity ofthe firms in the sample appear in Figure 2. Ahigh 42 per cent are strongly export-intensive, which means that exports accountfor over 60 per cent of their sales. The re-sponses show that the main export market isthe EU, but the CEE region is also significant.

Figure 2The foreign-trade patterns of the companies in the

sample

42.1

1

25.0

0

6.58

11.8

4

14.4

7

10.0

6

28.9

9

15.9

8

14.7

9

30.1

8

20.5

7

21.7

1

21.1

425.7

1

10.8

6

0,00

10,00

20,00

30,00

40,00

50,00

Less

than

20%

20-4

0%

40-6

0%

60-8

0%

Abo

ve 8

0%

The share of intra-firm trade in totaltrade was also requested. In this case, thesample is ‘two-tailed’, with relatively highnumbers of firms reporting either hardlyany intra-firm trade or more than 80 percent intra-firm trade. The share of importedinputs is less than 20 per cent in 30 per centof the firms.

19

2. Evaluation of the responsesThe first main experience with the

survey was that some questions are simplynot relevant to the respondent firms. In thesecases, the number of missing responses(blanks) is very high. (The numbered ques-tions are reproduced in the Appendix.) Thefirst such question was No. 3: Would one ofthose difficulties be that EU technical regu-lations differ from national requirements?This question refers back to No. 2: Do youface any particular difficulties in exportingto the EU market compared with the domes-tic market? Because the majority (73 percent) answered no to No. 2, the subsequentquestions were not applicable.

The situation was somewhat similarwith No. 4a: Have you needed to redesignyour products for sale in the EU to meetthese requirements? The majority (85.6 percent) had answered no, so that the follow-upquestions were inapplicable and not an-swered in many cases.

The number of missing answers wasalso high for No. 6: If you had to redesignyour products to satisfy EU norms; has thishelped your sales in the domestic market orin the CEFTA countries? Again, this is be-cause most firms did not have to redesigntheir products.

These questions formed an essentialpart of the survey, referring to the existenceof technical barriers and their effects on thefirms. The fact that they remained unan-swered in large numbers shows the low im-portance of such barriers for Hungarianfirms.

With No. 1, it is reassuring that almostall (95.3 per cent) of the firms were awarethat EU accession means they have to takeover EU product-related legislation and itssystem of standardization by the date of ac-cession.

No. 2, already mentioned, showed thatfor the majority of the sample, exporting tothe EU was no more difficult than local sales.The majority (73 per cent) of the Hungarianfirms did not face particular difficulties withEU exports. However, for the 60 per centwho answered yes, one of the difficulties

was that EU technical regulations differfrom national requirements (No. 3), al-though they reported it as a moderate or mi-nor barrier to their EU exports.

Forty-five firms in the sample faceddifficulties in exporting to the EU marketcompared with the domestic market. (Theseanswered yes to No. 2.) Of these, 28 (62 percent) employed less than 250 persons and20 were FIEs. The export and import pat-terns of this sub-sample resembled those ofthe whole sample. However, the share of in-tra-firm trade in them was lower: less than20 per cent of total trade in 66.6 per cent ofcases. Of those reporting difficulties with EUexports, 63.6 per cent mentioned technicalregulations, but only 13.3 per cent thoughtthese a major barrier. Redesigning to meetEU requirements was reported by 33.3 per-cent of the firms, but 82.3 per cent of thesehad received no external support for doingso. Meanwhile 67.5 per cent were envisag-ing further investments to meet EU norms.(This was a considerably higher share thanin the whole sample). Furthermore, 26 percent thought the direct costs of obtaining acertificate would be ‘substantial’ (againhigher than in the whole sample). Twenty-five per cent of the firms had to satisfy dif-ferent technical requirements to export toCEFTA countries than to the EU or the na-tional market. Interestingly, 75 per cent ofthe firms reporting present difficulties inexporting to the EU expected an increase inexports from EU membership. This is con-siderably higher share than in the wholesample (59 per cent). Sixty-six per cent ofthese firms also expected accession to bringincreasing competition.

As mentioned already, 85.6 per cent ofthe responses to No. 4a were negative: firmshad not had to redesign their products. Forthose who did, it meant mainly a minor in-vestment (No. 4b), for which 86.9 per centreceived no support (No. 4c). Those who re-ceived support did so mainly from the for-eign investor. Regarding the future (No. 4d),56.5 per cent of the firms did not envisageadditional investments to meet EU norms.Apart from that, 83 per cent found the direct

20

costs of obtaining an EU certificate moderateor small (No. 4e).

Turning to the characteristics of the 24firms that had to redesign their products(which answered yes to No. 4a), they weresomewhat smaller than average for the sam-ple (71 per cent employing fewer than 250persons). Ten firms had foreign investmentand five were majority foreign-owned, sothat the group was mainly under domesticcontrol. Most (60.8 per cent) faced difficul-ties in exporting to the EU compared withthe domestic market, with different techni-cal regulations featuring among the diffi-culties in 85.7 per cent of cases. Contrary tothe general pattern, firms that had to redes-ign their products were more ready to makefurther investment, 74 per cent answeringthat they planned further expenditure tomeet EU norms. Redesigning of products hadhelped sales on the domestic market for 44per cent of the firms and on the CEFTA mar-ket for 50 per cent. This is also a significantdeviation from the pattern of the wholesample, where the proportions were muchless. The export and import patterns of thesefirms were more or less the same as for thewhole sample, except that they showedmuch lower shares of intra-firm trade.

No. 5 referred to the geographical dif-ferences in exports. Here the majority (87.9per cent) of respondents exporting to CEFTAcountries did not have to satisfy different re-quirements (from EU or from national re-quirements). For the low number of firmsanswering No. 6, redesigning the productshad not helped (64 per cent) orhad helped to a lesser extent(36 per cent) sales in local orCEFTA markets.

With No. 7, about thebenefits of harmonization withEU technical rules, firms werenot too optimistic: 92.4 per centof the sample expected har-monization to bring moderateor small benefits. Regarding expectations ingeneral, the questionnaire included No. 8:What do you expect from your country’s EUmembership? Two expectations proved high:increasing competition on the domestic

market for 59 per cent and increase in ex-ports also for 59 per cent.

The questionnaire contained also a ta-ble with the question: Please state whetherthe following measures related to the acces-sion to the EU will have an impact on yourfirm’s activities? Almost all of the firms inthe sample filled out this table according tothe following distribution (percentage):

Table 5The distribution of measures

Positive Noimpact Negative

Harmonization of technicalregulations and/or stan-dards with those of EU

61.1 35.8 3.2

Mutual recognition of yourcountry’s technical regula-tions and/or standards in EU

52.4 47.0 0.6

Conformity assessment pro-cedures 45.8 38.7 15.5

Elimination of customsdocumentation in trade withEU

91.8 6.4 1.8

Elimination of delays atfrontiers with EU 90.5 8.4 1.1

3. Sector-specific differencesAs mentioned earlier, certain manu-

facturing industries are strongly representedin the sample. The four most important(which have considerable weight in theHungarian economy as well) were selectedfor analysis, to see if there are sector-specificdifferences in the responses to the survey.The four industries appear in Table 6. It canalso be seen that the motor vehicle industryis by far the largest exporter.

The results show indeed that the sectorgroups have different characteristics fromthe whole sample, in relation to the techni-cal barriers to trade. The first issue where

Table 6The four most important industries represented in the sample

Sector No. of firms includedin the sample

Export sales of sectorin 1999, HUF billion

1. Textile, clothing, leather 25 223.32. Chemicals and rubber 24 396.43. Machinery 36 209.14. Motor vehicles 11 1190.1Data source: Central Statistical Office, Budapest.

21

this appears is the question of whether com-panies face any particular difficulties in ex-porting to the EU market. Figure 3 showsthat the majority of the firms in the groupsanswered no, as was the case with the sam-ple, but the machinery sector felt more af-fected by the difficulties, so that 32.3 percent answered yes. The picture is even moreuneven with the question of whether dif-fering EU technical regulations are one ofthose difficulties. Here two sector groupsshowed very high shares of positive answers:machinery and textile and clothing. Forthose firms, the main obstacles to EU exportsare technical barriers. A possible explana-tion may be the type of trade or cooperationprevalent among those firms. Those twosectors were the most heavily involved in the1990s in outward processing trade (OPT). Inthe early years, this concerned mainly thetextile-clothing branch, but later the OPTstructure shifted towards machinery. Thetechnical requirements of foreign partnersin OPT can be extremely strict and bindingon the Hungarian firms. Companies in themotor vehicle and chemical-rubber sectorsfelt fewer difficulties and fewer technicalbarriers to EU exports than the average formanufacturing.

Figure 3Yes answers in sector groups and the whole sample,

to the questions on export difficulties (No. 2)and different EU technical regulations (No. 3a)

26.9

22.2

32.3

24.0

23.1

6.7

56.3

33.3

75.0

30.0

0

10

20

30

40

50

60

70

80

Text

ile-

clot

hing

Che

mic

al-

rubb

er

Mac

hine

ry

Mot

orve

hicl

es

Tota

lsa

mpl

e

%

Difficulties Technical regulations

There were also considerable differ-ences among sectors in the efforts they hadmade to prepare products to fit EU standards(Figure 4). On average, 14.3 per cent offirms had had to redesign their products(No. 4a). However, the share was higher(22.2 per cent) in machinery and muchlower (7–10 per cent) in the other sectors. Itseems that the adaptation of products to EUstandards calls for more investment effort inthe machinery industry than in other cases.(In the latter, 16.7 per cent of firms indi-cated that this was a major investment, asopposed to 5.5 per cent of the whole sam-ple.)

Figure 4Yes answers in sector groups and the whole sample

to the questions on product redesigning (No. 4a)and planned additional investments (No. 4d)

14.3

10.0

22.2

8.3

7.7

43.4

51.6

38.1

26.1

22.2

0

10

20

30

40

50

60

Text

ile-

clot

hing

Cem

ical

-ru

bber

Mac

hine

ry

Mot

orve

hicl

es

Tota

lsa

mpl

e

%

Redesign Further investment

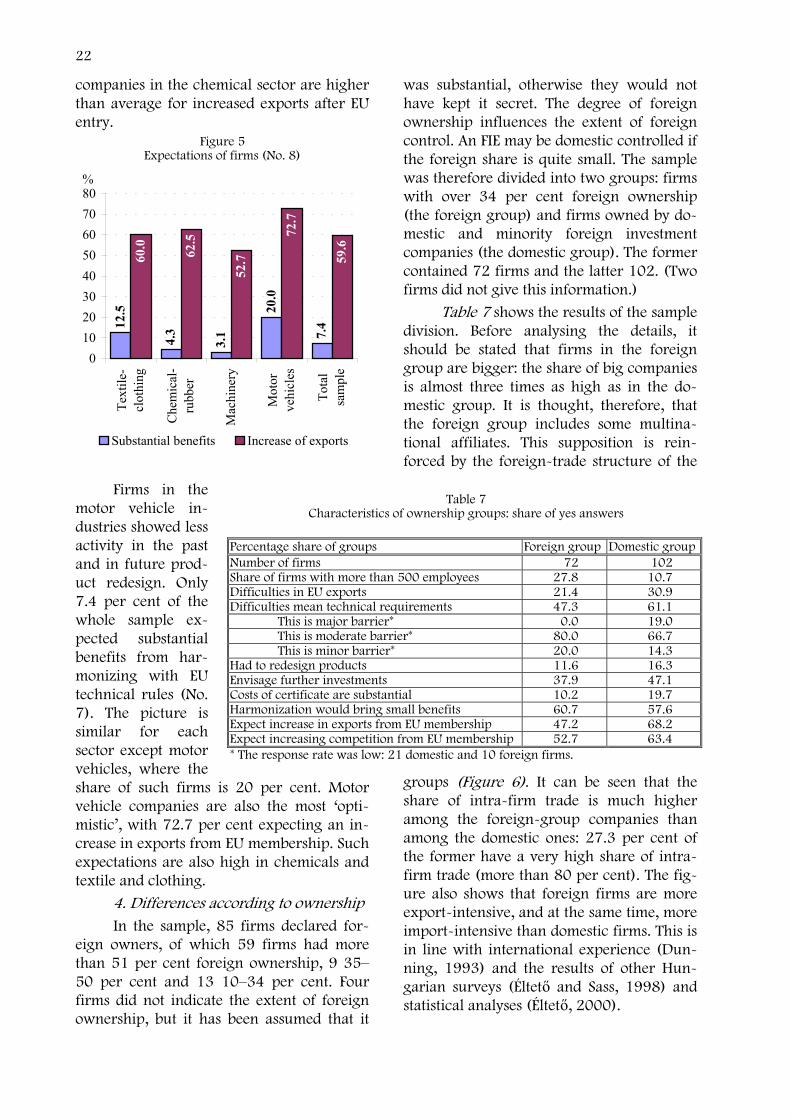

Regarding future investment to meetEU norms (No. 4d), the machinery sectoragain shows the highest share with suchplans. Here half the firms plan additional in-vestments. The share is also quite high in thechemical-rubber sector. It has been seen thatthis sector was one of the least affected byEU technical regulations: firms faced fewdifficulties in exports and had not redes-igned products. The reason may be that thechemical sector exports relatively less to theEU, because the CEE and developing regionsare also significant markets. However, as EUaccession approaches, firms plan to makeinvestments they have delayed hitherto, so asgain better access to EU markets. Indeed,Figure 5 shows that expectations among

22

companies in the chemical sector are higherthan average for increased exports after EUentry.

Figure 5Expectations of firms (No. 8)

7.4

20.0

3.14.312

.5

59.6

72.7

52.762

.5

60.0

01020304050607080

Text

ile-

clot

hing

Che

mic

al-

rubb

er

Mac

hine

ry

Mot

orve

hicl

es

Tota

lsa

mpl

e

%

Substantial benefits Increase of exports

Firms in themotor vehicle in-dustries showed lessactivity in the pastand in future prod-uct redesign. Only7.4 per cent of thewhole sample ex-pected substantialbenefits from har-monizing with EUtechnical rules (No.7). The picture issimilar for eachsector except motorvehicles, where theshare of such firms is 20 per cent. Motorvehicle companies are also the most ‘opti-mistic’, with 72.7 per cent expecting an in-crease in exports from EU membership. Suchexpectations are also high in chemicals andtextile and clothing.

4. Differences according to ownershipIn the sample, 85 firms declared for-

eign owners, of which 59 firms had morethan 51 per cent foreign ownership, 9 35–50 per cent and 13 10–34 per cent. Fourfirms did not indicate the extent of foreignownership, but it has been assumed that it

was substantial, otherwise they would nothave kept it secret. The degree of foreignownership influences the extent of foreigncontrol. An FIE may be domestic controlled ifthe foreign share is quite small. The samplewas therefore divided into two groups: firmswith over 34 per cent foreign ownership(the foreign group) and firms owned by do-mestic and minority foreign investmentcompanies (the domestic group). The formercontained 72 firms and the latter 102. (Twofirms did not give this information.)

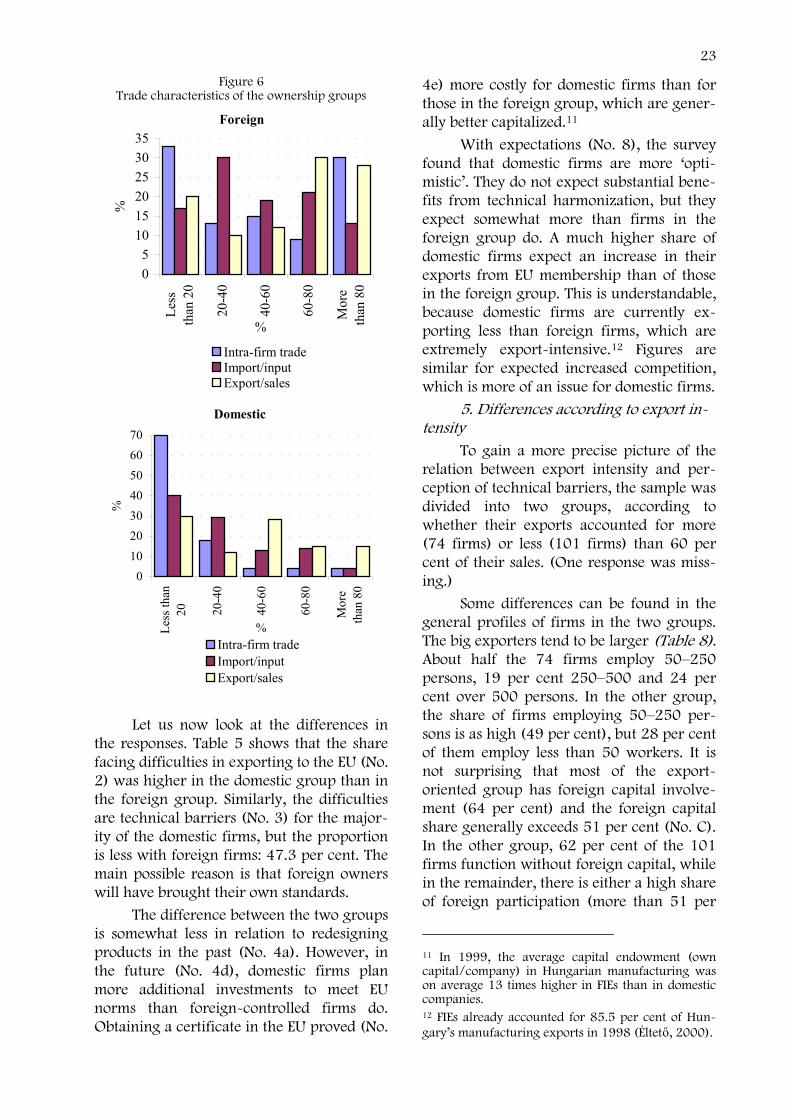

Table 7 shows the results of the sampledivision. Before analysing the details, itshould be stated that firms in the foreigngroup are bigger: the share of big companiesis almost three times as high as in the do-mestic group. It is thought, therefore, thatthe foreign group includes some multina-tional affiliates. This supposition is rein-forced by the foreign-trade structure of the

groups (Figure 6). It can be seen that theshare of intra-firm trade is much higheramong the foreign-group companies thanamong the domestic ones: 27.3 per cent ofthe former have a very high share of intra-firm trade (more than 80 per cent). The fig-ure also shows that foreign firms are moreexport-intensive, and at the same time, moreimport-intensive than domestic firms. This isin line with international experience (Dun-ning, 1993) and the results of other Hun-garian surveys (Éltető and Sass, 1998) andstatistical analyses (Éltető, 2000).

Table 7Characteristics of ownership groups: share of yes answers

Percentage share of groups Foreign group Domestic groupNumber of firms 72 102Share of firms with more than 500 employees 27.8 10.7Difficulties in EU exports 21.4 30.9Difficulties mean technical requirements 47.3 61.1

This is major barrier* 0.0 19.0This is moderate barrier* 80.0 66.7This is minor barrier* 20.0 14.3

Had to redesign products 11.6 16.3Envisage further investments 37.9 47.1Costs of certificate are substantial 10.2 19.7Harmonization would bring small benefits 60.7 57.6Expect increase in exports from EU membership 47.2 68.2Expect increasing competition from EU membership 52.7 63.4* The response rate was low: 21 domestic and 10 foreign firms.

23

Figure 6Trade characteristics of the ownership groups

Foreign

05

101520253035

Less

than

20

20-4

0

40-6

0

60-8

0

Mor

eth

an 8

0

%

%

Intra-firm tradeImport/inputExport/sales

Domestic

010203040506070

Less

than

20 20-4

0

40-6

0

60-8

0

Mor

eth

an 8

0

%

%

Intra-firm tradeImport/inputExport/sales

Let us now look at the differences inthe responses. Table 5 shows that the sharefacing difficulties in exporting to the EU (No.2) was higher in the domestic group than inthe foreign group. Similarly, the difficultiesare technical barriers (No. 3) for the major-ity of the domestic firms, but the proportionis less with foreign firms: 47.3 per cent. Themain possible reason is that foreign ownerswill have brought their own standards.

The difference between the two groupsis somewhat less in relation to redesigningproducts in the past (No. 4a). However, inthe future (No. 4d), domestic firms planmore additional investments to meet EUnorms than foreign-controlled firms do.Obtaining a certificate in the EU proved (No.

4e) more costly for domestic firms than forthose in the foreign group, which are gener-ally better capitalized.11

With expectations (No. 8), the surveyfound that domestic firms are more ‘opti-mistic’. They do not expect substantial bene-fits from technical harmonization, but theyexpect somewhat more than firms in theforeign group do. A much higher share ofdomestic firms expect an increase in theirexports from EU membership than of thosein the foreign group. This is understandable,because domestic firms are currently ex-porting less than foreign firms, which areextremely export-intensive.12 Figures aresimilar for expected increased competition,which is more of an issue for domestic firms.

5. Differences according to export in-tensity

To gain a more precise picture of therelation between export intensity and per-ception of technical barriers, the sample wasdivided into two groups, according towhether their exports accounted for more(74 firms) or less (101 firms) than 60 percent of their sales. (One response was miss-ing.)

Some differences can be found in thegeneral profiles of firms in the two groups.The big exporters tend to be larger (Table 8).About half the 74 firms employ 50–250persons, 19 per cent 250–500 and 24 percent over 500 persons. In the other group,the share of firms employing 50–250 per-sons is as high (49 per cent), but 28 per centof them employ less than 50 workers. It isnot surprising that most of the export-oriented group has foreign capital involve-ment (64 per cent) and the foreign capitalshare generally exceeds 51 per cent (No. C).In the other group, 62 per cent of the 101firms function without foreign capital, whilein the remainder, there is either a high shareof foreign participation (more than 51 per

11 In 1999, the average capital endowment (owncapital/company) in Hungarian manufacturing wason average 13 times higher in FIEs than in domesticcompanies.12 FIEs already accounted for 85.5 per cent of Hun-gary’s manufacturing exports in 1998 (Éltető, 2000).

24

Table 8Characteristics of firms in relation to export intensity

(% in each group)

Characteristic Export-intensivegroup

Less export-intensivegroup

Number of firms 74 101Share of firms with over 500 employees 24.3 12.8Foreign capital involvement 63.5 38.0Difficulties in EU exports 19.7 32.3Difficulties mean technical requirements 61.9 52.9

This is major barrier* 8.3 15.8This is moderate barrier* 50.0 84.2This is minor barrier* 41.7 0.0

Had to redesign products 13.9 14.7Envisage further investments 40.0 45.8Costs of certificate are substantial 3.8 24.3Harmonization would bring small benefits 58.6 58.9Expect increase in exports from EU membership 56.7 62.3Expect increasing competition from EU mem-bership 54.0 63.3

* The response rate was low: 21 domestic and 10 foreign firms.

Figure 7Trade characteristics according to export-intensity groups

Export-intensive

0

5

10

15

20

25

30

35

40

Less

than

20 20-4

0

40-6

0

60-8

0

Abo

ve 8

0

%

%

Intra-firm trade Import/input

Less export-intensive

0

10

20

30

40

50

60

Less

than

20

20-4

0

40-6

0

60-8

0

Abo

ve 8

0

%

%

Intra-firm trade Import/input

cent) or a very low one (less than 20 percent). Concerning the question related to theshare of trade with the foreign mother com-pany or its subsidiaries (No. G), these linksdominate in 35 per cent of the export-oriented group, but they are not very inten-sive for 28 per cent. Not surprisingly, the101 less export-intensive firms reportedweak links of this type (Figure 7). There aretwo similar features between the groups. Thefirst is that the proportions of firms estab-lished in customs-free zone (No. D) are neg-

ligible (3 per cent for export-oriented firmsand 0 per cent for the other group). Sec-ondly, there is a similarity in the geographi-cal orientation of exports (No. F), with EUand CEE markets by far the most important.

Perhaps surprisingly, the share ofthose who face difficulties in EU exports ismuch higher in the less export-intensivegroup than in the export-intensive group.This means that the mass exporters with es-tablished contacts on EU markets can exportrelatively more easily than firms that are

25

mainly oriented to the domestic market. Itwas emphasized in the general evaluation ofthe responses that firms are well aware ofthe need to implement EU legislation. For 80per cent of the export-intensive firms, theEU technical regulations (No. 3) do not cre-ate any problem before the accession, whilethe proportion is 69 per cent for the less ex-port-oriented firms. Nevertheless, wheredifficulties were faced, finding a solution re-quired major or moderate efforts and in-vestment in both groups. No external sup-port for meeting EU requirements (No. 4c)was received by 68 per cent of the export-oriented and 96per cent of the lessexport-intensivefirms. In the firstgroup, what sup-port there wascame, unsurpris-ingly, from theforeign investor.

To sum up,there are no sig-nificant differ-ences in the ex-pectations of theeffects of har-monization heldby the firms inthese two groups.As was mentionedin the generalevaluation of theresponses, bothexport-intensive and less export-orientedfirms stressed increased exports andstronger internal competition as the mostimportant consequences of membership ofthe EU and the single market. Responses onthe expected impact of the EU on the firm’sactivities were in line with Table 6, so thatno important differences emerged accordingto level of export intensity.

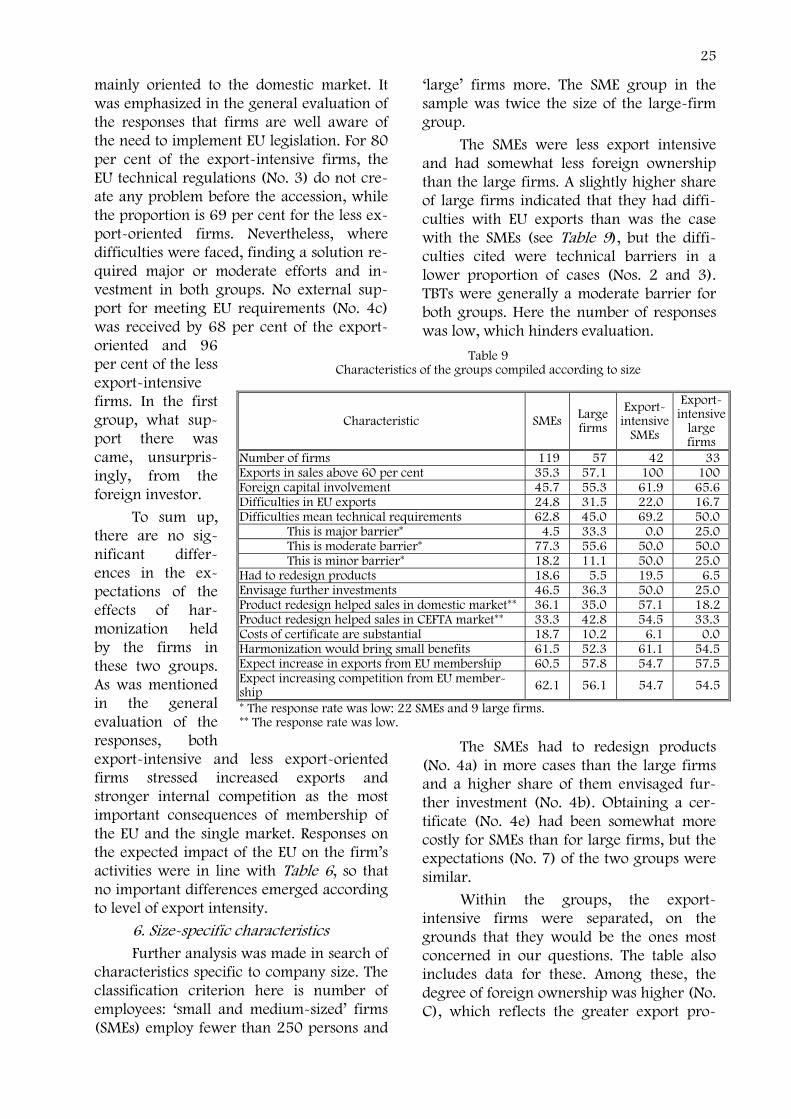

6. Size-specific characteristicsFurther analysis was made in search of

characteristics specific to company size. Theclassification criterion here is number ofemployees: ‘small and medium-sized’ firms(SMEs) employ fewer than 250 persons and

‘large’ firms more. The SME group in thesample was twice the size of the large-firmgroup.

The SMEs were less export intensiveand had somewhat less foreign ownershipthan the large firms. A slightly higher shareof large firms indicated that they had diffi-culties with EU exports than was the casewith the SMEs (see Table 9), but the diffi-culties cited were technical barriers in alower proportion of cases (Nos. 2 and 3).TBTs were generally a moderate barrier forboth groups. Here the number of responseswas low, which hinders evaluation.

The SMEs had to redesign products(No. 4a) in more cases than the large firmsand a higher share of them envisaged fur-ther investment (No. 4b). Obtaining a cer-tificate (No. 4e) had been somewhat morecostly for SMEs than for large firms, but theexpectations (No. 7) of the two groups weresimilar.

Within the groups, the export-intensive firms were separated, on thegrounds that they would be the ones mostconcerned in our questions. The table alsoincludes data for these. Among these, thedegree of foreign ownership was higher (No.C), which reflects the greater export pro-

Table 9Characteristics of the groups compiled according to size

Characteristic SMEs Largefirms

Export-intensive

SMEs

Export-intensive

largefirms

Number of firms 119 57 42 33Exports in sales above 60 per cent 35.3 57.1 100 100Foreign capital involvement 45.7 55.3 61.9 65.6Difficulties in EU exports 24.8 31.5 22.0 16.7Difficulties mean technical requirements 62.8 45.0 69.2 50.0

This is major barrier* 4.5 33.3 0.0 25.0This is moderate barrier* 77.3 55.6 50.0 50.0This is minor barrier* 18.2 11.1 50.0 25.0

Had to redesign products 18.6 5.5 19.5 6.5Envisage further investments 46.5 36.3 50.0 25.0Product redesign helped sales in domestic market** 36.1 35.0 57.1 18.2Product redesign helped sales in CEFTA market** 33.3 42.8 54.5 33.3Costs of certificate are substantial 18.7 10.2 6.1 0.0Harmonization would bring small benefits 61.5 52.3 61.1 54.5Expect increase in exports from EU membership 60.5 57.8 54.7 57.5Expect increasing competition from EU member-ship 62.1 56.1 54.7 54.5

* The response rate was low: 22 SMEs and 9 large firms.** The response rate was low.

26

pensity of foreign investors in Hungary andthe higher exporting activity of FIEs.

Table 8 shows that the export-intensive firms faced fewer difficulties withEU exports (No. 2, found before as well), butthe effect of size in this case was the oppositeto what it was in thesmall-large case. Largefirms as such were hitby difficulties more thanSMEs, but large export-intensive firms were hitless than SMEs. For bothgroups, one difficultylay in technical re-quirements (No. 3), butthese were only a minorbarrier.

With product re-design (No. 4a), thedifference was of similarextent and directionbetween the two sub-groups as in the two sizegroups. Interestingly,large export-intensive companies envisagethe least and small export-intensive firmsthe most further investment (No. 4d). Itseems that past or future redesign of prod-ucts mainly concerns export-intensive SMEs.

7. Groups according to the approachto TBTs

TBTs may force a producer to alter aproduct, to fulfil health, safety, environ-mental or similar regulations. EU policy to-wards standards, testing and certificationrequirements is currently based on two ap-proaches (Vancauteren, 1999): enforcementof the Mutual Recognition Principle (MRP),and where this fails, harmonization of tech-nical standards, by the Old Approach (OA)or New Approach (NA). The OA mainly ap-plies to products (chemical, motor vehicles,pharmaceuticals, foodstuffs) where the riskrequires product-by-product legislationcarried out by detailed directives. The long,highly technical and complicated decision-making procedure in the Council made itnecessary to adopt the NA, which only indi-cates essential requirements and leaves

greater freedom to manufacturers on how tosatisfy the requirements.

Where possible, the firms in the sam-ple were grouped according to the differentapproaches.13