Tech Mag Customer Profitability Analysis July07

32

Customer Profitability Analysis By Marc J. Epstein MANAGEMENT ACCOUNTING GUIDELINE Published by The Society of Management Accountants of Canada, the American Institute of Certified Public Accountants and The Chartered Institute of Management Accountants. MANAGEMENT STRATEGY MEASUREMENT

Transcript of Tech Mag Customer Profitability Analysis July07

CustomerProfitabilityAnalysis

By

Marc J. Epstein

MANAGEMENT ACCOUNTING GUIDELINE

Published by The Society of Management Accountants of Canada, the AmericanInstitute of Certified Public Accountants and The Chartered Institute ofManagement Accountants.

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

Copyright © 2000 by The Society of Management Accountants of Canada (CMA Canada), the American Institute of CertifiedPublic Accountants, Inc. (AICPA) and The Chartered Institute of Management Accountants (CIMA). All Rights Reserved.

No part of this publication may be reproduced, stored in a retrieval system or transmitted, in any form or by any means, withoutthe prior written consent of the publisher or a licence from The Canadian Copyright Licensing Agency (Access Copyright).For an Access Copyright Licence, visit www.accesscopyright.ca or call toll free to 1-800-893-5777.

ISBN: 1-55302-141-X

NOTICE TO READERS

The material contained in the Management Accounting Guideline Customer Profitability Analysis is designed to provide illustrativeinformation with respect to the subject matter covered. It does not establish standards or preferred practices.This material hasnot been considered or acted upon by any senior or technical committees or the board of directors of either the AICPA,CIMAor The Society of Management Accountants of Canada and does not represent an official opinion or position of either theAICPA,CIMA or The Society of Management Accountants of Canada.

CONTENTS EXECUTIVE SUMMARY

C U S TO M E R P RO F I TA B I L I T Y A N A LYS I S

INTRODUCTION

In Charlotte, North Carolina, the cus-tomer service center of First UnionCorporation, the sixth largest bank inthe United States, handles 45 millioncalls per year. The center’s computersystem, “Einstein”, determines the rank-ing of a customer – profitable or unprof-itable – in 15 seconds. Customers areassessed with respect to minimum bal-ance, account activity, branch visits,and other variables. At the service desk,the computer screen displays a color –red, green, or yellow – to signify thecustomer’s profitability rating. Thus,when a customer requests a lower creditcard interest rate or a waiver of accountservice fees, the service representative

INTRODUCTION 3ANALYZING CUSTOMER

PROFITABILITY 13IMPROVING CUSTOMER

PROFITABILITY 23CONCLUSION 27ENDNOTES 28BIBLIOGRAPHY 29

Strategic cost management and activity-based

costing have caused companies to look more

closely at the drivers of their costs. Increasingly,

companies have been focusing on the causes of

costs and profits to enable better management

of those costs and profits. First, companies focused

on product profitability and more recently on

customer profitability.

Companies recognize that though “exceeding

customer expectations” is a worthy goal, exceed-

ing those expectations profitably is necessary for

long-term corporate viability. Thus, an under-

standing of corporate profitability necessarily

relies on an understanding of what drives share-

holder value in organizations. Increasingly,

companies are focusing on the relationships

between employee satisfaction, customer satis-

faction, and corporate profitability. They are

focusing on the drivers of corporate profitability

and this requires an understanding of how to

increase customer revenues and how to decrease

customer costs. This management accounting

guideline provides a discussion with examples

of both the analysis of customer costs through

activity-based costing and the development of

long-term customer relationships for increased

revenues and profits through the measurement

of customer value.

Page

is able to respond quickly accordingto the customers’ rating.

A company can outperform rivals only ifit can establish a difference that it canpreserve. It must deliver greater value tocustomers or create comparable value ata lower cost, or do both.

Michael E. Porter. 1996. “What is strategy?” Harvard Business Review(November-December).

First Union recognizes that not allcustomers are the same. Though cus-tomer satisfaction is important, thegoal is to increase customer and cor-porate profitability. Customer prof-itability analysis is evolving as a basisfor determining the level of service

S T R A T E G Y

3

that customers receive and the level of theirfees. First Union estimates that its “Einstein”system will add at least $100 million to itsannual revenue. About half of that willcome from extra fees and other revenuefrom unprofitable customers, while therest will flow from pampering preferredcustomers who might otherwise leave thebank. First Union is not alone in this effort;an increasing number of companies employthe same procedures to determine profitableand unprofitable customers and managecustomer relationships to improve corporateprofits.

The example above is one of many thatdemonstrate the increased corporate focuson customers and their profitability. Thisguideline presents a discussion of the stateof the art and of best practices in determin-ing customer profitability with respect to:• understanding and analyzing customer

profitability.• maintaining and increasing customer

profitability.• turning unprofitable customers into

profitable ones.

The guideline does not present a detailedexamination of an all-inclusive analyticaltool for determining customer profitability.It does, however, provide the tools thatpermit the analysis of customer profitabilityand the implementation of programs toimprove these profits.

Over the last ten years, strategic costmanagement and activity-based costing(ABC) have created a framework for com-panies to more closely examine the drivers(or causes) of their costs in order to improvemanagement decisions and corporate prof-itability. Companies initially focused onproduct profitability are now using ABCand other models to further examine theprofitability of distribution channels andcustomers. Simultaneously, many companiesare exploring the drivers of profit and suc-cess through the use of the balanced score-card. Whichever model is used initially,determining customer profitability requiresa clearer understanding of the causes ofthe revenues and the costs. This guidelineprovides details of company experiences inexamining the causal relationships betweenthe drivers of customer satisfaction andcustomer revenues as well as in measuringthe profitability and costs of servicingexisting customers. Comprehensive systemsthat identify, measure, analyze and managecustomer profitability and its drivers are

only now being developed (Epstein,Kumar, and Westbrook 1999).

Expanding global competition is onereason behind the increased concern forcustomer profitability. Companies world-wide are being pressured to become morecustomer focused and to increase share-holder value. Customer profitability analysisis a useful tool in both areas.

Increasing Customer Focus

Many companies are convinced thatimproving corporate profitability requiresmore customer contact and closer customerrelationships. Further, many marketingprofessionals have directed recent attentionto increasing customer satisfaction, primar-ily examining the links between overallsatisfaction and revenues. Meanwhile,accountants have traditionally focused oncost reduction. Customer profitabilityanalysis attempts to bring together market-ing and accounting professionals to analyze,manage, and improve customer profitability.

Companies are attempting to betterunderstand and satisfy present and futurecustomer demands. However, the goal is toincrease customer satisfaction profitably.The analysis presented here, relying on ABCand other tools, can direct managerialattention to areas of improvement thatcan lead to greater customer and corporateprofits. An ABC system is not the onlymeans to measure customer profitability,but merely one of several tools that can beused.1

Since ABC provides a better understand-ing of the profitability of products and services, companies have started to use thesame approach to understand the profitabil-ity of customers. Following an ABC analysis,companies can examine the customer profit-ability information and determine how tomanage customer relationships in order toincrease customer satisfaction and theprofitability of both individual customersand customer segments. The ABC analysisoften provides information leading to suchimproved relationships that the profitabilityof both the company and its customers isincreased.

Companies have been using improvedinformation technology and large databasesto help refine marketing efforts. Marketingtools and IT systems now permit companiesto target individual customers and customergroups with pinpoint accuracy and to

4

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

determine whether or not a customer spendsenough to warrant the marketing effort. AtFederal Express, for example, customers whospend a lot of money but demand little cus-tomer service and marketing investment aretreated differently than those who spendjust as much but cost more to maintain. Inaddition, the company no longer marketsaggressively to those customers who spendlittle and show few signs of spending morein the future. This change in strategy hassubstantially reduced costs.

Fed Ex also analyzed the profitability ofthe 30 large customers that generated about10% of the total sales volume. The compa-ny found that certain customers, includingsome that required a lot of residential deliv-eries, were not bringing in as much revenueas they had agreed to initially when theynegotiated discounted rates. The companyincreased the rates for some customers andlost those who would not agree to the ratehikes. In this case the focus is not merelyon customers, but on profitable customers.When Federal Express says “100 percent cus-tomer satisfaction, by performing 100 per-cent to our standards, as perceived by thecustomer”, what do they really mean? Dothey always want to satisfy all customers?With customer profitability analysis, increas-ingly companies like Fed Ex are saying thatthey do want to satisfy customers, but theywant to do it profitably. They are also antic-ipating and creating new customers for theirproducts and services; for example FederalExpress created the overnight package deliv-ery market and is now creating anothermarket for same-day delivery. This is anotherway that Fed Ex satisfies customer demandand maintains profitability.

Another company that has benefited fromcustomer profitability analysis is Scotland-based Standard Life Assurance, Europe’slargest mutual life insurance company. Thecompany was stunned when the first resultsof a profitability survey showed that theinsurer was selling policies primarily to thosewho held little potential for making moneyfor the company. Instead of attracting theaffluent customers Standard Life wanted, its direct mail marketing campaign wasencouraging older couples and stay-at-homemothers to sign up for costly home visits bysales agents. Revenues were higher, but theywere the wrong kind of revenues; these werecustomers who typically bought only onepolicy and the margins were small. StandardLife was focused on customers, but was not

paying attention to the profitability of eachcustomer.

Increasing Shareholder Value

As the interest in increasing customer satis-faction has grown, so has the interest inincreasing shareholder value. Companies arecompeting globally not only for customers,laborers, and suppliers, but also for capital.This has caused companies to concentrateon satisfying investors and lenders throughan increase in shareholder value.

First Union is but one example of a company that has adopted new strategies toincrease shareholder value. Although exceed-ing customer expectations is a worthy goal,companies recognize that exceeding thoseexpectations profitably is necessary for long-term corporate viability. To improve corpo-rate profitability and shareholder value,companies must have a more completeunderstanding of the drivers of value intheir organizations. To do this, companiesincreasingly focus on the value drivers andon the causal relationships among employeesatisfaction, customer satisfaction, customerprofitability and corporate profitability.Improved corporate profitability requires adeeper understanding of ways to increasecustomer revenues and decrease customercosts. Essential components of improvedcustomer profitability include:• the analysis of the cost of customer

service through ABC;• the measurement of the lifetime value of

a customer; and• the development of long-term customer

relationships for increased revenues andprofits.

An important challenge for companies isto manage customer relationships in orderto make each customer profitable. Bank ofAmerica calculates its profits every monthon each of its more than 75 million accounts;this permits the company to focus on the10% of its customers that are the most prof-itable. Since it launched the program in1997, customer defections are down andaccount balances in the top 10% havegrown measurably. Calls from preferred andunprofitable customers are routed to differ-ent operators. A personal identificationnumber entered by each caller allows thebank to determine, among other things, thecustomer’s profitability ranking. The levelof attention and service will then differaccordingly. Bank of America still valuescustomer service, but also understands that

C U S TO M E R P RO F I TA B I L I T Y A N A LYS I S

5

there must be a balance between customerservice and customer profitability.

At First Chicago Corporation, a part ofBank One, profit and loss statements wereprepared for every client, and a $3 tellerfee was imposed in 1995 on some of themoney-losing customers. Thirty thousandof them, about 3% of the bank’s totalclients, closed their accounts. Some cus-tomers became more profitable by increas-ing their account balances to avoid the feeor by visiting ATMs instead of the tellers.While First Chicago lost some customers,it was also able to improve the profitabilityof most. Understanding customer profitabil-ity requires an understanding of the costsof customer service.

Paging Network, Inc., a paging serviceprovider located in Dallas, initially gaveaway its pagers to increase market share.After analyzing data on individual customersthe company determined that many cus-tomers were too costly to service profitably.It sent letters to marginal customers increas-ing the rates and subsequently lost 138,000customers in the third quarter of 1998. Of

the remaining 10.2 million subscribers, itexpected to lose another 325,000 customersbefore the end of 1998. The companydetermined that the cost to service thesecustomers was greater than the revenuebeing generated and decided to cut itslosses.2

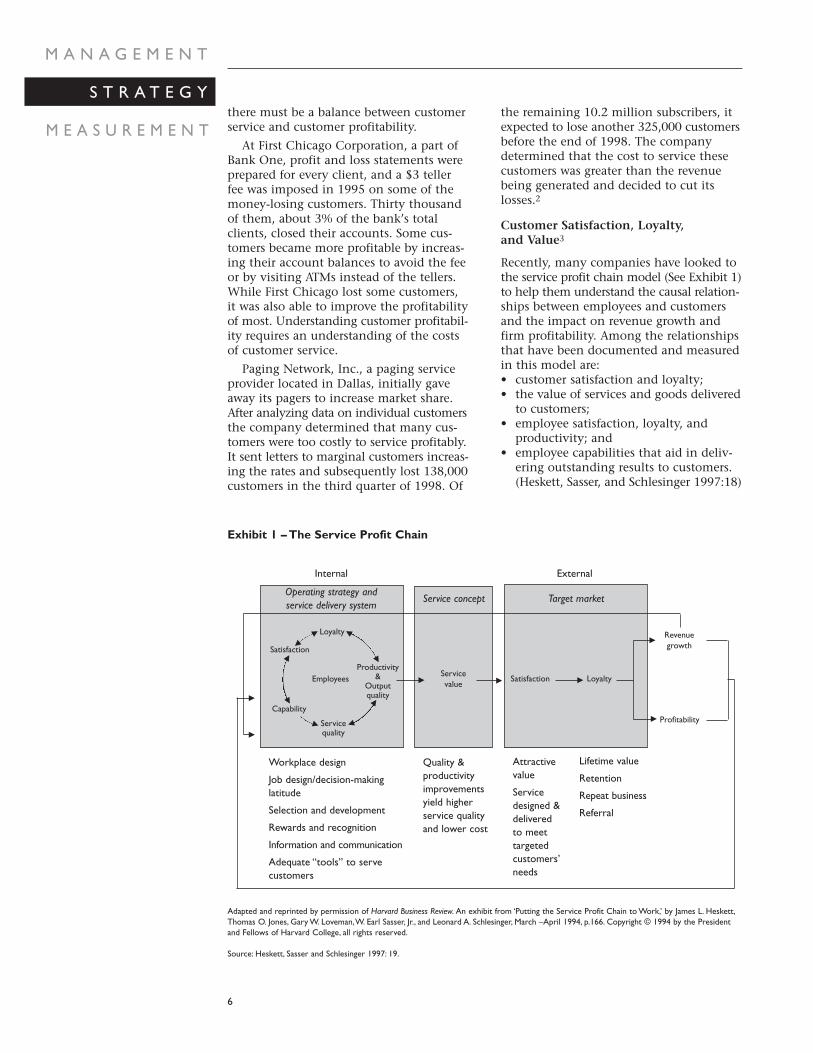

Customer Satisfaction, Loyalty, and Value3

Recently, many companies have looked tothe service profit chain model (See Exhibit 1)to help them understand the causal relation-ships between employees and customersand the impact on revenue growth andfirm profitability. Among the relationshipsthat have been documented and measuredin this model are:• customer satisfaction and loyalty;• the value of services and goods delivered

to customers;• employee satisfaction, loyalty, and

productivity; and• employee capabilities that aid in deliv-

ering outstanding results to customers.(Heskett, Sasser, and Schlesinger 1997:18)

6

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

Exhibit 1 – The Service Profit Chain

Adapted and reprinted by permission of Harvard Business Review. An exhibit from ‘Putting the Service Profit Chain to Work,’ by James L. Heskett,Thomas O. Jones, Gary W. Loveman,W. Earl Sasser, Jr., and Leonard A. Schlesinger, March –April 1994, p.166. Copyright © 1994 by the Presidentand Fellows of Harvard College, all rights reserved.

Source: Heskett, Sasser and Schlesinger 1997: 19.

Internal

Operating strategy andservice delivery system

Service concept Target market

External�

�

Service quality

Productivity&

Outputquality

Loyalty

EmployeesServicevalue

Profitability

Revenuegrowth

Satisfaction Loyalty

Satisfaction

Capability

���

��

Workplace design

Job design/decision-making latitude

Selection and development

Rewards and recognition

Information and communication

Adequate “tools” to servecustomers

Attractivevalue

Servicedesigned &delivered to meet targetedcustomers’needs

Lifetime value

Retention

Repeat business

Referral

Quality & productivityimprovementsyield higher service qualityand lower cost

�

�

�

�

�

�

�

�

�

Finance and accounting professionalsmust understand these relationships toassociate:• the human resource focus on employees;• the production focus on operations;• the marketing focus on revenues; and• the traditional accounting focus on costs.

The integration provides significant valueto marketing and general managementexecutives as they try to improve customerand corporate profitability. Some of the rela-tionships between customers and employeesare self-reinforcing: satisfied employees contribute to customer satisfaction, and satisfied customers contribute to employeesatisfaction.

To a customer, value involves the expectedbenefits and costs of a product or service, andthe customer’s perception is of significantrelevance. The expected benefits are derivedfrom the product and service attributes andthe expected costs include the transactioncosts, the life-cycle costs, and the risk.Transaction costs are typically the immediatefinancial outlay, which includes the price,delivery, and installation costs. The life-cyclecosts are the additional expected costs thatthe customer will incur over the life of theproduct. The risk is associated with the lifecycle costs (SMAC 1995:3).

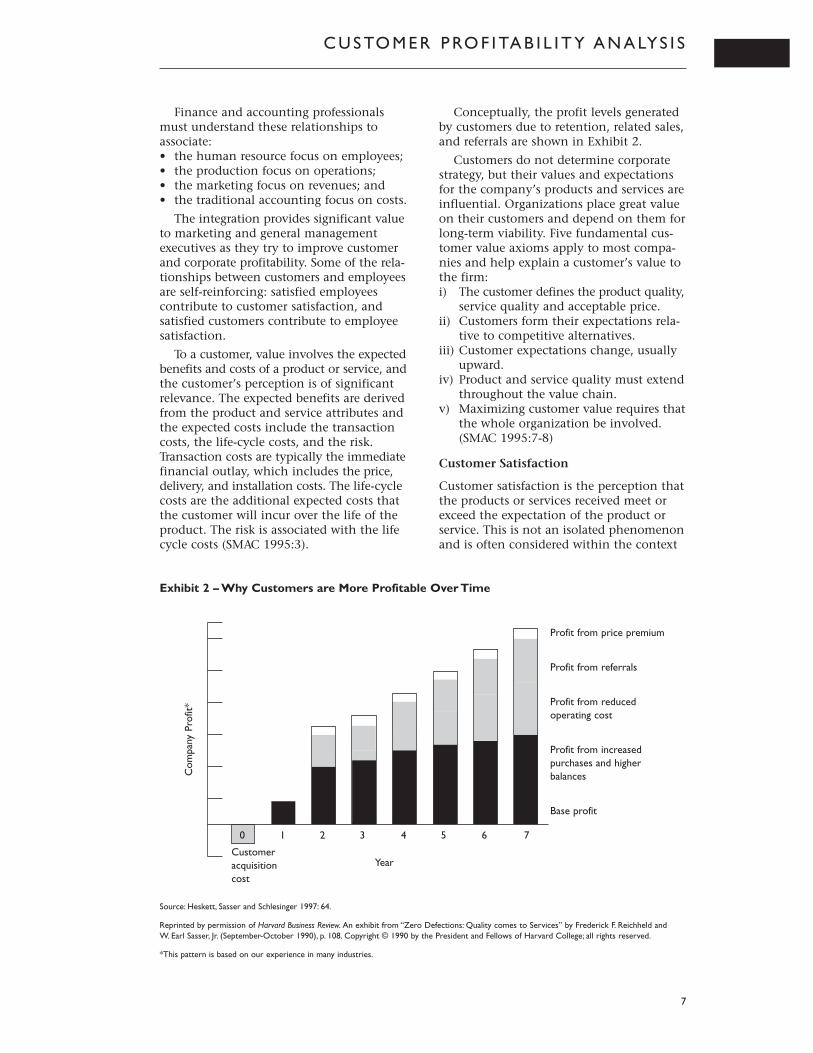

Conceptually, the profit levels generatedby customers due to retention, related sales,and referrals are shown in Exhibit 2.

Customers do not determine corporatestrategy, but their values and expectationsfor the company’s products and services areinfluential. Organizations place great valueon their customers and depend on them forlong-term viability. Five fundamental cus-tomer value axioms apply to most compa-nies and help explain a customer’s value tothe firm:i) The customer defines the product quality,

service quality and acceptable price.ii) Customers form their expectations rela-

tive to competitive alternatives.iii) Customer expectations change, usually

upward.iv) Product and service quality must extend

throughout the value chain.v) Maximizing customer value requires that

the whole organization be involved.(SMAC 1995:7-8)

Customer Satisfaction

Customer satisfaction is the perception thatthe products or services received meet orexceed the expectation of the product orservice. This is not an isolated phenomenonand is often considered within the context

C U S TO M E R P RO F I TA B I L I T Y A N A LYS I S

7

Exhibit 2 – Why Customers are More Profitable Over Time

Source: Heskett, Sasser and Schlesinger 1997: 64.

Reprinted by permission of Harvard Business Review. An exhibit from “Zero Defections: Quality comes to Services” by Frederick F. Reichheld and W. Earl Sasser, Jr. (September-October 1990), p. 108. Copyright © 1990 by the President and Fellows of Harvard College; all rights reserved.

*This pattern is based on our experience in many industries.

Profit from price premium

Profit from referrals

Profit from reduced operating cost

Profit from increased purchases and higher balances

Base profit

Com

pany

Pro

fit*

Customeracquisitioncost

0 1 2 3 4 5 6 7

Year

of loyalty, retention, and profitability.Researchers have shown that a causal rela-tionship exists between customer satisfac-tion and customer loyalty and that thisrelationship often leads to increases inprofitability.

Many companies have long held theview that customer satisfaction is a prereq-uisite for long-term profitability. Increasedcompetition and maturing markets havemade the issue of customer satisfactionmore significant. Further, the focus of salesand marketing has often shifted from anoffensive strategy of finding new customersto a defensive strategy of retaining currentcustomers and increasing the volume of their purchases (Fornell, Ryan, andWestbrook 1990:14).

A study by American Express Traveldemonstrated the relationship betweencustomer satisfaction and profitability. Afterestablishing that business travelers fromlarge companies were the most profitablecustomers, American Express determinedthat what these customers valued most wasfast service, professional treatment, experi-enced agents, and accurate ticketing. Theyalso found that those offices that deliveredthe fastest, most accurate ticketing wereamong the most profitable (Heskett, Sasserand Schlesinger 1997:20).

However, satisfied customers can also beunprofitable, as reported by Federal Expressand Page Net, and previously discussed.Individual customer satisfaction does notnecessarily lead to customer profitability.Customer retention, customer loyalty, and customer service costs must also beexamined.

Customer Retention and Customer Loyalty

Customer retention is the ongoing customerrelationship that yields revenues from thesale of additional products or services. Therevenues become more profitable as thecustomer becomes easier to serve. Sincethe customer is buying again it is assumedthat less sales effort is required, customerservice costs decrease, and the costs ofacquiring customers decline.

Ford Motor Company recently estimatedthe value of customer retention (i.e., thepercentage of the firm’s customers buyinga Ford as the next car). Ford’s stated goalwas to increase customer retention from60% to 80% as the company was convinced

that each additional percentage point ofcustomer retention was worth $100 millionin profits.

Software producer Intuit found the worthof a customer to be far greater than thecustomer’s original purchase of Quickensoftware. The revenue is $30 initially, butincreases to several hundred dollars ormore as satisfied customers buy additionalproducts. The revenues continue over timewhile the costs of customer service decrease.

Customer loyalty encompasses customerretention but also includes the customers’recommendation of the product or serviceto other potential customers. Word ofmouth recommendation is important toSouthwest Airlines, whose reservation system has never been accessible to travelagents. It has relied on advertising andcustomer loyalty to spread its message topotential customers. The airline, whichbegan flying in 1971, has consistently beenprofitable. Convinced that customer loyaltyis a more important factor in increasingprofitability than is market share, SouthwestAirlines strives to build customer loyaltyby providing at low fares dependable, fre-quent service over relatively short routes,delivered by friendly employees.

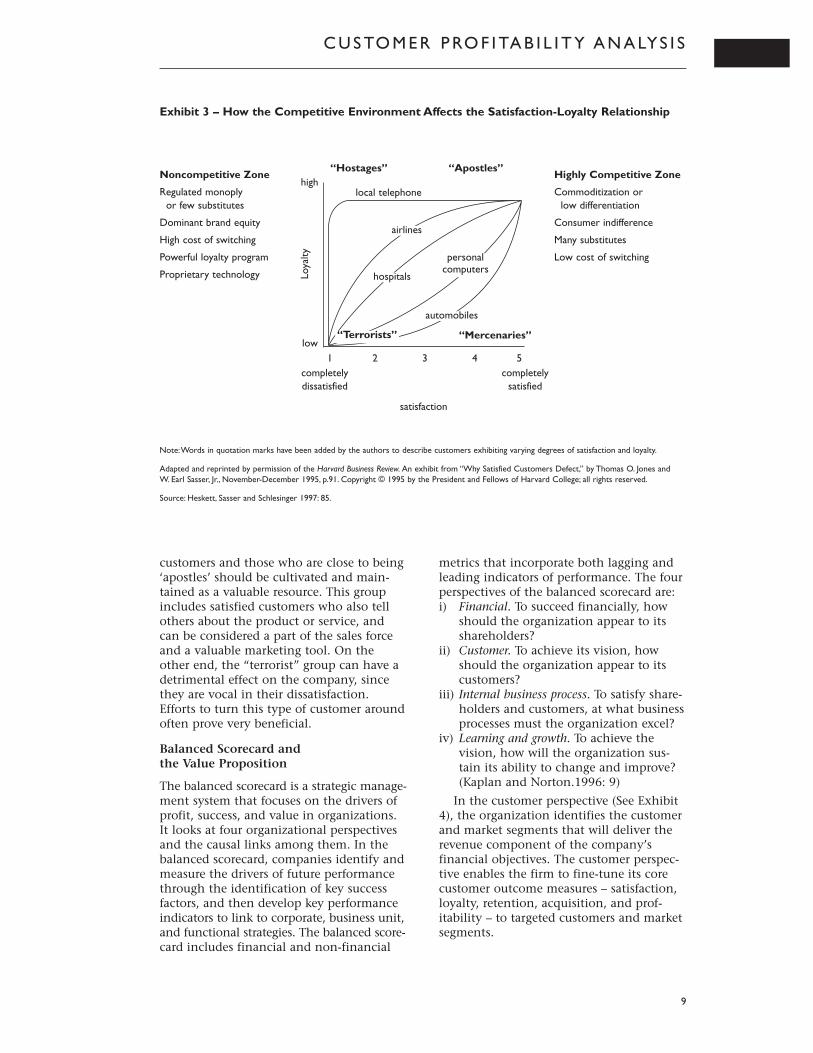

The relationship of customer loyaltyand customer satisfaction can be seen inthe following categorization of customers;it is important to understand fully theenvironment which the customer is work-ing, as extrinsic factors may drive themfrom one category to another: • Apostles. Customers who are loyal and

satisfied and recommend the service toothers.

• Mercenaries. Customers who may switchservice suppliers to obtain a lower price,but are highly satisfied.

• Hostages. Customers who are highly dis-satisfied but have few or no alternatives.

• Terrorists. Customers who have alterna-tives and use them, and also try to convert other customers by expressingtheir dissatisfaction. (Heskett, Sasser,and Schlesinger 1997:85)

The model in Exhibit 3 shows the rela-tionships between satisfaction and loyaltyfor these four groups in different competi-tive environments.

This model also suggests strategies forinvesting in customer satisfaction improve-ments for the greatest amount of profitimprovement. The “apostle” group of

8

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

customers and those who are close to being‘apostles’ should be cultivated and main-tained as a valuable resource. This groupincludes satisfied customers who also tellothers about the product or service, andcan be considered a part of the sales forceand a valuable marketing tool. On theother end, the “terrorist” group can have adetrimental effect on the company, sincethey are vocal in their dissatisfaction.Efforts to turn this type of customer aroundoften prove very beneficial.

Balanced Scorecard and the Value Proposition

The balanced scorecard is a strategic manage-ment system that focuses on the drivers ofprofit, success, and value in organizations.It looks at four organizational perspectivesand the causal links among them. In thebalanced scorecard, companies identify andmeasure the drivers of future performancethrough the identification of key successfactors, and then develop key performanceindicators to link to corporate, business unit,and functional strategies. The balanced score-card includes financial and non-financial

metrics that incorporate both lagging andleading indicators of performance. The fourperspectives of the balanced scorecard are:i) Financial. To succeed financially, how

should the organization appear to itsshareholders?

ii) Customer. To achieve its vision, howshould the organization appear to itscustomers?

iii) Internal business process. To satisfy share-holders and customers, at what businessprocesses must the organization excel?

iv) Learning and growth. To achieve thevision, how will the organization sus-tain its ability to change and improve?(Kaplan and Norton.1996: 9)

In the customer perspective (See Exhibit4), the organization identifies the customerand market segments that will deliver therevenue component of the company’sfinancial objectives. The customer perspec-tive enables the firm to fine-tune its corecustomer outcome measures – satisfaction,loyalty, retention, acquisition, and prof-itability – to targeted customers and marketsegments.

C U S TO M E R P RO F I TA B I L I T Y A N A LYS I S

9

Exhibit 3 – How the Competitive Environment Affects the Satisfaction-Loyalty Relationship

Note:Words in quotation marks have been added by the authors to describe customers exhibiting varying degrees of satisfaction and loyalty.

Adapted and reprinted by permission of the Harvard Business Review. An exhibit from “Why Satisfied Customers Defect,” by Thomas O. Jones and W. Earl Sasser, Jr., November-December 1995, p.91. Copyright © 1995 by the President and Fellows of Harvard College; all rights reserved.

Source: Heskett, Sasser and Schlesinger 1997: 85.

Noncompetitive Zone

Regulated monoply or few substitutes

Dominant brand equity

High cost of switching

Powerful loyalty program

Proprietary technology

Highly Competitive Zone

Commoditization or low differentiation

Consumer indifference

Many substitutes

Low cost of switching

“Hostages” “Apostles”

Loya

lty

1 2 3 4 5completelydissatisfied

low

high

satisfaction

completelysatisfied

“Terrorists” “Mercenaries”

automobiles

hospitals

airlines

local telephone

personalcomputers

Exhibit 4 suggests that there are causalrelationships within the core measurementgroup. The relationships among customersatisfaction, customer retention, and cus-tomer acquisition have a direct effect onthe profitability of the firm, reducing cus-tomer costs and increasing revenues.

The balanced scorecard relies on the valueproposition – that set of unique productsand services that differentiate the companyand provides value to its customers. Analysisof the value proposition is essential forunderstanding how customers are retained,what will satisfy them, and how they canbecome more profitable.

The proposition defines what is uniqueor valuable about the company’s productor service. From the customer’s perspective,this includes the attributes of the productsand services that create satisfaction andloyalty among the customers. The value

proposition (see Exhibit 5) is the primaryconcept for understanding the drivers ofsatisfaction, retention, acquisition, andmarket share. While these propositionswill vary significantly for different organi-zations, typically the following commonattributes are included:• product and service;• customer relationship; and• image and reputation.

The product and service characteristicsof the model include functionality, priceand quality (Kaplan and Norton 1996:73).How well does the product work? Is thequality good enough to keep the customersatisfied? Is the price too high or too low?A price that is too high will detract cus-tomers from buying the product in thelong run. Perhaps they will buy it once,but they will not be repeat or loyal cus-tomers.

10

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N TExhibit 4 – The Customer Perspective Core Measures

Source: Kaplan and Norton 1996: 68.

Customer

Profitability

Customer

Acquisition

Market

Share

Customer

Retention

Customer

Satisfaction

▲

▲ ▲

▲

▲▲▲

▲ ▲

▲

▲

▲

Market Reflects the proportion of business in a given market (in terms of number of Share customers, dollars spent, or unit volume sold) that a business unit sells.

Customer Measures, in absolute or relative terms, the rate at which a business unit Acquisition attracts or wins new customers or business.

Customer Tracks, in absolute or relative terms, the rate at which a business unit retains Retention or maintains ongoing relationships with its customers.

Customer Assesses the satisfaction level of customers along specific performance criteria Satisfaction within the value proposition.

Customer Measures the net profit of a customer, or a segment, after allowing for the Profitability unique expenses required to support that customer.

The relationship aspect includes thedelivery of the product or service to thecustomer and how the customer feels aboutpurchasing from the company. This relation-ship between the firm and its customers isimportant to maintain and often includespost-sale service. Some companies chooseto end the relationship between them andtheir customers at the point of sale, such asin the case of computers and appliancespurchased at discount stores. If these cus-tomers are unhappy with the product, theymust contact the manufacturer directly.

The image and reputation aspect reflectsthose intangible factors that attract a cus-tomer to a company, such as loyalty to abrand name. This aspect provides the com-pany an opportunity to define itself for itscustomers.

The customer value proposition commu-nicates throughout the organization theexpectations for customer satisfaction, cus-tomer loyalty, and consequently customerprofitability. The proposition is a compilationof what the company believes the customervalues and how the firm can deliver thisvalue, as well as a statement about how thecompany adds value to its customers throughits products and services. An understandingof the customer value proposition is criticalfor both the balanced scorecard model andcustomer profitability analysis.

Benefit of Increasing ProfitabilityThrough Understanding of Causal Relationships

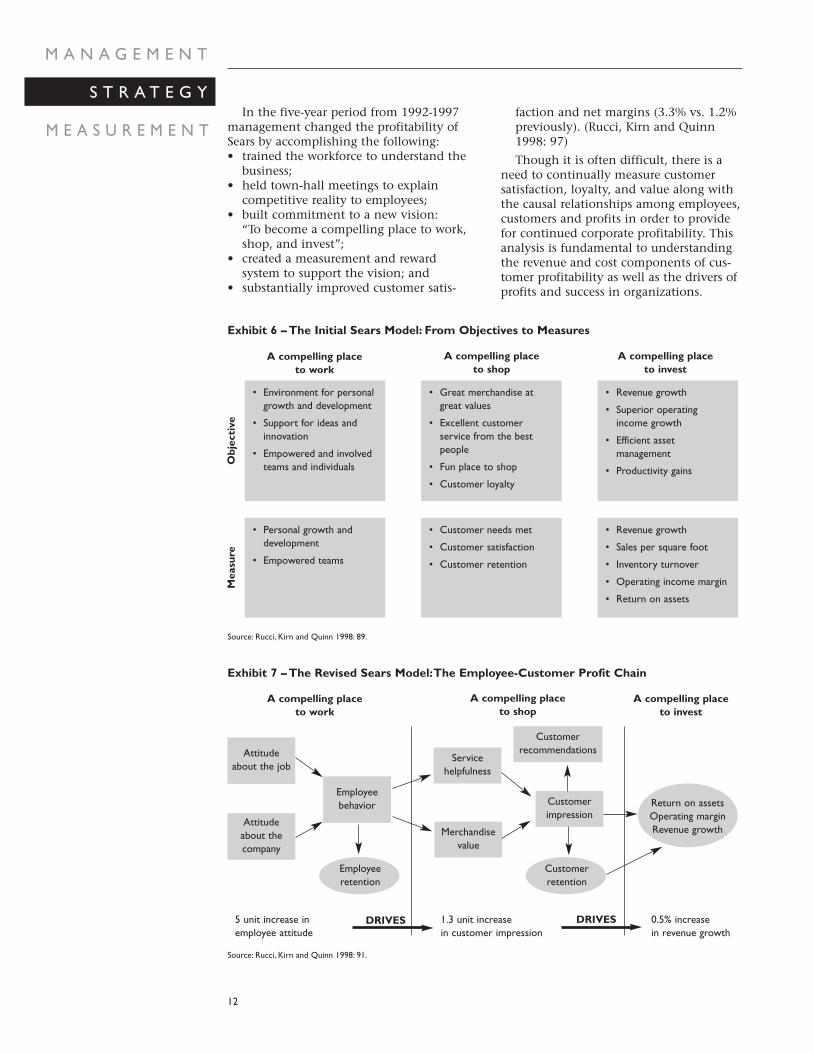

In 1992, Sears, Roebuck and Company, thelarge retailer, lost almost $4 billion. By 1997it reported a profit of $1.5 billion. Whilethere are many reasons for the change, theSears managers believed that it was due pri-marily to a change in the culture of theirbusiness. Sears believed that there was a gapbetween strategy and day-to-day operationsthat left employees uncertain about howthey could contribute to the company. Sears

developed an employee-customer-profitmodel and examined how direct and specificeffects of improvements in employee satis-faction would improve customer satisfaction,and ultimately profitability. After an initialdesign, analysis of substantial data, andtesting and modifying the original modelthe managers made specific measurableconclusions: “a 5 point improvement inemployee attitudes will drive a 1.3 pointimprovement in customer satisfaction, whichin turn will drive a 0.5% improvement inrevenue growth” (Rucci, Kirn and Quinn1998:91).

The Sears model was based on the orga-nizational objectives that were developed tobegin a transformation of the company. Thedesire was for Sears to be “a compelling placeto work, to shop and to invest”. The initialmodel included objectives and measures(see Exhibit 6). Total Performance Indicators(TPI) were developed to test and refine themodel and assumptions about causal link-ages between employee attitude and cus-tomer satisfaction and profitability wererefined. As a result of this process, a newmodel was developed and tested, andbecame operational company-wide with the 300,000 Sears employees.

Sears’ management believed that thisrevised model (see Exhibit 7) indicatedmeasurable causal linkages in the relation-ship of employees to customers, and thattheses linkages resulted in increased profit.Sears managers continued to seek detailedinformation from individual customersregarding their “shopping experiences” in order to learn more about customer satis-faction and retention, which they believeddirectly affected profitability. Whenemployees saw how their actions with cus-tomers mattered to the company, positiveattitudes were reinforced and the linkage wasidentified between improved attitude towardsthe firm and its customers and overallimproved profitability of the company.

C U S TO M E R P RO F I TA B I L I T Y A N A LYS I S

11

Exhibit 5 – The Customer Value Proposition

Source: Kaplan and Norton 1996: 74.

Generic Model

Value

Functionality Quality Price Time

ImageProduct/Service Attributes= + Relationship+

In the five-year period from 1992-1997management changed the profitability ofSears by accomplishing the following:• trained the workforce to understand the

business;• held town-hall meetings to explain

competitive reality to employees;• built commitment to a new vision:

“To become a compelling place to work,shop, and invest”;

• created a measurement and reward system to support the vision; and

• substantially improved customer satis-

faction and net margins (3.3% vs. 1.2%previously). (Rucci, Kirn and Quinn1998: 97)

Though it is often difficult, there is aneed to continually measure customer satisfaction, loyalty, and value along withthe causal relationships among employees,customers and profits in order to providefor continued corporate profitability. Thisanalysis is fundamental to understandingthe revenue and cost components of cus-tomer profitability as well as the drivers ofprofits and success in organizations.

12

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

Exhibit 6 – The Initial Sears Model: From Objectives to Measures

Source: Rucci, Kirn and Quinn 1998: 89.

A compelling place to invest

A compelling place to shop

Obj

ecti

veM

easu

re

• Environment for personalgrowth and development

• Support for ideas andinnovation

• Empowered and involvedteams and individuals

• Great merchandise atgreat values

• Excellent customer service from the bestpeople

• Fun place to shop

• Customer loyalty

• Revenue growth

• Superior operatingincome growth

• Efficient asset management

• Productivity gains

• Personal growth anddevelopment

• Empowered teams

• Customer needs met

• Customer satisfaction

• Customer retention

• Revenue growth

• Sales per square foot

• Inventory turnover

• Operating income margin

• Return on assets

A compelling place to work

A compelling place to invest

A compelling place to shop

A compelling place to work

Exhibit 7 – The Revised Sears Model:The Employee-Customer Profit Chain

Source: Rucci, Kirn and Quinn 1998: 91.

Attitude about the job

Attitude about the company

Employeebehavior

Merchandisevalue

Servicehelpfulness

Customerrecommendations

Customerimpression

Employeeretention

Customerretention

Return on assetsOperating marginRevenue growth

5 unit increase in employee attitude

1.3 unit increase in customer impression

0.5% increase in revenue growth

DRIVES DRIVES

ANALYZING CUSTOMER PROFITABILITY

How ABC Improves Understanding ofProduct and Customer Profitability

Traditional cost accounting assumes thatproducts and services cause costs to occur.Therefore, direct labor, direct material andother direct costs are traced directly to prod-ucts. All other costs are considered indirectcosts and allocated to products on arbitrarybases, such as product volume or direct laborhours. This costing system can work well aslong as indirect costs and product diversityare minimal. As the product mix becomesmore diverse, it becomes more difficult toaccurately allocate overhead costs.

Activity-based costing assumes that activ-ities cause costs and that product, servicesand customers are the reasons for the activ-ities. ABC focuses on determining whatcauses costs to occur rather than on merelyallocating what has been spent. ABC tracescosts to activities in the production processusing resource drivers and activity driversbased on cause and effect. There are fiveprimary steps in the ABC costing process:i) identify activities;ii) identify resource measures (inputs) from

the consumption of resources by theactivities;

iii) identify activity measures (outputs) bywhich the costs of a process vary mostdirectly;

iv) calculate the driver rate; andv) trace activity costs to cost objects such

as products, processes and customersbased on the usage of activities.

ABC has developed into a broad-basedtool that provides information on manyaspects of company functions in additionto product cost data. ABC can show howproducts, brands, customers, customergroups, facilities, regions or distributionchannels both generate revenue and usecompany resources (Cooper and Kaplan1991:130). Though not a complete solutionto all business problems, a good ABC systemprovides useful information that, in conjunc-tion with other management information,can facilitate improved business decisionmaking.

ABC offers a new way to analyze the allo-cation of costs to non-production activitiessuch as marketing, selling, distribution andadministration. Customer profitability ismore easily determined through the use ofABC, since the costs can be driven directly

to individual customers, some of whomplace more demands on the company thanothers. Some may require special orders,purchase just-in-time inventory, or havespecial delivery requirements; each of thesehas a cost that can be allocated to the spe-cific customer using activity-based drivers.Understanding the needs and costs of eachclient, and how each impacts corporateprofitability, can help to determine the levelof customer service that will benefit boththe customer and the company. The specialneeds of both large and small customers canbe accommodated through a better under-standing of the drivers of both the revenuesand the costs associated with each customer(Kaplan and Cooper 1998:181).

Customer Profitability Analysis

Typically traditional cost accounting is notable to identify product and service costs ordistribution and delivery costs for individualcustomers. ABC can help identify customeractivities and track those costs that are allo-cated to specific customers. This can providemanagement with unique information aboutcustomers and customer segments. Thebenefits include:• protecting existing highly profitable

customers;• repricing expensive services, based on

cost-to-serve;• discounting to gain business with low

cost-to-serve customers;• negotiating win-win relationships that

lower service costs to cooperative customers;

• conceding permanent loss customers tocompetitors; and

• attempting to capture high-profit cus-tomers from competitors (Kaplan andCooper, 1998:181).

Customer profitability analysis has becomean important new management accountingtool based on a recognition that each cus-tomer is different and that each dollar ofrevenue does not contribute equally to thefirm’s profitability. Customers utilize com-pany resources differently; thus customercosts vary from one customer to another.The following issues should be consideredwhen analyzing customer profitability:• how to develop reliable customer rev-

enue and customer cost information.• how to recognize future downstream

costs of customers.• how to incorporate a multiperiod hori-

zon in the analysis.

C U S TO M E R P RO F I TA B I L I T Y A N A LYS I S

13

• how to recognize different drivers ofcustomer costs. (Foster, Gupta andSjoblom 1996:10)

This requires a broader examination ofthe costs associated with customer service.For example, post-sale customer servicecosts must be included in any analysis ofcustomer costs. Some customers requiresubstantially more post-sale service thanothers. In addition, future environmentalliabilities related to the sales of currentproducts are additional downstream coststhat must be included. With management’sincreased focus on customers, this analysiscan provide forward-looking informationabout individual customers and customersegments and more broadly examine boththe revenues and costs related to customertransactions. Revenues can vary amongcustomers due to variations in volume levels,and differences in price structures, productsand services. Costs can also vary depend-ing on how customers use the company’sresources such as marketing, distribution,and customer service. Unless a completeanalysis of the benefits and costs of cus-tomer relationships is undertaken, compa-nies will unknowingly continue to serviceunprofitable customers. Only after a thor-ough analysis of the costs and benefits cana firm decide which customers to serviceand strategically price its products and services.

There are many costs that are often hid-den within the production, support, mar-keting, and general administrative areas.To better understand customer profitabilitythese costs should be examined and assignedappropriately using ABC methods. Thesecurrently hidden customer costs mayinclude items such as:• inventory carrying costs;• stocking and handling costs;• quality control and inspection costs;• customer order processing;• order picking and order fulfillment;• billing, collection and payment process-

ing costs;• accounts receivable and carrying costs;• customer service costs;• wholesale service and quality assurance

costs; and• selling and marketing costs. (Weinberg

1999:28)

ABC was recently used by a telecommu-nications company to improve customerprofitability. The company developed aprocess for identifying the cost drivers of

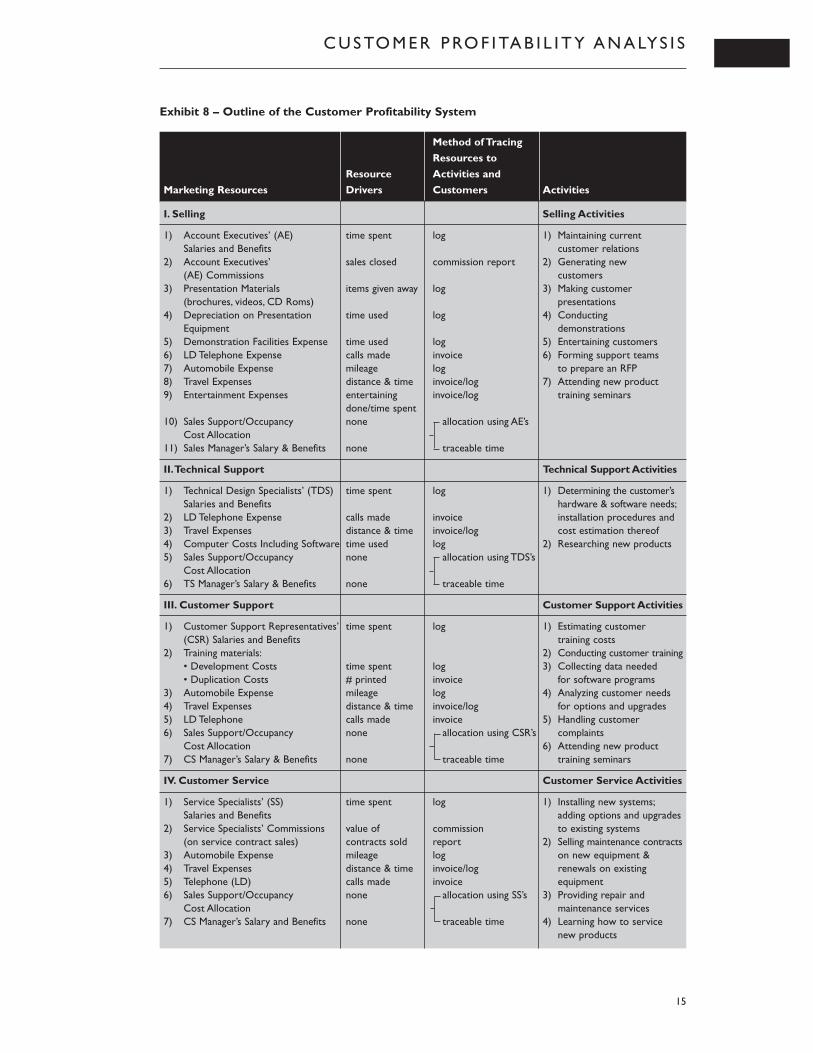

training costs, which is an important com-ponent of the company’s contract bids. Thecompany’s activities included the submis-sion of bids to large organizations for theinstallation of telecommunications systems.The bids were reasonably accurate in esti-mating the cost of the equipment hardware,the installation cost of the new equipment,and the programming costs. However, thecost of training the customer’s employeesabout the new equipment was more diffi-cult to determine. Exhibit 8 represents anoutline of the customer profitability report-ing system developed for one business unitof this company (Ortman and Buehlmann1998). This is an example of a detailed,comprehensive, and somewhat costlyapproach. As always there must be a bal-ance between the benefits of collectingadditional data and the associated cost.The availability and timeliness of data arealso significant issues in implementingcustomer profitability systems based onABC.

The major marketing activities wereidentified and the resources that theseactivities consumed were detailed. Employeetime was the major resource driver, andwas traced by an employee log to specificactivities. The company found that train-ing costs were significant but difficult tocalculate. Customer service representatives,who were at the front line in the trainingfunction and formed a liaison between thecompany, its customers and the engineerswho designed the systems, were interviewed.The company was then able to identifyseven different training activities andresource uses, along with potential costdrivers. The estimation of customer servicetraining costs through the use of ABCimproved the company’s understanding ofthe profitability of its different customers.

Whether customer-specific costs arenecessary and/or can be determined dependson several factors, including the fragmen-tation of the customer base, the cost struc-ture of the company, and the existence ofthe necessary information infrastructure.Analysis can be crude and simple and evenincomplete, yet still effective at providingvaluable customer profitability information.

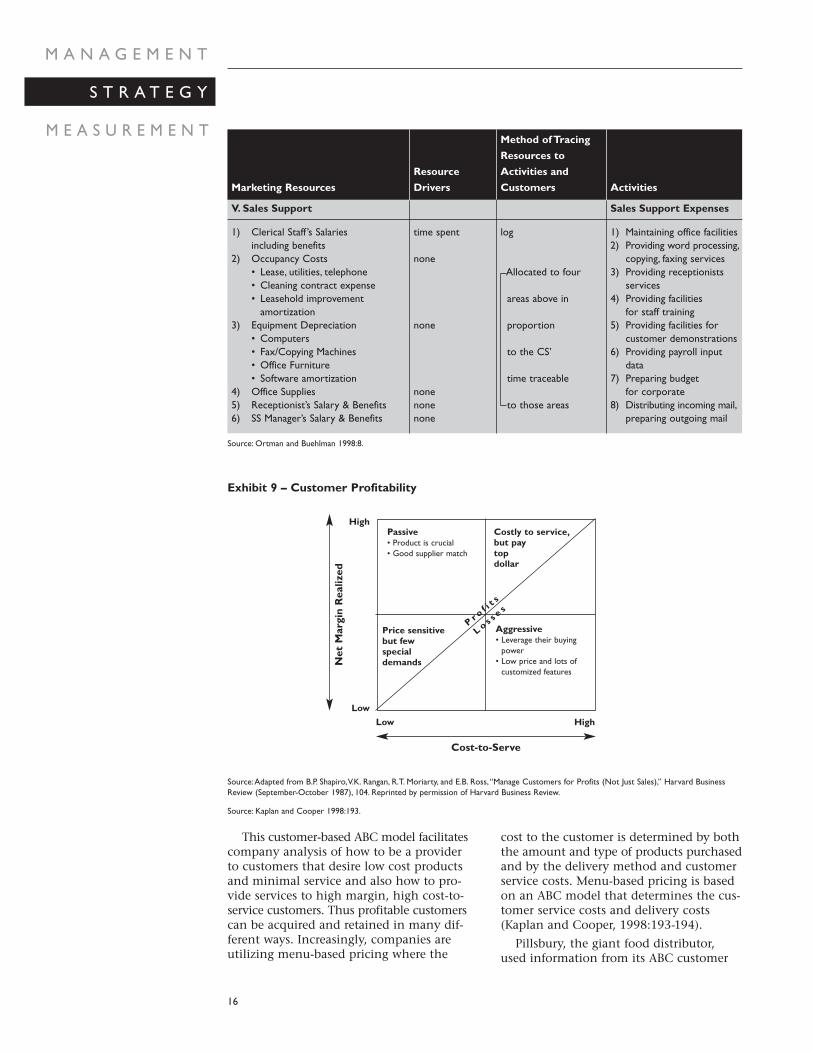

Some customer models have been devel-oped to provide companies with a frame-work to analyze the pricing of differentservices for different types of customers.An example of such a model can be seenin Exhibit 9.

14

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

C U S TO M E R P RO F I TA B I L I T Y A N A LYS I S

15

Exhibit 8 – Outline of the Customer Profitability System

Method of Tracing

Resources to

Resource Activities and

Marketing Resources Drivers Customers Activities

I. Selling Selling Activities

1) Account Executives’ (AE) time spent log 1) Maintaining current Salaries and Benefits customer relations

2) Account Executives’ sales closed commission report 2) Generating new (AE) Commissions customers

3) Presentation Materials items given away log 3) Making customer (brochures, videos, CD Roms) presentations

4) Depreciation on Presentation time used log 4) Conducting Equipment demonstrations

5) Demonstration Facilities Expense time used log 5) Entertaining customers6) LD Telephone Expense calls made invoice 6) Forming support teams7) Automobile Expense mileage log to prepare an RFP8) Travel Expenses distance & time invoice/log 7) Attending new product 9) Entertainment Expenses entertaining invoice/log training seminars

done/time spent10) Sales Support/Occupancy none allocation using AE’s

Cost Allocation11) Sales Manager’s Salary & Benefits none traceable time

II.Technical Support Technical Support Activities

1) Technical Design Specialists’ (TDS) time spent log 1) Determining the customer’s Salaries and Benefits hardware & software needs;

2) LD Telephone Expense calls made invoice installation procedures and3) Travel Expenses distance & time invoice/log cost estimation thereof4) Computer Costs Including Software time used log 2) Researching new products5) Sales Support/Occupancy none allocation using TDS’s

Cost Allocation6) TS Manager’s Salary & Benefits none traceable time

III. Customer Support Customer Support Activities

1) Customer Support Representatives’ time spent log 1) Estimating customer (CSR) Salaries and Benefits training costs

2) Training materials: 2) Conducting customer training• Development Costs time spent log 3) Collecting data needed • Duplication Costs # printed invoice for software programs

3) Automobile Expense mileage log 4) Analyzing customer needs 4) Travel Expenses distance & time invoice/log for options and upgrades 5) LD Telephone calls made invoice 5) Handling customer 6) Sales Support/Occupancy none allocation using CSR’s complaints

Cost Allocation 6) Attending new product 7) CS Manager’s Salary & Benefits none traceable time training seminars

IV. Customer Service Customer Service Activities

1) Service Specialists’ (SS) time spent log 1) Installing new systems;Salaries and Benefits adding options and upgrades

2) Service Specialists’ Commissions value of commission to existing systems(on service contract sales) contracts sold report 2) Selling maintenance contracts

3) Automobile Expense mileage log on new equipment & 4) Travel Expenses distance & time invoice/log renewals on existing 5) Telephone (LD) calls made invoice equipment6) Sales Support/Occupancy none allocation using SS’s 3) Providing repair and

Cost Allocation maintenance services7) CS Manager’s Salary and Benefits none traceable time 4) Learning how to service

new products

V. Sales Support Sales Support Expenses

This customer-based ABC model facilitatescompany analysis of how to be a providerto customers that desire low cost productsand minimal service and also how to pro-vide services to high margin, high cost-to-service customers. Thus profitable customerscan be acquired and retained in many dif-ferent ways. Increasingly, companies areutilizing menu-based pricing where the

cost to the customer is determined by boththe amount and type of products purchasedand by the delivery method and customerservice costs. Menu-based pricing is basedon an ABC model that determines the cus-tomer service costs and delivery costs(Kaplan and Cooper, 1998:193-194).

Pillsbury, the giant food distributor,used information from its ABC customer

16

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

1) Clerical Staff ’s Salaries time spent log 1) Maintaining office facilitiesincluding benefits 2) Providing word processing,

2) Occupancy Costs none copying, faxing services• Lease, utilities, telephone Allocated to four 3) Providing receptionists • Cleaning contract expense services• Leasehold improvement areas above in 4) Providing facilities

amortization for staff training3) Equipment Depreciation none proportion 5) Providing facilities for

• Computers customer demonstrations• Fax/Copying Machines to the CS’ 6) Providing payroll input • Office Furniture data• Software amortization time traceable 7) Preparing budget

4) Office Supplies none for corporate5) Receptionist’s Salary & Benefits none to those areas 8) Distributing incoming mail,6) SS Manager’s Salary & Benefits none preparing outgoing mail

Method of Tracing

Resources to

Resource Activities and

Marketing Resources Drivers Customers Activities

Source: Ortman and Buehlman 1998:8.

Net

Mar

gin

Rea

lized

Passive• Product is crucial• Good supplier match

Costly to service,but pay top dollar

Aggressive• Leverage their buying

power• Low price and lots of

customized features

Price sensitive but few special demands

P r o f it s

L o s s e s

Low High

High

Low

Exhibit 9 – Customer Profitability

Cost-to-Serve

Source:Adapted from B.P. Shapiro,V.K. Rangan, R.T. Moriarty, and E.B. Ross,“Manage Customers for Profits (Not Just Sales),” Harvard BusinessReview (September-October 1987), 104. Reprinted by permission of Harvard Business Review.

Source: Kaplan and Cooper 1998:193.

and store level profit and loss statements todetermine what its customers valued andwanted and then developed “menu-basedpricing”. The company began charging feesfor special services that were desired bysome but not all customers. In this way itdeveloped a base level of service that allcustomers received, plus service-based pric-ing for specially desired services. Furthersavings to consumers were obtained throughnegotiations with retailers for lower priceson Pillsbury products and for special mer-chandising and promotion of its products(Kaplan and Cooper 1998:198).

Swedbank, part of the largest bank groupin Sweden, resulted from a consolidation of several government-owned banks. Therewere 4.5 million individual accounts and100,000 business accounts. This is an exampleof a customer service company that madeuse of customer profitability analysis toidentify its unprofitable customers and tobecome more profitable overall. ThroughABC analysis and customer surveys, thebank determined that approximately 80%of its customers were satisfied but unprof-itable, while the remaining some 20% ofthe customers were dissatisfied with thebank’s services but very profitable – con-tributing more than 100 percent of the bank’sprofits. As a result, the bank began investingall new capital in profitable customers. Frontline employees were given more latitude,new products were introduced, employeetraining was increased, and a new manage-ment information system was introduced tocustomer and corporate profitability. Someunprofitable customers left and the profitablecustomers increased their usage of the bank’sproducts and services.

Swedbank proceeded to examine the rela-tionships and results of three related dimen-sions of performance: customer value added,people value added, and economic valueadded (profitability). This combination ofan ABC analysis with a balanced scorecardtype model provided the framework andthe information to improve customer andcorporate profitability.

Customer Profitability Analysis in a Manufacturing Company

The Kanthal case provides an excellentexample of how ABC can improve the mea-surement and management of customerprofitability. Kanthal, the largest division of Swedish manufacturer Kanthal-Hoganas,had sales in excess of $50 million per year.

Most sales, about 95%, were exports fromSweden. Kanthal manufactured and soldheating alloys for electric resistance heatingelements, heating elements for industrialfurnaces and thermo-bimetals for tempera-ture control devices. The company wasorganized into three divisions, two of whichheld substantial global market shares intheir particular products and the other haddeveloped a fully integrated manufacturingsystem to produce the thermo-bimetals.

The president of the company, Carl-ErikRidderstale, saw the need for a strategicplan to increase profits while maintainingan annual return on employed capital inexcess of 20% (Kaplan 1989:2). His Kanthal90 Strategy detailed profit objectives bydivision, product line, and market share.Ridderstale’s plan was to achieve this growthwithout the need for additional sales oradministrative staff to handle the expectedincrease in sales volume.

Ridderstale was also concerned that sell-ing and administrative expenses formed thelargest cost category in the company andwere growing. They accounted for 34% oftotal expenses and were treated as periodcosts rather than allocated to either productsor customers. Ridderstale wanted a newcosting system that could determine howmuch profit was earned every time an orderwas placed. He also wanted to find the hid-den profits and hidden costs in each order.Further, he believed that Kanthal had lowprofit and high profit customers dependingon the demands that the customer placedon the administrative and sales staff andthat these customers should be readilyidentifiable.

Kanthal had about 10,000 customers andproduced over 15,000 items. It stocked 20%of those (3,000 items) which represented 80%of the company’s sales. After assigning coststo customer orders, it became apparent thatthe sales of stocked items were significantlymore profitable than the processing andmanufacturing of non-stocked items. Sincethe existing system did not differentiatebetween orders for stocked and non-stockeditems the difference in profitability had notbeen apparent. The costs to produce non-stocked items was greater than the costs toproduce stocked items since special sched-uling was required for the purchase of theraw materials and the production process. Itwas also more costly to produce the itemsin small quantities.

C U S TO M E R P RO F I TA B I L I T Y A N A LYS I S

17

With the aid of consultants, the financialmanager of Kanthal, Per O. Ehrling, devel-oped an Account Management System toanalyze production, sales, and administra-tion costs using ABC. Two new cost driverswere added to the analysis: the additionalcost of producing non-stocked items, and,the normal expense associated with anycustomer order such as pricing, schedulingdelivery, invoicing, and collecting.

The company then accumulated, for eachcustomer, the profit and loss figures fromeach individual order placed by that cus-tomer (See Exhibit 10). The results of theABC analysis showed that while gross mar-gins for different customers may be thesame, the additional costs to produce spe-cial small orders and to fill stocked itemson small orders significantly reduced theprofitability of these customers. Kanthalnow realized that it had a few extremelyprofitable customers and a few extremelyunprofitable ones (Kaplan and Cooper 1998:185) and was surprised by the wide variationin customer profitability. Exhibit 10 graph-ically portrays select Kanthal customersand how they add or detract from prof-itability. Generally, the first few customersales vs. cost of sales contributed the mostprofit, while the last few customers gener-ated the largest losses due to high sellingor post-sale costs.

Even more surprising to Kanthal wasthat some of the customers with the mostsales were the most unprofitable. Two very

unprofitable customers were in the topthree in terms of sales volume. One ofthese unprofitable high volume customershad moved to just-in-time (JIT) orderingfrom its suppliers, placing orders weeklyand sometimes twice a week. Variations inthe profit margins on individual ordersranged from -179% to +65% as shown inExhibit 11.

The company also discovered that 40%of the Swedish customers generated 250%of the profits. Finally, it also discoveredthat the most profitable 5% of the customersgenerated 150% of the profits. This was ashocking discovery as it had been thoughtthat most customers contributed to profit.This phenomenon of a few customers beingthe most profitable is present in manycompanies.

Traditional cost accounting often supportsa 20-80 rule that 20% of the largest cus-tomers, who purchase the most products,contribute 80% of the profits. Using ABC,analysts have often found that 20% of thecustomers generate 300% of the profits.The remaining 80% of the customers areactually unprofitable and can result in aloss of 200% of the profits. When plottedon a graph, (See Exhibit 12), the “hump” of this “whale curve” indicates the profitearned by the company’s most profitablecustomers. The remaining customers arebreak-even or unprofitable and bring theoverall profit back down to 100%. Thegoal is to make each customer profitable.

18

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

Exhibit 10 – Customer Profitability: Ranked from Most to Least Profitable

Number of customers

P-Vol

Source: Kaplan 1989:13.

21 5 10 20 40 60 80 100 120 140 160 180 190 195 198 199 200

200

150

100

50

0

–50

–100

–150

–200

With a new understanding of which cus-tomers were profitable and which were not,Kanthal became dedicated to turning unprof-itable customers into profitable ones. Thecompany developed ways to retain the cus-tomers and decrease their administrativeand selling costs (Kaplan and Cooper 1998:188). In the short term, Kanthal tried the

following: reduce the size of its product lines,accept orders only for stocked items, useexternal distributors to reduce the cost ofsmall accounts, change compensation tosalesmen to emphasize profit rather thanonly sales volume, and engineer to reduceset-up times and improve operational effi-ciencies.

C U S TO M E R P RO F I TA B I L I T Y A N A LYS I S

19

S001S002S003S004S005S006S007S008S009S010S011S012S013S014S015S016

1389152118281222

1,21046,18451,10298,8803,150

24,1044,8602,705

51867,9584,105

87,8651,2741,813

37,0606,500

54310,08050,56760,7851,557

14,8892,6571,194

23351,9531,471

57,581641784

15,9746,432

5721,7164,5765,148

5722,8601,144

572572

4,5761,1444,576

5721,1441,1441,144

04,524

12,06413,5722,3404,6804,680

00

12,0640

12,0642,340

03,0163,016

9529,864

(16,105)19,375(1,319)

1,675(3,621)

939(287)(635)1,490

13,644(2,279)

(115)16,926(4,092)

8%65

-3220

-427

-7535

-55-13616

-179-646

-63

Exhibit 11 – Customer Order Analysis

Standard order cost: SEK572Manufacturing order cost for non-stocked products: Foil Elements: SEK1508

Finished Wire: SEK 2340

Invoiced Volume Order Operating

Country Order Value Cost Cost Non-Stocked Profit Profit

Customer Lines (SEK) (SEK) (SEK) (SEK) (SEK) Margin

Sweden

Note: All financial data reported in Swedish kroner (SEK).

Source: Kaplan 1989:11.

Exhibit 12 – Cumulative Profitability by Customers

Cumulative Profits

Cumulative % of Customers

Pro

fits:

% o

f To

tal

0 1 5 10 15 20 30 40 50 60 70 80 90 95 99 100

250

200

150

100

50

0

In the longer term, the following aresome of the actions taken as a result of thenew ABC system: • involvement of salespersons was

increased in discussions with manage-ment and customers;

• prices were increased for small, custom-ized orders;

• product managers were encouraged toreduce proliferation of sizes and variancein product line;

• salespersons emphasized standard prod-ucts; and

• customers were persuaded to make largerorders of stocked items.

With one particular customer, Customer#200 (see Exhibit 10), Kanthal devised anexcellent solution that would make thecompany profitable and satisfy the customer.The company went to the customer, sharedthe ABC analysis, and explained the impli-cations for profitability of producing onlysmall orders of non-stocked items. Kanthaloffered a new pricing structure that grantedthe customer a 10% discount on high vol-ume orders of stocked products and chargeda 60% price premium for small orders ofnon-stocked items. The results of this newpricing structure were reviewed one yearlater; Kanthal found that Customer #200gave the company the same volume ofbusiness but placed orders half as manytimes per year, and for half as many differ-ent products. Customer #200 changed fromthe most unprofitable customer into oneof the most profitable in the course of oneyear (Kaplan and Cooper 1998:188).

Kanthal’s approach was to work with itscustomers for the benefit of both the firmand the customer. The company providedsome customers with computer terminalsdirectly linked to the Kanthal office so thecustomers could order directly without anysales effort being employed. Another cus-tomer, who had placed several small ordersfor many different types of products, wasconverted to a distributor. Kanthal soldlarger quantities to the customer thatstocked the items for its own use. This cus-tomer also added a profit to some of theproducts and resold them to other smallcompanies. Thus Kanthal was thus able toreduce its service costs to this one customerand better service other small companies.

In these instances, Kanthal discovered,like many other companies, that rapidimprovements in information technologycould simultaneously provide substantial

benefits to both customer service and cus-tomer profitability. Further, companieshave recognized that customer behavior,customer satisfaction, and customer prof-itability can all be increased when thisnew information on customer profitabilityis shared directly with the customer.

The ability to determine customer prof-itability on an individual basis can addvalue to the company-customer relation-ship. As in the case of Kanthal, the cus-tomer can be helped to reduce its costsand the company can become more prof-itable. Increasingly with ABC, managementof activities is the focus - cost accountingbecomes more about managing costs (ratherthan cost accumulation), knowing whatcauses costs to occur, and making changesto reduce expenditures. Kanthal was ableto work with its existing customers fortheir mutual benefit.

Using customer profitability analysis todetermine the causes of costs and subse-quently making changes to reduce thosecosts are important lessons to be learnedfrom the Kanthal case. Customer profitabil-ity can only be increased by reducing costsor raising revenues. Ways to increase thatprofitability through better managementof customer costs are facilitated by improvedcost analysis. In this case, an ABC analysiswas critical. The managers were unwillingto take any action until they were present-ed with the data that indicated the prof-itability of products and customers.

Customer Profitability Analysis in a Service Company

The Co-operative Bank was founded inEngland in 1872 as a department in acooperative wholesale society, which wasthe central organization formed by cooper-ative societies throughout the country.Cooperative societies were formed to aidworking class people in obtaining goodsand services at lower costs through tradeand cooperation. The bank’s main functionwas to serve the banking needs of thewholesale cooperatives and thus had fewpersonal accounts. It expanded to servemany of the upcoming and growing coop-erative societies around the country.

In 1971, an Act of Parliament establishedthe bank as a separate legal entity. Thecooperative movement had declined alongwith deposit and loan accounts due tocompetitive pressure from private businesses.

20

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

Reorganized, the bank began to aggressivelypursue deposits from personal customers andby the 1990s had deposits of approximately3 billion pounds sterling. As the bank grew,it also broadened the range of products andservices for personal and corporate customers.Increased competition from other banksand customer demand led to new productsbeing introduced including credit cards,high-interest bearing current accounts, ATMcards, telephone banking and independentfinancial advice.

Under new management, the Co-operativeBank issued both a mission statement and astatement of ethical policy. These documentsdeclared the bank’s responsibility to its cus-tomers, its employees and its communities,and promoted the cooperative values estab-lished at the founding of the bank in 1872.In the early 1990s, Co-operative Bank founditself in the midst of an economic recessionand was forced to make changes to its oper-ations in order to be more competitive andefficient. It consolidated some of its opera-tions and reduced employment through vol-untary retirement. However, it also increasedits cross-selling activities to existing customersand began to offer a much wider choice ofproducts. While the bank believed it had anarray of excellent products and services forits customers, its cost-to-income ratio was

higher than its competition. Traditionalresponsibility accounting was being used tomeasure expenses for geographic and depart-mental cost centers but the bank was unableto track costs to customers or to products.

In 1993, the Co-operative Bank began anambitious project to improve its profitabilityand customer service. The new Project Sabre’sgoal was to improve the cost-to-income ratioand the service to customers. In order toaccomplish this, the bank needed additionalinformation for making changes that relatedto five corporate needs:• overhead reduction;• re-engineering of business processes,

particularly those that did not add valueto customers;

• product profitability;• customer profitability; and• segment profitability (Datar and Kaplan,

1995:5).

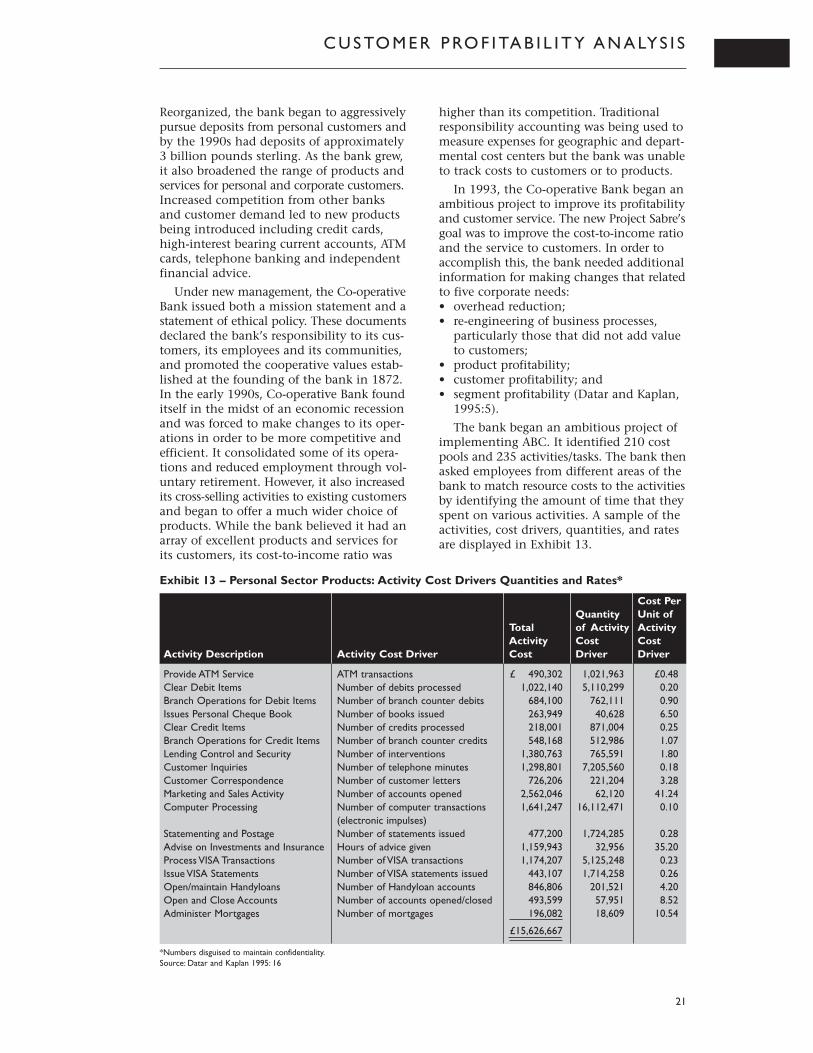

The bank began an ambitious project ofimplementing ABC. It identified 210 costpools and 235 activities/tasks. The bank thenasked employees from different areas of thebank to match resource costs to the activitiesby identifying the amount of time that theyspent on various activities. A sample of theactivities, cost drivers, quantities, and ratesare displayed in Exhibit 13.

C U S TO M E R P RO F I TA B I L I T Y A N A LYS I S

21

Exhibit 13 – Personal Sector Products: Activity Cost Drivers Quantities and Rates*

Provide ATM Service ATM transactions £ 490,302 1,021,963 £0.48Clear Debit Items Number of debits processed 1,022,140 5,110,299 0.20Branch Operations for Debit Items Number of branch counter debits 684,100 762,111 0.90Issues Personal Cheque Book Number of books issued 263,949 40,628 6.50Clear Credit Items Number of credits processed 218,001 871,004 0.25Branch Operations for Credit Items Number of branch counter credits 548,168 512,986 1.07Lending Control and Security Number of interventions 1,380,763 765,591 1.80Customer Inquiries Number of telephone minutes 1,298,801 7,205,560 0.18Customer Correspondence Number of customer letters 726,206 221,204 3.28Marketing and Sales Activity Number of accounts opened 2,562,046 62,120 41.24Computer Processing Number of computer transactions 1,641,247 16,112,471 0.10

(electronic impulses)Statementing and Postage Number of statements issued 477,200 1,724,285 0.28Advise on Investments and Insurance Hours of advice given 1,159,943 32,956 35.20Process VISA Transactions Number of VISA transactions 1,174,207 5,125,248 0.23Issue VISA Statements Number of VISA statements issued 443,107 1,714,258 0.26Open/maintain Handyloans Number of Handyloan accounts 846,806 201,521 4.20Open and Close Accounts Number of accounts opened/closed 493,599 57,951 8.52Administer Mortgages Number of mortgages 196,082 18,609 10.54

£15,626,667

Cost Per Quantity Unit of

Total of Activity Activity Activity Cost Cost

Activity Description Activity Cost Driver Cost Driver Driver

*Numbers disguised to maintain confidentiality.Source: Datar and Kaplan 1995: 16

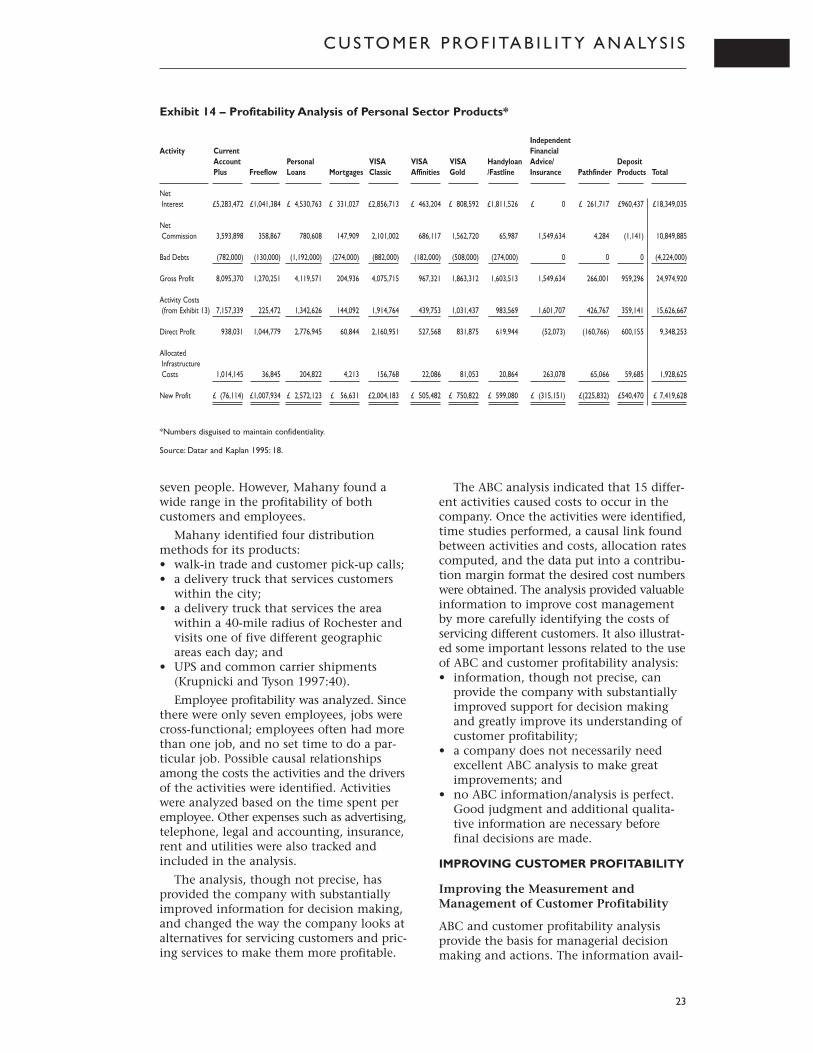

The total costs of each activity weredetermined by combining all of the resourcepool costs assigned to each activity. Thecosts of each activity were then traced tothe various bank products by definingactivity cost drivers for each activity. Theactivity cost driver represented the eventthat triggered the performance of eachactivity, such as a deposit that was processedor an account that was opened. The bankwas then able to distribute the activity coststo various bank products. Some bankingexpenses, sustaining costs representing 15%of the total costs, were not allocated toactivities or bank products. These costswere spread over the entire product andcustomer service range of activities. Ananalysis of product profitability was one ofthe results, as set out in Exhibit 14.

The profitability analysis provided thebank with vital information to make deci-sions about product offerings, strategy andfuture growth. The analysis showed thatthe Independent Financial Advice/Insuranceproduct considered by the bank to be ahighly profitable business was actually losingmoney. Current Account Plus, the basic coreproduct of the bank, was not profitable.The bank now had a wealth of informationabout the cost of each activity (the cost toprocess cheques and, credit card transac-tions, open and close accounts): with thisinformation the bank could reassess itsproduct and service offerings. The bankrealized that it had the highest cost-to-income ratio of United Kingdom banks andhad to cut its costs and services in order tosurvive. A weakness of the product prof-itability analysis was that it ignored thecross-selling opportunities of the differentproducts that the bank offered. For example,the Independent Financial Advice/Insuranceproduct while unprofitable may be attrac-tive to wealthy account holders, help toretain those customers and ultimatelyincrease their lifetime profitability.

The initial analysis was limited to productprofitability and the bank’s team wantedto extend the ABC analysis to customerprofitability by examining individual cus-tomers with current accounts. Specificassumptions were made in the allocationof the costs of the customer accounts. Theteam allocated 55% of current accountexpenses to transaction costs and 45% toaccount maintenance. Customers were seg-mented into Low, Medium and High basedon the turnover of funds in their accounts

in order to allocate the transaction costs.On the revenue side, the bank determinedthe income earned from the balances andfees for individual customers. By matchingincome with the allocated costs, managerswere now able to estimate the profitabilityof each customer. This revealed that up tohalf of all current accounts, particularlythose with low balances, were unprofitable.

In service organizations such as Co-oper-ative Bank, costs are usually committed farin advance. Thus there is little incrementalcost or savings from reducing or increasingcustomer service or activity. Each customeruses each bank product differently, so it is important to have substantial customeranalysis information. For a chequingaccount, some customers write a lot ofcheques and some do not; some customersmaintain high balances and some maintainonly minimal balances.

Once the information on product andcustomer profitability is obtained, whatshould management do with it? The bankdevised new strategies for profitabilitysuch as: • cross-sell more profitable products; • distinguish between new customer and

mature accounts;• switch unprofitable customers to ATM

transactions;• set pricing for minimum balances, ATM

fees, overdrafts; and• outsource ATM network, computer

operations and cheque clearing.

The Co-operative Bank used ABC to betterunderstand the costs of its wide range ofproducts and its diverse customers. Prior tothe ABC implementation, bank manage-ment was unable to agree on which werethe profitable and unprofitable productsand customers. The information from boththe product profitability analysis and thecustomer profitability analysis for individualcustomers and customer groups was essen-tial to improving customer and corporateprofitability.

Customer Profitability Analysis in a Small Company

Customer profitability analysis applies tosmall companies as well. When MahanyWelding Supply, a Rochester, New York distributor of welding supplies, examinedcustomer profitability, there were somesurprises. The company employs only

22

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

Exhibit 14 – Profitability Analysis of Personal Sector Products*

C U S TO M E R P RO F I TA B I L I T Y A N A LYS I S

23

Independent Activity Current Financial

Account Personal VISA VISA VISA Handyloan Advice/ Deposit Plus Freeflow Loans Mortgages Classic Affinities Gold /Fastline Insurance Pathfinder Products Total

Net Interest £5,283,472 £1,041,384 £ 4,530,763 £ 331,027 £2,856,713 £ 463,204 £ 808,592 £1,811,526 £ 0 £ 261,717 £960,437 £18,349,035

Net Commission 3,593,898 358,867 780,608 147,909 2,101,002 686,117 1,562,720 65,987 1,549,634 4,284 (1,141) 10,849,885

Bad Debts (782,000) (130,000) (1,192,000) (274,000) (882,000) (182,000) (508,000) (274,000) 0 0 0 (4,224,000)

Gross Profit 8,095,370 1,270,251 4,119,571 204,936 4,075,715 967,321 1,863,312 1,603,513 1,549,634 266,001 959,296 24,974,920

Activity Costs (from Exhibit 13) 7,157,339 225,472 1,342,626 144,092 1,914,764 439,753 1,031,437 983,569 1,601,707 426,767 359,141 15,626,667

Direct Profit 938,031 1,044,779 2,776,945 60,844 2,160,951 527,568 831,875 619,944 (52,073) (160,766) 600,155 9,348,253

Allocated Infrastructure Costs 1,014,145 36,845 204,822 4,213 156,768 22,086 81,053 20,864 263,078 65,066 59,685 1,928,625

New Profit £ (76,114) £1,007,934 £ 2,572,123 £ 56,631 £2,004,183 £ 505,482 £ 750,822 £ 599,080 £ (315,151) £(225,832) £540,470 £ 7,419,628

*Numbers disguised to maintain confidentiality.

Source: Datar and Kaplan 1995: 18.

seven people. However, Mahany found awide range in the profitability of both customers and employees.

Mahany identified four distributionmethods for its products:• walk-in trade and customer pick-up calls;• a delivery truck that services customers

within the city;• a delivery truck that services the area

within a 40-mile radius of Rochester andvisits one of five different geographicareas each day; and

• UPS and common carrier shipments(Krupnicki and Tyson 1997:40).

Employee profitability was analyzed. Sincethere were only seven employees, jobs werecross-functional; employees often had morethan one job, and no set time to do a par-ticular job. Possible causal relationshipsamong the costs the activities and the driversof the activities were identified. Activitieswere analyzed based on the time spent peremployee. Other expenses such as advertising,telephone, legal and accounting, insurance,rent and utilities were also tracked andincluded in the analysis.

The analysis, though not precise, hasprovided the company with substantiallyimproved information for decision making,and changed the way the company looks atalternatives for servicing customers and pric-ing services to make them more profitable.

The ABC analysis indicated that 15 differ-ent activities caused costs to occur in thecompany. Once the activities were identified,time studies performed, a causal link foundbetween activities and costs, allocation ratescomputed, and the data put into a contribu-tion margin format the desired cost numberswere obtained. The analysis provided valuableinformation to improve cost managementby more carefully identifying the costs ofservicing different customers. It also illustrat-ed some important lessons related to the useof ABC and customer profitability analysis: • information, though not precise, can

provide the company with substantiallyimproved support for decision makingand greatly improve its understanding ofcustomer profitability;