Team H Hasbro, Inc. - smf.business.uconn.edu · owns a broad portfolio of toys, games and...

38

Methodology Weight Price DCF 90% 107.13 $ EV/EBITDA 10% 103.61 $ Current Price 92.45 $ 1 Year Target Price 106.78 $ Upside Return 15.50% 2018 Dividend $2.52 Dividend Yield 2.36% Total Return 18.22% Valuation Date JAN 12th, 2018 Hasbro, Inc. DATE: January 12 th ,2018 TICKER: HAS RECOMMENDATION: BUY CURRENT PRICE: $92.45 TARGET PRICE: $107 INDUSTRY: Toys & Games EXECUTIVE SUMMARY: Hasbro is a multinational conglomerate, which owns a broad portfolio of toys, games and entertainment & license, including Nerf, Monopoly, Transformers, and My Little Pony, and consistently aims to create the world’s best play experience. Figure 1 Source: Bloomberg Figure 2 Source: Team Analysis Figure 3 Source: Team Analysis, Bloomberg Figure 5 Source: Team Analysis, Bloomberg Figure 4 1 Year Target Price Source: Bloomberg Better and worse case rage Closing Price Avg. Daliy Vol (mm) Shares O/S (mm) Market Cap ($mm) P/E Enterprise Value($mm) Market Date JAN 12th, 2018 $92.45 1.3 125 11,515 19.8x 13,556 1 HIGHLIGHTS Our recommendation is BUY with a 1-year target price of $107 per share, representing 18% total upside from the $92.45 closing price on January 12 th , 2018. Our valuation is based on a 90/10 mix of the Discounted Cash Flow Valuation and EV/EBITDA Comparable Valuation. Business Projections • Successful storytelling, primarily through movies, will continue to enhance sales. • Hasbro will maintain partnerships with major Intellectual Property (IP) owners such as Disney and Marvel and strengthen its market position by acquiring additional popular IPs. • Major markets will continue to grow for the next 7 years with YOY growth rates from 2.46% in 2018 to 0.94% in 2024. • By expanding global markets, Hasbro will execute its storytelling strategy through a broader base and will increase its sales accordingly. • Product diversification and brand awareness will help Hasbro maintain a sustainable business. Solid Fundamentals • High operating margins and EBITDA margin indicate effective corporate management and healthy operations. • High dividend growth rate shows confidence in Hasbro’s financial status and its willingness to reward its shareholders. We expect dividends to continue to grow at an average of 10% YOY for the next 7 years. • High EPS and ROE demonstrate Hasbro’s strong potential as a investment. Hasbro Future Price Forecast Fundamentals Industry Median Hasbro Investment Grade Business Investment Grade Revenue Growth 8% 7% Medium Storytelling Skill High Dividend Growth Rate 9% 12% High Corporate Strategy Medium EPS 1.61 4.64 High Product Diversification High Operating Magrin 10% 15% High Brand Awareness High EBITDA Margin 15% 18% High Management Team High ROE 20% 27% High IPs Maintenance High P/E 24.2 19.8 High Market Growth Medium Dividend Yield 2% 2.45% Medium Supply Chain Management Low Team H

Transcript of Team H Hasbro, Inc. - smf.business.uconn.edu · owns a broad portfolio of toys, games and...

Methodology Weight Price

DCF 90 10713$

EVEBITDA 10 10361$

Current Price 9245$

1 Year Target Price 10678$

Upside Return 1550

2018 Dividend $252

Dividend Yield 236

Total Return 1822

Valuation Date JAN 12th 2018

Hasbro IncDATE January 12th 2018 TICKER HAS RECOMMENDATION BUYCURRENT PRICE $9245 TARGET PRICE $107 INDUSTRY Toys amp Games

EXECUTIVE SUMMARY Hasbro is a multinational conglomerate whichowns a broad portfolio of toys games and entertainment amp licenseincluding Nerf Monopoly Transformers and My Little Pony andconsistently aims to create the worldrsquos best play experience

Figure 1

Source Bloomberg

Figure 2

Source Team Analysis

Figure 3

Source Team Analysis Bloomberg

Figure 5

Source Team Analysis Bloomberg

Figure 4

1 Year Target Price

Source Bloomberg

Better and worse case rage

Closing Price

Avg Daliy Vol (mm)

Shares OS (mm)

Market Cap ($mm)

PE

Enterprise Value($mm)

Market Date JAN 12th 2018

$9245

13

125

11515

198x

13556

1

HIGHLIGHTSOur recommendation is BUY with a 1-year target price of $107 per sharerepresenting 18 total upside from the $9245 closing price on January12th 2018 Our valuation is based on a 9010 mix of the Discounted CashFlow Valuation and EVEBITDA Comparable ValuationBusiness Projectionsbull Successful storytelling primarily through movies will continue to

enhance salesbull Hasbro will maintain partnerships with major Intellectual Property (IP)

owners such as Disney and Marvel and strengthen its market position byacquiring additional popular IPs

bull Major markets will continue to grow for the next 7 years with YOYgrowth rates from 246 in 2018 to 094 in 2024

bull By expanding global markets Hasbro will execute its storytelling strategythrough a broader base and will increase its sales accordingly

bull Product diversification and brand awareness will help Hasbro maintain asustainable business

Solid Fundamentalsbull High operating margins and EBITDA margin indicate effective corporate

management and healthy operationsbull High dividend growth rate shows confidence in Hasbrorsquos financial status

and its willingness to reward its shareholders We expect dividends tocontinue to grow at an average of 10 YOY for the next 7 years

bull High EPS and ROE demonstrate Hasbrorsquos strong potential as a investment

Hasbro Future Price Forecast

Fundamentals Industry Median Hasbro Investment Grade Business Investment Grade

Revenue Growth 8 7 Medium Storytelling Skill High

Dividend Growth Rate 9 12 High Corporate Strategy Medium

EPS 161 464 High Product Diversification High

Operating Magrin 10 15 High Brand Awareness High

EBITDA Margin 15 18 High Management Team High

ROE 20 27 High IPs Maintenance High

PE 242 198 High Market Growth Medium

Dividend Yield 2 245 Medium Supply Chain Management Low

Team H

BUSINESS DESCRIPTIONHasbro is a worldwide leader in childrens and familiesrsquo leisuretime entertainment products and services Hasbro is not limited to justgames it covers all types of entertainment ranging from toys and gamesto television movies and digital gaming Based on Franchise Brands andPartner Brands Hasbro offers a set of options covering a wide range ofaudiences including Nerf My Little Pony Transformers Play-DohMonopoly Magic The Gathering Marvel and Disney Princesses Withthe help of the Hasbro Studio and Allspark Pictures its self-financingco-financing film unit and Discovery Communications Hasbro deliversstorytelling products Through its high-standard of Corporate SocialResponsibility and philanthropic commitment Hasbro has devoted tomaking the world a better place for children and familiesHasbrorsquos international operations contributed 49 of net revenues in2016 growing from 39 in 2010 (Figure 7) In recent years the companyhas expanded its operations in the emerging markets of China RussiaBrazil Peru Colombia South Korea Romania and the Czech Republic

CORPORATE STRATEGYStorytellingHasbro supports its brands with storytelling leveraging and integratingtheir products with synergy and value created by stories In additionHasbro takes advantage of all the available platforms and mediaproviding a variety of digital experiences music publishing location-based entertainment and an impressive array of consumer productswithin a broad range of diverse categories For example after scanningthe barcode of My Little Pony consumer has the opportunity to interactwith digital forms of traditional games

Brand BlueprintSince 2009 Hasbro has applied Brand Blueprint as its core strategyHasbro gleans consumer insights and tells stories through immersiveentertainment experiences such as movies and TV series which becomean effective way of extending toy life cycles strengthening consumerloyalties and elevating brand awareness Then Hasbro uses its omni-channel retail partners to sell toys worldwide Moreover Hasbroacquired Backflip Studios in 2013 and created digital games from itsfranchise characters such as Transformers to leverage the digitizedtrend and capitalize on the opportunity integrating technologythroughout the engagement cycle

Expanding Our AudienceExpanding Our Audience serves as another core strategy Hasbrofocuses on ldquogrowing share of liferdquo by using different methods such asTV games music and theme parks to influence and expand its loyaltybase for all ages Through this strategy the company formed its ownunique culture which could be passed from generation to generation

CORPORATE MANAGEMENTThe Hasbro executive management team consists of 9 professionals(Figure 9) with an average of 8 years left on their contracts Eachexecutive has an average of 20 years experience within the company(See Appendix 28) Brian D Goldner the Chairman and CEO is the onlyexecutive serving on the board which suggests board independenceThe President has less than one year left on his contract Based on thehistory of the roles in Hasbrorsquos management team considering the priortwo CEOs both came from inside the company we do not anticipatemajor changes in the near future Approximately 45 of thecompensation of the top management team comes from stock andoptions (figure 10) offering incentive for better stock performance inthe future

Figure 6

Source Bloomberg

Figure 7

Source Bloomberg

Figure 8

Source Original

Figure 9

Figure 10

Source Bloomberg

Source Bloomberg

2

Brian D Goldner Chairman CEO

John A Frascotti President

Deborah M Thomas Executive VP CFO

Wiebe Tinga Executive VP CMO

Rudolph Johnson Executive VP CHO

Barbara Finigan Executive VP CLO

Duncan J Billing Executive VP CSO

Tom Courtney Executive VPGlobal Operations

Stephen Davis Executive VPCCO

Executive Officers

INDUSTRY OVERVIEWSGeneral TrendIn major markets that Hasbro covers traditional toys amp games had amarket size of $5509 billion in 2016 with a projection of $6310 billionin 2021 equivalent to a 275 YOY growth The total toys amp gamesindustry was $12676 billion in 2016 which is anticipated to expand to$16248 billion in 2021 509 YOY growth (Figure 13) The highergrowth is ascribed to the fast-developing digital games with a YOYgrowth of 675 from 2016 to 2021 We anticipate the traditional toysand games industry will continue to expand but the digital trend willgrow at a faster pace As the absolute leader in industry Hasbro is in astrong position to take advantage of the expansion in traditional toysand games (See Appendix 13)Consumer BehaviorWe focused on the US market since it generated 51 of Hasbrorsquosrevenue in 2016 Based on the Consumer Expenditure Survey from theBureau of Labor Statistics (Figure 14) the percentage of toyconsumption over annual expenditures falls in the range of 011 to035 among different age segments Although it represents a smallpercentage of personal income it indicates a steady growth in majorpopulation groups (population ages 25-34 and 35-44) Married coupleswith children from ages 0 to 17 the major consumers in the industryshowed an annual average spending of $385 in 2016 (Figure 15) Weexpect the future expenditure in toys will grow slightly along with anincrease in personal income especially with Hasbrorsquos Expanding OurAudience strategy which should help the company win a broaderaudience

CORPORATE GOVERNANCEHasbro has a Board of Directors of 12 members (Figure 11) in 5 differentcommittees Audit Compensation Executive Finance and GovernanceNominating amp Social Responsibility three more members than itscompetitor Mattel representing a more diversified and comprehensiveoutlook

$0

$50

$100

$150

$200

$250

Under 25years

25-34years

35-44years

45-54years

55-64years

65 yearsand older

65-74years

75 yearsand older

Spending on Toys Hobbies amp Playground Equipment

2013

2014

2015

2016

SHAREHOLDER STRUCTUREHasbro has 12456 million shares of common stock outstanding of whichInstitutional investors own 95 The top 5 holders are Vanguard Group(1044) BlackRock (864) Alan G Hassenfeld (665) Capital GroupCompany (496) and State Street Corp (386) Alan G Hassenfeldthe third biggest shareholder is the former chairman and current boardmember of Hasbro and the share under his name represents more thanhis personal holding According to Hasbro DEF 14A filed on April 4th2017 3844 of the holding belonged to Hassenfeld Family InitiativesLLC 52 holding was under Mr Hassenfeldrsquos name and 85 belongs toHasenfeld Foundation The shareholder structure is diversified with noshareholder holding more than 105 Although the insider holding(Figure 12) is higher compared with its competitor Mattel the trend hasbeen decreasing for the past few years (See appendix 23)SOCIAL RESPONSIBILITYHasbro aims to make safe toys to protect their workersrsquo rights andsafety to ensure materials are ethically sourced and to maintainenvironmental sustainability In 2016 Hasbro achieved 100 use ofrenewable energy realized carbon neutrality and launched sustainablepackaging principles Hasbro also works closely with regulatory bodies toprovide safer products For eight years Hasbro has not had a singleproduct recall In addition Hasbro provides a series of compliancetrainings to more than 5000 employees to help their employeesunderstand their rights In 2016 with volunteer service from employeesHasbro impacted 38 million children through its charitable programsand helped more than 225000 youths together with generationOn

$

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

Marriedcouple

only

Marriedcoupleoldestchild

under 6

Marriedcoupleoldestchild

6 to 17

Marriedcoupleoldest

child 18or older

Othermarriedcouple

Oneparentat least

one childunder 18

Singleperson

and otherconsumer

units

Spending by Composition of Consumer Unit

2013

2014

2015

2016

Figure 12

Source Bloomberg

Figure 11

Source Bloomberg

Figure 13

Source NPD

Source Bureau of Labor Statistics

Source Bureau of Labor Statistics

Figure 14

Figure 15

0

50000

100000

150000

200000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Total Toys amp Games Market Size

Traditional Toys and Games Video Games

3

Brian D Goldner Edward M Philip

Kenneth A Bronfin Linda K Zecher

Tracy A Leinbach Michael Burns

Alan G Hassenfeld Crispin H L Davis

Lisa Gersh Mary Beth Stone West

Richard S Stoddart Hope F Cochran

Board of Directors

-600

-400

-200

000

200

400

1990 1993 1996 1999 2002 2005 2008 2011 2014

Growth of Population from Age 0 to 14

United States European Union

Russian Federation China

Brazil

25

16

22

17

26

29

15

00

05

10

15

20

25

30

35

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

The US GDP Forecast

the US GDP Growth GDP Forecast from Federal Reserve

GDP Forecast from World Bank GDP Forecast from IMF

-10

-5

0

5

10

15

GDP Growth of Major International Markets

European Union Russian Federation

China Mexico

Brazil

0

5

10

15

20

25

0

1

2

3

4

5

6

7

8

9

Exchange Rate

Euro UK Pound

Canadian Dollar Hong Kong Dollar

Chinese Yuan Brazilian Real

Mexican Peso (RHS)

Figure 16

Source World Bank

Figure 17

Source Federal Reserve World Bank IMF

Figure 18

Source World Bank

Figure 19

Source Federal Reserve 4

Demographic ShiftEmerging markets have enjoyed more robust growth in 0-14 years oldpopulation (Figure 16) Even though majority of birth rates decreasedexcept for that in Russia population growth represents an opportunity forHasbro to grow its revenue Take China as an example due to the impactof the one-child policy the population between age 0-14 years olddecreased drastically in the 90s However after the termination of thepolicy the population from age 0-14 gradually increased With a higherpopulation of target customers in these markets the toys and gamesindustry should achieve more growth

International EconomyThe European economy has been stable for the past few years with aslight decrease recently With Brexit a bigger decrease is expected in thefuture The Russian economy has been suffering from the sagging crudeoil prices Combined with sanctions and the falling rubble the economyworsened further Latin America is facing corruption unremittingviolence and instabilities in its political system With three presidentialelections on the horizon in most the populous countries ColombiaMexico and Brazil in 2018 the future economy may become morevolatile The Chinese economy has been accelerating for a decade but itmay fall into the middle-income trap (Figure 18) We do not anticipate thiswill have an immediate effect but perhaps a more slowed growth in theChinese economy

Volatile Performance in Different BrandsEven though people have become more reliant on digital devices thedemand for traditional games and puzzles grew a 12 growth in 2016showing increased demand for face-to-face play experience (SeeAppendix 13) Although we predicted the revenue of the whole brandsportfolio the sub brands can also be volatile due to different populartrend and consumer taste shifts

MACRO ECONOMY PROJECTION

US EconomyUS economic growth remained strong in the third quarter of 2017realizing 3 growth On December 13th the Federal Reserve raised thebenchmark rate by 025 the third increase in 2017 signaling healthygrowth in the economy Economic projections from the Federal ReserveBoard members and Federal Reserve Bank presidents we expect theexpansion remain at or slow to 18 (Figure 17) in 2019 Moreoverforecasts from World Bank and International Monetary Fund also indicatea similar sentiment Consumer products toys and games may beadversely affected by the slowing GDP growth (See Appendix 14)

Exchange RateFrom January 2000 to December 2017 the majority of currencies inHasbrorsquos markets depreciated (Figure 19) except for the Hong KongDollar with only a slight depreciation of 047 and the Chinese Yuanwith an appreciation of 2726 With most of the suppliers located inChina the rising local currency put pressure on the costs of Hasbro But anappreciation in local currency would have the effect of boostingrepatriation in USD Therefore it will be a good opportunity to continue toexpand in the Chinese market As for other markets we expect lessfavorable exchange rates We anticipate there will be some loss due toexchange rates in other comprehensive income unless Hasbro adjusts thedistribution in the respective markets

Hasbro Third-Party Factory

China India Vietnam United States

Ireland Indonisia Japan Turkey

Figure 20

Source Hasbro Official Website

Figure 21

Source Team Analysis

Figure 22

Source Team Analysis

Figure 23

Source Team Analysis 5

HASBRO COMPETITIVE POSITIONThe toys amp games industry (Figure 21) is characterized by a strong rivalryamong existing competitors As one of the largest players in the USHasbro sustains an unyielding competitive position Even though strongcompetition exists in this industry consumers and suppliers have lessbargaining power due to exclusive IPs and excess number of suppliersrespectively In addition the threat from new entrants is low due to highcompetition and regulations and the high threat of the substitutes makesthis industry even less appealing (See Appendix 7)

HASBRO vs MATTELBoth companies overall have similar product lines For instance on themanufacturing side both produce most of the physical toys for movies andstory franchises such as Hasbrorsquos Star Wars and Transformers toys andMattelrsquos Jurassic Park and Batman vs Superman toys Moreover Mattelbegan to replicate Hasbrorsquos storytelling and entertainment success bypromoting and producing movies like Barbie which is scheduled to bereleased by August 2018 This shift in strategy will increase the productionof films targeting kids In 2017 the entertainment industry released 30childrens movies establishing a new record (See Appendix 19)Hasbrorsquos culture has been stable it involves a communal environment(Figure 22) where people are able to freely act and feel comfortable wheninteracting with their peers This culture has fostered more genuine andcollaborative relationships This approach will help Hasbro become moreproductive in the long term On the other hand Mattelrsquos culture has beenadversely effected by all the changes in its leadership team which hasproduced a lot of resentment and fragmentation within the departmentsand employees Many of the employees feel that they are being forced toadopt different cultures every time a reorganization occurs

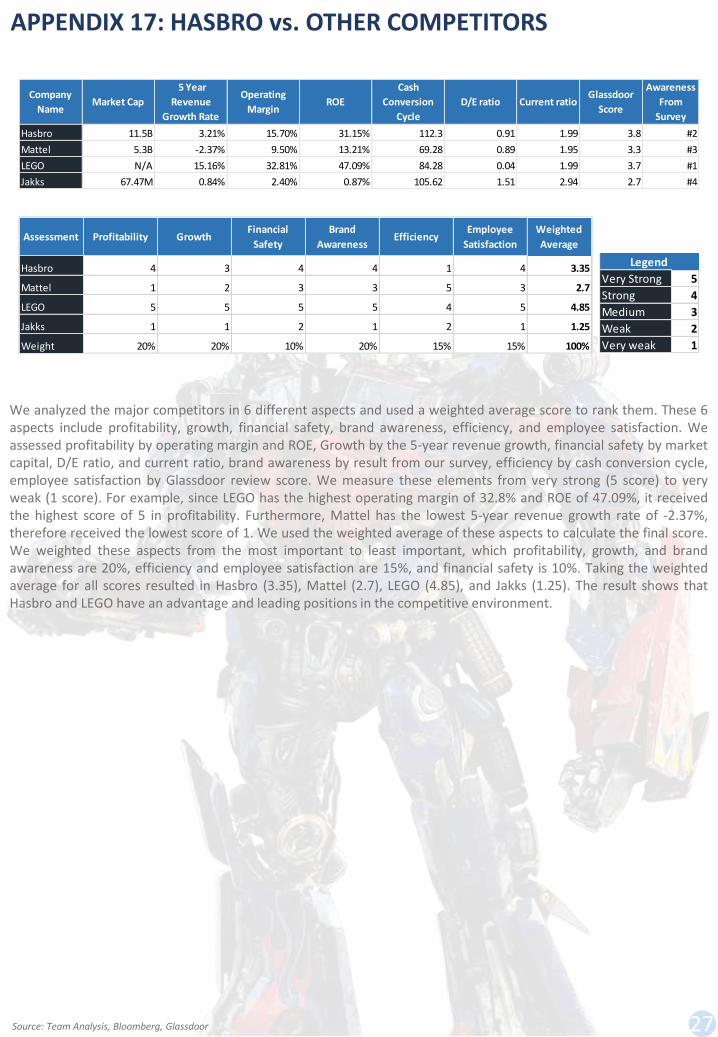

HASBRO vs COMPETITORSIn the US toys amp games market Hasbro has three major competitorsMattel Lego and Jakks Pacific In comparing characteristics listed in Figure23 Lego has a leading advantage over the other three competitors Hasbrostruggles in managing efficiency due to overseas manufacturing andinadequate supply chain management In addition both Hasbro and LEGOhave absolute leading positions in their respective growth and profitabilitywhile others are weak in these aspects From our survey (See Appendix 8)

SUPPLIERS amp RETAILERSRetailersThe largest three retailers of Hasbro are Walmart Target and Toys ldquoRrdquo Uswhich contribute around 62 of the net revenues in the US and Canadaand 18 9 and 9 respectively in its global net revenues Due to thehigh concentration any issues to one of the major customers willsignificantly impact HasbroSuppliersBased on Hasbrorsquos Third-Party Factory List in 2016 the majority ofsuppliers are located in China (Figure 20) due to its cheaper labor costsBecause of the appreciation in local currency and increasing labor coststhe company will move 30 of the production in China to suppliers inother countries such as India and Indonesia The trend of ldquomoving to Indiardquohas already begun with several of Hasbrorsquos suppliers making moves

Mercenary

Soci

abili

ty

LOW

LOW

HIG

H

HIGHSolidarity

Networked Communal

Organizational Culture Matrix

Fragmented

Hasbro

Mattel

we see that Lego and Hasbro havethe 1 and 2 brand awarenessamong all toy manufacturers As oneof the leading players in the industryHasbro can use these advantages togenerate more profits compared toMattel and Jakks (See Appendix 17)

Assessment Profitability GrowthFinancial

Safety

Brand

AwarenessEfficiency

Employee

Satisfaction

Weighted

Average

Hasbro 4 3 4 4 1 4 335

Mattel 1 2 3 3 5 3 27

LEGO 5 5 5 5 4 5 485

Jakks 1 1 2 1 2 1 125

Weight 20 20 10 20 15 15 100

Figure 24

Source Team Analysis Bloomberg

Figure 25

Source Team Analysis Bloomberg

Figure 25

Source Bloomberg

Figure 26

Source Bloomberg

Figure 27

Source NPD Team Analysis

Figure 28

Source Team Analysis Bloomberg

Historical Target Price amp Actual Price Gap

6

MARKET PERSPECTIVE OF THE STOCKFrom historical data of the 1-year target price of analysts following Hasbrowe can see that these analysts have had a conservative perspective on theHasbro 12month target stock price (Figure 25) From 2014 to 2017 Theseanalysts averaged a 1-year target price of about 14 lower than the 1-yearactual price Today the 17 analysts issue an average target price of $10554(Figure 26) which is higher than the current price of $9245

DCF VALUATIONDCF valuation method consists of a two-stage growth model The first phaseis based on individual year to year forecasts up to 2024 and the second phaseis terminal value based on a long term growth of 263 Based on our DCFanalysis the estimated 1 year target price is $107 (See Appendix 4)

REVENUE GROWTH PROJECTIONWe found three main revenue drivers the Transformers movies and partnerbrand movies new IP acquisitions and Hasbrorsquos growth in major marketsWe anticipate revenue will keep growing for the next 7 years primarily due tothe following reasons 1) the release of future Transformers movies in 20192021 and 2023 and other partner movies such as Avengers Infinity War in2018 and Frozen 2 in 2019 2) acquisitions of new IPs similar to Frozen andBeyblade and 3) Hasbrorsquos major markets should see continuous positivegrowth of 246 in 2018 to 094 growth in 2024 (Figure 27) We believethat Hasbrorsquos major traditional toys amp games business will be negativelyimpacted by the strong digital game market growthWe calculated the final revenue (Figure 28) by adjusting the market growthrate in accordance to the movie releases and potential new IPs as shown indetail in Appendix 9

INVESTMENT SUMMARYOur recommendation is BUY with a 1-year target price of $107 per sharewhich is based on a 9010 mix of the Discounted Cash Flow Valuation andEVEBITDA Comparable ValuationRevenue DriversFirst successful storytelling through movies such as the Transformers and MyLittle Pony will help Hasbro boost brand awareness Second by acquiringnew IPs in the future similar to Hasbrorsquos past acquisitions of Yo-Kai WatchBeyblade and Frozen Hasbro will increase future revenue Third Hasbrorsquosmajor markets are expected to have continuous positive growth for the next7 years from 246 in 2018 to 094 in 2024 Lastly Hasbro is expanding inemerging markets In November 2016 Hasbro partnered with Tmall whichincreased Transformersrsquo YOY growth by 47 on a single day there ispotential for Hasbro to grow in other emerging marketsStock Price DriversBased on historic analysis Hasbrorsquos stock price is 53 correlated to itsrevenue In combination with our projections for Hasbrorsquos revenues for thenext 7 years we believe the stock price will rise in concert with revenueFurthermore we expect dividends will continue growing at an average of10 YOY for the next 7 years (Figure 25) driven by revenue growth andadditional benefits from tax-reform

Buys 5290 9

Holds 4710 8

Sells 000 0

Avg 12M Tgt Px 10554$

Current Price 9245$

Institutions Recommendations

Revenue Breakdown FY 2016 FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

Revenue 5019822 537116 568183 617013 615860 657997 656823 675711 678776

Growth Rate 1287 700 578 859 -019 684 -018 288 045

Franchise Brands 2327668 255686 248016 262897 252381 265000 251750 261820 253965

Growth Rate 185 985 -300 600 -400 500 -500 400 -300

Partner Brands 141277 134015 140716 154787 147048 157341 155768 157325 162045

Growth Rate 2828 -514 500 1000 -500 700 -100 100 300

Hasbro Gaming 813433 97954 115585 133501 150856 166696 180031 189933 195631

Growth Rate 2282 2042 1800 1550 1300 1050 800 550 300

Emerging Brands 465951 49461 50203 51207 52488 54062 55954 58193 60811

Growth Rate 1693 615 150 200 250 300 350 400 450

Hasbros Major Market Growth Rate 287 246 243 217 232 207 126 094

Figure 29

Source Team Analysis Bloomberg

Figure 30

Source Team Analysis Bloomberg

Figure 31

Source Team Analysis Bloomberg

Revenue Breakdown FY 2014 FY 2015 FY 2016 FY 2017

Revenue 427721 444751 501982 537116

Growth rate 478 398 1287 700

Franchise Brands 234513 228541 232767 255686

Growth rate -255 185 985

Partner Brands 65406 110131 141277 134015

Growth rate 6838 2828 -514

Hasbro Gaming 64362 66232 81343 97954

Growth rate 291 2282 2042

Emerging Brands 63441 39847 46595 49461

Growth rate -3719 1693 615

Source Team Analysis

Figure 32

Figure 33

Source Team Analysis Bloomberg

FINANCIAL ANALYSIS

WACC amp LONG-TERM GROWTH RATE CALULATIONWe took the average of the cash paid for interest over long-term debt andthe companyrsquos bondsrsquo yields to calculate cost of debt We took the average ofthe CAPM and the Two-Stage Golden Growth Model to calculate the cost ofequity resulting in a WACC of 744 (Figure 30) We used the 10 yearTreasury Note yield as the risk free rate (255) market risk premium(545) data from Bloomberg and projected 2017 tax rateWe adopted three major resources to conduct the economic predictionsWorld Bank IMF and projections from the Federal Reserve Board membersand Federal Reserve Bank presidents We averaged the projections from thethree sources to get the projections for 2017 2018 2019 and calculated theweighted average based on the revenue breakdown in each area(Figure 31)(See Appendix 11)

DCF CALCULATIONWe used the Discounted Cash Flow Model to calculate free cash flow and theterminal growth rate to calculate terminal value We then added back cashsubtracted total debt to get the enterprise value and then divided by thenumber of basic shares outstanding as of 2017 to calculate the fair value ofHasbrorsquos stock price

CAPITAL EXPENDITURECapital expenditure increased in recent years because of Hasbrorsquos investmentin information systems as well as new office space for the Hasbroheadquarters Hasbro expects capital expenditures to be in the range of $130million to $160 million in 2017

COST OF GOODS SOLDWe expect COGS of Hasbro will increase by 136 (Figure 29) for 2 years andthen decrease by 032 from 2020 to 2024 The latter negative trend is dueto a decrease in plastic prices and a decrease in labor costs due to Hasbrorsquosplan to move 30 of production from China to India and other cheap laborcountries (See Appendix 10)

Revenue GrowthFrom 2007 to 2016 Hasbrorsquos revenue has grown steadily at a CAGR of 3(Figure 33) including three years of negative growth in 2010 2012 and 2013Though the 2008 financial recession effected many industries the toys ampgames industry seemed to be less effected indicated by both Hasbro andMattelrsquos steady revenue In 2007 Hasbro released the Transformers moviewhich had remarkable success and helped Hasbro increase its revenuesignificantly This franchise became the biggest revenue growth driver forHasbro For example in 2007 and 2009 The Transformers productsaccounted for 126 and 145 of consolidated net revenues respectivelyOther than the Transformers movies other partner brand movies such asJurassic Park and the Marvel movies also played important roles in therevenue growth During the last 9 years Hasbro worked with Beyblade Yo-Kai Watch and Disneyrsquos Frozen to generate significant revenue in 2011 2015and 2016 respectively (See Appendix 9) 7

COMPARABLE VALUATIONWe used EVEBITDA for the comparable valuation We chose industry peersbased on similarities of products and target customers (Figure 32) Some non-US toy companies and entertainment companies are included because theyeither indirectly compete with Hasbro or have similar strategies and businessmodels We also used benchmarks to identify similar candidates based onDebtEquity ratio EBITDA Margin and 5 year revenue growth Howeversince we view Mattel to be the only solid comparable we deemphasized theEVEBITDA comparable valuation and weighted the comparable valuation10 in calculating our final fair value Considering the comparable valuationwas based on interactive ratios between Hasbro and its industry peers itoffered insights about the industry and financial status of Hasbro (SeeAppendix 12)

CompanyAdjusted

EV

EBITDA

T12MEVEBITDA

Implied

Price

Median 550852 57137 964 $7201

Hasbro 1211031 99646 1215 $9211

Mattel 791931 48466 1634 $12560

Tomy 143064 18853 759 $5559

Bandai 550852 74605 738 $5395

Spin Master 441761 25523 1731 $13335

Alpha Group 314579 32600 965 $7208

Goldlok Toys 80568 3260 2471 $19260

Average 504827 43279 1359 $10361

Year 2018-2019 2020-2024

Freight -324 -100

Paper 011 010

Labor 867 -500

Plastics 300 000

Electronic Device -134 005

COGS Growth Rate 136 -032

Cost of Equity 785

2 - Stage Dividend Growth Model 720

CAPM 851

Cost of Debt 451

Average Bond Yield After Tax 279

Interes Over Long-Term Debt 622

Market Cap $mm 11515

Long-Term Debt $mm 18753

Tax Rate 2278

WACC 744

-50

0

50

100

150

2011 2012 2013 2014 2015 2016

Pay Out Ratio vs DividendFCF

Pay Out Ratio DividendFCF

Figure 34

Source Bloomberg

Figure 35

Source Bloomberg

Figure 36

Source Bloomberg

Figure 37

Source Bloomberg

Figure 38

Source Team Analysis Bloomberg

Operating MarginHasbrorsquos operating expenses consist of royalties product developmentadvertising amortization of intangibles program production costamortization and selling distribution and administration (Figure 34) Weexpect operating margins will slowly decrease in the future mainly due toincreasing royalties and COGS Hasbrorsquos largest IPs Marvel and Star Warswill end in 2018 Hasbro must renegotiate and we expect the royalties feeto increase (See Appendix 22) In the long run we expect operating marginswill be between 13 to 14 (Figure 35)

Dividend amp Stock BuybackUsually we analyze the payout ratio since dividend per share is a fixedamount However the common outstanding shares can be varied bydifferent operations such as stock buy back or issuance of options etcTherefore we introduced another way to look at the dividend policydividendFCF (Figure 36) FCF is cash after operations and capitalinvestment available to pay dividends The higher the ratio the less acompany retains for future use Although Hasbrorsquos pay out ratio oncepeaked at more than 70 dividendFCF consistently remains below 50(except for 2012 and 2014) which presents a safe level of dividends and agood retention rate for Hasbrorsquos future operations Moreover Hasbroconstantly buys back their shares which led to a decrease in its commonoutstanding shares We anticipate that future stock buybacks will continueand the dividend yield will continue to be raised

Key RatiosFrom the table (Figure 38) we can see that liquidity in the past has beenvery healthy and above the industry median Our forecast for futureliquidity is similarly healthy due to increasing revenue and stablebusinesses Profitability is also above the industry median due to thecompanyrsquos leading position in the industry and benefits from economies ofscale Hasbrorsquos Financial risk is low because it has a high interest coverageratio and stable future cash flows The payout ratio is expected to keepincreasing in the future due to high growth of dividends We believe atsome point in the future Hasbro will slow dividend growth to match therevenue growth and hence lower the payout ratio Hasbrorsquos cashconversion cycle is lower than industry median indicating improper supplychain management However the cash conversion cycle has continued todecrease since 2012 which indicates Hasbro is managing to become moreefficient (See Appendix 15)

Revenue Surprise amp Stock RelationFrom the chart (Figure 37) we can see that the quarterly revenue surpriserelative to consensus estimates (per Bloomberg) and the stock price has a53 correlation from 2014 to 2017 Consequently we believe that theHasbro stock price is strongly driven by revenue surprises

8

Liquidity Analysis FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 Industry Median FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

Cash Ratio 088 050 083 092 079 079 098 099 099 099 089 089 090 090

Current Ratio 261 182 253 269 199 195 221 222 223 223 220 220 221 221

Profitability Analysis

Operating Margin 1349 1144 1485 1556 1570 875 1494 1443 1374 1374 1370 1366 1361 1356

Return on Asset 795 656 931 977 1124 697 1002 1044 1018 1016 1078 1074 1075 1070

Return on Equity 2298 1795 2642 2888 3127 1359 2694 2784 2743 2745 2673 2668 2674 2660

Finacial Risk Analysis

Total Debt to Equity 108 081 120 100 091 049 088 088 089 089 070 070 070 070

Interest Coverage Ratio 606 442 682 713 809 756 743 728 729 909 907 909 906

Net Debt EBITDA 110 110 116 087 047 045 015 012 009 008 -005 -005 -007 -007

Other

Payout Ratio 5562 7288 5242 5081 4624 3396 4902 4919 5193 5642 5737 6207 6505 6962

Dividend Growth Rate 2000 1111 750 698 1087 1176 1053 1032 1007 980 952 924 896

Efficiency

Days Inventory Outstanding 7212 7233 7377 7858 7375 7375

Days Sales Outstanding 9366 9468 9311 9463 9201 5517

Days Payable Outstanding 3082 3614 4432 4796 5347 4009

Cash Conversion Cycle 13496 13087 12256 12525 11230 7425

Figure 41

Source Team Analysis

Figure 42

Source Team Analysis

PR

OB

ILIT

Y

LOW

MED

IUM

LOW

HIG

H

MEDIUM HIGH

IMPACT

MK1

MK2

M 3

F1F 2

MK4

OP4

OP3

OP2

OP1

OP5

0

200

400

600

800

1000

1200

$88 $90 $92 $94 $96 $99 $101 $103 $105 $107 $109 $111 $113 $115 $117 $120 $122 $124 $126 $128 $13 $132

Monte Carlo Simulation

Figure 39

Source Team Analysis

Target Price $107

Freq

uen

cy

Figure 40

Source Team Analysis

MONTE CARLO SIMULATIONWe used the Monte Carlo simulation to predict possible price changes andidentify the most sensitive variable for Hasbro in our assumptions Wetested the revenue growth rate long-term growth rate and discount rate inMonte Carlo Simulation The findings show that the price is effected most

SENSITIVITY AND SCENARIO ANALYSISWhile doing DCF analysis in addition to our base case we introduced twoother scenarios better case and worse case Better case includesacquiring new IPs twice in the next 7 years and revenues increasing fasterthan base case due to better than expected storytelling strategies In thisbetter case for example a new release of the Transformers movie wouldhave great success increasing the 1 year target price to $11694 (Bettercase does not include merger with Mattel) Worse case includes statusquo with no changes of IPs in the next 7 years and a lower growth rate for

MARKET RISKMK1 Macro Economy ChallengeWe expect Hasbro will be challenging doing business in Latin America TakeBrazil as an example although Hasbrorsquos revenue in Brazil grew 20 in Q42015 it faced challenges with macroeconomic factors and politicalinstability in 2017 Moving forward we are optimistic about the potentialin Latin America but expect more volatility As for Europe with the UKleaving the European Union the economy of the EU will be negativelyeffected which already decreased the sales of the UK and Germany in Q22017 We anticipate sales will continue to face challenges in this area Forthe Asia Pacific area China is the largest potential market Although theappreciation in local currency will benefit Hasbro stricter capital controlmay make the future repatriation more difficult bringing uncertainties inHasbrorsquos development in ChinaMK2 A Stronger US Dollar Can be ExpectedWe analyzed the data from June 11th 2008 to December 14th 2017 duringwhich the Federal Reserve changed its Policy Benchmark Rate five timesWith strong expectations that the Fed will continue to deal withforeseeable strong GDP growth and actively manage CPI a stronger USDwill be expected which will in turn have a negative impact on Hasbrorsquosoverseas businessMK3 Potential Threat from the Fast-Developing Digital TrendChildren are exposed to digital media at an earlier age which in turn hashelped digital games grow faster Hasbro must successfully execute astrategy that caters to the fast-developing trend and mitigate the risk

by changes in the long-term growth rate Weexpect the revenue growth rate and long-term growth rate will grow at a base casegrowth rate (See Appendix 16) and appliedrandom growth rates from a specific range tosimulate a range of stock prices After running10000 simulation paths the result indicates a4789 probability that the price of Hasbrowill be above $107 There is a 5020probability the price will be between $9245and $107 The probability of the price beinglower than $9245 (current price) is only191

revenue due to worse than expected storytellingstrategies decreasing the 1 year target price to$9507 (Figure 40) The sensitivity analysis showsthe price ranges from $9819 to $11887 (Figure41) by changing long-term growth rate (24-28) and WACC (71-77)

9

10713 710 720 730 744 750 760 770

280 11887 11614 11354 11011 10867 10638 10419

270 11674 11412 11161 10831 10692 10471 10260

263 11534 11279 11035 10713 10577 10362 10155

250 11275 11033 10800 10493 1036348 10158 9960

240 11089 10855 10631 10334 10209 10010 9819

Long-

Term

Growth

Rate

WACC

Share Price(Base Case) 10713$

Share Price(Better Case) 11694$

Share Price(Worse Case) 9507$

Hasbro 1 Year Target Price

000

050

100

150

90

100

110

120

130

140

USD Broad Index vs Federal PolicyBenchmark Rate

USD Broad Index Federal Policy Benchmark Rate

050

150

250

350

1990 1993 1996 1999 2002 2005 2008 2011 2014

Birth Rate

United States European Union

Russian Federation China

Brazil Mexico

0

1

2

3

4

5

6

7

8

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Fertility Rate (Births Per Woman)

United States European Union

Russian Federation China

Brazil Mexico

Figure 43

Source Bureau of Labor Statistics

Figure 44

Source Bureau of Labor Statistics

Figure 45

Source Federal Reserve World Bank IMF

Figure 46

Source Bloomberg

10

MK4 Demographic ShiftWomen are having fewer children and some developed economies are facinglow birth rates (Figure 43 Figure 44) which raise concerns of maintaining thepopulation level The birth rate in the US has declined every year since 2007The shift in demographics may cause slower end-user market growth

FINANCIAL amp CREDIT RISKFI1 Interest RateWith the interest rate increased three times in 2017 (Figure 45) and projectedto increase another three times in 2018 we can expect that financing andrefinancing costs will be higher (See Appendix 13)FI2 Bankruptcy of Toys ldquoRrdquo UsToys ldquoRrdquo Us accounts for 9 of Hasbrorsquos net revenue globally The Toys ldquoRrdquo Usbankruptcy is a potential risk to Hasbro as we anticipate more allowance fordoubtful accounts and less accounts receivable due to the uncertainty of ToysldquoRrdquo Us future Also it may complicate the retail channels of Hasbro since ToyldquoRrdquo Us has a strong US presence

OPERATIONAL RISKOP1 Hard to Provide New Loyal BrandsIt is hard for Hasbro to consistently deliver new brand stories AlthoughHasbro has spent tremendous capital on its storytelling strategy lately thecompany has found it challenging to create new unique trademarks whichhistorically have been the core of its salesOP2 Remain Average Level in Catering to E-CommerceE-commerce represents only 15 of its total revenue which is the same as theaverage level in the industry If Hasbro cannot stand out from the crowdother competitors may take advantage of the trendOP3 Revenues Heavily Rely on MediaThe success or failure of blockbuster movies or TV can significantly impact thesales volume and revenue in turn If the Transformers movies do not meetexpectations not only cannot they boost sales but also cost Hasbro in initialinvestmentsOP4 Fail to Maintain Partnership with IP OwnersDue to the dependency on successful stories maintaining good relationshipswith major IP owners is essential Hasbro will pay a high price if it loseslicenses from IP owners such as Disney or MarvelOP5 Potential Financial Challenges in Emerging MarketsIn Q1 2016 some retailers in emerging markets met with difficulties andincurred bad debt Moving forward using a more active strategy whenentering emerging markets Hasbro may face the same risk due to unfamiliarbusiness environments and macroeconomic conditions

MERGERS amp ACQUISITIONSIn November 2017 Hasbro offered its major rival Mattel a takeover plan andgot an immediate rejection It was not the first time that Hasbro proposed tomerge with Mattel (two other proposals in 1996 and late 2015 respectively)Based on our analysis we believe the possibility of MampA is low (See Appendix20) But Hasbro had a successful MampA history It conducted 21 deals (Figure 46)in the past with 10 financed fully in cash one with partly cash and partly debtand 10 remain undisclosed The target companies fit in three major industriesCyclical Consumer Goods amp Services Technology and Communications In thepast three MampA deals two belonged to Communication and one belonged toTechnology which may indicate Hasbrorsquos interest in growing its digitalfootprint We also interviewed two experts Lutz Muller the President ofKlosters Trading Corporation and top expert in the industry who published athorough article of the MampA between Hasbro and Mattel on Seeking Alphaand Professor Hillary Greene Zephaniah Swift Professor of Law at UConnSchool of law and a visiting scholar at Harvard Law School who is an expert inantitrust They both offer great insights about the case and valuablesuggestions for our research (See Appendix 21)

Compnay Type Total Value (mil) Total Number

Communication $700 2

Consumer Cycl $70389 6

Others $69538 8

Technology $26645 5

Total $167272 21

Historical MampA Information

Company Type

APPENDIX 1 GLOSSARY

FRANCHISE BRANDSTransformers A brand based on robots with human shapes that turn into different machinesNerf A toy gun that shoots form soft bulletsMy Little Pony An entertainment franchise based on storytelling This franchise also has physical and virtual toys thataccompany the storiesLittlest Pet Shop A franchise based on animated television series Monopoly A board game where the playersrsquo objective is to own all the properties and all the money availableMagic The Gathering A game where players battle against each other by using cards that represent creatures withpowers and Magics

PARTNER BRANDSMarvel A comic series based on well-known superheroes including Spider-Man Wolverine the Hulk Thor Iron ManCaptain America X-Men the Guardians of the Galaxy and the Fantastic FourFrozen An animated musical fantasy movie produced by Disney including characters of Elsa Anna and OlafDisney Princess Disney animated film characters of the franchise are Snow White Cinderella Aurora Ariel andBelleYo-Kai Watch A Japanese popular mixed-media franchise of role-playing video games created and developed byLevel-5 The franchise has also become a popular anime television seriesStar Wars An epic space opera media franchise centered on a film series created by George LucasBeyblade A Japanese manga series written and illustrated by Takao Aoki focused on a group of kids who form teamsand battle one another using Beyblades

HASBRO GAMING BRANDSTaboo A popular party game that involves filling in the blank with interesting word choicesJenga A game where players take turns removing one block at a time from a tower constructed of 54 blocksScrabble A game in which two to four players score points by placing tiles bearing a single letter onto a boardSpeak OUT A game that players try to say different phrases while wearing a mouthpiecePie Face A game involves two players revolving around the gag of getting a pie in the faceDungeons amp Dragons A fantasy tabletop role-playing game

EMERGING BRANDSPlayskool Educational toys and games for children including Mr Potato Head Tonka Alphie Weebles ElefunSesame Street toys and GlowormBaby Alive A baby doll that eats drinks wets and in some cases messes all with a movable mouthFurby An American electronic robotic toy released in 1998 It resembles a hamster or owl-like creature and wentthrough a period of being a must-have toy following its holiday season launch with continual sales until 2000GI Joe A line of action figures representing four of the branches of the US armed forces with the Action SoldierAction Sailor Action Pilot Action Marine and the Action NurseHanazuki An animated childrens web show made in conjunction with a line of Hanazuki toysFurReal Robotic toys range from guinea pigs to dinosaurs coming in many sizes some are able to be held in a childshand and others are able to be ridden by a child

1011

APPENDIX 2 BALANCE SHEET

Source Team Analysis Bloomberg

ASSUMPTIONSbull There will be no huge MampA in the nest 7 yearsbull Hasbro will not issue new bonds to retire the prior debt that matures in 2021bull Allowance for doubtful account increased in 2017 due to filing of Chapter 11 of Toy ldquoRrdquo Us and decreased to

previous level as uncertainty subsidesbull Hasbro will continue to buyback its stock in the futurebull Hasbro will not issue new shares in the near futurebull The dollarrsquos appreciation will have a slight negative impact in the near future

12

$mm FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

Cash and Equivalents 84970 68245 89317 97675 128229 173229 183248 197007 196638 180392 180018 186048 187027

Operating Current Assets 167810 181701 182593 190375 196212 216297 228808 248471 248007 264976 264503 272109 273343

Property Plant amp Equipment - Net 23041 23626 23749 23753 26740 26205 25681 25167 24664 24171 23929 23809 23571

Other Intangible Assets 41666 37600 32453 28081 24595 219 194 173 153 136 121 108 96

Goodwill 47493 59432 59344 59270 57056 56596 55908 55228 54557 53894 53239 52592 51953

Other Noncurrent Assets 69519 71523 65759 74409 77986 80121 82314 84568 86883 89261 91705 94216 96795

Allowance For Doubtful Accounts 1960 1900 1590 1490 1680 3390 1724 1665 1587 1659 1637 1627 1641

Total Assets 432539 440227 451624 472072 509137 570912 593656 626035 624499 624665 623868 637910 640612

Operating Current Liability 73607 92656 82245 90008 109556 129182 136654 148398 148120 158255 157972 162515 163252

Financial Debt 162079 139662 181238 171168 172097 187530 195001 205636 205132 175186 174963 178901 179659

Other Noncurrent Liabilities 46115 35130 38892 40488 38939 41880 39323 39721 40061 39304 39826 39943 39875

Total Liabilities 281801 267448 302375 301665 320593 358592 370977 393756 393313 372745 372761 381359 382786

MinorityNon Controlling Int (Stckhldrs Eqty) - 4545 4273 4017 2270 - - - - - - - -

Common Stock 10485 10485 10485 10485 10485 10485 10485 10485 10485 10485 10485 10485 10485

Additional Paid In Capital 65594 73418 80627 89363 98542 107763 117847 128875 140935 154124 168547 184319 201567

Treasury Stock (Amount) (253565) (255473) (298007) (304090) (318168) (334240) (351123) (368859) (387491) (407064) (427626) (449227) (471919)

Accumulated Other Comprehensive Income (7231) (3414) (9545) (14600) (19457) (22952) (26649) (30663) (34670) (38952) (43225) (47622) (52038)

Retained Earnings (Accumulated Deficit) 335455 343218 363007 385232 414872 451264 472119 492442 501928 533327 542927 558596 569732

Par Value 050 050 050 050 050 050 050 050 050 050 050 050 050

Shares Issued 20969 20969 20969 20969 20969 20969 20969 20969 20969 20969 20969 20969 20969

Total Shareholders Equity 150738 172779 149249 170407 188544 212321 222679 232280 231186 251919 251107 256551 257827

Total Liabilities and Shareholders Equity 432539 440227 451624 472072 509137 570912 593656 626035 624499 624665 623868 637910 640612

$mm FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

Cash and Equivalents 1964 1550 1978 2069 2519 3034 3087 3147 3149 2888 2886 2917 2920

Operating Current Assets 3880 4127 4043 4033 3854 3789 3854 3969 3971 4242 4240 4266 4267

Property Plant amp Equipment - Net 533 537 526 503 525 459 433 402 395 387 384 373 368

Other Intangible Assets 963 854 719 595 483 383 327 276 246 218 194 169 149

Goodwill 1098 1350 1314 1256 1121 991 942 882 874 863 853 824 811

Other Noncurrent Assets 1607 1625 1456 1576 1532 1403 1387 1351 1391 1429 1470 1477 1511

Allowance For Doubtful Accounts 045 043 035 032 033 059 029 027 025 027 026 026 026

Total Assets 10000 10000 10000 10000 10000 10000 10000 10000 10000 10000 10000 10000 10000

Operating Current Liability 2612 3464 2720 2984 3417 3602 3684 3769 3766 4246 4238 4261 4265

Financial Debt 5752 5222 5994 5674 5368 5230 5256 5222 5215 4700 4694 4691 4693

Other Noncurrent Liabilities 1636 1314 1286 1342 1215 1168 1060 1009 1019 1054 1068 1047 1042

Total Liabilities 10000 10000 10000 10000 10000 10000 10000 10000 10000 10000 10000 10000 10000

MinorityNon Controlling Int (Stckhldrs Eqty) 000 263 286 236 120 000 000 000 000 000 000 000 000

Common Stock 696 607 702 615 556 494 471 451 454 416 418 409 407

Additional Paid In Capital 4352 4249 5402 5244 5226 5075 5292 5548 6096 6118 6712 7184 7818

Treasury Stock (Amount) -16822 -14786 -19967 -17845 -16875 -15742 -15768 -15880 -16761 -16159 -17030 -17510 -18304

Accumulated Other Comprehensive Income -480 -198 -640 -857 -1032 -1081 -1197 -1320 -1500 -1546 -1721 -1856 -2018

Retained Earnings (Accumulated Deficit) 22254 19865 24322 22607 22004 21254 21202 21200 21711 21171 21621 21773 22097

Par Value 003 003 003 003 003 002 002 002 002 002 002 002 002

Shares Issued 1391 1214 1405 1231 1112 988 942 903 907 832 835 817 813

Total Shareholders Equity 10000 10000 10000 10000 10000 10000 10000 10000 10000 10000 10000 10000 10000

APPENDIX 3 INCOME STATEMENT

Source Team Analysis Bloomberg

$(mm) FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

Revenue 100 100 100 100 100 100 100 100 100 100 100 100 100

Revenue growth - - - - - - - - - - - - -

Cost of Goods Sold 4089 4098 3971 3771 3796 3936 3989 4044 4031 4018 4006 3993 3980

Royalties 739 830 714 853 816 780 800 820 840 861 883 905 928

Product development 492 509 520 546 531 500 504 508 512 516 520 524 528

Advertising 1033 975 983 920 930 935 934 935 935 936 937 938 939

Amortization of intangibles 124 192 123 098 070 060 050 040 035 030 025 020 015

Program production cost amortization 102 117 110 095 072 062 057 052 047 042 037 032 027

Selling distribution and administration 2072 2135 2094 2160 2213 2233 2223 2228 2225 2227 2226 2226 2226

Operating Income (Loss) 1349 1144 1485 1556 1570 1494 1443 1374 1374 1370 1366 1361 1356

Net Income GAAP 822 701 972 1016 1098 1065 1091 1033 1030 1024 1020 1015 1010

$(mm) FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

Revenue 408900 408220 427720 444750 501980 537116 568183 617013 615860 657997 656823 675711 678776

Revenue growth -459 -017 478 398 1287 700 578 859 -019 684 -018 288 045

Cost of Goods Sold 167200 167290 169840 167700 190550 211407 226674 249498 248248 264397 263094 269807 270177

COGS as Revenue 4089 4098 3971 3771 3796 3936 3989 4044 4031 4018 4006 3993 3980

Gross Profit 241700 240930 257880 277050 311430 325709 341510 367515 367612 393600 393729 405904 408599

- Operating Expenses 186522 194216 194346 207854 232630 245462 259517 282754 282969 303473 303983 313907 316525

Royalties 30207 33892 30532 37925 40952 41895 45432 50576 51750 56679 58000 61167 62988

Product development 20120 20759 22256 24294 26638 26856 28636 31344 31532 33953 34155 35407 35839

Advertising 42224 39810 42026 40939 46894 50220 53068 57691 57583 61589 61544 63382 63737

Amortization of intangibles 5057 7819 5271 4372 3476 3223 2841 2468 2156 1974 1642 1351 1018

Program production cost amortization 4180 4769 4709 4245 3593 3330 3239 3208 2895 2764 2430 2162 1833

Selling distribution and administration 84735 87168 89554 96080 111077 119938 126301 137467 137054 146515 146212 150438 151110

Operating Income (Loss) 55178 46714 63534 69196 78800 80247 81993 84761 84643 90127 89746 91997 92074

Operating margin 1349 1144 1485 1556 1570 1494 1443 1374 1374 1370 1366 1361 1356

- Non-Operating (Income) Loss 984 1153 954 88 956 6170 6584 7211 7259 7822 7874 8168 8272

Non-Operating (Income) Losssales 241 282 223 198 190 115 116 117 118 119 120 121 122

Pretax Income 45338 35184 53994 60396 69240 74077 75409 77549 77384 82305 81872 83829 83802

- Income Tax Expense (Benefit) 1174 679 1267 157 1593 1687 1342 1384 1392 1496 1488 1523 1523

Tax rate 2589 1930 2347 2600 2301 2278 1780 1785 1799 1817 1817 1817 1817

Income (Loss) from Cont Ops 33598 28394 41324 44696 53310 57204 61988 63709 63460 67348 66994 68595 68573

- Minority Interest 0 -23 -26 -5 -182 00 00 00 00 00 00 00 00

Net Income GAAP 33598 28624 41584 45196 55130 57204 61988 63709 63460 67348 66994 68595 68573

Basic Weighted Avg Shares 1301 1302 1284 125 1253 1245 1225 1205 1185 1165 1145 1125 1105

Basic EPS GAAP 258 220 324 362 440 459 506 529 536 578 585 610 621

ASSUMPTIONSbull Revenue will grow in the next 7 years due to the release of new movies new IP acquisitions and Hasbrorsquos

major marketsrsquo growthbull COGS will increase due to plastic and labor cost increases from 2018 - 2019 and slightly decrease from 2020 to

2024bull Operating expense will increase mainly due to increasing royalties and COGSbull Tax rate will decrease due to the new tax billbull Shares outstanding will decrease due to stock buybackbull EPS will increase due to stock buyback and revenue and earning increase

13

APPENDIX 4 DISCOUNTED CASH FLOW VALUATION

Source Team Analysis Bloomberg

We used the Discounted Cash Flow Model to calculate free cash flow asNet Income + Depreciation amp Amortization ndash Change in Working Capital ndash Capital Expense + Net Interest after taxand terminal value using long-term growth rate We added back cash and subtracted total debt to get the equityvalue and divided by the number of basic shares outstanding to calculate the fair value of Hasbrorsquos stock Wecalculated capital expenditure by change in Net PPampE+ depreciation Capital expenditure increased in recent yearsbecause of Hasbrorsquos investment in information systems and new office for its headquarters Hasbro also expectscapital expenditures to be in the range of $1300 million to $1600 million Forecasts of capital expenditure is basedon information from Q3 2017

14

$(mm) FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

Net Income 39776 38536 33598 28624 41584 45196 55130 57204 61988 63709 63460 67348 66994 68595 68573

Depreciation amp Amortization 14630 16040 15030 18100 15790 15540 15450 15682 15917 16156 16398 16644 16744 16844 16944

Working Capital 82022 87379 94203 89045 100348 100366 86656 87115 92154 100074 99887 106721 106531 109594 110091

Change in Wworking Capital 5357 6824 -5158 11303 018 -13711 459 5039 7920 -187 6834 -190 3063 497

Capex -11260 -9940 -12010 -11203 -11339 -14202 -16734 -14618 -15226 -17330 -14658 -17947 -15636 -17141 -16383

Net Interest expense 7293 9105 9396 9061 10676 9311 8853 9646 10031 10578 10552 9011 9000 9202 9241

Add Back Net Interest After Taxes 5713 7214 6963 7312 8170 6890 6816 7449 8245 8690 8653 7374 7364 7530 7562

FCF 46492 36757 47991 42903 53405 74373 65258 65885 63305 74040 66585 75657 72765 76198

WACC 744

Long-term Growth Rate 263

Year FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 10477 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

FCF 46492 36757 47991 42903 53405 74373 65258 65885 63305 74040 66585 75657 72765 762

Terminal Value 16269

Total 46492 36757 47991 42903 53405 74373 65258 65885 63305 74040 66585 75657 72765 17031

Enterprise Value 13566

Add Back Initial Cash 1732

Asset value 15298

Subtract Initial Debt 1875

Imputed Equity Value 13423 10713 710 720 730 744 750 760 770

Divide by Shares Outstanding 125 280 11887 11614 11354 11011 10867 10638 10419

Share Value(Base case) 10713 270 11674 11412 11161 10831 10692 10471 10260

Share value(Better Cae) 11841 263 11534 11279 11035 10713 10577 10362 10155

Share Value(Worse case) 9411 250 11275 11033 10800 10493 1036348 10158 9960

Current market value per share 9245 240 11089 10855 10631 10334 10209 10010 9819

Long-

Term

Growth

Rate

WACC

SENSITIVITY

BETTER CASE REVENUE

WORSE CASE REVENUE

BASE CASE REVENUE

APPENDIX 5 SCENARIO ANALYSIS

Source Team Analysis

ASSUMPTIONSbull Franchise Brands revenue will be lumpy increase sharply in the years with a new Transformers moviebull Partner Brands revenue will increase in the years that have partner brand movie releases and new IP dealsbull Hasbro Gaming revenue will increase but the rate at which it will increase will slow down due to the impact of

the digital gaming trendbull Emerging Brands will slowly improve due to continues investment in products and brands innovationbull Hasbrorsquos major marketsrsquo will increase due to growth in traditional toys amp games industry

ASSUMPTIONSbull Franchise Brands revenue will increase faster than the base case due to better than expected storytelling

strategiesbull Partner Brands revenue will increase faster than the base case due to precise capturing of consumersrsquo tastes and

acquisition of more new IPsbull Hasbro Gaming revenue will be supported by stronger demand for face to face play experiencebull Emerging Brands will increase due to successful investment and catering to the popular trendsbull Hasbrorsquos major marketsrsquo growth will remain the same as in base case

ASSUMPTIONSbull Franchise Brands revenue will increase slower than the base case due to inadequate execution of strategiesbull Partner Brands revenue will increase slower than base case due to no new IP acquisitionbull Hasbro Gaming revenue will increase but will have a larger negative impact from the digital gaming trendbull Emerging Brands will increase slower than expected due to inefficient investment and unmeet consumersrsquo tastebull Hasbrorsquos major marketsrsquo growth will remain the same in base case

15

Revenue Breakdown FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

Revenue 537116 568183 617013 615860 657997 656823 675711 678776

Growth Rate 700 578 859 -019 684 -018 288 045

Franchise Brands 255686 24802 26290 25238 26500 25175 26182 25397

Growth Rate 985 -3 6 -4 5 -5 4 -3

Partner Brands 134015 14072 15479 14705 15734 15577 15733 16205

Growth Rate -514 5 10 -5 7 -1 1 3

Hasbro Gaming 97954 11559 13350 15086 16670 18003 18993 19563

Growth Rate 2042 18 16 13 11 8 6 3

Emerging Brands 49461 5020 5121 5249 5406 5595 5819 6081

Growth Rate 615 150 200 250 300 350 400 450

Hasbros Major Market Growth Rate 287 246 243 217 232 207 126 094

Bace Case

Revenue Breakdown FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

Revenue 537116 576169 639807 654623 716589 734610 792943 818555

Growth Rate 700 727 1104 232 947 251 794 323

Franchise Brands 255686 25313 27338 26791 28667 27807 29475 29180

Growth Rate 985 -100 800 -200 700 -300 600 -100

Partner Brands 134015 14340 16060 15579 16981 17150 19380 20349

Growth Rate -514 700 1200 -300 900 100 1300 500

Hasbro Gaming 97954 11559 13870 16298 18742 21085 23193 24933

Growth Rate 2042 18 200 175 150 125 100 75

Emerging Brands 49461 5020 5196 5404 5647 5929 6256 6631

Growth Rate 615 150 3500 4000 4500 5000 5500 6000

Hasbros Major Market Growth Rate 287 246 243 217 232 207 126 094

Better Case

Revenue Breakdown FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

Revenue 537116 558190 594964 582080 596070 583416 589011 579741

Growth Rate 700 392 659 -217 240 -212 096 -157

Franchise Brands 255686 24290 25262 23746 24458 22746 23201 22041

Growth Rate 985 -500 400 -600 300 -700 200 -500

Partner Brands 134015 13804 14908 13864 13171 12776 12648 12775

Growth Rate -514 300 800 -700 -500 -300 -100 100

Hasbro Gaming 97954 11363 12897 14315 15532 16464 17040 17211

Growth Rate 2042 1600 1350 1100 850 600 350 100

Emerging Brands 49461 5020 5020 5045 5096 5172 5276 5408

Growth Rate 615 150 000 050 100 150 200 250

Hasbros Major Market Growth Rate 287 246 243 217 232 207 126 094

Worse Case

bull Fast-developing digital games may become substitutes

for traditional toys

bull Increasing options may intensify the competition in the

market

bull Uncontrollable seasonality in critical sales seasons due to

consumersrsquo behaviors

bull Fierce competition in storytelling strategy (eg Japanese

comics)

bull Increasing labor cost in China where most suppliers are

located

bull Regulatory changes and macroeconomic challenges

globally

APPENDIX 6 SWOT ANALYSIS

W

TO

S

SWOT

bull One of the largest and most recognized companies in

the toys amp games industry globally

bull Strong sales growth (464 compounded annual

growth in the past five years)

bull Exclusive license with well-known IP owners such as

Marvel and Disney

bull Comprehensive product portfolio including games

toys movies and TV series

bull High consumer loyalty and long product life cycles

thanks to storytelling strategy

bull Global presence operational efficiencies involve

increasing sales while decreasing cost

bull Strong penetration in emerging markets (Russia Brazil

and China)

bull Highly concentrated in 3 retailers accounting 64 of

the US sales

bull Encounter difficulties in creating new and unique

brands

bull Heavily rely on existing brands such as Transformers

and Nerf

bull Too big to nimbly respond to the market changes

bull Low percentage of sales in e-commerce accounting for

only 15 of the total sales

bull Integrate the digital trend into the every engagement

experience

bull Create new brands by executing storytelling strategy

bull Partner with e-commerce to elevate sales

bull Partner or create new toys incorporating local culture

(eg acquire IPs of famous Japanese comic stories and

manufacture characters and other toys)

16

APPENDIX 7 PORTER FIVE FORCES ANALYSIS

5 Very High

4 High

3 Medium

2 Low

1 Very Low

LEGEND

Threat of New Entrants ndash Low The threat of new entrants in the toys amp games industry is low Expansion of the digital gamesmarket has brought a lot of small digital game making companies to the industry which have taken market share from HasbroFor example in 2014 Blizzard Company launched Hearthstone (A digital card game similar to the Magic The gathering) whichnow has over $20M revenue per month However the traditional toys market has always been competitive highly consolidatedand always required high-economic-scale for generating profits Accordingly the barriers to entry remain relatively highCompanies in this industry enjoy high brand loyalty because consumers love exclusive characters such as Barbie Transformersand Monopoly which makes it more difficult for new companies to enter Moreover due to the high safety awareness oftraditional toys companies manufacturing processes require non-toxic materials with stricter regulations which not onlyincrease cost but also raise the barriers to entry In rare cases a company may enter the industry by capturing niche market thathas not been occupied by other companies

Bargaining Power of Buyers ndash Low The Bargaining Power of Buyers in the toys amp games industry is low Large retail stores

such as Toys ldquoRrdquo Us Walmart and Target are direct buyers in this industry The bargaining power of direct buyers is low because

there are so many different distribution channels for companies in the industry For example if Walmart refuses to sell Hasbro

products due to high price Hasbro has the ability to keep the same price to every other retailer who desires the product For the

end consumer the bargaining power is low due to exclusive characters belonging to only certain companies Even if prices are

high consumers will not find other companies selling the same characters and have no choice but to accept the price This is

why Toys ldquoRrdquo Us performed well in the past holiday season even during their Chapter 11 bankruptcy process Finally Hasbro will

eventually find new homes for its products even if certain retailers disappear

Bargaining Power of Suppliers ndash Low Hasbro outsources all of its production to third-party suppliers mainly located in

China Since China has a surplus of factories pricing remains competitive in order to get orders These suppliers do not have

much bargaining power with Hasbro Also there are more competitors located in countries with lower labor costs such as India

and Indonesia Considering the increasing labor costs in China Hasbro plan to move 30 of the production from China

Threat of Substitutes ndash Very high The threat for substitute products in this industry is strong and foreseeable Toys amp games

are goods used for a variety of purposes such as entertainment and relaxation People have abundant ways to entertain

themselves and relax themselves Instead of buying Transformers and Marvel heroes consumers may choose to play outdoors or

play other digital games Since there are varieties of entertainment besides toys and games the threat of being substituted in

this industry is very high Some kids prefer digital games over traditional toys making traditional toy making companies face

difficulties if they cannot adapt to the fast-developing digital trend

Rivalry Among Existing Competitors ndash High Rivalry among existing competitors is high due to the highly concentrated

distribution in the industry and limited growth in the future Although each company has its own consumer groups and exclusive

characters the slow growth and increasing number of new characters may lower the profitability and intensify competition

among the existing players

17

APPENDIX 8 SURVEY ANALYSIS

Where Do You Buy Toys

22

21

37

17

0

5

10

15

20

25

30

35

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

When Do You Buy Toys

Lego 1875 1

Hasbro 679 2

Mattel 661 3

Others 298 4

Jakks 179 5

Brand Awareness Weigted Average

We designed a proprietary survey to gauge brand awareness and gain insights on consumer behaviors in the toyindustry We received 116 results (it varied according to different questions) that further supported our analysis

Brand Awareness We mixed several famous toys from different brands such as Hasbro Mattel Lego Jakks andothers and asked respondents to order three items by their interest and awareness We then calculated theweighted average of each brand and analyzed the brand awareness based on the result Since the respondentsconsisted of different age stratification it was easily observed that Lego Barbie and Play-Doh impressed differentgenerations

Digital Games vs Traditional Toys When faced with the question ldquoWhat do your kids cousins nephews nieces andgrandkids typically play withrdquo surprisingly 74 selected traditional toys 16 chose video games while only 10answered tablets Although digital games may offer different play experiences traditional toys are critical inchildhood which we anticipate only modest change in the future

Purchase places Amazon has become the preferred channel to purchase toys It echoed our analysis that if Hasbrocan grow its sales through ecommerce and stand out among its peers they may get more advantage and expandtheir potential market share by capturing increasing group of customers who prefer online shopping

Purchasing and Seasonality Our findings indicated that most sales are concentrated in November December andJanuary with percentages of 14 29 12 respectively which indicates the strong seasonality in the industryAlthough some toys can be popular throughout the year 82 of parents expressed that they would wait until aspecial occasion or holiday season to buy toys for their children

18

GROWTH PROJECTIONWe observed that each Transformers movie release increased revenue of Boyrsquos sector over 60 in 2007 33 in2011 20 in 2014 We also observed that revenue of Boyrsquos sector decreased dramatically in the years without arelease of a Transformers movie For example in years 2010 2012 and 2013 the revenue of Boyrsquos sector decreased7 13 and 21 respectively We believe that the first Transformers movie significantly increased consumerawareness and helped Hasbro increase total revenue The follow-up movies had a smaller impact on the revenueand this impact will further reduce in the future due to competition of other Superhero movies such as DC moviesand Marvel movies Moreover audiences may lose loyalty to Transformers movies as time goes on So we anticipatethat the future release of Transformers movies expected in 2019 2021 and 2023 would have less impact on therevenue In 2011 2015 and 2016 Hasbro acquired new IPs such as Beyblade Yo-Kai Watch and Frozen which helpedHasbro increase revenue In 2011 Beyblade accounted for 111 of the total net revenue In 2016 Frozen helpedHasbro increase Girlrsquos sector revenue by 50 Understanding these historic patterns we expect that Hasbro toacquire new IPs to generate revenue in the forecast period

MARKET PROJECTIONWe believe that Hasbrorsquos major traditional toys amp games business will be negatively impacted by the strong digitalgames market growth We project that Hasbrorsquos major markets will have a downward trend in growth rate from297 in 2017 to 094 growth rate in 2024 We calculated Hasbrorsquos major market growth rate by taking theweighted average of each of Hasbrorsquos lines of businesses in different areas such as Asia Pacific US and Canada andLatin America and the traditional toys amp games growth rate in those markets The results indicate that Hasbrorsquosmajor market will keep growing in the future but the growth rate will slow The final revenue projection is as shownbelow

APPENDIX 9 REVENUE GROWTH PROJECTIONFY 2007 FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016

Revenue 38376 40215 40679 40022 42856 40890 40822 42772 44475 50198

Growth rate 479 115 -162 708 -459 -017 478 398 1287

Boysrsquo Toys 10240 10833 14710 13449 18215 15770 12376 14840 17759 18496

Growth rate 579 3578 -857 3544 -1342 -2152 1990 1967 415

Games and Puzzles 13236 13154 13409 12938 11670 11921 13112 12598 12765 13871

Growth rate -062 194 -351 -980 215 999 -392 133 866

Girlsrsquo Toys 6973 7905 7908 8304 7414 7923 10017 10226 7982 11939

Growth rate 1337 004 500 -1072 687 2643 209 -2194 4956

Preschool Toys 4349 4807 4514 5325 5530 5276 5316 5108 5968 5892

Growth rate 1053 -609 1796 385 -459 077 -391 1683 -127

Other (Licensing) 1056 814 139 06 27 mdash mdash mdash mdash mdash

Growth rate -2295 -8296 -9550 33189 mdash mdash mdash mdash mdash

Source Team Analysis NPD

19

Region FY 2016 FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

USCanada 348 215 145 138 091 134 100 -050 -100

EU 275 290 239 208 184 147 117 087 057

Asia Pacific 493 548 584 595 596 590 548 501 453

Latin America -398 334 366 397 394 391 386 381 374

EampL 500 500 500 500 500 500 500 500

Revenue Break 2016 2017 2018 2019 2020 2021 2022 2023 2024

US 51 5050 5000 4950 4900 4850 4800 4750 4700

EU 28 2740 2680 2620 2560 2500 2440 2380 2320

Asia Pacific 7 770 840 910 980 1050 1120 1190 1260

Latin America 9 940 980 1020 1060 1100 1140 1180 1220

EampL 5 500 500 500 500 500 500 500 500

Total 100 10000 10000 10000 10000 10000 10000 10000 10000

Weighted average 287 246 243 217 232 207 126 094

Traditional Toys Market Growth Rate

Revenue Breakdown FY 2016 FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

Revenue 5019822 537116 568183 617013 615860 657997 656823 675711 678776

Growth Rate 1287 700 578 859 -019 684 -018 288 045

Franchise Brands 2327668 255686 248016 262897 252381 265000 251750 261820 253965

Growth Rate 185 985 -300 600 -400 500 -500 400 -300

Partner Brands 141277 134015 140716 154787 147048 157341 155768 157325 162045

Growth Rate 2828 -514 500 1000 -500 700 -100 100 300

Hasbro Gaming 813433 97954 115585 133501 150856 166696 180031 189933 195631

Growth Rate 2282 2042 1800 1550 1300 1050 800 550 300

Emerging Brands 465951 49461 50203 51207 52488 54062 55954 58193 60811

Growth Rate 1693 615 150 200 250 300 350 400 450

Hasbros Major Market Growth Rate 287 246 243 217 232 207 126 094

Source Team Analysis Bloomberg

Source statisticscom

Source plasticsnewscom

Source FRED

APPENDIX 10 COGS ANALYSIS

Source Bloomberg

Source Bloomberg

Year 2018-2019 2020-2024

Freight -324 -100

Paper 011 010

Labor 867 -500

Plastics 300 000

Electronic Device -134 005

COGS Growth Rate 136 -032

We recognize the main factors in cost of goods sold include 2 major components freight and product costsAccording to our research we believe paper plastic labor and electronic devices are the four biggest materialsHasbrorsquos suppliers needs Plastics are the main materials which contribute 45 of cost Paper freight labor andelectronic devices contribute 30 10 5 10 respectively According to Hasbrorsquos supplier list most suppliers arebased in China Therefore the material price data we used were of Chinese market data