TAXPRO monthly - National Association of Tax … · · 2017-05-10Annual Semiannual Quarterly...

16

Issue 6 Volume 39 June 2017 “Other income” or miscellaneous deductions? By Cindy Van Beckum Legal Fees In 2008, Seattle Bank hired Ellen Sas as president and CEO. In July 2010, she received a bonus of $612,000, which she and her husband, Roger, reported as wage income on their 2010 Form 1040, U.S. Individual Income Tax Return. In September 2010, Seattle Bank terminated Ellen’s employment, and later filed a complaint against her alleging breach of fiduciary duty. The bank hoped to recover the $612,000 bonus. In January 2011, Ellen filed her answer and counterclaims, including a claim of employment discrimination. Both parties settled and agreed to pay nothing and release and dismiss all claims against each other. Ellen incurred $25,000 and $55,798 in legal expenses associated with this lawsuit in 2010 and 2011, respectively. During 2010 and 2011, the taxpayers maintained an accounting and consulting business. The couple filed a Schedule C, Profit or Loss From Business, with their 2010 Form 1040, reporting Roger as the sole proprietor. On their Forms 1040 for 2010 and 2011, the couple reported “other income” in the negative amounts of $25,000 and $55,798, respectively, for the legal fees paid for the lawsuit with Seattle Bank. The IRS filed a notice of deficiency disallowing these expenses as negative “other income” but allowed them as miscellaneous itemized deductions subject to the 2% AGI limitation in §67(a), thereby reducing the deductible amounts to $4,525 and $50,579 for 2010 and 2011, respectively. The taxpayers timely petitioned the Court for redetermination. The parties do not dispute the amounts of legal fees incurred or their deductibility; the only dispute is whether the legal fees are miscellaneous itemized –continued on page 13 How To Offer in Compromise: The mechanics to acceptance 4 Tax Talk In Vitro Fertilization: Deductions denied 12 Government News Private Debt Collection: IRS rolls out new program 2 monthly TAXPRO

Transcript of TAXPRO monthly - National Association of Tax … · · 2017-05-10Annual Semiannual Quarterly...

Issue 6Volume 39 June 2017

“Other income” or miscellaneous deductions? By Cindy Van Beckum

Legal Fees

In 2008, Seattle Bank hired Ellen Sas as president and CEO. In July 2010, she received a bonus of $612,000, which she and her husband, Roger, reported as wage income on their 2010 Form 1040, U.S. Individual Income Tax Return. In September 2010, Seattle Bank terminated Ellen’s employment, and later filed a complaint against her alleging breach of fiduciary duty. The bank hoped to recover the $612,000 bonus. In January 2011, Ellen filed her answer and counterclaims, including a claim of employment discrimination. Both parties settled and agreed to pay nothing and release and dismiss all claims against each other. Ellen incurred $25,000 and $55,798 in legal expenses associated with this lawsuit in 2010 and 2011, respectively. During 2010 and 2011, the taxpayers maintained an accounting and consulting business. The couple filed a Schedule C, Profit or Loss From Business, with their 2010 Form 1040, reporting Roger as the sole proprietor. On their Forms 1040 for 2010 and 2011, the couple reported “other income” in the negative amounts of $25,000 and $55,798, respectively, for the

legal fees paid for the lawsuit with Seattle Bank. The IRS filed a notice of deficiency disallowing these expenses as negative “other income” but allowed them as miscellaneous itemized deductions subject to the 2% AGI limitation in §67(a), thereby reducing the deductible amounts to $4,525 and $50,579 for 2010 and 2011, respectively. The taxpayers timely petitioned the Court for redetermination. The parties do not dispute the amounts of legal fees incurred or their deductibility; the only dispute is whether the legal fees are miscellaneous itemized

–continued on page 13

How To

Offer in Compromise:

The mechanics to acceptance

4 TaxTalk

In Vitro Fertilization:

Deductions denied

12Government News

Private Debt Collection:

IRS rolls out new program

2monthlyTAXPRO

Government News

Congress gave the IRS the authority under a federal law enacted in December 2015 (Fixing America’s Surface Transportation Act) to use private debt collectors. The new program, which began this year, enables these designated contractors to collect unpaid tax debts on the government’s behalf. In most cases, these are unpaid individual tax obligations that were assessed by the tax agency several years ago and are not currently being worked by IRS collection employees.

As expected, the public and some government officials raised concerns regarding the potential for fraud with the use of private debt collectors. National Taxpayer Advocate Nina Olson has already identified the use of private tax col-lection as one of the top problems for taxpayers. She plans to offer more detail on that opinion in her semiannual report to Congress in June. Olson believes “that the col-lection of federal tax debt is an inherently governmental function and should not be outsourced to

private agencies.” Rep. John Lewis, D-Ga., issued a statement April 4 saying that he will sponsor legisla-tion to repeal the program claiming “it exposes taxpayers to fraud.” The IRS has taken extraordinary steps to reduce the chances of fraud. The most important being that they will always notify a taxpayer before transferring his/her account to a private collection agency (PCA). First, the IRS will send letters to the taxpayer and their tax representative informing them that the taxpayer’s account is being assigned to a PCA and giving the name and contact information for the PCA. This mailing will include a copy of Publication 4518, What You Can Expect When the IRS Assigns Your Account to a Private Collection Agency. Only four private groups are participating in this program:• CBE Group of Cedar Falls,

Iowa; • Conserve of Fairport, N.Y.; • Performant of Livermore, Calif.;

and • Pioneer of Horseheads, N.Y.

The taxpayer’s account will only be assigned to one of these agencies, never to all four. No other private

Private Debt Collection

In April, the IRS started sending letters to a small group of taxpayers whose overdue federal tax accounts are being assigned to one of four private-sector collection agencies. The program will grow to thousands a week later in the spring and summer.

IRS rolls out new program By Cindy Hockenberry, EA

2 NATP TAXPRO Monthly / natptax.com

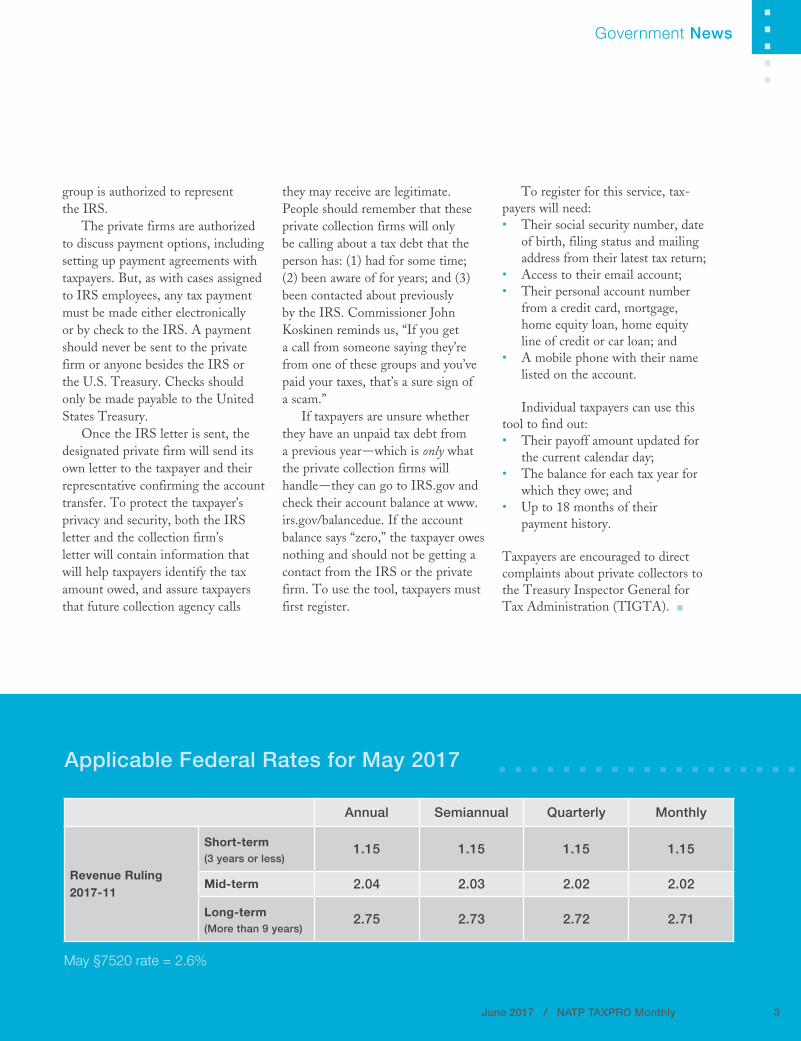

May §7520 rate = 2.6%

Applicable Federal Rates for May 2017

June 2017 / NATP TAXPRO Monthly 3

group is authorized to represent the IRS. The private firms are author ized to discuss payment options, including setting up payment agreements with taxpayers. But, as with cases assigned to IRS employees, any tax payment must be made either electronically or by check to the IRS. A payment should never be sent to the private firm or anyone besides the IRS or the U.S. Treasury. Checks should only be made payable to the United States Treasury. Once the IRS letter is sent, the designated private firm will send its own letter to the taxpayer and their representative confirming the account transfer. To protect the taxpayer’s privacy and security, both the IRS letter and the collection firm’s letter will contain information that will help taxpayers identify the tax amount owed, and assure taxpayers that future collection agency calls

they may receive are legitimate. People should remember that these private collection firms will only be calling about a tax debt that the person has: (1) had for some time; (2) been aware of for years; and (3) been contacted about previously by the IRS. Commissioner John Koskinen reminds us, “If you get a call from someone saying they’re from one of these groups and you’ve paid your taxes, that’s a sure sign of a scam.” If taxpayers are unsure whether they have an unpaid tax debt from a previous year—which is only what the private collection firms will handle—they can go to IRS.gov and check their account balance at www.irs.gov/balancedue. If the account balance says “zero,” the taxpayer owes nothing and should not be getting a contact from the IRS or the private firm. To use the tool, taxpayers must first register.

To register for this service, tax-payers will need:• Their social security number, date

of birth, filing status and mailing address from their latest tax return;

• Access to their email account;• Their personal account number

from a credit card, mortgage, home equity loan, home equity line of credit or car loan; and

• A mobile phone with their name listed on the account.

Individual taxpayers can use this tool to find out:• Their payoff amount updated for

the current calendar day; • The balance for each tax year for

which they owe; and • Up to 18 months of their

payment history.

Taxpayers are encouraged to direct complaints about private collectors to the Treasury Inspector General for Tax Administration (TIGTA). n

Government News

Annual Semiannual Quarterly Monthly

Revenue Ruling 2017-11

Short-term (3 years or less)

1.15 1.15 1.15 1.15

Mid-term 2.04 2.03 2.02 2.02

Long-term(More than 9 years)

2.75 2.73 2.72 2.71

Offer in Compromise

When a client has past tax liabilities and cannot pay, you may want to consider an Offer in Compromise. Practitioners who provide such a service must be aware of the mechanics that make an offer acceptable to the IRS.

The mechanics to acceptanceBy Stephanie Davis, EA

Rev. Proc. 2003-71 suggests the IRS will accept an Offer in Compromise based on two primary categories: Doubt as to Liability and Doubt as to Collectibility. Another option, Promotion of Effective Tax Administration, generally applies only when full collection is possible but would cause severe economic hardship to the taxpayer. Consider this option for clients who do not qualify for the other two categories; public policy or equity consideration allows acceptance for less than the liability. Doubt as to Liability is exactly what it sounds like—the liability may not belong to the taxpayer or the taxpayer should not be responsible for the outstanding tax balance. The IRS is more likely to accept this offer if the taxpayer provides a valid explanation as to why he or she is not liable. The IRS considers whether the pursuit of this liability, if not the taxpayer’s, warrants further collection or if the offer prepared is reasonable and, by accepting this offer, all parties are satisfied. Even if the taxpayer disagrees with the tax liability, he or she must make a payment with the offer. Doubt as to Collectibility addresses the taxpayer’s current and future financial situation. If

the taxpayer operates a business, has ownership interest in an S corporation, C corporation, partnership or real estate rental activities, the IRS views this as future income. In other words, the taxpayer has the means to pay an outstanding balance. Generally, the IRS looks at the current economic situation and projects a steady revenue stream to that taxpayer. In such cases, an installment agreement—not an offer—is the proper collection method. Clients with W-2 employment, social security retirement income or any other limited income source might have better results. Before beginning the actual paperwork required to present an offer, you should thoroughly interview the client. (Tip: An IRS Pre-Qualifier questionnaire is available on irs.gov.) Any error or inconsistency will result in a rejected offer. During this initial interview, be prepared to ask tough questions. It’s our job to help the client present an offer that is acceptable and beneficial to both parties. Ask questions that may provide a clue as to whether the taxpayer is capable of paying more. This should ensure the offer is not rejected after being reviewed by the IRS agent assigned to the case.

Begin the process by collecting information supportive of the taxpayer’s financial situation. Use the checklist provided on the IRS website in Form 656 Booklet, Offer in Compromise. Once you have collected and reviewed all the information, begin completing the application. It’s important to involve the taxpayer in this process because the information cannot be estimated. Supporting documentation is required for all entries on this form. A realistic solution to the taxpayer’s situation may involve a more in-depth conversation about his or her per-sonal history and future financial plans. Some preparers may be apprehensive with this approach, but in order to best serve the client, these sensitive questions must be asked. Seek answers to the following:• Does the taxpayer have any

assets of value that could be sold? • How does the taxpayer plan

to pay the offer amount and continue with the payment plan?

• What sources is the client using to make the initial 20% payment with the offer?

• Is there any reason the taxpayer may be eligible for a reduced offer based on future financial circumstances?

How To

4 NATP TAXPRO Monthly / natptax.com

June 2017 / NATP TAXPRO Monthly 5

• Is the client expecting any type of settlement or inheritance?

• What are the current living expenses and how could these be decreased?

• Does the taxpayer enjoy eating out?

Some of these questions might sounds trivial, but full disclosure of bank statements doesn’t always paint an accurate picture. Look for details that make up the big picture. Obtaining assets during time of wealth without meeting tax obligations will come back to haunt the taxpayer during the Offer in Compromise process. An IRS agent assigned to the case will see these charges on the submitted bank statements. Frivolous expenses are considered unacceptable when there is a tax liability. Review these items with the client prior to submitting the offer. Proof that the taxpayer is not living lavishly while avoiding his or her tax responsibility will have a favorable impact on the agent.

ExampleJane J. Taxpayer’s application for an Offer in Compromise reflects a reasonable offer based on the collected information. Jane opened

her own business in 2010 without seeking professional advice. She operated a small lawn care business that employed two other individuals. Jane hired a bookkeeper to handle the payroll, but was unaware of the tax ramifications associated with being self-employed. She was also not very knowledgeable about payroll tax liabilities. Over the next year and into 2011, some payroll reports and a few deposits were submitted on behalf of the business. Self-employment taxes and payroll liabilities totaled approxi-mately $60,000, including penalties and interest. Jane is a single mother, but does receive child support and alimony. When the IRS notices started to arrive, she closed her busi-ness in 2011 at the end of the season and began working as a bank teller. The notices were for payroll reports not filed, penalties and tax due. After careful review and a thorough conversation with Jane, her tax professional prepared an Offer in Compromise. Jane owns a personal residence that carries a mortgage, and a vehicle financed at a high interest rate. Her monthly income supports her and her son. Approximately $300 remains after paying living expenses. Jane will use a family loan to make the 20% initial

payment submitted with the offer and the $186 filing fee due when the form is mailed to the applicable IRS Service Center. (See pages 6–11 for Jane’s Form 433-A and Form 656.)

ConclusionOnce the offer has been submitted, the waiting game begins. Rarely is an offer accepted without a request for more information by the assigned agent. This part of the process should not be viewed as an indication the offer will be rejected. The agent will review the items listed on the offer for any errors that may favor the IRS (e.g., living expenses not considered exempt or considered excessive). Be prepared to work with the agent. Together, you’ll find a solution that benefits both parties. Important Notice: Beginning with Offer in Compromise applica-tions received on or after March 27, 2017, the IRS will return any newly filed OIC application if the taxpayer has not filed all required tax returns. Any application fee included with the OIC will also be returned. Any initial payment required with the returned application will be applied to reduce the taxpayer’s balance due. This policy does not apply to current year tax returns if there is a valid extension on file. n

How To

How To (continued from page 5)

6 NATP TAXPRO Monthly / natptax.com

June 2017 / NATP TAXPRO Monthly 7

How To (continued from page 7)

8 NATP TAXPRO Monthly / natptax.com

June 2017 / NATP TAXPRO Monthly 9

How To (continued from page 9)

10 NATP TAXPRO Monthly / natptax.com

June 2017 / NATP TAXPRO Monthly 11

12 NATP TAXPRO Monthly / natptax.com

Tax Talk

In vitro fertilization (IVF), involving the use of an egg donor and a gestational surrogate, is generally used when the hopeful parents cannot conceive on their own. Modern medicine has come far to allow people to do this. A similarity between a traditional birth and an IVF is that a child is born into a family who must bear the medical expenses. The same cannot be said for medical deductions for a gestational surrogate under §213. Joseph Morrissey paid over $50,000 in medical expenses, legal fees and consultation fees for an IVF. While Joseph wasn’t necessarily infertile himself, he could not conceive a child with his partner, another male. The child did not come to term; however, this was not litigated in this case. Joseph filed an amended tax return for 2011 in December 2012 to claim the medical expenses for the IVF, which the IRS rejected. Joseph filed suit against the IRS while carefully choosing his argument since IVF expenses have been denied before (see William Magdalin v. Commissioner, TC Memo 2008-293). In the Magdalin case, the taxpayer argued that there should be freedom in choosing a method of reproduction, which they lost on the grounds that IVF, when done using a gestational surrogate, does not impact the taxpayer, the taxpayer’s spouse or the body of the taxpayer’s dependent. Joseph instead argued that because he is homosexual, he is rendered practically infertile, so the expenses cure his own infertility. The Court was

not persuaded. Both the IRS and the Court referred to the plain language of the code. The code defines medical care as amounts paid “for the diagnosis, cure, mitigation, treatment, or prevention of disease, or for the purpose of affecting any structure or function of the body….for the expenses paid during the taxable year, not compensated for by insurance or otherwise, for medical care of the taxpayer, his spouse or a dependent.” The expenses paid did not mitigate, cure, diagnose, prevent a disease or treat a part of Joseph’s body. Joseph then argued that the IRS discriminated against him in the application of §213 because of his sexual orientation. The IRS properly pointed out that they have consistently applied this statute to heterosexual couples as well, where an infertile wife was unable to conceive, incurred expenses for an IVF procedure and were denied the deduction because it did not impact the taxpayer’s body. The refund denial was based purely on the interpretation of §213 itself. Couples who are considering IVF using a gesta-tional surrogate will surely be faced with expensive fees and medical bills. A taxpayer who has spent over $50,000 on a procedure would probably describe the inability to deduct the expenses as “salt on an open wound.” Nonetheless, the IRS takes the position that expenses for an IVF done in this manner are nondeductible when carried by a third party (INFO 2002-0291). Additionally, the IRS has a winning track record in court on IVF fees. If you have clients who passionately believe that IVF expenses incurred while using a gestational surrogate should be a deductible expense, warn them of the substantial authority stacked against their position. Lastly, as a tax preparer, you may not sign a tax return that contains an unreasonable position, which is a position without substantial authority supporting such position. Even a disclosed position on Form 8275 is unreasonable if the position is merely arguable. Consider abstaining from signing a tax return that contains an unreasonable position. n

Morrissey v. U.S.119 AFTR 2d 2017-401

Deductions for In Vitro Fertilization Denied

Sexual orientation is irrelevantBy Genaro Cardaropoli, CPA

June 2017 / NATP TAXPRO Monthly 13

deductions subject to the 2% AGI limitation under §67(a). The taxpayers offer two reasons for deducting the legal fees without limitation. First, they claim that the legal fees are deductible as an adjustment to gross income under §62(a)(20) as legal fees paid in connection with an action involving a claim of unlawful discrimination. Alternatively, they argue that the legal fees are deductible under §§62(a)(1) and 162 as ordinary and necessary business expenses. Generally, when a litigant’s recovery constitutes tax-able income, that income includes the portion of the recovery paid to the litigant’s attorney. Section 62(a)(20) allows a deduction for the litigant’s legal fees and court costs in connection with any action involving a claim of unlawful discrimination as defined under §62(e). In addition to requiring a claim for unlawful dis-crimination, §62(a)(20) provides that the section “shall not apply to any deduction in excess of the amount includible in the taxpayer’s gross income for the taxable year on account of a judgment or settlement … result-ing from such claim.” The couple attempts to fit their claimed deductions within this limitation by arguing that Ellen included the bonus as income when it was received and was able to retain the bonus because of her counterclaims. Therefore, they reason, Ellen’s bonus was included in the couple’s gross income on account of a judgment or settlement relating to her action. Contrary to this viewpoint, the “amount includible in the taxpayer’s gross income” cannot reasonably be interpreted to include prevention of potential loss of income that would be includible in the absence of any claim. Ellen’s bonus was received and includible in the couple’s gross income because of her employment with Seattle Bank. Under the settlement agreement, neither party received any amount includible in gross income. Assuming that Ellen’s counterclaims were in connection with unlawful discrimination, she did not receive, and did not include in gross income for 2010 or 2011, any amount because of the settlement of her claims. Because the entire amount of Ellen’s legal fees was “in excess of the amount includible in … [their] gross income for the taxable year on account of” the settlement, the taxpayers may not deduct any of the legal fees as an adjustment to gross income under §62(a)(20). Next, the couple argues that the legal fees are deductible as ordinary and necessary business expenses under §162. Expenses are deductible under §162 if the taxpayer establishes that they were ordinary, necessary

and paid or incurred during the tax year and were directly connected with, or proximately resulted from, a trade or business of the taxpayer. The deductibility of legal fees under §162 depends on the origin and character of the claim for which the legal fees were incurred and whether that claim bears a sufficient nexus to the taxpayer’s business or income-producing activities. The taxpayers do not argue that Ellen’s claim was rooted in their accounting business; rather, they argue that the lawsuit would have an adverse effect on Ellen’s professional reputation, which in turn could damage the reputation of their accounting business. Therefore, the couple contends that the legal fees were necessary expenses of their business. While the taxpayers may have been right that returning her bonus could harm her professional reputation and in turn the couple’s accounting business, the Court must look to the origin of the claim, not the potential consequences of a win or loss. The Court found that Ellen’s claims arose from her status as a former employee of Seattle Bank, not from the couple’s accounting business, and the taxpayers hired an attorney because Seattle Bank was attempting to recover a bonus Ellen received in connection with her employment at Seattle Bank. Therefore, the couple is not permitted to deduct the legal fees as ordinary and necessary expenses of their accounting business under §162. Because the Court sustained the IRS’s determina-tion that the taxpayer’s must deduct the legal fees as miscellaneous itemized deductions subject to the 2% limitation in §67(a) rather than under either §62(a)(20) or §162, the Court also sustained the increase to the taxpayer’s alternative minimum tax of $12,888 for tax year 2011, which is a computational adjustment. n

Ellen M. Sas and Roger A. Jones v. CommissionerTC Summary Opinion 2017-2

Tax Talk

Legal Fees (continued from page 1)

EA Exam Review Online Workshops

Part I - May 10Part II - May 24

Part III - June 15Workshops come with:

• E-book.

• Study guides.

• Study questions with reasoning for correct/incorrect answers.

• Electronic flashcards.

• Practice exam, styled to prepare you for the real thing.

Spend the day with our experienced instructor in a classroom setting! Review the areas of the EA exam that tax professionals struggle with most

and receive insight on passing the test the first time.

Prepare the right way

Start studying! Register today at natptax.com or call 800.558.3402

(001-839) (ISSN 1535-5896) is published monthly by NATP

National Association of Tax Professionals3517 N. McCarthy Road

Appleton, WI 54913

Periodicals postage paid at Appleton, WIand additional mailing office.

Editor: Cindy Van BeckumManaging Editor: Cindy Hockenberry, EA

Contributing Writers:Genaro Cardaropoli, CPA

Stephanie Davis, EACindy Hockenberry, EA

Cindy Van Beckum

Postmaster: Send address changes to:TAXPRO Monthly c/o NATP

3517 N. McCarthy RoadAppleton, WI 54913

Change of address?Please contact NATP at:

800.558.3402 ext. [email protected]

natptax.com

Views expressed in TAXPRO Monthly are not necessarily endorsed by the National Association of Tax Professionals.© Copyright 2017

National Association of Tax Professionals, Inc.All rights reserved.

monthlyTAXPRO

Q and A

June 2017 / NATP TAXPRO Monthly 15

A cash basis sole proprietor sold his business assets and discontinued his business operations. In a later year, he paid some expenses for supplies he used in his business and he paid off the business loan he had with the bank. Is there any place he can deduct the expenses for the supplies he used and the business interest he paid on this later year tax return?

Yes. The expenses he paid for his business are deductible on his Schedule C in the year paid. Even though he is no longer in business, the expenses qualify as business expenses and are deductible on the same form they would have been had he not discontinued his business operations (Rev. Rul. 67-12).

Q

A

About NATPNATP is the largest association dedicated to equipping tax professionals with the resources, connections and education they need to provide the highest level of service to their clients. NATP is comprised of over 23,000 leading tax professionals who believe in a superior standard of ethics and exemplify professional excellence. Members rely on NATP to deliver professional connections, content expertise and advocacy that provides them with the support they need to best serve their clients. The organization welcomes all tax professionals in their quest to continually meet the needs of the public, no matter where they are in their careers.

EA Exam Review Online Workshops

Part I - May 10Part II - May 24

Part III - June 15Workshops come with:

• E-book.

• Study guides.

• Study questions with reasoning for correct/incorrect answers.

• Electronic flashcards.

• Practice exam, styled to prepare you for the real thing.

Spend the day with our experienced instructor in a classroom setting! Review the areas of the EA exam that tax professionals struggle with most

and receive insight on passing the test the first time.

Prepare the right way

Start studying! Register today at natptax.com or call 800.558.3402

natptax.com/taxstore | 800.558.3402, ext. 3

Small Business and Individual (printed or downloadable) editions available.

Starts shipping in June.

TAX STORE

Pre-Order Your

Summer Tax Tips Client Newsletters!