Taxation Issues Related to Debt Restructuring ... · PDF fileTaxation Issues Related to Debt...

43

November 21, 2011 Taxation Issues Related to Debt Restructuring, Modifications, and Bankruptcies Steven D. Bortnick, Esq. [email protected] Michelle M. Moersfelder, Esq. [email protected] #15005995v.3

-

Upload

truongdang -

Category

Documents

-

view

216 -

download

0

Transcript of Taxation Issues Related to Debt Restructuring ... · PDF fileTaxation Issues Related to Debt...

1

November 21, 2011

Taxation Issues Related to Debt Restructuring, Modifications, and Bankruptcies Steven D. Bortnick, Esq. [email protected] Michelle M. Moersfelder, Esq. [email protected]

#15005995v.3

2

Agenda

• Debt Restructurings • Cancellation of Indebtedness Income • Investing in Distressed Debt • Section 382 and Bankruptcy

3

Debt Restructurings

• Repurchase or settlement of debt by issuer for cash or other property (including stock)

• Actual exchange of old debt for new debt with significantly modified terms

• Significant modification of old debt (deemed exchange)

• Purchase of old debt by “related party” of issuer (deemed exchange) − “Related party” – described in §267(b) or 707(b)(1);

attribution rules apply

4

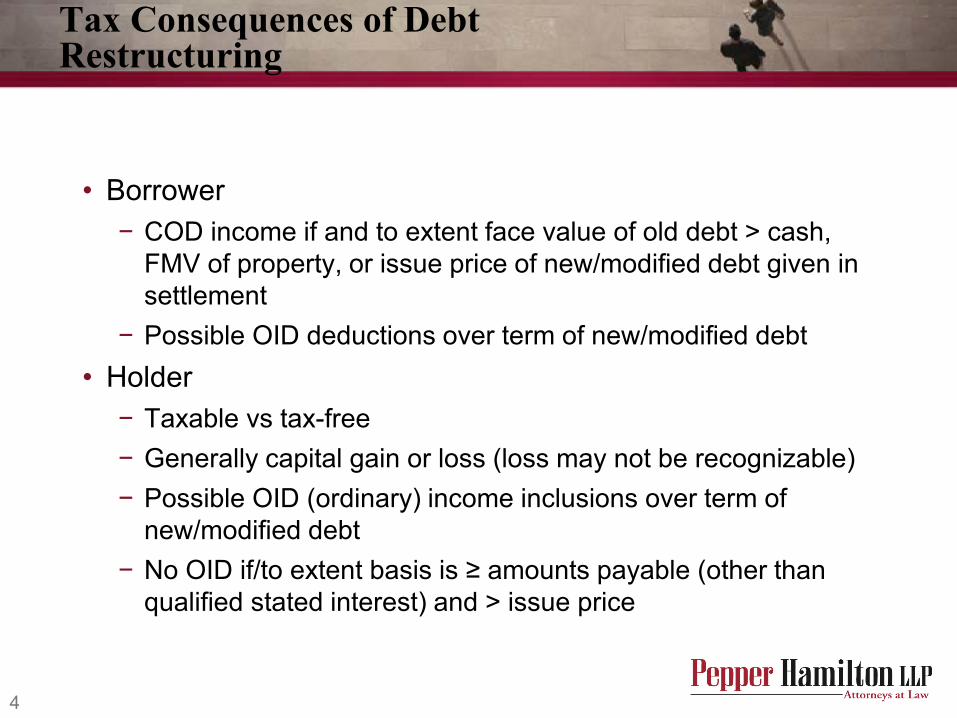

Tax Consequences of Debt Restructuring

• Borrower − COD income if and to extent face value of old debt > cash,

FMV of property, or issue price of new/modified debt given in settlement

− Possible OID deductions over term of new/modified debt • Holder

− Taxable vs tax-free − Generally capital gain or loss (loss may not be recognizable) − Possible OID (ordinary) income inclusions over term of

new/modified debt − No OID if/to extent basis is ≥ amounts payable (other than

qualified stated interest) and > issue price

5

Repurchase of Debt at Discount for Cash

• CODI • How to measure

− Debt issued with OID − Debt issued without OID

• Character of income • Traditional exceptions to recognition of CODI

− Bankruptcy − Insolvency − Contribution to capital − No more debt for equity exclusion (including equity of

partnerships) • Deferral Election (discussed below)

6

Cancellation of Debt Income – Tax Treatment to Debtor

• Immediately taxable to debtor if no exclusion applies; Debtor may (mostly) offset with available NOLs

• Exclusion for bankruptcy, insolvency, or non-corporate qualified real property indebtedness: reduce tax attributes (NOLs, asset basis - subject to “liability stop”) by amount of COD (§ 108(a), (b))

• Elect to defer COD income under American Recovery and Reinvestment Tax Act of 2009 (Pub. L. No. 111-5) (“ARRTA”) (Principal IRC provisions: §§ 108(i); 163(e)(5)(F))

7

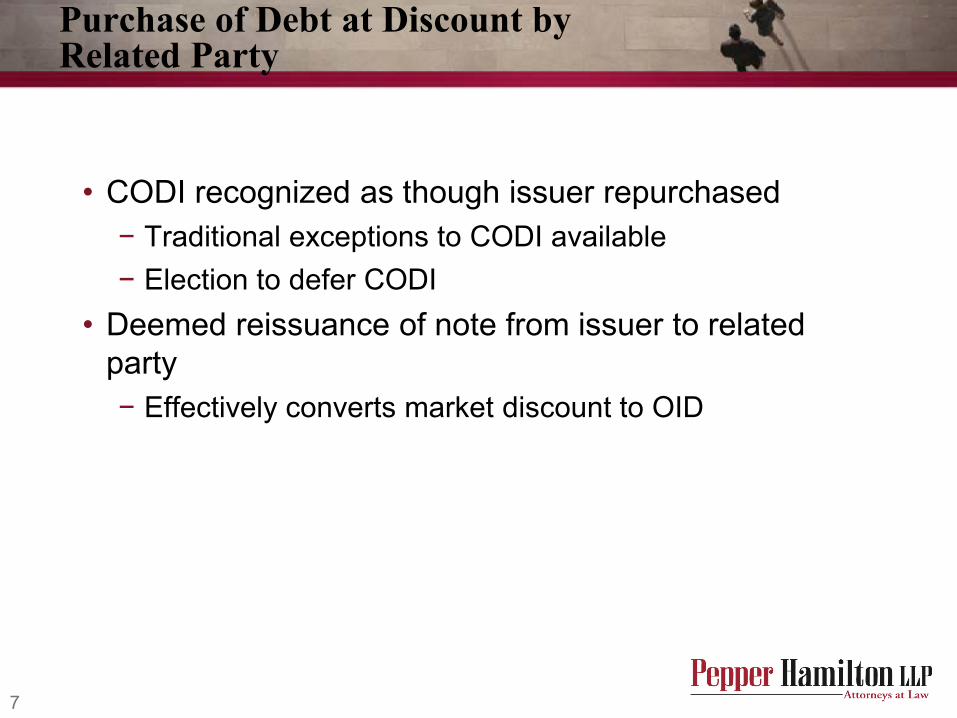

Purchase of Debt at Discount by Related Party

• CODI recognized as though issuer repurchased − Traditional exceptions to CODI available − Election to defer CODI

• Deemed reissuance of note from issuer to related party − Effectively converts market discount to OID

8

OID vs Market Discount

• Original Issue Discount − Accrues daily − Constant yield basis − Taken into income currently − Generally deductible by issuer (subject to AHYDO and certain

related party timing rules) • Market Discount

− Accrued market discount generally treated as interest income − Accrues daily − Ratable basis unless elect constant yield − Only taken into income on payment or sale − Not deductible by issuer

9

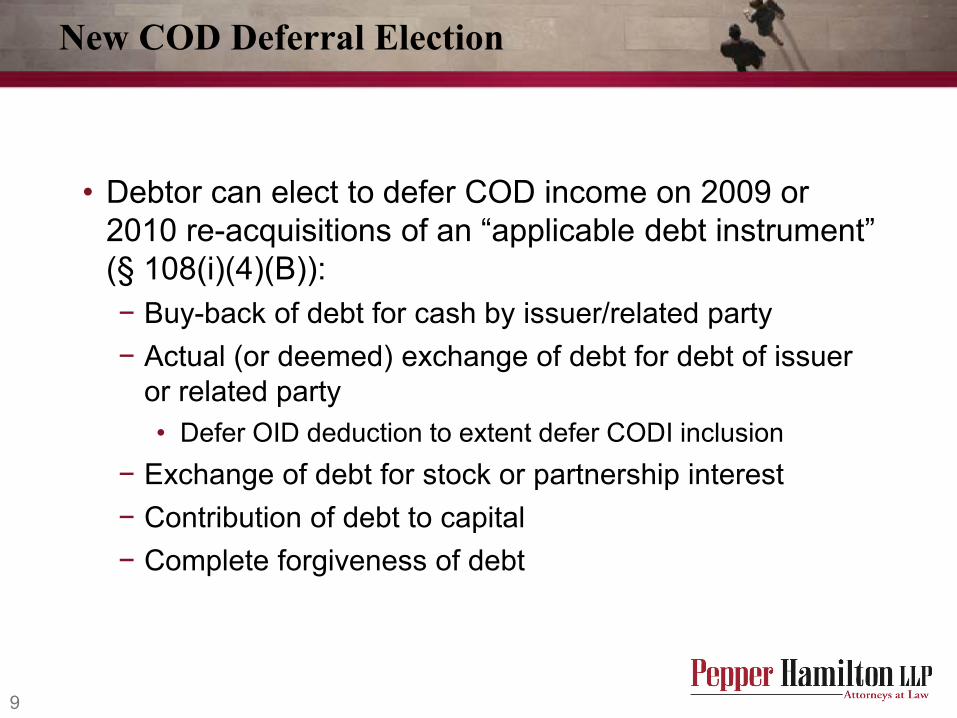

New COD Deferral Election

• Debtor can elect to defer COD income on 2009 or 2010 re-acquisitions of an “applicable debt instrument” (§ 108(i)(4)(B)): − Buy-back of debt for cash by issuer/related party − Actual (or deemed) exchange of debt for debt of issuer

or related party • Defer OID deduction to extent defer CODI inclusion

− Exchange of debt for stock or partnership interest − Contribution of debt to capital − Complete forgiveness of debt

10

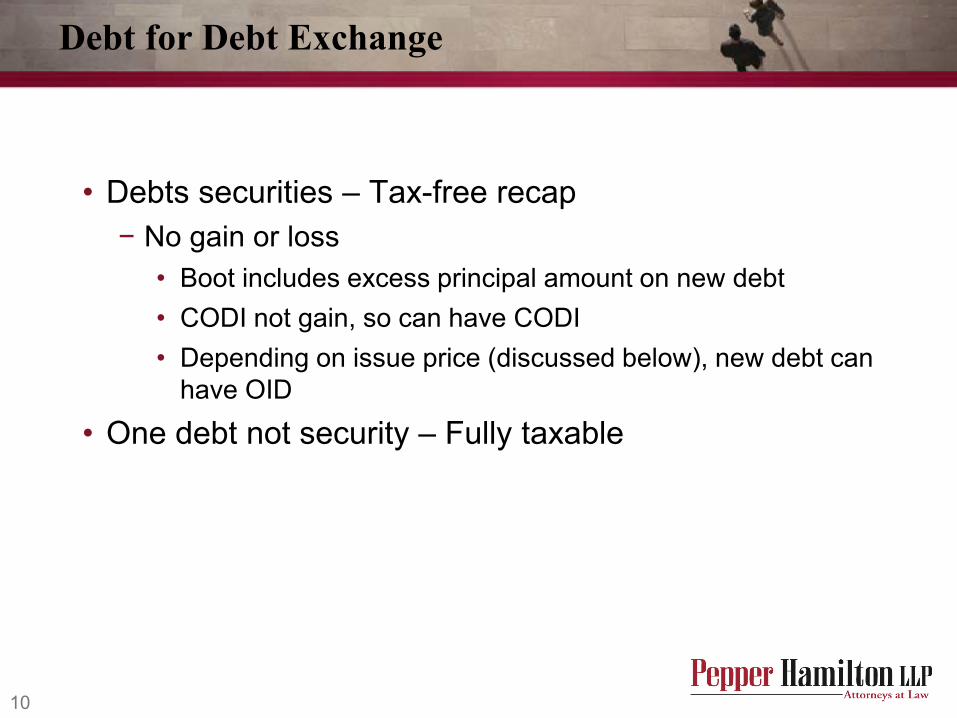

Debt for Debt Exchange

• Debts securities – Tax-free recap − No gain or loss

• Boot includes excess principal amount on new debt • CODI not gain, so can have CODI • Depending on issue price (discussed below), new debt can

have OID

• One debt not security – Fully taxable

11

Taxable Debt for Debt Exchange

• CODI − Issue price of new debt < adjusted issue price of old

debt • Holder may recognize gain or loss • Amount realized deemed equal to issue price of new

debt

12

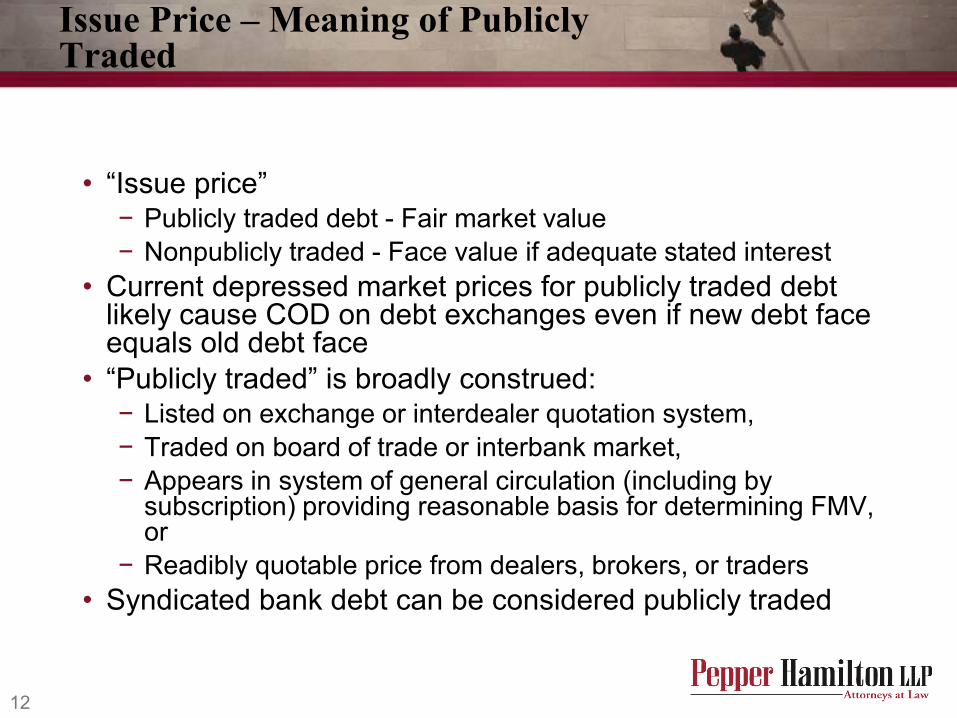

Issue Price – Meaning of Publicly Traded

• “Issue price” − Publicly traded debt - Fair market value − Nonpublicly traded - Face value if adequate stated interest

• Current depressed market prices for publicly traded debt likely cause COD on debt exchanges even if new debt face equals old debt face

• “Publicly traded” is broadly construed: − Listed on exchange or interdealer quotation system, − Traded on board of trade or interbank market, − Appears in system of general circulation (including by

subscription) providing reasonable basis for determining FMV, or

− Readibly quotable price from dealers, brokers, or traders • Syndicated bank debt can be considered publicly traded

13

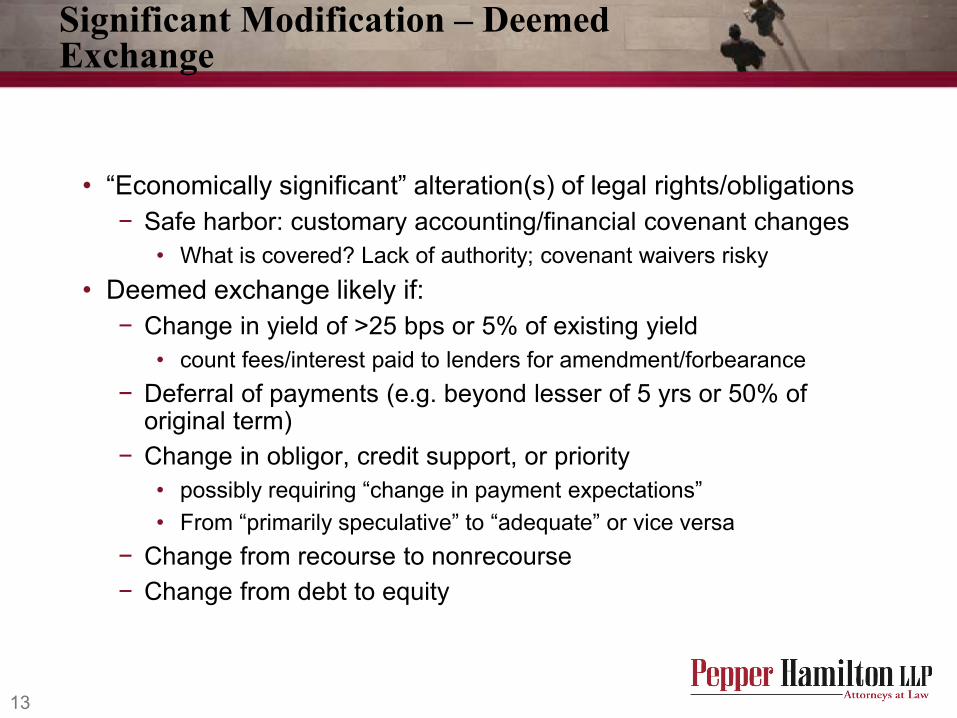

Significant Modification – Deemed Exchange

• “Economically significant” alteration(s) of legal rights/obligations − Safe harbor: customary accounting/financial covenant changes

• What is covered? Lack of authority; covenant waivers risky • Deemed exchange likely if:

− Change in yield of >25 bps or 5% of existing yield • count fees/interest paid to lenders for amendment/forbearance

− Deferral of payments (e.g. beyond lesser of 5 yrs or 50% of original term)

− Change in obligor, credit support, or priority • possibly requiring “change in payment expectations” • From “primarily speculative” to “adequate” or vice versa

− Change from recourse to nonrecourse − Change from debt to equity

14

Equity Treatment

• Modification resulting in “non-debt” is “significant” • Mere deterioration in ability to pay not taken into

account in determining if modification results in “non-debt,” unless change in obligors in connection with modification.

• Section 382 effect

15

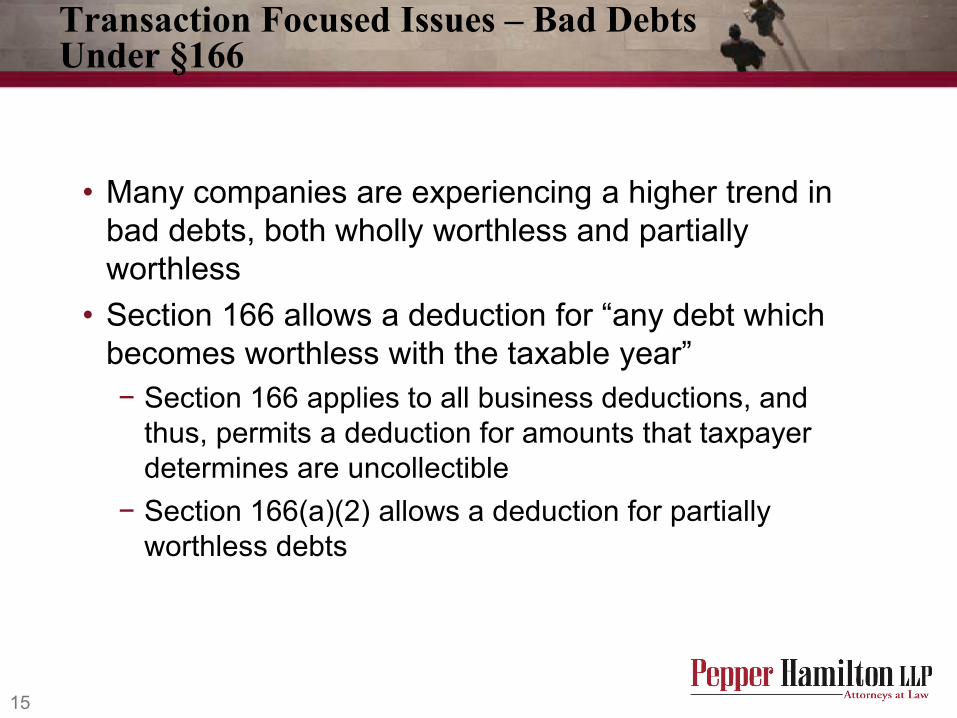

Transaction Focused Issues – Bad Debts Under §166

• Many companies are experiencing a higher trend in bad debts, both wholly worthless and partially worthless

• Section 166 allows a deduction for “any debt which becomes worthless with the taxable year” − Section 166 applies to all business deductions, and

thus, permits a deduction for amounts that taxpayer determines are uncollectible

− Section 166(a)(2) allows a deduction for partially worthless debts

16

Transaction Focused Issues – Bad Debts Under §166

• Taxpayer is responsible for demonstrating worthlessness − TP must show that debt had value at the beginning of the tax

year and no value at the end of the year − Deduction is warranted if surrounding circumstances indicate

legal action would not result in satisfaction − Determination of partial or total worthlessness is a factual inquiry

• Factors indicating worthlessness may include: − Value of the collateral as compared to outstanding obligation − Financial condition of the Debtor − Debtor bankruptcy generally indicates worthlessness − Insolvency of Debtor, without more, is insufficient to determine

worthlessness • Determining tax year when debt becomes worthless may also be

challenging

17

Transaction Focused Issues – Bad Debts Under §166

• Section 166 bad debt rules don’t apply to securities • REMIC investments are treated as debt under Section

860B • Impairment may lead to bad debt deduction

18

Transaction Focused Issues – Bad Debts Under §166

• Section 166(a)(2) allows a deduction for partially worthless debts − TP must satisfy the charge-off requirement for a partial

worthlessness deduction; and − TP must demonstrate that the loan or receivable is actually

worthless to the extent of the deduction • Taxpayer may wait for debt to become wholly worthless and not

required to treat debt as partially worthlessness − If business debt is recoverable only in part, a deduction is

available to the extent it is written off on the taxpayer's books within the year

− But, a creditor is not required to take a partial bad debt deduction even though it becomes certain within the year that the debt is partially worthless

− He may instead wait until the debt becomes wholly worthless and deduct the full amount of the debt at that time

19

Transaction Focused Issues – Bad Debts Under §166

• IRS guidance does not define “charge off” • Taxpayer must take action to remove the worthless portion

of an asset from its books as an indication of worthlessness

• Courts have held that a reserve or a contra-account that is credited with regard to a specific debt constitutes a charge-off under Section 166(a)(2), even if the debt is not removed from the taxpayer’s books

• Automatic change in method of accounting under Rev. Proc. 2008-52 − Change from a reserve method (or other improper method) to

a specific charge-off method that complies with section 166 − Applies to a taxpayer other than a bank

20

Transaction Focused Issues – Losses Under §165

• Section 165(a) allows a deduction for any loss sustained during the taxable year which is not compensated for by insurance or otherwise

• Additionally, Section 165(g) allows a deduction in the year that a security becomes worthless − Losses are treated as losses from a sale or exchange of the

underlying security − Capital loss treatment provided − Section 165(g)(3) provides ordinary loss treatment if worthless

securities were issued by an affiliated corporation • With the increase in loss transactions under section 165,

additional consideration of the reportable transactions under section 6011 and the regulations is required

21

Transaction Focused Issues – Losses Under §165

• Section 165(g)(3) provides ordinary loss treatment for certain worthless securities issued by an affiliated corporation

• Affiliation test: − TP owns directly stock in such corporation meeting the

requirements of section 1504(a)(2) and − More than 90% of the aggregate of its gross receipts for all

taxable years has been from sources other than investments (e.g., royalties, rents, dividends, interest, annuities, and gains from sales or exchanges of stocks and securities)

• Allows ordinary treatment for companies that are not consolidated and have losses attributable to operations and not investment activity

22

Transaction Focused Issues – Losses Under §165

• Potential relief from recent guidance − PLR 200710004 – Dividends paid by an operating

company to a holding company constitute passive dividend income to the holding company under Section 165(g)(3)(B)

− TAM 200914021 – Exception applies to subsidiary that never had gross receipts

23

Transaction Focused Issues – Losses Under §165

• Section 165(g)(3) allows ordinary treatment for companies that cannot access operating losses of affiliate due to lack of consolidation, e.g., foreign/US relationship, C Corp/partnership, insurance – life and non-life entities

• Section 165(g)(3) treatment should be carefully considered for ancillary tax issues − Detailed basis determination is required to support loss − Possible Section 382 limitation may prevent access to operating

losses • Commentators have requested guidance similar to Rev. Rul. 88-

65, which allows ordinary treatment for a business with significant investment activity − Argument is that losses should be ordinary because insurance

business is an active trade or business − Similar issues will be present in other industries with investment

component in operations (e.g., financial institutions)

24

Transaction Focused Issues – Losses Under §165

• A “loss transaction” is a reportable transaction • A transaction is a “loss transaction” if a taxpayer

claims a loss under Section 165 − Corporation: $10M/one year $20M/two+ years − S Corps/Trusts: $2M/one year $4M/two+ years

25

Transaction Focused Issues – Losses Under §165

• Exceptions to the Section 165 reportable transaction filter are in Rev. Proc. 2004-66

• Exclusions: − Arises from casualty/theft, etc. − Recognized under move-to market rules (475(a)/1256(a)) − Recognized in a hedging transaction − Arises from abandonment of tangible T/B property − Cash payment by TP (e.g., cash payment by guarantor) − Loss from bulk sale of inventory − Loss from sale to someone other than a related party

• Treas. Reg. Section 1.6011-4(e)(1) states, “If a reportable transaction results in a loss which is carried back to a prior year, the disclosure statement for the reportable transaction must be attached to the taxpayer’s application for tentative refund or amended tax return for that prior year.”

26

Section 382 Basics

• Limits a “loss corporation” • That undergoes an “ownership change”

− An ownership change occurs if immediately after an owner shift or an equity structure shift - The percentage by value of stock of the loss corporation owned by one or more 5-percent shareholders has increased by more than 50 percentage points over the lowest percentage ownership of such shareholders

• During a 3-year “testing period” • From utilizing “pre-change losses” or other tax

attributes • Against “post-change” income

27

Section 382

• Loss Corporation − NOL, tax credit, capital loss, or other attribute

carryforward − Net Unrealized Built-In Loss (“NUBIL”)

• Testing period − Begins on the first day of the tax year when carryforward

begins − 3-year “rolling” period unless change occurs

28

Equity Under 382

What generally counts as “equity” when determining a Section 382 ownership change?

− Common voting stock − Convertible preferred stock − Voting preferred stock

29

NOL Poison Pills

Protect your NOLs with a NOL poison pill plan − Shareholder rights plans deter new 5% shareholders − Can prohibit existing shareholders from buying more

without board approval − Board can waive − Watch out – Selectica, Inc. v. Versata Enterprises, Inc.,

No. 4241-VCN (Del. Ch. January 3, 2009)

30

Section 382 Limitation Value

• Does not include any new investment being made on the change date

• Value of pure preferred (1504(a)(4) stock) is included in the limitation calculation − Even though not tracked for equity shifts

• Market capitalization of a public company may be the starting point − Does a control premium matter? See TAM 200513027

31

Adjustments to Value

• Holding “substantial nonbusiness assets” (1/3 of total asset value) immediately after the ownership change

• May be required to back out value of capital contributions made within 2 years of ownership change if they are pursuant to a plan

• Annual limitation may become zero if continuity of business enterprise is violated within 2 years of change − A loss group is treated as a single entity for this test

• Need at least one member loss group member to continue business

• Corporate contractions − PLR 200406027 no corporate contraction where target

guaranteed debt

32

Calculation of the Section 382 Limitation

Section 382 Limitation Example: • Value immediately before change $1,820 • Capital Contributions pursuant to a plan ($200) • Adjusted value $1,620 • Published rate (L.T. tax exempt) 5.00% • Annual NOL Limitation $81 • Annual limitation accrues, even if unused

33

Successive Ownership Changes

• If two or more successive ownership changes, then each Section 382 limitation is applied independently (Reg. Section 1.382-5(d)) − Later ownership changes may result in a lower, but not

a higher, Section 382 limitation − Application of rule may result in layers of NOLs where

each layer is subject to different limitations − A single low limitation can trap prior NOLs, and

subsequent limitations can not create a higher limitation for previously limited NOLs

34

Section 382 in Bankruptcy

Special Rules • Assuming that loss corporation has NOLs and other

attributes that survive attribute reduction under Section 108(b), Section 382 will likely apply to the utilization of losses post bankruptcy − Consider the impact of an election under Section 108(b)(5)

• 382(l)(5) - generally provides for no limitation on use of NOLs if certain requirements are met

• 382(l)(6) – generally provides for increased limitation if certain requirements are met − (l)(6) is applicable if requirements for (1)(5) are not met or if

debtor elects out of (l)(5)

35

Section 382 in Bankruptcy

382(l)(5) • In title 11 immediately before the change • Continuity of interest (tests pre-change shareholders and

“qualified creditors”) − Post bankruptcy former creditors or historic shareholders must

hold greater than 50% of the vote and value • Special option rules for determining ownership that may have

retroactive effect • Example: options or warrants exercised by creditors and

historic shareholders within three years of emergence from bankruptcy could allow a loss corporation to qualify for Section 382(l)(5) benefits back to the emergence from bankruptcy

36

Section 382 in Bankruptcy

382(l)(5) Effects and Consequences • The use of pre-change losses is not subject to limitation under

Section 382 • If another ownership change occurs within 2 years, the Section

382 limitation with respect to the second ownership change will be zero

• Interest haircut: − NOLs & excess credits are reduced by:

• Interest on the debt converted into equity in the bankruptcy proceeding (interest haircut) that was paid or accrued in:

• Any taxable year ending during the three-year period preceding the taxable year in which the ownership change occurs, and

• The period of the taxable year in which the ownership change occurs on or before the change date

• CCA 200915033 – (l)(5) not available for “pre-packaged bankruptcy”

37

Section 382 in Bankruptcy

Example: • A loss corporation enters bankruptcy with $500M in

NOL • $300M of debt is cancelled and the creditors receive

$100M worth of equity • $50M of interest was incurred on the converted debt

during the look back period • $200M of COD is excluded, none of which relates to

accrued interest on the converted debt • The NOLs are reduced to $250M ($500-$200-$50)

38

Section 382 in Bankruptcy

382(l)(6) • Certain tax-free reorganizations; or • Title 11 case; and • 382(l)(5) doesn’t apply • Must continue the business for 2 years following the

change date or the 382 limitation is 0

39

Section 382 in Bankruptcy

382(l)(6) Effects • 382 limit applies • Limitation is based on enhanced value following

surrender or cancellation of creditor’s claims • Interest haircut does not apply

40

Section 382 in Bankruptcy

Choosing between (l)(5) and (l)(6) • Compare amount of NOLs • Compare amount of COD income • Interest haircut • Comfort the transaction will qualify under (l)(5) • Application of Notice 2003-65 • Future plans

− Ownership change − Continuing the business − May want to modify bylaws/charter to prevent sales for 2

years

41

Our Locations

BERWYN 400 Berwyn Park 899 Cassatt Road

Berwyn, PA 19312-1183 610.640.7800

FAX 610.640.7835

BOSTON 15th Floor, Oliver Street Tower

125 High Street Boston, MA 02110-2736

617.204.5100 FAX: 617.204.5150

DETROIT Suite 3600

100 Renaissance Center Detroit, MI 48243-1157

313.259.7110 FAX 313.259.7926

HARRISBURG Suite 200

100 Market Street P.O. Box 1181

Harrisburg, PA 17108-1181 717.255.1155

FAX 717.238.0575

NEW YORK The New York Times Building 37th Floor, 620 Eighth Avenue

New York, NY 10018-1405 212.808.2700

FAX: 212.286.9806

ORANGE COUNTY Suite 1200

4 Park Plaza Irvine, CA 92614-85955

949.567.3500 FAX 949.863.0151

PHILADELPHIA 3000 Two Logan Square

Eighteenth and Arch Streets Philadelphia, PA 19103-2799

215.981.4000 FAX 215.981.4750

PITTSBURGH 50th Floor

500 Grant Street Pittsburgh, PA 15219-2502

412.454.5000 FAX 412.281.0717

PRINCETON Suite 400

301 Carnegie Center Princeton, NJ 08543-5276

609.452.0808 FAX 609.452.1147

WASHINGTON Hamilton Square

600 Fourteenth Street, N.W. Washington, DC 20005-2004

202.220.1200 FAX 202.220.1665

WILMINGTON Hercules Plaza, Suite 5100

1313 Market Street P.O. Box 1709

Wilmington, DE 19899-1709 302.777.6500

FAX 302.421.8390

42

Pepper Locations

Pepper has expanded from its Philadelphia origins to 11 locations.

Detroit, MI Pittsburgh, PA

New York, NY

Wilmington, DE

Philadelphia, PA

Berwyn, PA

Harrisburg, PA

Washington, DC

Princeton, NJ

Orange County, CA

Boston, MA

43

For more information, visit www.pepperlaw.com.