General Sales Tax (GST): Presentation on GST Legislation LAWYERS.

Upload

oswinfoCategory

view

146download

0

T a x Q u e s t / N o v e m b e r 2 0 1 6

© 2016 K. Vaitheeswaran Page | 1 All rights reserved.

Tax Quest An e-newsletter from

K. VAITHEESWARAN & CO.

Advocates & Tax Consultants

Chennai, India. GST Special

November 2016

Issue No.7

CONTENTS

GST REGISTRATION……………....2

GST – IMPACT ON

MANUFACTURING SECTOR……….6

ARTICLE ………………………..…8 GST –The Rate of Tax Debate

T a x Q u e s t / N o v e m b e r 2 0 1 6

© 2016 K. Vaitheeswaran Page | 2 All rights reserved.

GST - REGISTRATION

Introduction:

The Goods & Service Tax regime is most likely to become a reality from April

2017. The Government of India has been taking a number of steps at unbelievable

speed to implement the new regime. Following the Model Law, the Draft Rules

for registration, payment, invoice, returns and refunds were released. The

Government has also released an FAQ on GST.

Trade and industry will have to gear up to this massive change in indirect tax laws

and the first step namely registration is discussed here. The analysis is based on

the various documents made available in the public domain by the Government.

Who needs to take registration?

(i) Every supplier requires registration in respect of taxable supply of goods and

/ or services if his aggregate turnover in a financial year exceeds Rs.9 lakhs.

(ii) The limit is Rs.4 lakhs for North Eastern States including Sikkim.

(iii) Every person who is registered or holds a licence under the earlier law before

the appointed day.

(iv) The transferee or the successor - where a registered taxable person transfers

his business.

(v) In case of amalgamation, demerger by an order of High Court - the transferee

(vi) Persons though not liable under the Act can still obtain registration

voluntarily.

(vii) Specialized agency of the UNO or Any Multilateral Financial Institution and

Organization notified under United Nations (Privileges and Immunities) Act,

1947, Consulate or Embassy of foreign countries or other persons notified by

the Board/ Commissioner.

(viii) A person having multiple business verticals in a State may obtain separate

registration for each business. ‘Business vertical’ means ‘business segment’

as per AS17 issued by the ICAI.

T a x Q u e s t / N o v e m b e r 2 0 1 6

© 2016 K. Vaitheeswaran Page | 3 All rights reserved.

What is the meaning of aggregate turnover?

Aggregate turnover is the value of all taxable and non-taxable supplies, exempt

supplies and exports of goods and / or services of a person having the same PAN to

be computed on all India basis and excludes taxes if any charged under the CGST

Act, SGST Act and IGST Act.

It does not include value of supply on which tax is levied on reverse charge basis

and value of inward supplies.

Who are the persons requiring mandatory registration irrespective of

threshold limits?

(i) Person making inter-state taxable supply

(ii) Casual Taxable Person.

(iii) Person required to pay tax under reverse charge mechanism

(iv) Non-resident taxable person.

(v) Person required to deduct tax at source under Section 37

(vi) Person who effect supply on behalf of other registered taxable person

whether as agent or otherwise.

(vii) Input service distributor

(viii) Persons who supply goods and / or services other than branded services

through e-commerce operator.

(ix) Electronic commerce operator

(x) An aggregator who supplies services under his brand name/ trade name.

(xi) Such other persons as may be notified by the Central or State Government

on the recommendation of the GST Council.

Is registration required in every State?

Every person who is liable to be registered under Schedule-III of the Act shall

apply for registration in every such State in which he is so liable within 30 days

T a x Q u e s t / N o v e m b e r 2 0 1 6

© 2016 K. Vaitheeswaran Page | 4 All rights reserved.

from the date on which he becomes liable to registration in the manner and subject

to conditions prescribed – Section 19(1), Model GST Law.

When is registration not required?

No registration required if the supply of goods and/ or services is not liable to tax

as per the Act unless it falls in the mandatory list.

What is the procedure for fresh registration?

The Draft Rules provide that before applying for registration certain information

has to be declared in the prescribed form on the common portal either directly or

through facilitation center notified by the Board or Commissioner. This would be

verified and rest of the procedures would follow. A flow chart detailing the

procedures is given below:-

DECLARATION - PAN, Mobile & Email

Verification

Generation of Application Reference Number

E-filing of application with prescribed documents

Generation of Acknowledgment Number

Verification of details furnished

Clarification in Case of

Deficiency

Grant of Certificate of

Registration with GSTIN

Rejection of application for

reasons recorded in writing if the

officer is not satisfied with the

clarification or information.

T a x Q u e s t / N o v e m b e r 2 0 1 6

© 2016 K. Vaitheeswaran Page | 5 All rights reserved.

Is there a mechanism for existing Assessees to migrate into GST?

Section 142 of the Model GST Law deals with migration of existing tax payers to

GST and contemplates issue of certificate of registration on a provisional basis in

such form and manner as may be prescribed. This provisional registration would

be valid for 6 months from the date of issue and within that period, the person has

to furnish such information as may be prescribed. On furnishing of such

information, the registration would be granted on a final basis.

Every person who is registered under an earlier law and having a valid PAN shall

be granted registration on a provisional basis. Subsequently, prescribed

information has to be provided along with an application electronically on the

common portal. Registration would be granted or rejected in case the information

or clarification is not provided.

The process for migration would be facilitated through the portal and the details

such as login id and password would be communicated to the assessees soon.

Whether digital signature would be required?

All applications, reply to the notices, returns, appeals or any other documents are

required to be submitted electronically at the common portal duly authenticated

using Digital Signature Certificate (DSC) or through E- Signature as specified

under the Information Technology Act, 2000 or through any other mode of

signature notified by the Board / Commissioner in this behalf.

Who is a non-resident taxable person?

A non-resident taxable person is a taxable person who occasionally undertakes

transaction involving supply of goods and / or services whether as principal or

agent or in any other capacity but who has no fixed place of business in India.

Who is a casual taxable person?

A casual taxable person is a person who occasionally undertakes transactions

involving supply of goods and / or services in the course or furtherance of business

whether as principal, agent or in any other capacity in a taxable territory where he

has no fixed place of business.

T a x Q u e s t / N o v e m b e r 2 0 1 6

© 2016 K. Vaitheeswaran Page | 6 All rights reserved.

Who is an electronic commerce operator?

E-commerce operator includes every person who directly or indirectly, owns,

operates or manages an electronic platform that is engaged in facilitating the

supply of any goods and / or services or in providing any information or any other

services incidental to or in connection therewith but shall not include persons

engaged in supply of such goods and / or services on their own behalf.

GST – IMPACT ON MANUFACTURING SECTOR

Significant inter-State sales

Currently, where a manufacturer from one State effects sale of goods to a customer

in another State, he would charge CST at the rate of 2% subject to issue of C-

Forms by the buyer. In the GST regime, the taxable event would be supply and an

inter-Supply of goods would attract IGST in terms of Section 4(1) of the Model

IGST Law.

The buyer in the other State would be in a position to avail input tax credit of the

IGST charged as against the CST 2% which forms part of the cost in the current

regime.

Better pricing

Currently non-availability of CST credit has worked as a stumbling block in

product pricing. When IGST is available as a credit, there is a possibility of price

discovery.

Review of Depots

In the current regime when there is an inter-State stock transfer by a manufacturer,

the excise duty charged forms part of the cost in case the Depot sells to a dealer

who cannot avail cenvat credit. While the stock transfer does not attract CST it also

results in loss of some element of input tax credit due to proportionate reversal.

In the GST regime if the inter-state stock transfers are taxed, the depot would be

entitled to IGST credit and can set it off against the CGST and SGST payable

when the depot supplies the goods. Where the turnaround time of the depot is fast

then the depots would continue if business needs such a depot. On the other hand if

the business does not warrant many depots or the turnaround time is quite slow,

T a x Q u e s t / N o v e m b e r 2 0 1 6

© 2016 K. Vaitheeswaran Page | 7 All rights reserved.

then the manufacturer could very well scale down the depot and examine direct

supplies to the dealers in the other State.

Freedom of sourcing

In the current regime, many manufacturers source locally on account of VAT

credits and avoid CST purchases unless it is material or there is a price advantage.

GST will open up the sourcing segment and the manufacturer will have the

ultimate freedom to procure from any location since credit availability would no

longer be a restraining factor.

Increased Credit on services

Currently the CENVAT credit for a manufacturer is restricted since in some cases

some services may not meet the test of the definition of input service. Once the

concept of manufacture is eliminated in the GST regime, credit availability should

increase and this would bring down cost.

Elimination of cascading effect

The biggest advantage of GST would be the elimination of cascading effect of

taxes. VAT is charged after excise duty. Excise duty charged by the manufacturer

is not available as credit to the dealer. When GST is introduced, the GST charged

by the manufacturer would qualify as a credit in the hands of the dealer and the

cost would come down in the hands of the dealer. While this would bring down

prices to some extent depending upon the GST rates, manufacturers may not prefer

the entire profits on account of cost savings to flow to the dealer and this would

reflect in review of supply chain as well as price review.

While there are significant positive aspects for the manufacturer, if the rates are

very high, the benefits would be completely lost. Further, manufacturers will have

to plan for huge cash outflow in the initial period as well as under GST due to

higher rates of tax on procurements; GST on advances; GST by way of reverse

charge on certain supply of goods. But overall the manufacturers should gain in

the GST regime.

T a x Q u e s t / N o v e m b e r 2 0 1 6

© 2016 K. Vaitheeswaran Page | 8 All rights reserved.

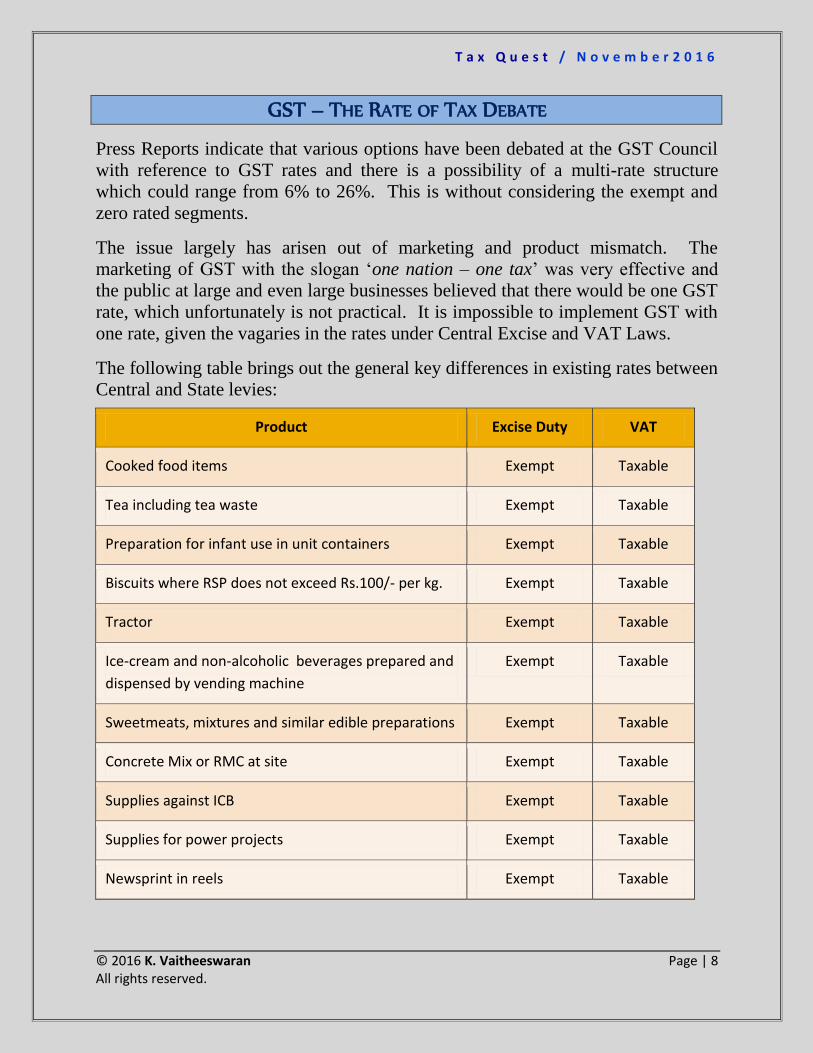

GST – THE RATE OF TAX DEBATE

Press Reports indicate that various options have been debated at the GST Council

with reference to GST rates and there is a possibility of a multi-rate structure

which could range from 6% to 26%. This is without considering the exempt and

zero rated segments.

The issue largely has arisen out of marketing and product mismatch. The

marketing of GST with the slogan ‘one nation – one tax’ was very effective and

the public at large and even large businesses believed that there would be one GST

rate, which unfortunately is not practical. It is impossible to implement GST with

one rate, given the vagaries in the rates under Central Excise and VAT Laws.

The following table brings out the general key differences in existing rates between

Central and State levies:

Product Excise Duty VAT

Cooked food items Exempt Taxable

Tea including tea waste Exempt Taxable

Preparation for infant use in unit containers Exempt Taxable

Biscuits where RSP does not exceed Rs.100/- per kg. Exempt Taxable

Tractor Exempt Taxable

Ice-cream and non-alcoholic beverages prepared and

dispensed by vending machine

Exempt Taxable

Sweetmeats, mixtures and similar edible preparations Exempt Taxable

Concrete Mix or RMC at site Exempt Taxable

Supplies against ICB Exempt Taxable

Supplies for power projects Exempt Taxable

Newsprint in reels Exempt Taxable

T a x Q u e s t / N o v e m b e r 2 0 1 6

© 2016 K. Vaitheeswaran Page | 9 All rights reserved.

Special purpose motor vehicles Exempt Taxable

Vehicles designed for transport of more than 6

persons excluding driver

Exempt Taxable

Vehicles designed for transport of compressed or

liquefied gases falling under 8704

Exempt Taxable

Three wheeled motor vehicles Exempt Taxable

Customized software, audio cassettes Exempt Taxable

*The position is different in some States.

The challenges are broadly as under:-

Pruning of Exemptions:

(i) The list of goods exempted by the State for the purpose of VAT is much

lower than the list of goods that are exempted by the Centre for the purpose

of excise duty and hence if the Central Government list of exemption has to

be pruned down to the State List, a massive set of goods would come into the

ambit of GST and hence the rate at which they are taxed is a critical

decision.

(ii) Even though major attempts were made in 2011 to bring in a concept of 2%

excise duty without cenvat, for many items, excise law still deals with a

number of exemptions.

(iii) In 2004, excise duty was withdrawn on tractors on the premise that the

withdrawal of duty would benefit the farmers. On the contrary, the prices of

tractors went up due to non-availability of cenvat credit benefit. Most States

levy VAT on tractors. Similarly, wind energy items are exempt from excise

but are liable to VAT. Would the Centre levy GST on these items like the

States or convince the States to exempt these items?

T a x Q u e s t / N o v e m b e r 2 0 1 6

© 2016 K. Vaitheeswaran Page | 10 All rights reserved.

Bullion and Jewellery:

(i) The VAT rate on bullion and jewellery is at 1% except Kerala which levies a

higher rate. Only now the Central Government has imposed excise duty on

jewellery and that too at a rate of 1%.

(ii) If this sector is sought to be taxed at say 6% or 4%, it is not something

which would be so easily accepted given the fact that even a 1% levy of

excise duty could not be implemented without a paradigm shift from

‘removal’ to ‘sale’ and a manifold increase in the threshold limits for SSI

exemption. In a GST regime the threshold of exemption is likely to be Rs.20

lakhs.

Luxury Goods:

(i) The VAT regime had the peak rate as a residual category. The standard rate

of excise duty did not have any link to the concept of luxury or elitist

consumption. India would be seen in poor light globally if an abnormal rate

of GST at 26% is contemplated on the so called ‘luxury goods’

(ii) When the entire country had more or less concluded that the peak rate could

be 18% and some believed that it could be slightly more, reports indicating

that nearly 25% of the products may attract 26% is worrying. The benefits

of GST through simplification, lower rates, higher compliance, equitable

distribution of taxes and increase in tax base are all likely to be lost if the

number of items in the 26% rate is higher and is based on the concept of

‘luxury’.

Goods Vs. Services:

(i) Multiple rates and that too 6% / 12% / 18% / 26% would also mean that as a

natural corollary, there would be difference in rates between goods and

services.

(ii) When the consumer is unhappy with the existing 15% (service tax + SBC +

KKC) on services and is dreading a rate of 18%, it is unlikely that the GST

Council would even think of a 26% rate on services. Even if services are at

say 18% and some goods are at 6% / 12% / 26%, the distinction between

goods and services and the eternal debate would be back in full form.

(iii) One had hoped that the fight between goods and services would get over on

implementation of GST, but if the 26% list goes up beyond the so called

T a x Q u e s t / N o v e m b e r 2 0 1 6

© 2016 K. Vaitheeswaran Page | 11 All rights reserved.

known ‘sin products’, classification disputes between goods and services

would arise. The definition of ‘goods’ and ‘services’ in the Model Law are

likely to complicate the issue further. Different set of rules for place of

supply of goods and place of supply of services with a rate of tax distinction

would only add to the misery.

Issues for States:

(i) It would also be a challenge politically for a State to justify say 12% or 18%

on hotels and restaurants. Currently, Tamil Nadu levies VAT at the rate of

2% on hotels and restaurants. Karnataka has a compounding rate of 5% for

restaurants which do not serve liquor. Most States have similarly lower rates

for hotels.

(ii) It would be politically a very big challenge for a State to impose 12% or

18% on hotels and restaurants which would indicate a steep tax rate hike.

The argument that restaurants pay service tax at 6% in addition to VAT, is

only relevant for air-conditioned restaurants and even in that segment, the

effective rate jumps from say 8% to 12% or 18%.

(iii) Apart from general product exemptions, some States have exemption for

specific products linked with turnover limits. (Tamil Nadu exempts chilies,

chili powder, coriander, coriander powder, turmeric, turmeric powder, etc.

where the total turnover of a dealer does not exceed Rs. 300 crores; pulses

and grams where the turnover of the dealer does not exceed Rs. 500 crores;)

Other States have different types of exemptions and politically it would not

be easy to tax these items given the fact that input tax credit is irrelevant for

these sectors.

Cess to fund Compensation:

(i) The idea to impose cess over and above the 26% GST rate to fund

compensation needs to be rejected outright. When States expressed their fear

of losses on account of GST, the Centre gave multiple assurances and

walked the extra mile to guarantee compensation through the Constitution

itself.

(ii) Section 18 of the 101st Constitution Amendment Act, 2016 provides that

Parliament shall by law on the recommendation of the GST Council provide

for compensation to the States for loss of revenue arising on account of GST

implementation.

T a x Q u e s t / N o v e m b e r 2 0 1 6

© 2016 K. Vaitheeswaran Page | 12 All rights reserved.

(iii) The GST Council itself can recommend only GST rates and the cesses that

may be subsumed in the GST. The Council cannot recommend a levy of cess

over and above GST to fund compensation.

(iv) It is presumed that the Centre had done its calculations and based on the

confidence of increased revenue and taking a lead role in implementing a

major tax reform, the Centre assured the States on compensation. This

presumption is based on the fact that the CGST would be comprehensive in

its scope; SSI exemption would be scaled down and the Centre would tax

every person in the supply chain as against only manufacturers. If this

presumption was the basis for the assurance, it is quite surprising that cess

should even be contemplated as a levy over and above GST for funding

compensation. When the Centre is confident that there would not be a

necessity for compensation and the claim may be restricted to few States, the

Centre should use available resources and budgetary support for

compensation as against a levy of cess over and above GST.

Conclusion

It would not be economically feasible to have a single rate for GST. However,

having too many rates would only complicate the issue. A delicate balance has to

be struck. The fact that the meeting of the Council on rates was inconclusive and

clarity would emerge in November indicates that a healthy debate has indeed

commenced and various options are being considered. Industry Associations have

slowly understood the ramifications and the next few weeks would usher in

representations for exemptions and lower rates. It may not be easy to outright

reject the representations on lower rates and exemptions since it is the business

community which understands the market and the impact of tax rates. The GST

benefits would take time to translate and one cannot expect prices of goods to fall

immediately whereas the prices of services would go up immediately.

*****

T a x Q u e s t / N o v e m b e r 2 0 1 6

© 2016 K. Vaitheeswaran Page | 13 All rights reserved.

***

Disclaimer:- Tax Quest is only for the purpose of information and does not constitute or purport to be an advise

or opinion in any manner. The information provided is not intended to create an attorney-client relationship and is

not for advertising or soliciting. K.Vaitheeswaran & Co. do not intend in any manner to solicit work through this

Newsletter. The Newsletter is only to share information based on recent decisions and regulatory changes.

K.Vaitheeswaran & Co. is not responsible for any error or mistake or omission in this Newsletter or for any action

taken or not taken based on the contents of the Newsletter.

CHENNAI BENGALURU

‘VENKATAGIRI’

Flat No.8/3 and 8/4, Ground Floor,

No.8 (Old No.9), Sivaprakasam Street,

T. Nagar,

Chennai – 600 017.

Tel.: 044 + 2433 1029 / 2433 4048

402, Front Wing,

House of Lords,

15 / 16, St. Marks Road,

Bengaluru – 560 001.

Tel.: 092421 78157