Tax Exemptions Assessment Year: 2018-2019 … Savings...Tax Exemptions Assessment Year: 2018-2019...

27

Tax Exemptions Assessment Year: 2018-2019 Financial Year: 2017-2018

Transcript of Tax Exemptions Assessment Year: 2018-2019 … Savings...Tax Exemptions Assessment Year: 2018-2019...

Tax Exemptions

Assessment Year: 2018-2019Financial Year: 2017-2018

TAX SLABS

For Individuals (Men & Women)◦ Taxable Income Tax Amount

Up to Rs.2,50,000/- NIL

Rs.2,50,001 –Rs.5,00,000/- 05 %

Rebate Under section 87-A:

Rs. 2,500/- if Taxable Income up to Rs. 3,50,000/-

Rs.5,00,001 – Rs.10,00,000/- 20%

Above Rs.10,00,000/- 30%

TAX SLABS

For Senior Citizens (Age 60 years or More )◦ Taxable Income Tax

Amount

Up to Rs.3,00,000 NIL

Rs.3,00,001 – Rs.5,00,000/- 05 %

Rs.5,00,001 – Rs.10,00,000/- 20%

Above 10,00,000 30%

TAX SLABS

For Super Senior Citizens (Age 80 years)◦ Taxable Income Tax Amount

Up to Rs.5,00,000/- NIL

Rs.5,00,001 – Rs.10,00,000/- 20%

Above Rs.10,00,000/- 30%

Surcharge:

◦ Taxable Income Surcharge

Rs.50 Lacs - 1 Crore 10% of Income tax

Above Rs. 1 Crore 20% of Income tax

Cess: 3% on total of income tax + surcharge.

Conveyance Allowance

- Exemption under Income Tax is Rs.1,600/- Per Month

Medical Reimbursement

- Exemption is allowed up to Rs.15,000/- during the year

(Subject to Submission of Original Bills)

Food Coupons

- Exemption under Income Tax is Rs.1,100/- Per Month(Employee is eligible for deduction based on Working days)

Leave Travel Allowance

o This concession is allowed for the employee and his family. This

allowance is limited to two children only and that too to only

those born after Oct 01, 1998. This could also be a stepchild or an

adopted one.

o The Income Tax Department counts twins as one child.

o The family includes spouse, children, parents, brother, sister,

who are wholly or mainly dependent on the employee. But the

employee must accompany the trip.

Leave Travel Allowanceo The exemption is restricted only to the travel cost

incurred by the employee.o The tax exemption is not valid for the costs incurred

during the entire trip which might include expenses suchas food expenses, shopping expense and other expense.

o Exemption is allowed for only two travels within a blockof four years. The current block is between Jan’2014 toDec’2017

o if LTA isn’t claimed in a particular block, it can becarried over to the next block and used in the first year ofthe next block itself

o Leave Travel Allowance covers only domestic travel anddoes not cover international travel

Leave Travel Allowanceo Below are the list that are exempted restricted to expense

incurred :oTravel by Air - Economic classoTravel by Rail - A.C First class fareo Journey performed by other mode of transportoPlace of origin and destination of journey connected by rail

- A.C First Class Train FareoPlace of origin and destination of journey not connected by rail but

connected by other recognized Public transport system- First Class or Deluxe class fare by shortest Route

oPlace of origin and destination place of journey not connected by railand not connected by other recognized Public transport system

- A.C First Class Train Fare by shortest route (as journeyperformed by Rail)

House Rent Allowance

Least of the following:

HRA Allowed

40 % on Basic in Non – Metro Cities

50 % on Basic in Metro Cities

Actual Rent Paid

Actual Rent Paid Less 10% of BasicMetros: Delhi, Calcutta, Mumbai, Chennai

Deduction allowed for Self Occupied House

Interest and Principal for Self Occupied HouseMaximum of Rs.2,00,000/- will be allowed as a

deduction for the Interest paid during the year.Maximum of Rs.1,50,000/- will be allowed as

deduction under sec-80c for the Principleamount paid during the year.

Deduction allowed for Let out House

Interest on Loan Taken for Let out Property Total Interest paid during the year for the loan taken for let

out property. Rental Income received from the let out property is treated as

Income from House Property and tax will be calculatedaccordingly-Rental Income declared should not be less thanthe Municipal Rental value of the area.Condition-1: Even if the house is vacant we need to provide the

Notional Rental Value (Municipal Rental Value) in order to get theexemption of interest paid during the year.Condition-2: Interest and Principal on housing loan on letout property

is allowed if the house is not occupied by the employee due to theemployment. i.e., it is at least 20 kms from the place of work.

Deduction allowed for Let out House

Interest on Loan Taken for Let out Property

Particulars AmountActual Rent Received XXXXXLess : Municipal Taxes Paid (XXX)Net Rental Income (NRI) XXXXXLess : 30% Deduction on NRI (XXX)Less : Interest Paid (XXXX)Eligible Deduction (MaxRs.2,00,000)

(XXXXX)

Deduction allowed for Let out House

Interest on Loan Taken for Let out Property Loss from Let out property is restricted to Rs.2,00,000/-

from this Financial Year. (Sec 71(3A))

Municipal Taxes Paid during the year will be allowed asdeduction

Maximum of Rs.1,50,000/- will be allowed as deduction under sec-80c for the Principle amount paid during the year.

Loss from House Property Income including Self occupied and Letout Property can be set off with the other income only upto Rs.200000/- balance amount can be set off in next 8 years.

Pre-construction interest

– Will be allowed when the assessee has taken a loan for purchase or

construction of a house property (not allowed in case of loan for

repairs or reconstruction). The deduction for this interest is allowed in

5 equal installments starting from the year in which the house is

purchased or the construction is completed.

Additional deduction under Section 80EE – Interest on Housing

Loan

Additional Interest of Rs.50000/- is allowed on housing loan subject

to below conditions:

(i) the loan has been sanctioned by the financial institution during theperiod beginning on the 1st day of April, 2016 and ending on the 31st dayof March, 2017;

(ii) the amount of loan sanctioned for acquisition of the residential houseproperty does not exceed 35 lakh rupees;

(iii) the value of residential house property does not exceed 50 lakh rupees; (iv) the assessee does not own any residential house property on the date of

sanction of loan.

Deduction allowed for Mediclaim policy Under Sec 80D

For Self, Spouse, Children up to Rs.25,000/- will be allowed as

deduction towards mediclaim policy premium paid during the year

For Dependent Parents

(Age <60 years) up to Rs.25,000/- will be allowed as deduction

towards mediclaim policy premium paid during the year

(Age >60 years) up to Rs.30,000/- will be allowed as deduction

towards mediclaim policy premium paid during the year

Deduction allowed for Education Loan-80E

Interest paid during the year will be allowed as deduction

under section- 80-E

Deduction will be allowed for Self, Spouse, children

Deduction allowed in Initial Assessment Year and 7

preceding years.

Deduction allowed for Donations – Sec 80 GDonations deducted up to 50% or 100% based on the

notifications under Income Tax Act.Condition: Institution to which donation is made

should be recognized by Government of India andexemption certificate has to obtain from Income Taxdepartment by the institution

Caution: Please check before making a donationwhether the Institution is recognized and whetherexemption is up to 50% or 100%

Deduction Under Section 80 C & 80 CCCDeduction under Section 80-C & 80CCC will be allowed up to Rs.1,50,000/-

for the Investments made in the following :

o Life Insurance premium

o Public Provident Fund

oDeposit in NSC

oULIP

o Principal on Repayment of Housing Loan

oMutual Funds

o ELSS

Deduction Under Section 80 C & 80 CCCDeduction under Section 80-C & 80CCC will be allowed up to Rs.1,50,000/-

for the Investments made in the following :

o Children Education expenses (Tuition Fees)

o Fixed Deposits in Banks (Term 5 years or More)

o House Registration charges paid during the year

o Contribution to Pension Fund Sec 80CCC

o Sukanya Samrudhi Scheme

Deduction Under Section 80 CCD (1)

Investments made in National Pension Schemes notified

by the Government of India is Rs.50,000/- per year

under section 80 CCD (1), this exemption is over and

above the exemption allowed under section 80 C and

80 CCC.

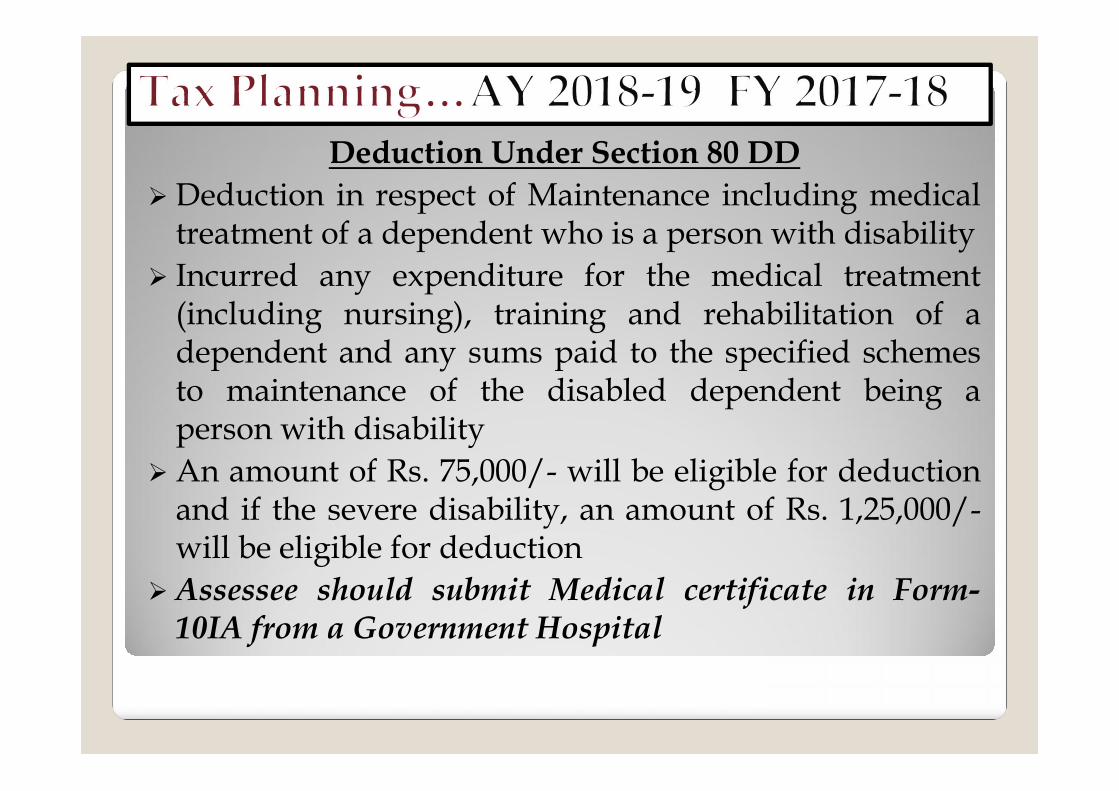

Deduction Under Section 80 DD Deduction in respect of Maintenance including medical

treatment of a dependent who is a person with disability Incurred any expenditure for the medical treatment

(including nursing), training and rehabilitation of adependent and any sums paid to the specified schemesto maintenance of the disabled dependent being aperson with disability

An amount of Rs. 75,000/- will be eligible for deductionand if the severe disability, an amount of Rs. 1,25,000/-will be eligible for deduction

Assessee should submit Medical certificate in Form-10IA from a Government Hospital

Deduction Under Section 80 DD Diseases allowed under section -80DDBlindnessLow visionLeprosy-curedHearing impairmentLoco motor disabilityMental retardationMental illnessAutismCerebral palsyMultiple disabilities

Person with disability means suffering with not less 40% ofthe above diseases, Person with severe disability meanssuffering with more than 80% or multiple disabilities

Deduction Under Section 80 DDB Deduction in respect of Medical Treatment etc for himself of

or a dependent. The Assessee shall be allowed a deduction of the amount

actually paid or a sum of Rs.40,000/- which ever is less and ifthe dependent is senior citizen an amount of Rs.60,000/- oractual amount incurred which ever is less is eligible fordeduction.

An amount of Rs.80,000/- or actual amount incurred whichever is less will be eligible for deduction if the dependent isvery senior citizen.

Assessee should submit Medical certificate in Form-10IAfrom a Neurologist, oncologist, urologist, hematologist,immunologist or such other specialist and may be prescribed

Deduction Under Section 80 DDB Diseases allowed under Section 80DDB

(i ) Neurological Diseases where the disability level has been certifiedto be of 40% and above,—

(a) Dementia(b) Dystonia Musculorum Deformans(c) Motor Neuron Disease(d) Ataxia(e) Chorea(f) Hemiballismus(g) Aphasia(h) Parkinsons Disease

(ii)Malignant Cancers(iii)Acquired Immuno-deficiency Syndrome (AIDS)(iv) Chronic Renal Failure (v)Hematological Disorders