Tax Audit Applicability - Loya Bagriloyabagri.com/admin/images/utility_pdf/774820.pdf · Tax Audit...

12

Tax Audit Applicability Section 44AB, Section 44AD & Section 44ADA As amended by Finance Act, 2016 i.e. for A.Y. 2017-18 Loya Bagri & Co. / Loya Bagri & Associates

Transcript of Tax Audit Applicability - Loya Bagriloyabagri.com/admin/images/utility_pdf/774820.pdf · Tax Audit...

Tax Audit ApplicabilitySection 44AB, Section 44AD & Section 44ADA

As amended by Finance Act, 2016 i.e. for A.Y. 2017-18

Loya Bagri & Co. / Loya Bagri & Associates

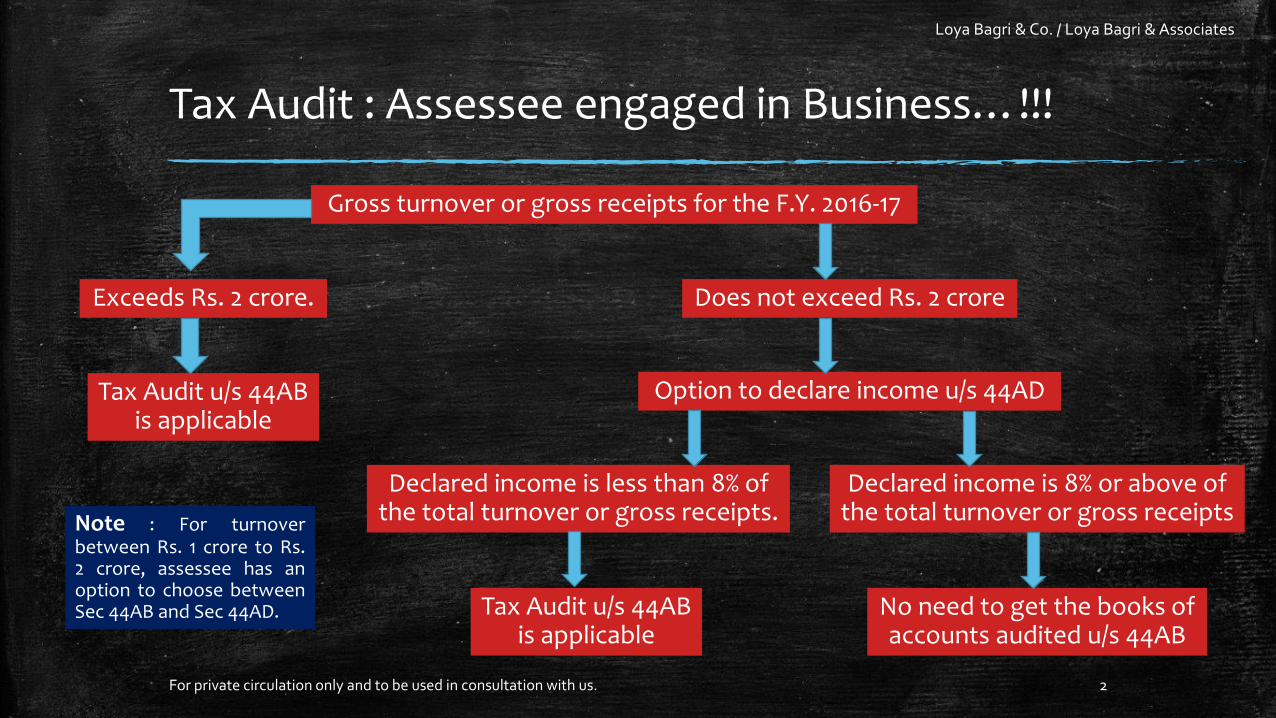

Tax Audit : Assessee engaged in Business…!!!

Gross turnover or gross receipts for the F.Y. 2016-17

Does not exceed Rs. 2 croreExceeds Rs. 2 crore.

Tax Audit u/s 44AB is applicable

Option to declare income u/s 44AD

Declared income is 8% or above of the total turnover or gross receipts

Declared income is less than 8% of the total turnover or gross receipts.

Tax Audit u/s 44AB is applicable

No need to get the books of accounts audited u/s 44AB

Note : For turnoverbetween Rs. 1 crore to Rs.2 crore, assessee has anoption to choose betweenSec 44AB and Sec 44AD.

For private circulation only and to be used in consultation with us. 2

Loya Bagri & Co. / Loya Bagri & Associates

Important amendment w.r.t Sec 44AD in Finance Act, 2017, applicable from A.Y. 2017-18.

“8%” in Sec 44AD, shall beconsidered as “6%.”, inrespect of the amount oftotal turnover or gross

receipts which is RECEIVEDby an account payee chequeor an account payee bankdraft or use of electronicclearing system through abank account during the F.Y.2016-17 or before the due datespecified in section 139(1) inrespect of F.Y. 2016-17.

▪ In the following example, the benefit obtained by traders and small businesses is explained in 3 different scenario.

Particulars 100% Cash Turnover

(Rs.)

60% Digital

Turnover (Rs.)

100% Digital

Turnover (Rs.)

Total Turnover 2 Crore 2 Core 2 Crore

Cash Turnover 2 Crore 0.80 Crore NIL

Digital Turnover NIL 1.2 Crore 2 Crore

Profit on Cash

Turnover @ 8%

16 Lakh 6.40 Lakh NIL

Profit on Digital

turnover @ 6%

NIL 7.20 Lakh 12 Lakh

Total Profit 16 Lakh 13.60 Lakh 12 Lakh

Deduction u/s 80C 1.5 Lakh 1.5 Lakh 1.5 Lakh

Taxable Income 14.50 Lakh 12.10 Lakh 10.50 Lakh

Tax Payable 2,67,800 1,93,640 1,44,200

Tax Saving NIL 74,160 1,23,600

For private circulation only and to be used in consultation with us. 3

Loya Bagri & Co. / Loya Bagri & Associates

Tax Audit : Assessee engaged in Profession…!!!

Gross receipts for the F.Y. 2016-17

Does not exceed Rs. 50 LakhsExceeds Rs. 50 Lakhs

Tax Audit u/s 44AB is applicable

Option to declare income u/s 44ADA

Declared income is 50% or above of the gross receipts

Declared income is less than 50% of the gross receipts.

Tax Audit u/s 44AB applicable

No need to get the books of accounts audited u/s 44AB

For private circulation only and to be used in consultation with us. 4

Loya Bagri & Co. / Loya Bagri & Associates

Analysis of Section 44AB

▪ Every person

▪ Has to get his accounts audited (Form 3CA-CB and Form 3CA-CD)

▪ on or before 30th September, 2017 (30th Nov, 2017 if Transfer Pricing provisions are applicable), if

▪ IN BUSINESS : Total sales, turnover or gross receipts, in business exceeds Rs. 1 Crore in F.Y. 2016-17.

▪ IN BUSINESS : Provisions of section 44AD(4) is applicable and his income exceeds the maximum amountwhich is not chargeable to income-tax.

(Section 44AD(4) is explained in Page 7)

▪ IN PROFESSION : Gross receipts in profession exceeds Rs. 50 Lakhs in F.Y. 2016-17.

▪ IN PROFESSION (where gross total receipts does not exceed Rs. 50 Lakhs) : If the assessee claims income tobe lower than 50% of total gross receipts and his income exceeds the maximum amount which is notchargeable to income-tax.

Penalty for non-compliance (Sec 271B) : ½% of the total sales, turnover or gross receipts or Rs.1,50,000/-, whichever is less.

For private circulation only and to be used in consultation with us. 5

Loya Bagri & Co. / Loya Bagri & Associates

Analysis of Section 44AD

▪ A resident individual, HUF or partnership firm (excl. LLP)▪ Engaged in Business (except plying, hiring or leasing goods carriage u/s 44AE), whose▪ Total turnover or gross receipts do not exceed Rs. 2 crore in F.Y. 2016-17,

and▪ Assesse claims a sum of 8% of the total turnover or gross receipts or more

to have been earned.▪ No need of to get the books of accounts audited in such situation.

Deduction u/s 30 to 38 is deemed to have been given, hence no furtherdeduction.

No additional deduction w.r.t salary & interest paid to partners shall be allowed.(The deduction of salary & interest were allowed till F.Y. 2015-16)

In case of Loss, Sec 44AD is not applicable.

For private circulation only and to be used in consultation with us. 6

Loya Bagri & Co. / Loya Bagri & Associates

Issues w.r.t sub-section 4 of Sec 44AD

▪ Where the assessee declares profit for any F.Y. in accordance with Sec 44AD.▪ And he declares profit for any of the 5 F.Y. succeeding such F.Y., not in accordance with

Sec 44AD, then▪ He shall not be eligible to claim the benefit of the provisions of Sec 44AD for 5 F.Y’s

subsequent to the F.Y. in which the profit has not been declared in accordance with theprovisions Sec 44AD.

Understanding with an example Assessee declared income U/s 44AD for A.Y. 2017-18. He continues to declare the income u/s 44AD for A.Y 2018-19 and 2019-20. However for A.Y 2020-21 he has not declared income u/s 44AD. Then the assessee will not be able to avail the benefit of declaring income u/s 44AD for 5

A.Y succeeding A.Y2020-21 i.e. he will not be allowed to declare income u/s 44AD fromA.Y 2021-22 to 2025-26.

On applicability of Sub-section 4, assessee has to get the tax audit done u/s 44AB.

For private circulation only and to be used in consultation with us. 7

Loya Bagri & Co. / Loya Bagri & Associates

Analysis of Section 44ADA

▪ A resident

▪ Engaged in Profession, whose

▪ Total gross receipts do not exceed Rs. 50,00,000/- in F.Y. 2016-17, and

▪ Assesse claims a sum of 50% of the total gross receipts or more to havebeen earned.

▪ No need of to get the books of accounts audited in such situation.

Deduction u/s 30 to 38 is deemed to have been given, hence no further deduction.

If Assesse claims a sum of less than 50% of the total gross receipts to have beenearned by the assessee, tax audit u/s 44AB has to be done.

For private circulation only and to be used in consultation with us. 8

Loya Bagri & Co. / Loya Bagri & Associates

Section 44AB (Bare Text)As amended by Finance Act, 2016

Every person,—

(a) carrying on business shall, if his total sales, turnover or gross receipts, as the case may be, in business exceed orexceeds Rs. 1 Crore in any previous year; or

(b) carrying on profession shall, if his gross receipts in profession exceed Rs. 50 Lakhs in any previous year; or

(c) carrying on the business shall, if the profits and gains from the business are deemed to be the profits and gains ofsuch person under section 44AE or section 44BB or section 44BBB, as the case may be, and he has claimed his incometo be lower than the profits or gains so deemed to be the profits and gains of his business, as the case may be, in anyprevious year; or

(d) carrying on the profession shall, if the profits and gains from the profession are deemed to be the profits andgains of such person under section 44ADA and he has claimed such income to be lower than the profits and gains sodeemed to be the profits and gains of his profession and his income exceeds the maximum amount which is notchargeable to income-tax in anyprevious year; or

(e) carrying on the business shall, if the provisions of sub-section (4) of section 44AD are applicable in his case and hisincome exceeds the maximum amount which is not chargeable to income-tax in any previous year,

get his accounts of such previous year audited by an accountant before the specified date and furnish by that datethe report of such audit in the prescribed form duly signed and verified by such accountant and setting forth suchparticulars as may be prescribed.For private circulation only and to be used in consultation with us. 9

Loya Bagri & Co. / Loya Bagri & Associates

Section 44AD (Bare Text)As amended by Finance Act, 2016

(1) Notwithstanding anything to the contrary contained in sections 28 to 43C, in the case of an eligibleassessee engaged in an eligible business, a sum equal to 8% of the total turnover or gross receipts of theassessee in the previous year on account of such business or, as the case may be, a sum higher than theaforesaid sum claimed to have been earned by the eligible assessee, shall be deemed to be the profitsand gains of such business chargeable to tax under the head "Profits and gains of business orprofession".

(2) Any deduction allowable under the provisions of sections 30 to 38 shall, for the purposes of sub-section(1), be deemed to have been already given full effect to and no further deduction under those sectionsshall be allowed.

(3) The written down value of any asset of an eligible business shall be deemed to have been calculated as ifthe eligible assessee had claimed and had been actually allowed the deduction in respect of thedepreciation for each of the relevant assessment years.

(4) Where an eligible assessee declares profit for any previous year in accordance with the provisions of thissection and he declares profit for any of the 5 assessment years relevant to the previous year succeedingsuch previous year not in accordance with the provisions of sub-section (1), he shall not be eligible toclaim the benefit of the provisions of this section for 5 assessment years subsequent to the assessmentyear relevant to the previous year in which the profit has not been declared in accordance with theprovisions of sub-section (1).

For private circulation only and to be used in consultation with us. 10

Loya Bagri & Co. / Loya Bagri & Associates

Cont.… Section 44AD (Bare Text)As amended by Finance Act, 2016

(5) Notwithstanding anything contained in the foregoing provisions of this section, an eligible assessee to whomthe provisions of sub-section (4) are applicable and whose total income exceeds the maximum amount which is notchargeable to income-tax, shall be required to keep and maintain such books of account and other documents asrequired under sub-section (2) of section 44AA and get them audited and furnish a report of such audit as requiredunder section 44AB.

(6) The provisions of this section, notwithstanding anything contained in the foregoing provisions, shall not apply to-

(i) a person carrying on profession as referred to in sub-section (1) of section 44AA;

(ii) a person earning income in the nature of commission or brokerage; or

(iii) a person carrying on any agency business.

___________________________________________________________________________________________

(a) "eligible assessee" means,—

(i) an individual, HUF or a partnership firm, who is a resident, but not a LLP firm as defined under section 2(1)(n) of the LLP Act, 2008 (6 of2009); and

(ii) who has not claimed deduction under any of the sections 10A, 10AA, 10B, 10BA or deduction under any provisions of Chapter VIA under theheading "C. - Deductions in respect of certain incomes" in the relevant assessment year;

(b) "eligible business" means,—

▪ (i) any business except the business of plying, hiring or leasing goods carriages referred to in section 44AE; and

▪ (ii) whose total turnover or gross receipts in the previous year does not exceed an amount of Rs. 2 crore.For private circulation only and to be used in consultation with us. 11

Loya Bagri & Co. / Loya Bagri & Associates

Section 44ADA (Bare Text)As amended by Finance Act, 2016

(1) Notwithstanding anything contained in sections 28 to 43C, in the case of an assessee, being a resident in India,who is engaged in a profession referred to in sub-section (1) of section 44AA and whose total gross receipts donot exceed Rs. 50,00,000/- in a previous year, a sum equal to 50% of the total gross receipts of the assessee in theprevious year on account of such profession or, as the case may be, a sum higher than the aforesaid sum claimedto have been earned by the assessee, shall be deemed to be the profits and gains of such profession chargeable totax under the head "Profits and gains of business or profession".

(2) Any deduction allowable under the provisions of sections 30 to 38 shall, for the purposes of sub-section (1), bedeemed to have been already given full effect to and no further deduction under those sections shall be allowed.

(3) The written down value of any asset used for the purposes of profession shall be deemed to have beencalculated as if the assessee had claimed and had been actually allowed the deduction in respect of thedepreciation for each of the relevant assessment years.

(4) Notwithstanding anything contained in the foregoing provisions of this section, an assessee who claims thathis profits and gains from the profession are lower than the profits and gains specified in sub-section (1) andwhose total income exceeds the maximum amount which is not chargeable to income-tax, shall be required tokeep and maintain such books of account and other documents as required under sub-section (1) of section44AA and get them audited and furnish a report of such audit as required under section 44AB.

For private circulation only and to be used in consultation with us. 12

Loya Bagri & Co. / Loya Bagri & Associates