Tax Anti-Avoidance Recent Developments & Updates

40

Tax Anti-Avoidance Recent Developments & Updates by CA R. BUPATHY Past President - ICAI AGN INTERNATIONAL ASIA PACIFIC MEET 19 th to 21 st June INDIA PERSPECTIVE Partner R Bupathy & Co., India 1

-

Upload

emma-blackwell -

Category

Documents

-

view

39 -

download

0

description

AGN INTERNATIONAL ASIA PACIFIC MEET. Tax Anti-Avoidance Recent Developments & Updates. 19 th to 21 st June. INDIA PERSPECTIVE. by CA R. BUPATHY Past President - ICAI. Partner R Bupathy & Co., India. Measures to ensure Compliance of Tax Laws. - PowerPoint PPT Presentation

Transcript of Tax Anti-Avoidance Recent Developments & Updates

1

Tax Anti-Avoidance Recent Developments & Updates

by CA R. BUPATHYPast President - ICAI

AGN INTERNATIONAL ASIA PACIFIC MEET

19th to 21st June

INDIA PERSPECTIVE

Partner R Bupathy & Co., India

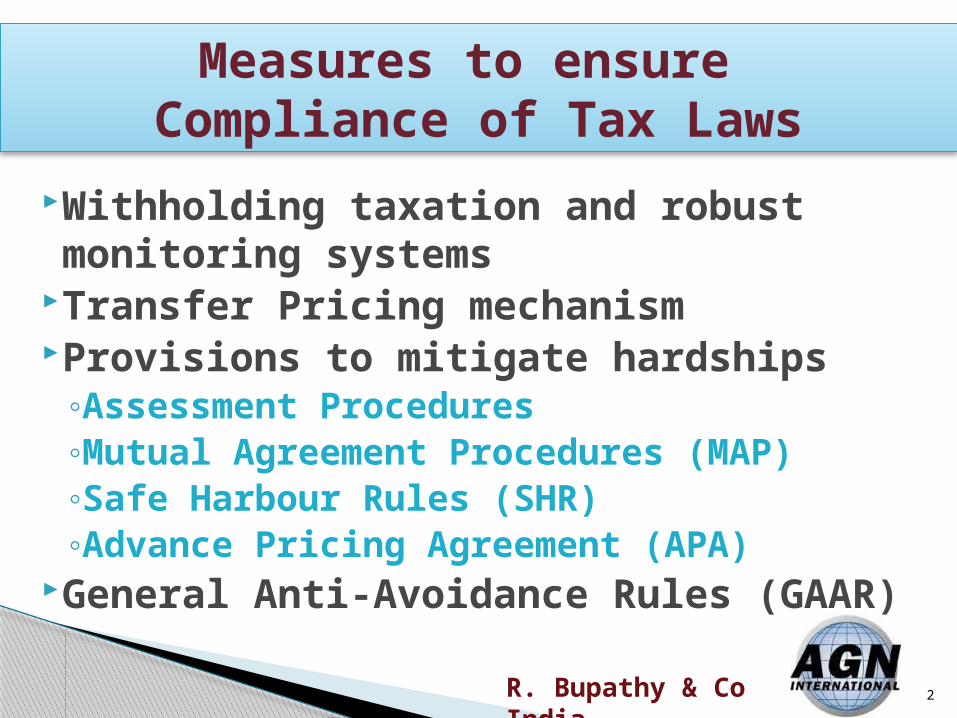

2R. Bupathy & Co India

Withholding taxation and robust monitoring systems

Transfer Pricing mechanismProvisions to mitigate hardships

◦Assessment Procedures◦Mutual Agreement Procedures (MAP)◦Safe Harbour Rules (SHR)◦Advance Pricing Agreement (APA)

General Anti-Avoidance Rules (GAAR)

Measures to ensure Compliance of Tax Laws

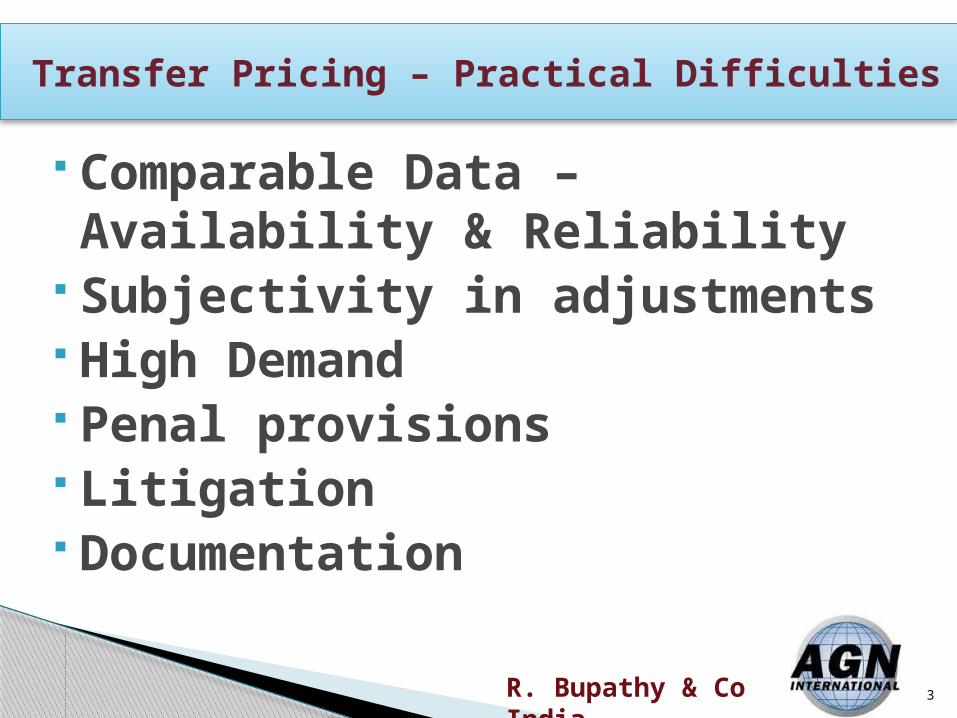

3R. Bupathy & Co India

Comparable Data – Availability & Reliability

Subjectivity in adjustments High Demand Penal provisions Litigation Documentation

Transfer Pricing – Practical Difficulties

4R. Bupathy & Co India

Penal ProvisionsParticulars Penalty

Non-Maint of info or doc 2% of the Transaction ValueNon Furn of info or doc 2% of the Transaction ValueIncorrect Maint of info or doc 2% of the Transaction ValueIncorrect furn of info or doc 2% of the Transaction ValueNon-submission of audit report Rs. 1 LakhAddition to income – treated as concealment

Min penalty – tax sought to be avoided.Max penalty – thrice the tax avoided.

5R. Bupathy & Co India

1. Assessment procedures2. Mutual Agreement Procedure (MAP)3. Safe Harbour Rules4. Advance Pricing Agreement (APA)

Provisions to mitigate hardships

6R. Bupathy & Co India

ASSESSMENT PROCEDURE

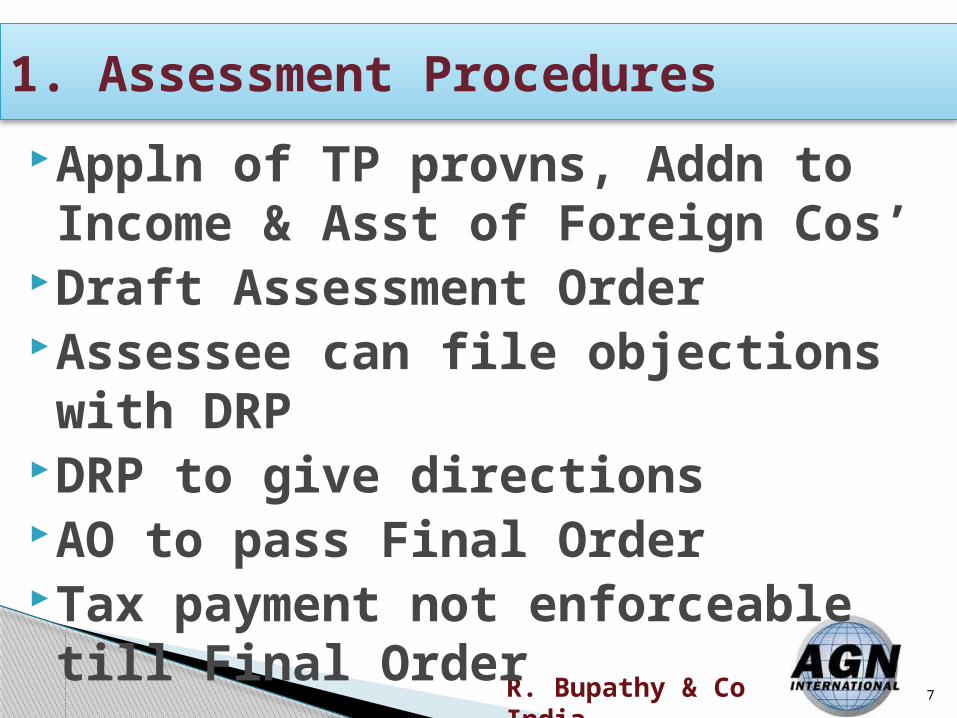

7R. Bupathy & Co India

Appln of TP provns, Addn to Income & Asst of Foreign Cos’

Draft Assessment OrderAssessee can file objections with DRPDRP to give directionsAO to pass Final Order Tax payment not enforceable till Final Order

1. Assessment Procedures

8R. Bupathy & Co India

MUTUAL AGREEMENT PROCEDURE

9R. Bupathy & Co India

2. Mutual Agreement Procedure

Permissible only if Treaty contains MAP clause◦Article 25 of UN Model or OECD Model◦Interpretation Issues◦CAs “shall endeavor” to reach a solution.

No obligation to reach a solution Time LimitParallel proceedingsArbitration

10R. Bupathy & Co India

Interpretation Issues

Benefits of Treaty denied to a resident of a State

CAs on their own initiative resolve questions of interpretation or application of the treaty

No specific provision to avoid double taxation in treaty

11R. Bupathy & Co India

Time Limit

Application for MAP◦Withholding Tax : within 3 years from

date of payment◦Others : Within 3 years from the date

of tax notification

12R. Bupathy & Co India

Parallel Proceedings

Application made for MAP Other proceedings can continue under

Indian tax laws Agreement reached under MAP To be implemented notwithstanding any

time limits in the domestic laws

13R. Bupathy & Co India

Arbitration

No provision for arbitration in India tax treaties

14R. Bupathy & Co India

SAFE HARBOUR RULES

Applicable from 18th September 2013

15R. Bupathy & Co India

Eligible Assessee Eligible transactions Operating Margin

- Operating Margin means Profit before Int & Tax and exceptional items

3. Safe Harbour Rules (SHR)

16R. Bupathy & Co India

Operating Margins Sl.No

Eligible Intl Transaction Circumstances

(i) Software Dev Services TV <= Rs.500 Cr : OM min 20% of OETV > Rs.500 Cr : OM min 22% of OE

(ii) ITES TV <= Rs.500cr : OM min 20% of OETV > Rs.500cr : OM min 22% of OE

(iii) KPO OM min 25% of OE(iv) Intra Grp loan<=Rs.50 Cr INT min Base rate of SBI as of

30th June (PY) + 150 basis points(v) Intra Grp loan >Rs.50Cr INT min Base rate of SBI as of

30th June (PY) + 300 basis points

17R. Bupathy & Co India

Operating Margins (Cont….) Sl.No

Eligible Intl Transaction Circumstances

(vi) Corporate Guarantee (a) Commn/Fee min 2% p.a. on AG

(vii) Corporate Guarantee (b) Commn/Fee min 1.75% p.a. on AG

(viii) Contract R&D – Software Dev(wholly or partly)

OM min 30% of OE

18R. Bupathy & Co India

Sl. No

Eligible Intl Transaction Circumstances

(ix) Contract R&D – generic pharma drugs (wholly or partly)

OM min 29% of OE

(x) Mfre & export of core auto components OM min 12% of OE(xi) Mfre & export of non-core auto

componentsOM min 8.5% of OE

OM – Operating Margin INT - InterestTV – Transaction Value OE – Operating ExpenseAG – Amount guaranteed

Operating Margins (Cont….)

19R. Bupathy & Co India

Concept of significant risk For 5 years from AY’2013-’14 Option for lesser period Decision of assessee to opt out Time bound Procedure

Features of SHR

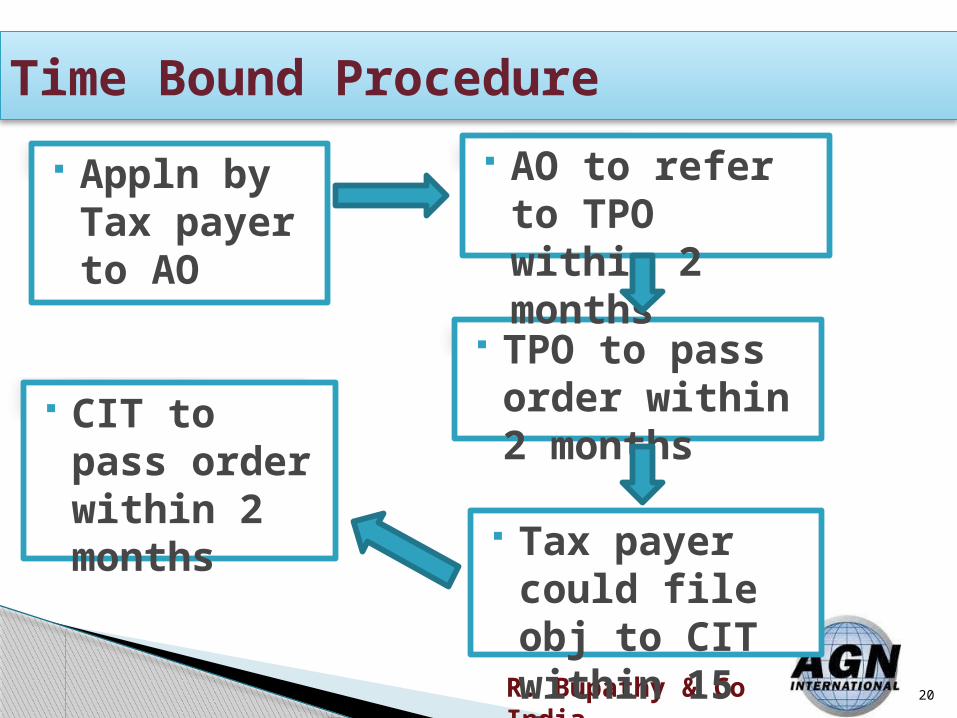

20R. Bupathy & Co India

Tax payer could file obj to CIT within 15 days

Time Bound Procedure

TPO to pass order within 2 months

AO to refer to TPO within 2 months

Appln by Tax payer to AO

CIT to pass order within 2 months

21R. Bupathy & Co India

MeritsCertaintySpecified yearsBenefit to opt outDemerits No relief against double taxation Persons in notified jurisdictional areas, tax

havens and low tax countries kept out MAP cannot be invoked

Merits & Demerits (SHR)

22R. Bupathy & Co India

Categorization of services Definition of KPO

Business process outsourcing provided mainly with the assistance or use of information technology requiring application of knowledge & advanced analytical & technical skills.

Issues

23R. Bupathy & Co India

ADVANCE PRICING AGREEMENT

Applicable from 01st July 2012

24R. Bupathy & Co India

Applies only to Intl transactionsVoluntaryTax-payer initiatedNot a time bound processAny assesseeNo threshold limitTerm – Max 5 years

Advance Pricing Agreement

25R. Bupathy & Co India

APA - Types

Unilateral APA◦Application to DGIT

Bilateral & Multilateral APA◦Application to Competent Authority of India

(CAI)

26R. Bupathy & Co India

Request for pre-filing consultation to be filed by taxpayers

Pre-filing consultation bwn taxpayer and revenue

Filing APA appln with applicable fees

Preliminary processing and removal of deficiencies in appln

Application proceeded with

Processing by APA Team/ Competent Authority• Meetings• Calling for docs• Visit to applicants business premises• Enquiries

Manually agreed drafts of APA

Central Govt. approval

APA agtt

Advance Pricing Agreement - Procedure

27R. Bupathy & Co India

Request for Bilateral or Multilateral

A tax treaty exists between India & other country(ies)

The tax treaty contains an article on MAP In case of double taxation there should be

an enabling clause in the tax treaty.◦Refer Art 9(2) of OECD Model Convention

The corresponding APA program exists in the other country

28R. Bupathy & Co India

Merits of APA

Tax certainty on ALP of covered transactions

Reduced risk of double taxation through Bilateral/Multilateral APAs

Reduced compliance costsCertainty on records & docs

29R. Bupathy & Co India

APA – Application fees

Amount of international transaction

Fee

Not exceeding Rs.100 crores 10 lacs

Not exceeding Rs.200 crores 15 lacs

Exceeding Rs.200 crores 20 lacs

30R. Bupathy & Co India

Compliances

Annual Compliance Report (ACR) ◦Within 30 days from due date of filing

ITR◦Non-furnishing of ACR – cancellation of

APA by CBDT◦Mandatory Compliance Audit by

jurisdictional TPO (6 months)

31R. Bupathy & Co India

APA - Issues

Withdrawal of applicationValidity of APA when actual TO exceeds

the amount specified in applicationCan Unilateral APA be converted into

Bilateral or Multilateral APARe-opening past assessments

32R. Bupathy & Co India

GENERAL ANTI-AVOIDANCE RULE

Applicable from FY 1st April 2015

AY 2016-’17

33R. Bupathy & Co India

Consequences:a) Disregarding, combining or re-characterising any

step in, or a part or whole of the IAA;b) Treating the IAA as if it had not been entered into;c) Disregarding any accommodating party;d) Deeming connected persons to be one and the

same person;(contd.,)

Impermissible Avoidance Arrangement (IAA)

34R. Bupathy & Co India

Consequences: (e) Re-allocating amongst the parties;

(i) Any accrual, or receipt of a capital or revenue nature; (ii)Any expense, relief or rebate

(f) Treating place of residence or situs of an asset or of a transaction at a place other than the; (i) place of residence; (ii) location of the asset; (iii)location of the transaction;as provided in the arrangement.

(contd.,)

Impermissible Avoidance Arrangement (IAA)

35R. Bupathy & Co India

Consequences:(g) Looking through any arrangement by lifting the

corporate veil;For the purpose of this section:(i) any equity may be treated as debt or vice versa;(ii) any accrual or receipt of a capital nature may be treated as revenue in nature or vice versa;(iii) any expenditure, deduction, relief or rebate may be re-characterised

Impermissible Avoidance Arrangement (IAA)

36R. Bupathy & Co India

Main purpose is to obtain a “TAX BENEFIT” and

(a) Creates rights or obligations which are not ordinarily created between persons dealing at arms length;

(b) Results directly or indirectly in the misuse or abuse of the provisions of the Act;

(c) Lacks commercial substance;(contd.,)

Definition of IAA

37R. Bupathy & Co India

(d) Entered into or carried on by means or in a manner which are not ordinarily employed for bonafide purposes;(e) Burden of proof is on the assessee to establish that the arrangement is not an IAA

Definition of IAA (Cont…)

38R. Bupathy & Co India

GAAR Procedure

AO – Reasons to believe IAA – Notice to Assessee Referral to CIT with reasons Assessee files objections (max 60 days) CIT considers the reference and objection:

◦If CIT rejects reference, to issue directions to AO within 1 month from end of month notice expires

◦If reference of AO accepted, reference to Approving Panel within 2 months

39R. Bupathy & Co India

GAAR Procedure

Approving Panel to issue directions to AO within 6 months

AO to pass Orders as per directions of Approving Panel

The directions are binding on –◦the assessee; and◦the CIT and his sub-ordinates

No appeal under the Act lies against such directions

40R. Bupathy & Co India

Thank you