TAX AND DEVELOPMENT - ITC · TAX AND DEVELOPMENT ... TransferTransferpricing pricing 3 ......

12

TAX AND DEVELOPMENT TAX AND DEVELOPMENT Overview Ben Dickinson ITC Meeting, 19 October 2012

Transcript of TAX AND DEVELOPMENT - ITC · TAX AND DEVELOPMENT ... TransferTransferpricing pricing 3 ......

TAX AND DEVELOPMENTTAX AND DEVELOPMENT

OverviewBen Dickinson

ITC Meeting, 19 October 2012

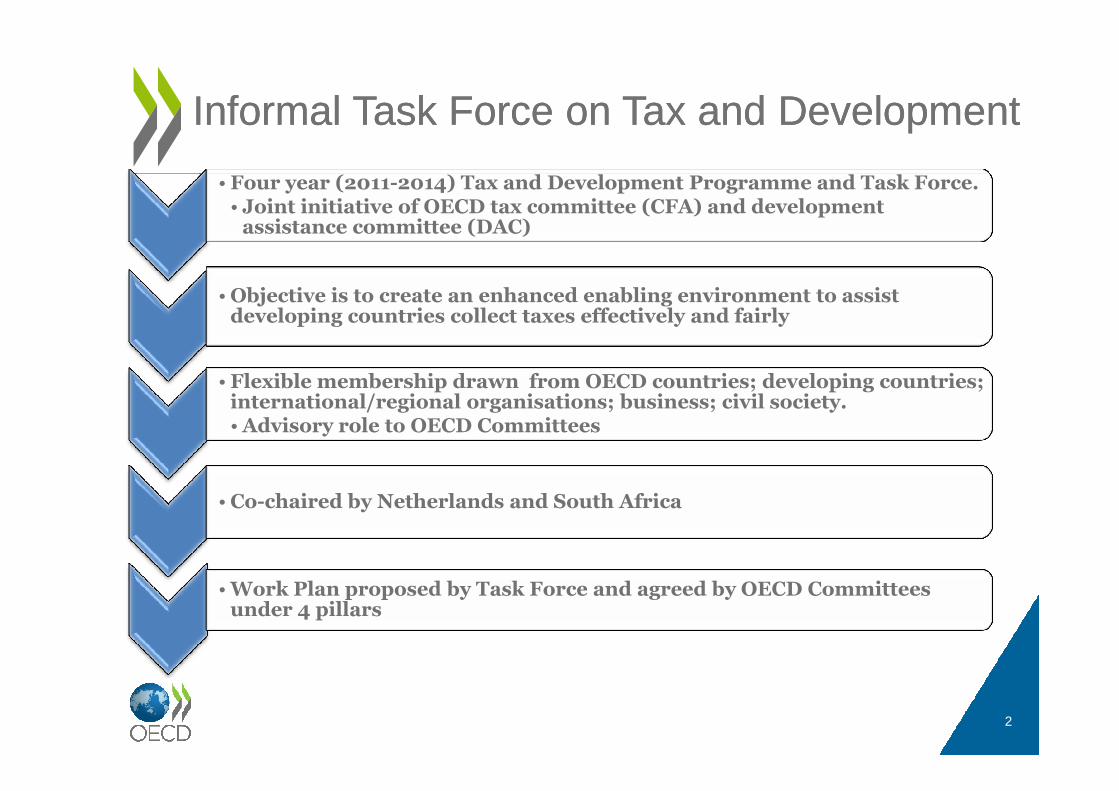

• Four year (2011-2014) Tax and Development Programme and Task Force.• Joint initiative of OECD tax committee (CFA) and development assistance committee (DAC)

•Objective is to create an enhanced enabling environment to assist developing countries collect taxes effectively and fairly

• Flexible membership drawn from OECD countries; developing countries; international/regional organisations; business; civil society.

Informal Task Force on Tax and DevelopmentInformal Task Force on Tax and Development

international/regional organisations; business; civil society.•Advisory role to OECD Committees

•Co-chaired by Netherlands and South Africa

•Work Plan proposed by Task Force and agreed by OECD Committees under 4 pillars

2

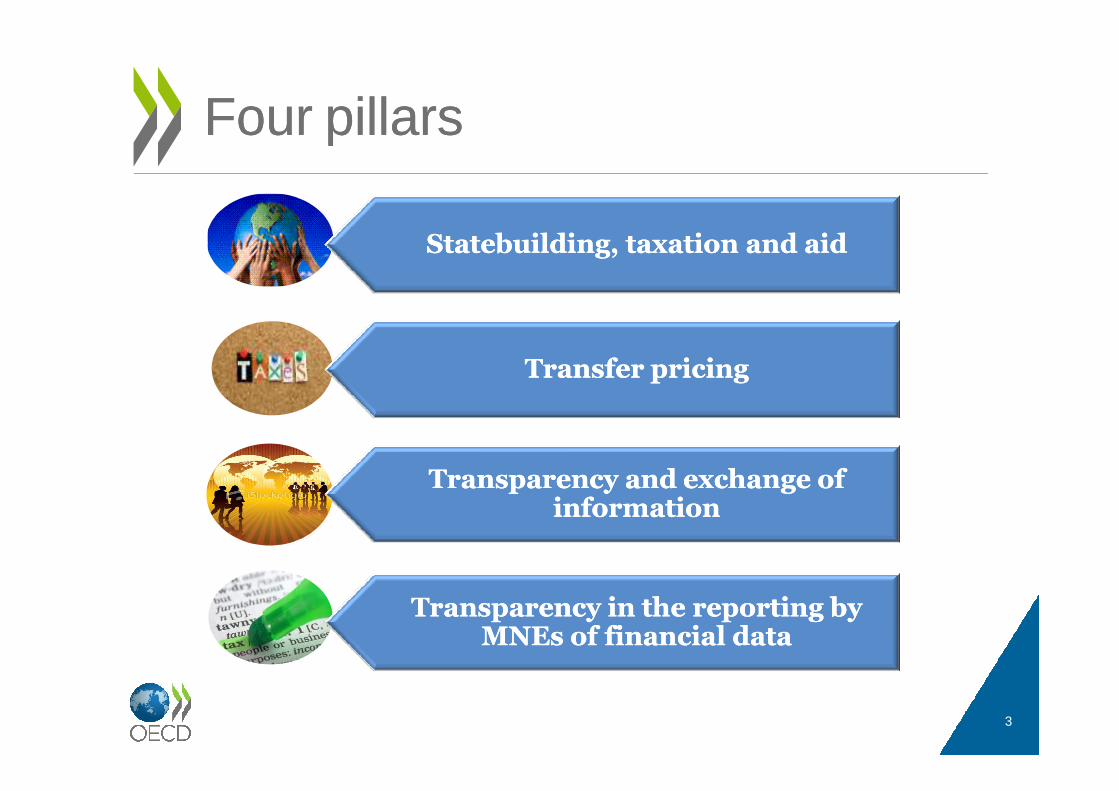

FourFour pillarspillars

Statebuilding, taxation and aidStatebuilding, taxation and aid

TransferTransfer pricingpricing

3

TransparencyTransparency inin thethe reportingreporting bybyMNEsMNEs ofof financialfinancial datadata

TransparencyTransparency andand exchangeexchange ofofinformationinformation

Tax Inspectors Without Borders (TIWB) – Feasibility Study

• To explore the feasibility of the establishing a new initiative to deploy tax auditors to developing countries on a demand-led basis. Key components:

• Mechanism to facilitate the wide-spread sharing of international audit expertise, in an efficient and effective way.

Statebuilding, taxation and aidStatebuilding, taxation and aid

(1)(1)

efficient and effective way.

• Match demand from developing countries with experts from a pool of the best tax inspectors available.

• Real-time audit assistance focused on cases with international tax aspects e.g. Transfer Pricing

• In depth discussion required with ITC and other partners (December 2012)

4

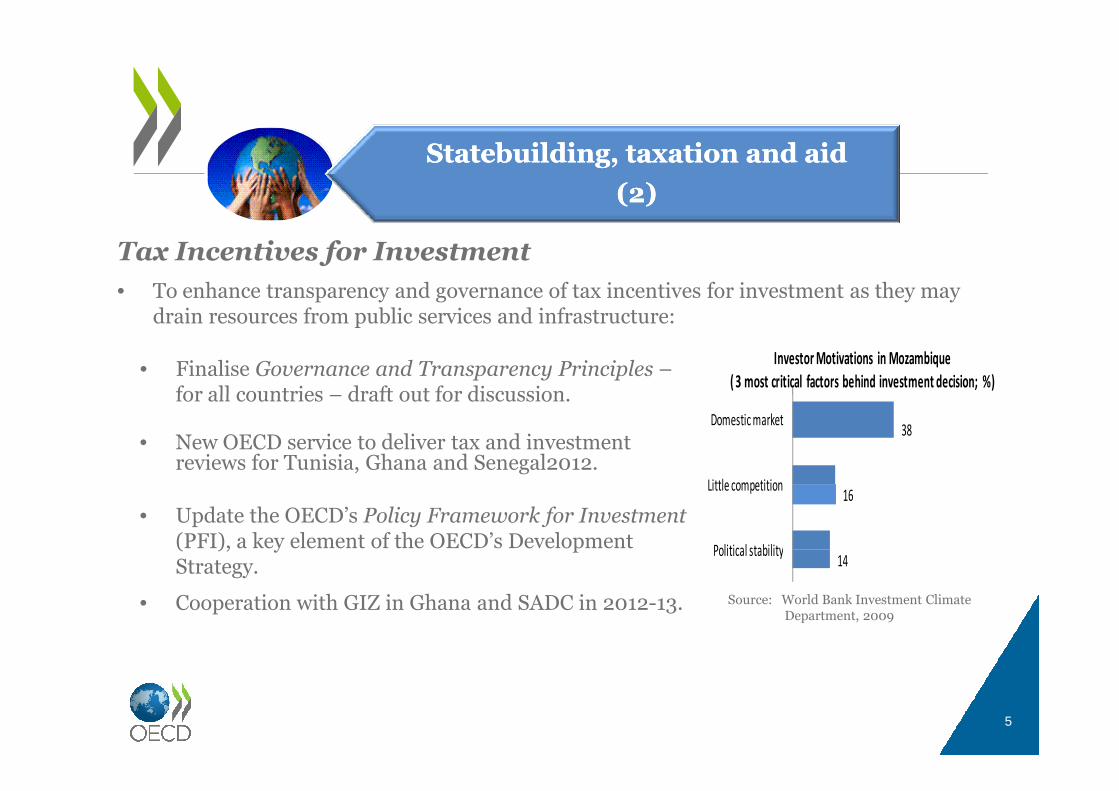

Investor Motivations in Mozambique

( 3 most critical factors behind investment decision; %)

Tax Incentives for Investment

• To enhance transparency and governance of tax incentives for investment as they may drain resources from public services and infrastructure:

Statebuilding, taxation and aidStatebuilding, taxation and aid

(2)(2)

• Finalise Governance and Transparency Principles –for all countries – draft out for discussion.

Source: World Bank Investment Climate Department, 2009

14

16

38

Political stability

Little competition

Domestic market

5

for all countries – draft out for discussion.

• New OECD service to deliver tax and investment reviews for Tunisia, Ghana and Senegal2012.

• Update the OECD’s Policy Framework for Investment (PFI), a key element of the OECD’s Development Strategy.

• Cooperation with GIZ in Ghana and SADC in 2012-13.

Principles for International Engagement in Supporting Developing Countries in Revenue Matters

• To enhance the quality and quantity of international assistance for tax system development, builds on successful OECD/ITC collaboration on Aid Modalities Study.

• Validate the Principles in Ghana, Uganda and others (Needs ITC field support)

Statebuilding, taxation and aidStatebuilding, taxation and aid

(3)(3)

6Source: OECD Secretariat*Does not include IMF -0,05%

0,00%

0,05%

0,10%

0,15%

0,20%

0,25%

0

20

40

60

80

100

120

140

160

180

200

2004 2005 2006 2007 2008 2009 2010

USD millions

Tax activities (left

scale)

Share in total ODA (right

scale)

Estimates of Official Development Assistance aimed at supporting tax systems 2004--2010*

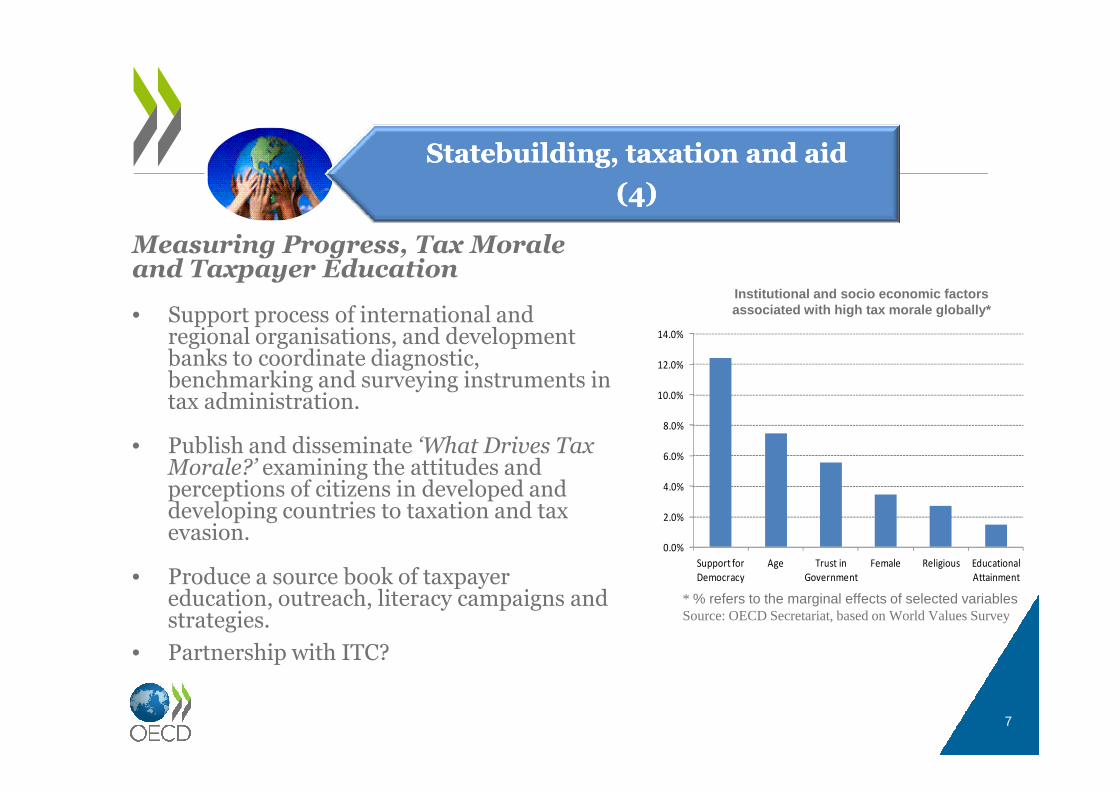

Measuring Progress, Tax Morale and Taxpayer Education

• Support process of international and regional organisations, and development banks to coordinate diagnostic, benchmarking and surveying instruments in tax administration.

Statebuilding, taxation and aidStatebuilding, taxation and aid

(4)(4)

Institutional and socio economic factors associated with high tax morale globally*

10.0%

12.0%

14.0%

tax administration.

• Publish and disseminate ‘What Drives Tax Morale?’ examining the attitudes and perceptions of citizens in developed and developing countries to taxation and tax evasion.

• Produce a source book of taxpayer education, outreach, literacy campaigns and strategies.

• Partnership with ITC?

7

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Support for

Democracy

Age Trust in

Government

Female Religious Educational

Attainment

* % refers to the marginal effects of selected variablesSource: OECD Secretariat, based on World Values Survey

TransferTransfer pricingpricing

To support developing countries implement transfer pricing regimes. Support programme includes:

• Comprehensive support to transfer pricing capacity development programmes in Colombia, Ghana, Kenya, Rwanda and Vietnam (and others)

• Excellent partnership with World Bank, EC, SECO and GIZ.• Excellent partnership with World Bank, EC, SECO and GIZ.

• Development of a “Train the Trainers” programme for developing countries.

• Assistance to regional organisations (e.g. ATAF) in delivering their work programmes on transfer pricing and the development of new guidance and tools.

• Development of tools and training materials to support capacity development in transfer pricing.

• Testing the applicability and relevance of OECD guidance on transfer pricing in the developing country context.

8

TransparencyTransparency andand exchangeexchange ofofinformationinformation

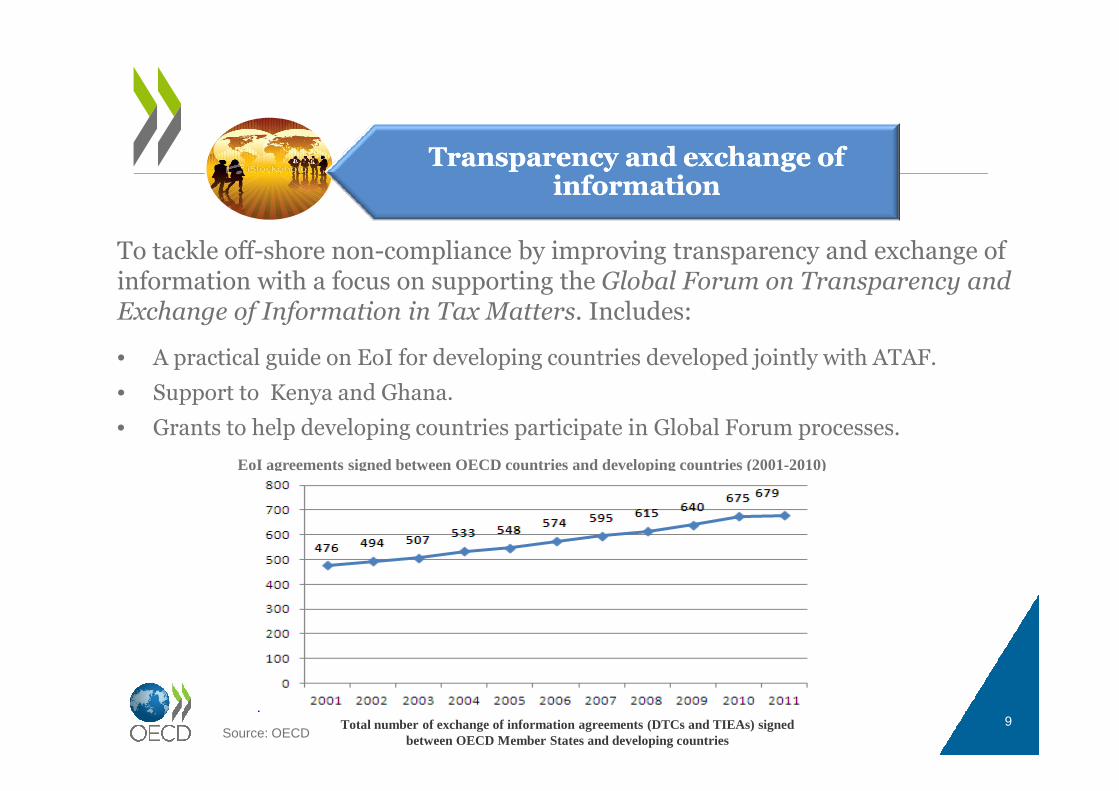

To tackle off-shore non-compliance by improving transparency and exchange of information with a focus on supporting the Global Forum on Transparency and Exchange of Information in Tax Matters. Includes:

• A practical guide on EoI for developing countries developed jointly with ATAF.

• Support to Kenya and Ghana.• Support to Kenya and Ghana.

• Grants to help developing countries participate in Global Forum processes.

9Source: OECD

EoI agreements signed between OECD countries and developing countries (2001-2010)

Total number of exchange of information agreements (DTCs and TIEAs) signed between OECD Member States and developing countries

TransparencyTransparency in the reporting by in the reporting by MNEs of financial dataMNEs of financial data

To improve tax compliance, contribute to the enhancement of transparency in the reporting of financial data:

• No consensus on costs and benefits of calls for ‘country-by-country reporting’ (of financial data by MNEs).

• Disseminate report exploring the potential value of the public registration of local statutory accounts of unlisted companies in developing countries as a tool to promote transparency.

• Monitor current government and business led initiatives to increase transparency in financial reporting by MNEs, in particular the implementation of the Dodd-Frank Act in the USA and the European Union Transparency Directive.

10

• More field level partnerships with ITC partners.

• Taxation of Natural Resources?

• OECD member participation in OECD Task Force

What next?What next?

• OECD member participation in OECD Task Force ‘core group’.

• Post Busan process and DRM.

11

• Contact: OECD Tax and Development Secretariat

Ben Dickinson – [email protected]

For additional informationFor additional information

12

www.oecd.org/tax/globalrelationsintaxation/