TAX AMNESTY ACT

33

TAX AMN Present RHODORA GARC RHODORA GARC Tax Advisor 9 NESTY ACT ted by: CIA CIA-ICARANOM ICARANOM r/Consultant

Transcript of TAX AMNESTY ACT

TAX AMNESTY ACT

1

Presented by:

RHODORA GARCIARHODORA GARCIA--ICARANOMICARANOMTax Advisor/Consultant

1RGI CPAs 2019

TAX AMNESTY ACT

1

Presented by:

RHODORA GARCIARHODORA GARCIA--ICARANOMICARANOMTax Advisor/Consultant

1

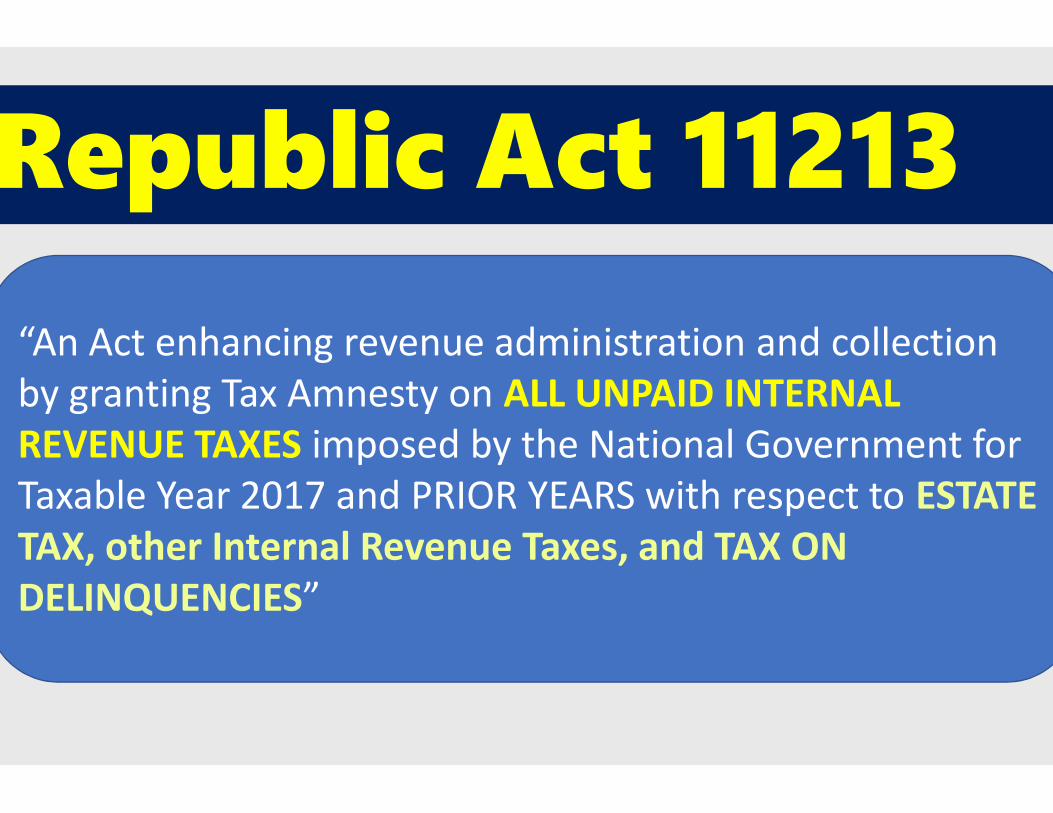

Republic Act 11213“An Act enhancing revenue administration and collectionby granting Tax Amnesty on ALL UNPAID INTERNALREVENUE TAXES imposed by the National Government forTaxable Year 2017 and PRIOR YEARS with respect to ESTATETAX, other Internal Revenue Taxes, and TAX ONDELINQUENCIES”

“An Act enhancing revenue administration and collectionby granting Tax Amnesty on ALL UNPAID INTERNALREVENUE TAXES imposed by the National Government forTaxable Year 2017 and PRIOR YEARS with respect to ESTATETAX, other Internal Revenue Taxes, and TAX ONDELINQUENCIES”

Republic Act 11213“An Act enhancing revenue administration and collectionby granting Tax Amnesty on ALL UNPAID INTERNALREVENUE TAXES imposed by the National Government forTaxable Year 2017 and PRIOR YEARS with respect to ESTATETAX, other Internal Revenue Taxes, and TAX ONDELINQUENCIES”

2

“An Act enhancing revenue administration and collectionby granting Tax Amnesty on ALL UNPAID INTERNALREVENUE TAXES imposed by the National Government forTaxable Year 2017 and PRIOR YEARS with respect to ESTATETAX, other Internal Revenue Taxes, and TAX ONDELINQUENCIES”

REPUBLIC ACT 11213

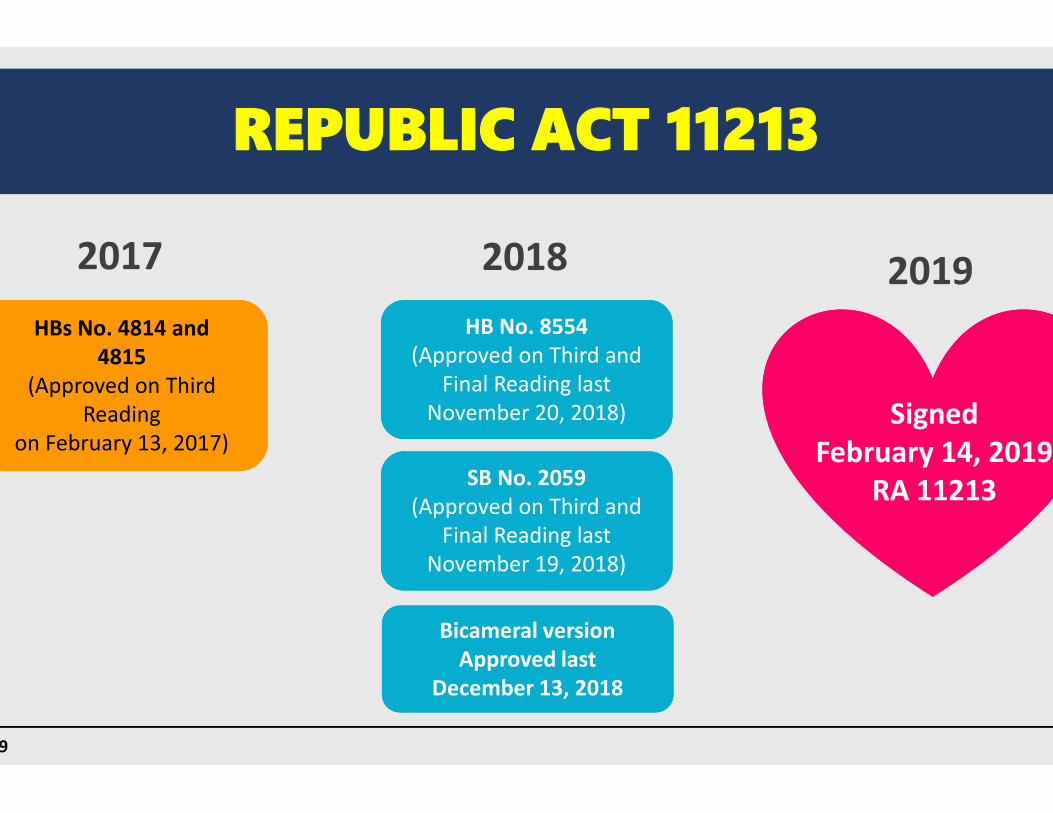

2017 2018HBs No. 4814 and

4815(Approved on Third

Readingon February 13, 2017)

HBs No. 4814 and4815

(Approved on ThirdReading

on February 13, 2017)

HB No. 8554(Approved on Third and

Final Reading lastNovember 20, 2018)

HB No. 8554(Approved on Third and

Final Reading lastNovember 20, 2018)

3

HBs No. 4814 and4815

(Approved on ThirdReading

on February 13, 2017)

HBs No. 4814 and4815

(Approved on ThirdReading

on February 13, 2017)

HB No. 8554(Approved on Third and

Final Reading lastNovember 20, 2018)

HB No. 8554(Approved on Third and

Final Reading lastNovember 20, 2018)

SB No. 2059(Approved on Third and

Final Reading lastNovember 19, 2018)

SB No. 2059(Approved on Third and

Final Reading lastNovember 19, 2018)

Bicameral versionApproved last

December 13, 2018

Bicameral versionApproved last

December 13, 2018

3RGI CPAs 2019

REPUBLIC ACT 11213

2018 2019HB No. 8554

(Approved on Third andFinal Reading last

November 20, 2018)

HB No. 8554(Approved on Third and

Final Reading lastNovember 20, 2018) Signed

February 14, 2019RA 11213

3

HB No. 8554(Approved on Third and

Final Reading lastNovember 20, 2018)

HB No. 8554(Approved on Third and

Final Reading lastNovember 20, 2018)

SB No. 2059(Approved on Third and

Final Reading lastNovember 19, 2018)

SB No. 2059(Approved on Third and

Final Reading lastNovember 19, 2018)

Bicameral versionApproved last

December 13, 2018

Bicameral versionApproved last

December 13, 2018

SignedFebruary 14, 2019

RA 11213

3

TAX AMNESTY ACT OF 2019

4

Build, build, buildStrengthening the country’s

Infrastructure backbone

EducationAchieving a more conducive

learning environment

TARGET COLLECTION:

Source: Estrellita Suansing in an interview dated November 20, 2018

4RGI CPAs 2019

TAX AMNESTY ACT OF 2019

4

EducationAchieving a more conducive

learning environment

Social ServicesProviding better healthcare

services and facilities

TARGET COLLECTION: Php 114.8 BillionSource: Estrellita Suansing in an interview dated November 20, 2018

4

OBJECTIVES OF THE TAX AMNESTYACT

One-time opportunity tosettle estate tax

obligations; to givereasonable tax relief toestates with deficiency

estate taxes.

One-time opportunity tosettle estate tax

obligations; to givereasonable tax relief toestates with deficiency

estate taxes.

Enhance revenuecollection by providing a

tax amnesty ondelinquencies that will

minimize administrativecosts in pursuing tax

cases and de-clog thedockets of the BIR and

the courts.

Enhance revenuecollection by providing a

tax amnesty ondelinquencies that will

minimize administrativecosts in pursuing tax

cases and de-clog thedockets of the BIR and

the courts.

5

One-time opportunity tosettle estate tax

obligations; to givereasonable tax relief toestates with deficiency

estate taxes.

One-time opportunity tosettle estate tax

obligations; to givereasonable tax relief toestates with deficiency

estate taxes.

Enhance revenuecollection by providing a

tax amnesty ondelinquencies that will

minimize administrativecosts in pursuing tax

cases and de-clog thedockets of the BIR and

the courts.

Enhance revenuecollection by providing a

tax amnesty ondelinquencies that will

minimize administrativecosts in pursuing tax

cases and de-clog thedockets of the BIR and

the courts.

5RGI CPAs 2019

OBJECTIVES OF THE TAX AMNESTYACT

Enhance revenuecollection by providing a

tax amnesty ondelinquencies that will

minimize administrativecosts in pursuing tax

cases and de-clog thedockets of the BIR and

the courts.

Enhance revenuecollection by providing a

tax amnesty ondelinquencies that will

minimize administrativecosts in pursuing tax

cases and de-clog thedockets of the BIR and

the courts.

Provide a more equitabletax system by adopting a

comprehensive taxreform program that will

simplify therequirements on tax

amnesties with the useof simplified forms, and

utilization of informationtechnology in

broadening the tax base.

Provide a more equitabletax system by adopting a

comprehensive taxreform program that will

simplify therequirements on tax

amnesties with the useof simplified forms, and

utilization of informationtechnology in

broadening the tax base.

5

Enhance revenuecollection by providing a

tax amnesty ondelinquencies that will

minimize administrativecosts in pursuing tax

cases and de-clog thedockets of the BIR and

the courts.

Enhance revenuecollection by providing a

tax amnesty ondelinquencies that will

minimize administrativecosts in pursuing tax

cases and de-clog thedockets of the BIR and

the courts.

Provide a more equitabletax system by adopting a

comprehensive taxreform program that will

simplify therequirements on tax

amnesties with the useof simplified forms, and

utilization of informationtechnology in

broadening the tax base.

Provide a more equitabletax system by adopting a

comprehensive taxreform program that will

simplify therequirements on tax

amnesties with the useof simplified forms, and

utilization of informationtechnology in

broadening the tax base.

5

GENERALGENERALTAXTAX

AMNESTYAMNESTY

ESTATE TAXESTATE TAXAMNESTY ONAMNESTY ON

LASTLASTDECEDENTDECEDENT

POLICYPOLICY

VETOED BY THE PRESIDENT:

6

GENERALGENERALTAXTAX

AMNESTYAMNESTY

ESTATE TAXESTATE TAXAMNESTY ONAMNESTY ON

LASTLASTDECEDENTDECEDENT

POLICYPOLICY

6RGI CPAs 2019

ESTATE TAXESTATE TAXAMNESTY ONAMNESTY ON

LASTLASTDECEDENTDECEDENT

POLICYPOLICY

VETOED BY THE PRESIDENT:

6

PRESUMPTIONPRESUMPTIONOF CORRECTNESSOF CORRECTNESS

OF THE ESTATEOF THE ESTATETAX AMNESTYTAX AMNESTY

RETURNSRETURNS

ESTATE TAXESTATE TAXAMNESTY ONAMNESTY ON

LASTLASTDECEDENTDECEDENT

POLICYPOLICY

6

PRESUMPTIONPRESUMPTIONOF CORRECTNESSOF CORRECTNESS

OF THE ESTATEOF THE ESTATETAX AMNESTYTAX AMNESTY

RETURNSRETURNS

AMNESTY TAX as APPROVED

1.) Estate Tax Amnesty

2.) Tax Amnesty on Delinquencies

7

3.) Confidentiality of Tax Amnesty Returns

7RGI CPAs 2019

3.) Confidentiality of Tax Amnesty Returns

4.) Penalties on Exchange and Unlawful Divulgence of Info

5.) Creation of Information Management System

6.) Creation of Congressional Oversight Committee

AMNESTY TAX as APPROVED

2.) Tax Amnesty on Delinquencies

7

3.) Confidentiality of Tax Amnesty Returns

7

3.) Confidentiality of Tax Amnesty Returns

4.) Penalties on Exchange and Unlawful Divulgence of Info

5.) Creation of Information Management System

6.) Creation of Congressional Oversight Committee

TAX AMNESTY ON DELINQUENCIESCOVERAGE & AVAILMENT

BIRBIR

Income TaxIncome Tax

Withholding TaxWithholding Tax

Capital Gains TaxCapital Gains Tax

8

Capital Gains TaxCapital Gains Tax

Donor’s TaxDonor’s Tax

Value Added TaxValue Added Tax

Other Percentage TaxesOther Percentage Taxes

Excise TaxExcise Tax

Documentary Stamp TaxDocumentary Stamp Tax8RGI CPAs 2019

TAX AMNESTY ON DELINQUENCIESCOVERAGE & AVAILMENT

88

TAX AMNESTYTAX AMNESTYONON

DELINQUENCIESDELINQUENCIES

9

TAX AMNESTYTAX AMNESTYONON

DELINQUENCIESDELINQUENCIES

9RGI CPAs 2019

TAX AMNESTYTAX AMNESTYONON

DELINQUENCIESDELINQUENCIES

9

TAX AMNESTYTAX AMNESTYONON

DELINQUENCIESDELINQUENCIES

9

Delinquencies and assessments, which have become final and executory ,including delinquent tax account, where the application of compromisehas been requested on the basis of:i) doubtful validity of assessment; orii) financial incapacity of the taxpayer, but the same was denied by the

Regional Evaluation Board or the National Evaluation Board on or beforethe IRRs take effect

Delinquencies and assessments, which have become final and executory ,including delinquent tax account, where the application of compromisehas been requested on the basis of:i) doubtful validity of assessment; orii) financial incapacity of the taxpayer, but the same was denied by the

Regional Evaluation Board or the National Evaluation Board on or beforethe IRRs take effect

Pending criminal cases with the DOJ or the courts for tax evasion and othercriminal offenses under Chapter II of Title X of the NIRC, as amended, with

or without assessments duly issued; and

Pending criminal cases with the DOJ or the courts for tax evasion and othercriminal offenses under Chapter II of Title X of the NIRC, as amended, with

or without assessments duly issued; and

COVERAGE

COVERAGE

10

Pending criminal cases with the DOJ or the courts for tax evasion and othercriminal offenses under Chapter II of Title X of the NIRC, as amended, with

or without assessments duly issued; and

Pending criminal cases with the DOJ or the courts for tax evasion and othercriminal offenses under Chapter II of Title X of the NIRC, as amended, with

or without assessments duly issued; and

Tax cases subject of final and executory judgement by the courts on orbefore the IRR take effect;

Tax cases subject of final and executory judgement by the courts on orbefore the IRR take effect;

Withholding tax agents who withheld taxes but failed to remit the same tothe BIR

Withholding tax agents who withheld taxes but failed to remit the same tothe BIR

COVERAGE

COVERAGE

10RGI CPAs 2019

Delinquencies and assessments, which have become final and executory ,including delinquent tax account, where the application of compromisehas been requested on the basis of:i) doubtful validity of assessment; orii) financial incapacity of the taxpayer, but the same was denied by the

Regional Evaluation Board or the National Evaluation Board on or beforethe IRRs take effect

Delinquencies and assessments, which have become final and executory ,including delinquent tax account, where the application of compromisehas been requested on the basis of:i) doubtful validity of assessment; orii) financial incapacity of the taxpayer, but the same was denied by the

Regional Evaluation Board or the National Evaluation Board on or beforethe IRRs take effect

Pending criminal cases with the DOJ or the courts for tax evasion and othercriminal offenses under Chapter II of Title X of the NIRC, as amended, with

or without assessments duly issued; and

Pending criminal cases with the DOJ or the courts for tax evasion and othercriminal offenses under Chapter II of Title X of the NIRC, as amended, with

or without assessments duly issued; and

10

Pending criminal cases with the DOJ or the courts for tax evasion and othercriminal offenses under Chapter II of Title X of the NIRC, as amended, with

or without assessments duly issued; and

Pending criminal cases with the DOJ or the courts for tax evasion and othercriminal offenses under Chapter II of Title X of the NIRC, as amended, with

or without assessments duly issued; and

Tax cases subject of final and executory judgement by the courts on orbefore the IRR take effect;

Tax cases subject of final and executory judgement by the courts on orbefore the IRR take effect;

Withholding tax agents who withheld taxes but failed to remit the same tothe BIR

Withholding tax agents who withheld taxes but failed to remit the same tothe BIR

10

• shall mean the latest amountof tax assessment issued bythe BIR against the taxpayer,exclusive of interest, penaltiesand surcharge.

BASIC TAX ASSESSED - Defined

11

• shall mean the latest amountof tax assessment issued bythe BIR against the taxpayer,exclusive of interest, penaltiesand surcharge.

11RGI CPAs 2019

• shall mean the latest amountof tax assessment issued bythe BIR against the taxpayer,exclusive of interest, penaltiesand surcharge.

BASIC TAX ASSESSED - Defined

11

• shall mean the latest amountof tax assessment issued bythe BIR against the taxpayer,exclusive of interest, penaltiesand surcharge.

11

ENTITLEMENT & RATESSec. 18. Any person may enjoy the immunities and privileges of the TAD and pay the following taxamnesty rates:

Nature of DelinquencyDelinquencies and assessments which have become final andexecutoryTax cases subject of final and executory judgement by courts

12

Tax cases subject of final and executory judgement by courts

Pending criminal cases with criminal information filed with theDepartment of Justice or the courts for tax evasion and othercriminal offences under Chapter II of Title X and Section 275 ofthe National Internal Revenue Code of 1997, as amended, withassessments duly issued and otherwise excluded in Title II and IIIhereofWithholding agents who withheld taxes but failed to remit thesame to the Bureau of Internal Revenue

12RGI CPAs 2019

ENTITLEMENT & RATESSec. 18. Any person may enjoy the immunities and privileges of the TAD and pay the following taxamnesty rates:

Nature of Delinquency RateDelinquencies and assessments which have become final andexecutory

40% of the basictax assessed

Tax cases subject of final and executory judgement by courts 50% of the basictax assessed

12

Tax cases subject of final and executory judgement by courts 50% of the basictax assessed

Pending criminal cases with criminal information filed with theDepartment of Justice or the courts for tax evasion and othercriminal offences under Chapter II of Title X and Section 275 ofthe National Internal Revenue Code of 1997, as amended, withassessments duly issued and otherwise excluded in Title II and IIIhereof

60% of the basictax assessed

Withholding agents who withheld taxes but failed to remit thesame to the Bureau of Internal Revenue

100% of the basictax assessed

12

• Sworn Tax Amnesty on Delinquencies (TADR)• Certification of Delinquencies

WHAT to File?

WHEN to File?

RETURNS & FILING OF TAD

13

RDO which has jurisdiction over the residence or principal place of business of thetaxpayer

Within one (1) year from the effectivity of the IRRWHEN to File?

WHERE to File?

RDO shall issue and endorse ACCEPTANCE PAYMENT FORMHOW to File?

13RGI CPAs 2019

• Sworn Tax Amnesty on Delinquencies (TADR)• Certification of Delinquencies

RETURNS & FILING OF TAD

13

RDO which has jurisdiction over the residence or principal place of business of thetaxpayer

Within one (1) year from the effectivity of the IRR

RDO shall issue and endorse ACCEPTANCE PAYMENT FORM

13

TAP (TAX AMNESTY PROCESS)

TADR+

APF “PAID”

TADR+

APF “PAID”

STAMP“RECEIVED”BY BIR RDO

STAMP“RECEIVED”BY BIR RDO

RDO submission

14

TADR+

APF “PAID”

TADR+

APF “PAID”

STAMP“RECEIVED”BY BIR RDO

STAMP“RECEIVED”BY BIR RDO

14RGI CPAs 2019

TAP (TAX AMNESTY PROCESS)

14

Within 15 days from submission

ATCA

14

BEYOND 15 days

DEEMEDAPPROVED

OR

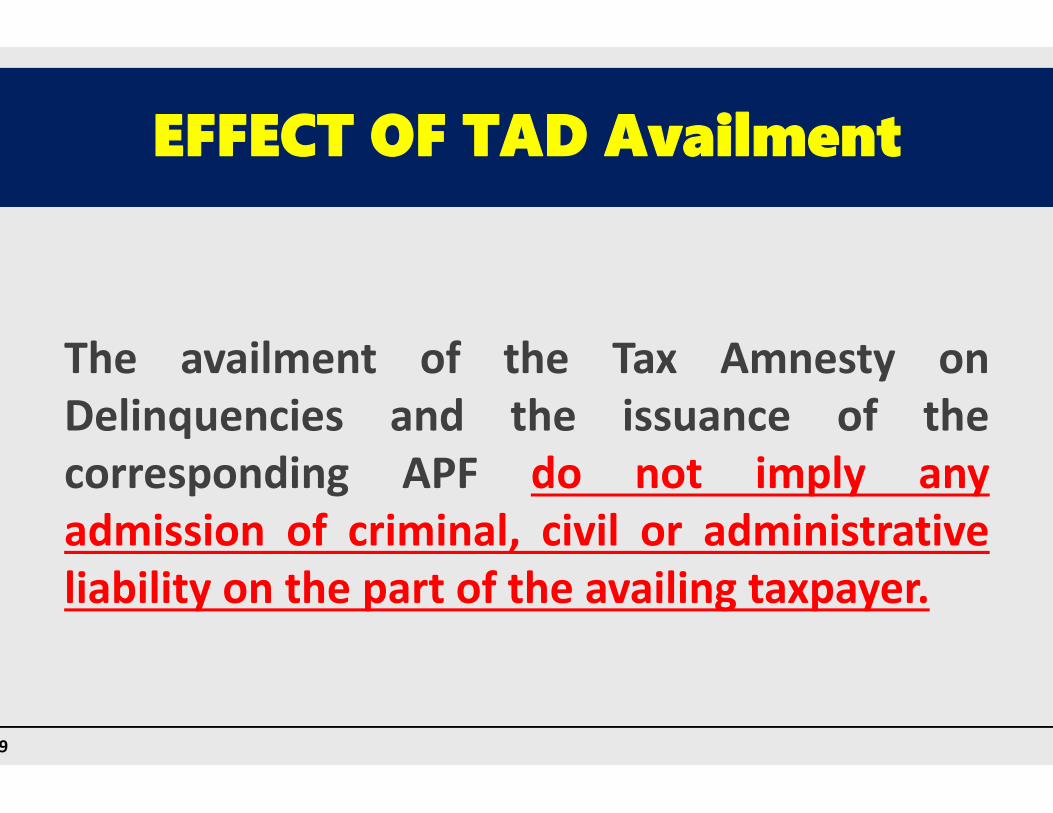

EFFECT OF TAD Availment

The availment of the Tax Amnesty onDelinquencies and the issuance of thecorresponding APF do not imply anyadmission of criminal, civil or administrativeliability on the part of the availing taxpayer.

15

The availment of the Tax Amnesty onDelinquencies and the issuance of thecorresponding APF do not imply anyadmission of criminal, civil or administrativeliability on the part of the availing taxpayer.

15RGI CPAs 2019

EFFECT OF TAD Availment

The availment of the Tax Amnesty onDelinquencies and the issuance of thecorresponding APF do not imply anyadmission of criminal, civil or administrativeliability on the part of the availing taxpayer.

15

The availment of the Tax Amnesty onDelinquencies and the issuance of thecorresponding APF do not imply anyadmission of criminal, civil or administrativeliability on the part of the availing taxpayer.

15

IMMUNITIES AND PRIVILEGES

The tax delinquency shall be considered settled and the criminal case and itscorresponding civil or administrative case, if applicable, be terminated.

The taxpayer shall be immune from all suits or actions, including the payment ofsaid delinquency or assessment, as well as additions thereto, and from allappurtenant civil, criminal, and administrative cases, and penalties.

16

The taxpayer shall be immune from all suits or actions, including the payment ofsaid delinquency or assessment, as well as additions thereto, and from allappurtenant civil, criminal, and administrative cases, and penalties.

Any notices of levy, attachments and/or warrants of garnishment issued againstthe taxpayer shall be set aside pursuant to a lifting of notice of levy/garnishmentduly issued by the BIR or its authorized representative.

16RGI CPAs 2019

IMMUNITIES AND PRIVILEGES

The tax delinquency shall be considered settled and the criminal case and itscorresponding civil or administrative case, if applicable, be terminated.

The taxpayer shall be immune from all suits or actions, including the payment ofsaid delinquency or assessment, as well as additions thereto, and from allappurtenant civil, criminal, and administrative cases, and penalties.

16

The taxpayer shall be immune from all suits or actions, including the payment ofsaid delinquency or assessment, as well as additions thereto, and from allappurtenant civil, criminal, and administrative cases, and penalties.

Any notices of levy, attachments and/or warrants of garnishment issued againstthe taxpayer shall be set aside pursuant to a lifting of notice of levy/garnishmentduly issued by the BIR or its authorized representative.

16

IMMUNITIES AND PRIVILEGES

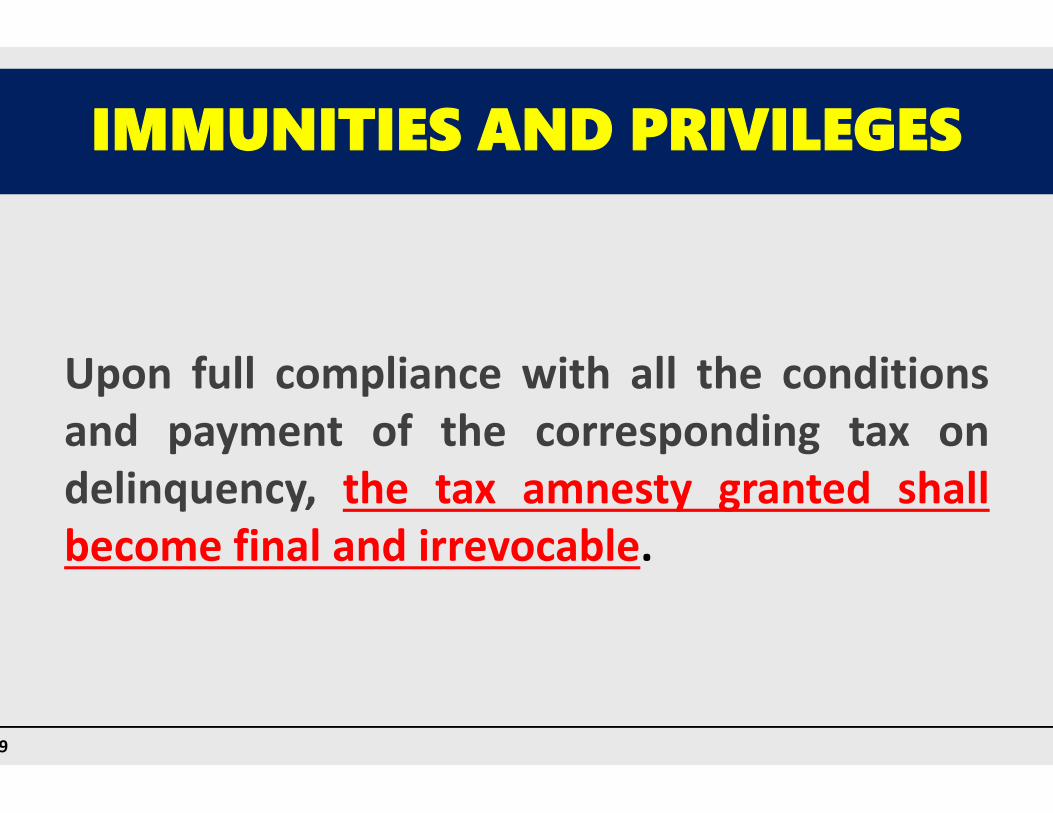

Upon full compliance with all the conditionsand payment of the corresponding tax ondelinquency, the tax amnesty granted shallbecome final and irrevocable.

17

Upon full compliance with all the conditionsand payment of the corresponding tax ondelinquency, the tax amnesty granted shallbecome final and irrevocable.

17RGI CPAs 2019

IMMUNITIES AND PRIVILEGES

Upon full compliance with all the conditionsand payment of the corresponding tax ondelinquency, the tax amnesty granted shallbecome final and irrevocable.

17

Upon full compliance with all the conditionsand payment of the corresponding tax ondelinquency, the tax amnesty granted shallbecome final and irrevocable.

17

ESTATE TAXESTATE TAXAMNESTYAMNESTY

18

ESTATE TAXESTATE TAXAMNESTYAMNESTY

18RGI CPAs 2019

ESTATE TAXESTATE TAXAMNESTYAMNESTY

18

ESTATE TAXESTATE TAXAMNESTYAMNESTY

18

Estate of decedents whodied on or before December31, 2017

Estate of decedents whodied on or before December31, 2017

19

COVERAGE

COVERAGE

Estate of decedents whodied on or before December31, 2017

Estate of decedents whodied on or before December31, 2017

19RGI CPAs 2019

COVERAGE

COVERAGE

Estate of decedents whodied on or before December31, 2017

Estate of decedents whodied on or before December31, 2017

19

Estate of decedents whodied on or before December31, 2017

Estate of decedents whodied on or before December31, 2017

19

20

with or without assessments duly issuedthereforwith or without assessments duly issuedtherefor

that have remained unpaid or have accrued asof December 31, 2017that have remained unpaid or have accrued asof December 31, 2017

COVERAGE

COVERAGE

20

that have remained unpaid or have accrued asof December 31, 2017that have remained unpaid or have accrued asof December 31, 2017

shall not cover persons or cases enumeratedunder Exceptionsshall not cover persons or cases enumeratedunder Exceptions

COVERAGE

COVERAGE

RGI CPAs 2019 20

with or without assessments duly issuedthereforwith or without assessments duly issuedtherefor

that have remained unpaid or have accrued asof December 31, 2017that have remained unpaid or have accrued asof December 31, 2017

20

that have remained unpaid or have accrued asof December 31, 2017that have remained unpaid or have accrued asof December 31, 2017

shall not cover persons or cases enumeratedunder Exceptionsshall not cover persons or cases enumeratedunder Exceptions

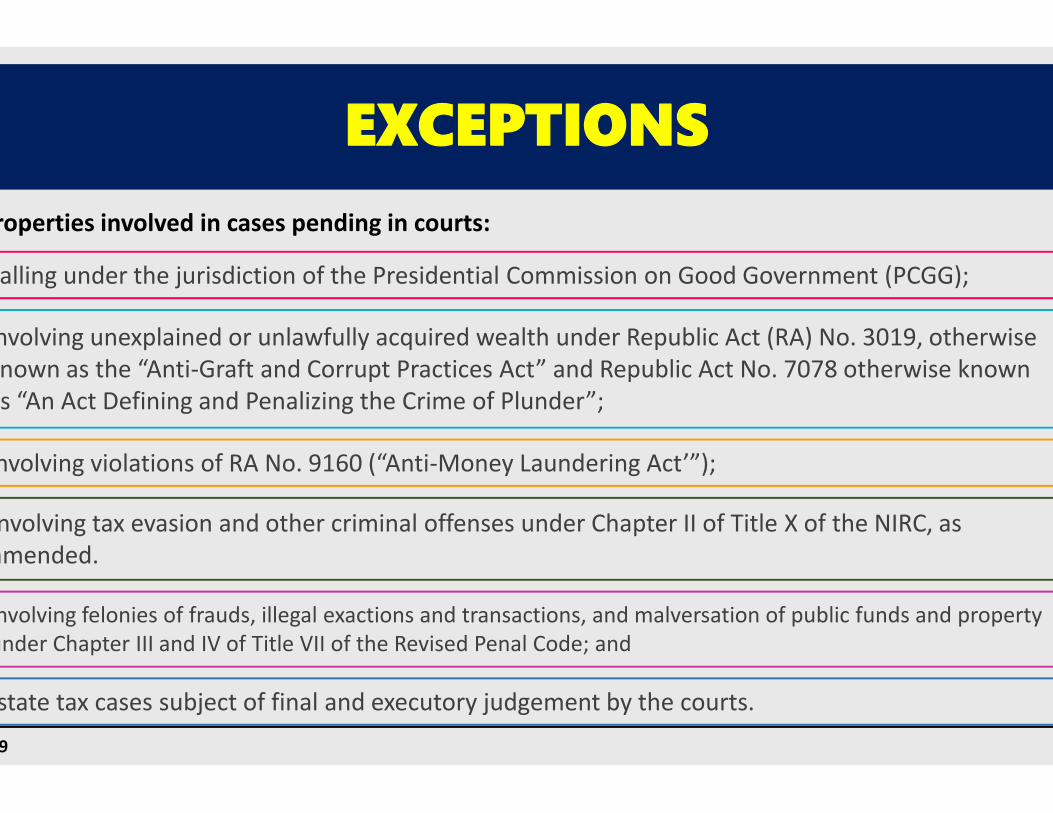

EXCEPTIONS

Falling under the jurisdiction of the Presidential Commission on Good Government (PCGG);

Involving unexplained or unlawfully acquired wealth under Republic Act (RA) No. 3019, otherwiseknown as the “Anti-Graft and Corrupt Practices Act” and Republic Act No. 7078 otherwise knownas “An Act Defining and Penalizing the Crime of Plunder”;

21

Properties involved in cases pending in courts:

Involving unexplained or unlawfully acquired wealth under Republic Act (RA) No. 3019, otherwiseknown as the “Anti-Graft and Corrupt Practices Act” and Republic Act No. 7078 otherwise knownas “An Act Defining and Penalizing the Crime of Plunder”;

Involving violations of RA No. 9160 (“Anti-Money Laundering Act’”);

Involving tax evasion and other criminal offenses under Chapter II of Title X of the NIRC, asamended.

Estate tax cases subject of final and executory judgement by the courts.21

Involving felonies of frauds, illegal exactions and transactions, and malversation of public funds and propertyunder Chapter III and IV of Title VII of the Revised Penal Code; and

RGI CPAs 2019

EXCEPTIONS

Falling under the jurisdiction of the Presidential Commission on Good Government (PCGG);

Involving unexplained or unlawfully acquired wealth under Republic Act (RA) No. 3019, otherwiseknown as the “Anti-Graft and Corrupt Practices Act” and Republic Act No. 7078 otherwise knownas “An Act Defining and Penalizing the Crime of Plunder”;

21

Involving unexplained or unlawfully acquired wealth under Republic Act (RA) No. 3019, otherwiseknown as the “Anti-Graft and Corrupt Practices Act” and Republic Act No. 7078 otherwise knownas “An Act Defining and Penalizing the Crime of Plunder”;

Involving violations of RA No. 9160 (“Anti-Money Laundering Act’”);

Involving tax evasion and other criminal offenses under Chapter II of Title X of the NIRC, asamended.

Estate tax cases subject of final and executory judgement by the courts.21

Involving felonies of frauds, illegal exactions and transactions, and malversation of public funds and propertyunder Chapter III and IV of Title VII of the Revised Penal Code; and

Within two (2) years from the effectivity of the IRR

Estate Tax Amnesty ReturnWHAT to File?

WHEN to File?

RESIDENT DECEDENT

22

RDO which has jurisdiction over the last residence ofthe decedent

Within two (2) years from the effectivity of the IRR

WHERE to File?

Submit “Paid” Estate Tax Amnesty Return, with alldocumentary requirements

HOW to File?

22RGI CPAs 2019

Within two (2) years from the effectivity of the IRR

Estate Tax Amnesty Return

RESIDENT DECEDENT

22

RDO which has jurisdiction over the last residence ofthe decedent

Within two (2) years from the effectivity of the IRR

Submit “Paid” Estate Tax Amnesty Return, with alldocumentary requirements

22

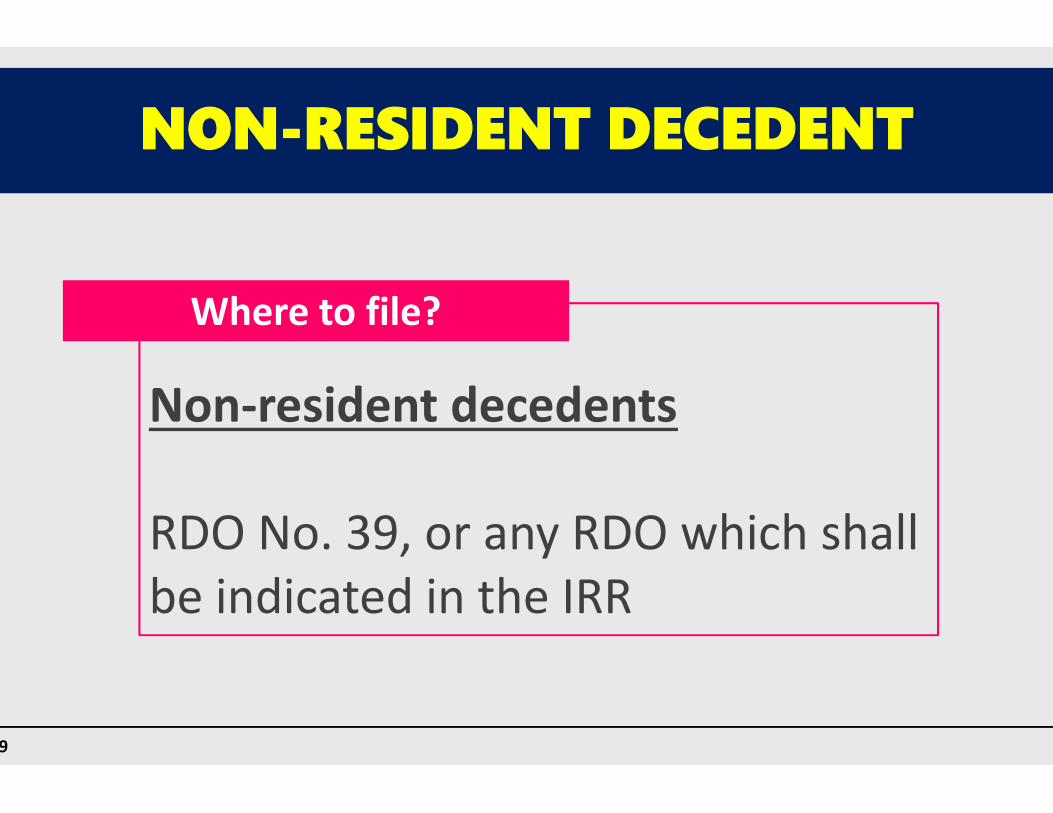

Non-resident decedents

RDO No. 39, or any RDO which shallbe indicated in the IRR

Where to file?

NON-RESIDENT DECEDENT

23

Non-resident decedents

RDO No. 39, or any RDO which shallbe indicated in the IRR

23RGI CPAs 2019

Non-resident decedents

RDO No. 39, or any RDO which shallbe indicated in the IRR

NON-RESIDENT DECEDENT

23

Non-resident decedents

RDO No. 39, or any RDO which shallbe indicated in the IRR

23

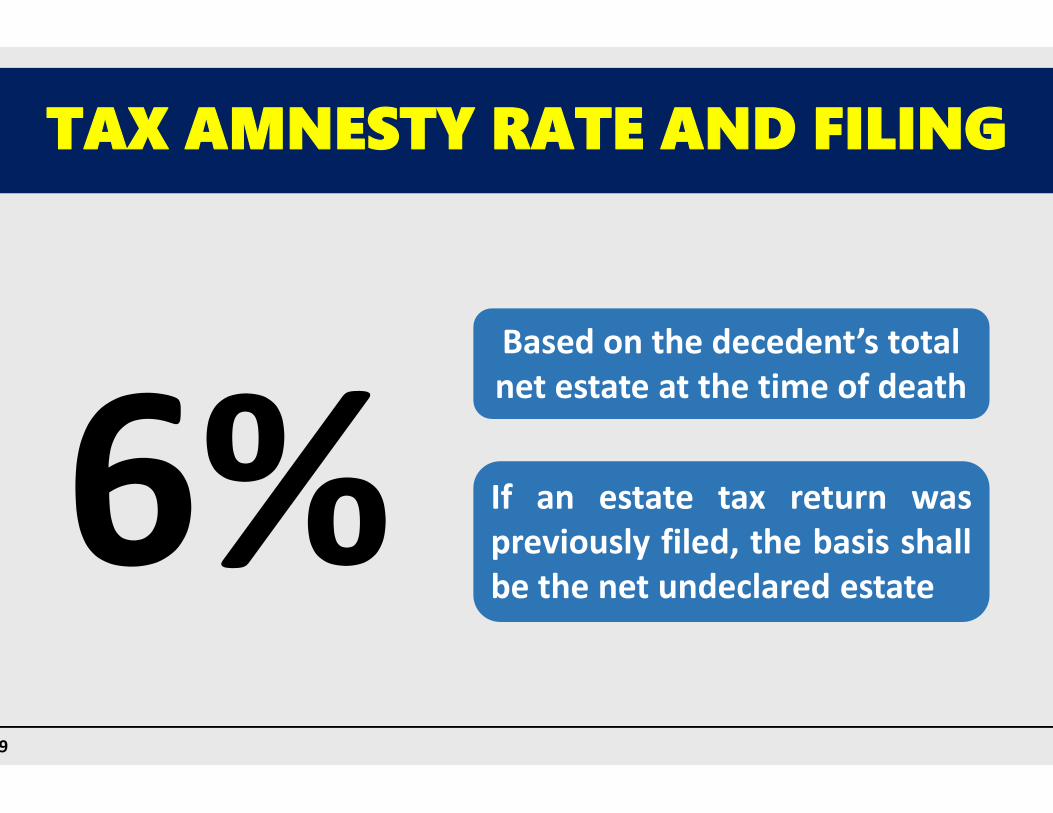

TAX AMNESTY RATE AND FILING

Based on the decedent’s totalnet estate at the time of death6%

24

Based on the decedent’s totalnet estate at the time of death

If an estate tax return waspreviously filed, the basis shallbe the net undeclared estate

6%24RGI CPAs 2019

TAX AMNESTY RATE AND FILING

Based on the decedent’s totalnet estate at the time of death6%

24

Based on the decedent’s totalnet estate at the time of death

If an estate tax return waspreviously filed, the basis shallbe the net undeclared estate

6%24

25

If the estate involved has properties whichare still in the name of another decedent ordonor, the heirs, executors or administratorsthereof shall file ALL the Estate Tax Amnesty

Returns

Note

ESTATE TAX AMNESTY

25

If the estate involved has properties whichare still in the name of another decedent ordonor, the heirs, executors or administratorsthereof shall file ALL the Estate Tax Amnesty

Returns

RGI CPAs 2019 25

If the estate involved has properties whichare still in the name of another decedent ordonor, the heirs, executors or administratorsthereof shall file ALL the Estate Tax Amnesty

Returns

ESTATE TAX AMNESTY

25

If the estate involved has properties whichare still in the name of another decedent ordonor, the heirs, executors or administratorsthereof shall file ALL the Estate Tax Amnesty

Returns

TAX AMNESTY RATE AND FILING

P 5,000

26

P 5,000Minimum Estate Tax Amnesty

26RGI CPAs 2019

TAX AMNESTY RATE AND FILING

P 5,000

26

P 5,000Minimum Estate Tax Amnesty

26

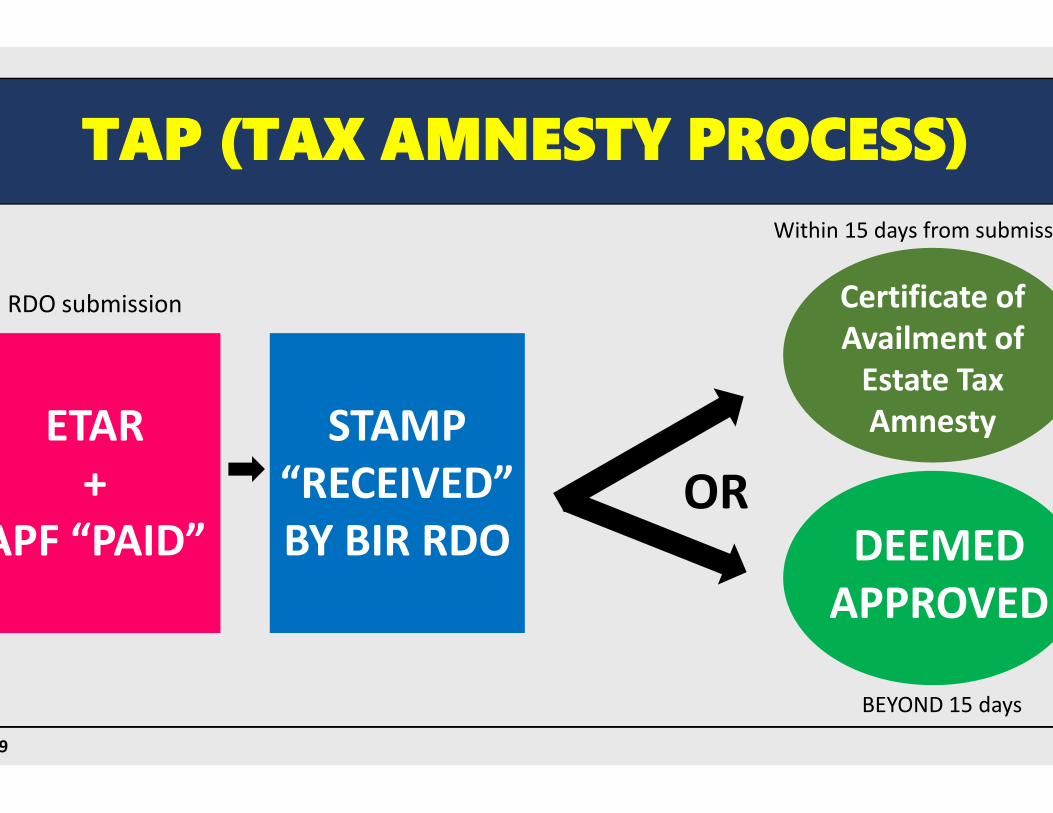

TAP (TAX AMNESTY PROCESS)

ETAR+

APF “PAID”

ETAR+

APF “PAID”

STAMP“RECEIVED”BY BIR RDO

STAMP“RECEIVED”BY BIR RDO

RDO submission

27

ETAR+

APF “PAID”

ETAR+

APF “PAID”

STAMP“RECEIVED”BY BIR RDO

STAMP“RECEIVED”BY BIR RDO

27RGI CPAs 2019

TAP (TAX AMNESTY PROCESS)

STAMP“RECEIVED”BY BIR RDO

STAMP“RECEIVED”BY BIR RDO

Within 15 days from submission

27

Certificate ofAvailment of

Estate TaxAmnestySTAMP

“RECEIVED”BY BIR RDO

STAMP“RECEIVED”BY BIR RDO

BEYOND 15 days27

Certificate ofAvailment of

Estate TaxAmnesty

DEEMEDAPPROVED

OR

ESTATE TAX AMNESTY POLICY

Without prejudice to compliance with applicable lawson succession as a mode of transfer, the Bureau ofInternal Revenue, in coordination with the applicableregulatory agencies, shall set up a system enabling thetransfer of title over properties to heirs and/orbeneficiaries and cash withdrawals from the bankaccounts of the decedent, when applicable.

28

Without prejudice to compliance with applicable lawson succession as a mode of transfer, the Bureau ofInternal Revenue, in coordination with the applicableregulatory agencies, shall set up a system enabling thetransfer of title over properties to heirs and/orbeneficiaries and cash withdrawals from the bankaccounts of the decedent, when applicable.

28RGI CPAs 2019

ESTATE TAX AMNESTY POLICY

Without prejudice to compliance with applicable lawson succession as a mode of transfer, the Bureau ofInternal Revenue, in coordination with the applicableregulatory agencies, shall set up a system enabling thetransfer of title over properties to heirs and/orbeneficiaries and cash withdrawals from the bankaccounts of the decedent, when applicable.

28

Without prejudice to compliance with applicable lawson succession as a mode of transfer, the Bureau ofInternal Revenue, in coordination with the applicableregulatory agencies, shall set up a system enabling thetransfer of title over properties to heirs and/orbeneficiaries and cash withdrawals from the bankaccounts of the decedent, when applicable.

28

29

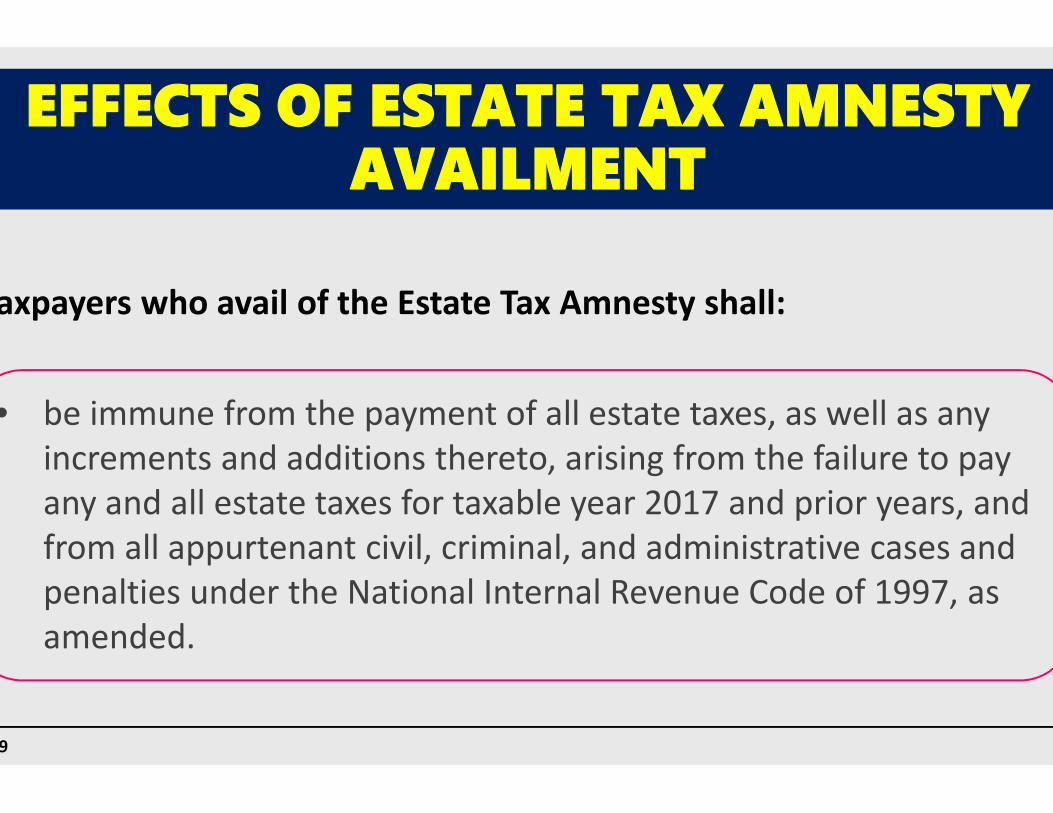

EFFECTS OF ESTATE TAX AMNESTYAVAILMENT

Taxpayers who avail of the Estate Tax Amnesty shall:

• be immune from the payment of all estate taxes, as well as anyincrements and additions thereto, arising from the failure to payany and all estate taxes for taxable year 2017 and prior years, andfrom all appurtenant civil, criminal, and administrative cases andpenalties under the National Internal Revenue Code of 1997, asamended.

29

• be immune from the payment of all estate taxes, as well as anyincrements and additions thereto, arising from the failure to payany and all estate taxes for taxable year 2017 and prior years, andfrom all appurtenant civil, criminal, and administrative cases andpenalties under the National Internal Revenue Code of 1997, asamended.

RGI CPAs 2019 29

EFFECTS OF ESTATE TAX AMNESTYAVAILMENT

Taxpayers who avail of the Estate Tax Amnesty shall:

• be immune from the payment of all estate taxes, as well as anyincrements and additions thereto, arising from the failure to payany and all estate taxes for taxable year 2017 and prior years, andfrom all appurtenant civil, criminal, and administrative cases andpenalties under the National Internal Revenue Code of 1997, asamended.

29

• be immune from the payment of all estate taxes, as well as anyincrements and additions thereto, arising from the failure to payany and all estate taxes for taxable year 2017 and prior years, andfrom all appurtenant civil, criminal, and administrative cases andpenalties under the National Internal Revenue Code of 1997, asamended.

CONFIDENTIALITYCONFIDENTIALITYAND NONAND NON--USEUSE

OF INFORMATIONOF INFORMATIONAND DATAAND DATA

AND AMENDMENTAND AMENDMENTTO THE STA/SALNTO THE STA/SALN

30

CONFIDENTIALITYCONFIDENTIALITYAND NONAND NON--USEUSE

OF INFORMATIONOF INFORMATIONAND DATAAND DATA

AND AMENDMENTAND AMENDMENTTO THE STA/SALNTO THE STA/SALN

30RGI CPAs 2019

CONFIDENTIALITYCONFIDENTIALITYAND NONAND NON--USEUSE

OF INFORMATIONOF INFORMATIONAND DATAAND DATA

AND AMENDMENTAND AMENDMENTTO THE STA/SALNTO THE STA/SALN

30

CONFIDENTIALITYCONFIDENTIALITYAND NONAND NON--USEUSE

OF INFORMATIONOF INFORMATIONAND DATAAND DATA

AND AMENDMENTAND AMENDMENTTO THE STA/SALNTO THE STA/SALN

30

CONFIDENTIALITY AND NON-USE OFINFORMATION AND DATA

Any information or data contained in, derived from orprovided by a taxpayer in the Tax Amnesty Return,Statement of Total Assets or Statement of Assets,Liabilities, and Networth, as the case may be andappurtenant documents shall be confidential in natureand shall not be used in any investigation or prosecutionbefore any judicial, quasi-judicial, and administrativebodies.

31

Any information or data contained in, derived from orprovided by a taxpayer in the Tax Amnesty Return,Statement of Total Assets or Statement of Assets,Liabilities, and Networth, as the case may be andappurtenant documents shall be confidential in natureand shall not be used in any investigation or prosecutionbefore any judicial, quasi-judicial, and administrativebodies.

31RGI CPAs 2019

CONFIDENTIALITY AND NON-USE OFINFORMATION AND DATA

Any information or data contained in, derived from orprovided by a taxpayer in the Tax Amnesty Return,Statement of Total Assets or Statement of Assets,Liabilities, and Networth, as the case may be andappurtenant documents shall be confidential in natureand shall not be used in any investigation or prosecutionbefore any judicial, quasi-judicial, and administrativebodies.

31

Any information or data contained in, derived from orprovided by a taxpayer in the Tax Amnesty Return,Statement of Total Assets or Statement of Assets,Liabilities, and Networth, as the case may be andappurtenant documents shall be confidential in natureand shall not be used in any investigation or prosecutionbefore any judicial, quasi-judicial, and administrativebodies.

31

Any SALN, financial statements, information sheets, andany such other statements or disclosures that may havebeen previously submitted by the taxpayer as requiredby existing laws are deemed to have been amended bythe Tax Amnesty Return and/or the STA or SALN, as thecase may be, and may not be the subject of anyinvestigation or prosecution or be used in anyinvestigation or prosecution before any judicial, quasi-judicial, and administrative bodies.

32

CONFIDENTIALITY AND NON-USE OFINFORMATION AND DATA

Any SALN, financial statements, information sheets, andany such other statements or disclosures that may havebeen previously submitted by the taxpayer as requiredby existing laws are deemed to have been amended bythe Tax Amnesty Return and/or the STA or SALN, as thecase may be, and may not be the subject of anyinvestigation or prosecution or be used in anyinvestigation or prosecution before any judicial, quasi-judicial, and administrative bodies.

32RGI CPAs 2019

Any SALN, financial statements, information sheets, andany such other statements or disclosures that may havebeen previously submitted by the taxpayer as requiredby existing laws are deemed to have been amended bythe Tax Amnesty Return and/or the STA or SALN, as thecase may be, and may not be the subject of anyinvestigation or prosecution or be used in anyinvestigation or prosecution before any judicial, quasi-judicial, and administrative bodies.

32

CONFIDENTIALITY AND NON-USE OFINFORMATION AND DATA

Any SALN, financial statements, information sheets, andany such other statements or disclosures that may havebeen previously submitted by the taxpayer as requiredby existing laws are deemed to have been amended bythe Tax Amnesty Return and/or the STA or SALN, as thecase may be, and may not be the subject of anyinvestigation or prosecution or be used in anyinvestigation or prosecution before any judicial, quasi-judicial, and administrative bodies.

32

TTHHAANNKK YYOOUU!!

33

TTHHAANNKK YYOOUU!!

33RGI CPAs 2019

TTHHAANNKK YYOOUU!!

33

TTHHAANNKK YYOOUU!!

33

![Service Tax Voluntary Compliance Encouragement Scheme, 2013 [Chapter VI of Finance Act, 2013] Amnesty Scheme – Updated with Department Clarification.](https://static.fdocuments.us/doc/165x107/56649dde5503460f94ad6daa/service-tax-voluntary-compliance-encouragement-scheme-2013-chapter-vi-of.jpg)