TAX AGENTS SEMINAR Fazrul Rahman Acting General Manager ... · TAX AGENTS SEMINAR Fazrul Rahman...

17

TAX AGENTS SEMINAR Fazrul Rahman Acting General Manager Taxation FRCA

-

Upload

truonglien -

Category

Documents

-

view

223 -

download

3

Transcript of TAX AGENTS SEMINAR Fazrul Rahman Acting General Manager ... · TAX AGENTS SEMINAR Fazrul Rahman...

TAX AGENTS SEMINAR

Fazrul Rahman Acting General Manager Taxation

FRCA

Objective

The objectives of this presentation are to provide an overview of tax policy reforms and explain policy intentions behind the new Income Tax Act.

• Balance between: • “Economic Efficiency”; and

• Maximum Revenue vs Minimum Welfare Loss • Non-distortionary effect

• “Equity” principles • Vertical Equity and • Horizontal Equity

• Supported by Simple administration • Clarity in law • Simple processes

• Achieves neutrality in taxation

What is an effective Tax Policy?

• Broadly, • Fiji’s tax policy reforms is consistent with best global practice • Fiji has adopted a low rate and broad based taxation • Fiji has adopted pro growth tax policies • Fiji has eliminated discrimination in tax treatments across different tax

bases • Fiji has moved toward indirect taxation as the primary source of revenue • Over the last 5 years, Fiji has modernized its tax administration with a

new: • a tax administration law from 2010; • A new Income Tax Act from 2016 • A simple Personal Income Tax system (ie, PAYE AS a final tax) • A simple dividend tax system from 2016

• Fiji has adopted solid and modern tax compliance laws

Fiji’s Tax Policy Experience?

• An OECD Study [Tax Policy Reform and Economic Growth (2010)] has found:

• A growth oriented tax reform will shift part of the tax burden from income to consumption; and

• Corporate Taxes are most harmful to growth, followed by Personal Income Tax and then Consumption Tax, with recurrent tax on immovable property being least harmful to growth.

What is an effective Tax Policy?

0

1,000,000,000

2,000,000,000

3,000,000,000

4,000,000,000

5,000,000,000

6,000,000,000

7,000,000,000

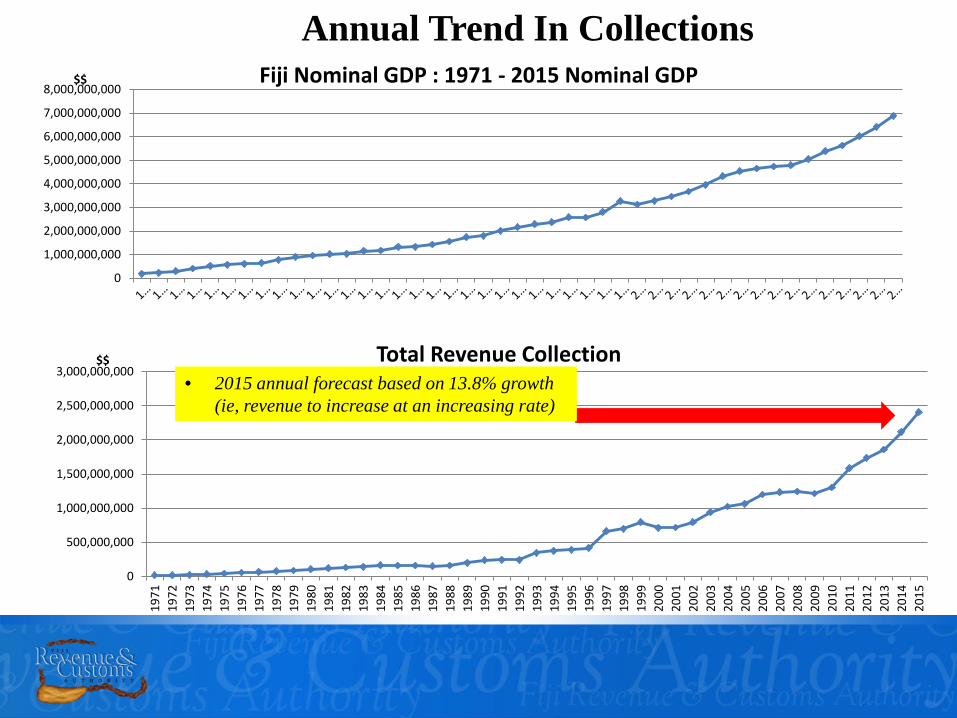

8,000,000,000$$ Fiji Nominal GDP : 1971 - 2015 Nominal GDP

0

500,000,000

1,000,000,000

1,500,000,000

2,000,000,000

2,500,000,000

3,000,000,000

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

$$ Total Revenue Collection

Annual Trend In Collections

• 2015 annual forecast based on 13.8% growth (ie, revenue to increase at an increasing rate)

YEAR Income Tax VAT Customs Others Total 1982 58.2 41.8 100 1992 44.6 16.5 38.9 - 100 1993 36.5 29.3 34.2 - 100 2002 34.1 34.8 31.1 - 100 2010 32.7 38.0 26.9 2.4 100 2012 27.3 38.7 21.2 12.8 100

Fiji Tax Trends (10 year intervals)

Tax Mix (last 15 years)

Income Tax

40.3%

VAT 29.2%

Trade 30.5%

Revenue Mix 2000

Income Tax 31%

VAT 40%

Trade Taxes 29%

Revenue Mix 2004

21%

37% 24%

3% 6% 2% 7%

Re venue Mix 2015

Income Tax VAT Trade Taxes

STT Departure tax Resouce Tax

Others

20%

Global average: 30.6%

0%

10%

20%

30%

40%

50%

60%

70%

Finl

and

Japa

nN

orw

ayIc

elan

dA

ustra

liaU

nite

d K

ingd

omZi

mba

bwe

Luxe

mbo

rgM

ali

Sout

h A

fric

aSw

itzer

land

Kor

ea (S

outh

)A

rgen

tina

Bar

bado

sIn

dia

New

Zea

land

Indo

nesi

aM

exic

oC

anad

aB

razi

lSa

moa

Nig

eria

Fiji

Sing

apor

eTo

nga

Ukr

aine

Mau

ritiu

sY

emen

Jord

anTi

mor

Les

teK

azah

ksta

nM

onte

negr

oG

uate

mal

a

Personal Income Tax Rate

• Tax system is made truly progressive

Personal Income Tax

Chargeable Income Tax Payable 1992

0 -4,500 Nil

4,501 – 7,000 Nil + 15% of excess of $4,500

7,001 – 15,000 375 + 25% of excess of $7,000

15,001 2,375 + 35% of excess of $15,000

Chargeable Income ($) Tax Payable 2011

0-15,000 Nil 15,001-15,600 Nil + 15% of excess of $4,500 15,601-22,000 375 + 25% of excess of $7,000

22,001+ 2,375 + 35% of excess of $15,000

2014 Tax Table

Fiji’s Tax Policy Experience?

Chargeable Income ($) PAYE Tax Payable ($) Social Responsibility Tax (SRT) Payable

0-16,000 Nil

16,001 – 22,000 7% of excess over $16,000

22,001– 50,000 420 +18% of excess over $22,000

50,001 – 270,000 5,460 +20% of excess over $50,000

270,001 - 300,000 49,460 + 20% of excess over $270,000 23% of excess over $270,000

300,001 - 350,000 55,460 +20% of excess over $300,000 6,900 + 24% of excess over $300,000

350,001 - 400,000 65,460 + 20% of excess over $350,000 18,900 + 25% of excess over $350,000

400,001 - 450,000 75,460 + 20% of excess over $400,000 31,400 + 26% of excess over $400,000

450,001 – 500,000 85,460 + 20% of excess over $450,000 44,400 + 27% of excess over $450,000

500, 001 – 1,000,000 95,460 + 20% of excess over $500,000 57,900 + 28% of excess over $500,000

1,000,001 + 195,460 + 20% of excess over $1,000,000 197,900 + 29% of excess over $1,000,000

• What has changed? Tax threshold increased by more than 3 fold and SRT applies on high income.

Fiji’s Tax Policy Experience?

0.00%5.00%

10.00%15.00%20.00%25.00%30.00%35.00%40.00%45.00%50.00%

1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Resident Corporate Income Tax rate Resident Personal Income Tax rate

0

2000

4000

6000

8000

10000

12000

14000

16000

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Income Tax Exemption Threshold ($)

• Tax Rates Coming Down

• Income Tax Exemption Threshold going up

20%

Global Average: 24%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Uni

ted

Stat

esJa

pan

Arg

entin

aSu

dan

Zam

bia

Sint

Maa

rten

Ven

ezue

laIn

dia

Fran

ceIta

lyA

ustra

liaM

ali

Mex

ico

Nig

eria

New

Zea

land

Sout

h A

fric

aSr

i Lan

kaSa

moa

Can

ada

Zim

babw

eB

arba

dos

Bra

zil

Indo

nesi

aTo

nga

Indo

nesi

aK

orea

(Sou

th)

Uni

ted

Kin

gdom Fi

jiSw

itzer

land

Sing

apor

eR

oman

iaM

aurit

ius

Tim

or L

este

Qat

arPa

raqu

ay

Corporate Tax Rate

14

Year Tariff Structure Bands

2009 - 2012 0, 5%,15%,32% 4

2008 0,5%,15%,27% 4

2006 & 2007 0,3%,15%,27% 4

2005 0%,3%,15%,27% 4

2004 0%, 3%, 15%, 27% 4

2003 0%, 3%, 10%, 15%, 20%, 27% 6

2002 0%, 3%, 10%, 15%, 20%, 27% 6

2001 0%, 3%, 10%, 15%, 20%, 27% 6

2000 0%, 10%, 15%, 27% 4

1999 0%, 10%, 15%, 27% 4

1998 0% 10%, 20%, 22.5%, 35%, 60%, 75% Note: Due to Devaluation, the bands were temporarily restructured as follows:-

0%, 9.5%, 15%, 30%, 45%, 62%

7 6

1997 0%, 10%, 22.5%, 35%, 60%,75% 6

1996 0%, 5%, 10%, 15%, 17.5%, 22.5%, 30%, 35%, 50%, 60% 10

1995 0%, 10%, 20%, 22.5%, 60%, 80% 6

1994 0%,5%, 10%, 20%, 25%, 65%, 35%, 30%, 25%, 10%, 50%, 60%, 80% 13

1993 0%,5%,7.5%, 10%, 25%, 65%, 35%, 30%, 25%, 10%, 60%, 100% 11

1992 0%, 5%, 7.5%, 10%, 15%, 20%, 25%, 30, 35%, 70%, 75% 11

1991 0%,5%,7.5%, 10%, 25%, 30%, 40%, 50% 6

1990 0%,5%,7.5%, 15%,20%,25%, 30%,40%, 50%,60%,80%,190% 12

1989 0%,5%, 7.5%,10%,15%, 20%,25%,30%,35%,40%,45%,50%,55%, 60%,70%,80%90%,200%, 18

1988 0%, 7.5%, 20%,25%,30%,35%,40%, 50%,60%,80%,70%,75%,185% 13

• Tax Administration Decree • First part of legislative reform • Harmonized the administrative provisions

• New Income Tax Act • Second part of the legislative reform • A rewrite of the substantive provision • A simple single tax code covering income tax, capital gains tax

and fringe benefits tax with harmonized rules • Based on modern drafting language

Fiji’s Tax Policy Experience?

• New Income Tax Act • Supports both domestic and foreign investment with clear rules

• Internalized the foreign tax credit • Clear source and residency rules • Closer alignment with treaty rules such as PE • Depreciation options • Amortization on intangibles deductions allowed • Mining Provisions

• Supports SMEs • Presumptive tax regime

• Improves tax compliance • Thin capitalization • Transfer Pricing rules • Trust rules

Fiji’s Tax Policy Experience?

Thank You