Taunton & S Somerset viab · Affordable Housing Site Viability Study Page ii 8. The sites were...

157

Taunton & South Somerset Housing Market Areas Strategic Housing Land Viability Assessment February 2009 Final Report

Transcript of Taunton & S Somerset viab · Affordable Housing Site Viability Study Page ii 8. The sites were...

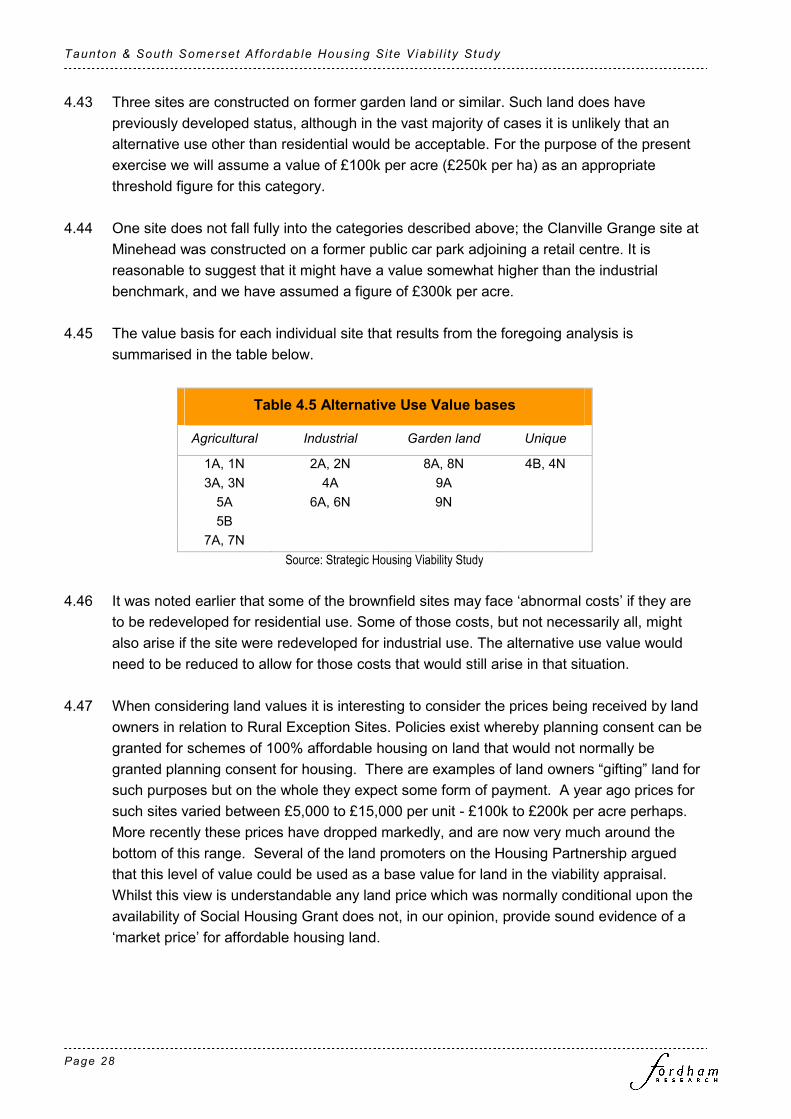

Taunton & South Somerset

Housing Market Areas

Strategic Housing Land

Viability Assessment

February 2009

Final Report

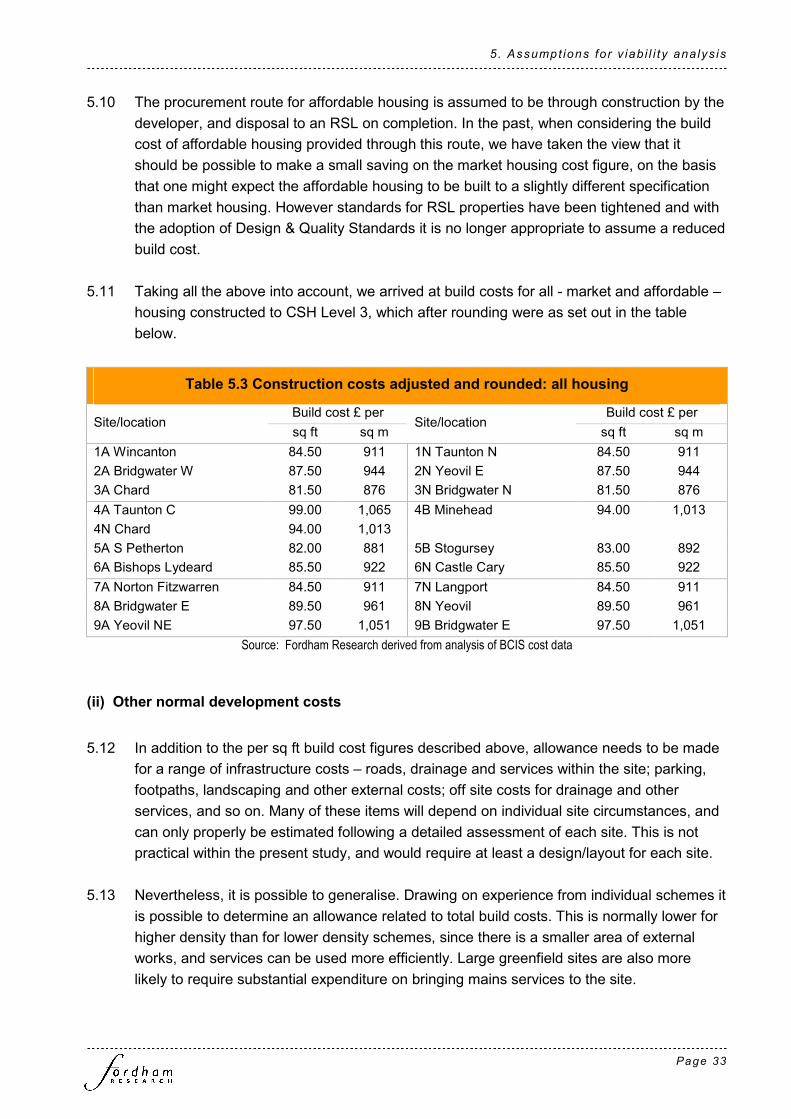

Execut ive Summary

Page i

Executive Summary

1. Fordham Research was commissioned by the four Councils to carry out a study of

affordable housing viability in the two Housing Market Areas (HMAs) of Taunton & South

Somerset. The viability study formed part of a wider Strategic Housing Market Assessment

for these areas. It was intended to inform ongoing work on the preparation of Local

Development Frameworks, by examining the impact on housing viability of alternative

levels of affordable housing requirement.

2. The study involved preparing financial appraisals for a number of actual (permitted or

proposed) and notional housing sites in the two HMAs. The appraisals were designed to

assess the impact on development viability of alternative requirements for affordable

housing provision. Viability would be examined for a range of sites in a variety of

development situations. A ‘modelling’ approach was taken, using bespoke spreadsheet

software.

3. In discussions the four Councils had developed a nine-category site typology. Using this

they identified a combination of twelve ‘actual’ sites together with seven notional sites

(identical to an actual site but located elsewhere), for testing. The sites ranged in size from

two to 300+ dwellings.

4. Of the actual sites, eight had been permitted and reached construction stage; three others

were permitted or otherwise resolved to permit. An application for the remaining site was

expected imminently. Reflecting the selection typology, the sites were a mixture of

greenfield, and previously developed land.

5. The twelve actual sites provided just over 800 dwellings, at densities ranging from 20 to

104 dwellings per ha.

6. All of the actual sites (except one) were subject to a comparatively recent planning

application, the details of the development proposals were used in carrying out appraisals.

For the site with no application, a schedule of proposed accommodation which had been

made available in advance was used.

7. The development proposals provide for a considerable mixture of development types and

situations. We normally find that development densities (measured in terms of sq ft per acre

or sq m per ha point to a ‘baseline’ urban density of around 15,000-15,500 sq ft per acre

(3,450-3,550 sq m per ha). In fact, three of the actual sites produce densities in this range;

three more rural/edge of town sites have densities a little below this range, and five a little

above; one site has a significantly higher, inner urban density reflecting a three storey

apartment built form.

Affordable Hous ing Si te Viab i l i ty Study

Page ii

8. The sites were tested with no affordable housing, and for options of 15%, 30%, and 45%

affordable housing. In each case the affordable housing was assumed to be a combination

of social rented and intermediate housing; options for a 60/40 split and 80/20 split were

both tested. The intermediate housing was expected to achieve the target outgoings for

intermediate housing being proposed in the parallel SHMA study.

9. The affordable housing was to be provided on the basis of zero Social Housing Grant.

Advice was sought from Councils’ partner RSLs about appropriate selling prices with zero

grant. We also considered appropriate levels for the total cost of other planning gain

contributions which might apply for each of the sites, using a combination of the actual

contributions secured or sought - where available - and an assessment of what might be

sought today. As an alternative to this approach we also considered a tariff type approach,

with the overall figure being set at two levels of £13,000 and £20,000 per dwelling

respectively.

10. The local market for residential development was examined. There is a fair supply of

newbuild housing across the area as a whole. Prices vary quite widely within the area,

being highest in some of the smaller towns and villages, and lowest in all or parts of the

main towns. Prices in the most expensive areas are more than half again of those in the

cheapest. Taking into account current selling prices on schemes across the Market Area,

we determined price levels for flats and houses on each site.

11. We also looked at evidence in respect of land values for appropriate alternative uses for the

sites.

12. We considered assumptions in respect of development costs and the other financial and

site assumptions required to carry out appraisals. Abnormal costs were expected to arise

on several sites. Appropriate assumptions to determine the building programme for each

site were determined.

13. Appraisals for each site were produced in respect of all of the affordable options. They used

a bespoke spreadsheet based financial analysis package. The approach was to determine

the residual land value, i.e. what value the site would have after taking into account the

costs of development, the likely income from sales and/or rents, and an appropriate amount

of developer’s profit. In order for the proposed development to be viable, the residual value

must exceed the value from a valid alternative use.

14. The appraisals showed that with no requirement for affordable housing, the sites delivered

land values between about £100k and £1.2 m per acre (£250k-£3.0m per ha). These

results were somewhat below what VOA published data and information on locally available

small plots suggested local values for ‘oven ready’ land would be. The appraisals are

therefore felt much more likely to present a ‘worst case’ than to be unduly optimistic.

Execut ive Summary

Page iii

15. As increasing amounts of affordable housing are introduced, the land value falls away.

About half of the sites still achieved a positive land value with the highest requirement of

45% affordable housing. However on some sites, those with highest densities, land value

falls away much more quickly as the affordable contribution increases. On such sites the

land value, the main source of the affordable contribution, is a much lower proportion of the

scheme’s total cost. Since land value is the main means of providing ‘developer subsidy,’

this means that it cannot go as far on high density schemes as with a low density

development.

16. Whether each individual option produces a viable outcome will depend on the land value

from alternative uses. For the identified sites the alternative use was normally either

industrial, agricultural or garden land. Of these, industrial use was assumed to have the

highest alternative use value, ranging from £285k per acre (£600k per ha) in the three

larger towns down to £175k per acre (£430k per ha) in the two smaller settlements where it

applied. Agricultural use was the least valuable at £25k per ha/£10k per acre. Unused

garden land was assumed to be worth £100k per acre (£250k per ha). One site, a former

car park, was assumed to have a comparatively high existing use value of £300k per acre

(£750k per ha).

17. This information, adjusted for any abnormal development costs that would still arise in the

alternative use, was used to deduce whether the individual sites were viable at different

levels of affordable housing provision. The results showed that one notional site was

unviable even with 100% market housing. Of the 19 sites i.e. including the latter, 13 could

produce 15% affordable housing and remain viable, plus two which were classed as

marginal because although there was a surplus over alternative use value, this did not

provide a sufficient ‘cushion’ to bring the site forward. At 30% this and two additional sites

became unviable, and one more became marginal. By 45%, only four sites remained viable

(plus four marginals).

18. Alternative appraisals were prepared assuming developer contributions at £13k and £20k

per dwelling. The greater financial burden these imposed impacted on viability, particularly

for the smaller sites; with the lower rate only six sites were fully viable at 30% affordable,

falling to five for the higher rate.

19. Councils will need to consider these findings carefully in formulating policy targets in

emerging Local Development Documents. Their impact is considered further in Chapter 29

of the main SHMA study, where practical proposals for appropriate targets are set out.

20. Stakeholders contributed to the production of the study, and their contribution was

invaluable. There were disagreements in some areas and where this was so, we have

endeavoured to highlight the issue. A key area of disagreement was with how much

account should be taken of the costs of bringing land forward for development, which under

the former Local Plan system could at times be quite considerable.

Affordable Hous ing Si te Viab i l i ty Study

Page iv

Table of Con tents

Page i

TABLE OF CONTENTS

Executive Summary ........................................................................................................... i

List of abbreviations ........................................................................................................ iii

Preamble ............................................................................................................................1

1. Introduction....................................................................................................................3

National guidance ....................................................................................................................................... 3

Housing market downturn........................................................................................................................... 4

Fordham Research ..................................................................................................................................... 5

Structure of this report ................................................................................................................................ 5

2. Individual development sites........................................................................................7

Introduction ................................................................................................................................................. 7

Two market areas ....................................................................................................................................... 7

Identifying a range of sites.......................................................................................................................... 7

The actual sites........................................................................................................................................... 9

Development assumptions ....................................................................................................................... 11

3. Affordable housing and other developer contributions...........................................13

Introduction ............................................................................................................................................... 13

Affordable housing assumptions............................................................................................................... 13

Other developer contributions................................................................................................................... 17

4. Local market conditions .............................................................................................19

Introduction ............................................................................................................................................... 19

Issues to consider ..................................................................................................................................... 19

The residential market .............................................................................................................................. 20

Price assumptions for financial appraisals ............................................................................................... 23

Land values............................................................................................................................................... 24

Current and alternative use values ........................................................................................................... 26

5. Assumptions for viability analysis.............................................................................31

Introduction ............................................................................................................................................... 31

Development costs ................................................................................................................................... 31

Financial and other appraisal assumptions .............................................................................................. 35

Site acquisition and disposal costs ........................................................................................................... 37

Alternative use value comparison............................................................................................................. 38

Affordable Hous ing Si te Viab i l i ty Study

Page ii

6. Results of viability analysis........................................................................................39

Introduction ............................................................................................................................................... 39

Financial appraisal approach and assumptions ....................................................................................... 39

Appraisal results: ...................................................................................................................................... 39

Alternative use benchmarks ..................................................................................................................... 41

Comparison results ................................................................................................................................... 45

Community Infrastructure Levy................................................................................................................. 47

7. Implications of results.................................................................................................49

Our approach ............................................................................................................................................ 49

Implications of appraisal results................................................................................................................ 50

Individual Council areas: guidance ........................................................................................................... 52

Appendices ......................................................................................................................53

Appendix 1. Newbuild schemes .....................................................................................55

Appendix 2. House price variations...............................................................................59

Appendix 3. Additional appraisals : 35% target............................................................63

Appendix 4. Variant appraisals : community infrastructure levy ................................65

Appendix 5. Financial appraisal summaries .................................................................69

Lis t o f abbrev ia t ions

Page i i i

List of abbreviations

£ k thousand pounds

£ m million pounds

dw dwelling

dwgs dwellings

ft foot

ha hectare

m metre

Q1 Quarter 1

sq square

Preamble

Page 1

Preamble

1. It is a requirement of Planning Policy Statement 3 (PPS3) that a target is set for the proportion

of affordable housing to be delivered through new developments. This target should reflect not

only the need for affordable housing but also the impact on the viability of new development of

including affordable housing. This study responds to that requirement. It uses a methodological

approach which is easily ‘updatable’, allowing the targets to be periodically revisited and

reviewed.

2. This work is part of a wider study, Strategic Housing Market Assessments (SHMAs) for the two

housing market areas of Taunton & South Somerset. The SHMAs will now provide input into

ongoing work on preparation of Local Development Frameworks for each of the Districts.

3. Based on an assessment of the balance between the need for market housing and the need for

affordable housing, the SHMAs found the levels of need suggested targets for the amounts of

affordable housing to be provided in new projects of around 35% in the South Somerset

Housing Market Area (HMA) and 40% in the Taunton HMA. However, these targets do not take

account of the commercial factors of what it is viable and realistic for developers to be asked to

provide. The 35% and 40% targets are the correct targets to balance the overall housing

market over time – but may not be the appropriate targets now.

4. The purpose of this viability study is to enable the councils to set robust targets for affordable

housing policy which reflect current commercial circumstances. It is important to note that the

actual amount of affordable housing to be achieved on any specific site must be assessed for

that actual site, and will take into the particular factors of developing that site at that point of the

economic cycle. Any such assessment will not only take into account the normal costs of

developing that site (including on one hand S106 and Community Infrastructure Levy (CIL)

payments and on the other the availability of grants and subsidies), but also the abnormal costs

(such as off-site highways works etc).

5. The availability and cost of land is at the core of the viability of any development of new

houses. The fact that a developer has ‘over paid’ for a site will not excuse them from providing

affordable housing – and likewise the fact that they have underpaid will not require him to

provide more. It has been recognised by stakeholders that in the current development and

planning regime the cost of meeting S106 requirements and the provision of affordable housing

is a factor in development appraisals and does impact on land values.

Taunton & South Somerset Af fordable Hous ing Si te Viab i l i ty Study

Page 2

6. This study is to inform the setting the current target in a robust way. Since the work was first

commissioned, it has become clear that the targets which are set in Local Development

Frameworks (LDFs) will need to be reviewed regularly to reflect changes in the general viability

of development. The housing market has declined markedly since early 2008, and continues to

do so, which makes it absolutely essential that the findings are regularly reviewed. At the

conclusion of the study the financial software package is to be made available to the four

Councils, with training. This will enable the study results to be reviewed and updated regularly,

in house, so as to ensure ongoing support for the emerging and eventual plan policies.

7. We would like to take this opportunity to thank all the stakeholders that have contributed to this

report (and the SHMA process generally). During the preparation of this report a wide range of

views were expressed. The contribution of all stakeholders, especially the house builders has

been invaluable. Where agreement was not reached on substantive points we have made a

judgement, and highlighted the various views expressed. Agreement was reached on all points

other than around that of land prices used in the viability study where differences remain over

how much account should be taken of the costs of promoting, assembling and bringing land

forward for development. It has not been possible to reach agreement on several substantive

matters affecting viability and in these cases the text of this report represents the Fordham

Research’s considered opinion. We have identified these areas of disagreement in the text of

the report.

8. Part of the reason for the diversity of views in this area is due to the change from the old local

plan system to the new Local Development Framework system. We acknowledge that in the

past the business of promoting land through the local plan system could often be protracted

and expensive. The new LDF system is less complicated, and whilst the costs of land

assembly will remain, the costs – and therefore the risks – of promoting will be substantially

less. We have taken the view that it is correct to base this study on the LDF system rather than

the historic local plan system. Several land promoters in the Partnership expressed the view

that this assumption had yet to be proved. They pointed out that all previous changes to the

Planning System, ostensibly made with the intention of speeding the process and reducing

costs for applicants, had actually had the opposite effect, and they contend that there is no

basis for the assumption made.

1. In t roduct ion

Page 3

1. Introduction

1.1 Fordham Research was commissioned by the four Councils in April 2008, to produce

guidance on the financial viability implications of alternative targets and size thresholds for

affordable housing provision within the combined area. This study is structured so as to be

easily updatable so to allow the targets to be periodically revised.

1.2 This work formed part of a wider study, Strategic Housing Market Assessments (SHMAs)

for the two housing market areas of Taunton & South Somerset. The SHMAs were being

carried out in parallel, to develop an understanding of local housing markets in this sub-

region, to build a picture of housing needs and requirements, and to suggest appropriate

targets for housing provision based on this analysis. The SHMAs will provide input into

ongoing work on preparation of Local Development Frameworks for each of the Districts.

1.3 The viability study will ensure that advice on targets in the main SHMAs are supported by

rigorous analysis showing that the targets can be achieved without undermining site

viability and imperilling the delivery of housing provision overall. Like the main study, it is

being produced with the benefit of involvement from stakeholders.

1.4 This study is to inform the setting the current target in a robust way. This target will need to

be reviewed regularly to reflect changes in the profitability of development. The housing

market has declined markedly during the period of this study – and continues to do so, it is

therefore essential that the findings are regularly reviewed.

National guidance

1.5 Guidance on affordable housing policy issues is now provided by PPS3.

1.6 Whilst from 2000 onwards the earlier guidance, Planning Policy Guidance 3 (PPG3),

recognised the need to take into account the economics of development when setting

affordable housing targets and negotiating contributions from developers, PPS3 further

reinforces this message. It suggests that Local Development Documents (LDDs) should set

an overall target for the amount of affordable housing to be provided, which should:

‘&.reflect an assessment of the likely economic viability of land for housing within the area,

taking account of the risks to delivery and drawing on informed assessments of the likely

levels of finance available for affordable housing, including public subsidy and the level of

developer contribution that can reasonably be secured.’ (S29)

Taunton & South Somerset Af fordable Hous ing Si te Viab i l i ty Study

Page 4

1.7 LDDs should also set out the range of circumstances in which affordable housing will be

required. The national indicative minimum size threshold is to be 15 dwellings However,

Local Planning Authorities (LPAs) may:

‘&set lower minimum thresholds, where viable and practicable, including in rural areas.

This could include setting different proportions of affordable housing to be sought for a

series of site-size thresholds over the plan area. LPAs will need to undertake an informed

assessment of the economic viability of any thresholds and proportions of affordable

housing proposed&.’ (S29)

1.8 The analysis in the present study is designed to be consistent with the above requirements.

However it also needs to address the particular implications of the dramatic downturn in the

housing market that set in from early 2008.

Housing market downturn

1.9 The normal approach in a viability study of this kind is to prepare financial appraisals for a

range of sites representative of development in the area as a whole, testing varying

alternative levels of affordable housing provision. The work would involve deciding what

form of development would be expected on each site; as is conventional with such

appraisals, they would use current figures for build costs and house prices, making

sensible assumptions about other developer contributions(‘planning gain’), and a variety of

other technical matters.

1.10 By the spring of 2008 it had become clear that the onset of a ‘credit crunch’, which

emerged during the previous autumn, had triggered a serious downturn in the housing

market. A severe reduction in the availability of mortgages led to a reduction in prices,

which have impacted in turn on purchaser confidence. At the time of calculating the

information for this report, July 2008, it has become clear that, after a very long interval in

historical terms, during which house prices have been rising almost continuously, we have

now entered a period of adjustment. A similar adjustment was precipitated in the early 90s,

after rapid price rises in the period 1986-89. During that previous adjustment house prices

fell back considerably over a number of years. However at that time significant economic

problems, and historically high interest rates, contributed to the need for a very substantial

price adjustment.

1.11 The trigger for the present conditions within the housing market lay outside the housing

market. The underlying demand/supply relationship remains, with an increasing need for

more homes due to demographic changes, so it is more than likely that growth will return to

the market at some time in the future. As and when that will be, and to what extent, are not

a matter for this study. As prices appear still to be falling, and it is not possible to

determine where or when they might stabilise, a study based on today’s prices only, is

going to be of limited use and will require regular review.

1. In t roduct ion

Page 5

1.12 We have considered whether the proposed study approach should be modified to take

account of this unusual situation. Clearly, continued and regular monitoring of the

development situation will be required. Fortunately, the existing agreed arrangement to

pass the appraisal software to the Councils at the end of the study will conveniently provide

for this to happen. However, it will be necessary to subject appraisals to price sensitivity

tests, and to frame policy advice from an appropriate starting point in price terms.

Fordham Research

1.13 Fordham Research has been providing advice to Councils in respect of planning gain and

development viability since the late 1980s. The firm’s approach throughout this time has

involved the preparation of financial appraisals. Over the last few years in particular,

Councils have increasingly commissioned the firm to evaluate financial appraisals which

have been prepared by developers in order to support a case for a reduced affordable

housing contribution, for enabling development, and so on.

1.14 Since 1993 Fordham Research has become a leading consultancy in carrying out Housing

Needs Surveys (and more recently the more wide ranging Strategic Housing Market

Assessments that have largely replaced them) and advising Councils on affordable housing

policy issues. Since that time we have assisted Councils on very many occasions by

providing expert witness services at Local Plan and S78 Inquiries, in order to successfully

support housing need and affordable housing policies. Particularly in recent years, this has

regularly included evidence in respect of viability issues.

Structure of this report

1.15 The remainder of the report covers the following topics:

Chapter 2 - The individual development sites

Chapter 3 - Affordable housing and developer contributions assumptions

Chapter 4 - Local market conditions

Chapter 5 - Assumptions for viability analysis

Chapter 6 - Results of viability analysis

Chapter 7 - Implications of viability results

Taunton & South Somerset Af fordable Hous ing Si te Viab i l i ty Study

Page 6

2. Ind iv idual development s i tes

Page 7

2. Individual development sites

Introduction

2.1 This Section deals with the sites identified for study, first outlining the key characteristics of

each site, and then considering the assumptions made about proposed development upon

each site for the purpose of producing a financial appraisal.

2.2 The individual sites chosen were visited at an early stage in the work.

Two market areas

2.3 The four Councils together provide an area of some diversity, geographically as well as in

terms of market conditions. The South Somerset area comprises a range of substantial

settlements, much the largest centre at Yeovil, spread across an area of undulating

topography with many attractive villages. The three other districts look to a principal centre

at Taunton, but there are other sizeable centres at Bridgwater, Burnham/Highbridge, and

Minehead. Much of Sedgemoor is flat fen country, though hills border it east and northward,

and the town of Cheddar lies within the boundary.

2.4 The areas of attractive landscape and/or building character, and access to the coast, mean

that many parts of both HMAs are popular with incoming households, particularly those

moving to retire or those anticipating future retirement. There are therefore areas of high

house prices and housing pressures, whilst in other areas, less attractive or with less

favourable local economic circumstances, prices are a little less.

2.5 In order for the present study to address development viability across the combined

Councils’ area it will need to deal with the variety of built form and density that is currently

to be found.

Identifying a range of sites

2.6 It was decided at an early stage that the study should consider a combination of actual and

notional sites in order to provide the most useful guidance across the two housing market

areas. In discussion with the steering group, it was decided that a total of 19 sites would be

required, comprising a total of twelve actual sites, and seven notional sites, the notional

sites being developments identical to one of the actual sites, but theoretically transposed to

an alternative location.

Taunton & South Somerset Af fordable Hous ing Si te Viab i l i ty Study

Page 8

2.7 The site selection process involved a typology with nine categories of site, giving a

minimum of eighteen sites (nine actual, nine notional) in total to cover the two HMAs. In

practice twelve ‘actual’ sites were chosen, doubling up actual sites in three of the

categories. Two of these pairings were split across the two HMAs, removing the need for

the corresponding notional, but the third was not, requiring an additional notional in the

other HMA.

2.8 The typology categories were developed by the Councils in discussion, before the study

formally commenced. They were designed to cover the range of development

circumstances that required testing, and accordingly focused on larger and smaller centres,

where viability was anticipated to be more marginal than in the villages and rural areas,

where prices tend to be higher. The twelve ‘actual’ sites were selected in discussion from a

larger initial shortlist of sites. The typology is set out below.

Table 2.1 Site selection typology

No Description No of dwgs

1 Large greenfield site in town 75+

2 Large previously developed site in town 75+

3 Medium greenfield site in town 25-74

4 Medium previously developed site in town 25-74

5 Medium greenfield site in small market town 25-74

6 Medium previously developed site in small market town 25-74

7 Small greenfield site 4-15

8 Small previously developed site 4-15

9 Very small site 1-4

Source: Strategic Housing Viability Study

2.9 The twelve actual sites chosen to represent this typology are set out below, with the nine

notionals added for completeness. The twelve range in size from two to circa 350

dwellings, although in reflecting the local development situation ten of the twelve contain

fewer than 60 dwellings. All the sites were envisaged as wholly residential.

2. Ind iv idual development s i tes

Page 9

Table 2.2 Site selection typology

S Somerset HMA Taunton HMA Ref

no Location No

dwgs Location

No

dwgs LA

1 1A - Deanesley Way,

Wincanton 212 (1N) (212)

2 (2N) (350) 2A Gerber Factory, Bridgwater 350 SDC

3 3A – Touches, Chard 24 (3N) (24)

4A - 2 Priory Ave Taunton 24 TDBC 4 (4N) (24/48)

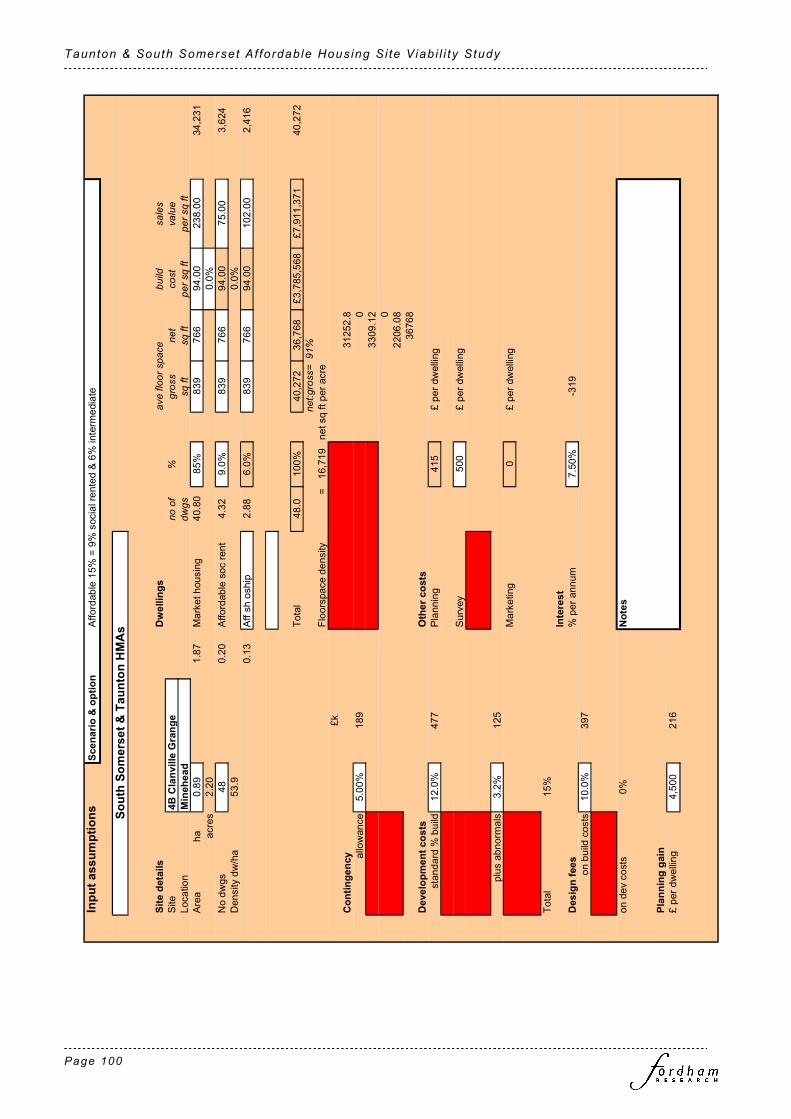

4B - Clanville Grange Minehead 48 WSC

5 5A - St Michael’s Gdns South

Petherton 55 5B - Haddons Field Stogursey 59 WSC

6 (6N) (32) 6A - Kings Yard Bishops Lydeard 32 TDBC

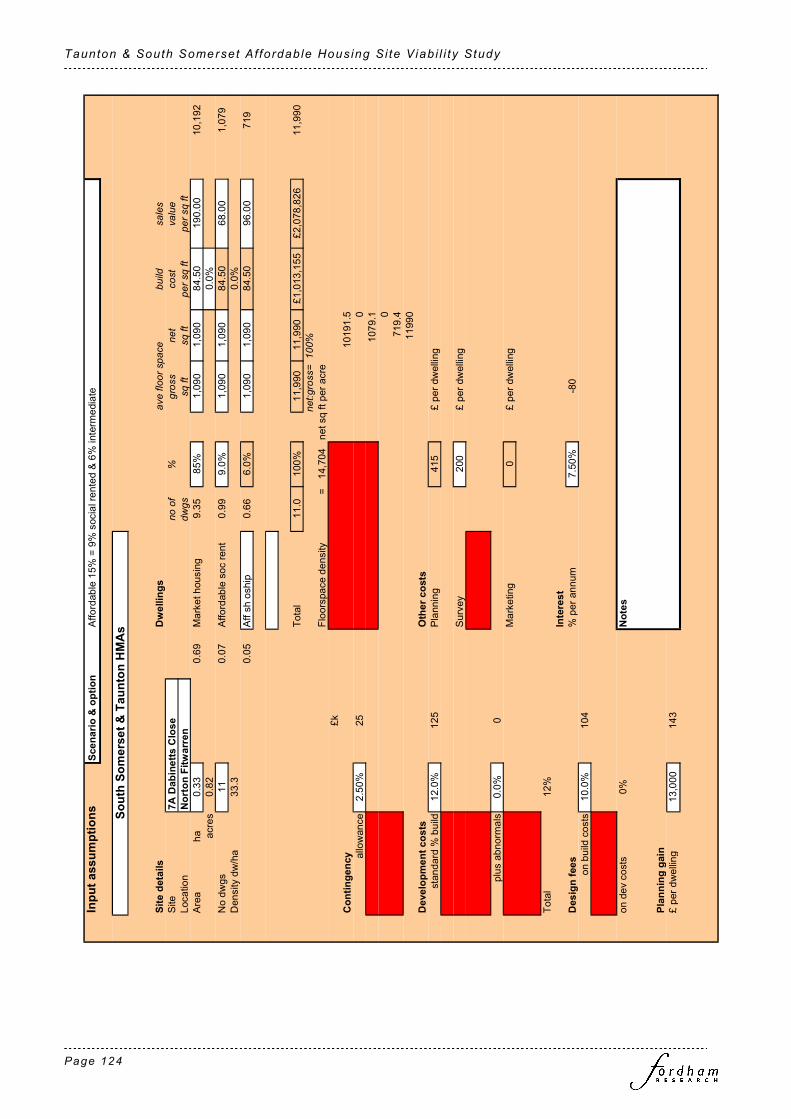

7 (7N) (11) 7A - Dabinett Cl Norton Fitzwarren 11 TDBC

8 (8N) (10) 8A - Opposite rail station Bridgwater 10 SDC

9 9A - Ilchester Rd Yeovil 2 9B - Pittacre House Bridgwater 2 SDC

Source: Strategic Housing Viability Study

2.10 Appropriate shadow locations for the nine ‘notional’ sites were selected. These were as

follows:

Table 2.3 Notional sites – locations

South Somerset HMA Taunton HMA

1N North Taunton

2N Eastern Yeovil

3N Bridgwater

4N Chard

6N Castle Cary

7N Langport

8N Yeovil

Source: Strategic Housing Viability Study

2.11 Site 4N could of course be based on two alternative models, sites 4A or 4B; after

discussion it was agreed that site 4B (Clanville Grange Minehead) was the preferred

model.

The actual sites

2.12 Summary details of the twelve actual sites identified by the Councils are set out in the table

below. The sites were at various stages in the planning process, though a clear majority,

eight, had reached construction stage; three of these were now completed. Three were

subject to planning applications which were to some degree resolved to permit, whilst for

one, the largest site, an application was imminently awaited.

Taunton & South Somerset Af fordable Hous ing Si te Viab i l i ty Study

Page 10

2.13 Information available from the various planning applications was clearly important in

considering the appropriate development forms to use in our appraisals. However we would

normally also take into account other recent schemes currently being developed, in

formulating development assumptions.

2.14 The table below shows both total site area, and for those sites including an open space or

similar non-residential component, the net residential area. The overall density using this

latter measure, is 46.1 dwellings per ha; two sites are at densities significantly above this

figure. One site with a density below 30 dw/ha, comprises bungalows on a particularly

awkwardly shaped and accessed plot. The rest are broadly within the range 30-50 dw/ha.

2.15 The sites accommodate just over 800 dwellings in total.

Table 2.4 Actual site details

Area ha Density Site

no Site

gross net Dw net

(dw/ha)

Planning status

1A Deanesley Way, Wincanton 7.23 4.83 212 43.9 Permission rescinded,

application

2A Gerber Factory, Bridgwater 6.00 NA 330 55.0 Application imminent

3A Touches, Chard 0.60 NA 24 40.0 Under construction

4A 2 Priory Ave Taunton 0.23 NA 24 104.3 Completed all occupied

4B Clanville Grange Minehead 1.33 0.89 48 53.9 Completed

5A St Michael’s Gdns S Petherton 1.70 NA 55 32.4 Under construction

5B Haddons Field Stogursey 3.23 1.95 59 30.3 Under construction

6A Kings Yard Bishops Lydeard 0.66 NA 32 48.5 Outline approved, reserved

matters minded to approve

7A Dabinett Cl N Fitzwarren 0.33 NA 11 33.3 Completed all occupied

8A Opp rail station Bridgwater 0.14 NA 10 71.4 Appln - minded to approve

9A Ilchester Rd Yeovil 0.10 NA 2 20.0 Under construction

9B Pittacre House Bridgwater 0.04 NA 2 50.0 Under construction

Total 21.6 17.5 809 46.1

Source: Strategic Housing Viability Study

2.16 The sites were chosen so as to test development viability fully, in a variety of situations

across the area. Reflecting the chosen selection typology they include both urban and more

suburban locations and a mixture of greenfield and previously developed land. The

previously developed uses include manufacturing (2A), garage (4A), car parking (4B),

repair of HGVs & machinery (6A), and unused residential garden land (9A/9B). The site at

8A is vacant land whose previous use was not fully clear.

2. Ind iv idual development s i tes

Page 11

Development assumptions

2.17 The Strategic Housing Land Viability Assessment has not considered within its site

typology strategic housing urban extension sites (typically in excess of 500 dwellings). Past

experience in South Somerset indicates that for the South Somerset sub-regional Housing

Market Area such sites would merit specific consideration in relation to abnormal promotion

costs that are usually incurred in the light of their size, complexity and nature.

2.18 In arriving at appropriate assumptions for residential development on each site, the

development form in an approved planning application would always be an important

consideration. All but one of the sites are in fact subject to an application which has been

approved or is likely to be approved subject to specific matters, (though it is possible that

one or two of the applications are now relatively historic and that an application today might

look slightly different, to reflect emerging market patterns).

2.19 For the one site without an application, 2A Gerber Factory, we have considered the

Development Brief and also a proposed accommodation schedule which was provided in

anticipation of the formal application.

2.20 In general, the details accord with our experience from a wide variety of development

situations in other parts of the country. In recent years, as development proposals have

engaged with the various implications of PPG3, but aided by rising land values, a common

development format has emerged for significant sized sites located within urban areas and

increasingly also in smaller centres.

2.21 This format provides for a majority of houses (with perhaps 15-30% flats) in a mixture of

two storey and two and a half to three storey form, with some rectangular emphasis to the

layout. It generates a floorspace density of around 15,000-15,500 sq ft per acre (3,550 sq

m/ha) on a substantial or sensibly shaped smaller site. Typical dwelling density would be

40-45 dwellings per ha.

2.22 Alongside this, of course, in appropriate, more urban locations - and indeed sometimes

elsewhere - there have been large numbers of higher density schemes providing largely or

wholly apartments, in blocks of three storeys and often rather higher. These provide

floorspace density from around 30,000 sq ft per acre (6,900 sq m/ha) upwards, at densities

of 100 dw/ha plus.

2.23 A development form which is somewhat more intensified or urban than the baseline, with

more flats or a stronger emphasis otherwise on three storey units might produce densities

of around 19,000 or so sq ft per acre (4,350 sq m/ha).

Taunton & South Somerset Af fordable Hous ing Si te Viab i l i ty Study

Page 12

2.24 On the other hand, of course, there are situations where, for planning reasons, in rural or

edge of settlement locations perhaps, schemes with densities below the baseline density

will come forward. Typically this situation might give a density of 12,500 sq ft per acre

(2,875 sq m/ha).Very small or awkwardly shaped sites might also make it difficult to

achieve fully the baseline density figure.

2.25 As suggested, the built form details for the twelve sites broadly fit with these observations,

as the table below indicates.

Table 2.5 Typology of development form

Category Ref Location net sq

ft/acre

net

sq m/ha

Dwgs

per ha

Rural/town 5B Stogursey 11,700 2,670 30

edge 5A South Petherton 12,200 2,800 32

9A Ilchester Rd Yeovil 12,650 2,900 20

Base 7A Norton Fitzwarren 14,700 3,375 33

9B Pittacre Ho B’water 14,800 3,400 50

3A Chard 14,850 3,410 40

Urban 4B Minehead 16,700 3,840 54

1A Wincanton 17,750 4,075 44

2A Gerber B’water 18,550 4,260 55

6A Bishops Lydeard 21,250 4,880 48

8A Station B’water 21,950 5,040 71

High 4A Taunton 38,700 8,900 104

Source: Strategic Housing Viability Study

2.26 The table shows three sites in the baseline category. There are three in the lower density

more rural group, and five in the higher density more urban group. Two of these are only a

little above the baseline:

• The Wincanton scheme is perhaps borderline, a broadly baseline mix which

benefits from a linear form designed to address the sloping nature of this large,

edge of town site.

• At Clanville Grange, the very steeply sloping site constrains the achievement of a

density to fully match the type mix.

2.27 There is one site, comprising wholly flats or coach houses, in the higher density category.

The Ilchester Rd site, being very small, awkwardly shaped and comprising two bungalows

might otherwise have been expected to make the baseline density.

2.28 The table is also felt to demonstrate quite well the comparatively loose relationship

between floorspace and dwelling density, reflecting variations in the average dwelling size.

3. Af fordable hous ing and other developer contr ibut ions

Page 13

3. Affordable housing and other developer

contributions

Introduction

3.1 This Section considers the assumptions used to test a range of affordable housing

scenarios for the individual sites, and similarly the developer contributions assumed for

each site.

Affordable housing assumptions

3.2 We undertook appraisals for a number of development scenarios which involved varying

proportions of affordable housing, and tenure split. The assumptions in respect of

proportions, and the financial terms on which they are to be provided, are considered

below.

3.3 The approach to seeking affordable housing will inevitably vary in detail between individual

Councils, reflecting its historical evolution, local choices and circumstances, and so on.

However, in order to reduce the appraisal work (and results) to a manageable task, a single

common approach was assumed to apply across the whole of the study area, and for all

sites. The use of a common approach is consistent with the overview perspective provided

in a SHMA. The differences in approach are not very great, and it is not felt that the use of

a common approach will undermine the validity of the appraisal results.

(i) Affordable proportions

3.4 Following discussions with the Councils we tested the following options1:

• NO affordable housing

• 15% affordable

• 30% affordable

• 45% affordable

1 Note that following the testing of these options, the Taunton & South Somerset Housing Market Partnership requested

that the Draft Regional Spatial Strategy proposed delivery of 35% affordable housing was subsequently tested; the

results are set out at Appendix 3.

Taunton & South Somerset Af fordable Hous ing Si te Viab i l i ty Study

Page 14

3.5 The four Councils currently operate policies seeking varying affordable housing

proportions, some site specific, but all lying broadly between 20% and 35%. However

higher proportions might be proposed in emerging Local Development Framework

Documents, though this will be subject to the ongoing SHMA work and more specifically will

be informed by the results of the present study.

(ii) Tenure split

3.6 We understand that all the Councils currently seek a balance of social rented and

intermediate housing. After discussion and consideration, all the affordable target options

were tested with two tenure split scenarios; the first a 60/40 split between social rented and

intermediate housing, and the second at 80/20.

3.7 In principle intermediate tenure could constitute a wide range of different housing

propositions, reflecting variations in individual Councils’ current policies and approaches.

However the Strategic Housing Market Assessment, proceeding a little in advance of the

viability study, has provided guidance on appropriate outgoings for affordable intermediate

housing and it would be sensible to follow these. They are set out in Tables 9.5 to 9.8 of the

SHMA Report, but for convenience are summarised below.

Table 3.1 Table of target outgoings for intermediate housing

Weekly outgoings £ as at May 2008

South Somerset Sedgemoor West Somerset Taunton Deane

1 bed 71 75 76 76

2 bed 95 86 95 96

3 bed 106 104 113 116

4 bed 118 125 132 132

Source: Taunton and South Somerset SHMA Report

3.8 After consideration, it was decided to consider two options; firstly intermediate rent housing

set to achieve the guidance outgoings for each Council area, and secondly shared

ownership on a corresponding basis.

(iii) Size profile

3.9 In practice the four Councils would be expected to seek a range of preferred bedroom

profiles for affordable housing provision, and the emerging SHMA will provide further

guidance. It was not practical in a study of this nature to address the requirements in detail,

with a limited number of sites in each District.

3. Af fordable hous ing and other developer contr ibut ions

Page 15

3.10 Instead, it was agreed that we should assume that the mix of affordable housing on each

site should broadly follow the market housing, achieving an average dwelling size (i.e. net

sq ft) in line with that of the market housing. This assumption also ensures that as the

affordable housing proportion varies between the options being tested, the floorspace

density remains constant - a desirable aim if the appraisals are to constitute a realistic

development scenario, consistently, across the options.

(iv) Financial terms

3.11 The financial terms on which a developer would make affordable dwellings he has

constructed available to an RSL will depend critically on the availability of public subsidy, as

acknowledged in PPS3 s29 (quoted above at 1.7). Where the availability of grant support is

expected to be quite limited it is common for appraisals to be prepared assuming zero

availability for Social Housing Grant (SHG) such an approach assumes that such grant as

is available, is to be used to support particular initiatives, strategic aims, and sites with

particular problems - or to support a more stringent mix where this was justified by local

considerations.

3.12 The zero grant assumption has become a common starting point or default position for

exercises of this kind, though it is by no means a universal one. It has the further

advantage that grant requirements can more easily be calculated from a zero grant starting

point than one which already assumes some level of grant. After discussion this approach

was the one adopted for the study.

3.13 It was necessary to seek advice from the Councils’ partner RSLs about the terms on which

properties of various sizes, would be purchased from the developer in order to achieve the

‘zero grant’ scenario. We sought information from ten Associations in respect of social

rented housing, and intermediate housing. As discussed above prices were sought on two

bases: intermediate rented housing to match the SHMA target outgoings guidance; and for

25% and 50% shared ownership, provided at rent levels of 2% on the unsold equity. To

assist with this, indicative guideline Open Market Values (OMVs) were provided for each

dwelling size.

3.14 Four of the RSLs (Knightstone, Magna, Raglan and South Somerset Homes) provided

figures in time for inclusion in our work. Not all RSLs were able to provide figures for every

option for every Council area; nevertheless a reasonable degree of coverage was

achieved. The figures show some variations in estimated ‘offer prices’ for affordable

dwellings on the basis described above, though they are not particularly great. Such

variations could, in practice, result from a number of factors, including the individual

organisation’s assumed level of contribution to the development from reserves. Given the

pattern of the RSL data it was felt reasonable to take an average from the figures provided

in each case.

Taunton & South Somerset Af fordable Hous ing Si te Viab i l i ty Study

Page 16

3.15 The question of which of the alternative bases for intermediate housing to use was

considered. Information had been provided for intermediate rent designed to meet the

SHMA guidance outgoings, and for shared ownership at 25% & 50% share, with rent

limited to 2%.

3.16 From the information provided it appeared that the 25% shared ownership option would

achieve the target outgoings for the smaller dwellings, but exceed it slightly for the larger

units. However we had more reliable data for shared ownership than for intermediate rent,

where only two RSLs provided responses. Even so, the purchase price ‘offer’ was not

greatly different between the options; the intermediate rent price was slightly higher for the

smaller units and a little lower for the larger units. Accordingly we took an average for the

two, halfway for the smaller units, but for the larger units, weighted somewhat more

towards the lower intermediate offer.

3.17 This process led to estimated for overall £ per sq ft prices for flats and houses in the four

Council areas under zero SHG as shown in Table 3.2. The figures for social rented homes

vary between Districts whilst those for intermediate housing apply throughout.

Table 3.2 Selling prices: zero grant basis

£ per sq ft (sq m)

Sedgemoor South

Somerset

Taunton

Deane

West

Somerset

Social rented Flat 73 75 75 77

House 65.5 68 68 70

Flat (785) (807) (807) (829)

House (705) (732) (732) (753)

Intermediate rent Flat 106 106 106 106

House 96 96 96 96

Flat (1,141) (1,141) (1,141) (1,141)

House (1,033) (1,033) (1,033) (1,033)

Source: data from RSLs

3. Af fordable hous ing and other developer contr ibut ions

Page 17

Other developer contributions

3.18 Aside from affordable housing, developer contributions could potentially be sought by the

District and County Councils under a number of headings and these need to be taken into

account. As with affordable housing, each District has in practice its own policies, protocol

and arrangements for determining the nature and hence cost of any developer

contributions - although the County elements should in principle be common. The four

individual approaches are also evolving, over time and with the emerging option of a

Community Infrastructure Levy. What was actually sought or secured on the ‘actual’ sites in

the past is therefore, though helpful, not a completely sound guide to what contributions

should be assumed if the sites were to be developed in say a few months from the present

time.

3.19 In fact, carrying out the detailed assessment required to assess impact and determine the

appropriate contribution for each of the sites was beyond the scope of the study.

Furthermore, since the ‘notional’ sites had only broad indicative locations this would not in

any case deliver meaningful results for them. We obtained varying amounts of information

from each Council on what they would seek currently from the site. The information we

received was incorporated into a ‘modelling’ approach to arrive at a view of the total £ per

dwelling cost of contributions. In doing this we relied, in part only, on the firm’s considerable

experience over a number of years from assessing developer contributions requirements

for Councils in respect of major residential projects.

3.20 The results are set out below. The main areas where contributions arise are Open space &

Recreation for the District, and for the County, Education & Transport where an appropriate

impact would arise. As dwellings numbers decline and thresholds come into play,

contributions for the latter drop out, reducing the overall total £ per dwelling figures

appreciably. The figures are designed to be broadly consistent across the Housing Market

Area, with the figures for South Somerset, in a separate HMA from the other three, set

higher to reflect the contributions now to be sought from a newly emerging Planning

Obligations Calculator produced by the Council.

Taunton & South Somerset Af fordable Hous ing Si te Viab i l i ty Study

Page 18

Table 3.3 Developer contributions base scenario

Size group Ref Location No

dwgs

£ per

dwelling

100 dwgs + 2A Gerber Bridgwater 330 £8,000

2N (Yeovil East) 330 £9,500

1A Wincanton 212 £4,500

1N (North Taunton) 212 £8,000

50-99 dwgs 5B Stogursey 59 £6,000

5A South Petherton 55 £6,300

25-49 dwgs 4B Minehead 44 £4,500

4N (Chard) 44 £6,000

6A Bishops Lydeard 32 £3,300

6N (Castle Cary) 32 £5,500

10-24 dwgs 4A Taunton 24 £3,000

3A Chard 24 £4,500

3N (Bridgwater) 24 £3,000

7A Norton Fitzwarren 11 £3,000

7N (Langport) 11 £4,500

8A Station Bridgwater 10 £2,000

8N (Yeovil) 10 £4,000

Under 10 dwgs 9B Pittacre Ho Bridgwater 2 £2,000

9A Yeovil 2 £4,000

Source: Strategic Housing Viability Study

3.21 The figures set out above should not be regarded as in any sense definitive. They are

simply a way of arriving at a plausible £ per dwelling scenario, using a combination of

known information and judgement. The figures cannot be assumed to constitute the

contributions that would arise in practice. These will depend on the current (or historic)

policies and approach of each Council, and indeed on the outcome of the negotiation

process.

3.22 Proposals to reflect the emerging Community Infrastructure Levy initiative are at various

stages across the four Councils, and indeed detailed proposals for a Taunton Deane

Infrastructure Tariff have been published. Looking at the figures in the table, it is clear that

generally speaking tariff proposals are likely to place an appreciably heavier burden on

viability, particularly for the smaller sites since they will apply universally. Nevertheless we

were asked to prepare appraisals with alternative contributions options, with figures at

£13,000 and £20,000 per dwelling, in lieu of the S106 costs identified in Table 3.3.

4. Local market condi t ions

Page 19

4. Local market conditions

Introduction

4.1 This Section sets out an assessment of the local housing market in the four Districts,

providing a basis for the assumptions on house prices and costs to be used in financial

appraisals for the 19 sites tested in the study.

4.2 As well as house prices, however, land values are also considered. They are required in

order to form a view of likely alternative use values for all of the sites, and it is such values

that will represent a minimum viability threshold when appraisals are prepared for the range

of affordable housing scenarios.

4.3 Before looking at the results from the market assessments, there are some general points

arising from the nature of the exercise.

Issues to consider

4.4 It is necessary to assess property market conditions in the study area in order to provide a

reasonable guide as to likely values to use in evaluating different development proposals.

4.5 Although development schemes do have similarities, every scheme is unique to some

degree, even schemes on neighbouring sites. While market conditions in general will

broadly reflect a combination of national economic circumstances and local supply/demand

factors, even within a town there will be particular localities, and ultimately site specific

factors, that generate different values and costs. There are indeed quite significant value

variations in different parts of the study area.

4.6 Property market forces are in a constant state of flux and assessments of viability can

change over relatively short periods of time, in response to broader economic fluctuations

such as the impact of changes in interest rates on the costs of borrowing. Equally

significant, sub-area market conditions are often changed by local factors.

4.7 Most crucially, as previously discussed at 1.11 onwards, we have now clearly entered a

period of downwards price adjustment. This resulted from external financial issues which

severely constrained the supply of mortgage finance, although the resulting price falls have

adversely affected the attractiveness of house purchase.

Taunton & South Somerset Af fordable Hous ing Si te Viab i l i ty Study

Page 20

The residential market

4.8 The housing market across the four Districts, to some extent, reflects national trends but

there are local factors that underpin the market including;

• A predominantly rural area containing many attractive settlements and individual

buildings of great character, popular with incoming households.

• A considerable length of coastline, providing a variety of opportunities and

environments, but also meaning that several larger settlements in particular are

either in need of, or undergoing regeneration in response to the reduction in holiday

and water related activity.

• Major employment centres at Taunton and Yeovil, generating housing demand in

the immediately adjoining rural areas

• A number of attractive smaller centres

• Rolling topography, some more dramatic, over much of the two Market Areas,

creating tourist potential and interest, including part of a National Park (Exmoor) and

three Areas of Outstanding Natural Beauty (AONBs) (Mendips, Quantock and

Blackdown Hills)

• A flatter area of low lying historic fenland to the north and centred on Bridgwater,

with consequent flooding issues

• Good transportation - westward into the peninsula and north east to Bristol and the

Midlands, or towards London – for localities close to the M5 motorway and to some

degree the A303. Comparative remoteness in and around Exmoor.

4.9 We analysed various sources of market information but the most relevant are the prices of

units on new developments. A list setting out details of some relevant new developments in

the area, as at July 2008, is provided in Appendix 1.

4.10 Analysis of these, and other schemes in the study area, shows that prices for newbuild

homes vary quite widely across the area, ranging between approximately £160 and £300

per square foot (£1,720 - £3,225 per square metre). This is the range for individual

properties; averaged over the complete scheme the degree of variation will of course be

somewhat less than this. However it is clear that the price per sq ft will vary considerably

between the 19 sites in the study. (As in other parts of the country, the smaller units and

apartments in particular show a price premium per square foot compared to larger houses).

4.11 Land Registry data confirms that there are significant variations in house prices across the

area. Table 4.1 shows average prices for the four Council areas. It suggests that, on

average, prices are appreciably higher in West Somerset than in the other three areas.

These are all broadly similar, except that prices for detached homes are at something of a

premium in South Somerset & Taunton Deane, whilst Taunton Deane also shows a

premium for flats compared to the other two.

4. Local market condi t ions

Page 21

4.12 Although the Land Registry data covers both second-hand and newbuild prices, the former

will predominate. The average prices in the table are compared to a corresponding England

& Wales figure and expressed as indices.

Table 4.1 Average house prices by Council area Q4 2007

Ave price (£k & % index) Area

Detached Semi Terrace Flat

Sedgemoor £k £301.3 £183.0 £154.2 £126.0

Index 97% 97% 96% 92%

South Somerset £k £347.1 £180.8 £156.9 £120.2

Index 111% 96% 98% 87%

Taunton Deane £k £350.6 £189.1 £153.2 £147.6

Index 113% 100% 96% 107%

West Somerset £k £419.7 £215.1 £159.0 £158.9

Index 135% 114% 99% 116%

Source: Land Registry data.

Index compares LA’s figure to the median LA value across England & Wales for house type.

4.13 However it is also clear that within a Council area there can be considerable variations in

price, larger than those between Councils. Land Registry house price data at postcode

sector level helps to illuminate these variations. Because the number of sales in individual

postcode areas in a single quarter can be quite small, we looked at information for two

separate quarters (Q2 2007 & Q4 2007). The data has been expressed as an index – as a

percentage of the nationwide average postcode price level - and standardised, to allow for

variations in type mix.

Taunton & South Somerset Af fordable Hous ing Si te Viab i l i ty Study

Page 22

Fig 4.1 Postcode price indices

Source: Land Registry data.

4.14 Appendix 2 provides a worked example of the index calculation, and sets out the resulting

price index figures for the two quarters examined. It can be seen that variations between

the two quarters’ indices are in many cases relatively slight. They are greater for rural areas

and town centres, which are mostly numerically smaller and more diverse, than for urban

areas generally, where postcode sectors are larger numerically and can often be more

uniform.

4.15 The figures show quite clearly that the lowest prices, between about 80% and 95% of

national average, are concentrated in the main towns – Bridgwater, Yeovil and Taunton - or

in Burnham/Highbridge, and Chard. (Yeovil and Bridgwater are wholly in this group, except

for the west of Bridgwater; Taunton however has several higher priced sectors). The

highest prices relate closely to the areas of attractive landscape – Exmoor, the Quantocks,

Mendips & Blackdown Hills.

4.16 The majority of the postcodes, including most rural areas but also some of the smaller

towns, have prices above the national average. In the most expensive areas prices are as

much as 50% higher than the national average. Among the locations for our sites

Stogursey, Bishops Lydeard, South Petherton and Minehead all have prices well above

average.

4. Local market condi t ions

Page 23

4.17 Looking at the map in Figure 4.1, it is clear that areas of higher and lower prices are quite

well distributed across the area as a whole. Three of the four districts contain a good

mixture of higher, middle, and lower prices; it is because West Somerset has no significant

lower priced urban areas that its overall average price is higher than the other three.

Price assumptions for financial appraisals

4.18 It is necessary to form a view about the appropriate prices for the 19 individual schemes to

be appraised in the study. The information suggests that there will be significant variations

in selling prices across the area. However on the whole the sites are mostly in towns, or

otherwise locations of low to medium price level. This is a sensible approach as the areas

of highest prices have mainly been avoided.

4.19 It is also clear that we must allow for differences between apartments and houses,

particularly in locations where flats are going to be attractive. Finally, in drawing on the

newbuild price data we have to bear in mind that the prices at which homes are offered can

sometimes include appreciable discounts, such as deposit paid for first time purchasers, or

stamp duty. Discounts can be particularly significant at the very end of the scheme’s life

when only one or two units are left unsold; however such ‘bargains’ cannot form a basis for

selling prices across the whole scheme .

4.20 Taking these points into consideration we arrived at a set of sale prices for flats and for

houses on each of the 19 sites. The two were then combined on the basis of the

proportions of flats and houses in each scheme, to produce a single composite average

price. The resulting figures are set out in Table 4.2 below.

Table 4.2 Price bands

Price £ per Price £ per Site/location

Sq ft Sq m Site/location

Sq ft Sq m

1A Wincanton 207 2,230 1N Taunton N 200 2,147

2A Bridgwater W 206 2,217 2N Yeovil E 190 2,039

3A Chard 190 2,044 3N Bridgwater N 195 2,098

4A Taunton C 225 2,421 4B Minehead 238 2,559

4N Chard 196 2,113 191 2,044

5A S Petherton 230 2,475 5B Stogursey 216 2,322

6A Bishops Lydeard 241 2,589 6N Castle Cary 211 2,269

7A Norton Fitzwarren 190 2,044 7N Langport 210 2,260

8A Bridgwater E 195 2,098 8N Yeovil 185 1,991

9A Yeovil NE 240 2,582 9B Bridgwater E 185 1,991

Source: Strategic Housing Viability Study

Taunton & South Somerset Af fordable Hous ing Si te Viab i l i ty Study

Page 24

4.21 The figures cover a range from £185 per sq ft in Yeovil, to approx £240 in Minehead &

Bishops Lydeard. This is somewhat less than the spread of prices we saw in the Land

Registry data for second-hand prices, but partly reflects the sites’ concentration in the lower

to medium priced locations. It should be emphasised that the figures are intended to be

relatively realistic selling prices, and should not include major discounts.

4.22 It is necessary to consider whether the presence of affordable housing would have a

discernible impact on sales prices. In fact affordable housing will be present on many of the

sites whose selling prices have informed our analysis. Our view is that in any case any

impact can and should be minimised through an appropriate quality design solution.

Land values

4.23 In considering land values we have not only looked at the evidence of transactions in the

market but have also considered how developers source land. Developers do buy land that

has the benefit of planning consent and is ready for development (and the requirements for

S106 contributions and affordable housing are known and reflected in the price) but much

land that is also brought forward that has been promoted through the planning system –

historically often over many years and at significant expense to the developer or land

owner. There is an allowance for this cost in the Fees heading (see 5.19) but it would

certainly not cover every case which has been brought to our attention. Depending on

where a site is in the planning process we must also recognise that it may have developed

an amount of ‘Hope Value’ – at least in the eyes of the owner.

4.24 The availability and cost of land is at the core of the viability of any development of new

houses. The fact that a developer has over paid for a site will not excuse them from

providing affordable housing – and likewise the fact that they have underpaid will not

require them to provide more. It has been recognised by stakeholders (including builders

and developers) that in the current development and planning regime the cost of meeting

S106 requirements and delivering an amount of affordable housing is a factor in

development appraisals and does impact on land values.

4.25 The land price element of a viability appraisal has caused much debate. This study does

not try to set land values – that will always be a private matter between buyers and sellers

and is not a matter for the planning authority. This study does not attempt to predict when

a landowner may sell the land, if at all, as all land owners have very different

circumstances. It may be for example that in circumstances such as at present, in the

current economic climate, some landowners (particularly the long term holders of land such

as farmers and estate owners) will decide not to sell land for the time being. That being

said, the value of land can only be assessed for a study of this type by reference to the

prevailing planning framework. The provision of affordable housing and other requirements

under S106 are a reality of planning, and do impact on the value of land.

4. Local market condi t ions

Page 25

4.26 In our consideration around what a landowner may or may not accept the promoters of land

raised the ‘cost’ of taxation. The sale of land is subject to Capital Gains Tax. We have

wrestled with how to deal with this however the circumstances of individual owners is so

very different that we have not made specific reference to it. We do however acknowledge

that promoters of strategic land are likely to have substantial tax bills following very large

sales of land and farmers and long term landowners lesser bills.

4.27 We firmly believe that the notion of the open market value of land with planning consent for

housing, but no requirement for affordable housing or any of the other factors that may be

introduced under S106 has no direct relevance; if landowners have an expectation of

receiving values that do not reflect the provision of affordable housing and other legitimate

contributions, that view should be regarded as naïve and misguided.

4.28 We have considered general figures from the Valuation Office Agency (VOA) relating to

residential land values. Land values vary dramatically depending upon the development

characteristics (size and nature of the site, density permitted etc.) and any affordable or

other development contribution.

4.29 The VOA figures for residential land published in the Property Market Report cover the

South West Region as a whole, and major towns like Taunton and Exeter.

4.30 These values can only provide broad guidance because it is possible that they incorporate,

to some degree, allowances for developer contributions and/or affordable housing

requirements. They can therefore be only indicative, and it may be that values for ‘oven

ready’ land with no affordable provision or other contribution, or servicing requirement, are

in fact a little higher. We would highlight that these figures are somewhat historic and do

not truly reflect the current downturn.

Table 4.3 Residential Land Values

Land Value £m per acre (hectare) Area

Small sites Bulk sites Land for apartments

South West Region £1.31m

(£3.25m)

£1.14m

(£2.80m)

£1.50m

(£3.71m)

Taunton £1.21m

(£3.00m)

£1.13m

(£2.75m)

£1.42m

(£3.50m)

Exeter £1.62m

(£4.00m)

£1.21m

(£3.00m)

£1.62m

(£4.00m)

Bristol £1.50m

(£3.70m)

£1.21m

(£3.00m)

£1.62m

(£4.00m)

Source: VOA Property Market Report Jan 2008

Taunton & South Somerset Af fordable Hous ing Si te Viab i l i ty Study

Page 26

4.31 Values in Taunton are fairly close to the average for the region, though the value premium

for flatted schemes is smaller; by comparison, the major cities show a substantial premium

for apartment land – and also for small sites. These values will take no real account of the

changes to the national housing market since the beginning of the year. It is also difficult to

assess how much provision is made in the reported values, for affordable housing or for

other developer contributions. It is therefore necessary to seek information about values

from residential land currently on sale in the Borough.

4.32 An examination of small land plots currently available – in mostly rural locations - points in

the main to values in the range of about £800-1,250k per acre (£1,975-2,965k per ha) for

oven ready land. This does suggest that the VOA figures might be a little high, and are not

particularly heavily discounted.

Current and alternative use values

4.33 In order to assess development viability the appropriate starting point must be an analysis

is of current and alternative use values. Current use values refer to the value of the land in

its current use, for example, as agricultural land. Alternative use values refer to any

potential use for the site. For example, a brownfield site may have an alternative use as

industrial land.

4.34 We would recognise that for some greenfield sites and occasionally otherwise, depending

on where a site is in the planning process it may have developed an amount of ‘Hope

Value’ – at least in the eyes of the owner. This is a matter which must be taken into

account in due course. However current and alternative use value has to be the starting

point.

4.35 To assess viability, the value of the land for the particular residential scheme adopted

needs to be compared to the alternative use value, to determine if there is another use

which would derive more revenue for the landowner. If the assessed value does not exceed

the alternative use value, then the development is not viable.

4.36 For the purpose of the present study, it is necessary to take a comparatively simplistic

approach to determining the alternative use value. In practice a wide range of

considerations could influence the precise value that should apply in each case, and at the

end of extensive analysis the outcome might still be contentious.

4.37 Our ‘model’ approach is outlined below for the twelve actual sites (but would apply to the

corresponding notionals):

i) For five sites previously in agricultural use, then agricultural land represents the

existing use value.

4. Local market condi t ions

Page 27

ii) Where the development is on former industrial or similar land, then the alternative

use value is considered to be industrial. An average value of industrial land for the

area is therefore adopted as the alternative use value for three sites.

iii) One site was previously in use as a public car park convenient for the main retail

centre at Minehead (site 4B).

iv) The remaining sites are on unused garden land, or land otherwise adjoining a

residential use. Whilst such land is going to have previously developed status, it is

unlikely that an alternative use other than residential would be available. In practice