tasmia afsari

38

Executive summary This term paper is the based on the performance analysis of a bank operating in Bangladesh that is being listed in the Dhaka stock exchange. There are currentl y 29 banks list ed in Dhaka stock exchange. Based on the past stable performance I decided to work on Prime Bank Ltd and chose Eastern Bank Ltd for comparisons since they are close competitors. I evaluated the performance of both banks during the years 2004-2008 and used both companies annual report. I used the following kinds of ratio to analyze the performance. Liquidity ratios: Prime bank is in better position of liquidity management compared to eastern bank derived from conclusions using liquid security indicator, cash position indicator and capacity ratio. Leverage ratios: both prime and eastern bank is highly leveraged as they are financial institutions Efficiency ratios: eastern bank was superior to prime bank in terms of efficiency of tax management, asset utilization and operating efficiency. Profitability ratios: The overall profitability of eastern bank is better than prime bank ltd. Market Position ratios: Eastern bank is in superior position compared to prime bank in terms of EPS, Price earning ratio and market to book value ratio. At the beginning of the project, I gave a brief introduction about the company and methodology, limitations and description of all the ratios that is used in this project. 1

-

Upload

sarah-tasnia -

Category

Documents

-

view

228 -

download

0

Transcript of tasmia afsari

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 1/38

Executive summary

This term paper is the based on the performance analysis of a bank operating in Bangladesh that

is being listed in the Dhaka stock exchange. There are currently 29 banks listed in Dhaka stock

exchange. Based on the past stable performance I decided to work on Prime Bank Ltd and chose

Eastern Bank Ltd for comparisons since they are close competitors. I evaluated the performance

of both banks during the years 2004-2008 and used both companies annual report. I used the

following kinds of ratio to analyze the performance.

Liquidity ratios: Prime bank is in better position of liquidity management

compared to eastern bank derived from conclusions using liquid security indicator, cash

position indicator and capacity ratio.

Leverage ratios: both prime and eastern bank is highly leveraged as they are financial

institutions

Efficiency ratios: eastern bank was superior to prime bank in terms of efficiency of tax

management, asset utilization and operating efficiency.

Profitability ratios: The overall profitability of eastern bank is better than

prime bank ltd.

Market Position ratios: Eastern bank is in superior position compared to prime bank in

terms of EPS, Price earning ratio and market to book value ratio.

At the beginning of the project, I gave a brief introduction about the company and methodology,

limitations and description of all the ratios that is used in this project.

1

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 2/38

I used as many effective ratios as possible to evaluate the bank from every angle. After

calculating the ratios, I showed a time series, cross sectional graph to show the change over five

years and compare it with the other bank, and decided which one is comparatively doing well.

At the end of this project, I showed the final decision about the financial condition of both bank

and my recommendation. Included are calculations, extract from balance sheet and income

statement.

2

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 3/38

Introduction

The main purpose of this assignment was to use the skill in strategic financial ratio analysis. I

had to demonstrate analytical abilities in explaining the implications of different ratios and

provide general assessment of a chosen company versus its competitor in the market.

I tried to complement my study of the absolute numbers by using ratios to ascertain trends,

identify areas of concern and identify areas of strength. I tried to provide the ‘Trend Analysis’ of

the ratios which graphically shows the likelihood of improvement and deterioration in financial

conditions of the firms. This project was about comparing two different public limited companies

from the banking industry.

I choose “Prime Bank Limited” as my main company and “Eastern Bank Ltd.” for

comparisons for the following year 2004-2008. The reasons behind choosing the companies were

simple. Prime bank limited is one of the banks that follows international standard in Banking and

Finance and its sheer size and stature as a Bank company is outstanding. As of early march 2010,

their stock prices were very good in the bank industry and the company’s performance reflectedin the stock prices. Its stock was listed as Category ‘A’ stocks on the Dhaka Stock Exchange.

Given the basic information about the company and its stock market performances, I was

convinced that Prime bank Limited would be a great company to work with. The financial

reports turned out to be straight forward, very well explained and user friendly.

To go put up against Prime bank Limited, I had to choose a company that was its close

competitor. Eastern Bank Limited is one of the modern banks in Bangladesh. As of early march

2010, their stock prices were excellent among the bank industry. Both the companies were trying

to increase market share and profitability.

3

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 4/38

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 5/38

Methodology

This report is based on ratio analysis of Prime Bank ltd and Eastern bank limited of the year

2004 to 2008.

Different types of data are used to complete this report. Data are collected from different sources.

The data about the companies are found from the website of the both company. The

mathematical data are found from the annual report of the both banks. I collected the financial

data from the annual report that was necessary for the ratio analysis. I mainly used the income

statement and balance sheet to analyze the ratios.

There are different types of ratio that can be used to analyze the financial condition of the bank.

Since the balance sheet and income statement of banks are very different from any other

company so I had to choose all the ratios very carefully.

I used the ratio analysis of five year in a time series and cross sectional graph to analyze all the

difficulties of both banks.

I used the dividend growth model to find out the intrinsic value of the company to compare it

with the current market price to see if the stock is over or under priced.

Finally, I compared both of them and made my recommendation. In some ratios, the

performance of the banks was very low or very high. I tried to find out the reasons behind this

problem and necessary solution.

5

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 6/38

Limitation

Like any other analyzing process, I found some difficulties and problem at the time of preparing

the report. The limitations are given below.

Annual report of both company are not perfect. In the balance sheet the yearly

report are sometimes wrong and sometimes value of same data in different annual

report is different. Therefore, it is hard to find out the validity.

The ratio does not reflect the true financial condition of a bank all the time.

Inflation or deflation in economy does not affect the ratio analysis. Therefore, it

does not always show the true condition of a company.

Ratio analysis may find the problem but it does not provide any solution of the

problem.

6

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 7/38

Overview of the bank

A group of visionary entrepreneurs established Prime Bank in April 1995. Known for its superior

service quality, brand Image, strong corporate Governance and a corporate culture committed to

excellence, Prime Bank is a top-tier bank in Bangladesh.

The Prime Bank Group focuses on a wide range of banking and financial services, which include

commercial banking, retail & SME asset management, Islamic banking, investment banking,

merchant banking and card business. Prime Bank is a market leader in corporate to consumer

banking and retail lending to SMEs in Bangladesh.

Prime Bank ranked 15th in Bangladesh by market capitalization, which stood at Tk.15349

million as at the end of 2008. DSE-20 Index has ranked it as fourth company as per performance.

The Prime Bank Group is the second largest banking group in Bangladesh by asset size, with

total assets of Tk. 110,437 million. The Bank’s deposits and lending growth were 24.83 and

30.29 respectively in 2008.

The Prime Bank Group has a large and well-distributed branch network of 70 full fledged

branches and 3 Off shore Banking Unit & Booths in Bangladesh with a strong tradition of

service excellence. The Bank has also made its presence in Singapore through its fully owned

subsidiary Prime Exchange Co. Ltd. For facilitating inward foreign remittance to Bangladesh.

The Prime Bank Group has a strong capital base with a risk-weighted capital adequacy ratio of

10.88 percent and a Tier-1 of 8.67 percent at the end of 2008. The Group has one of the most

7

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 8/38

efficient capital structures in Bangladesh. The Bank also has good asset quality in the banking

industry and very strong financial ratings.

Prime Bank continues to earn recognition and trust for its strong and sustained financial

performance and product management. In 2008, ICAB and SAFA Bronze Award in the region

honored Prime Bank with best bank award in Bangladesh.

The Prime Bank Group is committed to deliver value to its stakeholders. To its customers, the

Group will continue to provide effective and competitive financial solutions and services. To its

shareholders and investors, the Group will continue to enhance shareholder value through

consistent financial performance and efficient capital management. To its employees, the Group

will continue to foster a strong performance and learning culture that allows the development of

the best talents for the Group.

Stakeholders in the Prime Bank Group, including shareholders, customers, investors and the

public in general has access to various sources of information on the Prime Bank Group.

Prime Bank’s website at (www.prime-bank.com) and (www.primebank.com.bd) provide a wide

range of information about the bank’s corporate information, Board of Directors, senior

management, corporate vision mission, financial information, corporate philosophy products and

services and awards and recognition of the bank.

Credit Rating on Prime Bank Limited by CRISL

Long Term Short Term

Surveillance

Rating (2007)AA ST-2

Entity Rating(2006)

AA ST-2

Outlook Stable

Date of Rating 29th June, 2008

Literature Review

8

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 9/38

To analyze the performance of any commercial bank we need the published financial statements

of the institution notably the Report of Condition, the Report of Income and the stock price in

over the period of assessment. We need to find out the key objectives of the company and using

various techniques evaluate the performance of the company. One key objective of a commercial

bank is to maximize the value of the firm or stock.

The technique used for performance appraisal is financial ratio analysis. Two types of ratio

comparisons can be made: cross sectional and time series. Cross sectional analysis or

benchmarking involves the comparison of financial ratios at the same point of time with their

competitors. Time series analysis evaluates performance over time, which enables to assess the

firm’s progress.

Financial ratios are divided into five basic categories: liquidity, profitability, leverage, efficiency

and market position. Liquidity, activity and debt ratios primarily measure risk. Profitability

measure return. Market ratios capture both risk and return.

• PROFITABILITY AND EFFICIENCY RATIOS

Financial analysts use profitability ratios as surrogates for indicators of stock values. Some of

these ratios are return on equity, return on assets, net interest margin, net noninterest margin, net

operating margin, earning spread, earning per share.

Return on assets is primarily an indicator of managerial efficiency. It indicates how capable

management has been in converting assets into net earnings.

Return on equity is a measure of the rate of return flowing to shareholders. It indicates the net

benefit that the stockholder has received from investing their capital in the financial firm.

9

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 10/38

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 11/38

Net interest margin (NIM) or net interest income to total assets is an indication of managements

efficiency in achieving a positive spread between interest revenue and interest cost by close

control over earning assets and pursuit of the cheapest source of funding.

Net noninterest margin or net non-interest income to total assets measures the amount of

noninterest revenue stemming from service fees the financial firm has been able to collect

relative to noninterest expenses such as salaries, maintenance and loan loss expenses.

Net operating margin or net operating income to total assets is also a measurement of

profitability and efficiency just like the previous two ratios. It indicates how well management

and staff have been able to keep growth of revenue ahead of rising costs.

Earning spread is another traditional measure of earning efficiency. The spread measures the

effectiveness of a financial firms intermediation function in borrowing and lending money and

the intensity of competition in the firm’s market area. Greater competition other factors held

constant will squeeze the difference between average asset yield and average liability cost.

Earning per share is generally of interest to present or prospective stockholders and management.

EPS represents the number of dollars earned during the period on behalf of each outstanding

share of common stock.

• LIQUIDITY RATIOS

Cash position indicator or cash and deposit due from depository institution / total assets indicates

the percentage of total assets in cash in vault and other depository institution. The greater the

ratio the stronger the position to handle immediate cash needs.

Liquid security indicator or government security / total assets compares the most marketable

securities an institution can hold with the overall size of its asset portfolio. The greater the

proportion of government security, the more liquid the depository institutions position tends to

be.

11

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 12/38

Capacity ratio or net loans and leases / total assets are really a negative liquidity indicator

because loans and leases are often the most illiquid of assets.

• Market ratios

Price earning ratio is commonly used to assess the owner’s appraisal of share value. The P/E

ratio measures the amount that investors are willing to pay for each dollar of a firm’s earnings.

The level of this ratio indicates the confidence that investors have in the firm’s future

performance. The higher the P/E ratio, the greater the confidence.

Market to book value ratio provides an assessment of how investors view the firm’s

performance. It relates the market value of the firms shares to their book strict accounting value.

To calculate the firms M/B ratio we need to calculate book value per share of common stock.

Book value per share of common stock = common stock equity / no of outstanding common

stock

Market / book ratio = market price per share of stock/ book value per share of common stock

• LEVERAGE

Debt ratio measures the proportion of total assets financed by the firm’s creditors. The higher

this ratio, the greater the amount of other people’s money being used to generate profits.

Findings and Analysis

o PROFITABILITY AND EFFICIENCY RATIO

12

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 13/38

TAX MANAGEMEN

EXPENSE CONTROL EF

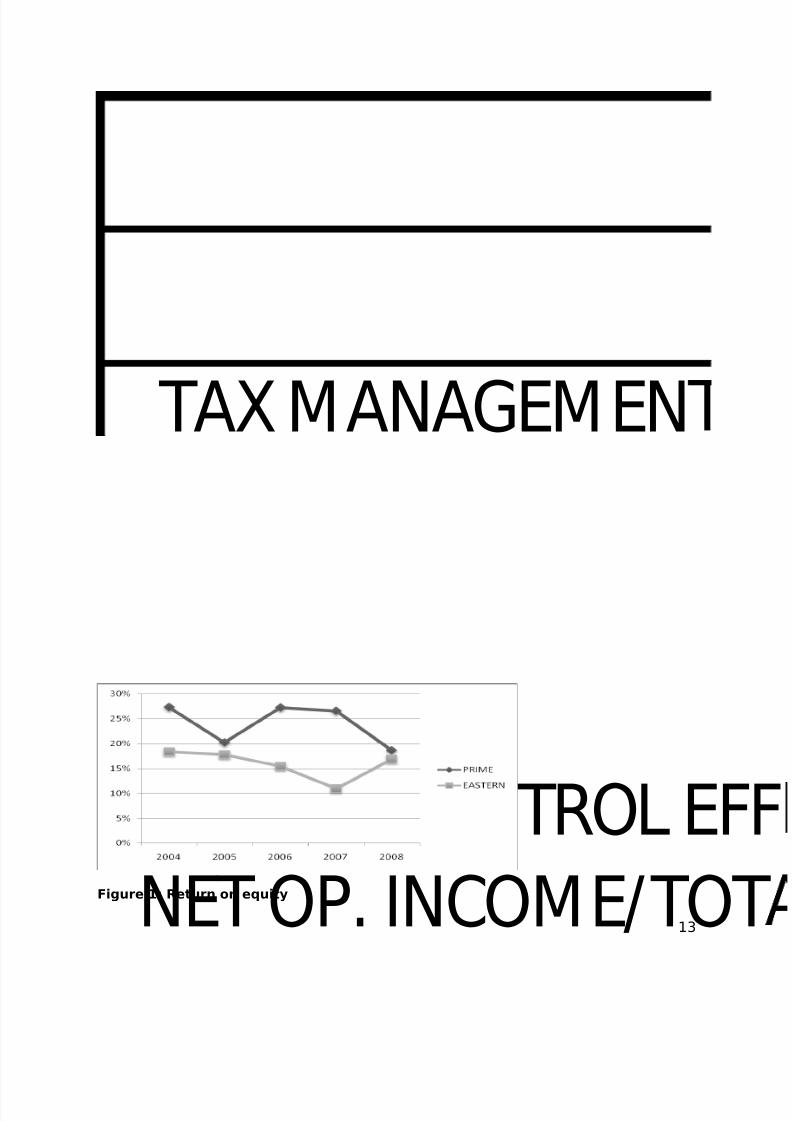

NET OP. INCOME/TOTFigure 1: Return on equity

13

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 14/38

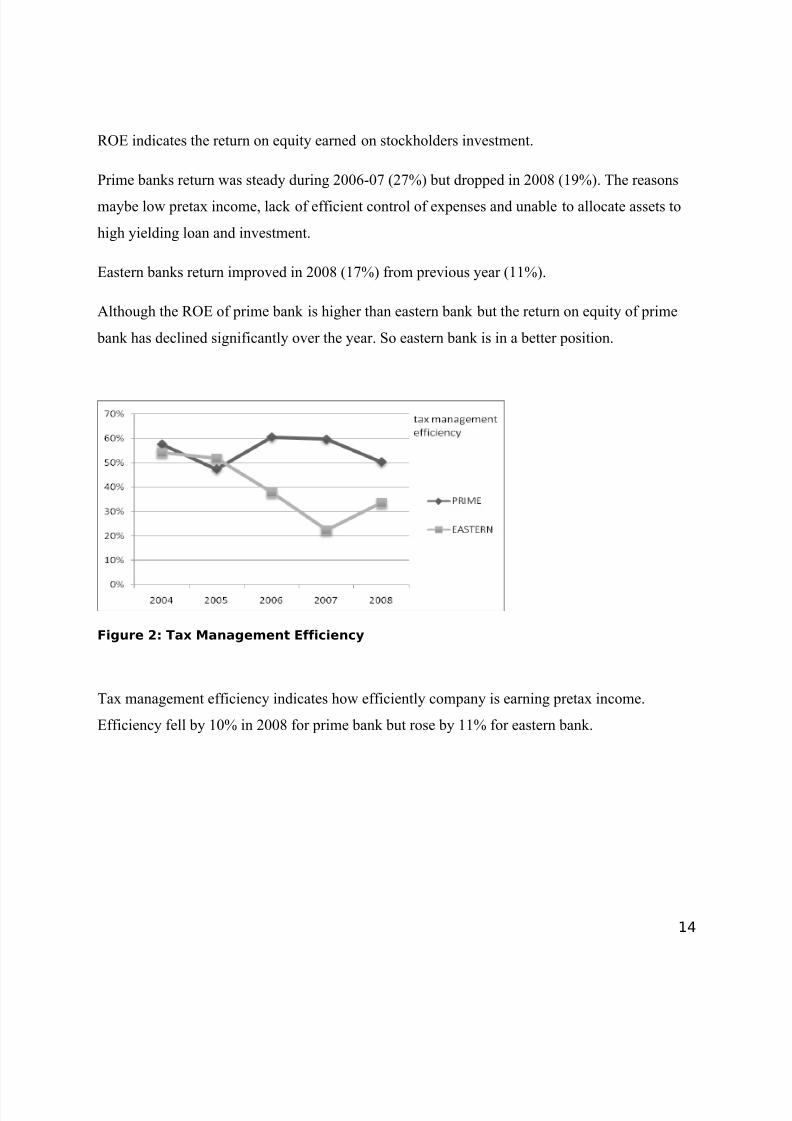

ROE indicates the return on equity earned on stockholders investment.

Prime banks return was steady during 2006-07 (27%) but dropped in 2008 (19%). The reasons

maybe low pretax income, lack of efficient control of expenses and unable to allocate assets to

high yielding loan and investment.

Eastern banks return improved in 2008 (17%) from previous year (11%).

Although the ROE of prime bank is higher than eastern bank but the return on equity of prime

bank has declined significantly over the year. So eastern bank is in a better position.

Figure 2: Tax Management Efficiency

Tax management efficiency indicates how efficiently company is earning pretax income.

Efficiency fell by 10% in 2008 for prime bank but rose by 11% for eastern bank.

14

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 15/38

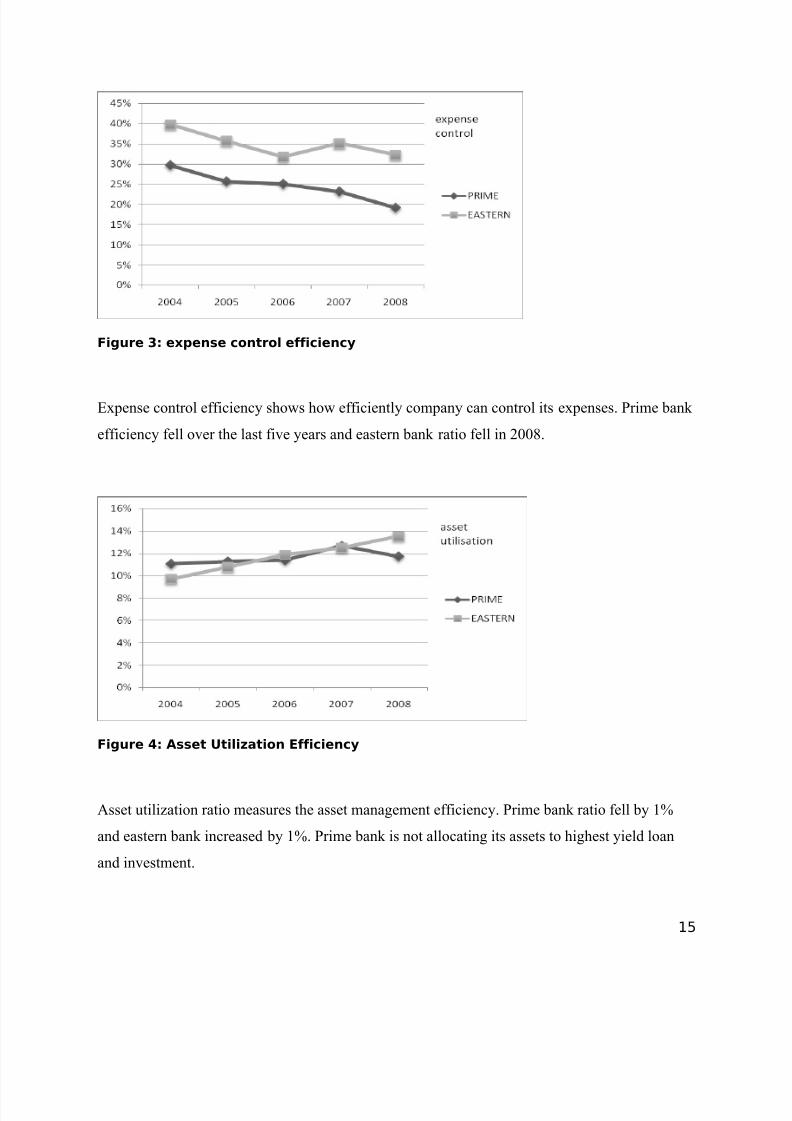

Figure 3: expense control efficiency

Expense control efficiency shows how efficiently company can control its expenses. Prime bank

efficiency fell over the last five years and eastern bank ratio fell in 2008.

Figure 4: Asset Utilization Efficiency

Asset utilization ratio measures the asset management efficiency. Prime bank ratio fell by 1%

and eastern bank increased by 1%. Prime bank is not allocating its assets to highest yield loan

and investment.

15

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 16/38

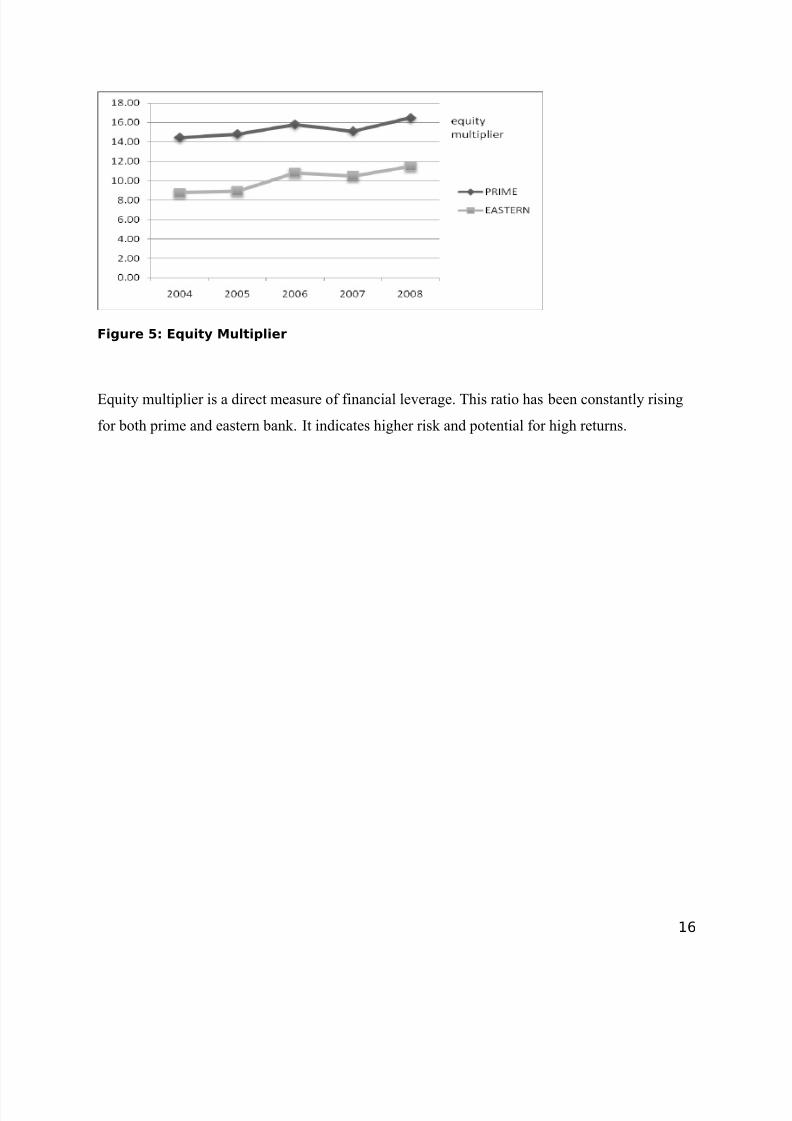

Figure 5: Equity Multiplier

Equity multiplier is a direct measure of financial leverage. This ratio has been constantly rising

for both prime and eastern bank. It indicates higher risk and potential for high returns.

16

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 17/38

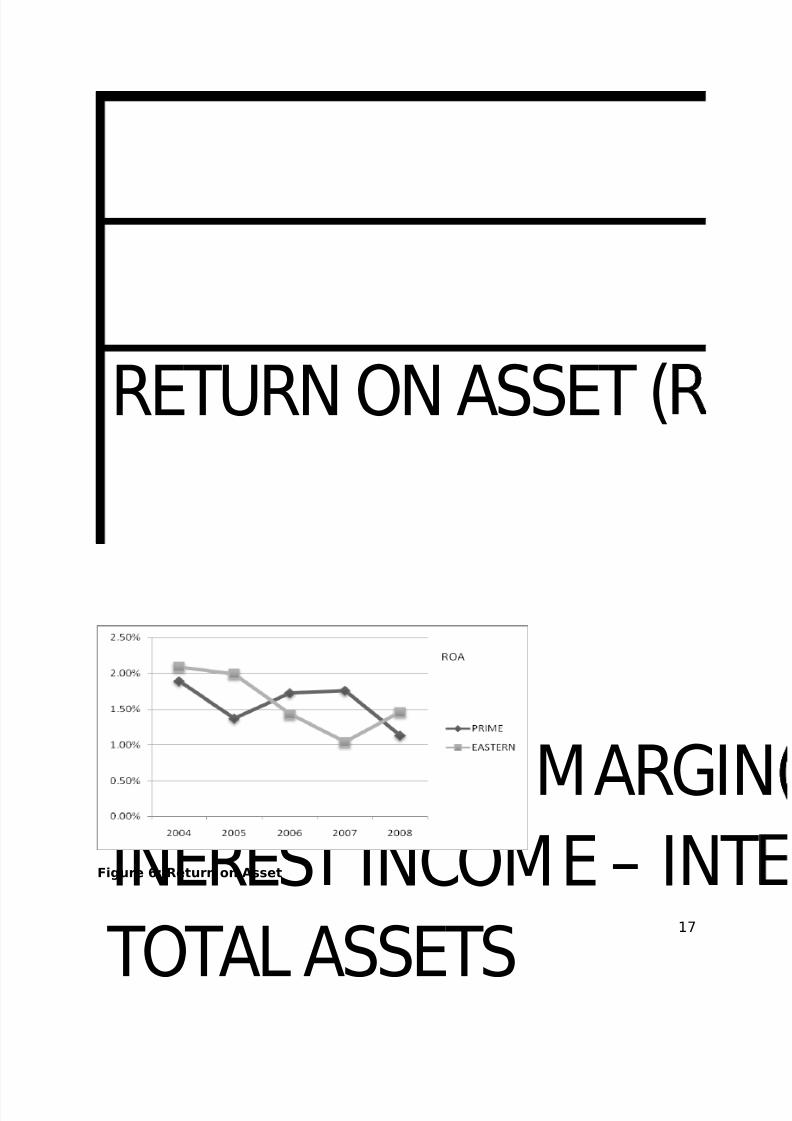

RETURN ON ASSET (

NET INTEREST MARGININEREST INCOME – INT

TOTAL ASSETS

Figure 6: Return on Asset

17

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 18/38

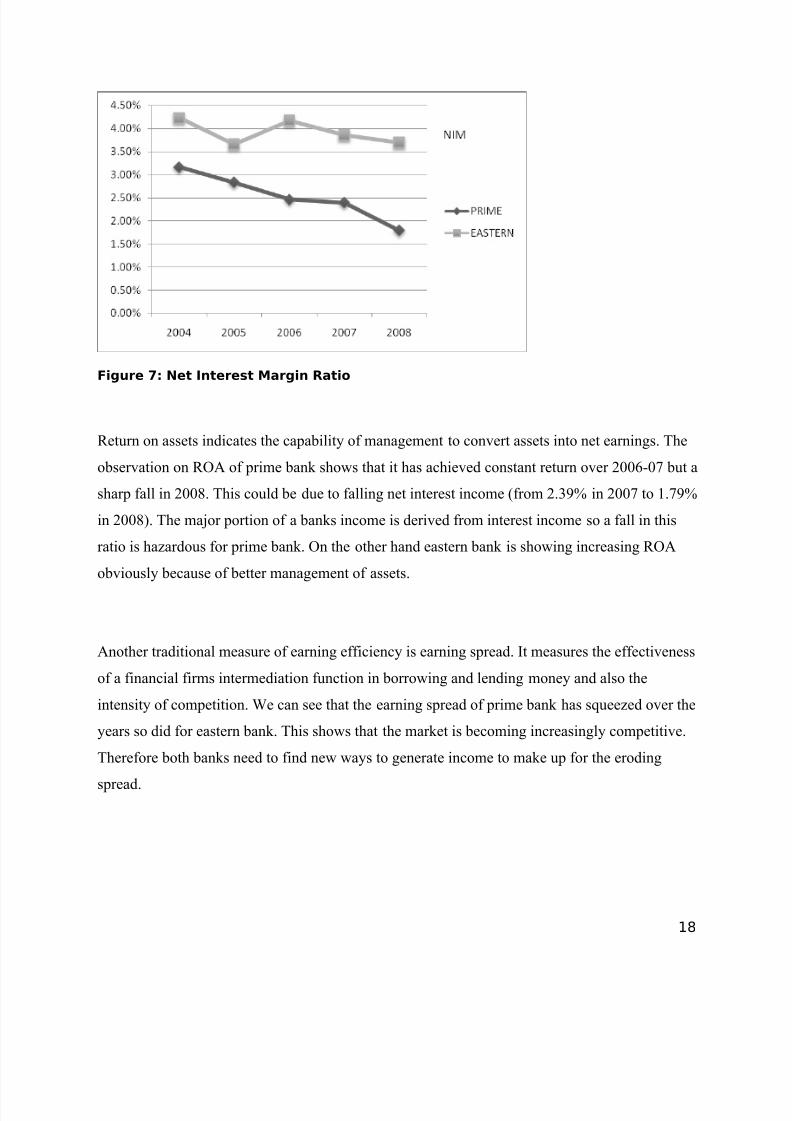

Figure 7: Net Interest Margin Ratio

Return on assets indicates the capability of management to convert assets into net earnings. The

observation on ROA of prime bank shows that it has achieved constant return over 2006-07 but a

sharp fall in 2008. This could be due to falling net interest income (from 2.39% in 2007 to 1.79%

in 2008). The major portion of a banks income is derived from interest income so a fall in this

ratio is hazardous for prime bank. On the other hand eastern bank is showing increasing ROA

obviously because of better management of assets.

Another traditional measure of earning efficiency is earning spread. It measures the effectiveness

of a financial firms intermediation function in borrowing and lending money and also the

intensity of competition. We can see that the earning spread of prime bank has squeezed over the

years so did for eastern bank. This shows that the market is becoming increasingly competitive.

Therefore both banks need to find new ways to generate income to make up for the eroding

spread.

18

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 19/38

OPERATING EFFIC

OPERATING EX

OPERATING

EM PLOYEE PROD

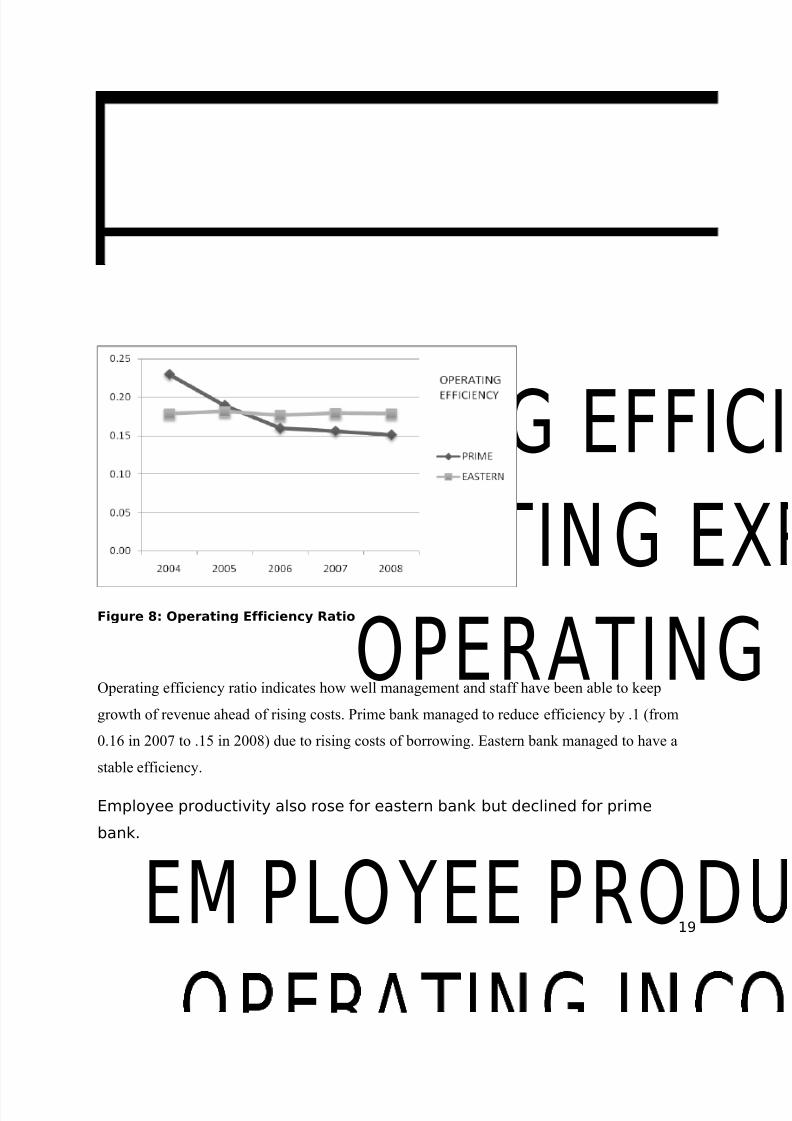

Figure 8: Operating Efficiency Ratio

Operating efficiency ratio indicates how well management and staff have been able to keep

growth of revenue ahead of rising costs. Prime bank managed to reduce efficiency by .1 (from

0.16 in 2007 to .15 in 2008) due to rising costs of borrowing. Eastern bank managed to have a

stable efficiency.

Employee productivity also rose for eastern bank but declined for prime

bank.

19

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 20/38

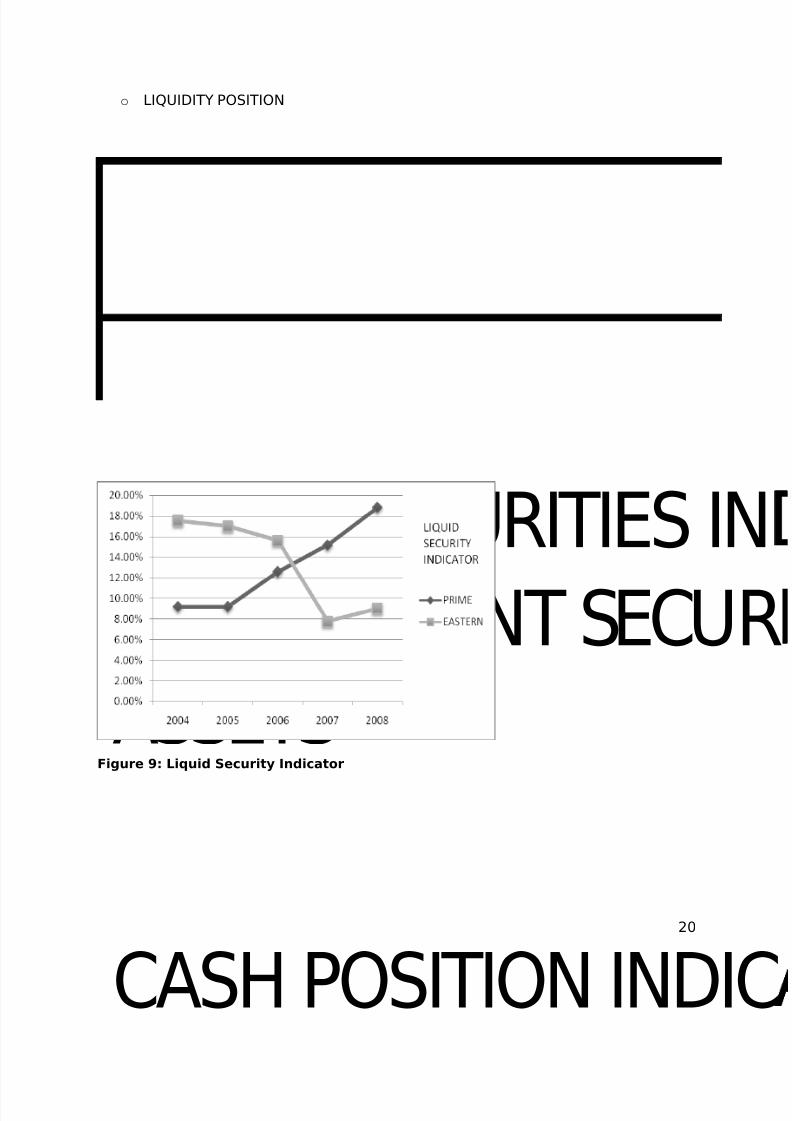

o LIQUIDITY POSITION

LIQUID SECURITIES IN

GOVERNMENT SECU

ASSETS

CASH POSITION INDI

Figure 9: Liquid Security Indicator

20

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 21/38

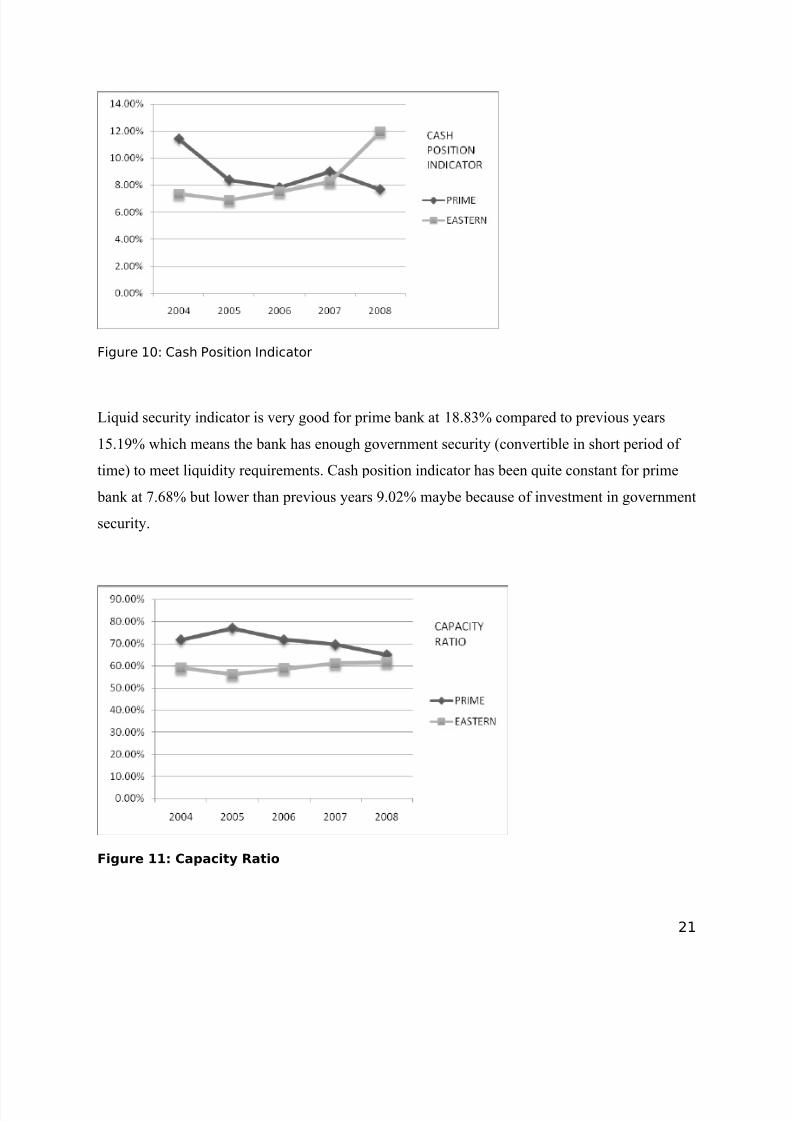

Figure 10: Cash Position Indicator

Liquid security indicator is very good for prime bank at 18.83% compared to previous years

15.19% which means the bank has enough government security (convertible in short period of

time) to meet liquidity requirements. Cash position indicator has been quite constant for prime

bank at 7.68% but lower than previous years 9.02% maybe because of investment in government

security.

Figure 11: Capacity Ratio

21

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 22/38

Rising liquid security indicator proves the lower capacity ratio. Company has been investing in

government and private interest bearing security rather than increasing loans and leases.

Therefore, capacity ratio fell from previous year 69.57% to 64.92%. This is good for liquidity

because loans and leases are the most illiquid of all assets. However, it may indicate opportunity

cost of greater earning capacity.

The liquidity position of prime is very good and in a confident position not to disrupt the

reputation of the company.

On the other hand, liquidity position of eastern bank is not better than prime bank in terms of

liquid security indicator and cash position indicator and the capacity ratio do not show greater

investment in loans and leases. Maybe they are holding too much cash in vault or other

depository institution or invested in capital expenditure.

22

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 23/38

DEBT RATIO: T

LIABILITIES/TOTA

DEBT TO EQUIT

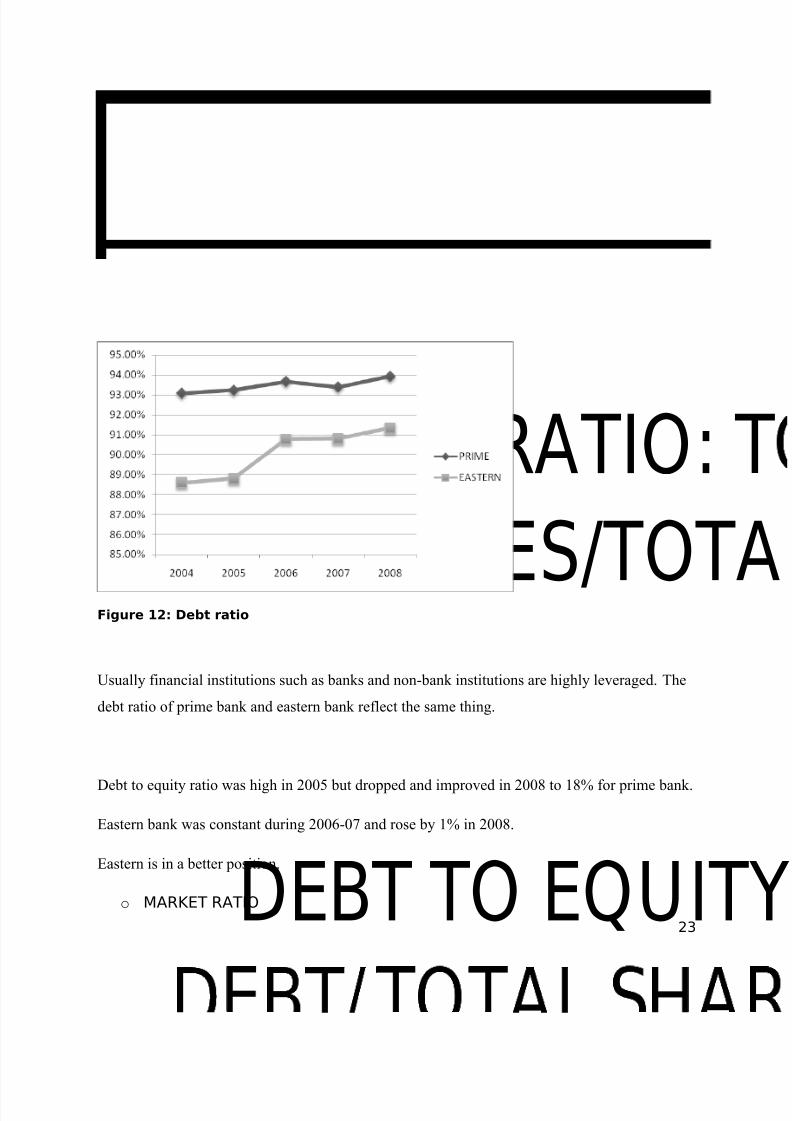

Figure 12: Debt ratio

Usually financial institutions such as banks and non-bank institutions are highly leveraged. The

debt ratio of prime bank and eastern bank reflect the same thing.

Debt to equity ratio was high in 2005 but dropped and improved in 2008 to 18% for prime bank.

Eastern bank was constant during 2006-07 and rose by 1% in 2008.

Eastern is in a better position.

o MARKET RATIO

23

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 24/38

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 25/38

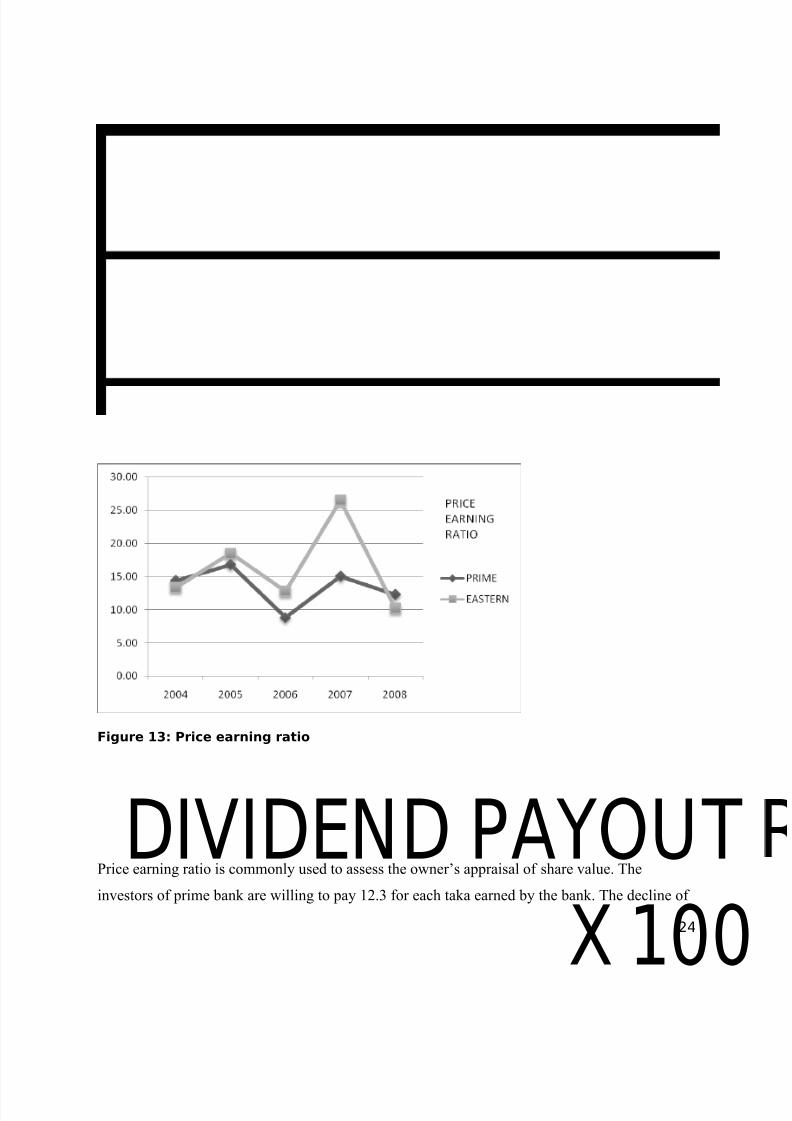

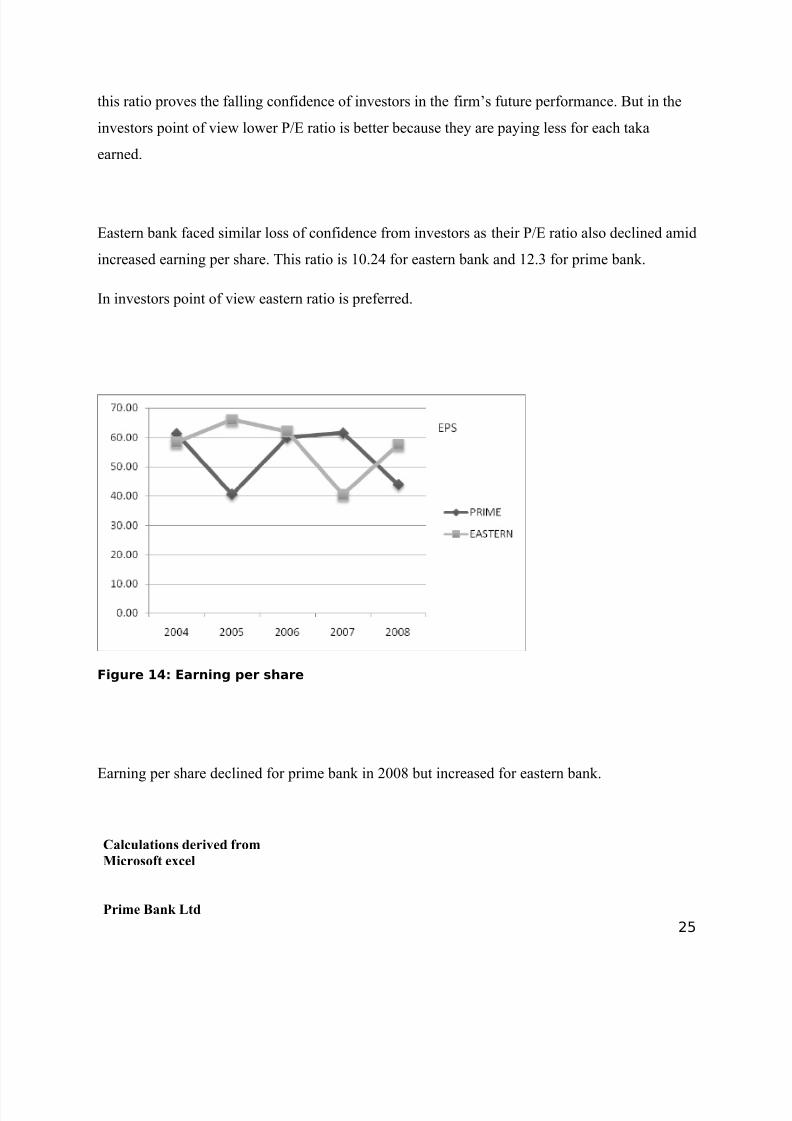

this ratio proves the falling confidence of investors in the firm’s future performance. But in the

investors point of view lower P/E ratio is better because they are paying less for each taka

earned.

Eastern bank faced similar loss of confidence from investors as their P/E ratio also declined amid

increased earning per share. This ratio is 10.24 for eastern bank and 12.3 for prime bank.

In investors point of view eastern ratio is preferred.

Figure 14: Earning per share

Earning per share declined for prime bank in 2008 but increased for eastern bank.

Calculations derived from

Microsoft excel

Prime Bank Ltd

25

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 26/38

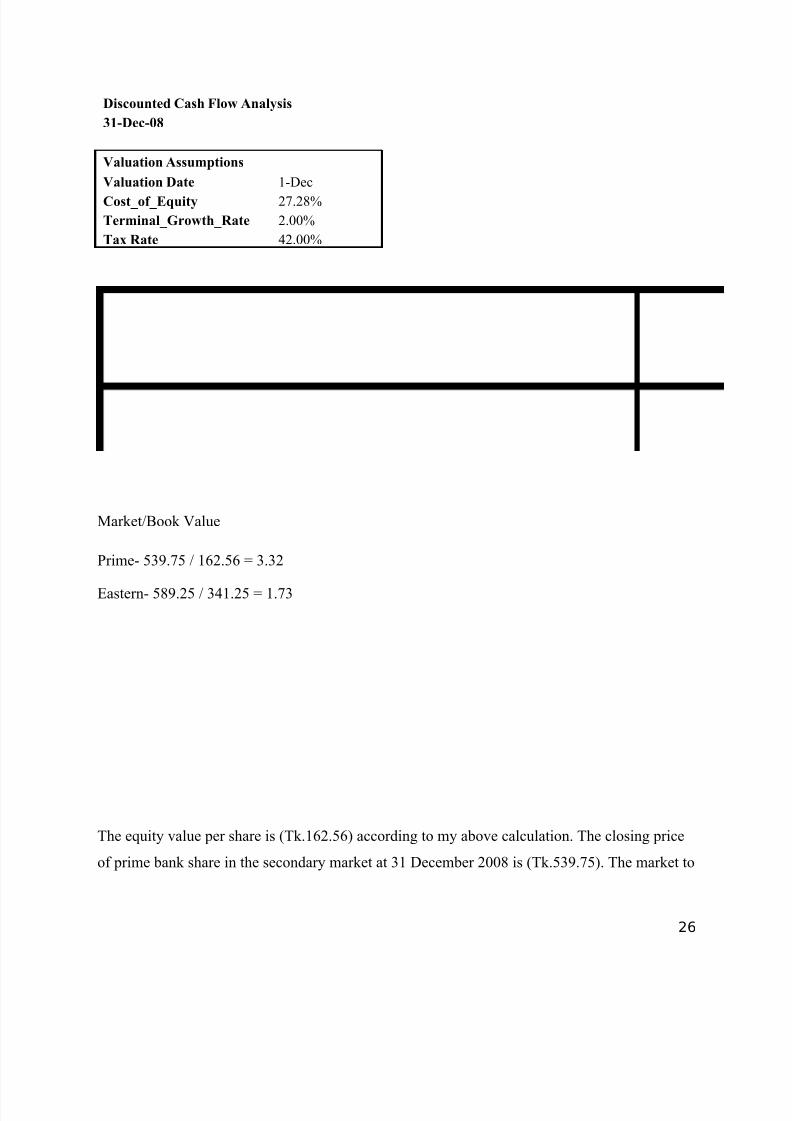

Discounted Cash Flow Analysis

31-Dec-08

Valuation Assumptions

Valuation Date 1-Dec

Cost_of_Equity 27.28%

Terminal_Growth_Rate 2.00%

Tax Rate 42.00%

Market/Book Value

Prime- 539.75 / 162.56 = 3.32

Eastern- 589.25 / 341.25 = 1.73

The equity value per share is (Tk.162.56) according to my above calculation. The closing price

of prime bank share in the secondary market at 31 December 2008 is (Tk.539.75). The market to

26

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 27/38

book value ratio suggests 3.32. The market price of the share is overpriced. It means if the

market reaches a position of correctness than the price of share might fall.

On the other hand, the equity value of eastern bank is 341.25 according to some calculations.

The closing price is Tk. 589.25 as at 31 December 2008. The market to book value is 1.73.

The ratio is lower for eastern bank so this stock is preferred over the other.

Recommendation

27

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 28/38

TAX MANA

EXPENSE C

EQUITY MULTIPLIER

ROE

ROA

NET INTEREST MARGI

NET NON INTEREST MA

Profitability

The overall profitability of eastern bank is better than prime bank ltd.

The average ROE of prime bank shows favorable than eastern bank, yet it is declining in 2008 so

it is not reflective of good earnings this year. The ROA of prime bank is falling due to falling net

interest income. On the other hand, eastern bank is showing increasing trend. Eastern bank has a

stable operating efficiency compared to prime banks declining ratio.

Liquidity

Prime bank is in better position of liquidity management compared to eastern bank derived from

conclusions using liquid security indicator, cash position indicator and capacity ratio.

28

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 29/38

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 30/38

The outcome of this report suggests that an investor holding prime bank shares at the time should

sell off their shares to avoid depletion of their wealth. The advice to prospective investors is to

utilize their money by investing in eastern bank shares because the prospects are rewarding.

Both the companies are first generation banks and have achieved considerable amount of growth

since their inception. The markets for secondary shares are always risky in Bangladesh because

the stock market here is what is known as ‘inefficient market’. Sometimes the fundamentals of a

company does not reflect actual price of the share in the market. However, I tried my best to get

a picture from my viewpoint and present a recommendation.

Bibliography

30

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 31/38

1. http://ebl.com.bd

2. Annual Reports of Eastern Bank Ltd (2004-2008).

3. www.primebank.com.bd/

4. Annual Re ports of Prime Bank Limited (2004-2008).

5. Peter S. Rose & Sylvia C. Hudgins, Bank Management & Financial Services, 7th edition,

2008, McGraw-Hill publications.

31

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 32/38

Appendix 1

Profitability ratio and efficiency ratio

32

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 33/38

YEAR

NET INCOM E

INTEREST EXPENSE

NON INTEREST REVENU

NON INTEREST EXPENS

PRETAX NET OP. INCOM

TOTAL OPERATING EXP

TOTAL OPERATING RE

TAX MANAGEMENT

33

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 34/38

RETURN ON ASSET (R

NET INTEREST MARGININEREST INCOME – INT

TOTAL ASSETSOPERATING EFFICI Leverage Ratio

34

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 35/38

YEAR

TOTAL EQUITY

TOTAL LIABIDEBT RATIO

LIABILITIES/TO Liquidity Ratio

35

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 36/38

GOVERNM ENT SECU

YEA

CASH & DEPOSIT DU

INSTITUTION

NET LOANS AND LEA

Market Ratio

36

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 37/38

8/6/2019 tasmia afsari

http://slidepdf.com/reader/full/tasmia-afsari 38/38

Appendix 2