Task 23 Task Meeting The Role of Customers in Delivering ... DSM Task 23 Experts Meeting No... ·...

107

Task 23 Task Meeting The Role of Customers in Delivering Effective Smart Grids 4 th and 5 th July Steinkjer, Norway

Transcript of Task 23 Task Meeting The Role of Customers in Delivering ... DSM Task 23 Experts Meeting No... ·...

Task 23 Task Meeting

The Role of Customers in Delivering

Effective Smart Grids

4th

and 5th

July

Steinkjer, Norway

Agenda Day One: Thursday 4th July

09:00 Sub-task 2:

Re-cap on aims / objectives of sub-task

Review of progress

Identify any gaps

Agree way forward

10:00 Review of case studies 15 minute (max) presentation by Experts on country case study – focus on presenting

main lessons learnt from customer perspective

Netherlands (Yvonne)

Norway (Even)

Sweden (Magnus)

11:00 Break

11:30 Review of case studies – continued

Italy (Simone)

UK (Esther)

Republic of Korea (Yeoungjin)

Re-cap of main lessons learnt (All)

12:30 Update from UK team

Consumer survey

13:00 Lunch

14:00 DemoSteinkjer demonstration

17:00 Close

2

Agenda Day Two: Friday 5th July

09:00 Sub-task 3:

Re-cap on aims / objectives of sub-task

Review of progress

Identify any gaps

Agree way forward

10:00 Sub-task 4:

Re-cap on aims / objectives of sub-task

Agree way forward

10:45 Break

11:00 Sub-task 5:

Re-cap on aims / objectives of sub-task

Agree way forward

11:45 Date / location of next meeting

What happens at end of current work programme?

12:00 Lunch

13:00 Close

3

Agenda Day One: Thursday 4th July

09:00 Sub-task 2:

Re-cap on aims / objectives of sub-task

Review of progress

Identify any gaps

Agree way forward

10:00 Review of case studies 15 minute (max) presentation by Experts on country case study – focus on presenting

main lessons learnt from customer perspective

Netherlands (Yvonne)

Norway (Even)

Sweden (Magnus)

11:00 Break

11:30 Review of case studies – continued

Italy (Simone)

UK (Esther)

Korea (Yeoungjin)

Re-cap of main lessons learnt (All)

12:30 Update from UK team

Consumer survey

13:00 Lunch

14:00 DemoSteinkjer demonstration

17:00 Close

4

Overall Aim

“ to identify and, where possible, quantify the risks and rewards associated with Smart Meters and Smart Grids from the perspective of the consumer, both now and in

the future”

5

Scope

– “limited to customers with Smart Meters and thus, likely to be expected to play an important role in the future as Smart Grids are deployed”

• Customer Types – Residential

– Small Commercial, business and local authority customers

• Have similar access to the market as residential customers

6

Expected Outcome

• Identification of the factors that need to be addressed in order to ensure Smart Grids are able to achieve their full potential by ensuring that all industry stakeholders, including customers, benefits from their deployment.

• Achieved through: – Understanding of impact of energy markets on customers

– Understanding of interaction between technology and customers

– Identification of Risks and Rewards associated with Smart Grids from the perspective of customers

– Identification of offers and programmes that help ensure Smart Grids meet the needs of customers

7

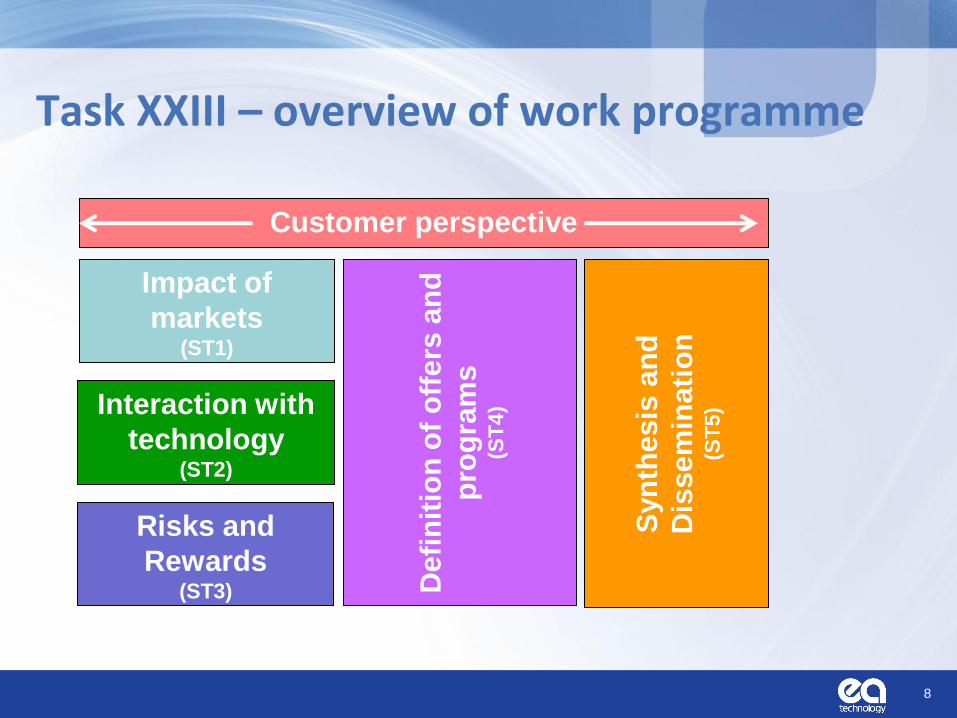

Task XXIII – overview of work programme

8

Impact of

markets (ST1)

Interaction with

technology (ST2)

Risks and

Rewards (ST3) D

efi

nit

ion

of

off

ers

an

d

pro

gra

ms

(ST

4)

Syn

thesis

an

d

Dis

se

min

ati

on

(S

T5)

Customer perspective

Task 23:

9

TECHNOLOGY TOOLS

POLICY

CUSTOMER

SMART GRID

TECHNOLOGY TOOLS

POLICY

CUSTOMER

TECHNOLOGY TOOLS

POLICY

CUSTOMER

TECHNOLOGY TOOLS

POLICY

CUSTOMER

SMART GRID

Technology: • Smart meter

• In-home display

• Smart appliances

Policy: • Smart meter standards

• Smart appliance standards

• Mandate for Time of Use tariffs

• Market structure

• Settlement arrangements

• Billing arrangements

Tools: • Time of Use Tariff

• Energy services

• Demand aggregation

• Energy advice

ST 2: Interaction with Technology

Activity Funding Status Agree scope of

technologies to be included

Cost Share and Task Share Done

Background research on

agreed technologies

Cost Share Done

Country specific

experiences from specific

pilots and trials

Task Share On-going

Assess TRLs and MRLs Cost Share On-going

Identify key factors impact

on customers

Cost Share On-going

What we said we would do

Subtask 2 Report

• Background

• Approach

• Consumer Surveys

• Case Studies

• Conclusions

11

Sub-Task 2: Scope widened to look at interventions not just technology

12

Intervention Description

Time of Use Tariff (T)

A form of pricing that penalises consumers that use energy at certain times and/or rewards consumption at other times. This can include static Time of Use (ToU) tariffs, Critical Peak Pricing (CPP), Peak Time Rebates (PTR), Real Time Pricing (RTP).

Control (C)

Controls to actively manage the pattern of consumption. This can include direct load control, automatic load controls, home energy management systems, thermostats for heating and air-conditioning and building energy management systems.

Feedback (F)

Feedback of energy end use information based on the actual energy end use of the individual, i.e. relying on data collected from the smart meter. This can include in-home displays of real time and historic data, web based feedback and billing information. Alternative forms of feedback also exist, such as web-based feedback or the use of smart phones or other portable devices.

Advice (A)

Advice on how consumers can deliver outcomes that support the effective delivering of Smart Grids. This can include advice targeted to an individual on processes/end uses that can be managed, or general advice distributed to groups.

Understanding Energy Behaviour

13

Approach

• Consumer Surveys – 21 surveys reviewed

– Looking at customer reactions to:

• Smart Grids / Smart Metering

• Electricity industry in general

• Other related topics (travel)

• Case Studies – ~30 case studies selected

– Case study template used to gather information

14

Assessment

• Four criteria – Initiative Readiness Level

– Market Readiness Level

– Customer Willingness

– Customer Engagement

15

Initiative Readiness Level

16

IRL 9: Actual system completed and qualified through successful operations

IRL 8: Actual system completed and qualified through test and demonstration

IRL 7: System prototype demonstration in an operation environment

IRL 6: System/subsystem or prototype demonstration in a relevant environment

IRL 5: Components and/or basis subsystem validation in a relevant environment

IRL 4: Components and/or basis subsystem validation in a laboratory environment

IRL 3: Analytical and experimental critical function and/or characteristic proof-of-concept

IRL 2: Concept and/or application formulated

IRL 1: Basic principles observed and reported

IRL 9

IRL 6

IRL 5

IRL 3

IRL 2

IRL 4

IRL 8

IRL 7

IRL 1

Market Readiness Level

17

MRL 9: Approach fully understood and accepted by vast majority of consumers. (e.g. a mobile phone has become a social ‘norm’ rather than landlines for many calls)

MRL 8: Most consumers understand the principles, but only accepted as the ‘norm’ for certain groups (e.g. the use of a Smart Phone to access the internet is regarded as the ‘norm’ for young)

MRL 7: Benefits reasonably well understood by all, but may not be sufficient to drive demand except for certain niche markets (i.e. costs considered to outweigh the benefits) (e.g. iPAD)

MRL 6: General awareness of benefits, but majority of individuals unable to identify the costs/benefits to themselves. (e.g. need for a 3D TV not well justified)

MRL 5: Some customers actively attempting to find out more, i.e. there is some ‘market pull’ from early adopters, but benefits/costs not well understood by most customers.

MRL 4: Some customers aware of basic principles , but limited or no information on potential benefits/costs )

MRL 3: Some consumers starting to actively find out more

MRL 2: Some consumer awareness – but limited, small minority open minded to the idea

MRL 1: Consumers as a whole are unaware

MRL 9

MRL 6

MRL 5

MRL 3

MRL 2

MRL 4

MRL 8

MRL 7

MRL 1

Customer Willingness

• How were participants invited to take part in the initiative? – Was it voluntary?

• How were they recruited?

• Was there a high drop out rate?

– Was it mandatory?

• What were the main concerns of customers?

• Were any changes made to accommodate customer concerns?

• What happened at the end of the initiative? – Did they revert back to ‘business as usual’?

– Did they retain the interventions (i.e. did they stay on the ToU tariff)?

18

Customer Engagement

• The extent to which customers were actively engaged in an initiative, – By how much did their energy consumption behaviour change

• Quantitative – % energy reduction

– % peak reduction

• Qualitative – Reduced thermostat settings

– Switched off appliances when not used

– Shifted usage of appliances

19

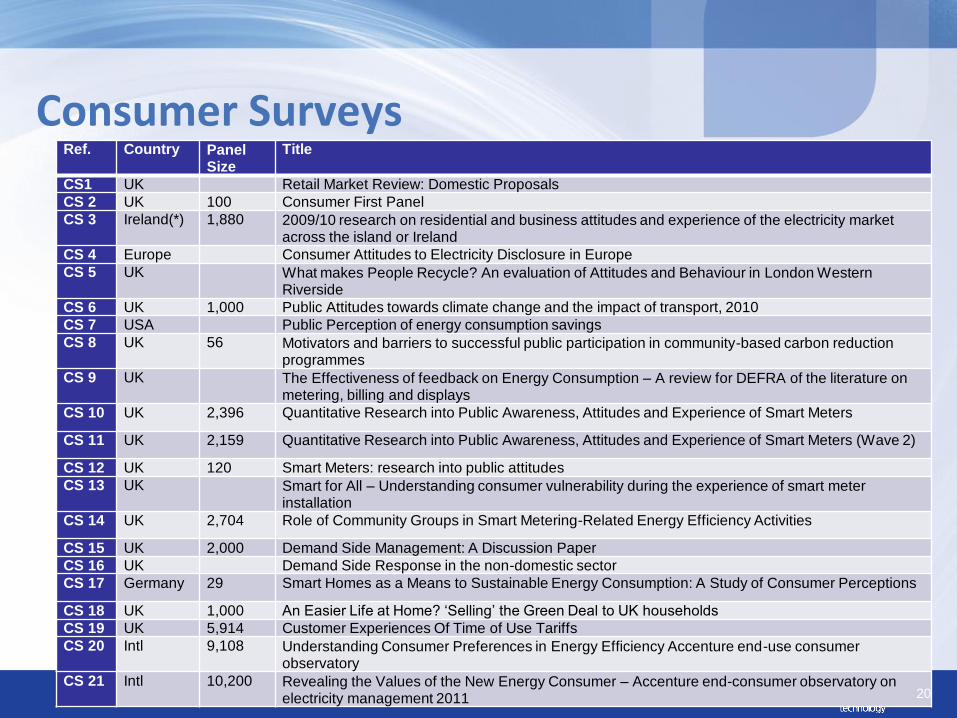

Consumer Surveys Ref. Country Panel

Size Title

CS1 UK Retail Market Review: Domestic Proposals CS 2 UK 100 Consumer First Panel CS 3 Ireland(*) 1,880 2009/10 research on residential and business attitudes and experience of the electricity market

across the island or Ireland CS 4 Europe Consumer Attitudes to Electricity Disclosure in Europe CS 5 UK What makes People Recycle? An evaluation of Attitudes and Behaviour in London Western

Riverside CS 6 UK 1,000 Public Attitudes towards climate change and the impact of transport, 2010 CS 7 USA Public Perception of energy consumption savings CS 8 UK 56 Motivators and barriers to successful public participation in community-based carbon reduction

programmes CS 9 UK The Effectiveness of feedback on Energy Consumption – A review for DEFRA of the literature on

metering, billing and displays CS 10 UK 2,396 Quantitative Research into Public Awareness, Attitudes and Experience of Smart Meters

CS 11 UK 2,159 Quantitative Research into Public Awareness, Attitudes and Experience of Smart Meters (Wave 2)

CS 12 UK 120 Smart Meters: research into public attitudes CS 13 UK Smart for All – Understanding consumer vulnerability during the experience of smart meter

installation CS 14 UK 2,704 Role of Community Groups in Smart Metering-Related Energy Efficiency Activities

CS 15 UK 2,000 Demand Side Management: A Discussion Paper CS 16 UK Demand Side Response in the non-domestic sector CS 17 Germany 29 Smart Homes as a Means to Sustainable Energy Consumption: A Study of Consumer Perceptions

CS 18 UK 1,000 An Easier Life at Home? ‘Selling’ the Green Deal to UK households CS 19 UK 5,914 Customer Experiences Of Time of Use Tariffs CS 20 Intl 9,108 Understanding Consumer Preferences in Energy Efficiency Accenture end-use consumer

observatory CS 21 Intl 10,200 Revealing the Values of the New Energy Consumer – Accenture end-consumer observatory on

electricity management 2011 20

Overview of results of

Consumer Surveys

21

22

Consumer understanding of the electricity industry

Consumer Awareness of the Electricity Market – an example

Are consumers aware of the industry stakeholders and what they do?

Role Residential Customers

Republic of Ireland

ESB

Networks

Supplier Don’t know

Responsibility for

power failure

repair

56% 28% 15%

Maintenance of

grid

56% 25% 18%

Responsibility for

Meter reading

17% 64% 16%

Responsibility for

billing and

payment

10% 74% 14%

Findings from the 2009/2010 research on residential and business attitudes and experiences of the electricity market across the island

of Ireland, The Research Perspective Ltd for CER and Utility Regulator, 2010, p20

Implications?

24

Reasons for not switching electricity supplier

Like current service A factor 54%

Not a factor 19%

No reason to A factor 46%

Not a factor 28%

Concern about an alternative

supplier’s provision of a reliable supply

of electricity

A factor 36%

Not a factor 34%

Concern about alternative supplier to

be as responsive if there is a power

outage

A factor 35%

Not a factor 35%

Do not believe that prices will remain

as low as the alternative supplier

claims

A factor 35%

Not a factor 32%

Which electricity supplier

should I choose?

25

Consumer awareness of specific

technologies and concepts – Smart

Meter example

Yes, I have one 5%

Yes, but I don't have

one 44%

No, I have never heard

of them 50%

Before today, had you heard of smart meters?

Quantitative Research into Public Awareness, Attitudes, and Experience of Smart Meters, wave 2, Feb 2013,

MORI for DECC

26

Consumer awareness of specific

technologies and concepts – Smart

Meter example

Quantitative Research into Public Awareness, Attitudes, and Experience of Smart Meters, wave 2, Feb 2013,

MORI for DECC

A great deal 5%

A fair amount

19%

Just a little 56%

Heard but know

nothing 20%

How much, if anything, would you say you know about smart meters?

Comments on Smart Meters …

• “It is quite a good idea really but they want every home in the UK to have one and it makes you think who is going to pay for it? The costs will be passed onto us one way or another, they always are.”

• “I find it hard to see why an energy supplier should give you a device that means you use less of their product.”

• “I’ve got a smart meter, it’s a white one, they booked and told us when they were going to come, they said it was a smart meter, but I had no idea what that meant, I didn’t know it transmitted data till this gentleman said just now.

27 Smart Meters: research into public attitudes, Navigator for DECC, 2012

Consumer awareness of technologies In Home Display example

• Participants in a trial were asked “Do you have a visual display in your home, that tells you how much electricity or gas you are using?”

Intervention RTD

(elec only)

RTD

(dual fuel)

RTD + ToU RTD + Usage

Alarm

RTD +

Heating

controller

Total

Yes 45.8% 35.2% 50.9% 62.4% 36.1% 46.5%

No 54.2% 64.8% 49.1% 37.6% 63.9% 53.5%

Number 83 105 114 109 97 508

Energy Demand Research Project: Final Analysis, AECOM, June 2011

RTD = real time display

ToU = time of use (tariff)

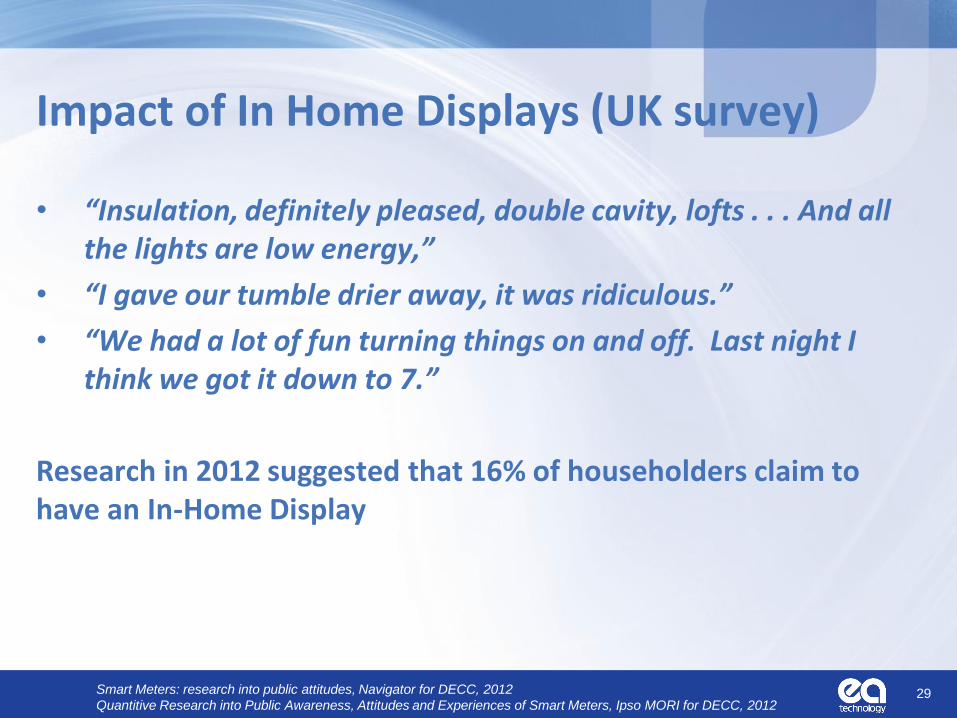

Impact of In Home Displays (UK survey)

• “Insulation, definitely pleased, double cavity, lofts . . . And all the lights are low energy,”

• “I gave our tumble drier away, it was ridiculous.”

• “We had a lot of fun turning things on and off. Last night I think we got it down to 7.”

Research in 2012 suggested that 16% of householders claim to have an In-Home Display

29 Smart Meters: research into public attitudes, Navigator for DECC, 2012

Quantitive Research into Public Awareness, Attitudes and Experiences of Smart Meters, Ipso MORI for DECC, 2012

Consumer Awareness of Energy Efficiency

• What actions lead to the greatest energy savings?

• What is the magnitude of energy savings?

30 Understanding Consumer Preferences in Energy Efficiency, Accenture end-consumer observatory on electricity management 2010

yes, 75%

no, 25%

Do you think you understand enough about the actions you can take to to optimise your energy consumption?

yes, 75%

no, 25%

Do you think you understand enough about the actions you can take to to optimise your energy consumption?

Consumer Awareness of Energy Efficiency

• What actions lead to the greatest energy savings?

• What is the magnitude of energy savings?

• A 2010 US study found: – Consumers not proficient at identifying ways of saving energy

• Focus on curtailment actions rather than energy efficiency improvements

• Tendency to underestimate energy use

• Particularly the magnitude of differences

31 Public perceptions of energy consumption and savings, Shahzeen Z et al., PNAS, 2010

Understanding of specific technologies and concepts - DSR

• Very little awareness that the wholesale cost of electricity changes within the day

• Difficulty understanding the benefits of deferring peak electricity consumption

Demand Side Response: A discussion paper, 82/10, Ofgem, July 2010, p33

32

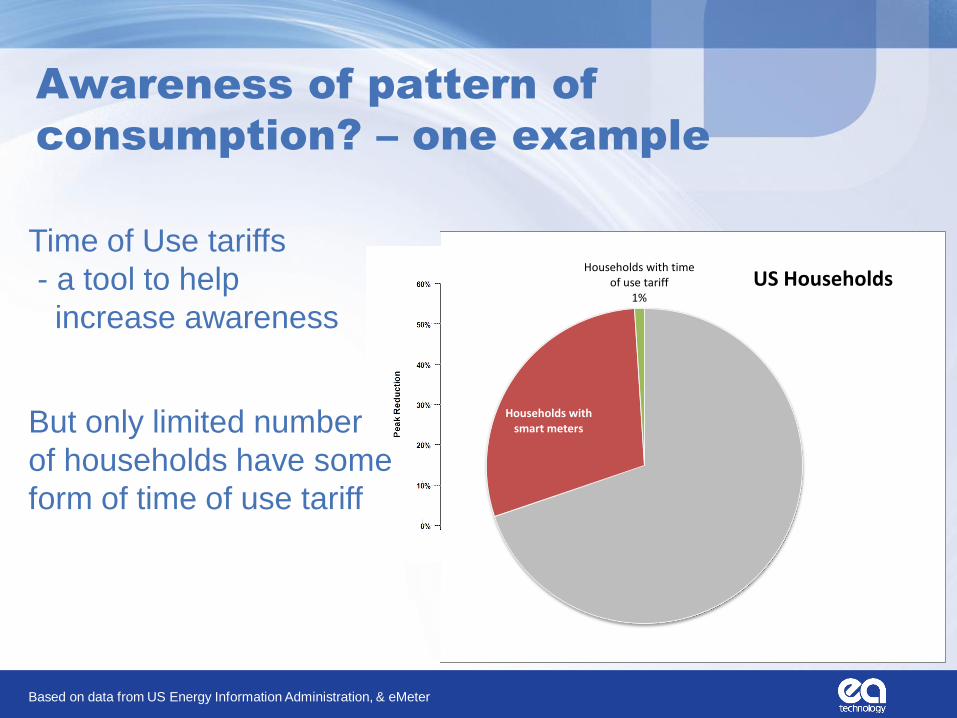

Awareness of pattern of

consumption? An example

Source: SEMO

€305/MWh

€52/MWh

Disjoint between retail price paid by customers and wholesale price

Retail price (€/MWh)

Awareness of pattern of

consumption? – one example

Households with smart meters

Households with time of use tariff

1%

US Households

But only limited number

of households have some

form of time of use tariff

Based on data from US Energy Information Administration, & eMeter

Time of Use tariffs

- a tool to help

increase awareness

How long might the process of changing public attitudes and behaviours take?

• Look at two examples:

– Drink Driving in the UK

– Recycling in the UK

35

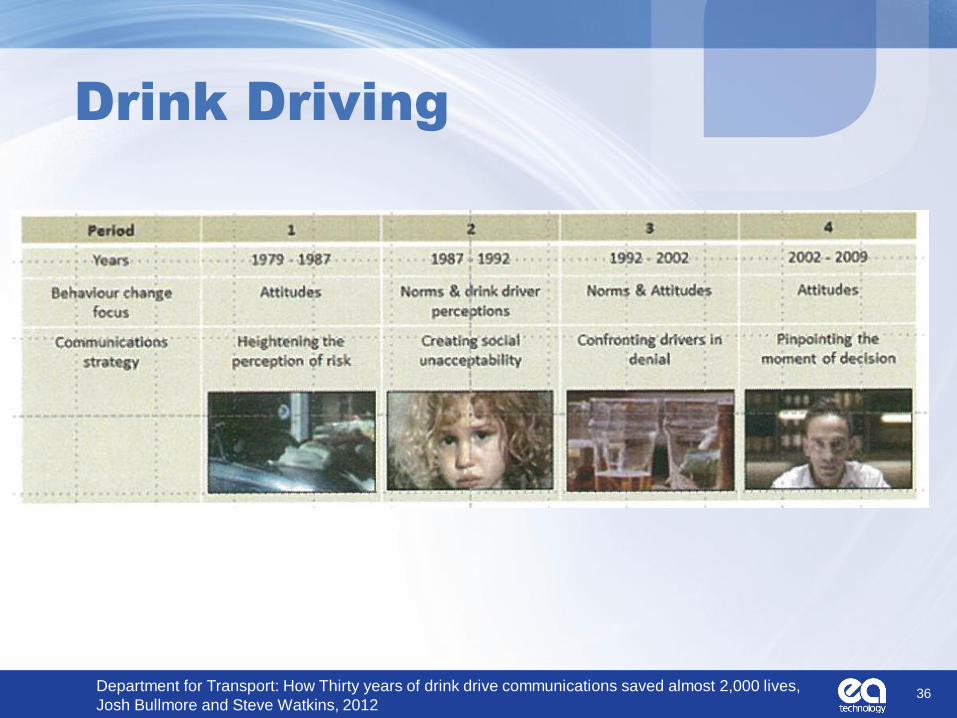

Drink Driving

36 Department for Transport: How Thirty years of drink drive communications saved almost 2,000 lives,

Josh Bullmore and Steve Watkins, 2012

Drink driving

37

38

Recycling - England

http://www.defra.gov.uk/statistics/environment/waste/wrfg16-recycrates/

Why do consumers participate in Smart Grid related initiative?

• Money?

• Environment?

• Communal good?

• Other benefits?

39

Money?

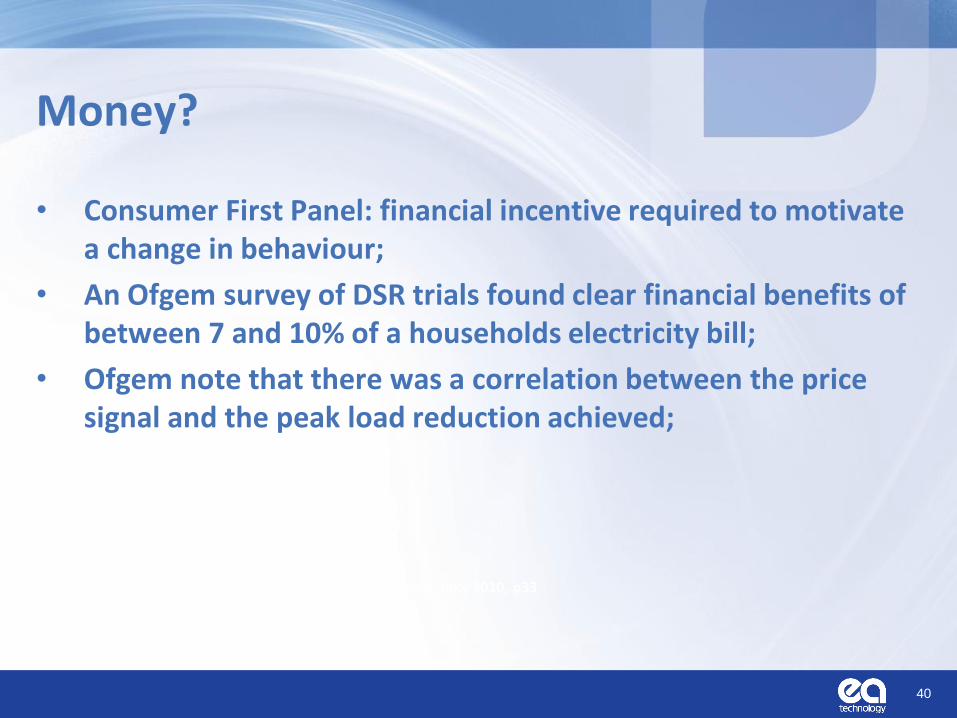

• Consumer First Panel: financial incentive required to motivate a change in behaviour;

• An Ofgem survey of DSR trials found clear financial benefits of between 7 and 10% of a households electricity bill;

• Ofgem note that there was a correlation between the price signal and the peak load reduction achieved;

•Demand Side Response: A Discussion Paper, 82/10, Ofgem, Juky 2010, p33

40

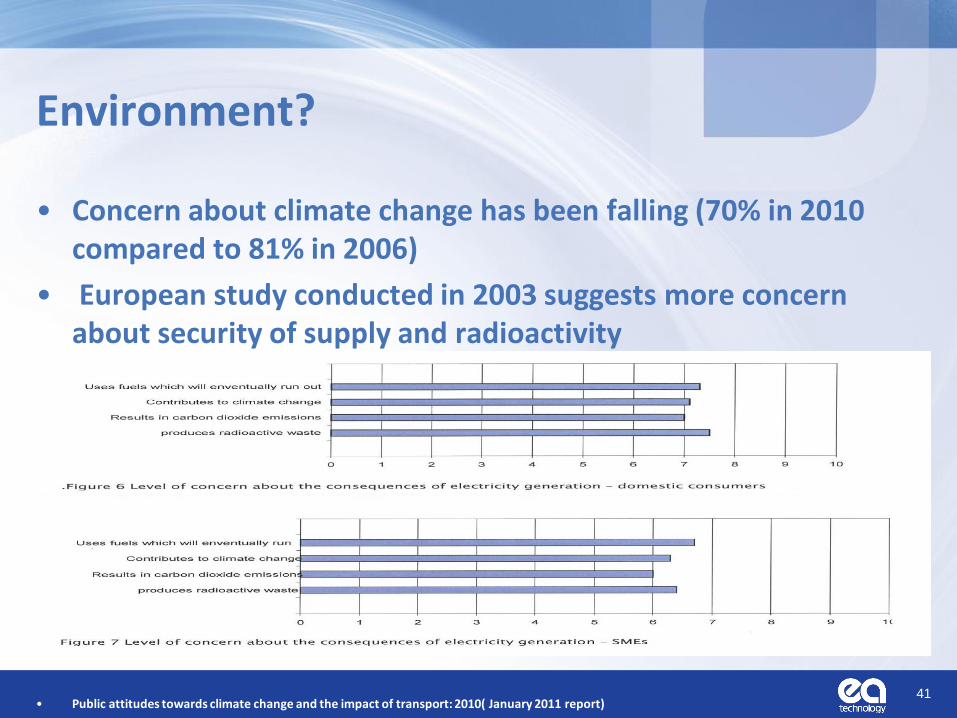

Environment?

• Concern about climate change has been falling (70% in 2010 compared to 81% in 2006)

• European study conducted in 2003 suggests more concern about security of supply and radioactivity

• Public attitudes towards climate change and the impact of transport: 2010( January 2011 report)

• Consumer attitudes to electricity disclosure in Europe, 4C Electricity, 2003

41

Environment?

• “Environment, no, not at the moment, it should, and if everything in garden was rosy and times not so hard you would pay attention to that, and it would be a factor, but that’s not the way things are at the moment.”

• “I could do more but the eco thing irritates me slightly, don’t do this, do that, but one Jumbo for Spain uses more energy in one take off than my whole street does in a year.”

• “They’re not doing it for the good of the environment.”

•Smart Meters: research into public attitudes, p36

42

Communal good?

Eco-Watts trial, Brittany, France.

• Problems with network constraints limiting supply to the Brittany peninsular, - only generates 8% of electricity it uses and a high level of electric heating

• Introduced a voluntary scheme to encourage households to alter electricity use during periods of peak demand

• 9,400 customers signed up in 2008/9. By 2012 50,000 households had signed up

• Demand reduced by 2-3% in the winter of 2011/12 during critical periods

• Alerts delivered by internet, SMS, Mobile phone apps, RSS feeds and email

• No rewards, just an explanation about the problem and the threat of a loss of supply, plus a sense of community in the region

Would this work in the everywhere?

•http://www.ecowatt-bretagne.fr/

43

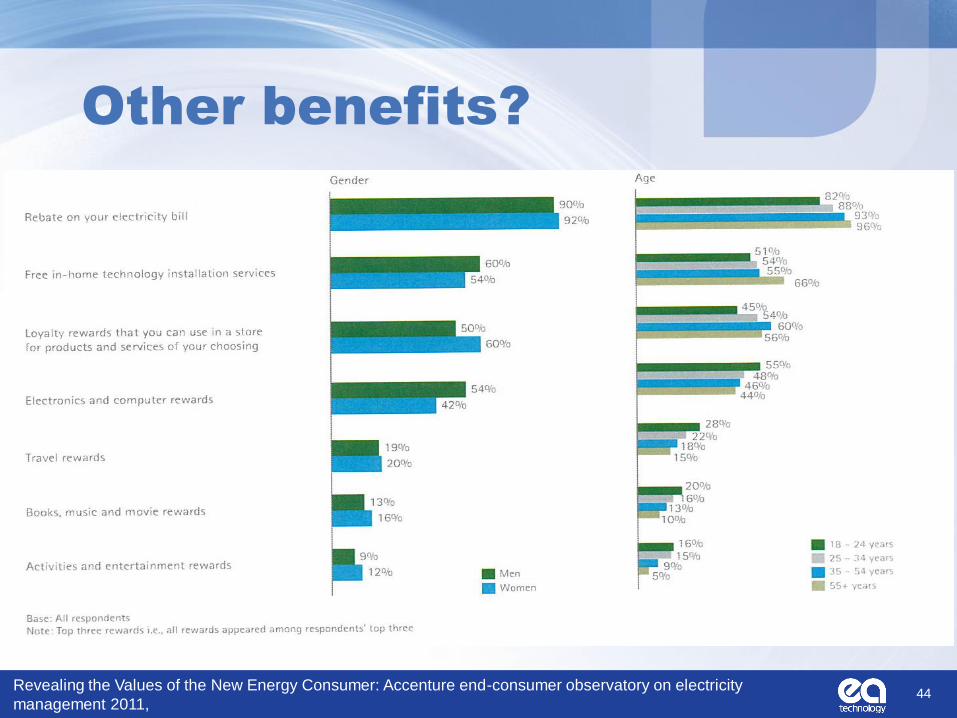

Other benefits?

44 Revealing the Values of the New Energy Consumer: Accenture end-consumer observatory on electricity

management 2011,

Will consumers participate?

47

27

58

37

21

46

0

10

20

30

40

50

60

70

use public transportmore

cycle more often walk more often

%

Willingness to use other modes more often instead of travelling by car

willing to able to

45 Public attitudes towards climate change and the impact of transport: 2010 (January 2011 report, ONS,

Conclusion of Consumer Surveys

• Increasing interest in energy efficiency but ignorance of structure of the industry, Smart Meters and DSR;

• Consumers are motivated by money but other, non-financial rewards could be considered;

• They may be willing to consider DSR • Not well understood at the moment

46

Overview of Case Studies – so fare

• General Comments – Lots of trials underway

• Little published to date

– ‘What did not go well’

• Not well publicised

– Focus generally on % load reduction / £ savings

47

Early conclusions from case studies - based on UK, US, Australia results - will be updated following meeting for NE, NO, IT, SE, KR case studies

• Pilots involving Time of Use Tariffs: – Customers often provided with assurance that they will not pay more

than they would have done

– Some customer unwilling to operate appliances at night due

• safety concerns

• Loss of convenience

– Customer disappointed by scale of bill reduction

– Customers are willing to compromise on comfort

• CPP trials of a/c and heating

48

Early conclusions from case studies - based on UK, US, Australia results - will be updated following meeting for NE, NO, IT, SE, KR case studies

• Control of end use appliances – Most experience is with air-conditioning / space heating

• In areas where these contribute significantly to peak load

– In UK – no single load contributes to peak load (from domestic) • With possible exception of lighting / cooking

• Not obvious targets for peak load shifting

– Customers willingness to cede control of their appliances to third parties varies considerably

• Examples from US show willingness is ‘high’

• Examples from Australia suggest willingness is much lower

– Worry about damage occurring to their equipment

– Unhappy about installers entering their property

• Large incentives often provided to persuade customers to participate

– Free heating system (UK / remote control of heat pumps)

49

Early conclusions from case studies - based on UK, US, Australia results - will be updated following meeting for NE, NO, IT, SE, KR case studies

• Feedback via IHDs – Displays including £’s liked by customers

– Traffic light displays liked

– Audible warnings disliked

– Interaction with a computer – less popular

– More effective if combined with energy efficiency advice

• Even where they are already aware of that advice

50

Next steps

• Incorporate findings from remaining case studies

• Complete report

• Circulate to Experts for approval

• Circulate to ExCo for approval

• Publish

51

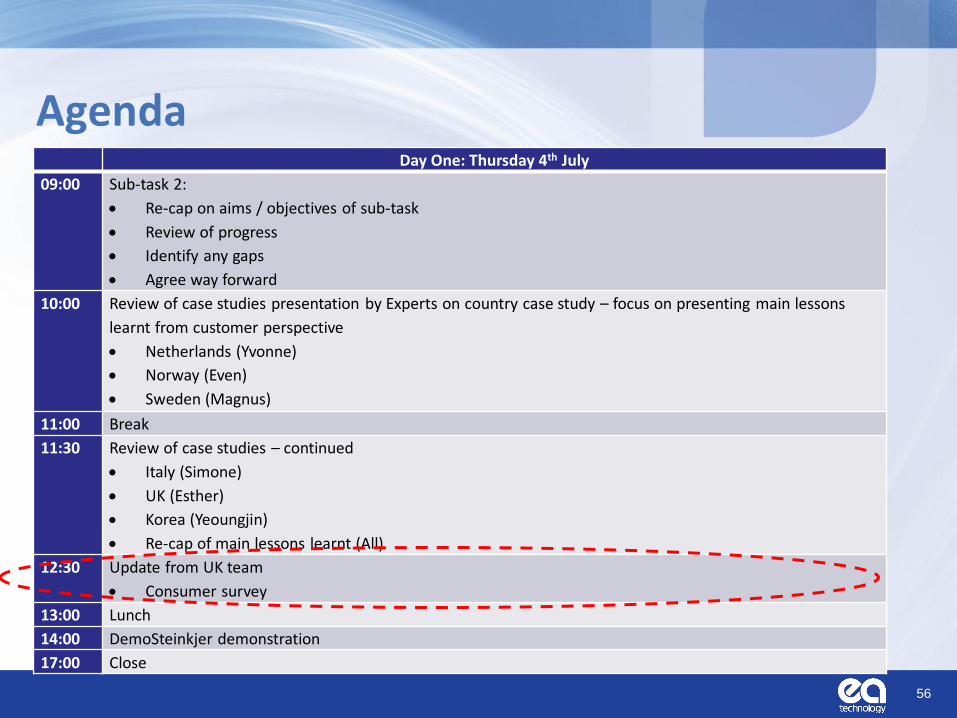

Agenda Day One: Thursday 4th July

09:00 Sub-task 2:

Re-cap on aims / objectives of sub-task

Review of progress

Identify any gaps

Agree way forward

10:00 Review of case studies presentation by Experts on country case study – focus on presenting main lessons

learnt from customer perspective

Netherlands (Yvonne)

Norway (Even)

Sweden (Magnus)

11:00 Break

11:30 Review of case studies – continued

Italy (Simone)

UK (Esther)

Korea (Yeoungjin)

Re-cap of main lessons learnt (All)

12:30 Update from UK team

Consumer survey

13:00 Lunch

14:00 DemoSteinkjer demonstration

17:00 Close

52

Review of Case Studies

• Main points to highlight: – What did customer like?

– What customers didn’t like?

– Was it difficult to recruit / retain customers?

53

Case Studies

• Discussion – General conclusions

– Main learning points

– What worked well / what didn’t work well?

54

ST 2: Interaction with Technology

Activity Funding Status Agree scope of

technologies to be included

Cost Share and Task Share Done

Background research on

agreed technologies

Cost Share Done

Country specific

experiences from specific

pilots and trials

Task Share On-going

Assess TRLs and MRLs Cost Share On-going

Identify key factors impact

on customers

Cost Share On-going

What we said we would do

Agenda Day One: Thursday 4th July

09:00 Sub-task 2:

Re-cap on aims / objectives of sub-task

Review of progress

Identify any gaps

Agree way forward

10:00 Review of case studies presentation by Experts on country case study – focus on presenting main lessons

learnt from customer perspective

Netherlands (Yvonne)

Norway (Even)

Sweden (Magnus)

11:00 Break

11:30 Review of case studies – continued

Italy (Simone)

UK (Esther)

Korea (Yeoungjin)

Re-cap of main lessons learnt (All)

12:30 Update from UK team

Consumer survey

13:00 Lunch

14:00 DemoSteinkjer demonstration

17:00 Close

56

Agenda Day One: Thursday 4th July

09:00 Sub-task 2:

Re-cap on aims / objectives of sub-task

Review of progress

Identify any gaps

Agree way forward

10:00 Review of case studies presentation by Experts on country case study – focus on presenting main lessons

learnt from customer perspective

Netherlands (Yvonne)

Norway (Even)

Sweden (Magnus)

11:00 Break

11:30 Review of case studies – continued

Italy (Simone)

UK (Esther)

Korea (Yeoungjin)

Re-cap of main lessons learnt (All)

12:30 Update from UK team

Consumer survey

13:00 Lunch

14:00 DemoSteinkjer demonstration

17:00 Close

57

Agenda Day Two: Friday 5th July

09:00 Sub-task 3:

Re-cap on aims / objectives of sub-task

Review of progress

Identify any gaps

Agree way forward

10:00 Sub-task 4:

Re-cap on aims / objectives of sub-task

Agree way forward

10:45 Break

11:00 Sub-task 5:

Re-cap on aims / objectives of sub-task

Agree way forward

11:45 Date / location of next meeting

What happens at end of current work programme?

12:00 Lunch

13:00 Close

58

ST 3: Risks and Rewards

59

What we said we would do

Activity Status

Produce a matrix showing the

interrelationship between industry

stakeholder needs and customer

needs

Cost Share On-going

Identify specific case studies or

example scenarios Cost Share / Task Share In parallel with ST2

Identify risks and rewards arising

from case study / scenario analysis Cost Share / Task Share On-going

Develop a risk-reward calculator Cost Share -

Impact of markets

Interaction with

technology

Risks and

Rewards

Definition of

offers and

programs

Synthesis and

Dissemination

Customer perspective

ST 3: Risk and rewards

• Customer’s do not consider risks and rewards on an economically rational basis?

• Limited value in developing a ‘risk – reward calculator’

• Alternative approach proposed

• Focus on learning from case studies using a qualitative approach

• Use specific examples to highlight types of risks that are identified by consumers themselves

– If appropriate, quantify risks and rewards in a selected number of examples

60

ST 3: Risks and Rewards

What is risk?

• The possibility of misfortune or loss and is generally defined as the combination of: – The probability / likelihood of an undesirable event or outcome

occurring; and

– The resulting consequences / impacts if the undesirable event occurs

and what is reward?

• The possibility of fortune or gain and is generally defined as the combination of: – The probability / likelihood of a desirable event or outcome

occurring; and

– The resulting consequences / impacts if the desirable event occurs

Undesirable/Desirable Outcomes? Undesirable Desirable

Money / financial

(£, $, €,

loyalty points)

Spend more on electricity

(ToU tariff & don’t/can’t shift

demand)

Spend less on electricity

(ToU tariff & do shift demand, or

already have favourable energy

profile)

Receive a penalty for not

delivering a demand reduction

(Demand Response contract)

Receive payments for delivering

demand reduction / energy efficiency

(Demand Response contract)

Time /

Inconvenience

(minutes / hours)

Can’t use appliances at times of

peak demand

Time saved (through use of remote /

automatic control of appliances?)

Additional time taken to shop

around (e.g. to choose a smart

appliance)

Undesirable/Desirable Outcomes?

Undesirable Desirable

Comfort

(degC / year of

over/under

heating)

Colder house (if heating poorly

controlled or interruption too long)

Improved comfort through

avoided over/under-heating

Hotter house (if air-condition

poorly controlled or interruption

too long)

Environmental

(kg CO2 / year)

Increased CO2 emissions

(operation of standby generators)

Reduced CO2 emissions

(avoided use of fossil fired

central generation)

‘Feel good’

(units ??)

‘Feel Bad’ if can’t do anything to

change pattern of demand

‘Feel Good’ factor (e.g. feeling

that ‘doing your bit’ to help

reduce impact on the climate)

Network Security

(CMLs, CIs)

Improved security of supply

(reduced instances of black-

outs/brown outs)

Undesirable/Desirable Outcomes?

Undesirable Desirable

Others that lead to the consequences already identified:

Safety

Fire arising from appliances

running unattended while home is

unoccupied

• Impacts will be financial, time,

loss of ‘feel good’

Remote / Automated systems

could provide warnings that

appliances have been left on

unattended, or that no electricity

use may indicate that an elderly

person needs assistance.

Privacy

Misuse of data (i.e. to plan a

burglary)

• Impacts will be financial, time,

loss of ‘feel good’

Data could be used to advantage

of customers (to indicate when

appliances are faulty)

Decision Making process

• There are many different factors that affect the decision making process

66

Ambiguity

effect

Negativity

bias

Ingroup bias False-

consensus

effect

Status quo

bias

Illusion-of-

truth effect

Irrational

escalation.

Forer effect. Primacy effect Positivity

effect

Less-is-

better effect

Anchoring Neglect of p

robability

Just-world

phenomenon

Functional

fixedness

Stereotyping. Illusory

correlation

Conjunction

fallacy

Pro-

innovation bias

Change bias Empathy gap. Loss aversion.

Availability

heuristic

Observation

selection

bias

Naive cynicism Forer effect or

Barnum effect

Subjective

validation

Leveling and

Sharpening

Conservatism

(Bayesian)

Reactance Conservatism

/ Regressive

Bias

Essentialism Mere exposure

effect

Availability

cascade

Observer-

expectancy

effect

Outgroup

homogeneity bias

Framing effect Survivorship

bias

Levels-of-

processing

effect

Contrast effect Reactive

devaluation

Consistency

bias

Exaggerated

expectation

Money illusion

Congruence

bias

Post-

purchaserati

onalization

Choice-

supportive bias

Illusion of

validity

Serial position

effect Processing diffi

culty effect Reminiscence

bump Rosy retrospect

ion Self-relevance

effect Self-

serving bias Subadditivity

effect

Backfire effect Omission

bias

Projection bias Frequency

illusion

Texas sharpsh

ooter fallacy

List-

length effect

Curse of

knowledge

Recency bias Context effect Experimenter's

or expectation

bias

Moral

credential

effect.

Bandwagon

effect

Optimism

bias

Self-serving bias Gambler's

fallacy

Time-

saving bias

Misinformation

effect.

Decoy effect Recency

illusion

Cross-race

effect

Illusory

correlation

Source

Confusion .

Base rate

fallacy

Ostrich

effect

System

justification

Hard-

easy effect

Unit bias Misattribution Denomination

effect

Restraint bias Cryptomnesia Impact bias Spacing effect

Belief bias Outcome

bias.

Trait ascription

bias

Hindsight bias Well travelled

road effect

Modality effect Distinction bias Rhyme as

reason effect

Egocentric bias Information

bias

Stereotypical

bias

Attentional

bias

Normalcy

bias

Moral luck Focusing effect Subadditivity

effect

Lag effect Conservatism /

regressive

bias

Pseudo

certainty effect

Childhood amn

esia

Endowment

effect

Ludic fallacy.

Bias blind

spot

Overconfide

nce effect

Ultimate attribution

error

Hostile media

effect

Zero-risk bias Mood-

congruent

memory bias

Duration

neglect

Risk

compensation.

Fading affect

bias

Insensitivity to

sample size

False

consensus

effect

Choice-

supportive

bias

Pareidolia. Worse-than-

average effect

Hot-

hand fallacy

Zero-

sum heuristic

Next-in-

line effect.

Selective

perception.

False memory Social

desirability bias

Humor effect Just-world

hypothesis

Clustering

illusion

Pessimism

bias

Memory errors and

biases

Hyperbolic

discounting.

Social

biases

Osborn effect Semmelweis

reflex

Generation

effect.

Dunning Kruger

effect

Persistence Hindsight bias

Confirmation

bias

Planning

fallacy

Bizarreness

effect

Illusion of

control

Actor-

observer bias

Part-list

cueing effect

Selection bias. Google effect Egocentric bias Picture

superiority

effect

Defensive

attribution

hypothesis

Social

comparison

bias

Placement

bias

Recency effect Zeigarnik effect Verbatim effect

Telescoping

effect

Peak-end rule

Extrinsic

incentives bias Fundamental

attribution error Tip of the

tongue Von Restorff

effect

Suggestibility. Suffix effect

Illusory

superiority

Illusion of

transparency

Illusion of

external

agency

Illusion of

asymmetric

insight

Halo effect

Group

attribution error

67

Selected Factors That Affect Decision Making in Smart Grid context

• Loss Aversion

• Framing Effect

• How risks are valued – Absolute vs Relative

• The amount / type of choices available

• Faulty Discounting

• Priming

68

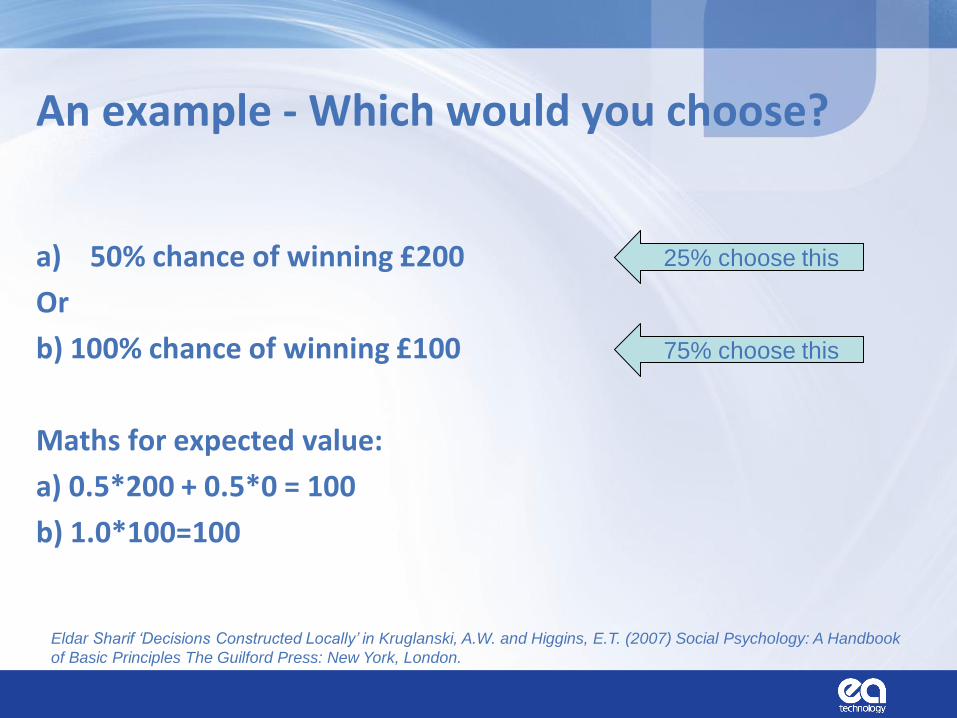

Risks & Rewards are not treated in the same way

• The ‘pleasure’ of winning £100

vs

• The ‘pain’ of losing £100

‘pain’ of losing £100 = 2+ x ‘pleasure’ of winning £100

As a result – losses and gains are treated differently

An example - Which would you choose?

a) 50% chance of winning £200

Or

b) 100% chance of winning £100

Maths for expected value:

a) 0.5*200 + 0.5*0 = 100

b) 1.0*100=100

25% choose this

75% choose this

Eldar Sharif ‘Decisions Constructed Locally’ in Kruglanski, A.W. and Higgins, E.T. (2007) Social Psychology: A Handbook

of Basic Principles The Guilford Press: New York, London.

An example - Which would you choose?

a) 50% chance of losing £200

Or

b) 100% chance of losing £100

Maths for expected value:

a) 0.5*200 + 0.5*0 = 100

b) 1.0*100 = 100

65% choose this

35% choose this

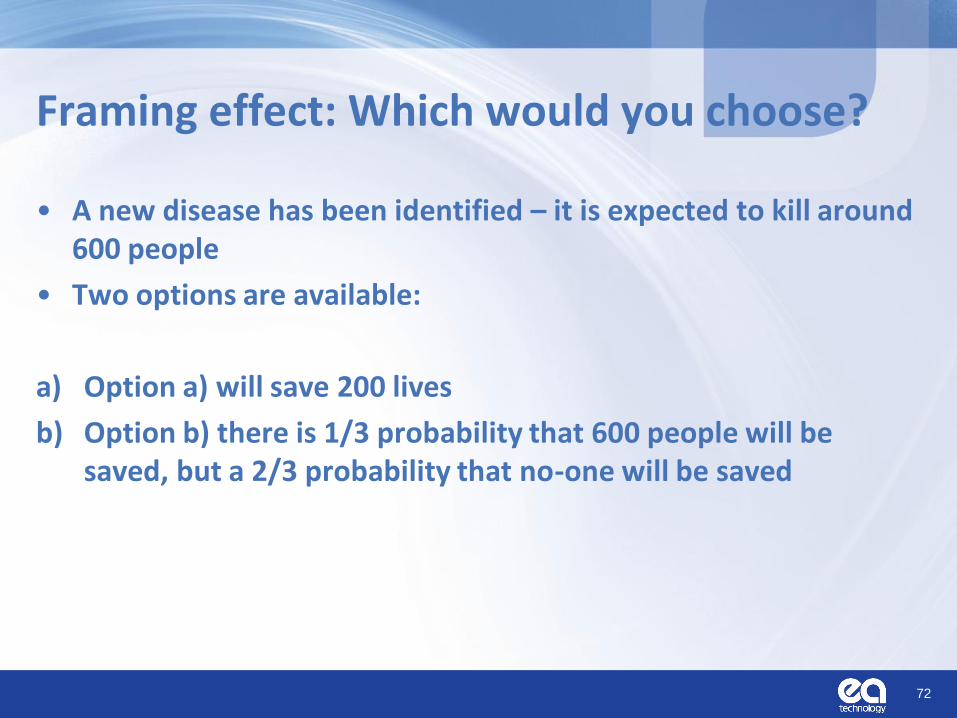

Framing effect: Which would you choose?

• A new disease has been identified – it is expected to kill around 600 people

• Two options are available:

a) Option a) will save 200 lives

b) Option b) there is 1/3 probability that 600 people will be saved, but a 2/3 probability that no-one will be saved

72

What about now?

• A new disease has been identified – it is expected to kill around 600 people

• What if you are given these two options:

c) Option c) 400 people will die

d) there is 1/3 probability that no-one will die, but a 2/3 probability that everyone will die

73

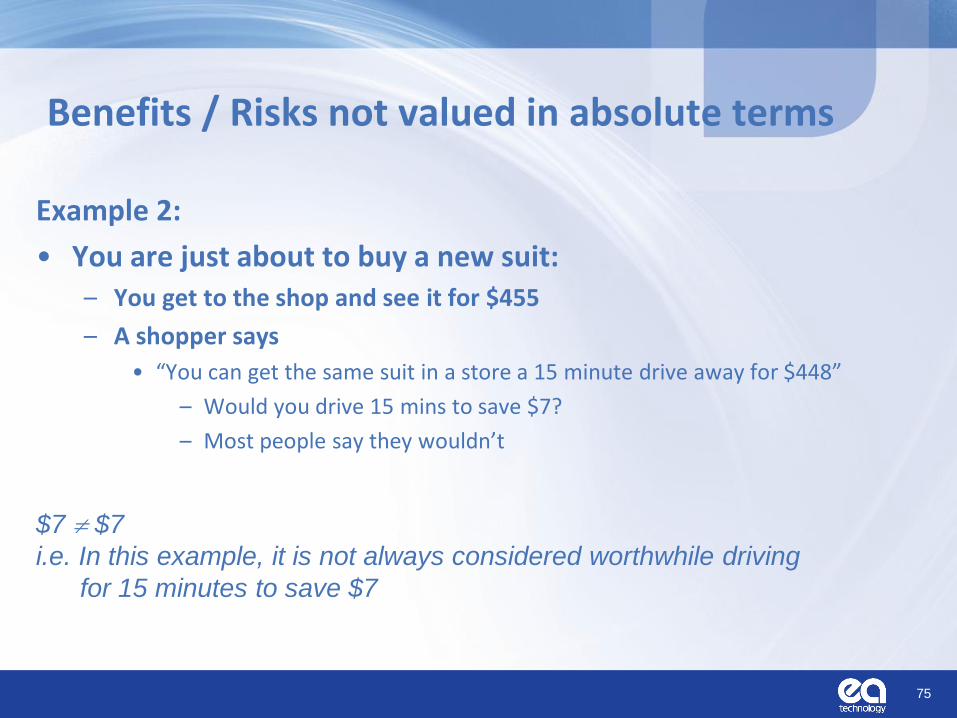

Benefits & Risks not valued in absolute terms

Example 1:

• You are just about to buy a new pen: – Arrive at the shop and see it for $25

– A shopper says

• “You can get the same pen in a store a 15 minute drive away for $18”

– Would you drive 15 mins to save $7?

– Most people say they would

74

Benefits / Risks not valued in absolute terms

Example 2:

• You are just about to buy a new suit: – You get to the shop and see it for $455

– A shopper says

• “You can get the same suit in a store a 15 minute drive away for $448”

– Would you drive 15 mins to save $7?

– Most people say they wouldn’t

75

$7 $7

i.e. In this example, it is not always considered worthwhile driving

for 15 minutes to save $7

Faulty Discounting

• People (generally) do not discount linearly with time

• Would you rather receive $100 now or $110 tomorrow? – More people prefer to receive $100 now rather than £110 in a day’s time

• Would you rather receive $100 in 30 days, or $110 in 31 days’ time? – Very few people choose £100 after 30 days’ time if they have the option to

choose £110 in 31 days’ time instead.

• Both options involve choosing whether or not to gain an additional £10 by delaying payment by one day. – Referred to as Hyperbolic discounting

– People tend to prefer to receive a smaller reward sooner rather than a larger reward later

• But this changes as the reward gets further into the future

76

Priming

• Consumers remember an item best in the form and context in which they first learned about it

77

Quantifying risks/rewards

– an example

78

Loft Insulation - example

• Rewards:- ~ £180/year reduced heating bill

~ 730kg/year reduced CO2 emissions

79 Source: Energy Saving Trust, http://www.energysavingtrust.org.uk/Insulation/Roof-and-loft-insulation

Based on three bedroomed semi-detached house, with no insulation, heated with gas

Loft Insulation

• Risks (example numbers only!!!):-

80

Type Consequence Probability Risk

Scratched paintwork €30 0.33 € 10

Damaged ceiling €200 0.01 € 2

Time (sorting) 8 hours 1 € 80

Damage to wiring €150 0.001 < € 1

Theft of valuable item €1000 .0004 < € 1

Total € 94

Is there another example?

ST 3: Risks and Rewards

81

What we said we would do

Activity Status

Produce a matrix showing the

interrelationship between industry

stakeholder needs and customer

needs

Cost Share On-going

Identify specific case studies or

example scenarios Cost Share / Task Share In parallel with ST2

Identify risks and rewards arising

from case study / scenario analysis Cost Share / Task Share On-going

Develop a risk-reward calculator Cost Share -

Impact of markets

Interaction with

technology

Risks and

Rewards

Definition of

offers and

programs

Synthesis and

Dissemination

Customer perspective

Stakeholder Needs

Want / opportunity Measure

Government Delivery of energy policy, meeting of

renewables and emissions targets

MW of installed renewable

generation

Number of electric cars

Installations of heat pumps etc.

Generators

(decentralised)

To be able to dispatch / store all electricity

generated Generating plant not constrained off

Suppliers

Best use of available resources and

therefore minimising energy costs

Smart meters will enable suppliers to

provide energy advice / tailored solutions

to customers

Meeting CO2 reduction obligations

Increased profitability

Improved customer satisfaction

leading to reduced customer churn

Reduction in CO2

Distribution Network

Operators

Facilitate the move to a low carbon

economy

Alleviate network constraints

Development of network in cost-effective

manner

Deferment or avoidance of network

investment

Optimised use of the existing

network

System Operator Sufficient resources to maintain balance

of supply and demand in real time System Availability

Appliance

Developers /

Manufacturers

Opportunities to develop smart equipment

/ appliances Number of appliances sold

82

Customer Needs

Want / need Examples

Customer Tangible benefits

Cost savings

Time savings

Incentives

(Improved comfort)

Information on usage / learning

Customer Autonomy

Choice (products / tariffs / service offering)

Control over home environment

Control over how information is shared / used

Some customer groups "Feel good" factor Reduced emissions / impact on climate

83

The interrelationship between industry stakeholder needs and customer needs

84

Cost savings Customers

Suppliers

Network

operators Behavioural Changes

Reduced energy

costs

ToU Tariff Deferred / avoided

CAPEX

Increased

profitability

Reduced network

charges

Outperform

regulatory targets Increased

profit

The interrelationship between industry stakeholder needs and customer needs

85

Information /

learning Customers

Cost savings

Suppliers

Network

Operators

Smart meter

data

Improved utilisation /

optimisation of network

assets

Improved

customer

satisfaction

Customer

retention

Increased

profits

Reduced energy

costs

Behavioural

changes

Reduced CO2

emissions

Carbon Emissions

Reduction

Obligation

Reduced network

charges Cost savings

Outperform

regulatory targets

Increased

profit

Matrix of needs / Interrelationship

• Use of flow charts rather than a matrix – Is this acceptable?

– Is this useful?

• Which other ‘scenarios’ should be considered?

86

ST 3: Risks and Rewards

87

What we said we would do

Activity Status Produce a matrix showing

the interrelationship

between industry

stakeholder needs and

customer needs

Cost Share On-going

Identify specific case

studies or example

scenarios

Cost Share / Task Share In parallel with ST2

Identify risks and rewards

arising from case study /

scenario analysis

Cost Share / Task Share On-going

Develop a risk-reward

calculator Cost Share Selected example(s)

Impact of markets

Interaction with

technology

Risks and

Rewards

Definition of

offers and

programs

Synthesis and

Dissemination

Customer perspective

Agenda Day Two: Friday 5th July

09:00 Sub-task 3:

Re-cap on aims / objectives of sub-task

Review of progress

Identify any gaps

Agree way forward

10:00 Sub-task 4:

Re-cap on aims / objectives of sub-task

Agree way forward

10:45 Break

11:00 Sub-task 5:

Re-cap on aims / objectives of sub-task

Agree way forward

11:45 Date / location of next meeting

What happens at end of current work programme?

12:00 Lunch

13:00 Close

88

Impact of

markets

Interaction with

technology

Risks and

Rewards

Definition

of offers

and

programs

Synthesis and

Dissemination

Customer perspective

Overview

Sub-task 4: What we said we would do

90

Activity Approach

Review of different approaches to

the implementation of Smart Grids

Operating Agent /

Participants

Cost Share /

Task Share

Identify examples of best practice Operating Agent Cost Share

Identify tools and measures Operating Agent Cost Share

Quantify potential impact of the

implementation of selected tools on

implementation of Smart Grids

Operating Agent Cost Share

Subtask4: Overview of proposal

• Smart Grid Implementation Requirements in order to achieve customer ‘buy-in’: – need to provide tangible benefits to customers

– need to minimise risks to customers

– What things should / could be mandated?

– What things should / could be standardised?

91

“The grid has gotten smarter over the last few years, but it has not captured the

imagination of mainstream consumers. Why? It’s because most people can’t

figure out how the smart grid improves their daily lives”, Gene Wang

http://www.smartgridnews.com/artman/publish/Business_Consumer_Engagement/Smart-homes-for-the-smart-grid-5818.html#.UdGSBZ1wapo

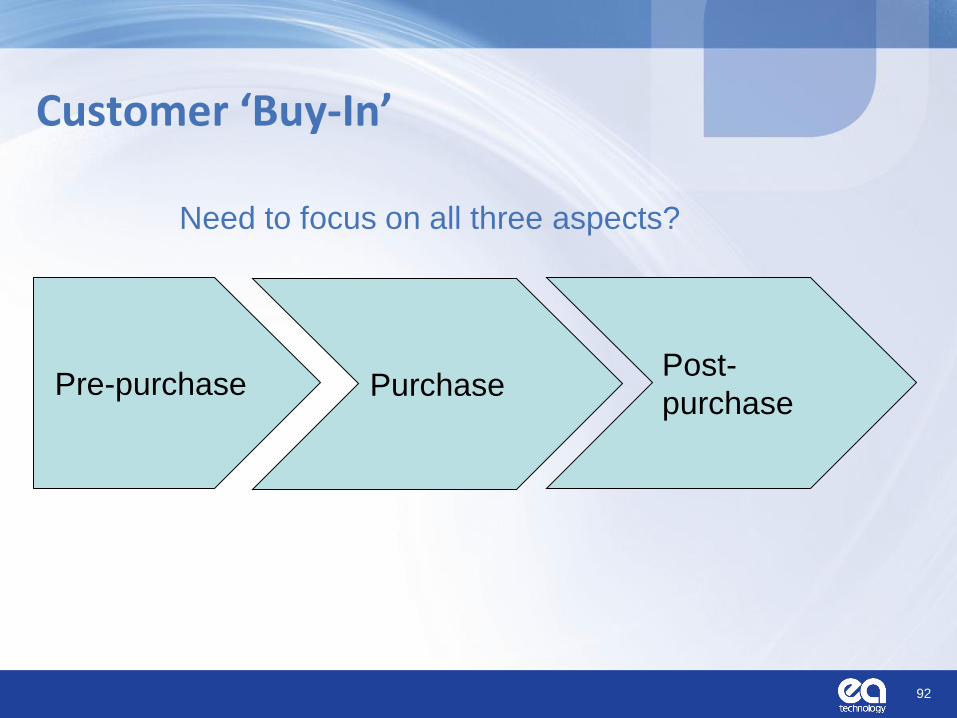

Customer ‘Buy-In’

92

Pre-purchase Purchase Post-

purchase

Need to focus on all three aspects?

Customer ‘Buy-In’

93

Pre-purchase Purchase Post-

purchase

Do I need to buy a car?

• Do I already have a car?

- Is it suitable for my needs?

• Can I use public transport?

• Can I walk/cycle?

What kind of car do I buy?

• A family car

• Car with lots of safety features

• A car that ‘looks good’

• A car that doesn’t cost too much

- to buy

- to run

- to maintain

How do I use my car

• Drive as efficiently as possible

• Always maintained / serviced

• Walk short distances

Car buying example

Car Advertising – target audiences

94

Family car

Sports car

Electric car

Offering:

• tailored to meet specific

needs of target audience

What is the target

audience for smart

grids?

Target market for Smart Grid offerings

Segmentation for dynamic pricing structures (Duneworks)

• Segment 1: Idealistic savers

• Segment 2: Selfless inconsistent energy savers

• Segment 3: Thrifty energy savers

• Segment 4: Materialistic energy consumers

• Segment 5: Comfort-oriented indifferent energy consumers

• Segment 6: Problem Conscious welfare oriented energy consumers

95

Toolbox of options

96

Options for Segment 1

97

Segmentation approach

• Is the Segmentation approach useful for Task 23

• Are the Segments appropriate for Task 23

98

Designing Offers – initial thoughts

• Tariffs: – Some choice (not too much / not too little)

– Default position needs to be chosen carefully

• What is the social norm?

• Technology: – Standards to ensure key technologies are compatible with DSR

• Heat pumps

• Electric vehicles

• Air-conditioners

– Appliances

• Need to prove benefits of smart appliances first

99

Allows possibility for customers to

participate in DSR in the future

Designing Offers – initial thoughts

• Feedback (In Home Displays):

• Advice / Education – 1 on 1 advice is very effective but very expensive

– Wide-scale customer campaigns can be effective

• Switch-over to Digital TV in UK

10

0

Mandated

Ensures all customers have

opportunity to receive feedback

‘one-size’ does not fit all

Optional Provides customers with choice

(do they want feedback and how

do they want to receive it)

Many reasons why customers

will not ‘take-up’ feedback

Key Requirements For Successful Smart Grids

• Access: – To information and communication networks

• Choice – Of products, partners and service offerings

• Control – Over the home environment and private information

• Value – From new services, products and quality of life

• Others

10

1

Tendril “A Vision of the Consumer Smart Grid”

Discussion

• Approach?

• Next steps?

• Outputs?

10

2

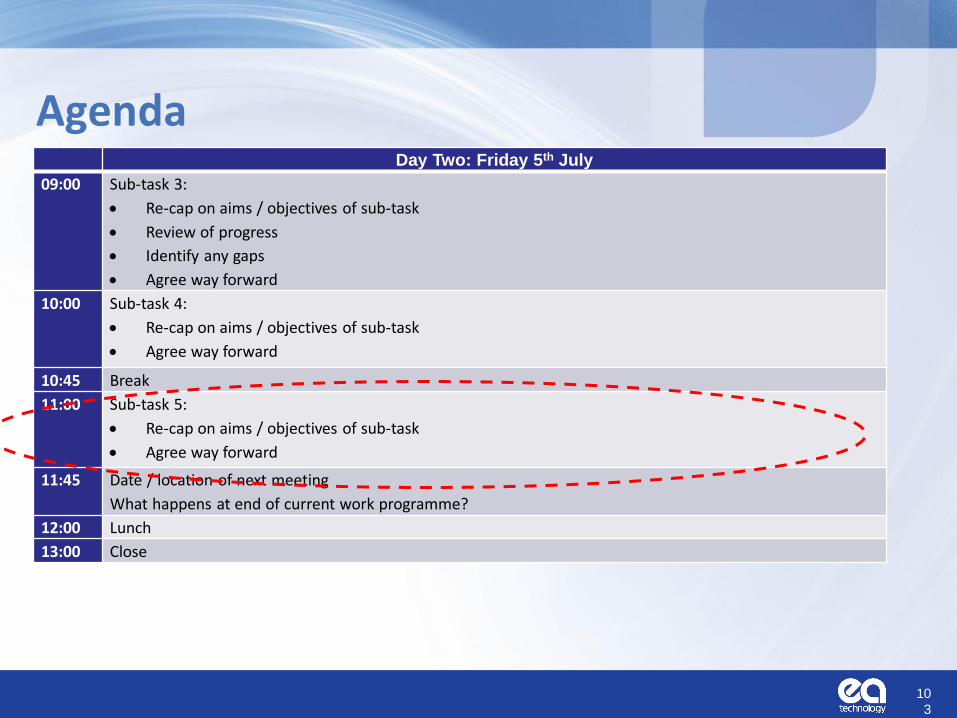

Agenda Day Two: Friday 5th July

09:00 Sub-task 3:

Re-cap on aims / objectives of sub-task

Review of progress

Identify any gaps

Agree way forward

10:00 Sub-task 4:

Re-cap on aims / objectives of sub-task

Agree way forward

10:45 Break

11:00 Sub-task 5:

Re-cap on aims / objectives of sub-task

Agree way forward

11:45 Date / location of next meeting

What happens at end of current work programme?

12:00 Lunch

13:00 Close

10

3

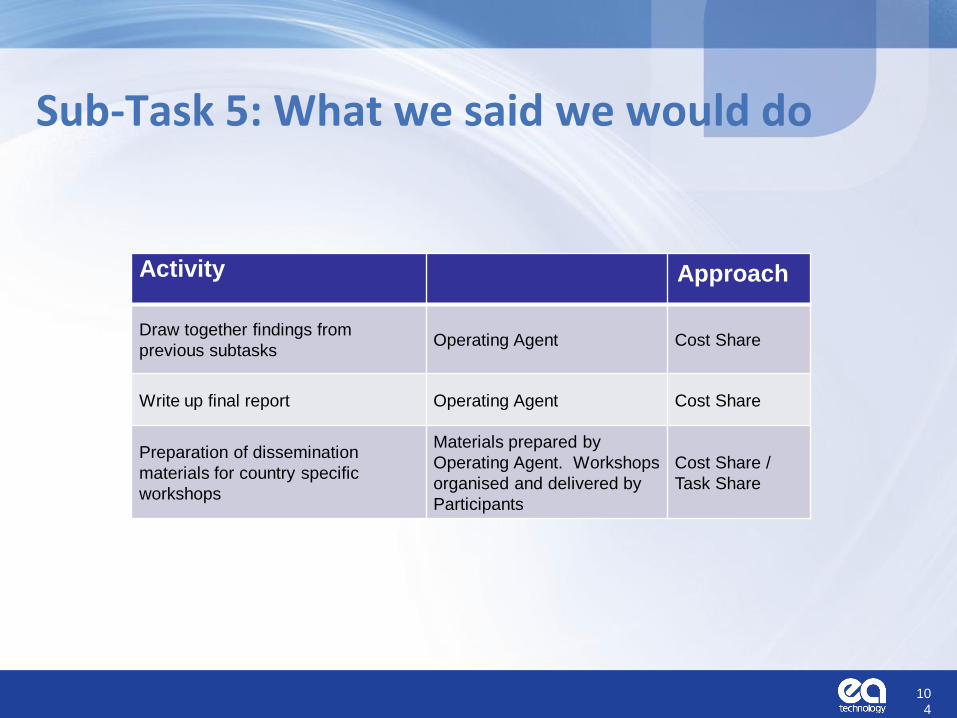

Sub-Task 5: What we said we would do

10

4

Activity Approach

Draw together findings from

previous subtasks Operating Agent Cost Share

Write up final report Operating Agent Cost Share

Preparation of dissemination

materials for country specific

workshops

Materials prepared by

Operating Agent. Workshops

organised and delivered by

Participants

Cost Share /

Task Share

Sub-Task 5

• What are National Experts planning for the dissemination phase? – What materials are required?

• Power-point

• Executive summary

• Newsletter articles

10

5

Discussion of what needed

Work Programme

10

6

Jun

-12

Jul-

12

Au

g-1

2

Sep

-12

Oct

-12

No

v-1

2

De

c-1

2

Jan

-13

Feb

-13

Mar

-13

Ap

r-1

3

May

-13

Jun

-13

Jul-

13

Au

g-1

3

Sep

-13

Oct

-13

No

v-1

3

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Subtask 1 Impact of markets

Subtask 2 Impact of technologies

Subtask 3 Risks and Rewards

Subtask 4 Tools

Subtask 5 Dissemination

Forecast

Planned

Actual

Planned

Actual

Planned

Actual

Planned

Forecast

Planned

Summary

• Re-cap on agreed actions – Sub-task 2

– Sub-task 3

– Sub-task 4

– Sub-task 5

• Date / Location of Final Meeting

10

7