Talaat Mostafa Group Holding Companytalaatmoustafagroup.com/Portals/0/TMG Presentation.pdf ·...

39

Company Logo Talaat Mostafa Group Holding Company Group Presentation M h 2010 March 2010

Transcript of Talaat Mostafa Group Holding Companytalaatmoustafagroup.com/Portals/0/TMG Presentation.pdf ·...

CompanyLogo

Talaat Mostafa Group Holding Company

Group Presentation

M h 2010March 2010

Safe Harbour Statement

CompanyLogo

Certain information disclosed in this presentation consists of forward looking statements reflecting the current view of thecompany with respect to future events and are subject to certain risks uncertainties and assumptions Many factors couldcompany with respect to future events, and are subject to certain risks, uncertainties and assumptions. Many factors couldcause the actual results, performance or achievements of the company to be materially different from any future results,performance or achievements that may be expressed or implied by such forward looking statements, including worldwideaccount of trends, economic and political climate of Egypt, the Middle East, and changes in business strategy and variousother factors. Should one or more of these risks or uncertainties materialize or should underlying assumptions provei t t l lt t i ll f th d ib d i h f d l ki t t tincorrect, actual results may vary materially from those described in such forward looking statements.

2

Outline

G C P fil CompanyLogoTMG Corporate Profile

TMG at a Glance

Projects Development, Achievements and Growth ProspectsProjects Development, Achievements and Growth Prospects

Share Data

Board of Directors and Corporate Governance, Executive Team and Business Partners

Strategy and Business Model, Quality Control and Operating Systems

Market and Operational ReviewMacroeconomic Indicators Real Estate Drivers Tourism DriversMacroeconomic Indicators, Real Estate Drivers, Tourism Drivers

Financial and Operational Review, Hotels & Resorts Operational Review

Future GrowthReal Estate Development Plans And Projects Progress

Real Estate Future Growth

Hotels & Resorts Future Growth

Investment and Risk Considerations

G C P fil CompanyLogoTMG Corporate Profile

TMG at a Glance

Projects DevelopmentProjects Development

Achievements and Growth Prospects

Share Data

Board of Directors and Corporate Governance

Executive Team and Business Partners

Strategy and business modelStrategy and business model

Quality Control and Operating Systems

TMG

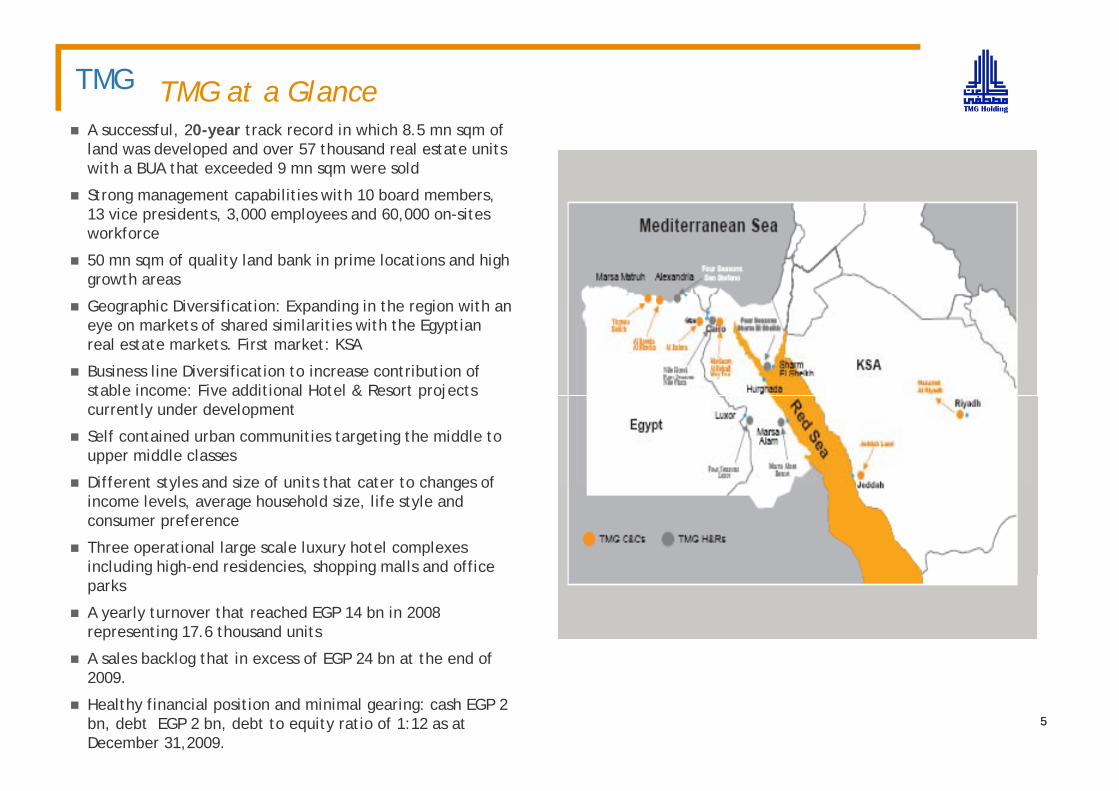

A f l 20 t k d i hi h 8 5 f

TMG at a GlanceCompany

LogoA successful, 20-year track record in which 8.5 mn sqm of land was developed and over 57 thousand real estate units with a BUA that exceeded 9 mn sqm were sold

Strong management capabilities with 10 board members, 13 vice presidents 3 000 employees and 60 000 on-sites 13 vice presidents, 3,000 employees and 60,000 on sites workforce

50 mn sqm of quality land bank in prime locations and high growth areas

Geographic Diversification: Expanding in the region with an Geographic Diversification: Expanding in the region with an eye on markets of shared similarities with the Egyptian real estate markets. First market: KSA

Business line Diversification to increase contribution of stable income: Five additional Hotel & Resort projects stable income: Five additional Hotel & Resort projects currently under development

Self contained urban communities targeting the middle to upper middle classes

Different styles and size of units that cater to changes of Different styles and size of units that cater to changes of income levels, average household size, life style and consumer preference

Three operational large scale luxury hotel complexes including high-end residencies, shopping malls and office g g pp gparks

A yearly turnover that reached EGP 14 bn in 2008 representing 17.6 thousand units

A sales backlog that in excess of EGP 24 bn at the end of

55

g2009.

Healthy financial position and minimal gearing: cash EGP 2 bn, debt EGP 2 bn, debt to equity ratio of 1:12 as at December 31,2009.

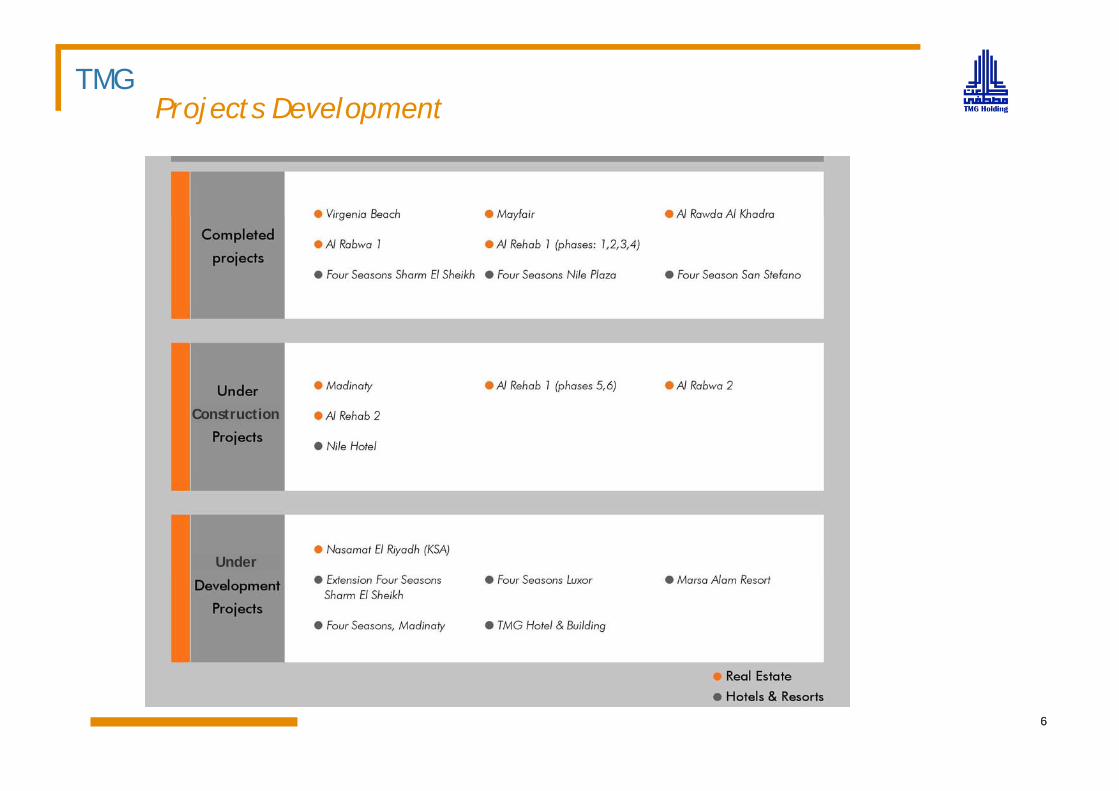

TMGProjects Development

CompanyLogo

Construction

Under

66

TMG

A hi t CompanyLogo

2.6% 0.2%1.1%0 8%

0.5%

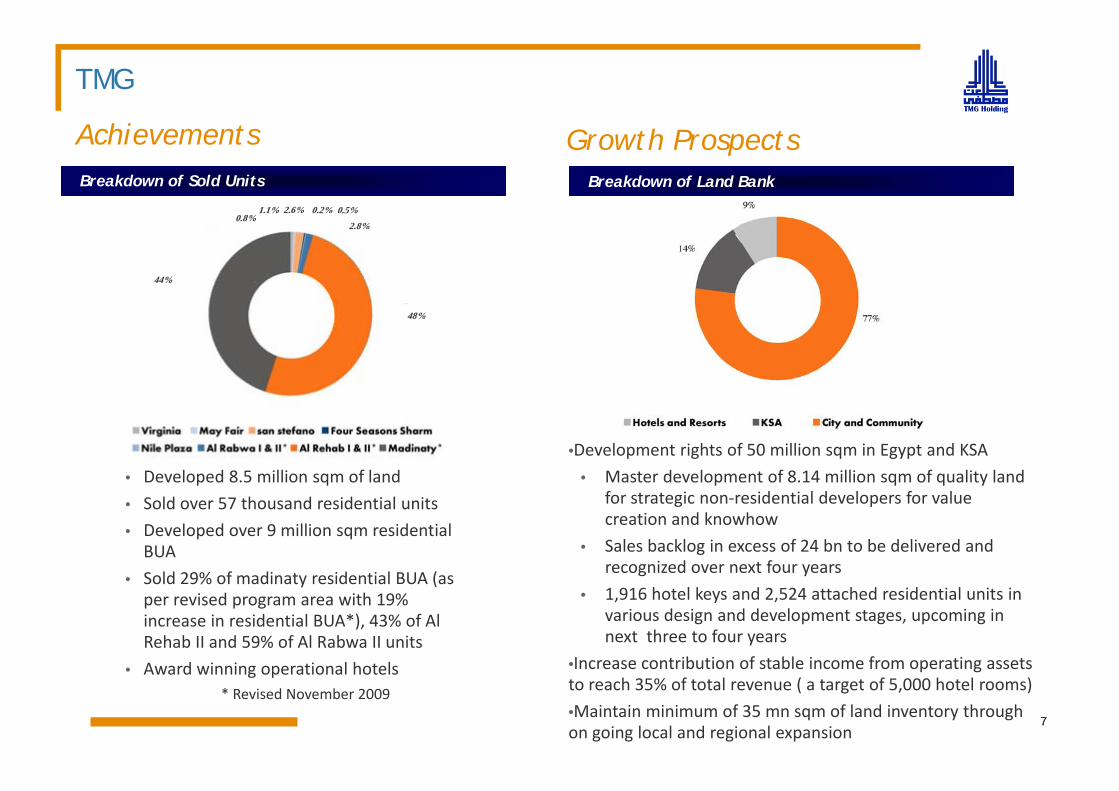

AchievementsBreakdown of Sold Units Breakdown of Land Bank

Growth Prospects

44%

2.8%0.8%

48%

• Developed 8.5 million sqm of land

•Development rights of 50 million sqm in Egypt and KSA

• Master development of 8.14 million sqm of quality land p q

• Sold over 57 thousand residential units

• Developed over 9 million sqm residential BUA

S ld 29% f di t id ti l BUA (

p q q yfor strategic non‐residential developers for value creation and knowhow

• Sales backlog in excess of 24 bn to be delivered and recognized over next four years

• Sold 29% of madinaty residential BUA (as per revised program area with 19% increase in residential BUA*), 43% of Al Rehab II and 59% of Al Rabwa II units

A d i i ti l h t l

g y

• 1,916 hotel keys and 2,524 attached residential units in various design and development stages, upcoming in next three to four years

•Increase contribution of stable income from operating assets

77

• Award winning operational hotels* Revised November 2009

•Increase contribution of stable income from operating assets to reach 35% of total revenue ( a target of 5,000 hotel rooms)

•Maintain minimum of 35 mn sqm of land inventory through on going local and regional expansion

TMGShare DataCompany

Logo

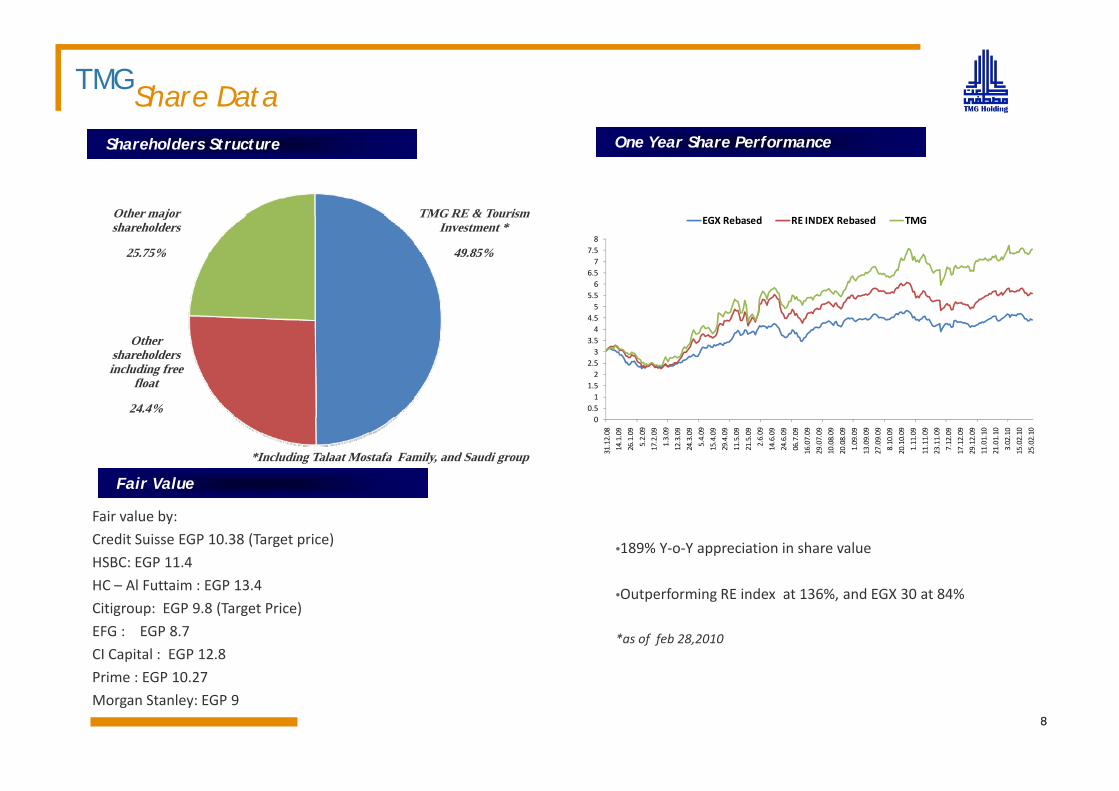

TMG RE & TourismOther major

Shareholders Structure One Year Share Performance

TMG RE & Tourism Investment *

49.85%

Other major shareholders

25.75%

55.56

6.57

7.58

EGX Rebased RE INDEX Rebased TMG

Other shareholders including free

float1

1.52

2.53

3.54

4.55

24.4%

*Including Talaat Mostafa Family, and Saudi group

Fair Value

00.51

31.12.08

14.1.09

26.1.09

5.2.09

17.2.09

1.3.09

12.3.09

24.3.09

5.4.09

15.4.09

29.4.09

11.5.09

21.5.09

2.6.09

14.6.09

24.6.09

06.7.09

16.07.09

29.07.09

10.08.09

20.08.09

1.09.09

13.09.09

27.09.09

8.10.09

20.10.09

1.11.09

11.11.09

23.11.09

7.12.09

17.12.09

29.12.09

11.01.10

21.01.10

3.02.10

15.02.10

25.02.10

•189% Y‐o‐Y appreciation in share value

Fair value by:

Credit Suisse EGP 10.38 (Target price)

HSBC: EGP 11.4

Fair Value

•Outperforming RE index at 136%, and EGX 30 at 84%

*as of feb 28,2010

HC – Al Futtaim : EGP 13.4

Citigroup: EGP 9.8 (Target Price)

EFG : EGP 8.7

CI Capital : EGP 12.8

88

Prime : EGP 10.27

Morgan Stanley: EGP 9

Board of Directors and Corporate GovernanceTMG

CompanyLogo

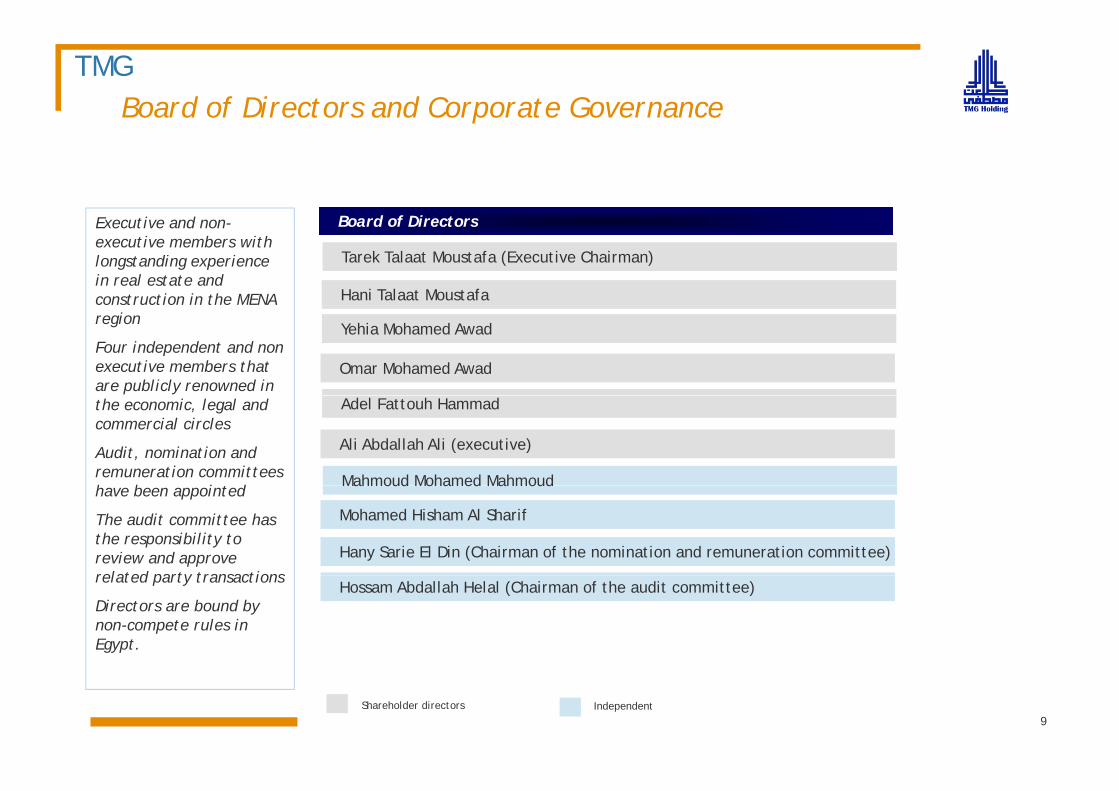

B d f Di t Executive and non-executive members with longstanding experience in real estate and construction in the MENA

Board of Directors

Hani Talaat Moustafa

Tarek Talaat Moustafa (Executive Chairman)

region

Four independent and non executive members that are publicly renowned in

Yehia Mohamed Awad

Omar Mohamed Awad

the economic, legal and commercial circles

Audit, nomination and remuneration committees h b i d

Mahmoud Mohamed Mahmoud

Adel Fattouh Hammad

Ali Abdallah Ali (executive)

have been appointed

The audit committee has the responsibility to review and approve related party transactions

Mahmoud Mohamed Mahmoud

Mohamed Hisham Al Sharif

Hany Sarie El Din (Chairman of the nomination and remuneration committee)

related party transactions

Directors are bound by non-compete rules in Egypt.

Hossam Abdallah Helal (Chairman of the audit committee)

Shareholder directors Independent9

Executive Management

TMG

CompanyLogo

Executive Management

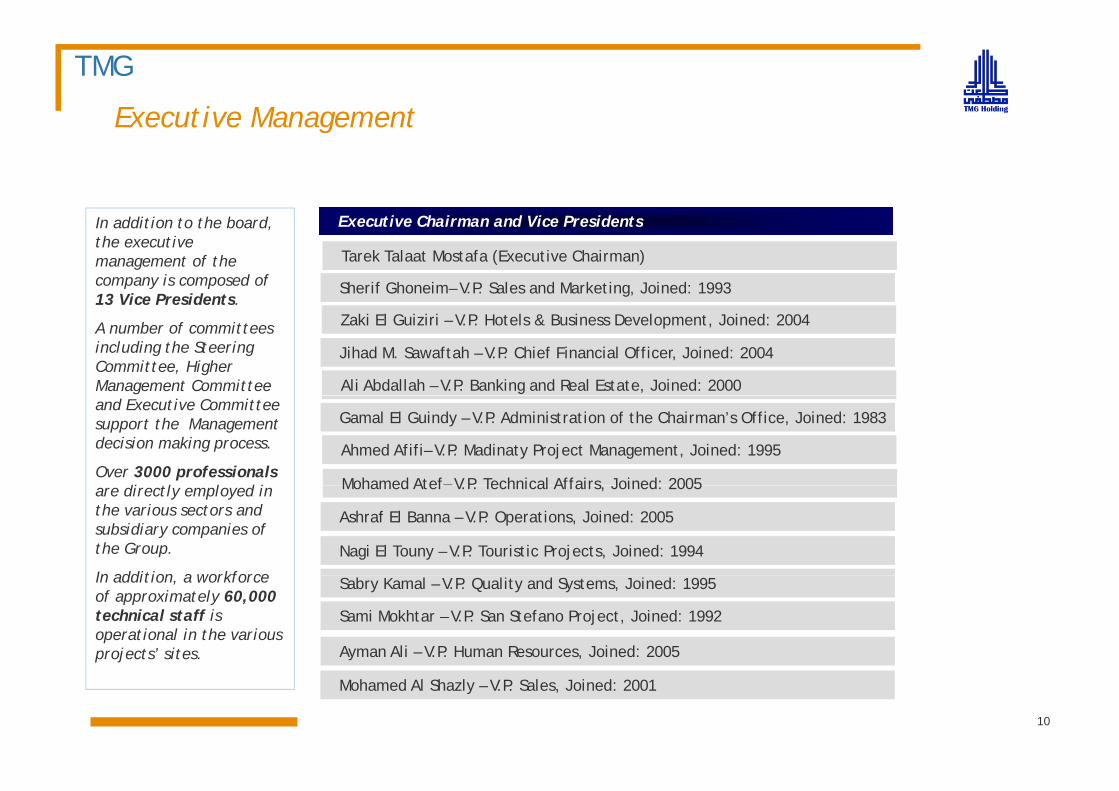

E ti Ch i d Vi P id t In addition to the board, the executive management of the company is composed of 13 Vice Presidents.

Executive Chairman and Vice Presidents

Sherif Ghoneim– V.P. Sales and Marketing, Joined: 1993

Tarek Talaat Mostafa (Executive Chairman)

A number of committees including the Steering Committee, Higher Management Committee

Zaki El Guiziri – V.P. Hotels & Business Development, Joined: 2004

Ali Abdallah – V.P. Banking and Real Estate, Joined: 2000

Jihad M. Sawaftah – V.P. Chief Financial Officer, Joined: 2004

and Executive Committee support the Management decision making process.

Over 3000 professionals di l l d i Mohamed Atef– V P Technical Affairs Joined: 2005

Ahmed Afifi– V.P. Madinaty Project Management, Joined: 1995

Gamal El Guindy – V.P. Administration of the Chairman’s Office, Joined: 1983

are directly employed in the various sectors and subsidiary companies of the Group.

In addition a workforce

Mohamed Atef V.P. Technical Affairs, Joined: 2005

Ashraf El Banna – V.P. Operations, Joined: 2005

Nagi El Touny – V.P. Touristic Projects, Joined: 1994

In addition, a workforce of approximately 60,000 technical staff is operational in the various projects’ sites.

Sami Mokhtar – V.P. San Stefano Project, Joined: 1992

Sabry Kamal – V.P. Quality and Systems, Joined: 1995

Ayman Ali – V.P. Human Resources, Joined: 2005

Mohamed Al Shazly – V.P. Sales, Joined: 2001

10

Business Partners

TMG

CompanyLogo

Th F S d K i ki i t ti ll t bl g t h i f h t l

Business Partners

The Four Seasons and Kempinski :internationally reputable management chains of our hotels

A Joint Venture with Hill International for projects management

A joint venture with Al Mehedeb, Al Fawzan and Al Kahtani through Al Oula for Real Estate S.A.E, Local Saudi Partners for Saudi Developments

Top class worldwide contractors, master planners, designers of projects components and execution:

Main contractor for our projects as Joannou and paraskavides, Hundai, Murray and Roberts and Binladen

The master planning of madinaty was made by a group of consulting firms from the United States: Sasaki, SWA and HHCP and their Egyptian counterparts Cairo Group for planning and architecture

Architects as HKS, USA for sharm extension design WZMH, Canada for luxor design, Studio sergi, Italy for marsa alam design

MEP companies as MMM Canada for sharm extension

I t i d i i GA UK f LInterior design companies as GA, UK for Luxor

Signature golf courses designers as Robert Trent Jones II and HHCP Design International

1111

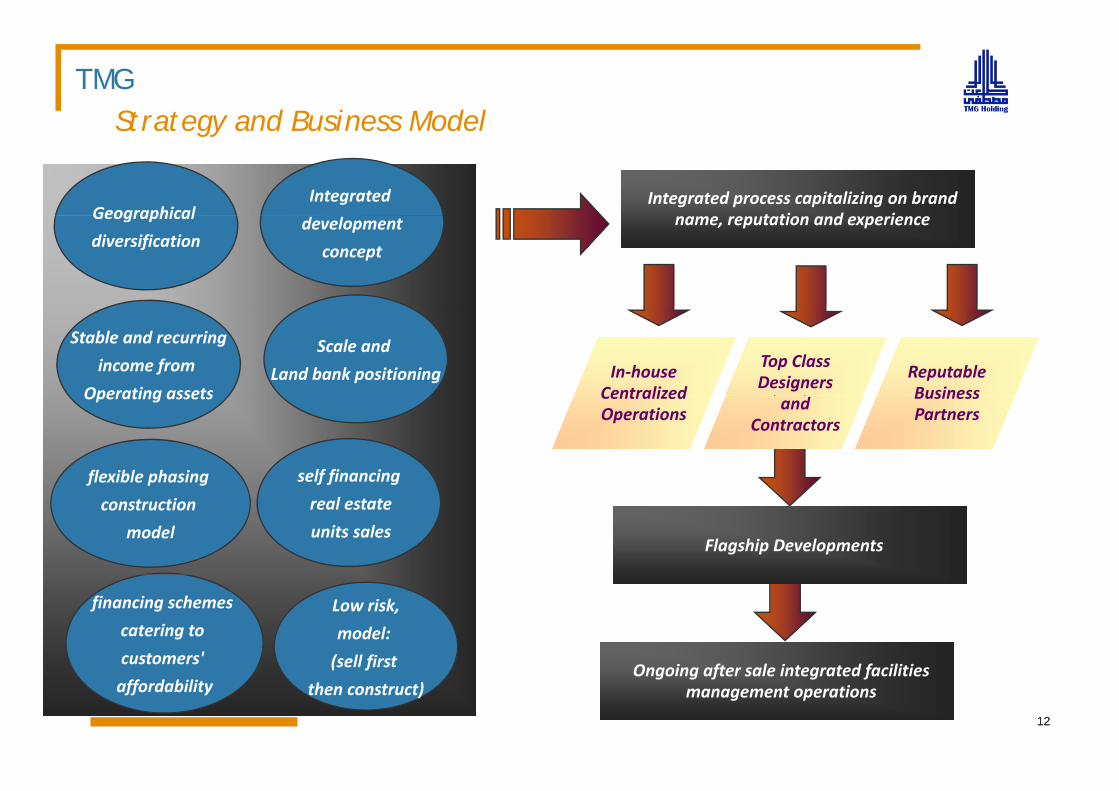

TMGStrategy and Business Model Company

LogoStrategy and Business Model

Integrated Integrated process capitalizing on brand t ti d i

Integrated process capitalizing on brand t ti d iGeographical development

concept

name, reputation and experiencename, reputation and experienceGeographical

diversification

In‐houseCentralized

Stable and recurring

income from

Operating assets

Top Class Designers Reputable

Business

Scale and

Land bank positioning

flexible phasing

Centralized Operations

self financing

Operating assets and Contractors

Business Partners

f p g

construction

model

real estate

units salesFlagship DevelopmentsFlagship Developments

financing schemes

catering to

customers'

Low risk,

model:

(sell first O i f l i d f ili iO i f l i d f ili i

1212

affordability(sell first

then construct)Ongoing after sale integrated facilities

management operationsOngoing after sale integrated facilities

management operations

TMG

Quality Control and Advanced Operating Systems CompanyLogo

Quality Control and Advanced Operating Systems

• 2007: Application of the SAP Enterprise Resources Planning System (ERP) on all functions of the Group • 2007: Application of the SAP Enterprise Resources Planning System (ERP) on all functions of the Group Subsidiaries. The result is a smooth process integration between sales, accounting and treasury, with facilitated financial and managerial reporting, streamlined accounting bookkeeping and consolidation, improved administration of internal controls, corporate governance and transparency, and an optimized cash management processcash management process.

• Feb 2008: qualified for the ISO 9001:2000 certification requirements for a quality management system and maintained the certificate upon renewal in 2009 where an organization:maintained the certificate upon renewal in 2009 where an organization:

1. needs to demonstrate its ability to consistently provide product that meets customer and applicable regulatory requirements, and

2 aims to enhance customer satisfaction through the effective application of the system including 2. aims to enhance customer satisfaction through the effective application of the system, including processes for continual improvement of the system and the assurance of conformity to customer and applicable regulatory requirements.

13

k d O i l R i CompanyLogoMarket and Operational Review

Macroeconomic Indicators

Real Estate Market Drivers Real Estate Market Drivers

Tourism Market Drivers

Financial Review

Consolidated Operational Review

Hotels & Resorts Operational Review

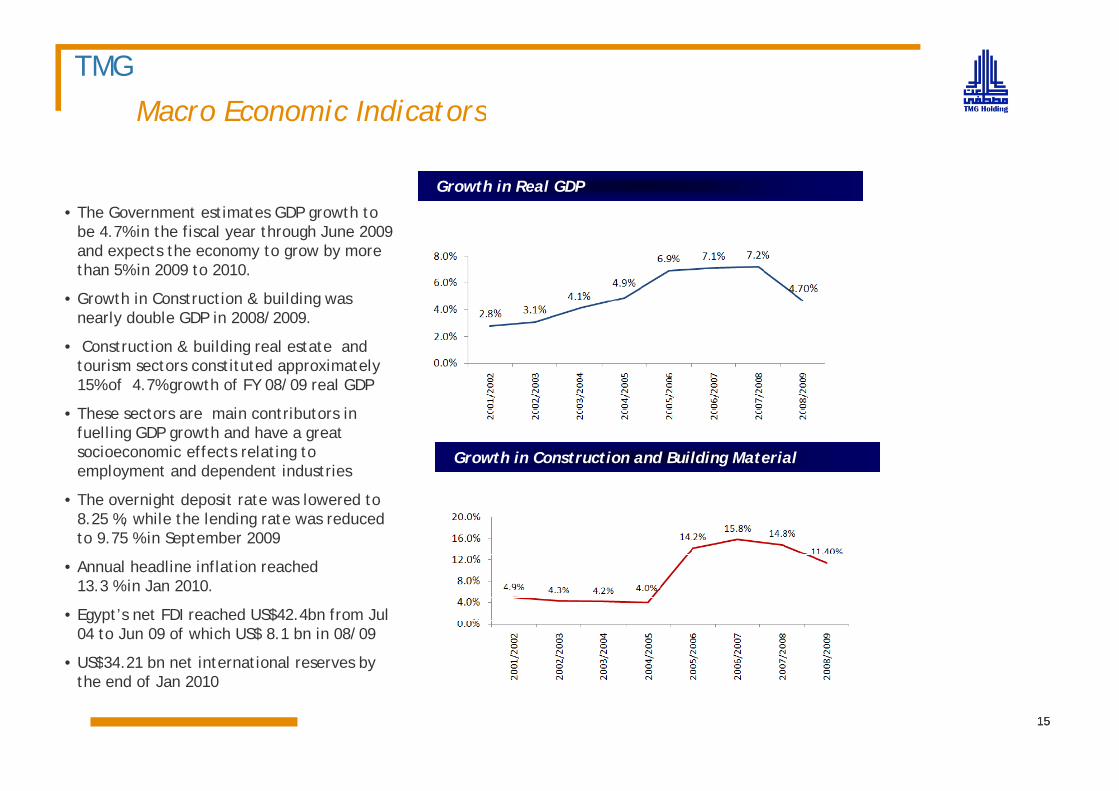

Macro Economic Indicators

TMG

CompanyLogo

Growth in Real GDP

• The Government estimates GDP growth to The Government estimates GDP growth to be 4.7% in the fiscal year through June 2009 and expects the economy to grow by more than 5% in 2009 to 2010.

• Growth in Construction & building was gnearly double GDP in 2008/2009.

• Construction & building real estate and tourism sectors constituted approximately 15% of 4.7% growth of FY 08/09 real GDP

Growth in Construction and Building Material

• These sectors are main contributors in fuelling GDP growth and have a great socioeconomic effects relating to employment and dependent industries

• The overnight deposit rate was lowered to 8.25 %, while the lending rate was reduced to 9.75 % in September 2009

• Annual headline inflation reached 13.3 % in Jan 2010.

• Egypt’s net FDI reached US$42.4bn from Jul 04 to Jun 09 of which US$ 8.1 bn in 08/09

• US$34 21 bn net international reserves by

1515

US$34.21 bn net international reserves by the end of Jan 2010

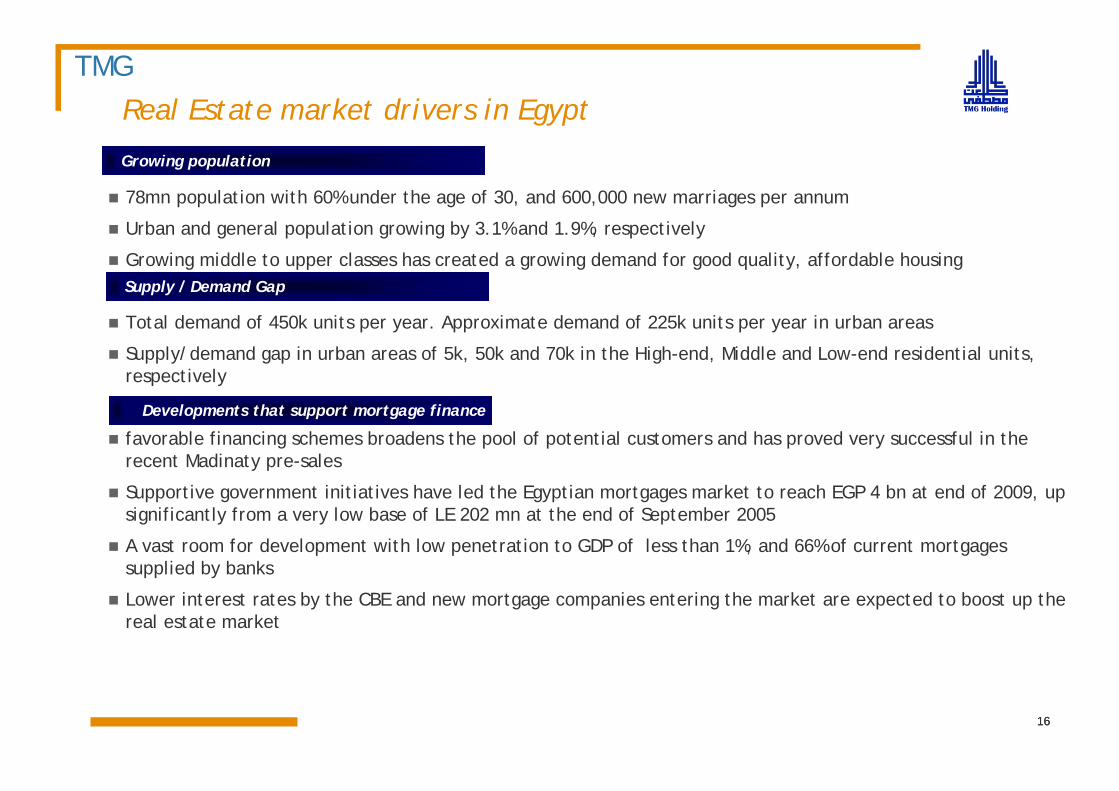

Real Estate market drivers in EgyptTMG

CompanyLogo

78mn population with 60% under the age of 30, and 600,000 new marriages per annum

Growing population

Urban and general population growing by 3.1% and 1.9%, respectively

Growing middle to upper classes has created a growing demand for good quality, affordable housingSupply / Demand Gap

Total demand of 450k units per year. Approximate demand of 225k units per year in urban areas

Supply/demand gap in urban areas of 5k, 50k and 70k in the High-end, Middle and Low-end residential units, respectively

favorable financing schemes broadens the pool of potential customers and has proved very successful in the recent Madinaty pre-sales

S i i i i i h l d h E i k h EGP 4 b d f 2009

Developments that support mortgage finance

Supportive government initiatives have led the Egyptian mortgages market to reach EGP 4 bn at end of 2009, up significantly from a very low base of LE 202 mn at the end of September 2005

A vast room for development with low penetration to GDP of less than 1%, and 66% of current mortgages supplied by bankspp y

Lower interest rates by the CBE and new mortgage companies entering the market are expected to boost up the real estate market

1616

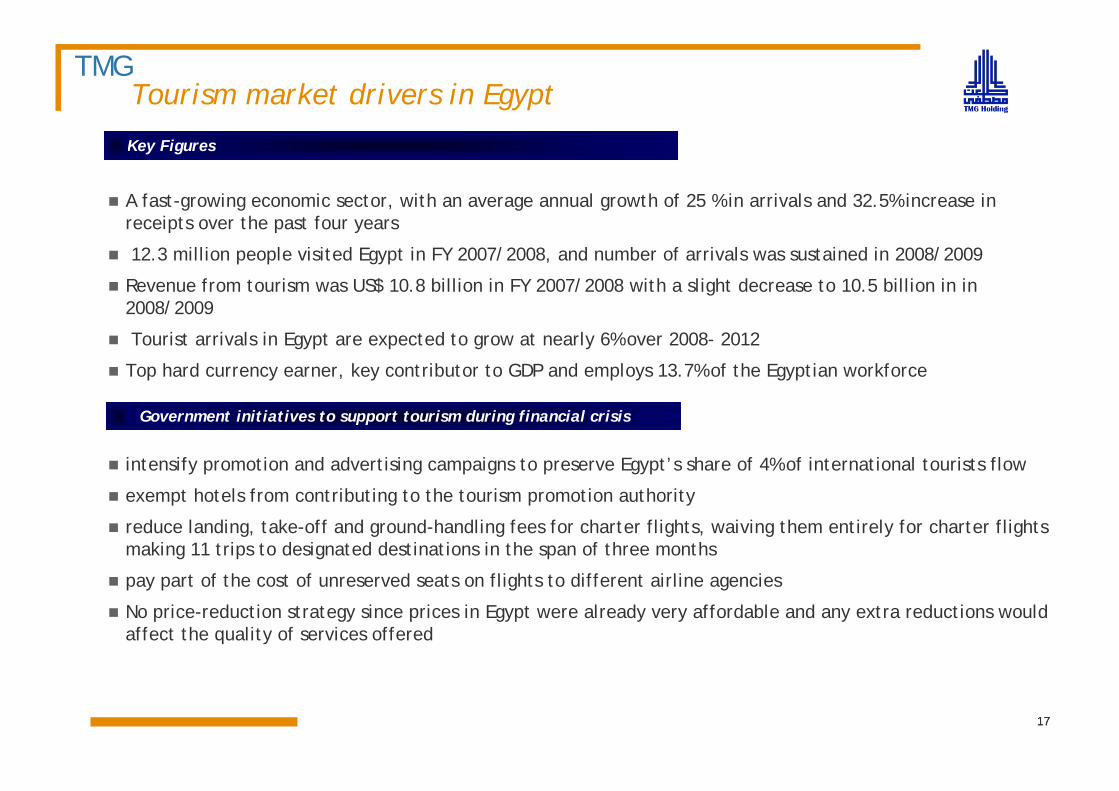

Tourism market drivers in EgyptTMG

CompanyLogo

A fast-growing economic sector, with an average annual growth of 25 % in arrivals and 32.5% increase in i h f

•Key Figures

receipts over the past four years

12.3 million people visited Egypt in FY 2007/2008, and number of arrivals was sustained in 2008/2009

Revenue from tourism was US$ 10.8 billion in FY 2007/2008 with a slight decrease to 10.5 billion in in 2008/20092008/2009

Tourist arrivals in Egypt are expected to grow at nearly 6% over 2008- 2012

Top hard currency earner, key contributor to GDP and employs 13.7% of the Egyptian workforce

intensify promotion and advertising campaigns to preserve Egypt’s share of 4% of international tourists flow

Government initiatives to support tourism during financial crisis

exempt hotels from contributing to the tourism promotion authority

reduce landing, take-off and ground-handling fees for charter flights, waiving them entirely for charter flights making 11 trips to designated destinations in the span of three months

t f th t f d t fli ht t diff t i li ipay part of the cost of unreserved seats on flights to different airline agencies

No price-reduction strategy since prices in Egypt were already very affordable and any extra reductions would affect the quality of services offered

1717

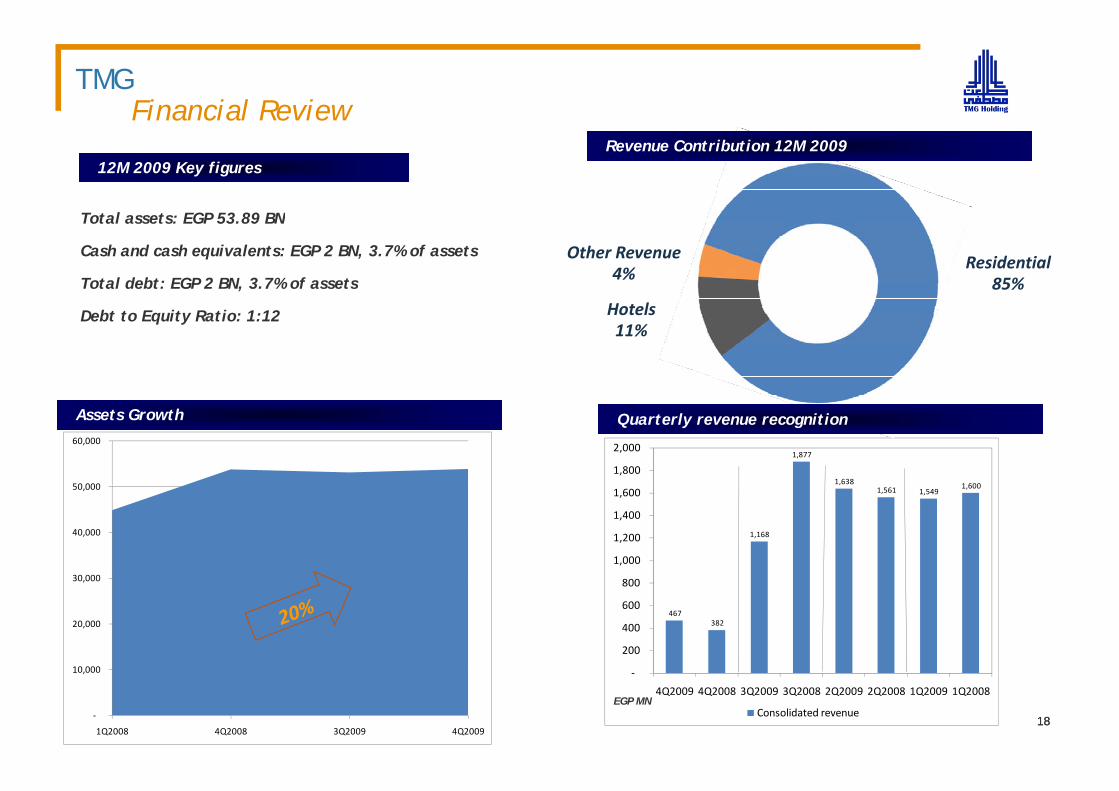

TMGFinancial Review

CompanyLogoRevenue Contribution 12M 2009

Total assets: EGP 53 89 BN

12M 2009 Key figures

H t l

Residential85%

Other Revenue4%

Total assets: EGP 53.89 BN

Cash and cash equivalents: EGP 2 BN, 3.7% of assets

Total debt: EGP 2 BN, 3.7% of assets

Hotels11%

Debt to Equity Ratio: 1:12

1,877

1,638 1 600

1,800

2,000

50 000

60,000

Quarterly revenue recognitionAssets Growth

1,168

1,561 1,549 1,600

1,000

1,200

1,400

1,600

30 000

40,000

50,000

467 382

200

400

600

800

20,000

30,000

‐

4Q2009 4Q2008 3Q2009 3Q2008 2Q2009 2Q2008 1Q2009 1Q2008

Consolidated revenue‐

10,000

1Q2008 4Q2008 3Q2009 4Q20091818

EGP MN

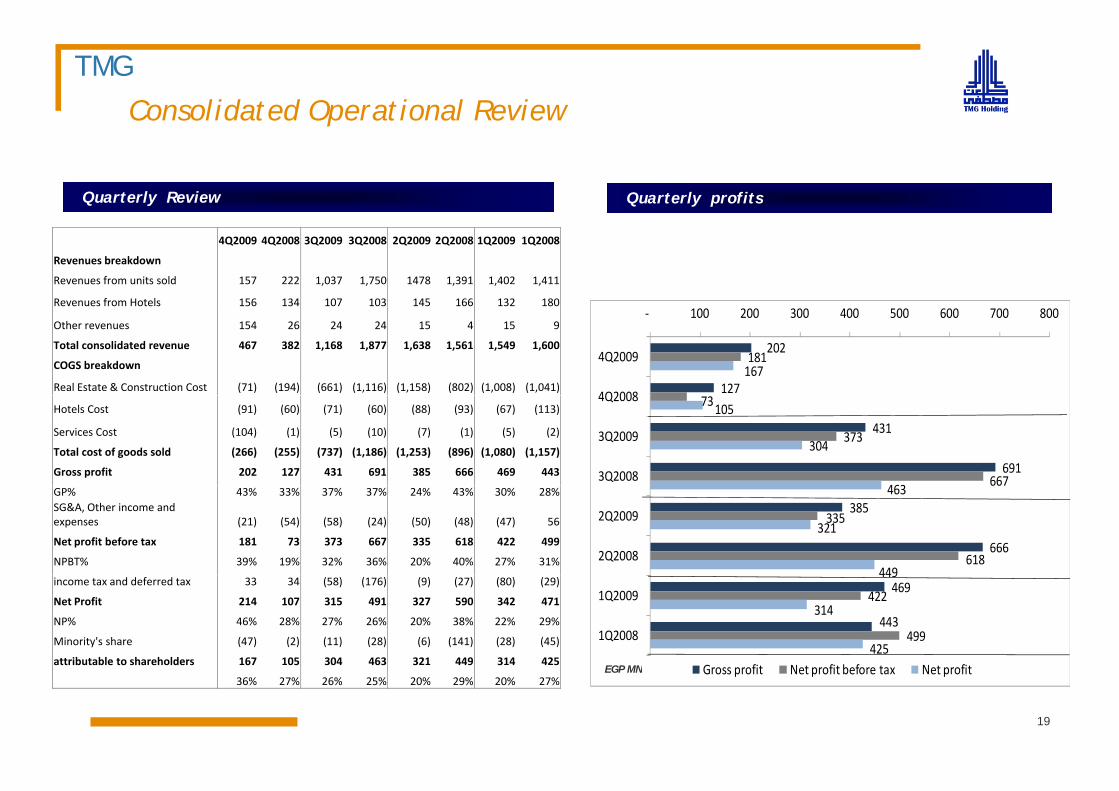

TMG

Consolidated Operational ReviewCompany

Logo

p

Quarterly profitsQuarterly Review

4Q2009 4Q2008 3Q2009 3Q2008 2Q2009 2Q2008 1Q2009 1Q2008

Revenues breakdown

Revenues from units sold 157 222 1,037 1,750 1478 1,391 1,402 1,411

Revenues from Hotels 156 134 107 103 145 166 132 180

202

127

181 167

‐ 100 200 300 400 500 600 700 800

4Q2009

4Q2008

Revenues from Hotels 156 134 107 103 145 166 132 180

Other revenues 154 26 24 24 15 4 15 9

Total consolidated revenue 467 382 1,168 1,877 1,638 1,561 1,549 1,600

COGS breakdown

Real Estate & Construction Cost (71) (194) (661) (1,116) (1,158) (802) (1,008) (1,041)

431

691

73

373

667

105

304

463

4Q2008

3Q2009

3Q2008

Hotels Cost (91) (60) (71) (60) (88) (93) (67) (113)

Services Cost (104) (1) (5) (10) (7) (1) (5) (2)

Total cost of goods sold (266) (255) (737) (1,186) (1,253) (896) (1,080) (1,157)

Gross profit 202 127 431 691 385 666 469 443

385

666

667

335

618

463

321

449

2Q2009

2Q2008

GP% 43% 33% 37% 37% 24% 43% 30% 28%SG&A, Other income and expenses (21) (54) (58) (24) (50) (48) (47) 56

Net profit before tax 181 73 373 667 335 618 422 499

NPBT% 39% 19% 32% 36% 20% 40% 27% 31%

469

443

422

499

449

314

425

1Q2009

1Q2008

G fi N fi b f N fi

income tax and deferred tax 33 34 (58) (176) (9) (27) (80) (29)

Net Profit 214 107 315 491 327 590 342 471

NP% 46% 28% 27% 26% 20% 38% 22% 29%

Minority's share (47) (2) (11) (28) (6) (141) (28) (45)

attributable to shareholders 167 105 304 463 321 449 314 425Gross profit Net profit before tax Net profit

19

EGP MNattributable to shareholders 167 105 304 463 321 449 314 425

36% 27% 26% 25% 20% 29% 20% 27%

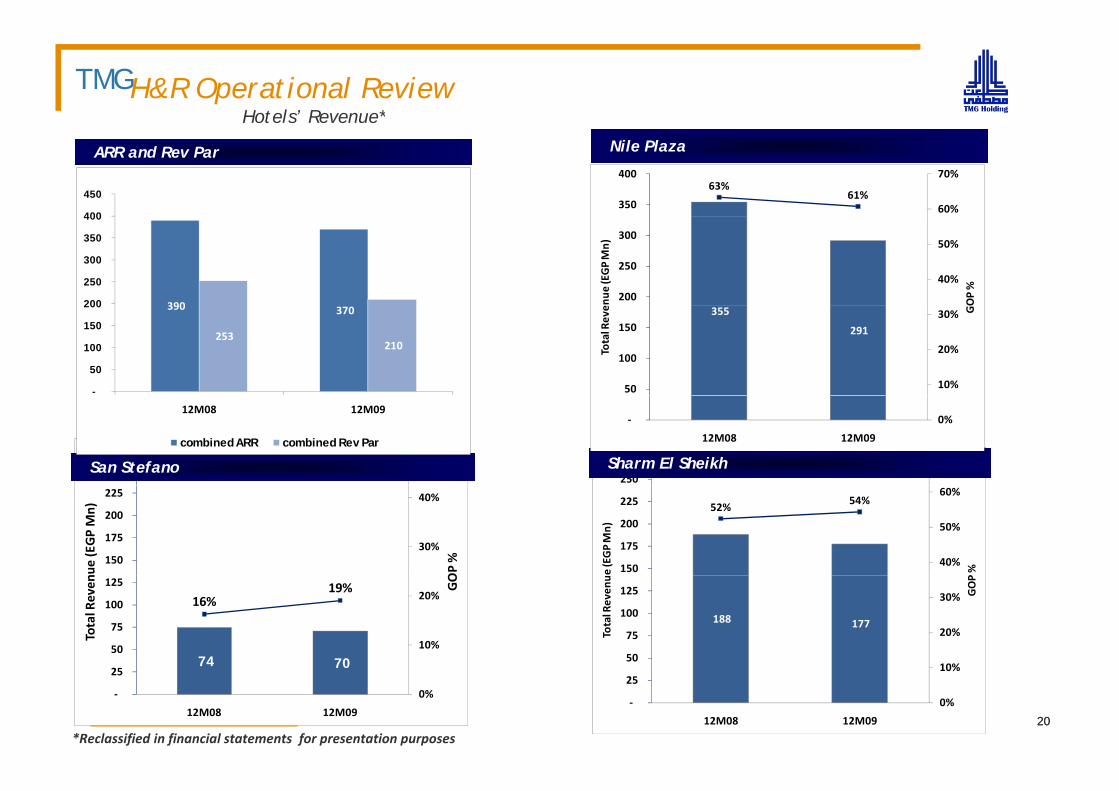

TMGH&R Operational ReviewHotels’ Revenue*

CompanyLogoNile PlazaARR and Rev Par

400

450 63%

61%60%

70%

350

400

390200

250

300

350

400

40%

50%

200

250

300

OP %

enue

(EGP Mn)

390 370

253 210

-

50

100

150

200 355

291

10%

20%

30%

50

100

150

G

Total Reve

70%

250

275 50%

250

275 Sharm El SheikhSan Stefano

12M08 12M09

combined ARR combined Rev Par

0%‐

12M08 12M09

52%54%

40%

50%

60%

150

175

200

225

P %e (EGP Mn)

30%

40%

150

175

200

225

OP %

nue (EGP Mn)

188 177

10%

20%

30%

50

75

100

125 GOP

Total Reven

u

74 70

16%19%

10%

20%

50

75

100

125 GO

Total Reven

0%

10%

‐

25

12M08 12M09

74 70

0%‐

25

12M08 12M092020

*Reclassified in financial statements for presentation purposes

G h CompanyLogoFuture Growth

Real Estate Development Plans

Real Estate Projects ProgressReal Estate Projects Progress

Real Estate Future Growth

Hotels and Resorts Future Growth

TMG

CompanyLogoFuture Growth

R l E t t D l t Hotels and ResortsReal Estate Development

• Capitalizing on landbank in existing projects

Hotels and Resorts

•The target is to build a stock of 5,000 hotel • Master Development and sale of prime land plots; value created through project development and units delivery over 10 ten year period

The target is to build a stock of 5,000 hotel rooms with a minimum IRR of 18%, and increase the contribution of stable income to 35% of total revenue

•Development of hotel projects in the pipeline, y p• Looking for worthwhile opportunities to expand landbank in Egypt

• Expanding in the region with an eye on markets of shared similarities with the

early launch of real estate sales to co-finance development and enhance returns

•Continue to grow through purchase of minorities when the opportunity arise

markets of shared similarities with the Egyptian real estate markets

• The target is to have a minimum landbank of 35 million sqm at any point of time

•Looking for further local opportunities that enjoy prime location and have a market gap to increase weight of stable income from hotels operations.

22

TMG

Real Estate Development PlanCompany

Logo

p2010 Real Estate Market conditions:

• Egypt is one of the least affected economies at a GDP growth of 4 7% (estimated to reach 5% in 2010) and• Egypt is one of the least affected economies at a GDP growth of 4.7% (estimated to reach 5% in 2010) and construction growth of 11.4%

• Solid financial sector; No actual problem in the Egyptian real estate market• A state of pent up demand, buyers are adopting a temporary wait and see approach that will eventually end• A state of stagflation resulting from over money supply may follow in 2010

TMG at start of 2010:Sales backlog that exceeds EGP 24 bn• Sales backlog that exceeds EGP 24 bn

• Delivery dates of large scale developments starting April 2010

TMG’s plan for 2010:p• Introduce products that have the right mix of size and space utilization • Offer affordable financing scheme to attract new buyers• Delivery of sold units in Madinaty and Rehab Extension with required services making the cities alive and

d f h id iready for the residents move in• Opening of Nile Kempinski Hotel in Cairo

23

TMG

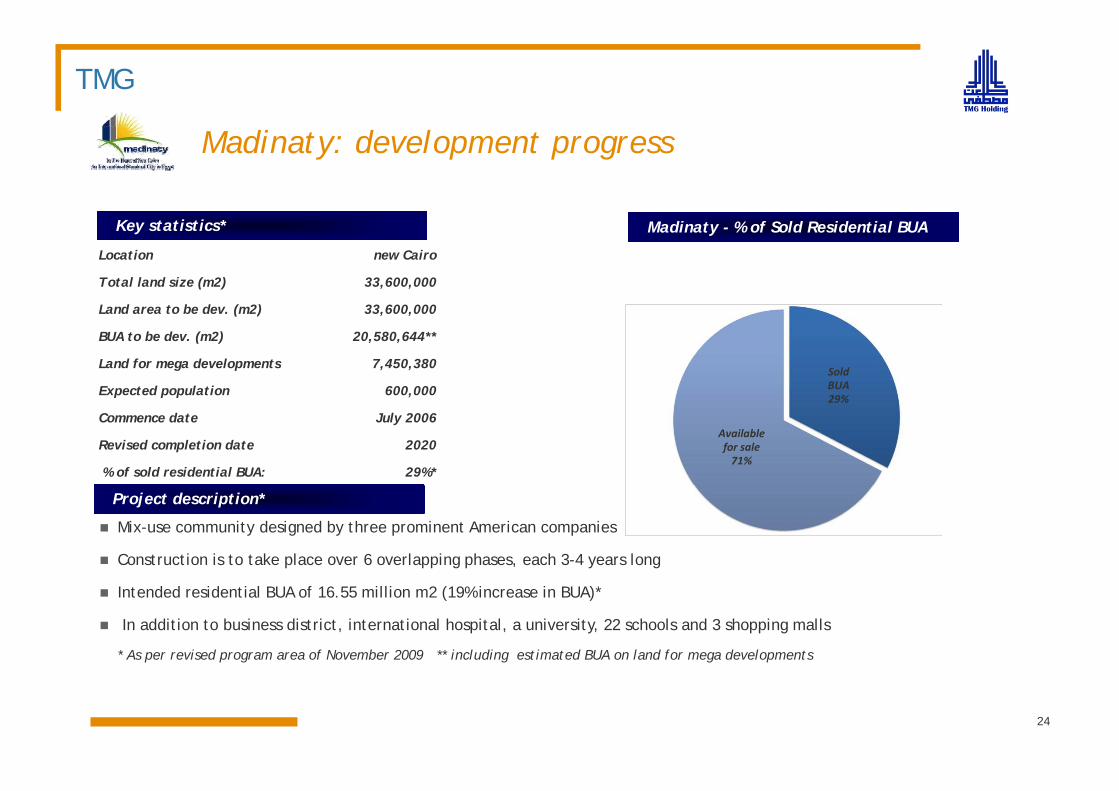

CompanyLogoMadinaty: development progress

Location new Cairo

Total land size (m2) 33,600,000

L d t b d ( 2) 33 600 000

Key statistics* Madinaty - % of Sold Residential BUA

Land area to be dev. (m2) 33,600,000

BUA to be dev. (m2) 20,580,644**

Land for mega developments 7,450,380

Expected population 600,000Sold BUA 29%

p p p ,

Commence date July 2006

Revised completion date 2020

% of sold residential BUA: 29%*

Available for sale71%

29%

Project description*

Mix-use community designed by three prominent American companies

Construction is to take place over 6 overlapping phases, each 3-4 years long

Intended residential BUA of 16.55 million m2 (19% increase in BUA)*

In addition to business district, international hospital, a university, 22 schools and 3 shopping malls

* As per revised program area of November 2009 ** including estimated BUA on land for mega developments

24

TMG

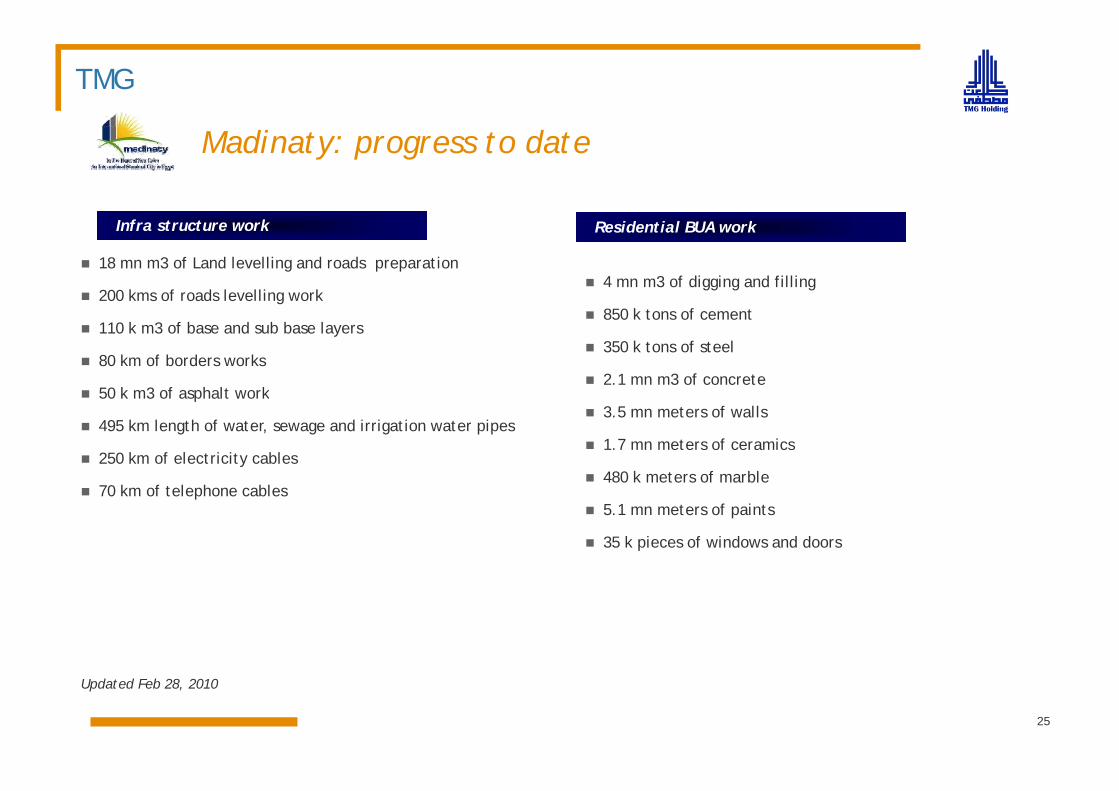

CompanyLogoMadinaty: progress to date

18 mn m3 of Land levelling and roads preparation

200 kms of roads levelling work

Infra structure work Residential BUA work

4 mn m3 of digging and filling

110 k m3 of base and sub base layers

80 km of borders works

50 k m3 of asphalt work

850 k tons of cement

350 k tons of steel

2.1 mn m3 of concrete50 k m3 of asphalt work

495 km length of water, sewage and irrigation water pipes

250 km of electricity cables

70 k f l h bl

3.5 mn meters of walls

1.7 mn meters of ceramics

480 k meters of marble70 km of telephone cables

5.1 mn meters of paints

35 k pieces of windows and doors

Updated Feb 28, 2010

25

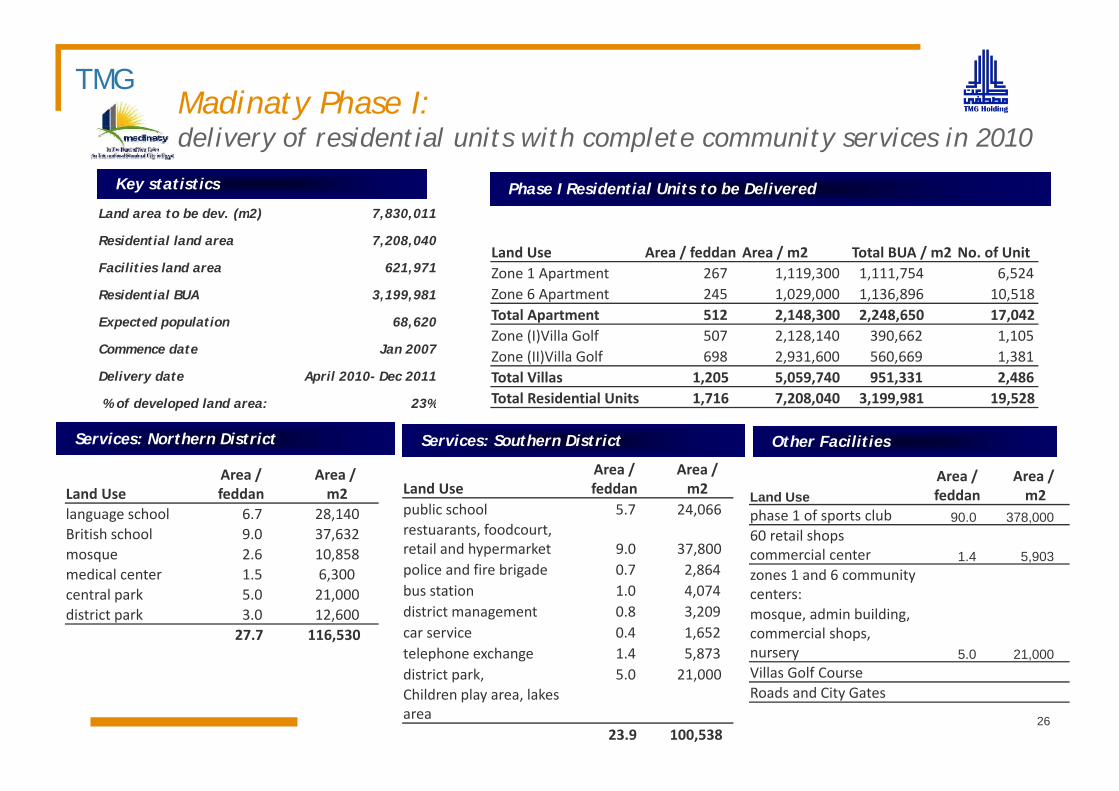

TMGMadinaty Phase I:

CompanyLogodelivery of residential units with complete community services in 2010

Phase I Residential Units to be DeliveredKey statistics

Land area to be dev. (m2) 7,830,011Land area to be dev. (m2) 7,830,011

Residential land area 7,208,040

Facilities land area 621,971

Residential BUA 3,199,981

Land Use Area / feddan Area / m2 Total BUA / m2 No. of UnitZone 1 Apartment 267 1,119,300 1,111,754 6,524 Zone 6 Apartment 245 1,029,000 1,136,896 10,518

Expected population 68,620

Commence date Jan 2007

Delivery date April 2010- Dec 2011

Total Apartment 512 2,148,300 2,248,650 17,042 Zone (I)Villa Golf 507 2,128,140 390,662 1,105 Zone (II)Villa Golf 698 2,931,600 560,669 1,381 Total Villas 1,205 5,059,740 951,331 2,486 Total Residential Units 1 716 7 208 040 3 199 981 19 528

Services: Northern District

% of developed land area: 23% Total Residential Units 1,716 7,208,040 3,199,981 19,528

Area / Area /

Services: Southern District

L d UArea / f dd

Area / 2

Area / Area /

Other Facilities

Land Use feddan m2language school 6.7 28,140 British school 9.0 37,632 mosque 2.6 10,858 medical center 1 5 6 300

Land Use feddan m2public school 5.7 24,066 restuarants, foodcourt, retail and hypermarket 9.0 37,800 police and fire brigade 0.7 2,864

Land Use feddan m2phase 1 of sports club 90.0 378,000 60 retail shops commercial center 1.4 5,903 zones 1 and 6 communitymedical center 1.5 6,300

central park 5.0 21,000 district park 3.0 12,600

27.7 116,530

p g ,bus station 1.0 4,074 district management 0.8 3,209 car service 0.4 1,652 telephone exchange 1.4 5,873

zones 1 and 6 community centers:mosque, admin building, commercial shops, nursery 5.0 21,000

26

district park, 5.0 21,000 Children play area, lakes area

23.9 100,538

Villas Golf CourseRoads and City Gates

TMG

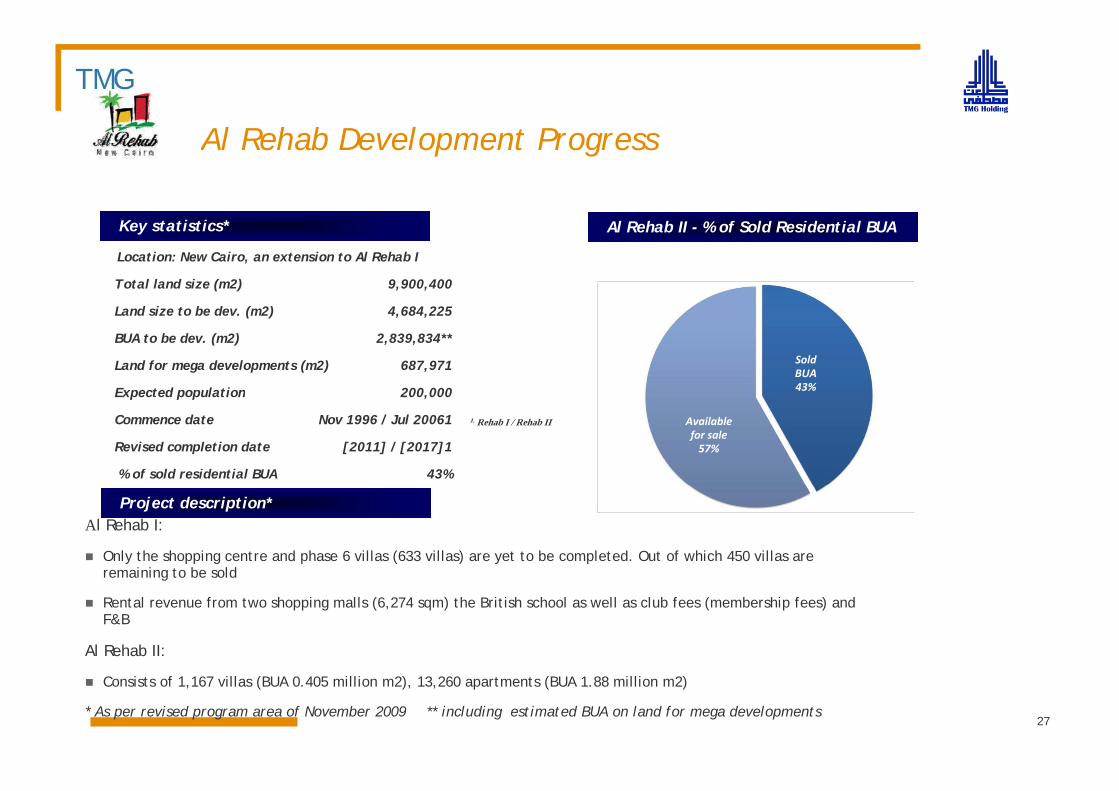

CompanyLogoAl Rehab Development Progress

Key statistics* Al Rehab II - % of Sold Residential BUA

Location: New Cairo, an extension to Al Rehab I

Total land size (m2) 9,900,400

d i b dLand size to be dev. (m2) 4,684,225

BUA to be dev. (m2) 2,839,834**

Land for mega developments (m2) 687,971

Expected population 200,000

Sold BUA 43%Expected population 200,000

Commence date Nov 1996 / Jul 20061

Revised completion date [2011] / [2017]1

% of sold residential BUA 43%

1. Rehab I / Rehab II Available for sale57%

Project description*Al Rehab I:

Only the shopping centre and phase 6 villas (633 villas) are yet to be completed. Out of which 450 villas are remaining to be soldremaining to be sold

Rental revenue from two shopping malls (6,274 sqm) the British school as well as club fees (membership fees) and F&B

Al Rehab II:

Consists of 1,167 villas (BUA 0.405 million m2), 13,260 apartments (BUA 1.88 million m2)

* As per revised program area of November 2009 ** including estimated BUA on land for mega developments27

TMG

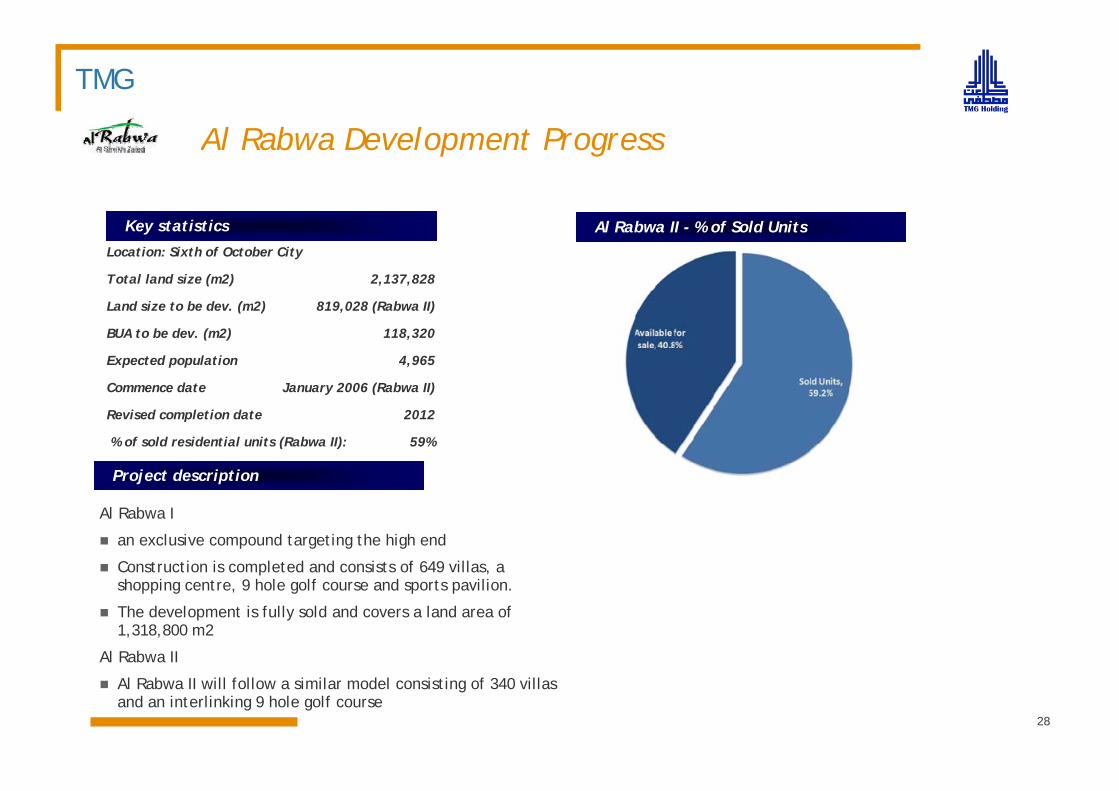

CompanyLogoAl Rabwa Development Progress

Key statistics Al Rabwa II - % of Sold UnitsLocation: Sixth of October City

Total land size (m2) 2,137,828

Land size to be dev (m2) 819 028 (Rabwa II)Land size to be dev. (m2) 819,028 (Rabwa II)

BUA to be dev. (m2) 118,320

Expected population 4,965

Commence date January 2006 (Rabwa II)

Project description

Revised completion date 2012

% of sold residential units (Rabwa II): 59%

Al Rabwa I

an exclusive compound targeting the high end

Construction is completed and consists of 649 villas, a pshopping centre, 9 hole golf course and sports pavilion.

The development is fully sold and covers a land area of 1,318,800 m2

Al Rabwa II

Al Rabwa II will follow a similar model consisting of 340 villas and an interlinking 9 hole golf course

28

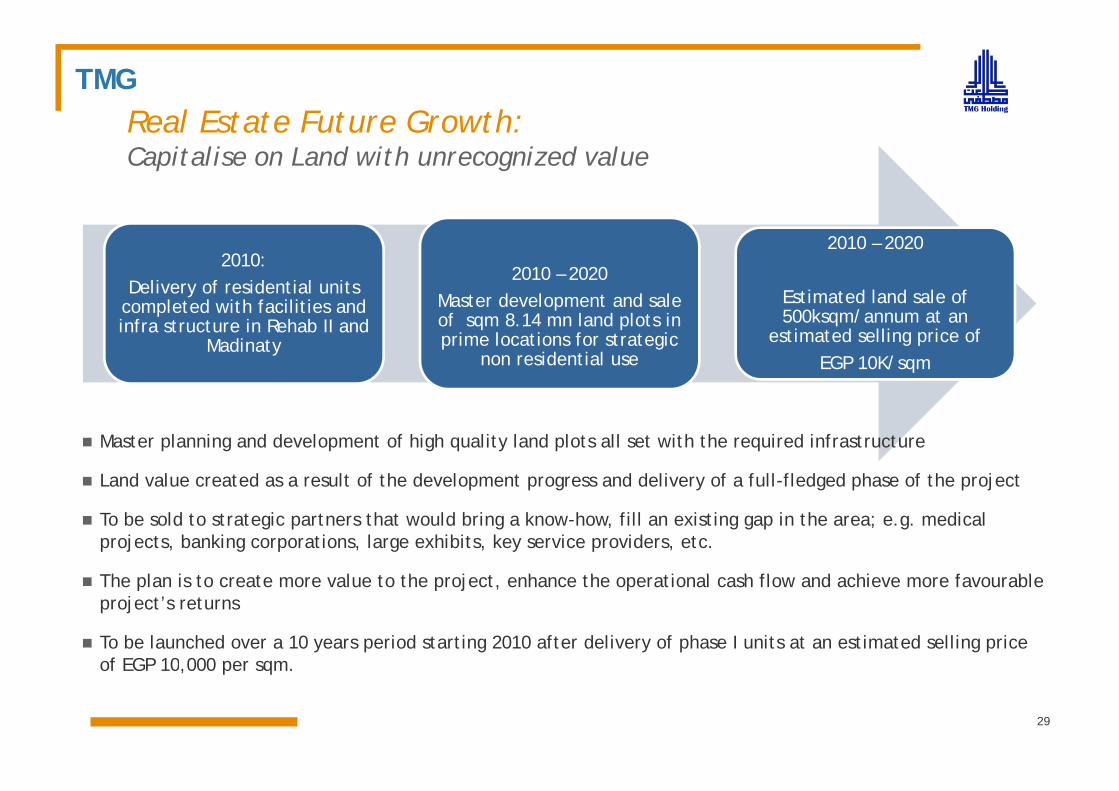

TMGReal Estate Future Growth: Company

LogoReal Estate Future Growth:Capitalise on Land with unrecognized value

2010: Delivery of residential units

completed with facilities and

2010 – 2020Master development and sale

2010 – 2020

Estimated land sale of completed with facilities and infra structure in Rehab II and

Madinaty

Master development and sale of sqm 8.14 mn land plots in prime locations for strategic

non residential use

500ksqm/annum at an estimated selling price of

EGP 10K/sqm

Master planning and development of high quality land plots all set with the required infrastructure

Land value created as a result of the development progress and delivery of a full-fledged phase of the projectLand value created as a result of the development progress and delivery of a full fledged phase of the project

To be sold to strategic partners that would bring a know-how, fill an existing gap in the area; e.g. medical projects, banking corporations, large exhibits, key service providers, etc.

Th l i t t l t th j t h th ti l h fl d hi f bl The plan is to create more value to the project, enhance the operational cash flow and achieve more favourable project’s returns

To be launched over a 10 years period starting 2010 after delivery of phase I units at an estimated selling price of EGP 10 000 per sqm

29

of EGP 10,000 per sqm.

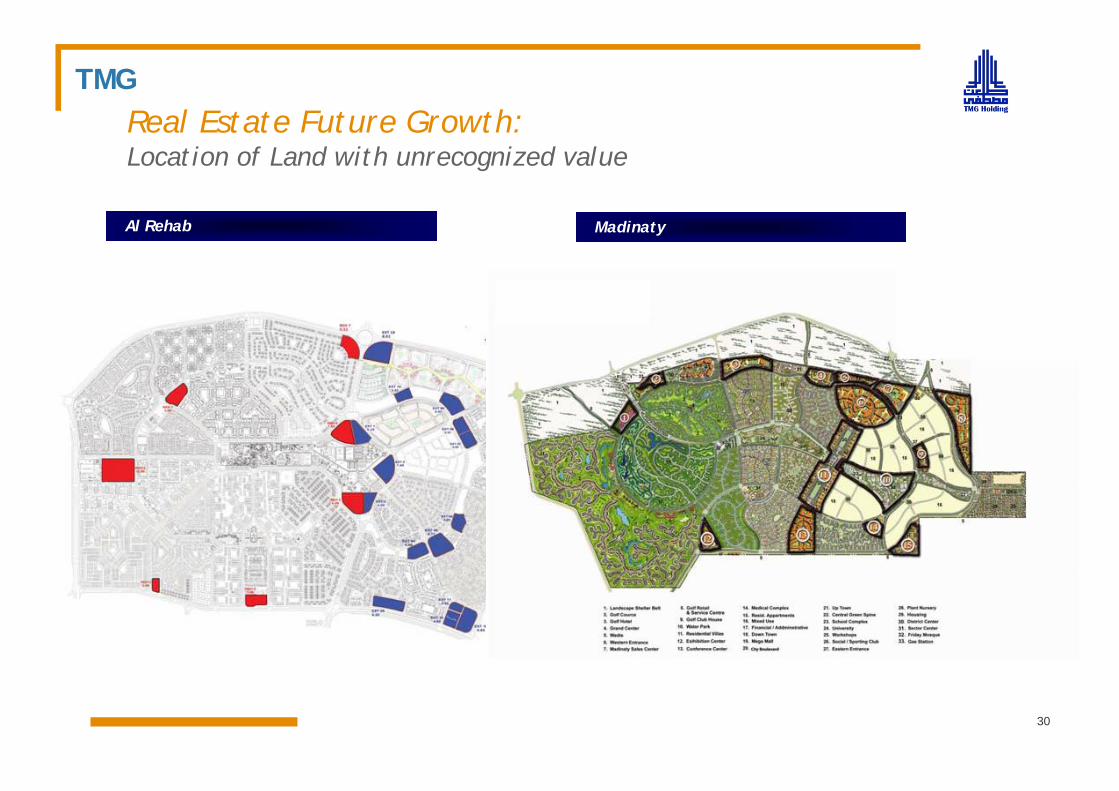

TMGReal Estate Future Growth: Company

LogoReal Estate Future Growth:Location of Land with unrecognized value

Al Rehab Madinaty

30

TMGReal Estate Future Growth:

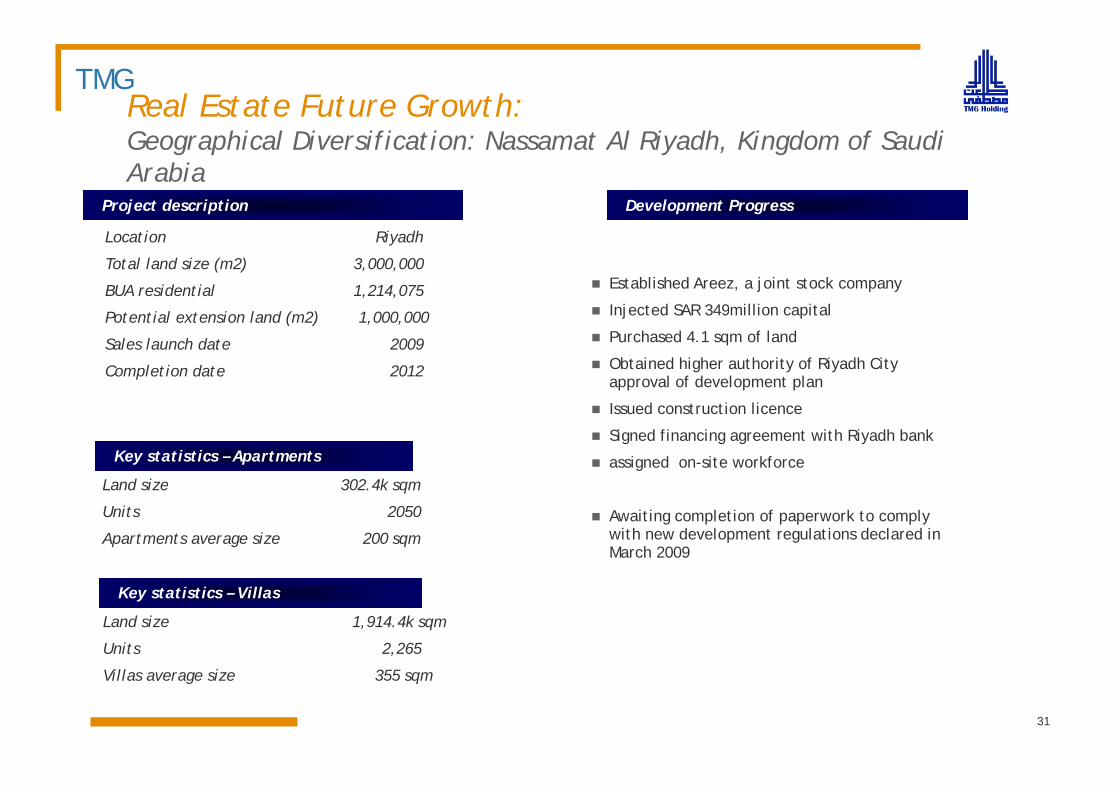

CompanyLogoGeographical Diversification: Nassamat Al Riyadh, Kingdom of Saudi

ArabiaProject description Development Progress

Location Riyadh

Total land size (m2) 3,000,000

BUA residential 1,214,075 Established Areez, a joint stock company

I j t d SAR 349 illi it lPotential extension land (m2) 1,000,000

Sales launch date 2009

Completion date 2012

Injected SAR 349million capital

Purchased 4.1 sqm of land

Obtained higher authority of Riyadh City approval of development plan

Key statistics – Apartments

Land size 302 4k sqm

Issued construction licence

Signed financing agreement with Riyadh bank

assigned on-site workforceLand size 302.4k sqm

Units 2050

Apartments average size 200 sqmAwaiting completion of paperwork to comply with new development regulations declared in March 2009

Key statistics – Villas

Land size 1,914.4k sqm

Units 2,265

Villas average size 355 sqm

31

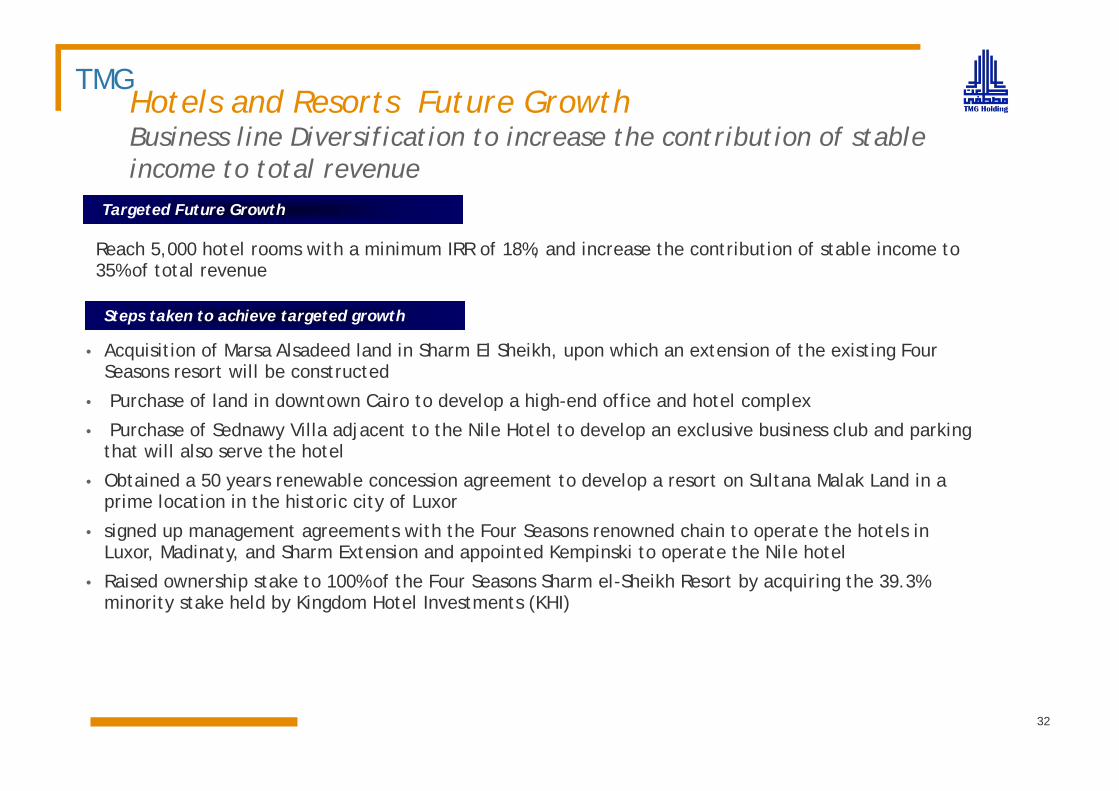

TMGHotels and Resorts Future Growth

l f h b f bl CompanyLogoBusiness line Diversification to increase the contribution of stable

income to total revenueTargeted Future Growthg

Reach 5,000 hotel rooms with a minimum IRR of 18%, and increase the contribution of stable income to 35% of total revenue

• Acquisition of Marsa Alsadeed land in Sharm El Sheikh, upon which an extension of the existing Four Seasons resort will be constructed

P h f l d i d t C i t d l hi h d ffi d h t l l

Steps taken to achieve targeted growth

• Purchase of land in downtown Cairo to develop a high-end office and hotel complex

• Purchase of Sednawy Villa adjacent to the Nile Hotel to develop an exclusive business club and parking that will also serve the hotel

• Obtained a 50 years renewable concession agreement to develop a resort on Sultana Malak Land in a Obtained a 50 years renewable concession agreement to develop a resort on Sultana Malak Land in a prime location in the historic city of Luxor

• signed up management agreements with the Four Seasons renowned chain to operate the hotels in Luxor, Madinaty, and Sharm Extension and appointed Kempinski to operate the Nile hotel

R i d hi t k t 100% f th F S Sh l Sh ikh R t b i i th 39 3% • Raised ownership stake to 100% of the Four Seasons Sharm el-Sheikh Resort by acquiring the 39.3% minority stake held by Kingdom Hotel Investments (KHI)

32

TMG

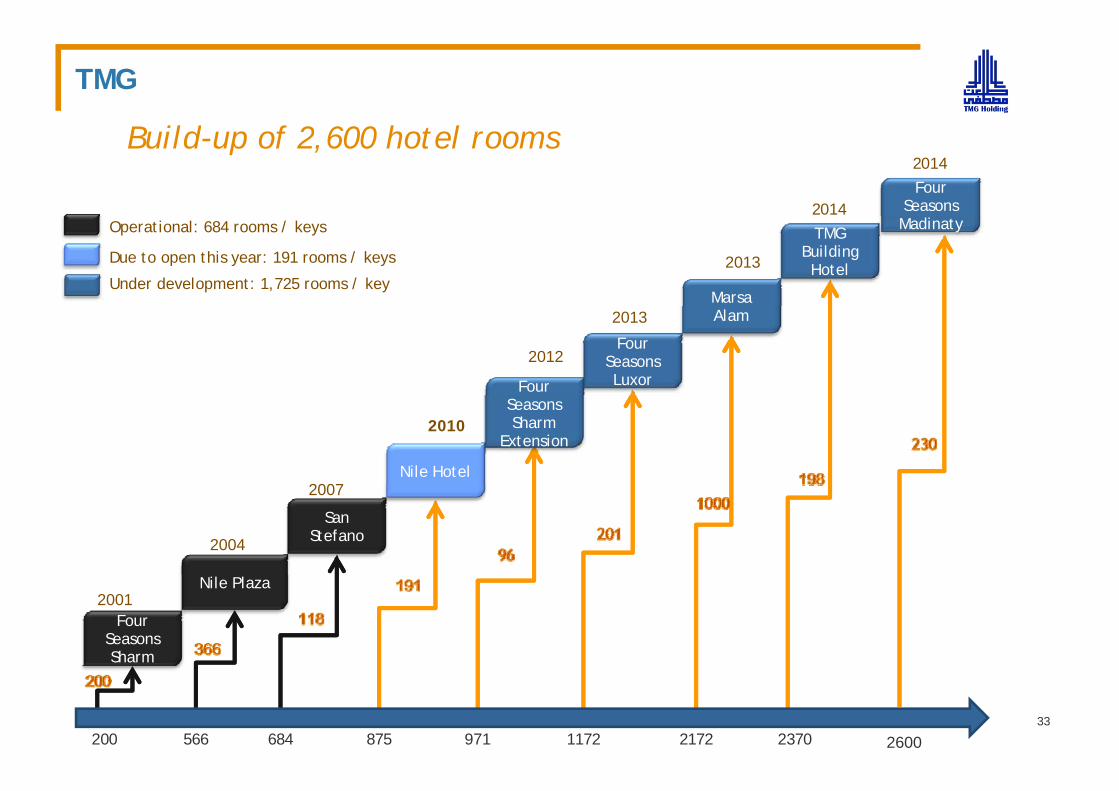

B ild f 2 600 h l CompanyLogoBuild-up of 2,600 hotel rooms

2014Four

Seasons

2014

Marsa

2013

TMG Building Hotel

Operational: 684 rooms / keys

Due to open this year: 191 rooms / keys

Under development: 1,725 rooms / key

Madinaty

Four

2012Four

Seasons Luxor

2013 Alam

2007Nile Hotel

2010Seasons Sharm

Extension

2004

2007

San Stefano

Nile Plaza

Four Seasons Sharm

2001

33237021721172971875684566200 2600

TMG

U i h l j CompanyLogoUpcoming hotel projects

Nile Hotel Development Progress

Rooms/ keys :191

Operator: Kempinski

Land area: 2 k sqm

Project in finalization stage

Purchased Sednawy Villa extension

Appointed kempinski management companyLand area: 2 k sqm

BUA: 19.8 k sqmInvestment cost: USD 34 MN

Appointed kempinski management company

Four Seasons Sharm Extension Development Progress

Rooms/ keys :96

Residential properties: 114

Operator: Four Seasons

Land area 960 k sqm

Purchased land

Finished design

Issued licenses and permitsq

BUA: 490 k sqmHotel Investment cost: USD 277 MN

Issued licenses and permits

Appointed four seasons management company

Marsa Alam Development Progress

Rooms/ keys :750

Residential properties: 2250

phase one : 1000 units

Land area 3.2 mn sqm

Purchased land

Finished design

Obtained TDA approval

34

Land area 3.2 mn sqm

BUA: 390 k sqmPhase I Investment cost: USD 211 MN

pp

Issued licenses and permits

TMG

U i h l j CompanyLogoUpcoming hotel projects

Four Seasons Luxor Development Progress

Rooms/ keys :201

Operator: Four Seasons

Land area 20 k sqm

Signed concession agreement

Finished design

Issued licenses and permits

Four Seasons Madinaty Development Progress

BUA: 43 k sqmInvestment cost: USD 135 MN

Appointed four seasons management company

Rooms/ keys :240

Residential properties: 100

Operator: Four Seasons

Land area 175 k sqm

Finished design

Appointed four seasons management company

q

BUA: 49 k sqmHotel Investment cost: USD 190 MN

TMG Building Hotel Development Progress

Rooms/ keys :200

Operator: TBD

Land area 2 k sqm

BUA 16 k

Purchased land

Finished design

Issued licenses and permits

35

BUA: 16 k sqmInvestment cost: USD 140 MN

CompanyLogo

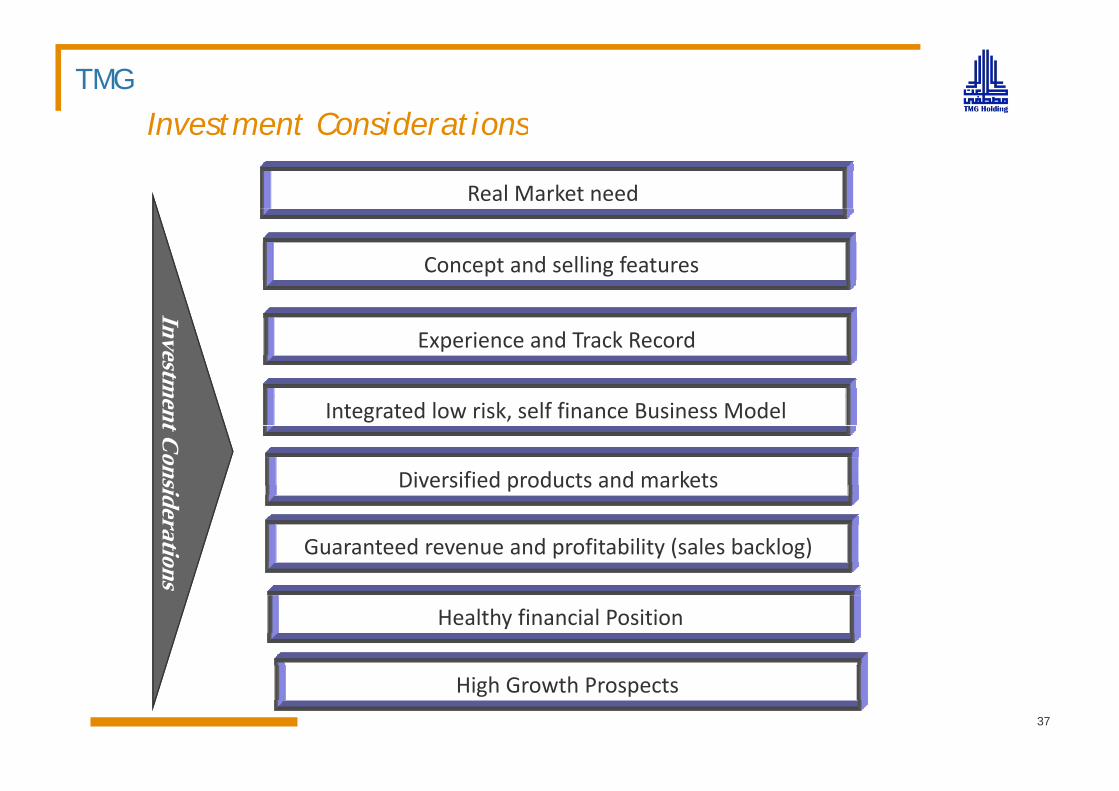

Investment Considerations

Risks and Mitigants

TMG

Investment Considerations CompanyLogo

Investment Considerations

Real Market need

Concept and selling features

Investm

Experience and Track Record

ment C

ons

Integrated low risk, self finance Business Model

Diversified products and marketssideration Guaranteed revenue and profitability (sales backlog)

Diversified products and markets

ns

Healthy financial Position

High Growth Prospects37

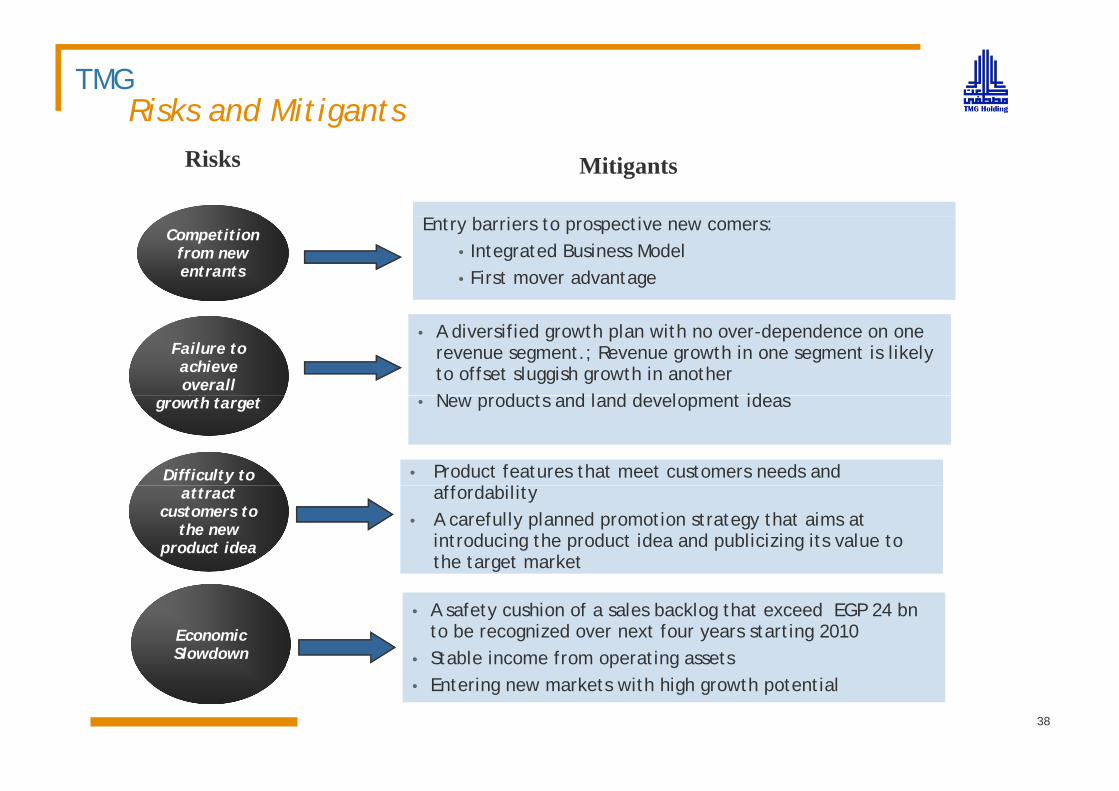

TMGRisks and Mitigants

CompanyLogo

gRisks Mitigants

Entry barriers to prospective new comers:• Integrated Business Model • First mover advantage

Competition from new entrants

• A diversified growth plan with no over-dependence on one revenue segment.; Revenue growth in one segment is likely to offset sluggish growth in another N d t d l d d l t id

Failure to achieve overall

• New products and land development ideasgrowth target

• Product features that meet customers needs and ff d b l

Difficulty to affordability

• A carefully planned promotion strategy that aims at introducing the product idea and publicizing its value to the target market

attract customers to

the new product idea

• A safety cushion of a sales backlog that exceed EGP 24 bnto be recognized over next four years starting 2010

• Stable income from operating assetsEconomic Slowdown p g

• Entering new markets with high growth potential

38

CompanyLogo

Thank you