Taking Data Analytics to the Next Level · Taking Data Analytics to the Next Level ... M&A due...

31

®2013 Association of Certified Fraud Examiners, Inc. Taking Data Analytics to the Next Level The New Structured Toolbox: Risk Scoring and Leading Analytics

Transcript of Taking Data Analytics to the Next Level · Taking Data Analytics to the Next Level ... M&A due...

®2013 Association of Certified Fraud Examiners, Inc.

Taking Data Analytics

to the Next Level

The New Structured Toolbox:

Risk Scoring and Leading Analytics

®2013 Association of Certified Fraud Examiners, Inc.

2 of 31

Today’s Agenda

Section 1: 70 minutes

Key concepts in forensic data analytics

Technical baseline

Break: 15 minutes

Section 2: 70 minutes

Advanced forensic analytics using structured data

Advanced forensic analytics using unstructured data

Break: 15 minutes

Section 3: 70 minutes

Bringing it all together with big data

®2013 Association of Certified Fraud Examiners, Inc.

3 of 31

Introductions and Course Objectives

What would you like to take away

from this course?

Discussion…

®2013 Association of Certified Fraud Examiners, Inc.

4 of 31

Reflecting on the Fraud Triangle The fraud triangle is a key element to every test we design.

Internal

Controls

Internal and External

Pressure

Increased

mediums of

communication

Race to expand

in emerging

markets

Opportunity to

Commit Fraud

Budgets are

decreasing.

Companies and

organizations are

doing more with

less

Companies are

downsizing and

decentralized,

which has an

immediate effect

on internal

controls

Stressed and

dissatisfied

employees might

have greater

ability to

rationalize

improper actions

Pressure

Opportunity

Rationalization

Significant

company

expansion into

emerging

markets (BRIC

countries)

Job stress

is high

®2013 Association of Certified Fraud Examiners, Inc.

5 of 31

Need for Integrating Analytics

Bribery and corruption remain top risks Aggressive enforcement continues

New U.S. DoJ/SEC guidance

Risk areas: Integrity of sales force

Integrity of suppliers and distributors

Integrity of employees, conflicts of interests

Improper payments in the forms of bribes/kickbacks

Travel & entertainment abuse

M&A due diligence

®2013 Association of Certified Fraud Examiners, Inc.

6 of 31

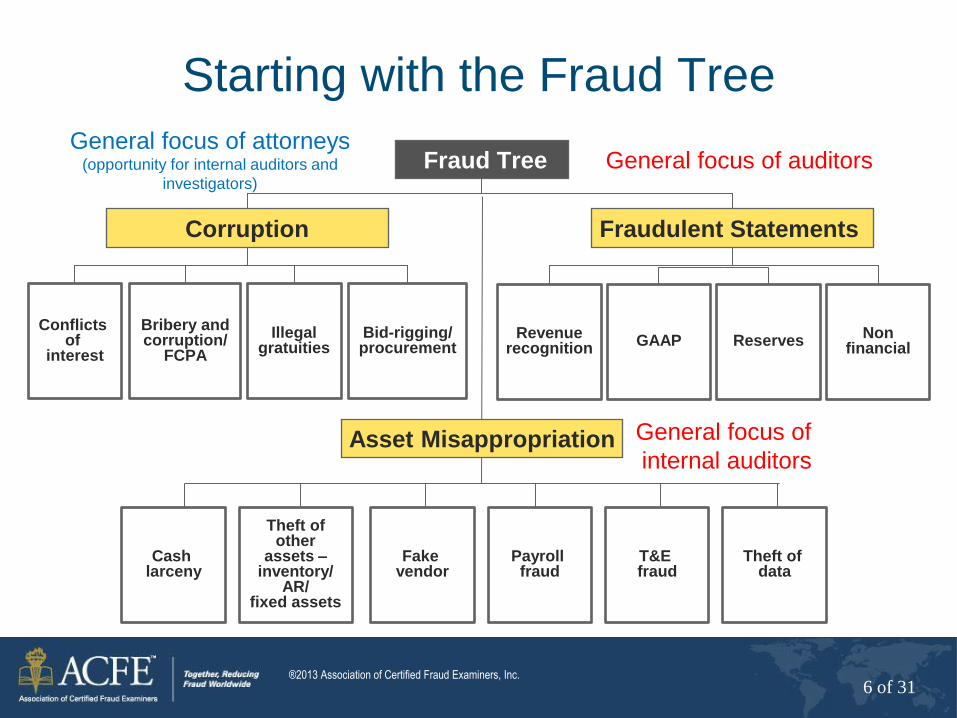

Fraud Tree

Cash larceny

Theft of other

assets – inventory/

AR/ fixed assets

Revenue recognition

Non financial

Conflicts of

interest

Bribery and corruption/

FCPA

Illegal gratuities

Bid-rigging/ procurement

Corruption Fraudulent Statements

Asset Misappropriation

Fake vendor

Payroll fraud

T&E fraud

Theft of data

GAAP Reserves

General focus of auditors

General focus of

internal auditors

General focus of attorneys (opportunity for internal auditors and

investigators)

Starting with the Fraud Tree

®2013 Association of Certified Fraud Examiners, Inc.

7 of 31

ACFE’s 2012 Report to the Nations on

Occupational Fraud and Abuse

Estimated 5% of revenues lost fraud

Median loss per incident was $140,000

Median fraud duration was 18 months

before detection

More than 50% of cases reported globally were

corruption and billing schemes

The presence of anti-fraud controls is notably

correlated with significant decreases in the cost

and duration of the scheme

®2013 Association of Certified Fraud Examiners, Inc.

8 of 31

372 global CFOs surveyed

2012 Ernst & Young Global Fraud Survey

39% of respondents say that bribery &

corruption practices occur frequently in their

countries

15% of CFOs surveyed said they would be

willing to make cash payments to win business

20% of CFOs surveyed said that they

are willing to make personal gifts to

win business

®2013 Association of Certified Fraud Examiners, Inc.

9 of 31

How Companies Are Responding

Compliance and legal are looking beyond

policies and training Teaming with internal audit and internal investigations to test for

effectiveness

Integrating new analytics specifically targeting

corruption—these aren’t your typical process

controls or SOX testing

®2013 Association of Certified Fraud Examiners, Inc.

10 of 31

How Companies Are Responding

Developing “big data” concepts including: Text mining (unstructured data)

Statistical analysis and anomaly detection

Visual analytics and interactive dashboards

100% data sampling, not just random sampling

Analytics used as “pre-field work” before the on-

site audit or interview

®2013 Association of Certified Fraud Examiners, Inc.

11 of 31

Elements of

a successful

corporate

anti-fraud,

bribery and

corruption

program

Anti-fraud,

bribery and

corruption

key activities

may

include

►Review of fraud policies

and controls

►Industry benchmark of

anti-fraud programs

►Gap analysis

►Future state design

session

►Assess roles and

responsibilities

►Fraud and risk

committee formulation

►Customized training

►Corporate governance

►Corporate anti-fraud

road map

►FCPA / anti-bribery

assessments

►Fraud risk assessment

►Targeted anti-fraud analytics

►Anti-bribery and corruption

analytics (pre-field work)

►On-site interviews and substantive

testing

►M&A Due Diligence

►3rd Party Due Diligence

►3rd Party Risk profiling

►Conduct background checks

►Investigations

►Fraud response

planning

►Forensic data

analytics

►Discovery and

document

review

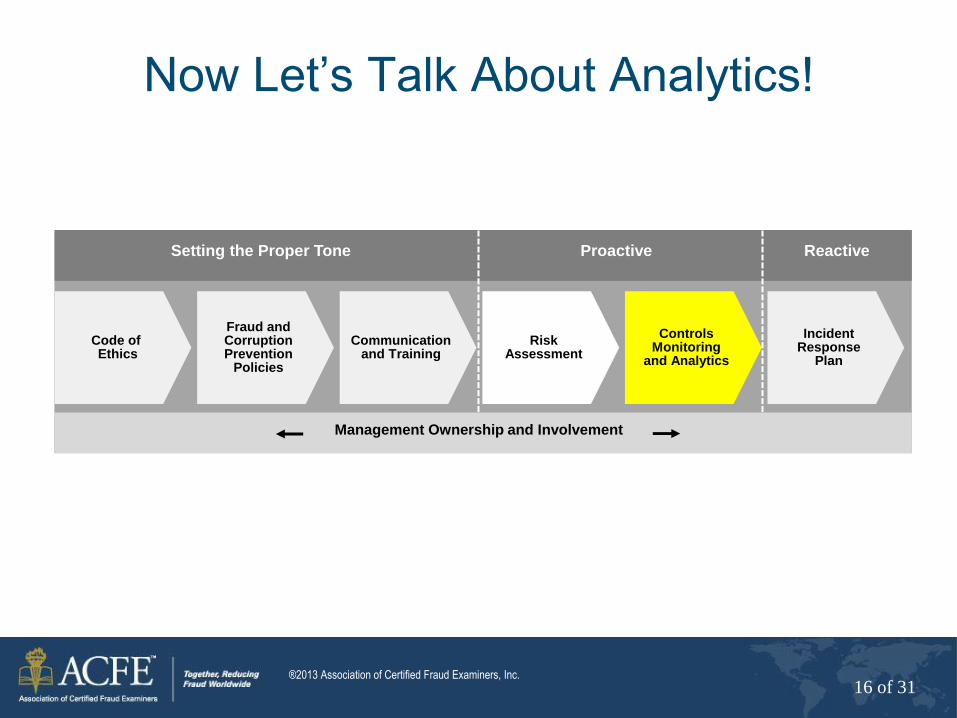

Code of Ethics

Fraud and Corruption Prevention

Policies

Communication and Training

Risk Assessment

Controls Monitoring

and Analytics

Incident Response

Plan

Reactive

Proactive

Setting the Proper Tone

Management Ownership and Involvement

Focus on analytics

Components of an Effective Anti-Fraud/

ABaC Compliance Program

®2013 Association of Certified Fraud Examiners, Inc.

12 of 31

Conducting a Fraud Risk Assessment

Code of Ethics

Fraud and Corruption Prevention

Policies

Communication and Training

Risk Assessment

Controls Monitoring

and Analytics

Incident Response

Plan

Reactive

Proactive

Setting the Proper Tone

Management Ownership and Involvement

®2013 Association of Certified Fraud Examiners, Inc.

13 of 31

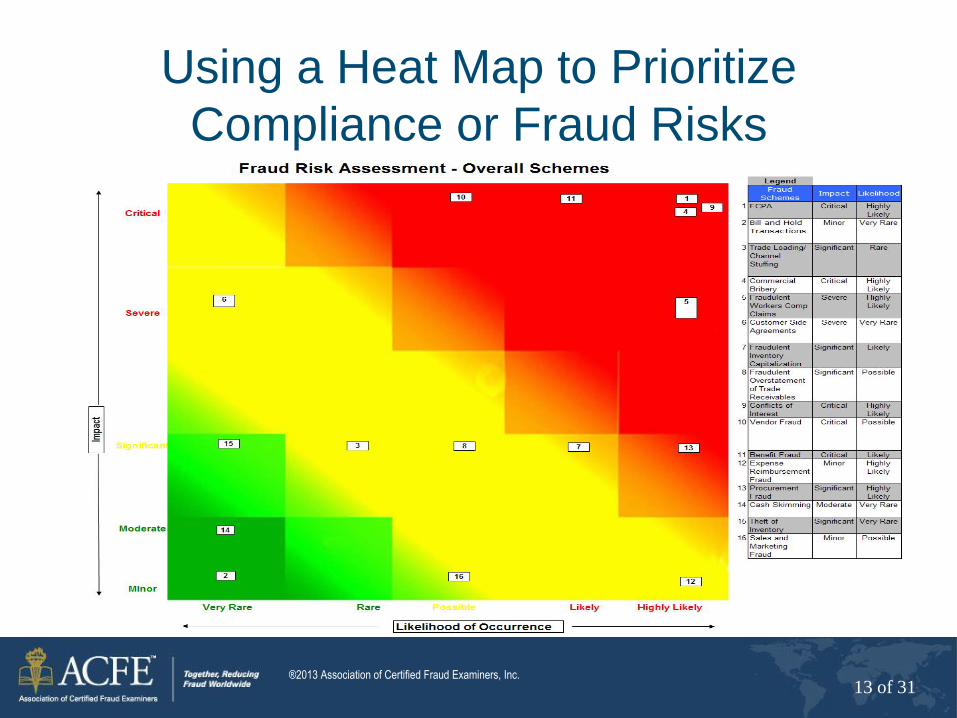

Using a Heat Map to Prioritize

Compliance or Fraud Risks

®2013 Association of Certified Fraud Examiners, Inc.

14 of 31

Risk Assessment: Using the Result Improve

• High risk exposures with low levels of control

form the priorities for improvement

opportunities.

Verify

• High risk exposures with strong controls and

management efforts form the focus for audit

to provide assurance that controls are

adequate and efficient.

Monitor

• Low risk exposures accompanied by a lower

level of control are often considered emerging

and must remain a focus of ongoing

monitoring efforts

Optimize

• Low risk exposures with a moderate level of

control may be consciously accepted or may

be a focus to optimize the processes and

controls for greater efficiency.

Verify Improve

Monitor Optimize

®2013 Association of Certified Fraud Examiners, Inc.

15 of 31

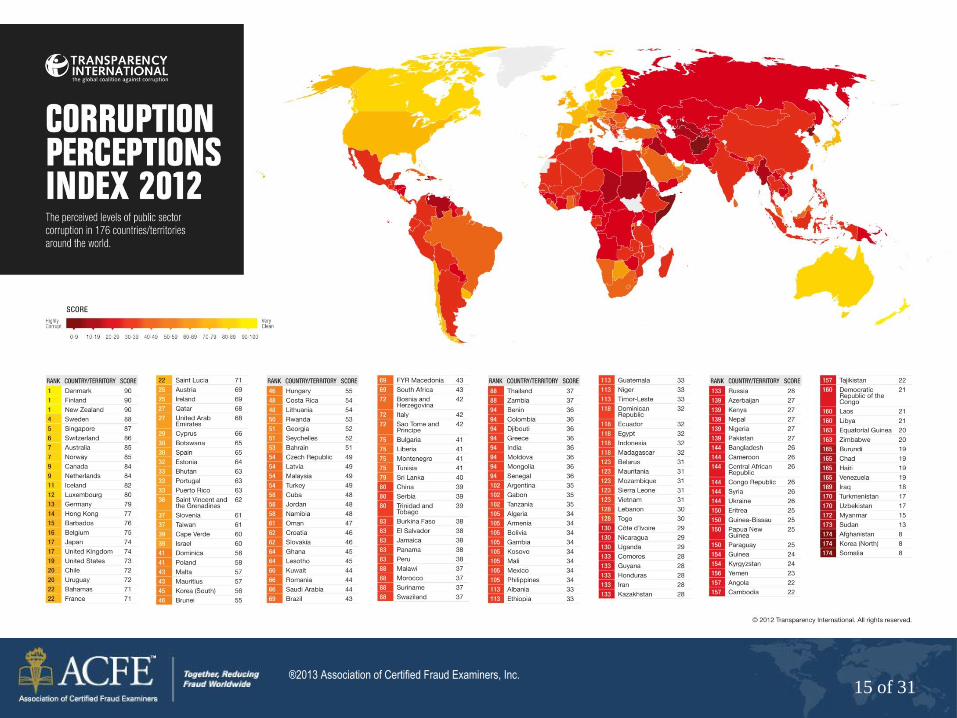

2011 Corruption Perceptions Index

®2013 Association of Certified Fraud Examiners, Inc.

16 of 31

Code of Ethics

Fraud and Corruption Prevention

Policies

Communication and Training

Risk Assessment

Controls Monitoring

and Analytics

Incident Response

Plan

Reactive

Proactive

Setting the Proper Tone

Management Ownership and Involvement

Now Let’s Talk About Analytics!

®2013 Association of Certified Fraud Examiners, Inc.

17 of 31

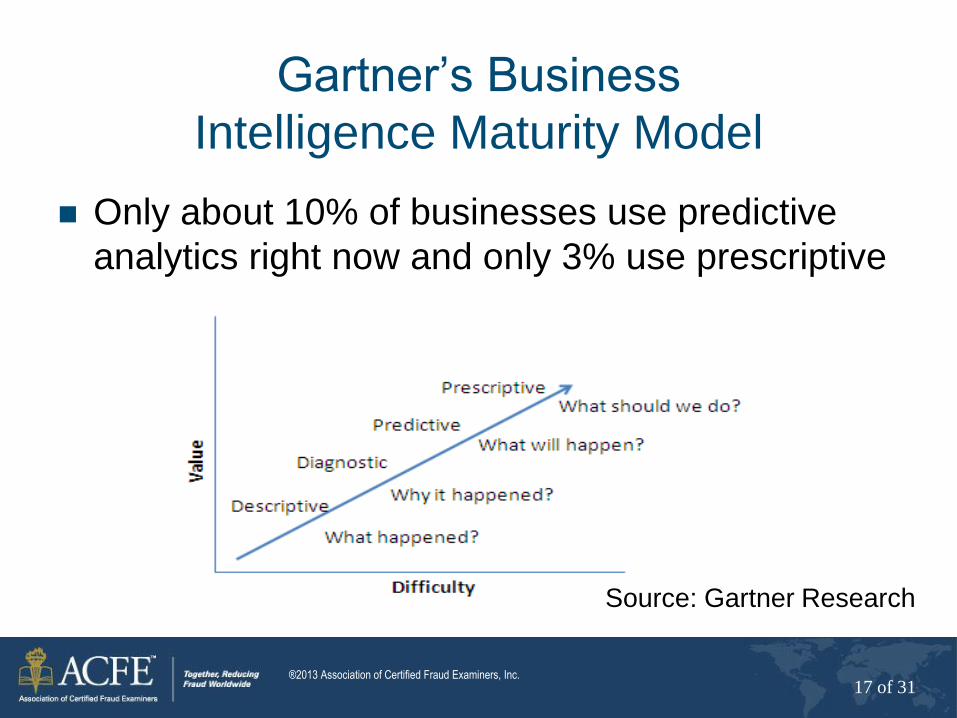

Gartner’s Business

Intelligence Maturity Model

Only about 10% of businesses use predictive

analytics right now and only 3% use prescriptive

Source: Gartner Research

®2013 Association of Certified Fraud Examiners, Inc.

18 of 31

Emerging Trends: Information and Analytics

Descriptive Analytics

What is happening?

Diagnostic Analytics

Why did it happen?

Predictive Analytics

What is likely to happen?

Prescriptive Analytics

What should I do about it?

Structured Hybrid Unstructured

/ Content

Source: Gartner Research

®2013 Association of Certified Fraud Examiners, Inc.

19 of 31

How Is Fraud Detected?

Source: ACFE 2010 Report to the Nations On Occupational Fraud

50% by tip or accident! Heavy use of “descriptive” analytics, if at all.

2012 ACFE Report to the Nations on Occupational Fraud

®2013 Association of Certified Fraud Examiners, Inc.

20 of 31

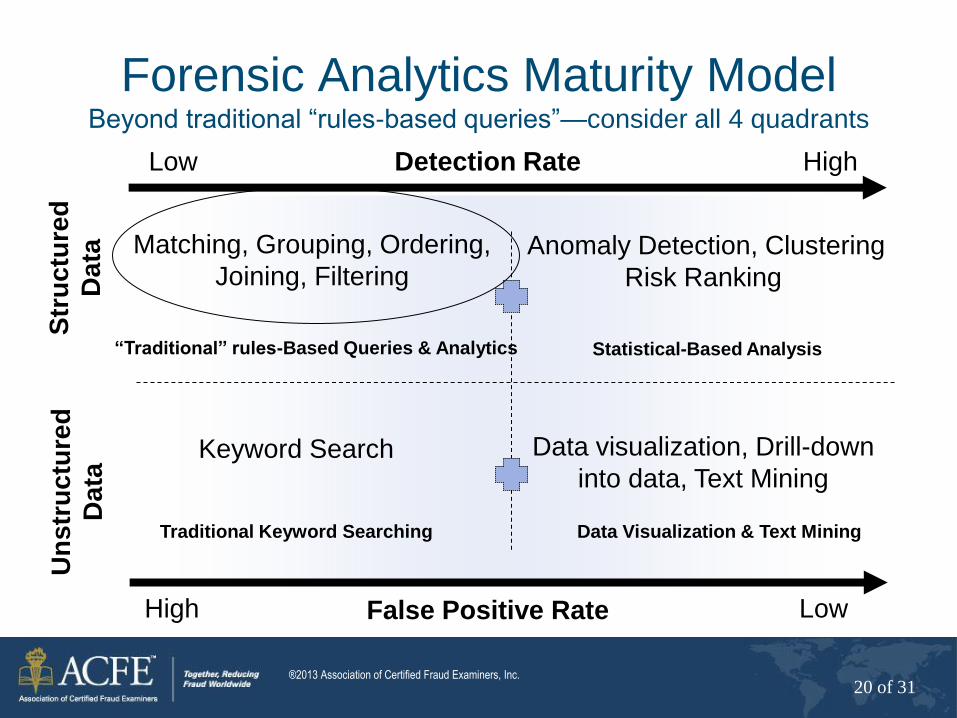

False Positive Rate High Low

Str

uc

ture

d

Da

ta

Detection Rate Low High

Un

str

uc

ture

d

Da

ta

“Traditional” rules-Based Queries & Analytics

Matching, Grouping, Ordering,

Joining, Filtering

Statistical-Based Analysis

Anomaly Detection, Clustering

Risk Ranking

Traditional Keyword Searching

Keyword Search

Data Visualization & Text Mining

Data visualization, Drill-down

into data, Text Mining

Forensic Analytics Maturity Model Beyond traditional “rules-based queries”—consider all 4 quadrants

®2013 Association of Certified Fraud Examiners, Inc.

21 of 31

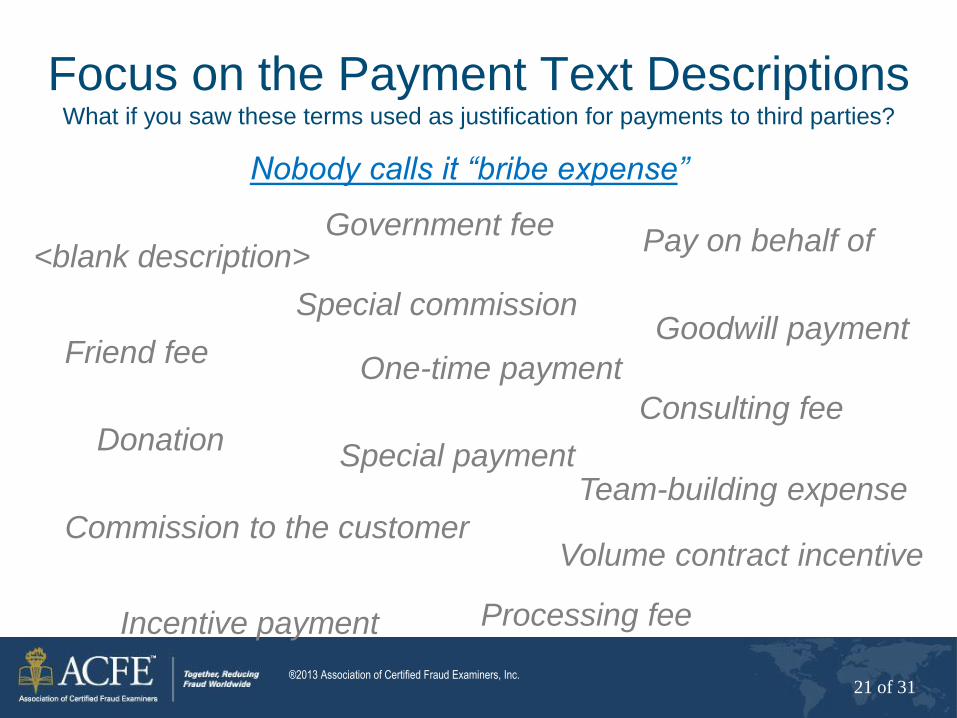

Focus on the Payment Text Descriptions What if you saw these terms used as justification for payments to third parties?

<blank description>

Donation

Pay on behalf of

Special payment

Volume contract incentive

One-time payment

Special commission

Incentive payment

Team-building expense

Friend fee

Nobody calls it “bribe expense”

Commission to the customer

Consulting fee

Government fee

Processing fee

Goodwill payment

®2013 Association of Certified Fraud Examiners, Inc.

22 of 31

Text Mining: Disbursements Analysis

®2013 Association of Certified Fraud Examiners, Inc.

23 of 31

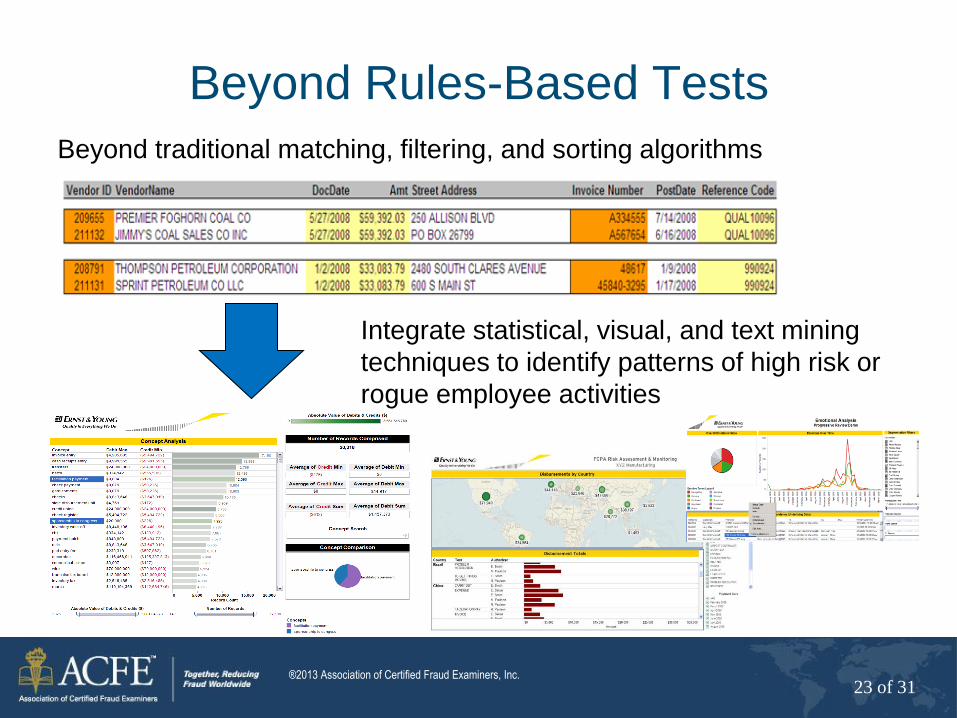

Beyond Rules-Based Tests

Beyond traditional matching, filtering, and sorting algorithms

Integrate statistical, visual, and text mining

techniques to identify patterns of high risk or

rogue employee activities

®2013 Association of Certified Fraud Examiners, Inc.

24 of 31

Technical Baseline

The right tools for the right

job

Working with IT

Data-mapping exercise

®2013 Association of Certified Fraud Examiners, Inc.

25 of 31

The Right Tools for the Right Job Partial list of examples

False Positive Rate High Low

Str

uc

ture

d

Da

ta

Detection Rate Low High

Un

str

uc

ture

d

Da

ta

Rules Based Queries & Analytics

Excel, Access, ACL,

SQL Server

Statistical-Based Analysis

SPSS, SAS, R, SAP Hana

Traditional Keyword Searching

dtSearch

Data Visualization & Text Mining

Tableau, i2, SPSS, SAS

®2013 Association of Certified Fraud Examiners, Inc.

26 of 31

Working With IT

Design your analytics based on fraud risks

Then determine your required data sources Structured and unstructured data

Prepare a data-request memo Specify table names if possible or field names if unknown

Specify desired data output (e.g., flat file, CSV, etc.)

Specify time frame

Be prepared to walk IT through your data

request

®2013 Association of Certified Fraud Examiners, Inc.

27 of 31

Common Data Sources:

Asset Misappropriation Schemes

Source Data

Vendor master Lists all approved vendors

Employee master Lists all employees

Accounts payable ledger Tracks when and to whom payments are due

Cash disbursements journal Tracks all cash disbursements

Purchases journal Tracks requests for purchases

Depending on the case, selected general ledger

accounts may also be selected.

®2013 Association of Certified Fraud Examiners, Inc.

28 of 31

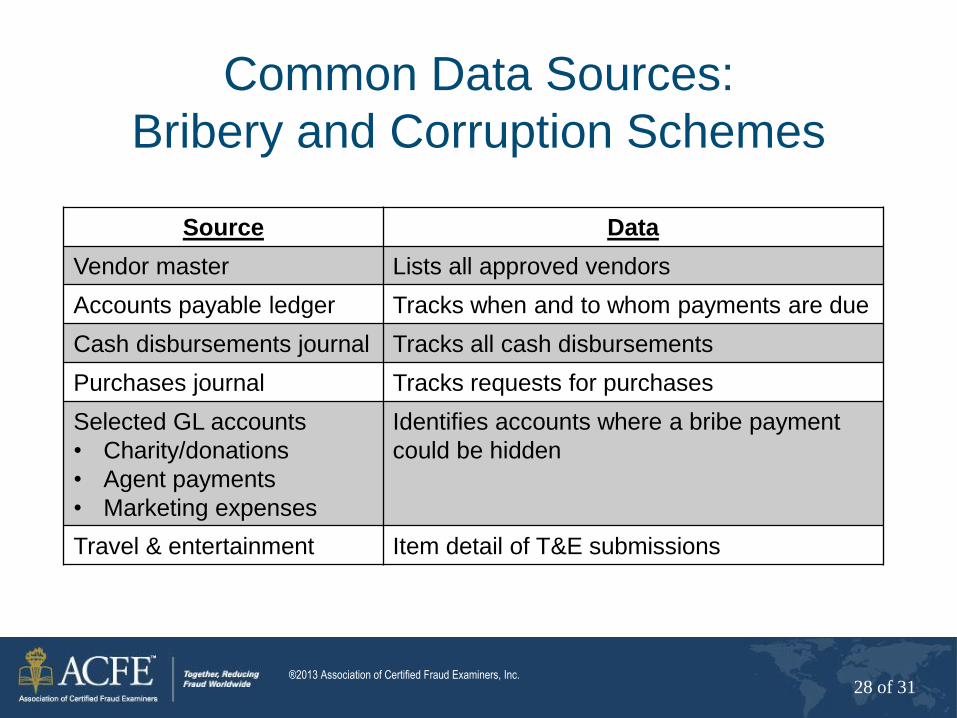

Common Data Sources:

Bribery and Corruption Schemes

Source Data

Vendor master Lists all approved vendors

Accounts payable ledger Tracks when and to whom payments are due

Cash disbursements journal Tracks all cash disbursements

Purchases journal Tracks requests for purchases

Selected GL accounts

• Charity/donations

• Agent payments

• Marketing expenses

Identifies accounts where a bribe payment

could be hidden

Travel & entertainment Item detail of T&E submissions

®2013 Association of Certified Fraud Examiners, Inc.

29 of 31

DOJ/SEC Guidance on Where

Bribery Risks Exist

DOJ/SEC FCPA

Resource Guide

– Nov. 2012

®2013 Association of Certified Fraud Examiners, Inc.

30 of 31

Common Data Sources:

Financial Misstatements

Source Data

Sales journal Sales by product, date, customer

Accounts receivable Tracks amounts due to company by customer, over

time

Customer master Lists all customers

Various sub-ledgers May include inventory, capital expenses, outstanding

loans, etc.

®2013 Association of Certified Fraud Examiners, Inc.

31 of 31

Practical Problem: Data-Mapping Exercise