taking care of your financial wellness.

55

Transcript of taking care of your financial wellness.

taking care of yourfinancial wellness.

An authorised �nancial services and credit providerMomentum Group Limited is a wholly-owned subsidiary of MMI Holdings Limited

advice | insurance | investments | health

Momentum, in collaboration with Unisa, is at the forefront of understanding the Financial Wellness of all South Africans. Visit www.momentum.co.za and click on Financial Wellness for more information.

Momentum. For your Financial Wellness.

tax guide2015/2016

C

M

Y

CM

MY

CY

CMY

K

Tax Guide 2015_3.pdf 2 2015/01/20 2:12 PM

1

This booklet is published by PKF Publishers (Pty) Ltd for and on behalf of

• Allinformationcontainedhereinisbelievedtobecorrectatthetimeofpublication, 25February2015.Thecontentsshouldnotbeusedasabasisforactionwithout furtherprofessionaladvice.• Whileutmostcarehasbeentakeninthecompilationofthispublicationno responsibilitywillbeacceptedforanyinaccuracies,errorsoromissions.• Theinformationincorporatescommentaryfromthebudgetspeechbutthelegislation finallyenactedmaydifferconsiderably.• Changesinratesoftaxannouncedinthebudgetspeechforthe2016taxyearbecome effectiveonlyoncethelegislationisenactedbyParliament.• Copyrightsubsistsinthiswork.Nopartofthisworkmaybereproducedinanyformor byanymeanswithoutthepublisher’swrittenpermission.

chartered accountants& business advisers

1 Medical Expense Tax Credit Toalleviatetheburdenfortaxpayersolderthan65years,itisproposed thatthemedicalexpensetaxcreditbetakenintoaccountforboth PAYEandprovisionaltax.

2 Harmonisation of Retirement Savings Thetaxationofcontributionsandtherulesoncompulsoryannuitisation forpensionfunds,providentfundsandretirementannuityfundswill commenceon1March2016.

3 Research and Development Thebacklogintheapprovalprocessiscreatingdifficultiesforsmall businesses.Measureswillbeconsideredtoensurethattaxpayersare notdisadvantaged.

4 Davis Tax Committee TheCommitteecontinuestoreviewtaxpolicy.Itisconsidering methodstoimprovetransferpricingdocumentationandrevisingthe rulesforcontrolledforeigncompanies.

5 Diesel Refund ItisproposedtodelinkthedieselrefundfromtheVATsystem.Due tothesignificantdisputesoverrecord-keeping,claritywillbeprovided.

6 Monitoring of Capital Flows TheSouthAfricanReserveBankandSARSwillbeworkingclosely togethertomonitorcapitalflows,inordertoreducecapitalleakageand taxevasion.

7 Energy-Efficiency Savings Tax Incentive Theenergy-efficiencysavingstaxincentivewillbeincreasedfrom 45c/kwhto95c/kwh.

8 Withholding Tax on Interest Itisproposedthattheterm“interest,”forwithholdingtaxpurposes,be specificallydefinedtoavoidconfusionwithotherdefinitions.

BUDGET PROPOSALS

2

INDEX AdministrativePenalties 48ArbitrationAwards 19AssessedLossesRing-fenced 43BodyCorporates 45Bond/InstalmentRepayments 38Broad-BasedEmployeeEquity 18BudgetProposals 1BursariesandScholarships 18CapitalGainsTax 24CapitalIncentiveAllowances 21CorporateTransactions 19Deductions-Donations 45Deductions-Employees 11Deductions-Retirement 16Deductions-Royalties 36Deductions-TravelExpenses 15DeemedCapital-DisposalofShares 27DeemedEmployees 10Directors-PAYE 29DisputeResolution 46DividendsTax 3DonationsTax 49DoubleTaxationAgreements 32EffectiveTaxRate 4EnvironmentalExpenditure 20EstateDuty 49ExchangeControlRegulations 40Executor’sRemuneration 49Exemptions-Individuals 11FarmingIncome 44ForeignCompanies/BranchTax 4FringeBenefits 12HeadquarterCompany 33HotelAllowances 20IndustrialPolicyProjects 28InterestRates-Changes 39IRP5Codes 50LearnershipAllowances 28LimitationofInterestDeduction 19MarriedinCommunityofProperty 19MedicalAidRebates/Credits 5MedicalExpenseCredit 9NationalCreditAct 39Non-Residents 32OfficialInterestRatesandPenalties 38PatentandIntellectualProperty 43Pre-PaidExpenditure 29Pre-ProductionInterest 46Pre-TradingExpenditure 46

PrimeOverdraftRates 37ProvisionalTax 8PublicBenefitOrganisations 45RecreationalClubs 45ReinvestmentRelief 27RelocationofanEmployee 16ResearchandDevelopment 27ResidenceBasedTaxation 30ResidentialBuildingAllowances 20RestraintofTrade 46RetentionofDocuments andRecords 52RetirementLumpSumBenefits 17SecuritiesTransferTax 29SkillsDevelopmentLevy 39SmallBusinessCorporations 7SecondaryTaxonCompanies 4SpecialEconomicZones 45StampDuty 29StrategicAllowances 24SubsistenceAllowances 14SuspensionofPayment 48TaxClearanceCertificates 47TaxFreeSavingsAccount 19TaxRates-Companies 4TaxRates-Individuals 5TaxRates-Trusts 6TaxRebates 5TaxThresholds 5TransferDuty 37TravelAllowances 14TrustDistributions 36TurnoverTax-MicroBusinesses 6UnderstatementPenalties 47UnquantifiedProceeds 27Value-AddedTax 42VariableRemuneration 15VATReliefforDevelopers 43VATReliefInter-group 43VentureCapitalInvestments 28VoluntaryDisclosure 47WearandTearAllowances 22WearandTearConnectedPersons 29WithholdingTaxesSummary 34WithdrawalLumpSumBenefits 17WithholdingTaxonInterest 32WithholdingTaxonRoyalties 33WithholdingTaxonServiceFees 33YouthEmploymentIncentive 18

3

DIVIDENDS TAX

Asfrom1April2012,DividendsTaxisapplicabletoallSouthAfricanresidentcompaniesaswellasnon-residentcompanieslistedontheJSE.Dividends Taxisbornebytheshareholderatarateof15%(subjecttoanyreductionintermsofadoubletaxationagreement).Taxondividendsin specieremains theliabilityofthecompanydeclaringthedividend.

Exemptions from Dividends TaxThefollowingshareholdersareexemptfromDividendsTax:SouthAfricanresidentcompanies,theGovernment,PBO’s,certainexemptbodies,closurerehabilitationtrusts,pension,providentandsimilarfunds,shareholdersinaregisteredmicrobusiness(providedthedividenddoesnotexceedR200000 intheyearofassessment),andanon-residentreceivingadividendfromanon-residentcompanywhichislistedontheJSE,i.e.adual-listedcompany.Thesameexemptionsapplyinrespectofdividendsin specie.Asfrom16January2014,thecompanypayingthedividendandthecompanyreceivingthedividendarerequiredtosubmitaDividendsTaxreturn.

Withholding Tax ObligationsInrespectofdividends,otherthandividendsin specie,thecompanydeclaringthedividendisrequiredtowithholdtheDividendsTaxonpayment.Liability forwithholdingtaxshiftsifthedividendispaidtoaregulatedintermediarywhichincludescentralsecuritiesdepositoryparticipants,brokers,collective investmentschemes,approvedtransfersecretariesandlinkedinvestmentserviceproviders.DividendsTaxcanbeeliminatedorreduceduponthe timelyreceiptofawrittendeclarationthattheshareholderiseitherentitled toanexemptionortodoubletaxationagreementreliefandawrittenunder- takingfromtheshareholderthatthecompanywillbeinformedshouldthere beachangeincircumstances.Inthecaseofdividendsin specie there is no withholdingobligationasthetaxremainsaliabilityofthecompany declaringthedividend.However,theDividendsTaxmaysimilarlybe eliminatedorreducedontimelyreceiptoftherelevantdeclarationsand undertakings.

STC CreditsCompaniesweredeemedtohavedeclaredadividendofnilon31March2012inordertoascertaintheSTCcreditsthatwouldbeavailableforset-offfrom 1April2012.STCcreditswillbeexhaustedfirst.STCcreditsmustbeusedonorbefore1April2015.

Revised Dividend DefinitionAsfrom1January2011,thedefinitionofadividendhasbeensimplifiedand includesalldistributionstoashareholderotherthan,amongstothers,a reductionofcontributedtaxcapital(whichconsistsofuntaintedstatedcapitalofacompany),capitalisationissuesandageneralsharebuy-backbyaJSElistedcompany.Adistributionofcontributedtaxcapitalisnotregardedasadividendifthedirectors,immediatelypriortomakingthedistribution,recordinwritingthat thedistributionismadeoutofcontributedtaxcapital.

Interest-Free LoansThereisadeemeddividendimplicationwherealowinterestorinterest-freeloanoradvanceismadebyacompanytoaresidentnaturalpersonortrustwhichisconnectedtothecompanyortoaperson(otherthanacompany) whoisconnectedtosuchnaturalpersonortrust.Thedeemeddividendis calculatedbyapplyingtotheloanoradvancethedifferencebetweenthe officialinterestrateandtheratechargedbythecompany.

4

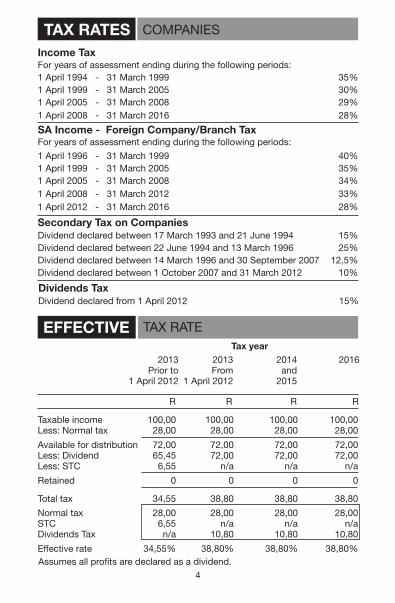

Income TaxForyearsofassessmentendingduringthefollowingperiods:1April1994-31March1999 35%1April1999-31March2005 30%1April2005-31March2008 29%1April2008-31March2016 28%

TAX RATES COMPANIES

SA Income - Foreign Company/Branch TaxForyearsofassessmentendingduringthefollowingperiods:

1April1996-31March1999 40%1April1999-31March2005 35%1April2005-31March2008 34%1April2008-31March2012 33%1April2012-31March2016 28%

Secondary Tax on CompaniesDividenddeclaredbetween17March1993and21June1994 15%Dividenddeclaredbetween22June1994and13March1996 25%Dividenddeclaredbetween14March1996and30September2007 12,5%Dividenddeclaredbetween1October2007and31March2012 10%

EFFECTIVE TAXRATE

Assumesallprofitsaredeclaredasadividend.

Taxableincome 100,00 100,00 100,00 100,00Less:Normaltax 28,00 28,00 28,00 28,00

Availablefordistribution 72,00 72,00 72,00 72,00Less:Dividend 65,45 72,00 72,00 72,00Less:STC 6,55 n/a n/a n/a

Retained 0 0 0 0

Totaltax 34,55 38,80 38,80 38,80

Normaltax 28,00 28,00 28,00 28,00STC 6,55 n/a n/a n/aDividendsTax n/a 10,80 10,80 10,80

Effectiverate 34,55% 38,80% 38,80% 38,80%

2013 2013 2014 2016 Priorto From and 1April2012 1April2012 2015

Tax year

R R R R

Dividends TaxDividenddeclaredfrom1April2012 15%

TAX RATES INDIVIDUALS-2015

Taxable income Rates of taxR0-R174550 18%ofeachR1R174551-R272700 R31419+25%oftheamountover R174550R272701-R377450 R55957+30%oftheamountover R272700R377451-R528000 R87382+35%oftheamountover R377450R528001-R673100 R140074+38%oftheamountover R528000R673101+ R195212+40%oftheamountover R673100

Amounts deductible from the tax payable 2015 2016Personsunder65 R12726 R13257Persons65andunder75 R19836 R20664Persons75andover R22203 R23130

TAX REBATES

Monthly amounts deductible from tax payable 2015 2016Mainmember R257 R270Mainmemberwithonedependant R514 R540Mainmemberwithtwodependants R686 R721

Eachadditionaldependantqualifiesforafurtherrebateorcreditof R181(2015:R172)permonth.

REBATES/CREDITS

5

TAX THRESHOLDS

Taxable income 2015 2016Personsunder65 R70700 R73650Persons65andunder75 R110200 R114800Persons75andover R123350 R128500

MEDICAL AID

TAX RATES INDIVIDUALS-2016

Taxable income Rates of taxR0-R181900 18%ofeachR1R181901-R284100 R32742+26%oftheamountover R181900R284101-R393200 R59314+31%oftheamountover R284100R393201-R550100 R93135+36%oftheamountover R393200R550101-R701300 R149619+39%oftheamountover R550100R701301+ R208587+41%oftheamountover R701300

6

Rate of tax 2015 2016

Alltaxableincome 40% 41%

Specialtrustsaretaxedattheratesapplicabletoindividuals,butarenotentitled to any rebate.Aspecial trustisonecreated:• solelyforthebenefitofapersonaffectedbyamentalillnessorserious physicaldisabilitywhichpreventsthatpersonfromearningsufficient incometomaintainhimself.Wherethepersonforwhosebenefitthe trustwasestablisheddiespriortooronthelastdayoftheyearof assessmentthetrustwillnolongerberegardedasaspecialtrust• asatestamentarytrustestablishedsolelyforthebenefitofminor childrenwhoarerelatedtothedeceased.Wheretheyoungest beneficiaryturns18(2013:21)yearsofagepriortooronthelastday oftheyearofassessment,thetrustwillnolongerberegardedasa specialtrust.

TAX RATES TRUSTS

TURNOVER TAX MICROBUSINESSESAsfrom1March2009,asimplifiedturnover-basedtaxsystemisapplicable tosmallsoleproprietors,partnershipsandincorporatedbusinesseswithaturnoveroflessthanR1millionperyear.Thissystemiselective.Foryearsofassessmentcommencing1March2012, amicrobusinesscanvoluntarilyexitthesystemattheendofanyyearof assessment.However,onceoutofthesystemthetaxpayerwillnotbe permittedtore-enter.Priortothis,athreeyearlock-inperiodexistedforexitandre-entryintothesystem.Personalservicesrenderedunderemployment-likeconditionsandcertainprofessionalservicesareexcludedfromthissystemtowhichthe followingtaxratesapply:

Turnover Rates of tax R0-R335000 Nil

R335001-R5000001%oftheamountoverR335000

R500001-R750000 R1650+2%oftheamountoverR500000

R750001-R1000000 R6650+3%oftheamountoverR750000

Yearsofassessmentendingbetween1April2015and31March2016

Turnover Rates of tax R0-R150000 Nil

R150001-R3000001%oftheamountoverR150000

R300001-R500000 R1500+2%oftheamountoverR300000

R500001-R750000 R5500+4%oftheamountoverR500000

R750001-R1000000 R15500+6%oftheamountoverR750000

Yearsofassessmentendingbetween1April2014and31March2015

7

Yearsofassessmentendingbetween1April2015and31March2016

Yearsofassessmentendingbetween1April2014and31March2015

These tax rates apply if:• Allshareholdersormembersthroughouttheyearofassessmentare naturalpersonswhodonotholdsharesinanyotherprivatecompanies ormembers’interestinanyotherclosecorporationsorco-operatives otherthanthosewhich: - areinactiveandhaveassetsoflessthanR5000;or - havetakenstepstoliquidate,winduporderegister(effectivefor yearsofassessmentcommencingonorafter1January2011).• GrossincomefortheyearofassessmentdoesnotexceedR20million (2013:R14million)• Notmorethan20%ofthegrossincomeandallthecapitalgains consistscollectivelyof investment incomeandincomefromrendering a personal service. Investment income includesanyannuity,interest,rentalincomefrom immovableproperty,royaltyoranyincomeofasimilarnature,local dividends,foreigndividends(asfrom1April2012)andanyproceeds derivedfrominvestmentortradinginfinancialinstruments(including futures,optionsandotherderivatives),marketablesecuritiesor immovableproperty. Personal serviceincludesanyserviceinthefieldofaccounting, actuarialscience,architecture,auctioneering,auditing,broadcasting, consulting,draughtsmanship,education,engineering,financialservice broking,health,informationtechnology,journalism,law,management, realestatebroking,research,sport,surveying,translation,valuationor veterinaryscience,whichisperformedpersonallybyanypersonwho holdsaninterestinthecompany,co-operativeorclosecorporation, exceptwheresuchsmallbusinesscorporationemploysthreeormore unconnectedfull-timeemployeesforcoreoperationsthroughouttheyear ofassessment• Thecompany,closecorporationorco-operativeisnotanemployment entity.

Investment incentiveThefullcostofanyassetuseddirectlyinaprocessofmanufactureandbroughtintouseforthefirsttimeonorafter1April2001,maybedeductedinthetaxyearinwhichtheassetisbroughtintouse.Asfrom1April2005, allotherdepreciableassetsmaybewrittenoffona50:30:20basis.

Taxable income Rates of taxR0-R73650 NilR73651-R365000 7%oftheamountoverR73650R365001-R550000 R20395+21%oftheamountoverR365000R550001+ R59245+28%oftheamountoverR550000

Taxable income Rates of taxR0-R70700 NilR70701-R365000 7%oftheamountoverR70700R365001-R550000 R20601+21%oftheamountoverR365000R550001+ R59451+28%oftheamountoverR550000

SMALL BUSINESS CORPORATIONS

8

PROVISIONAL TAX

Allprovisionaltaxpayersarerequiredtosubmitand,whereapplicable,makepaymentinrespectoftwoprovisionaltaxreturnsayear.Athirdvoluntaryreturnandpaymentmaybesubmittedtoavoidinterestbeingcharged.

First Year of AssessmentWhereataxpayerhasnotbeenassessedpreviously,areasonableestimateofthetaxableincomemustbemade.Thebasicamountcannotbeestimatedatnil,unlessfullymotivated.

First PaymentOnehalfofthetotaltaxinrespectoftheestimatedtaxableincomeforthe yearispayablewithinsixmonthsofthebeginningoftheyearofassessment.Theestimateoftaxableincomemaynotbelessthanthebasicamountwithout theconsentofSARS.

Second PaymentAtwo-tiersystemappliesdependingonthetaxpayer’staxableincome:• Actual taxable income of R1 million or less Toavoidanypenaltythebasicamountcanbeused.Ifalowerestimateis used,thismustbewithin90%ofthetaxableincomefinallyassessed.• Actual taxable income exceeds R1 million Toavoidanypenaltytheestimatemustbewithin80%ofthetaxable income,excludingretirementfundlumpsums,finallyassessed.Iftheaboverequirementsarenotmet,apenaltyof20%oftheprovisionaltaxunderpaidwillbeimposedunlesssufficientPAYEandprovisionaltaxhasbeenpaidintheyearofassessment.

Third PaymentThirdprovisionalpaymentsareonlyapplicabletoindividualsandtrustswithtaxableincomeinexcessofR50000andcompaniesandclosecorporationswithtaxableincomeinexcessofR20000.Suchpaymentsmustbemadebefore30SeptemberinthecaseofataxpayerwithaFebruaryyearendandwithinsixmonthsofotheryearendstoavoidinterestbeingcharged.

Basic AmountAsfrom1March2015,thebasicamountisthetaxableincomeofthelatestprecedingtaxyear,providedtheassessmentisissued14daysormorepriortothesubmissionoftheprovisionaltaxreturn.Ifthatassessmentisinrespectofayearolderthan18months,thebasicamountisincreasedby8%perannum.

Permissable Reductions in the Basic AmountCapitalgainsandretirementfundlumpsumsarenotincludedinthebasicamount.However,ifanestimatelowerthanthebasicamountisused,capitalgainsmustbeincludedintheestimate. CapitalgainsmustbeincludedinthesecondprovisionaltaxestimateifthetaxableincomeisexpectedtoexceedR1million.

EstimatesSARShastherighttoincreaseanyprovisionaltaxestimate,evenifbasedonthebasicamount,toanamountconsideredreasonable.

ExemptionsAsfrom1March2015,naturalpersons,excludingdirectorsofcompaniesandmembersofclosecorporations,areexemptfromprovisionaltaxifeitheroneofthefollowingisapplicable:• thetaxableincomedoesnotexceedthetaxthreshold• thetaxableincomederivedfrominterest,foreigndividendsandrentalfrom lettingimmovablepropertydoesnotexceedR30000.

9

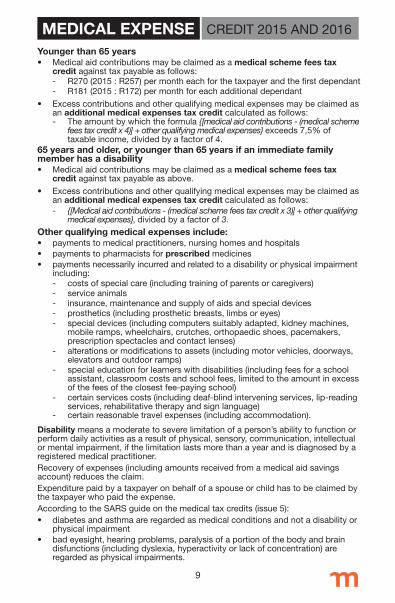

MEDICAL EXPENSE CREDIT2015AND2016

Younger than 65 years• Medicalaidcontributionsmaybeclaimedasamedical scheme fees tax creditagainsttaxpayableasfollows: - R270(2015:R257)permontheachforthetaxpayerandthefirstdependant - R181(2015:R172)permonthforeachadditionaldependant

• Excesscontributionsandotherqualifyingmedicalexpensesmaybeclaimedas an additional medical expenses tax creditcalculatedasfollows: - Theamountbywhichtheformula{[medical aid contributions - (medical scheme fees tax credit x 4)] + other qualifying medical expenses} exceeds7,5%of taxableincome,dividedbyafactorof4.65 years and older, or younger than 65 years if an immediate family member has a disability • Medicalaidcontributionsmaybeclaimedasamedical scheme fees tax creditagainsttaxpayableasabove.

• Excesscontributionsandotherqualifyingmedicalexpensesmaybeclaimedas an additional medical expenses tax creditcalculatedasfollows: - {[Medical aid contributions - (medical scheme fees tax credit x 3)] + other qualifying medical expenses}, dividedbyafactorof3.

Other qualifying medical expenses include:• paymentstomedicalpractitioners,nursinghomesandhospitals• paymentstopharmacistsforprescribedmedicines• paymentsnecessarilyincurredandrelatedtoadisabilityorphysicalimpairment including: - costsofspecialcare(includingtrainingofparentsorcaregivers) - serviceanimals - insurance,maintenanceandsupplyofaidsandspecialdevices - prosthetics(includingprostheticbreasts,limbsoreyes) - specialdevices(includingcomputerssuitablyadapted,kidneymachines, mobileramps,wheelchairs,crutches,orthopaedicshoes,pacemakers, prescriptionspectaclesandcontactlenses) - alterationsormodificationstoassets(includingmotorvehicles,doorways, elevatorsandoutdoorramps) - specialeducationforlearnerswithdisabilities(includingfeesforaschool assistant,classroomcostsandschoolfees,limitedtotheamountinexcess ofthefeesoftheclosestfee-payingschool) - certainservicescosts(includingdeaf-blindinterveningservices,lip-reading services,rehabilitativetherapyandsignlanguage) - certainreasonabletravelexpenses(includingaccommodation).

Disabilitymeansamoderatetoseverelimitationofaperson’sabilitytofunctionorperformdailyactivitiesasaresultofphysical,sensory,communication,intellectualormentalimpairment,ifthelimitationlastsmorethanayearandisdiagnosedbyaregisteredmedicalpractitioner.Recoveryofexpenses(includingamountsreceivedfromamedicalaidsavings account)reducestheclaim.Expenditurepaidbyataxpayeronbehalfofaspouseorchildhastobeclaimedby thetaxpayerwhopaidtheexpense.AccordingtotheSARSguideonthemedicaltaxcredits(issue5):• diabetesandasthmaareregardedasmedicalconditionsandnotadisabilityor physicalimpairment• badeyesight,hearingproblems,paralysisofaportionofthebodyandbrain disfunctions(includingdyslexia,hyperactivityorlackofconcentration)are regardedasphysicalimpairments.

10

Foryearsofassessmentcommencingonorafter1March2009:• A labour brokerisanaturalpersonwho,forreward,providesa clientwithotherpersonstorenderaservicefortheclientor procuresotherpersonsfortheclientandremuneratessuch persons• A personal service provider isacompany,closecorporationor trustwhereanyservicerenderedonbehalfoftheentitytoitsclient isrenderedpersonallybyanypersonwhoisaconnectedpersonin relationtosuchentity,andoneofthefollowingprovisionsapply: - thepersonwouldhavebeenregardedasanemployeeofthe client,iftheservicewasnotrenderedthroughanentity - thepersonorentityrenderingtheservicemustperformsuch servicemainlyatthepremisesoftheclientandsuchpersonor entityissubjecttothecontrolorsupervisionofsuchclientasto themannerinwhichthedutiesareperformed

- morethan80%oftheincomederivedfromservicesrenderedis receivedfromoneclientorassociatedpersoninrelationtothe client• Theentitywillnotberegardedasapersonal service provider wheresuchentityemploysthreeormoreunconnectedfull-time employeesforcoreoperationsthroughouttheyearofassessment.

Implications• Alabourbroker,notinpossessionofanexemptioncertificate,is subjecttoPAYEonincomereceivedattheratesapplicableto individualtaxpayers.Deductibleexpenditureislimitedto remunerationpaidtoemployees• ApersonalserviceproviderissubjecttoPAYEattherateof 28%(2012:33%)inthecaseofacompanyand40%inthecase of a trust• NoPAYEisrequiredtobedeductedwheretheentityprovides anaffidavitconfirmingthatitdoesnotreceivemorethan80%ofits incomefromonesource• ThedeemedemployeemayapplytoSARSforataxdirectivefora lowerrateoftaxtobeapplied• Deductionsavailabletopersonalserviceprovidersarelimitedto remunerationtoemployees,contributionstopension,providentand benefitfunds,legalexpenses,baddebts,expensesinrespectof premises,financecharges,insurance,repairs,fuelandmaintenance inrespectofassetsusedwhollyandexclusivelyfortradeandany amountpreviouslyincludedintaxableincomeandsubsequently refundedbytherecipient.

Labour brokers andpersonalserviceprovidersareregardedasdeemedemployees.

DEEMED EMPLOYEES

11

Employeesorholdersofofficearelimitedtothefollowingdeductionsfromtheirremuneration:• Baddebtsallowance• Doubtfuldebtsallowance• Wearandtearallowance• Pensionorretirementannuityfundcontributions• DonationstoqualifyingPBO’s• Homeofficeexpenses,subjecttocertainrequirements• Legalexpenses• Priorto1March2015,premiumspaidintermsofanallowableinsurance policy - totheextentthatthepolicycoversthepersonagainstlossof incomeasaresultofillness,injury,disabilityorunemployment,and - inrespectofwhichallamountspayableintermsofthepolicy constituteincomeasdefined• Asfrom1March2008,refundedawardsforservicesrenderedand refundedrestraintoftradeawards.

• DividendsreceivedoraccruedfromSouthAfricancompaniesorJSEdual listednon-residentcompaniesaregenerallynotsubjecttoincometax.• Asfrom1March2014,dividendsreceivedforservicesrenderedorby virtueofemploymentincludingashareincentivetrustdistributionsareno longerexempt.• Interestreceivedbyoraccruedtoanon-residentisexemptfromincome taxunlesstheindividualwasphysicallypresentinSouthAfricafora periodexceeding183daysinaggregateorcarriedonbusinessthrougha permanentestablishmentinSouthAfricaatanytimeduringthe12month periodpriortodateofreceiptoraccrual.Asfrom1March2015,where thisexemptionisapplicable,afinalwithholdingtaxof15%willbe imposedoninterestpaidtoanon-residentsubjecttoareductioninthe rateintermsofadoubletaxationagreement.• SouthAfricansourcedinterestreceivedbynaturalpersons: Personsunder65years R23800 (2013:R22800) Persons65yearsandolder R34500 (2013:R33000) Interestincludespropertyunittrustdistributionsandforeigninterest.• Asfrom1March2012,theforeigninterestanddividendexemption (2012:R3700)fellaway.Theforeigndividendexemptionisreplaced byaformulawherebythemaximumeffectiverateoftaxationis15%.• Unemploymentinsurancebenefits.• RoadAccidentFundpayoutsasfrom1March2012.Termination Lump Sum from EmployerAsfrom1March2011,employerprovidedseverancepaymentsforreasons ofage,illhealthandretrenchmentarealignedwiththetaxationoflumpsumbenefits,includingtheR500000(2012:R315000)taxfreelimit.Inthecaseofretrenchmentthisconcessiondoesnotapplywherethatpersonatanytimeheldaninterestofmorethan5%inthatentity.CompensationAsfrom1March2007,compensationawardspaidbyanemployeronthedeathofanemployeeinthecourseofemploymentareexempttotheextentofR300000.Asfrom1March2011,previousretrenchmentexemptionsarenolongerset-offagainstthisamount.

DEDUCTIONS EMPLOYEES

EXEMPTIONS INDIVIDUALS

12

Use of Company Provided Motor VehicleAsfrom1March2015,forvehiclesacquiredorfinanced,thedeterminedvalueforthefringebenefitistheretailmarketvalue(previouslycost)includingVATbutexcludingfinancechargesandinterest.Theemployeewillbetaxedon3,5%(2011:2,5%)permonthofthedeterminedvalueofthemotorvehiclelessanyconsiderationpaidbytheemployeetowardsthecostofthevehicle.Thefringebenefitisreducedto3,25%ifthevehicleissubjecttoamaintenanceplanfornotlessthanthreeyearsand/or60000kilometres.Asfrom1March2013,forvehiclesacquiredunderanoperatinglease,thevalueofthefringebenefitisbasedontherentalandfuelcosttotheemployer.Whereanemployeeisgiventheuseofmorethanonevehicleandcanprovethateachvehicleisusedprimarilyforbusinesspurposes,thevalueplacedontheprivateuseofallthevehiclesisdeterminedaccordingtothevalue attributedtothevehiclecarryingthehighestvalueforprivateuse.ForPAYEpurposestheemployerisrequiredtoincludeintheemployee’smonthlyremuneration80%ofthetaxablebenefit.Theinclusionratemaybe limitedto20%iftheemployerissatisfiedthatatleast80%oftheuseofthevehicleforayearofassessmentwillbeforbusinesspurposes.OnassessmentSARSisobliged,provideditissatisfiedthataccuraterecordshavebeenkeptinrespectofdistancestravelledfor:• businesspurposes,toreducethevalueofthefringebenefitbythesame proportionthatthebusinessdistancebearstothetotaldistancetravelled duringtheyearofassessment• privatepurposesandtheemployeehasbornethefullcostofthespecified vehiclerunningexpenses,toreducethevalueofthefringebenefit: - bythesameproportionthattheprivatedistancebearstothetotal distancetravelledduringtheyearofassessment,inthecaseof licence,insuranceandmaintenancecosts - byapplyingtheprescribedrateperkilometretothekilometrestravelled forprivatepurposesinthecaseofthefuelcostpertainingtoprivateuse.Novalueisplacedontheprivateuseofacompanyownedvehicleif:• itisavailabletoandusedbyallemployees,privateuseisinfrequentand incidentaltothebusinessuseandthevehicleisnotnormallykeptator nearthatemployee’sresidencewhennotinuseoutsidebusinesshours• thenatureoftheemployee’sdutiesrequiresregularuseofthevehiclefor theperformanceofdutiesoutsidenormalhoursofworkandprivateuse isinfrequentorincidentaltobusinessuseorlimitedtotravelbetween placeofresidenceandplaceofwork.Theprovisionofacompanyownedvehicleconstitutesadeemedsupplyfor VATpurposes.ThevendormustaccountforoutputVATonthedeemed considerationbyapplyingtheVATfraction(14/114)onamonthlybasis.Thedeemedconsiderationisdeterminedasfollows:Motorvehicle/Doublecab 0,3%ofcostofvehicle(excl.VAT)permonthBakkies 0,6%ofcostofvehicle(excl.VAT)permonth

Use of Business Cellphones and ComputersAsfrom1March2008,notaxablevalueisplacedontheprivateuseby employeesofemployer-ownedcellphonesandcomputerswhichareusedmainlyforbusinesspurposes.

Low Interest/Interest-Free Loans• Thefringebenefitisthedifferencebetweentheinterestratechargedby theemployerandtheofficialinterestrateappliedtotheloanamount• NofringebenefitariseswheretheloanislessthanR3000orwherealoan ismadetoanemployeetofurtherhisownstudies.

FRINGE BENEFITS

13

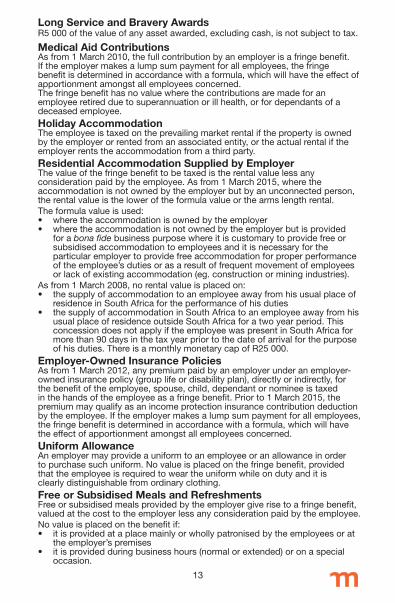

Long Service and Bravery AwardsR5000ofthevalueofanyassetawarded,excludingcash,isnotsubjecttotax.

Medical Aid ContributionsAsfrom1March2010,thefullcontributionbyanemployerisafringebenefit.Iftheemployermakesalumpsumpaymentforallemployees,thefringe benefitisdeterminedinaccordancewithaformula,whichwillhavetheeffectofapportionmentamongstallemployeesconcerned.Thefringebenefithasnovaluewherethecontributionsaremadeforan employeeretiredduetosuperannuationorillhealth,orfordependantsofa deceasedemployee.Holiday AccommodationTheemployeeistaxedontheprevailingmarketrentalifthepropertyisownedbytheemployerorrentedfromanassociatedentity,ortheactualrentaliftheemployerrentstheaccommodationfromathirdparty.Residential Accommodation Supplied by EmployerThevalueofthefringebenefittobetaxedistherentalvaluelessany considerationpaidbytheemployee.Asfrom1March2015,wherethe accommodationisnotownedbytheemployerbutbyanunconnectedperson,therentalvalueistheloweroftheformulavalueorthearmslengthrental.Theformulavalueisused:• wheretheaccommodationisownedbytheemployer• wheretheaccommodationisnotownedbytheemployerbutisprovided for a bona fidebusinesspurposewhereitiscustomarytoprovidefreeor subsidisedaccommodationtoemployeesanditisnecessaryforthe particularemployertoprovidefreeaccommodationforproperperformance oftheemployee’sdutiesorasaresultoffrequentmovementofemployees orlackofexistingaccommodation(eg.constructionorminingindustries).Asfrom1March2008,norentalvalueisplacedon:• thesupplyofaccommodationtoanemployeeawayfromhisusualplaceof residenceinSouthAfricafortheperformanceofhisduties• thesupplyofaccommodationinSouthAfricatoanemployeeawayfromhis usualplaceofresidenceoutsideSouthAfricaforatwoyearperiod.This concessiondoesnotapplyiftheemployeewaspresentinSouthAfricafor morethan90daysinthetaxyearpriortothedateofarrivalforthepurpose ofhisduties.ThereisamonthlymonetarycapofR25000.Employer-Owned Insurance PoliciesAsfrom1March2012,anypremiumpaidbyanemployerunderanemployer-ownedinsurancepolicy(grouplifeordisabilityplan),directlyorindirectly,for thebenefitoftheemployee,spouse,child,dependantornomineeistaxedinthehandsoftheemployeeasafringebenefit.Priorto1March2015,thepremiummayqualifyasanincomeprotectioninsurancecontributiondeductionbytheemployee.Iftheemployermakesalumpsumpaymentforallemployees,thefringebenefitisdeterminedinaccordancewithaformula,whichwillhavetheeffectofapportionmentamongstallemployeesconcerned.Uniform AllowanceAnemployermayprovideauniformtoanemployeeoranallowanceinorder topurchasesuchuniform.Novalueisplacedonthefringebenefit,provided thattheemployeeisrequiredtoweartheuniformwhileondutyanditis clearlydistinguishablefromordinaryclothing.Free or Subsidised Meals and RefreshmentsFreeorsubsidisedmealsprovidedbytheemployergiverisetoafringebenefit,valuedatthecosttotheemployerlessanyconsiderationpaidbytheemployee.Novalueisplacedonthebenefitif:• itisprovidedataplacemainlyorwhollypatronisedbytheemployeesorat theemployer’spremises• itisprovidedduringbusinesshours(normalorextended)oronaspecial occasion.

14

TRAVEL ALLOWANCESFixed Travel AllowancesAsfrom1March2010,80%ofthefixedtravelallowanceissubjecttoPAYE.Asfrom1March2011,wheretheemployerissatisfiedthatatleast80%oftheuseofthevehiclefortheyearofassessmentwillbeforbusinesspurposes,theinclusionratemaybelimitedto20%.Thefullallowanceisdisclosedontheemployee’sIRP5certificate,irrespectiveofthepercentageofbusinesstravel.Reimbursive Travel ExpensesWhereanemployeereceivesareimbursementbasedontheactualbusinesskilometrestravelled,noothercompensationispaidtotheemployeeandthecostiscalculatedinaccordancewiththeprescribedrateof318cents (2015:330cents)perkilometre,noPAYEisdeductible,providedthebusinesstraveldoesnotexceed8000kilometresperyear. Thereimbursementmustbedisclosedundercode3703ontheIRP5certificate.NoPAYEiswithheldandtheamountisnotsubjecttotaxationonassessment.Ifthebusinesskilometrestravelledexceed8000kilometresperyear,orifthereimbursiverateperkilometreexceedstheprescribedrate,orifother compensationispaidtotheemployeetheallowancemustbedisclosed separatelyundercode3702ontheIRP5certificate.Asfrom1March2013, PAYEiswithheldonapaymentbasis.

Low Cost Housing Transferred to EmployeeAsfrom1March2014,novalueisplacedonimmovablepropertytransferredtoanemployeewhereallthefollowingareapplicable:• themarketvalueofthepropertydoesnotexceedR450000• theemployee’sremunerationdoesnotexceedR250000• theemployeeisnotaconnectedpersoninrelationtotheemployer.

SUBSISTENCE ALLOWANCES

IfanemployeeisobligedtospendatleastonenightawayfromhisusualresidenceinSouthAfricaonbusiness,theemployermaypayanallowanceforpersonalsubsistenceandincidentalcostswithoutsuchamountsbeingincludedintheemployee’staxableincome,subjecttotheemployeetravellingforbusinessbynolaterthantheendofthefollowingmonth.Ifsuchallowanceispaidtoanemployeeandthatemployeedoesnottravelforbusinesspurposesbytheendofthefollowingmonth,theallowancebecomessubject toPAYEinthatmonth.Iftheallowancesdonotexceedtheamountsorperiodsdetailedbelow,thetotalallowancemustbereflectedundercode3714ontheIRP5certificate.Wheretheallowancesexceedtheamountsorperiodsdetailedbelow,thetotalallowancemustbereflectedundercode3704(local)or3715(foreign).Thefollowingamountsaredeemedtohavebeenincurredbyanemployeeinrespectofasubsistenceallowance:Local travel• R109(2015:R103)perdayorpartofadayforincidentalcosts• R353(2015:R335)perdayorpartofadayformealsandincidentalcosts.Whereanallowanceispaidtoanemployeetocoveraccommodation,mealsandincidentalcosts,theemployeehastoprovetheexpenseincurredwhileawayonbusiness,whichislimitedtotheallowancereceived.Overseas travelActualaccommodationexpensesplusanallowancepercountryassetouton www.sars.gov.za(2009:$215)perdayformealsandincidentalcostsincurredoutsideSouthAfrica.Thedeemedexpenditureisnotapplicablewherethe absenceisforacontinuousperiodinexcessofsixweeks.

15

Accuraterecordsoftheopeningandclosingodometerreadingsmustbemaintainedinallcircumstances.Asfrom1March2010,theclaimmustbebasedontheactualdistance travelledforbusinesspurposesassupportedbyalogbook.Thedeductioninrespectofbusinesstravelislimitedtotheallowancegrantedandmaybedeterminedusingactualexpenditureincurredoronadeemedcostperkilometrebasisinaccordancewiththetablebelow.ThecostofthevehicleincludesVATbutexcludesfinancecosts.WhereactualexpenditureisusedthevalueofthevehicleislimitedtoR560000 (2014:R480000)forpurposesofcalculatingwearandtear,whichmustbespreadoveraseven year period. ThefinancecostsarealsolimitedtoadebtofR560000(2014:R480000).Inthecaseofaleasedvehicle,theinstalmentsinanyyearofassessmentmaynotexceedthefixedcostcomponentinthetable.

DEDUCTIONS TRAVELEXPENSES

DEEMEDEXPENDITURE-2016

DoesnotexceedR80000 26105 78,7 29,3ExceedsR80001butnotR160000 46505 87,9 36,7ExceedsR160001butnotR240000 66976 95,5 40,4ExceedsR240001butnotR320000 84945 102,7 44,1ExceedsR320001butnotR400000 102974 109,9 51,8ExceedsR400001butnotR480000 121886 126,1 60,8ExceedsR480001butnotR560000 140797 130,4 75,6ExceedsR560000 140797 130,4 75,6

Fixed Fuel RepairsR cc

Cost of vehicle

DoesnotexceedR80000 25946 92,3 27,6ExceedsR80001butnotR160000 46203 103,1 34,6ExceedsR160001butnotR240000 66530 112,0 38,1ExceedsR240001butnotR320000 84351 120,5 41,6ExceedsR320001butnotR400000 102233 128,9 48,8ExceedsR400001butnotR480000 120997 147,9 57,3ExceedsR480001butnotR560000 139760 152,9 71,3ExceedsR560000 139760 152,9 71,3

DEEMEDEXPENDITURE-2015Fixed Fuel Repairs

R cc Cost of vehicle

VARIABLE REMUNERATIONAsfrom1March2013,variableremuneration,suchascommission,bonuses,overtime,leavepayandreimbursivetravel,istaxedonapaymentbasis.This isapplicableinrespectofthedeductionofPAYE,theemployee’sgrossincomeinclusionandtheemployer’sincometaxdeduction.

16

Current Pension Fund ContributionsLimitedto7,5%ofremunerationfromretirement-fundingemploymentor R1750,whicheveristhegreater.Remunerationfromretirement-funding employmentreferstoincomewhichistakenintoaccounttodetermine contributionstoapensionorprovidentfund.Excesscontributionsarenotcarriedforwardtothenextyearofassessmentbutareaccumulatedforthepurposeofdeterminingthetax-freeportionofthelumpsumuponretirement.Arrear Pension Fund ContributionsUptoamaximumofR1800peryear.Anyexcessmaybecarriedforward.Current Retirement Annuity Fund ContributionsLimitedto15%oftaxableincomefromnon-retirement-fundingemployment,excludinganyretirementfundlumpsumbenefits,orR3500lesscurrent contributionstoapensionfund,orR1750,whicheveristhegreater.Any excessmaybecarriedforward.Reinstated Retirement Annuity Fund ContributionsUptoamaximumofR1800peryear.Anyexcessmaybecarriedforward.Income Protection ContributionsPriorto1March2015,insurancepremiumspaidonincomeprotectionpoliciestotheextentthatsuchamountsreceivedunderthepolicyconstituteincome.Alignment of Retirement Fund ContributionsAsfrom1March2016,thetaxtreatmentofpension,retirementannuityandprovidentfundswillbechangedsothatcontributionsmadebytheemployerwillbeafringebenefit.Thischangemaybedelayedto1March2017.Thetotalcontributionsdeductiblebyanemployeewillbelimitedto27,5%of thegreaterofremunerationortaxableincome(excludinglumpsumsreceived),butcappedatanannuallimitofR350000.Excesscontributionswillbecarriedforwardtothenextyearofassessment.Allfundtofundtransfershavenotaxconsequences.Pension,retirementannuityandprovidentfundswillallbesubjecttotheone-thirdlumpsumandtwo-thirdsannuityrules,unlessthelumpsumisbelowR150000orthememberisatleast55yearsoldon1March2016.Lumpsumsfromprovidentfundswillbeapportionedtoensurecontributionsmadepriortothischangeandtheresultantgrowthmaybepaidoutasalumpsumnotsubjecttothenewannuitisationrules.Nolimitwillbeplacedonthedeductiontheemployermayclaim(previouslylimitedto20%oftheemployee’sremuneration)forcontributionsmadetothesefundsontheemployee’sbehalf.

DEDUCTIONS RETIREMENT

Thefollowingexpensesincurredbytheemployerforrelocation,appointmentorterminationofanemployeeareexemptfromtax:• transportationoftheemployee,membersofhishouseholdandpersonal possessions• hiringtemporaryresidentialaccommodationfortheemployeeand membersofhishouseholdforupto183daysaftertransfer• otherrelatedcosts,includingnewschooluniforms,replacementof curtains,bondregistrationandcancellationfees,legalfees,transfer duty,motorvehicleregistrationfeesandestateagentscommissionon saleofpreviousresidence.Expenseswhichdonotqualifyincludethelossonsaleoftheprevious residenceandarchitect’sfeesfordesignoforalterationstoanewresidence.

RELOCATION OF ANEMPLOYEE

17

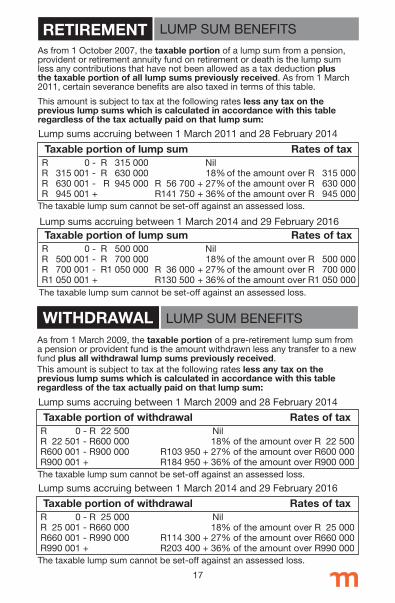

RETIREMENT LUMPSUMBENEFITS

Asfrom1October2007,thetaxable portionofalumpsumfromapension,providentorretirementannuityfundonretirementordeathisthelumpsumlessanycontributionsthathavenotbeenallowedasataxdeductionplus the taxable portion of all lump sums previously received.Asfrom1March2011,certainseverancebenefitsarealsotaxedintermsofthistable.

Thisamountissubjecttotaxatthefollowingratesless any tax on the previous lump sums which is calculated in accordance with this table regardless of the tax actually paid on that lump sum:

Taxable portion of lump sum Rates of tax R0- R315000 NilR315001-R630000 18%oftheamountoverR315000R630001- R945000 R56700+27%oftheamountoverR630000R945001+ R141750+36%oftheamountoverR945000

Taxable portion of lump sum Rates of tax R0- R500000 NilR500001-R700000 18%oftheamountoverR500000R700001-R1050000 R36000+27%oftheamountoverR700000R1050001+ R130500+36%oftheamountoverR1050000

Thetaxablelumpsumcannotbeset-offagainstanassessedloss.

Lumpsumsaccruingbetween1March2011and28February2014

Thetaxablelumpsumcannotbeset-offagainstanassessedloss.

Lumpsumsaccruingbetween1March2014and29February2016

WITHDRAWAL LUMPSUMBENEFITS

Asfrom1March2009,thetaxable portionofapre-retirementlumpsumfromapensionorprovidentfundistheamountwithdrawnlessanytransfertoanewfund plus all withdrawal lump sums previously received.Thisamountissubjecttotaxatthefollowingratesless any tax on the previous lump sums which is calculated in accordance with this table regardless of the tax actually paid on that lump sum:

Thetaxablelumpsumcannotbeset-offagainstanassessedloss.

Taxable portion of withdrawal Rates of tax R0-R22500 NilR22501-R600000 18%oftheamountoverR22500R600001-R900000R103950+27%oftheamountoverR600000R900001+ R184950+36%oftheamountoverR900000

Lumpsumsaccruingbetween1March2009and28February2014

Thetaxablelumpsumcannotbeset-offagainstanassessedloss.

Taxable portion of withdrawal Rates of tax R0-R25000 NilR25001-R660000 18%oftheamountoverR25000R660001-R990000R114300+27%oftheamountoverR660000R990001+ R203400+36%oftheamountoverR990000

Lumpsumsaccruingbetween1March2014and29February2016

18

YOUTH EMPLOYMENTINCENTIVEAsfrom1January2014,aspecialincentiveisallowedasacreditagainsttheemployer’smonthlyPAYEpaymenttoencouragetheemploymentofworkers.Toqualifyfortheincentive:• Employers must - beregisteredforPAYE - notbegovernmentoramunicipalentity - nothavebeendisqualifiedbytheMinisterofFinance - betaxcompliant• Employees must - haveavalidSouthAfricanbar-codedIDorasylumseekerpermit - bebetweentheagesof18and30 - notbeadomesticworker - notberelatedorconnectedtotheemployer - earnatleastR2000permonthortheminimumamountstipulatedbythe regulatedindustry - earnremunerationoflessthanR6000permonth - benewlyemployedonorafter1October2013Thecreditisdeterminedforeachqualifyingemployeeasfollows: Monthly Per month during the first Per month during the next Remuneration 12 months of employment 12 months of employment

R 0-R2000 50%ofmonthlyremuneration 25%ofmonthlyremuneration R2001-R4000 R1000 R500 R4001-R6000 R1000-(0,5x(Monthly R500-(0,25x(Monthly Remuneration-R4000)) Remuneration-R4000))

Asfrom1March2015,whereanemployeeisemployedonafulltimebasis inexcessof160hourspermonth,anemployerisentitledtoclaimthefullincentiveassetoutabove.Wheretheemployeeworkslessthanthisinthemonth,theincentivehastobeapportioned.WherethecreditexceedsthePAYEliabililtyoftheemployer,theexcessamountisrefundableprovidedtheemployeristaxcompliant.Thisincentiveceasestoapplyfrom1January2017.

EmployercompaniesmayissuequalifyingsharesuptoacumulativelimitofR50000(2008:R9000)peremployeeinrespectofthecurrenttaxyearandtheimmediatelyprecedingfour(2008:two)taxyears.AtaxdeductionlimitedtoamaximumofR10000(2008:R3000)peryearperemployeewillbeallowedintheemployer’shands.Therearenotaxconsequencesfortheemployee,otherthanCGT,providedtheemployeedoesnotsellthesharesforatleastfiveyears.

BROAD-BASED EMPLOYEEEQUITY

BURSARIES ANDSCHOLARSHIPSBona fidescholarshipsorbursariesgrantedtoenableanypersontostudy atarecognisededucationalinstitutionareexemptfromtax.Wherethebenefitisgrantedtoanemployee,theexemptionwillnotapplyunlesstheemployeeagreestoreimbursetheemployerintheeventthatthestudiesarenot completed.Wherethebeneficiaryisarelativeoftheemployee,theexemptionwillonlyapplyiftheannualremunerationoftheemployeeislessthanR250000(2013:R100000)andtotheextentthatthebursarydoesnotexceedR30000(2013:R10000)inrespectofhighereducationandR10000(2013:R10000)forbasiceducationtograde12.

19

TAX FREE SAVINGSACCOUNTSAsfrom1March2015,naturalpersonscaninvestuptoR30000annually,withalifetimelimitofR500000,inapprovedsavinginstrumentssuchasunittrusts,fixeddepositsorREITS.Allreturns,includinginterest,dividendsandcapitalgainsonthedisposaloftheseinvestments,aretaxfree.Apenaltyof40%oftheexcesscapitalcontributedisapplicablewheretheannualorlifetimelimitsareexceeded.

LIMITATION OFINTERESTDEDUCTIONDebt arising as a result of a Corporate RestructureAsfrom1April2014,theinterestdeductioninrespectofcertaincorporaterestructuresislimited,calculatedinaccordancewithaformula.Anyexcessinterestcannotbecarriedforwardtothenexttaxyear.Asaresultanyexcessinterestispermanentlylost.Theinterestdeductionlimitationmustbeappliedinthetaxyearinwhichtherestructuretransactionisenteredintoandthefivetaxyearsimmediatelythereafter.Recipient of interest is not subject to tax in South AfricaAsfrom1January2015,alimitationisplacedontheinterestdeduction availablewhereinterestispaidtoanexemptorforeignpersonwhoisnotsubjecttotaxinSouthAfrica.ThiswillgenerallyapplyinthecaseofinterestpaidtoaPBOoraforeign personwherethewithholdingtaxoninterestisreducedtonilintermsofadoubletaxationagreement.Thislimitationisonlyapplicablewhenthepartiesinvolvedareinacontrollingrelationship,wherebyapersondirectlyorindirectlyholdsmorethan50%oftheequitysharesorvotingrights.Theinterestdeductioniscalculatedinaccordancewiththeformulaandanyexcessinterestiscarriedforwardtothenexttaxyear.

ARBITRATION AWARDSArbitrationawardsaregenerallyawardedduetounfairdismissal,terminationoftheemploymentcontractpriortotheexpirydateorunfairlabourpractices.Amountspaidduetounfairdismissalandearlyterminationofthecontractconstituteremunerationandaretaxable.

Taxreliefexistsforcertaincorporatetransactions,including:• Assetforsharetransactions,includingshareforsharetransactions• Amalgamationandunbundlingtransactions• Intra-grouptransactions• Liquidation,windinguporderegistrationtransactionswithinagroup.Thisreliefalsoappliestotransactionsinvolvingspecificcontrolledforeigncompanies.

CORPORATE TRANSACTIONS

Taxpayersmarriedincommunityofpropertyaretaxedonhalfoftheirowninterest,dividend,rentalincomeandcapitalgainandhalfoftheirspouses’interest,dividend,rentalincomeandcapitalgain,regardlessofthespouseinwhosenametheassetsareregistered(otherthanassetsexcludedfromthejointestate).Allothertaxableincomeistaxedonlyinthehandsofthespousewhoreceivesthatincome.

MARRIED INCOMMUNITYOFPROPERTY

20

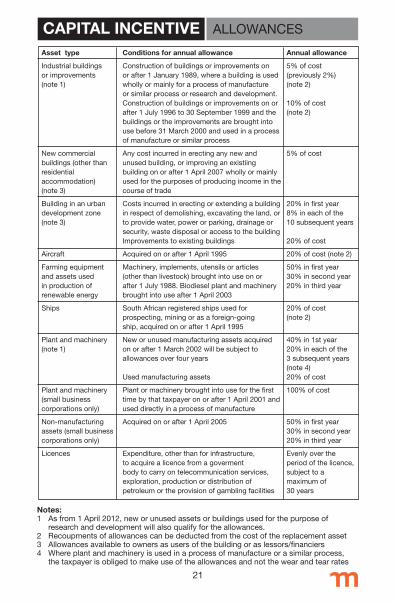

Asset type Conditions for annual allowance Annual allowance

Residential Buildingserectedonorafter1April1982and 2%ofcostandan buildings before21October2008consistingofatleast initialallowanceof fiveunitsofmorethanoneroomintendedfor 10%ofcost letting,oroccupationbybona fidefull-time employees

Newandunusedbuildingsacquired,erectedor 5%ofcostor10% improvedonorafter21October2008ifsituated ofcostforlowcost anywhereinSouthAfricaandownedbythetax- residentialunitsnot payerforuseinhistrade,eitherforlettingoras exceedingR300000 employeeaccommodation.Enhancedallowances forastand-aloneunit areavailablewherethelowcostresidentialunit orR350000inthe issituatedinanurbandevelopmentzone caseofanapartment

Employee 50%ofthecostsincurredorfundsadvancedor R6000priorto housing donatedtofinancetheconstructionofhousing 1March2008 foremployeesonorbefore21October2008 R15000between subjecttoamaximumperdwelling 1March2008and 20October2008

Employee Allowanceonamountsowingoninterestfree 10%ofamount housing loanaccountinrespectoflowcostresidential owingattheend loans unitssoldatcostbythetaxpayertoemployees ofeachyearof andsubjecttorepurchaseatcostonlyincaseof assessment repaymentdefaultorterminationofemployment

HOTEL ALLOWANCES

Hotelbuildings Constructionofbuildingsorimprovements, 5%ofcost providedusedintradeashotelkeeperorused by lessee in trade as hotelkeeper Refurbishments(note)whichcommenced 20%ofcost onorafter17March1993

Hotelequipment Machinery,implements,utensilsorarticles 20%ofcost broughtintouseonorafter16December1989

RESIDENTIAL BUILDING ALLOWANCES

Asset type Conditions for annual allowance Annual allowance

Note:• Refurbishmentisdefinedasanyworkundertakenwithintheexistingbuildingframework

ENVIRONMENTAL EXPENDITUREExpenditureincurredtoconserveormaintainlandisdeductibleifitiscarriedoutintermsofabiodiversitymanagementagreementwithadurationofatleastfiveyears.Wheretheconservationormaintenanceoflandownedbythetaxpayeriscarriedoutintermsofadeclarationofatleast30years’duration,theexpenditureincurredisdeemedtobeadonationtotheGovernmentwhichqualifiesasadeductionundersection18A.Incertaincircumstanceswherethelandisdeclaredanationalparkanannualdonationbasedon10%ofthelesserofcostormarketvalueofthelandisdeemedtobemadeandqualifiesforasection18Adeductionintheyearthedeclarationismadeandineachofthesubsequentnineyears.Recoupmentsarisewherethetaxpayerbreachestheagreement.

Notes:1 Asfrom1April2012,neworunusedassetsorbuildingsusedforthepurposeof researchanddevelopmentwillalsoqualifyfortheallowances.2 Recoupmentsofallowancescanbedeductedfromthecostofthereplacementasset3 Allowancesavailabletoownersasusersofthebuildingoraslessors/financiers4 Whereplantandmachineryisusedinaprocessofmanufactureorasimilarprocess, thetaxpayerisobligedtomakeuseoftheallowancesandnotthewearandtearrates

CAPITAL INCENTIVE ALLOWANCES

21

Asset type Conditions for annual allowance Annual allowance

Industrialbuildings Constructionofbuildingsorimprovementson 5%ofcost orimprovements orafter1January1989,whereabuildingisused (previously2%) (note1) whollyormainlyforaprocessofmanufacture (note2) orsimilarprocessorresearchanddevelopment. Constructionofbuildingsorimprovementsonor 10%ofcost after1July1996to30September1999andthe (note2) buildingsortheimprovementsarebroughtinto usebefore31March2000andusedinaprocess ofmanufactureorsimilarprocess

Newcommercial Anycostincurredinerectinganynewand 5%ofcost buildings(otherthan unusedbuilding,orimprovinganexistiing residential buildingonorafter1April2007whollyormainly accommodation) usedforthepurposesofproducingincomeinthe (note3) courseoftrade

Buildinginanurban Costsincurredinerectingorextendingabuilding 20%infirstyear developmentzone inrespectofdemolishing,excavatingtheland,or 8%ineachofthe (note3) toprovidewater,powerorparking,drainageor 10subsequentyears security,wastedisposaloraccesstothebuilding Improvementstoexistingbuildings 20%ofcost

Aircraft Acquiredonorafter1April1995 20%ofcost(note2)

Farmingequipment Machinery,implements,utensilsorarticles 50%infirstyear andassetsused (otherthanlivestock)broughtintouseonor 30%insecondyear inproductionof after1July1988.Biodieselplantandmachinery 20%inthirdyear renewableenergy broughtintouseafter1April2003

Ships SouthAfricanregisteredshipsusedfor 20%ofcost prospecting,miningorasaforeign-going (note2) ship,acquiredonorafter1April1995

Plantandmachinery Neworunusedmanufacturingassetsacquired 40%in1styear (note1) onorafter1March2002willbesubjectto 20%ineachofthe allowancesoverfouryears 3subsequentyears (note 4) Usedmanufacturingassets 20%ofcost

Plantandmachinery Plantormachinerybroughtintouseforthefirst 100%ofcost (smallbusiness timebythattaxpayeronorafter1April2001and corporationsonly) useddirectlyinaprocessofmanufacture

Non-manufacturing Acquiredonorafter1April2005 50%infirstyear assets(smallbusiness 30%insecondyear corporationsonly) 20%inthirdyear

Licences Expenditure,otherthanforinfrastructure, Evenlyoverthe toacquirealicencefromagoverment periodofthelicence, bodytocarryontelecommunicationservices, subjecttoa exploration,productionordistributionof maximumof petroleumortheprovisionofgamblingfacilities 30years

22

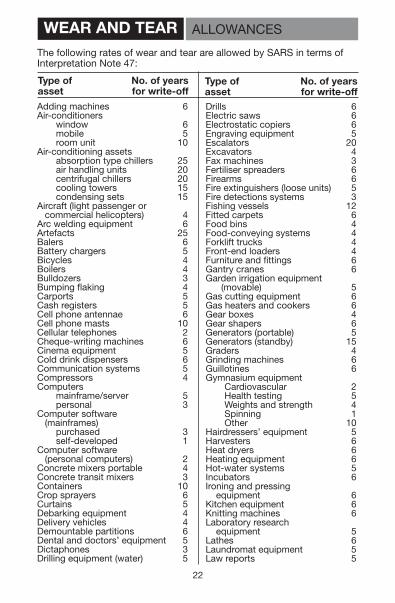

ThefollowingratesofwearandtearareallowedbySARSintermsofInterpretationNote47:

Type of No. of yearsasset for write-off

Type of No. of years asset for write-off

Addingmachines 6Air-conditioners window 6 mobile 5 roomunit 10Air-conditioningassets absorptiontypechillers 25 airhandlingunits 20 centrifugalchillers 20 coolingtowers 15 condensingsets 15Aircraft(lightpassengerorcommercialhelicopters) 4Arcweldingequipment 6Artefacts 25Balers 6Batterychargers 5Bicycles 4Boilers 4Bulldozers 3Bumpingflaking 4Carports 5Cashregisters 5Cellphoneantennae 6Cellphonemasts 10Cellulartelephones 2Cheque-writingmachines 6Cinemaequipment 5Colddrinkdispensers 6Communicationsystems 5Compressors 4Computers mainframe/server 5 personal 3Computersoftware(mainframes) purchased 3 self-developed 1Computersoftware(personalcomputers) 2Concretemixersportable 4Concretetransitmixers 3Containers 10Cropsprayers 6Curtains 5Debarkingequipment 4Deliveryvehicles 4Demountablepartitions 6Dentalanddoctors’equipment 5Dictaphones 3Drillingequipment(water) 5

Drills 6Electricsaws 6Electrostaticcopiers 6Engravingequipment 5Escalators 20Excavators 4Faxmachines 3Fertiliserspreaders 6Firearms 6Fireextinguishers(looseunits) 5Firedetectionssystems 3Fishingvessels 12Fittedcarpets 6Food bins 4Food-conveyingsystems 4Forklifttrucks 4Front-endloaders 4Furnitureandfittings 6Gantrycranes 6Gardenirrigationequipment(movable) 5Gascuttingequipment 6Gasheatersandcookers 6Gearboxes 4Gearshapers 6Generators(portable) 5Generators(standby) 15Graders 4Grindingmachines 6Guillotines 6Gymnasiumequipment Cardiovascular 2 Healthtesting 5 Weightsandstrength 4 Spinning 1 Other 10Hairdressers’equipment 5Harvesters 6Heatdryers 6Heatingequipment 6Hot-watersystems 5Incubators 6Ironingandpressingequipment 6Kitchenequipment 6Knittingmachines 6Laboratoryresearchequipment 5Lathes 6Laundromatequipment 5Lawreports 5

ALLOWANCESWEAR AND TEAR

23

Lift installations 12Medicaltheatreequipment 6Millingmachines 6Mobilecaravans 5Mobilecranes 4Mobilerefrigerationunits 4Motors 4Motorcycles 4Motorisedchainsaws 4Motorisedconcretemixers 3Motormowers 5Musicalinstruments 5Navigationsystems 10Neonsignsandadvertising boards 10Officeequipment electronic 3 mechanical 5Oxygenconcentrators 3Ovensandheatingdevices 6Ovensforheatingfood 6Packagingequipment 4Paintings 25Pallets 4Passengercars 5Patterns,toolinganddies 3Pelletmills 4Perforatingequipment 6Photocopyingequipment 5Photographicequipment 6Planers 6Pleasurecraft 12Ploughs 6Portable safes 25Powertools(hand-operated) 5Powersupply 5Publicaddresssystems 5Pumps 4Racehorses 4Radarsystems 5Radiocommunication 5Refrigeratedmilktankers 4Refrigerationequipment 6Refrigerators 6

Type of No. of yearsasset for write-off

Type of No. of years asset for write-off

Runwaylights 5Sanders 6Scales 5Securitysystemsremovable 5Seedseparators 6Sewingmachines 6Shakers 4Shopfittings 6Solarenergyunits 5Specialpatternsandtooling 2Spindryers 6Spotweldingequipment 6Stafftrainingequipment 5Surgebins 4Surveyors fieldequipment 5 instruments 10Taperecorders 5Telephoneequipment 5Televisionandadvertisingfilms 4Televisionsets,videomachinesanddecoders 6Textbooks 3Tractors 4Trailers 5Traxcavators 4Trollies 3Trucks(heavy-duty) 3Trucks(other) 4Truck-mountedcranes 4Typewriters 6Vendingmachines(includingvideogamemachines) 6Videocassettes 2Warehouseracking 10Washingmachines 5Waterdistillationandpurificationplant 12Watertankers 4Watertanks 6Weighbridges(movableparts) 10Wirelinerods 1Workshopequipment 5X-rayequipment 5

Notes1 Wearandtearmaybeclaimedoneitheradiminishingvaluemethodoronastraight- linebasis,inwhichcasecertainrequirementsapply2 Costsincurredinmovingbusinessassetsfromonelocationtoanotherarenot deductibleastheseareregardedasbeingcapitalinnature.Wearandtearmay beclaimedovertheremainingusefullifeoftheassets3 Whenanassetisacquiredfornoconsideration,awearandtearallowancemaybe claimedonitsmarketvalueatdateofacquisition4 Priorto1January2013,wearandtearonanyassetsacquiredfromaconnected personmayonlybeclaimedontheoriginalcosttothesellerlessallowancesclaimed bytheseller,plusrecoupmentsandCGTincludedintheseller’sincome5 Theacquisitionof“small”itemsatacostoflessthanR7000(2009:R5000)peritem maybewrittenoffinfullduringtheyearofacquisition.

24

STRATEGIC ALLOWANCES

Asfrom1October2001,CapitalGainsTax(CGT)appliestoaresident’sworldwideassetsandtoanon-resident’simmovablepropertyorassetsofapermanentestablishmentinSouthAfrica.

DisposalsCGTistriggeredondisposalofanasset.• Important disposals include - abandonment,scrapping,loss,donation - vestingofaninterestinanassetofatrustinthebeneficiary - distributionofanassetbyacompanytoashareholder - granting,renewal,extensionorexerciseofanoption• Deemed disposals include - terminationofSouthAfricanresidency - achangeintheuseofanasset - anassetceasingtobepartofapermanentestablishment - foryearsofassessmentcommencingonorafter1January2013,the reductionorwaiverofadebt,subjecttocertainexclusions• Disposals exclude - thetransferofanassetassecurityforadebtorthereleaseof suchsecurity - issueof,orgrantofanoptiontoacquireashare,debentureor unit trust - loansandthetransferorreleaseofanassetsecuringdebt

CAPITAL GAINSTAX

Asset type Conditions for annual allowance Annual allowance

Strategicprojects Anadditionalindustrialinvestmentallowanceis 100%ofcost (note) allowedonnewandunusedassetsusedfor preferredqualifyingstrategicprojectswhichwere approvedbetween31July2001and31July2005 Anyotherqualifyingstrategicprojects 50%ofcost

Pipelines Newandunusedstructurescontractedfor 10%ofcost andconstructioncommencedonorafter 23February2000

Electricityand Newandunusedstructurescontractedfor 5%ofcost telephonetrans- andconstructioncommencedonorafter missionlinesand 23February2000 railwaytracks

Airportand Newandunusedassetsandimprovementsbrought 5%ofcost Portassets intouseonorafter1January2008anduseddirectly andsolelyforpurposeofbusinessasairport, terminalortransportoperationorportauthority Rollingstock Broughtintouseonorafter1January2008 20%ofcost

Environmental Environmentaltreatmentandrecyclingassets 40%in1styear assets asfrom8January2008fornewandunusedassets 20%ineachofthe 3subsequentyears Environmentalwastedisposalassetsofa permanentnature 5%ofcost

Energyefficiency Allformsofenergyefficiencysavingsasreflected Determinedin savings onanenergysavingscertificateinanyyearof accordancewitha assessmentendingbefore1January2020 formula

Note:• Theallowanceislimitedtotheincomederivedfromtheindustrialprojectandtheexcessis deductibleintheimmediatelysucceedingtaxyear,subjecttocertainotherlimits

25

Calculation of a Capital Gain/Loss• Acapitalgainorlossisthedifferencebetweentheproceedsandthebase cost.Anaggregatecapitallossiscarriedforwardandisavailableforset-off againstsubsequentcapitalgains

Base Cost• Expenditure included in the base cost - acquisition,disposal,transfer,stampduty,STTandsimilarcosts - remunerationofadvisers,consultantsandagents - costsofmovinganassetandimprovementcosts• Expenditure excluded from the base cost - expensesdeductibleforincometaxpurposes - interestpaid,raisingfees(exceptinthecaseoflistedsharesandbusiness assets) - expensesinitiallyrecordedandsubsequentlyrecovered• Methods for asset acquired before 1 October 2001 - Valuationasat1October2001 - 20%oftheproceeds - Timeapportionmentbasecost Example: IfanassetcostR250000on1October1998andwassoldon 30September2014forR450000,asCGTwasimplementedon 1October2001,thebasecostis:

Originalcostexpenditure R250000 Add: R37500*

*Proceedsfromdisposal R450000 Less:Basecostexpenditure(R250000)

Timeapportionmentbasecost R287500

Note 1:Whendeterminingthenumberofyearstobeincludedinthetime apportionmentcalculation,apartoftheyearistreatedasafullyear. Note 2:Whereexpenditureinrespectofapre-valuationdateassetwasincurred onorafter1October2001andanallowancehasbeenallowedinrespectofthat asset,anextendedformulaisapplied. • Part disposals - Basecostisapportionedunlessitisseparatelyidentifiable

Proceeds• Thetotalamountreceivedoraccruedfromthedisposal• Excluded - amountsincludedingrossincomeforincometaxpurposes - amountsrepaidorrepayableorareductioninthesaleprice• Specific transactions - connectedpersons-deemedtobeatmarketvalue - deceasedpersons-marketvalueasatdateofdeath - deceasedestates-thebequestisdeemedtobeatthebasecost i.e.marketvalueatdateofdeath

2012 2013-2015 2016 2012 2013-2015 2016Individuals 25% 33,3% 33,3% 10% 13,3% 13,7%SpecialTrusts 25% 33,3% 33,3% 10% 13,3% 13,7%Companies 50% 66,6% 66,6% 14% 18,7% 18,7%Trusts 50% 66,6% 66,6% 20% 26,6% 27,3%

Inclusion rate Maximum effective rateInclusion Rates and Effective Rates

InthecaseofUnitTrusts(CIS),theunitholderisliablefortheCGTondisposaloftheunits.RetirementFundsareexemptfromCGT.

} x 316

26

Exclusions and Rebates• Annual exclusion NaturalpersonsandspecialtrustsR30000(2012:R20000) NaturalpersonsintheyearofdeathR300000(2012:R200000)• Other exclusions - Aprimaryresidence,ownedbyanaturalpersonoraspecialtrust, usedfordomesticresidentialpurposes,wheretheproceedsdonot exceedR2million.WheretheproceedsexceedR2million,the exclusionisR2million(2012:R1,5million)ofthecalculatedcapitalgain - Personaluseassetsownedbyanaturalpersonoraspecialtrust,not usedforthecarryingonofatrade - Lumpsumsfrominsuranceandretirementbenefits.Thisexclusion doesnotapplytosecond-handpoliciesunlesstheyarepurerisk policieswithnoinvestmentorsurrendervalue - Smallbusinessassetsoraninterestinasmallbusiness,limitedto R1,8million(2012:R900000)ifcertainrequirementsaremet,including: - thegrossassetvalueofthebusinessislessthanR10million (2012:R5million) -thenaturalpersonwasasoleproprietor,partneroratleast10% shareholderforatleastfiveyears,isatleast55yearsold,or suffersfromill-health,isinfirmordeceased - Compensation,prizesanddonationstocertainPBO’s - Assetsusedbyregisteredmicrobusinessesforbusinesspurposes.

Rollover ReliefThecapitalgainisdisregardeduntilultimatedisposaloftheassetorinthecaseofareplacementassetitisspreadoverthesameperiodaswearandtearmaybeclaimedforthereplacementasset,commencingwhenthereplacementassetisbroughtintouseunlessdisposedofearlier.Thereliefappliestothefollowing:• Certaininvoluntarydisposals• Replacementofqualifyingbusinessassets(excludingimmovableproperty)• Transferofassetsbetweenspouses• Shareblockconversionstosectionaltitleorfulltitle• Transferofresidencefromaqualifyingcorporateentityortrustbetween 11February2009and31December2012.Iftransferoccurredafter 1October2010,thetransferringentityhadtobeterminated.

ValuationsValuationsshouldhavebeenobtainedbefore30September2004.Forcertainassetsthesevaluationsshouldhavebeenlodgedwiththefirsttaxreturnsubmittedafter30September2004,orsuchothertimeasSARSmayallow,providedthevaluationwasinfactdonepriortotherequisitedate:• WherethemarketvalueofanyintangibleassetexceedsR1million• WherethemarketvalueofanyunlistedinvestmentexceedsR10million• WherethemarketvalueofanyotherassetexceedsR10million.

Non-resident Sellers of Immovable PropertyAsfrom1September2007,whereanon-residentdisposesofimmovable propertyinSouthAfricainexcessofR2million,thepurchaserisobligedtowithholdthefollowingtaxesfromtheproceeds(unlessadirectivetothe contraryhasbeenissued):

Seller’s status Withholding taxNaturalperson 5,0%Company 7,5%Trust 10,0%

27

Asfrom2November2006,specificdeductionsareallowedforexpenditureincurredinrespectofqualifyingresearchanddevelopment.As from 1 October 2012:• 100%automaticdeductionofexpenditureincurredsolelyanddirectlyin respectofseparatelyidentifiableresearchanddevelopmentactivities• 50%additionaldeductionofexpenditureincurredsolelyanddirectlyin respectofseparatelyidentifiableresearchanddevelopmentactivities, whichissubjecttopre-approvalbytheDepartmentofScienceand Technology.As from 1 January 2014:• Researchanddevelopmentexcludes: - internalbusinessprocessessthatareusedbyconnectedparties - routinetesting,analysis,collectingofinformationandqualitycontrol - marketresearch,markettestingorsalespromotion - thecreationordevelopmentoffinancialinstrumentsorproducts - thecreationorenhancementoftrademarksorgoodwill.• TheDepartmentofScienceandTechnologymustapprovetheentire 150%deduction.Onlyexpenditureincurredonorafterthedateofreceipt oftheapplicationiseligibleforthisdeduction.Researchanddevelopmentcapitalassetsarewrittenoffasfollows: - newandunusedmachineryorplantona50:30:20basis(priorto 1January2012-40:20:20:20) - buildingsorimprovementsat5%peryear.Thisincentiveceasestoapplyfrom1October2022.

RESEARCH ANDDEVELOPMENT

Taxpayerscandefertaxablerecoupmentsandcapitalgainsonthesaleofbusinessassets(excludingbuildings)iftheyfullyreinvestthesaleproceedsinotherqualifyingassetswithinaperiodofthreeyears.Taxontherecoupmentandcapitalgainuponthedisposaloftheoldassetisspreadoverthesameperiodaswearandtearmaybeclaimedforthereplacementasset.

REINVESTMENT RELIEF

UNQUANTIFIED PROCEEDSWhereanassetisdisposedofforanunquantifiedamount,theportionofthepurchasepricewhichcannotbequantifiedinthatyearisdeemedtoaccrue intheyearthatitbecomesquantifiable.Anyrecoupment,capitalgainorcapitallossarisingfromsuchtransactionisdeferreduntilsuchtimeastheconsiderationbecomesquantifiable.Forexample,iftheassetisbroughtintouseinyear1,buttheconsiderationonlybecomesquantifiableinyear2,thewearandtearforyear1andyear2willbeclaimedinyear2.

DISPOSALOFSHARESDEEMED CAPITALAsfrom1October2007,theproceedsonthesaleofanequityshareor collectiveinvestmentschemeunitwillautomaticallybeofacapitalnatureifheldcontinuouslyforatleastthreeyearsexceptinthecaseof:• ashareinanon-residentcompany,subjecttocertainexclusions• ashareinashareblockcompany• ahybridequityinstrument.Previouslythetaxpayercouldelectthattheproceedsonthesaleofalistedshareheldforatleastfiveyearsbetreatedascapital.

28

Asfrom1July2009,ataxpayerisentitledtoadeductionof100%ofthecostofsharesissuedbyaventurecapitalcompanysubjecttothe followinglimitations:• anaturalpersonmaydeductR750000inayearofassessmentanda totalofR2250000• alistedcompanyandanycompanyheld70%directlyorindirectlyby thatlistedcompanycandeductamaximumofthecostofupto40%of thetotalequityinterestintheventurecapitalcompany• theventurecapitalcompanymustbeapprovedbySARSasaqualifying companyandsatisfyanumberofpre-conditions.

Asfrom1January2012,alltaxpayersareentitledtothisdeductionwithoutanylimitationimposedontheamount,providedtheexpenditurecomprisesaninvestmentinequityshares,theinvestorisnotaconnectedpersonaftermakingtheinvestmentandisgenuinelyexposedtotheriskofeconomic lossintheeventoffailureoftheventure.Variousthresholdsregardingthelevelandnatureofexpenditurebytheventurecapitalcompanyhavealsobeenrelaxedtoattractmoreinterestinthisincentive.

VENTURE CAPITALINVESTMENTS

LEARNERSHIP ALLOWANCES

Employersareallowedtoclaimlearnershipallowancesforregistered learnerships(enteredintobefore1October2016)overandabovethe normalremunerationdeduction.Foryearsofassessmentendingonor after1January2010:• Whereanemployerispartytoalearnership,thelearnershipallowance consistsoftwobasicthresholds:arecurringannualallowanceof R30000andacompletionallowanceclaimableattheendofthe learnershipofR30000.Wherethelearnershipexceeds24monthsthe completionallowanceisclaimedcumulativelyforeverycompletedyear• Forlearnerswithdisabilitiestherelevantallowancesareincreasedto R50000• Learnershipsoflessthan12fullmonthsareeligibleforapro-rata amountoftheannualallowance(regardlessofthereasonthatthe learnershipfallsshortofthe12monthperiod).Ifalearnershipfalls overtwoyearsofassessment,theannualallowanceisallocated pro-ratabetweenbothyearsbasedonthecalendarmonths applicabletoeachyearbymultiplyingtheannualallowanceby thetotalcalendarmonthsofthelearnershipover12.

INDUSTRIAL POLICY PROJECTS

Anadditionalinvestmentallowanceforanapprovedprojectisavailabletoabrownfieldprojectexpansionorupgrade,oragreenfieldprojectfornew andunusedmanufacturingitems.Subjecttocertainlimits,theadditional allowanceis55%forpreferredprojectsand35%fornon-preferredprojects.Wheretheprojectisundertakeninanindustrialdevelopmentzonethe allowancesareincreasedto100%and75%respectively.ThereisalsoanadditionalprojectrelatedtrainingallowanceofR36000per employeeperannumforaperiodofsixyears,limitedtoR30millionfor preferredprojectsandR20millionfornon-preferredprojects.

29

DIRECTORS PAYE

Directorsofprivatecompaniesandmembersofclosecorporationsare deemedtohavereceivedamonthlyremuneration,subjecttoPAYE, calculatedinaccordancewithaformula.Theformulacalculatedremunerationdoesnotapplytodirectorsofprivatecompaniesandmembersofclosecorporationswhoearnatleast75%of theirremunerationintheformoffixedmonthlypayments.

SECURITIES TRANSFERTAX

Asfrom1July2008,SecuritiesTransferTax(STT)ispayableatarateof0,25%oftheconsideration,closingpriceormarketvalue(whicheverisgreater)onthetransfer,cancellationorredemptionofanylistedorunlistedshare,member’sinterestinaclosecorporationorcessionofarighttoreceivedistributionsfromacompanyorclosecorporation.• Onlistedsecurities,theSTTispayablebythe14thofthemonthfollowing themonthduringwhichthetransferoccurred• Onunlistedsecurities,theSTTispayablebytheendofthesecondmonth followingtheendofthemonthduringwhichthetransferoccurred• Ifnotpaidinfullwithintheprescribedperiodinterestisimposedatthe prescribedrateanda10%penaltyispayable• NoSTTispayableiftheconsideration,closingpriceormarketvalueis lessthanR40000.

CONNECTEDPERSONSWEAR AND TEARPriorto1January2013,whereadepreciableassetwasacquiredbyatax- payeranditwasheldbyaconnectedpersonatanytimeduringaperiod oftwoyearsbeforethatacquisition,thepurchasercouldclaimcapital allowancesonthelowerofthepurchasepriceorthefollowingdeemedcost:• thenettaxvalueoftheassettotheseller,plus• therecoupmentonthedisposalbytheseller,plus• thetaxablecapitalgainonthedisposalbytheseller.Thislimitationisnolongerapplicable.

Nostampdutyispayableonleasesofimmovablepropertyenteredintoafter1April2009.

STAMP DUTY

Expenditurepaidshouldbeapportionedtotheextentthatonlyexpenditureactuallyincurredinayearofassessmentisdeductible.Theremainderofthepre-paidexpenditurewillbedeductibleinsubsequentyearsofassessment.Thisdoesnotapply:• wherethegoods,servicesorbenefitsaresuppliedorrenderedwithinsix monthsaftertheendoftheyearofassessment• wherethetotalpre-paidexpendituredoesnotexceedR100000 (2012:R80000)• toexpenditurewithspecificallydeterminedtimingandaccrual• topre-paidexpenditurepayableintermsofalegislativeobligation.

PRE-PAID EXPENDITURE

30

Asfrom1January2001,residentsaretaxableontheirworldwideincome.

Resident means• AnaturalpersonwhoisordinarilyresidentinSouthAfrica• Asfrom1March2005,anaturalpersonwhoisphysicallypresentin SouthAfricaforatleast91daysinthecurrentandeachofthe precedingfivetaxyearsandatleast915daysduringthefivepreceding taxyears.Thesedaysdonotneedtobeconsecutive• Acompanyortrustthatisincorporated,established,formedorwhich hasitsplaceofeffectivemanagementinSouthAfrica.

Resident excludes• Anaturalperson,whowaspreviouslyregardedasadeemedresident,if physicallyabsentfromSouthAfricaforacontinuousperiodofatleast 330daysfromthedateofdeparture• Apersonwhoisdeemedtobeexclusivelyaresidentofanothercountry forthepurposesoftheapplicationofanydoubletaxationagreement (DTA).

Exemptions• RemunerationforservicesrenderedoutsideSouthAfricaduringthetax yearifsuchpersonwasoutsideSouthAfricaforperiodsinaggregateof morethan183days,ofwhichmorethan60dayswerecontinuous• Foreignpensionandsocialsecuritypayments.

Foreign DividendsForeigndividendsreceivedfromanon-residentcompanyanddividendsreceivedfromaheadquartercompanyaretaxable,exceptif:• theshareholderholdsatleast10%oftheequityandvotingrightsofthe distributingcompany• thedistributingcompanyislistedontheJSEandfrom1March2014 includesadividendin specie.• thedistributingcompanyisacontrolledforeigncompany(CFC)and thedividendsdonotexceedamountsdeemedtobetheresident shareholder’sincomeundertheCFCrules• foreigndividendsdeclaredbyonecompanytoanothercompanyresident inthesamecountry.Anyremainingtaxableforeigndividendissubjecttoaformulawherebythemaximumrateoftaxationis15%subjecttoareductionintermsofaDTA.Aresidentisentitledtoacreditforanywithholdingtaxpaidinrespectofaforeigndividendthatisincludedingrossincome,providedsuchdividendisnotfullyexempt.Asfrom1April2012,nodeductionisallowedforinterestincurredintheproductionofforeigndividends.

Controlled Foreign CompaniesACFCisanon-residentcompanyinwhichresidents,otherthanahead-quartercompany,directlyorindirectlyownorcontrolmorethan50%oftheparticipationorvotingrights.Asfrom1April2012,aresidentholdingbetween10%and20%ofaforeigncompany,maynolongerelecttotreatthecompanyasaCFC.

RESIDENCE BASED TAXATION

31

• Aresidentmustincludeinhisincome:

Resident’s participation rights in the CFC

Total participation rights in the CFC• ThenetincomeofaCFCshouldbecalculatedaccordingtoSouth Africantaxprinciples.Ifthecalculationresultsinaloss,thedeductions arelimitedtoincomeandtheexcessiscarriedforward.Exemptions• Thenetincome(includingcapitalgains)oftheCFCthatisderivedfrom anactivebona fideforeignbusinessestablishmentsituatedoutside SouthAfrica(subjecttocertainexclusions)• IncomeoftheCFCotherwisetaxedinSouthAfricaatnormalrates• ForeigndividendsreceivedbytheCFCfromanotherCFCtotheextent thattheincomefromwhichthedividendisdeclaredhasalreadybeen includedintheresident’staxableincomeundertheCFCrules• Netincomeattributabletointerest,royaltiesorsimilarincomepayable totheCFCbyotherforeigncompaniesformingpartofthesamegroup ofcompanies.• Thehightaxexemptionapplieswheretheaggregateofforeigntaxes payablebytheCFCisatleast75%oftheamountofSouthAfricantax thatwouldhavebeenimposedhadtheCFCbeenaSouthAfrican taxpayer.Tax Rebates• Wherearesidenthastoincludeinhistaxableincomeanyforeign sourcedincomeorcapitalgain,theproportionateamountofthenet incomeofaCFC,foreigndividends,orotherattributableamounts,a rebateinrespectofanyforeigntaxespaidorpayableinrespectofsuch amounttoaforeigngovernmentisallowed• Therebateislimitedtotheforeigntaxpayableandmaynotexceed:

Taxable foreign income

Total taxable income• Iftheforeigntaxpaidexceedsthelimitsetoutabove,theexcessforeign taxmaybecarriedforwardforamaximumofsevenyears• Asfrom1January2012,foreigntaxeswithheldonincomearisingfrom servicesrenderedinSouthAfricamaybeclaimedasarebate.General• AlossincurredincarryingonabusinessoutsideSouthAfricamaynotbe set-offagainstincomeinSouthAfrica• Theamountofforeigntaxpayablemustbeconvertedtorandsatthe lastdayofthetaxyearbyapplyingtheaverageexchangerateforthat taxyear• Foreignincomeisconvertedtorandsbyapplyingthespotexchange rateatthedatetheincomeaccrues.Naturalpersonsandnon-trading trustsmayelecttoapplytheaverageexchangerateforthattaxyear• Whereforeignincomemaynotberemittedbecauseofrestrictions imposedbythesourcecountry,suchincomeisincludedintheresident’s grossincomeinthetaxyearduringwhichthatamountmayberemitted toSouthAfrica• TaxwithheldinaforeigncountryinrespectofSouthAfricansourced income(exceptforincomearisingonservicesrenderedinSouthAfrica) isrecognisedasadeductionagainstsuchincomeratherthanasarebate againstSouthAfricantaxpayableonthatincome.

Net income of CFC x

Total South African normal tax x

32

AGREEMENTSDOUBLE TAXATIONDoubletaxationariseswheretwocountrieshaveataxingrightonthesameamount.SouthAfricahasnegotiateddoubletaxationagreementswithvariouscountriesaroundtheworld.Thepurposeoftheseagreementsistoeliminatedoubletaxation.Thedoubletaxationagreementsareavailableonwww.sars.gov.za

InterestInterestreceivedbyoraccruedtoanon-residentisexemptfromnormaltax unlesstheindividualwasphysicallypresentinSouthAfricaforaperiodof morethan183daysinaggregateorcarriedonbusinessthroughapermanentestablishmentinSouthAfricaatanytimeduringtheprior12monthperiod. Asfrom1March2015,wherethisexemptionisapplicable,afinal withholdingtaxof15%willbeimposedoninterestpaidtoanon-residentsubjecttoareductionintherateintermsofadoubletaxationagreement.DividendsAsfrom1April2012,DividendsTaxisduebytheshareholderatarateof15%,subjecttoareductionintherateintermsofadoubletaxation agreement.RoyaltiesAsfrom1January2015,afinalwithholdingtaxof15%(previously12%)isimposedonroyaltiespaidtoanon-resident,subjecttoareductionintherateintermsofadoubletaxationagreement.ResidentsrequireGovernmentandSARBapprovalforroyaltypaymentsto anon-resident.Service FeesAsfrom1January2016,afinalwithholdingtaxof15%willbeimposedon crossborderconsultancy,managementandtechnicalfeesfromaSouth Africansource,subjecttoareductionintherateintermsofadouble taxationagreement.Other IncomeNon-residentsaretaxedonSouthAfricansourcedincomeonly.Payment to Non-Resident EntertainersAwithholdingtaxof15%ispayablebynon-residentsportspersonsand entertainersonincomeearnedinSouthAfrica.

TAXATION OF NON-RESIDENTS

Asfrom1March2015,afinalwithholdingtaxof15%willbeimposedoninterestpaidtoanynon-residentfromaSouthAfricansourcesubjecttoareductionintherateintermsofadoubletaxationagreement,onthedateit ispaidorbecomesdueandpayableexceptinterest:• payablebyanysphereoftheSouthAfricanGovernment• arisingonanylisteddebtinstrument• arisingonanydebtowedbyabank,theDBSA,theIDCortheSARB• payablebyaheadquartercompanywheretransferpricingdoesnotapply• accruingtoanon-residentnaturalpersonwhowasphysicallypresentin SouthAfricaforaperiodexceeding183daysinaggregate,duringthat year,orcarriedonabusinessthroughapermanentestablishmentin SouthAfricaatanytimeduringtheprior12monthperiod• payablebyalocalstockbrokertoanon-resident.Thepersonpayingtheinteresthasawithholdingobligation,unlessheisinpossessionofawrittendeclarationandundertakingconfirmingthattherecipientiseitherentitledtoanexemptionortodoubletaxationreliefandthatsuchpersonwillinformhimofanychangeofcircumstances.

WITHHOLDING TAX ONINTEREST

33

WITHHOLDING TAX ONROYALTIES

Asfrom1January2015,afinalwithholdingtaxof15%(previously12%)isimposedonroyaltiespaidtoanon-residentsubjecttoareductionintherateintermsofadoubletaxationagreement.ThewithholdingtaxisonlyapplicabletoroyaltiesduefromaSouthAfricansource.Royaltiesareexemptfromthewithholdingtaxif:• thenon-residentnaturalpersonwasphysicallypresentinSouthAfricafor aperiodexceeding183daysinaggregateduringthe12monthperiod precedingthedateonwhichtheroyaltyispaid• thenon-residentnaturalperson,companyortrustcarriedonbusiness throughapermanentestablishmentinSouthAfricaduringthe12month periodprecedingthedateonwhichtheroyaltyispaid• theroyaltyispaidbyaheadquartercompanyandtheintellectual propertyissub-licencedtooneormoreortheforeigncompaniesin whichtheheadquartercompanyholdsatleast10%oftheequityand votingrights.Thepersonpayingtheroyaltyhasawithholdingobligation,unlessheisinpossessionofawrittendeclarationandundertakingconfirmingthattherecipientiseitherentitledtoanexemptionortodoubletaxationreliefandthatsuchpersonwillinformhimofanychangeofcircumstances.

Asfrom1January2016,afinalwithholdingtaxof15%willbeimposedon crossborderconsultancy,managementandtechnicalfeesfromaSouth Africansource,subjecttoareductionintherateintermsofadoubletaxationagreement.Servicefeesareexemptfromthewithholdingtaxif:• thenon-residentnaturalpersonwasphysicallypresentinSouthAfricafor aperiodexceeding183daysinaggregateduringthe12monthperiod precedingthedateonwhichtheservicefeeispaid• theserviceiseffectivelyconnectedwithapermanentestablishmentof thatnon-residentinSouthAfricaprovidedthatthenon-residentis registeredasataxpayerinSouthAfrica• theservicefeesconstituteremuneration.Thepersonpayingtheservicefeehasawithholdingobligation,unlessheisinpossessionofawrittendeclarationandundertakingconfirmingthattherecipientiseitherentitledtoanexemptionortodoubletaxationreliefandthatsuchpersonwillinformhimofanychangeofcircumstances.

WITHHOLDING TAX ONSERVICEFEES

Theheadquartercompanyrulesapplyfromyearsofassessment commencingonorafter1January2011andprovideforseveralbenefits,including:• itssubsidiariesarenottreatedascontrolledforeigncompanies• dividendsarenotsubjecttoDividendsTax• noapplicationofthincapitalisationortransferpricingrulesinthecaseof back-to-backcross-borderloans• exemptionfromthependingwithholdingtaxoninterestinrespectof back-to-backloans.Asfrom1January2011aspecialregionalinvestmentfundruleisapplicable.QualifyingforeigninvestorswillberegardedaspassiveinvestorswithnoexposuretoSouthAfricantaxwhenusingaSouthAfricanportfoliomanager.

HEADQUARTER COMPANY

34

Doubletaxationagreementsprovideforreliefinrespectofroyalties,dividendsandinterestwithholdingtaxes.

Algeria 10 10/15 10Australia 5 5/15 10Austria 0 5/15 0Belarus 5/10 5/15 5/10Belgium 0 5/15 10Botswana 10 10/15 10Brazil 10/15 10/15 10Bulgaria 5/10 5/15 5Canada 6/10 5/15 10Croatia 5 5/10 0Cyprus 0 0 0CzechRepublic 10 5/15 0DemocraticRepublicofCongo 10 5/15 10Denmark 0 5/15 0Egypt 15 15 12Ethiopia 15 10 8Finland 0 5/15 0France 0 5/15 0Germany 0 7,5/15 10Ghana 10 5/15 5/10Greece 5/7 5/15 8Hungary 0 5/15 0India 10 10 10Indonesia 10 10/15 10Iran 10 10 5Ireland 0 5/10 0Israel 0/15 15 15Italy 6 5/15 10Japan 10 5/15 10Korea 10 5/15 10Kuwait 10 0 0Lesotho 10 15 10Luxembourg 0 5/15 0Malawi 15 15 15Malaysia 5 5/10 10Malta 10 5/10 10Mauritius 0 5/15 0Mexico 10 5/10 10Mozambique 5 8/15 8Namibia 10 5/15 10Netherlands 0 5/10 0NewZealand 10 5/15 10Nigeria 7,5 7,5/10 7,5

WITHHOLDING TAXES SUMMARYDOUBLETAXATIONAGREEMENTS

Treaty Countries

Non-Treaty Countries 15 15 15