Systematic Alpha Monthly - Credit Suisse

53

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, LEGAL ENTITY DISCLOSURE AND ANALYST CERTIFICATIONS. 13 October 2016 Americas Fixed Income Research Index and Alpha Strategy INSTITUTIONAL CLIENTS ONLY/DO NOT FORWARD Systematic Alpha Monthly Research Analysts Baldwin Smith 212 325 5524 [email protected] Yongchu Song 212 538 7013 [email protected] Sherry Li 212-538-2585 [email protected] Olivia Zhong 1 212 538 4328 [email protected] Steven Tang 212 538 0339 [email protected] September 2016 ■ In this month’s Research Spotlight section, we examine the Credit Suisse Multi-Asset Trend Index Suite (MATRIX). ■ The MATRIX strategy is a trend-following strategy that aims to benefit from momentum across a variety of asset classes. ■ It attempts to do so by generating momentum signals comparing exponential moving averages in different time period. ■ Since its inception in April 2002, a multiple asset class basket index with global equity and bonds exposure within MATRIX suite has a Sharpe of 1.25 outperforming the traditional 60-40 portfolio with a Sharpe of 0.61.

Transcript of Systematic Alpha Monthly - Credit Suisse

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, LEGAL ENTITY DISCLOSURE AND ANALYST CERTIFICATIONS.

13 October 2016

Americas Fixed Income Research Index and Alpha Strategy

INSTITUTIONAL CLIENTS ONLY/DO NOT FORWARD

Systematic Alpha Monthly

Research Analysts

Baldwin Smith

212 325 5524

Yongchu Song

212 538 7013

Sherry Li

212-538-2585

Olivia Zhong

1 212 538 4328

Steven Tang

212 538 0339

September 2016

■ In this month’s Research Spotlight section, we examine the Credit Suisse

Multi-Asset Trend Index Suite (MATRIX).

■ The MATRIX strategy is a trend-following strategy that aims to benefit from

momentum across a variety of asset classes.

■ It attempts to do so by generating momentum signals comparing

exponential moving averages in different time period.

■ Since its inception in April 2002, a multiple asset class basket index with

global equity and bonds exposure within MATRIX suite has a Sharpe of

1.25 outperforming the traditional 60-40 portfolio with a Sharpe of 0.61.

13 October 2016

Systematic Alpha Monthly 2

Table of contents

Global Market Overview 4

Credit Suisse Alpha Strategies Platform 5

Individual Strategy Performance 6

Research Spotlight: Credit Suisse Multi-Asset Trend Index Suite (MATRIX) 8

Strategy Snapshots 12

Smart Beta 13

HS Global Style Rotation 13

HS Global Style Rotation Equity Hedged 14

HS Market Neutral Index Powered by HOLT® 15

Global Enhanced Momentum Strategy 16

GAINS 01E 17

Commodity Backwardation 18

Alternative Risk Premia 19

Global Carry Selector 19

Global Carry Selector II 20

Advanced Relative Value Volatility Index 21

Mean Reversion Index on Euro Stoxx 50 22

Dividend Alpha Index on Euro Stoxx 50 23

Adaptive Volatility Index Global 24

Adaptive Term Premium Index 25

Commodity Backwardation RV 26

Commodity Momentum Long/Short 27

Commodity Custom 24 Alpha 28

Commodity Custom 88 Enhanced 29

FX Metrics Carry 30

FX Metrics Momentum 31

FX Metrics Value 32

Dynamic Multi Asset Allocation 33

RAII HOLT®: Risk Appetite Investible Index Powered by HOLT® 33

RAII HOLT® Relative Value 34

ARROW 6% 35

Multi-Asset Futures Strategy 36

MASTRO 37

Systematic Tactical Asset Allocation 38

TEMPO 39

13 October 2016

Systematic Alpha Monthly 3

Portfolio Hedging 40

Equity Dynamic Tail Hedge SPX Index 40

Cheapest Slide Index 41

Advanced Defensive Volatility Index 42

Tail Risk Overlay Protection Strategy 43

Liquid Alternative Beta 44

Liquid Alternative Beta 44

Long/Short Liquid Index 45

Event-Driven Liquid Index 46

Merger Arbitrage Liquid Index 47

Managed Futures Liquid Index 48

Global Strategies Liquid Index 49

13 October 2016

Systematic Alpha Monthly 4

Global Market Overview Economics:The September Employment

Report was mostly in line with expectations, and does not fundamentally change the

broader US outlook. Payrolls growth remains on its slowing trend and income details recovered after a disappointing August report.

While this is not quite strong enough to return income growth to its previous trends, it does allay concerns about a sharper slowdown. CS

economists continue to expect personal consumption growth to soften slightly in H2 2016. Solid payrolls growth and the rebound in

labor income will support the hawkish case for a December hike. On the other hand, a sideways unemployment rate and continued

sluggishness in wage growth suggest there is little overheating in the labor market and few signs of inflationary pressure. In our view, the

data appear sufficient to support a hike this year, but the Fed’s cautious approach and the risks from the presidential election make further

delays more likely than not.

■ Fixed Income: The recent back-up in yields

has come on the back of a repricing of Fed hike expectations along with a shift in

international dynamics that had been supporting Treasuries. CS rates strategists expect that front-end inflation BEi will be more

sensitive to oil prices than the long end, marking the return of a more traditional relationship when compared to that observed

from mid-2014 to late last year.

■ Equities: While markets have shown

resilience following the UK referendum, CS equity strategists believe US equities remain

vulnerable to bad news heading into year-end, with risk of shifting negative due to recent weakness in buyback activity.

■ FX: CS FX strategists continue to expect the

PBOC to guide the CNY down about 1% - 1.5% vs. the CFETS basket over the next several months or 93.0 – 93.5 on the basket. This

would imply 6.69 – 6.72 on USDCNY given their broad USD forecast set, including their forecast for USDJPY to fall to 95. They

maintain the forecasts for 6.71 on USDCNY in 3 months and 6.80 in 12 months. A risk is that

the US Fed signals a rate hike at its December

meeting supporting the USD close to current levels. In this scenario their forecast for the CNY vs. its basket would imply 6.678 – 6.798

on USDCNY.

■ Commodities: CS commodity strategists think

that oil markets will remain trapped in a range of $45/b Brent plus or minus $5 through winter.

Fundamentally things will not likely tighten up in the next two quarters; but unlike last year, the wheels are not coming off the

fundamentals cart either. Starved without revenue, the industry and many sovereigns have had to cut back upstream activity sharply,

and oil production is falling in most places.

WTI Crude, Aug 1 to Oct 13, 2016

Note: Data as of 09/30/2016 Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

USDCNY, Aug 1 to Oct 13, 2016

Note: Data as of 09/30/2016 Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

Benchmark Performance

Benchmark

Current

Level

Sept

2016

2016 YTD

Return

VIX 17.1 -0.13 -4.92

MSCI World 1695.5 0.4% 3.8%

S&P GSCI 224.5 4.1% 5.1%

S&P 500 2139.2 -0.1% 6.1%

JPM Global Bond 384.1 -0.1% 6.8%

US 10yr Yield 1.74 0.01 -0.68

Gold 1259.2 0.5% 24.0%

Moody's BAA Spread 189.9 0.8% -20.5%

Note: Current level Data as of 10/13/2016; Sept 2016 uses Data as of 09/30/2016;Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

35

37

39

41

43

45

47

49

51

53

55

1-Aug 16-Aug 31-Aug 15-Sep 30-Sep

WTI Crude

6.56

6.58

6.6

6.62

6.64

6.66

6.68

6.7

6.72

6.74

1-Aug 16-Aug 31-Aug 15-Sep 30-Sep

USDCNY Curncy

13 O

cto

be

r 201

6

Credit Suisse Alpha Strategies Platform

Equities FX Interest Rates Commodities Multi-Asset

Smart Beta HOLT family Sector

Rotation GAINS LAB Broad

Backwardation LAB Managed

Futures

Alternative Risk Premia

Global Carry Selector family

Mean Reversion Momentum Adaptive

Volatility Backwardation

RV RAII HOLT Relative

Value

Advanced RVOL Dividend Alpha Carry Adaptive Term

Premium Momentum Long/Short

LAB Merger Arbitrage

LAB Long/Short Value GEMS Custom 24 Alpha LAB Event Driven

Custom 88 Enhanced

Portfolio Hedging

Dynamic Tail family

Advanced DVOL

TOPS

Cheapest Slide

Dynamic Asset Allocation

RAII HOLT STAA ARROW TEMPO CSMF1

Source: Credit Suisse

13 O

cto

be

r 201

6

Syste

matic

Alp

ha

Mo

nth

ly

6

Individual Strategy Performance

Strategy Asset ClassBloomberg

TickerLive Date Sep-16 Year-to-Date Past 12-Months

Total Return

Since Live

Past 12-

MonthsSince Live

Smart Beta

HS Global Sty le Rotation Equities HSGSRTR 10/14/2009 0.57% 6.18% 9.97% 10.97% 0.74 0.71

HS Global Sty le Rotation Equity Hedged Equities HSGSREH 1/4/2010 -0.03% -0.19% -1.99% 1.19% -0.55 0.36

HS Market Neutral Equities HSGMN 1/9/2007 0.18% -5.14% -4.88% -1.39% -1.07 -0.26

Global Enhanced Momentum Strategy Interest Rates CSGMEREU 1/1/2012 -0.51% -0.32% -1.00% -0.28% -0.56 -0.17

GAINS 01E Commodities CSGADER 10/15/2008 3.32% 8.30% -0.56% 0.33% -0.04 0.02

GAINS S&P GSCI Commodities CSGAGSER 10/15/2008 4.44% 5.27% -7.81% -3.37% -0.35 -0.17

GAINS 01E Long/Short Commodities CSGADLSE 10/15/2008 0.73% -0.94% 1.09% 9.60% 0.29 0.87

Commodity Backw ardation Commodities CSCUBKER 03/27/2012 2.38% 4.56% 3.15% -7.73% 0.26 -0.67

Alternative Risk Premia

Global Carry Selector Equities GCSCS 2/1/2009 3.42% -1.17% 7.45% 10.02% 0.52 0.49

Global Carry Selector II Equities GCSCS2 06/15/2012 1.21% -0.41% -0.94% -2.08% -0.14 -0.26

Adv anced Relativ e Value Volatility Equities CSEAARVL 09/26/2012 -0.73% 6.80% 2.01% -3.63% 0.30 -0.58

Mean Rev ersion on Euro Stox x 50 Equities CSEAMREU 03/27/2013 0.56% 10.93% 11.38% 3.44% 1.40 0.41

Div idend Alpha on Euro Stox x 50 Equities CSEADVAE 11/10/2013 1.28% 4.10% 3.69% 1.39% 1.23 0.35

Adaptiv e Volatility Index – Global Interest Rates CSVIXAEU 1/9/2012 0.58% 3.24% 4.93% 2.37% 1.21 0.58

Adaptiv e Volatility Index – USD Interest Rates CSVIXUSD 1/3/2009 0.67% 6.15% 8.42% 12.89% 1.48 1.39

Adaptiv e Volatility Index – JPY Interest Rates CSVIXJPY 1/1/2011 2.28% -2.81% -1.45% 1.99% -0.25 0.31

Adaptiv e Volatility Index – EUR Interest Rates CSVIXEUR 1/9/2012 -1.20% 6.44% 6.70% 4.42% 1.31 0.72

Adaptiv e Term Premium Index Interest Rates CATPU2P6 11/1/2011 -0.21% 2.83% 3.40% 2.06% 1.13 0.69

Commodity Backw ardation RV Commodities CSCUBKAE 3/6/2013 -0.72% -4.25% 4.98% 2.88% 0.47 0.34

Commodity Momentum Long/Short Commodities CSCUMLSE 11/12/2013 -0.07% -7.14% 2.44% 2.05% 0.17 0.19

Commodity Custom 24 Alpha Commodities CSCUS24A 2/15/2012 1.10% 8.60% 15.15% 11.13% 1.86 1.08

Commodity Custom 88 Enhanced Commodities CSCUE88E 6/18/2012 0.94% 2.30% 3.85% 2.24% 0.93 0.71

FX Metrics Carry FX FXMXCEUS 3/11/2010 0.61% 5.47% 8.25% -0.67% 0.89 -0.09

FX Metrics Momentum FX FXMXMEUS 3/11/2010 0.56% -3.92% -3.34% 0.11% -0.54 0.02

FX Metrics Value FX FXMXVEUS 3/11/2010 0.38% 1.50% 3.91% -0.09% 0.56 -0.02

RETURN SHARPE RATIO

Source: Credit Suisse

Note: Data as of 09/30/2016

Sharpe R at io : We calculate the Sharpe Ratio as the annualized average excess return divided by the annualized daily volat ility of the strategy. For excess return strategies, we simply use the raw strategy returns. For total return

strategies, we deduct the 1-month LIBOR for the currency in which the strategy is denominated. For more information, please visit us on Bloomberg at CSLI <GO>

Past performance should not be taken as an indicat ion or guarantee of future performance, and no representat ion or warranty, express or implied, is made regarding future performance. Information, opinions and est imates

contained in this report ref lect a judgment at the original date of publicat ion by CS and are subject to change without not ice. The price, value of and income from any of the securit ies or f inancial instruments mentioned in this report

can fall as well as rise. The value of securit ies and f inancial instruments may be subject to exchange rate f luctuat ion that may have a posit ive or adverse effect on the price or income of such securit ies or f inancial instruments. The P&L

results shown do not include relevant costs, such as commissions, interest charges, or other applicable expenses.

13 O

cto

be

r 201

6

Syste

matic

Alp

ha

Mo

nth

ly

7

Individual Strategy Performance (cont'd)

Strategy Asset ClassBloomberg

TickerLive Date Sep-16 Year-to-Date Past 12-Months

Total Return

Since Live

Past 12-

MonthsSince Live

Dynamic Multi Asset Allocation

RAII HOLT® Hy brid RAIIHUST 6/4/2010 1.15% -1.07% 3.37% 6.26% 0.19 0.43

RAII HOLT® Relativ e Value Hy brid RAIIHRVU 04/28/2011 0.45% -5.07% -5.60% -0.25% -0.63 -0.06

ARROW 6% Hy brid ARROWUT6 2/11/2011 0.29% 9.84% 7.78% 2.05% 1.37 0.35

Multi-Asset Futures Strategy Hy brid CSMF1ER 10/26/2011 2.38% 2.14% 3.98% 2.53% 0.34 0.27

MASTRO Hy brid CSMST4E 08/31/2010 0.65% -1.90% -2.42% -1.66% -0.31 -0.35

Sy stematic Tactical Asset Allocation Hy brid STAAUE 10/18/2013 0.05% 1.90% -0.34% -0.14% -0.07 -0.03

TEMPO Hy brid CSEATMP6 2/4/2014 -1.87% 3.63% 0.09% 0.28% 0.01 0.05

Portfolio Hedging

Equity Dy namic Tail Hedge SPX Index Equities CSEADTSP 12/15/2011 -0.04% -5.15% -6.25% -6.09% -3.58 -2.86

Cheapest Slide Index Equities CSEACHPS 8/12/2011 -0.75% -7.57% -10.54% -11.39% -0.73 -1.10

Adv anced Defensiv e Volatility Index Equities CSEAADVL 09/26/2012 -0.30% -4.92% -12.98% -10.20% -1.38 -1.15

Tail Risk Ov erlay Protection Strategy Interest Rates CSTSERUS 1/8/2011 -0.11% 1.14% 0.14% 2.57% 0.03 0.50

Liquid Alternative Beta

Liquid Alternativ e Beta Hy brid CSLAB 12/31/2009 0.45% 3.62% 4.16% 3.76% 0.95 0.62

Long/Short Liquid Index Equities CSLABLS 04/30/2008 0.46% -1.07% 2.99% 4.09% 0.44 0.40

Ev ent Driv en Liquid Index Hy brid CSLABED 12/31/2009 0.38% 8.28% 6.77% 5.37% 0.83 0.62

Merger Arbitrage Liquid Index Equities CSLABMA 12/31/2009 0.34% -1.23% 0.72% 1.51% 0.06 0.28

Managed Futures Liquid Index Hy brid CSLABMF 01/31/2011 0.45% 4.09% 1.85% 3.40% 0.15 0.32

RETURN SHARPE RATIO

Source: Credit Suisse

Note: Data as of 09/30/2016

Sharpe R at io : We calculate the Sharpe Ratio as the annualized average excess return divided by the annualized daily volat ility of the strategy. For excess return strategies, we simply use the raw strategy returns. For total return

strategies, we deduct the 1-month LIBOR for the currency in which the strategy is denominated. For more information, please visit us on Bloomberg at CSLI <GO>

Past performance should not be taken as an indicat ion or guarantee of future performance, and no representat ion or warranty, express or implied, is made regarding future performance. Information, opinions and est imates

contained in this report ref lect a judgment at the original date of publicat ion by CS and are subject to change without not ice. The price, value of and income from any of the securit ies or f inancial instruments mentioned in this report

can fall as well as rise. The value of securit ies and f inancial instruments may be subject to exchange rate f luctuat ion that may have a posit ive or adverse effect on the price or income of such securit ies or f inancial instruments. The P&L

results shown do not include relevant costs, such as commissions, interest charges, or other applicable expenses.

13 October 2016

Systematic Alpha Monthly 8

Research Spotlight: Credit Suisse Multi-Asset Trend Index Suite (MATRIX) Trend-following strategy takes advantage of a tendency that assets which have

outperformed will on average continue to have a better performance relative to peers, and

vice versa. This tendency, which is well-known as momentum, exhibits on various asset

markets. Many possible explanations for momentum exist, ranging from disequilibrium on the

market to investor irrationality. Trend can always be measured as positive autocorrelation of

asset prices, i.e., the asset price returns as positively correlated with the same asset’s

lagged return. Under the market environment when there’s a strong driver which causes the

upwards or downwards movement on asset prices, trend-following strategies perform well.

Moreover, those strategies can work as good diversifiers for risky asset portfolios under a

stressful environment.

Aiming to benefit from potential trends exhibited by a variety of assets, Credit Suisse has

developed the CS Multi-Asset Trend Index Suite. The suite contains three types of indices:

Single-Name Indices (SN Indices), which track trends of single types of assets, Single Class

Indices (SC Indices), which are baskets of SN Indices and track single asset class and

Multiple Asset Class Indices (MC Indices) tracking across several asset classes.

In Exhibit 1 and Exhibit 2 we plot one of the MC Indices, MTRXMLTL. This index is a basket

of equity SC Indices and bond SC Indices. We compare it with a group of trend-following

managed futures indices: NEIXCTA (SG CTA Index), BARCCTA (Barclay CTA Index) and

HEDGFUTR (Credit Suisse Managed Futures Liquidity Index). MTRXMLTL outperforms with

a higher Sharpe ratio of 1.25 and lower maximum drawdown of 7% since April 2002.

Exhibit 1: Cumulative Index Performance, Apr 2002 – Sep 2016

Exhibit 2: Performance Statistics, Apr 2002 – Sep 2016

Data as of Sep 30, 2016. Calculated on monthly basis. Data as of Sep 30, 2016

MTRXMLTL NEIXCTA BARCCTA HEDGFUTR

Annual Return

5.8% 5.6% 4.3% 6.5%

Annual Volatility

4.7% 8.2% 6.3% 11.6%

Sharpe Ratio

1.25 0.68 0.69 0.56

Max Drawdown

7% 12% 10% 17%

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

Methodology

The trend signals are generated on SN Index level. Each SN Index component of the

strategy utilizes the exponentially weighted moving averages (EWMA) of its underlying

futures series. We capture trends by comparing EWMA with different terms. In addition, we

adjust weights to inversely proportional to the trailing volatility of the underlying futures for

the purpose of volatility control.

For multi-asset trend harvester SC Indices and MC Indices, the portfolio reconstitution

occurs each month, representing baskets with weights set up to equal on rebalance date and

adjusted afterwards. The daily weight adjustment uses inverse-volatility weighting manner

within asset classes (for SC Indices) and across asset classes (for MC Indices). Meanwhile,

volatility target with leverage cap are applied for basket indices.

50

100

150

200

250

300

2002 2004 2006 2008 2010 2012 2014 2016

MTRXMLTL Index NEIXCTA Index

BARCCTA Index HEDGFUTR Index

13 October 2016

Systematic Alpha Monthly 9

Exhibit 3: Structure of CS Multi-Asset Trend Index Suite

Source: Credit Suisse

Performance Analysis

In Exhibit 4 and Exhibit 5, we plot the time spot when long/short momentum signals are

triggered and how these signals enhance the performance of MATRIX indices. Take two

long/short SN Indices as an example. MTRXSRXB has underlying Euro Bund rolling futures

and MTRXSESB has US S&P E-mini futures as underlying instruments. Both of the charts

show that the signals perform well in capturing the potential underlying trends. When a

strong upward/downward movement appears on the market, the long/short position is

triggered timely to chase positive returns or cut losses.

Exhibit 4: Momentum signal for MTRXSRXB, Apr 2002 – Sep 2016

Exhibit 5: Momentum signal for MTRXSRSB, Apr 2002 – Sep 2016

LHS: index level. RHS: Signal value. Data as of Sep 30, 2016. LHS: index level. RHS: Signal value. Data as of Sep 30, 2016.

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

Besides the efficiency of timing trends and gaining trend following returns, the strategy also

shows the feature of good risk diversification. Both of the advantages can be measured with

strength of correlations with benchmark indices. In the Exhibit 6 and 7, we plot 20 days and

180 days rolling correlation of SPX Index return with two MATRIX indices returns. Exhibit 6

shows MTRXSESB Index with S&P E-mini as underlying and Exhibit 7 shows MTRXCEQB

Index which is a SC Index with exposure on global equity market. When the market sells off,

as it did in during the financial crisis in 2008 and European debt crisis in 2011, the

correlations between MATRIX indices and benchmark index are negative, which shows the

delinking of those indices and market downside trend. On the other hand, the high positive

correlation when market is in risk on face could ensure the strategy will not miss upward

movements.

-1

-0.5

0

0.5

1

50

100

150

200

250

2002 2004 2006 2008 2010 2012 2014 2016

Momentum Long Signal

Momentum Short Signal

MTRXSRXB Index Value

Euro Bund Rolling Futures

-1

-0.5

0

0.5

1

50

100

150

200

250

2002 2004 2006 2008 2010 2012 2014 2016

Momentum Long SignalMomentum Short SignalMTRXSESB Index ValueS&P E-mini

13 October 2016

Systematic Alpha Monthly 10

Exhibit 6: 20- and 180-Day Rolling Correlations of MTRXSESB and SPX Index

Exhibit 7: 20- and 180-Day Rolling Correlations of MTRXCEQB and SPX Index

LHS: index level. RHS: rolling correlation. LHS: index level. RHS: rolling correlation.

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

Multi-Asset Trend Harvester Annual Performance

Exhibits 8 and 9 show the annual return and Sharpe ratio for MTRXMLTL, which is one of

MC Indices and has constituents of global bonds and equity futures. To compare with

MTRXMLTL, we construct a hypothetical combined 60/40 portfolio which consists of 60% of

stocks and 40% of bonds. We use the return of SPX Index as equity asset return and return

of US 10-year treasury index (ticker: BCEY4T) as bond asset return. The MATRIX suite has

multiple levels of volatility control process, which decrease the volatilities and annual

maximum drawdowns.

Exhibit 8: Annual Returns, Apr 2002 – Sep 2016 Exhibit 9: Annual Sharpe Ratios, Apr 2002 – Sep 2016

Data as of Sep 30, 2016. Data as of Sep 30, 2016.

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

-1.5

-1

-0.5

0

0.5

1

1.5

50

100

150

200

2003 2005 2007 2009 2011 2013 2015

20 Days Rolling Correlation

180 Days Rolling CorrelationMTRXSESB Index Value

SPX Index (normalized to same realized vol)

-1.5

-1

-0.5

0

0.5

1

1.5

50

70

90

110

130

150

2003 2005 2007 2009 2011 2013 2015

20 Days Rolling Correlation

180 Days Rolling Correlation

MTRXCEQB Index

SPX Index (normalized to the same realized vol)

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

200

2

200

3

200

4

2005

200

6

200

7

200

8

200

9

201

0

201

1

201

2

2013

201

4

201

5

201

6

MTRXMLTL Index Combined 60/40 Portfolio

-1

-0.5

0

0.5

1

1.5

2

2.5

3

200

2

200

3

200

4

200

5

200

6

200

7

2008

2009

2010

201

1

201

2

201

3

201

4

201

5

201

6

MTRXMLTL Index Combined 60/40 Portfolio

13 October 2016

Systematic Alpha Monthly 11

Overlaying to 60/40 Portfolio

We overlay MTRXMLTL to the hypothetical combined 60/40 portfolio with 60% stock and

40% bond allocation. From Exhibit 10 and 11 we can conclude that additional allocation of

CS MATRIX Index in the whole portfolio can enhance the performance with higher Sharpe

ratio and help investors earn extra profits.

Exhibit 10:Cumulative Index Performance, Apr 2002 – Sep 2016

Exhibit 11:Performance Statistics, Apr 2002 – Sep 2016

Data as of Sep 30, 2016. Data as of Sep 30, 2016.

60/40

Portfolio 60/40 Portfolio+

50% MTRXMLTL 60/40 Portfolio+

100% MTRXMLTL

Annual Return 7.1% 10.3% 13.6%

Annual Volatility 11.6% 12.4% 13.6%

Sharpe Ratio 0.61 0.76 0.91

Max Drawdown 33% 32% 32%

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

0

100

200

300

400

500

600

2002 2004 2006 2008 2010 2012 2014 2016

Combined 60/40 Portfolio

Combined 60/40 Portfolio + 50% MTRXMLTL

Combined 60/40 Portfolio + 100% MTRXMLTL

13 October 2016

Systematic Alpha Monthly 12

Strategy Snapshots

13 October 2016

Systematic Alpha Monthly 13

Smart Beta HS Global Style Rotation

Asset Class: Equities BBG Ticker: HSGSRTR

Strategy Overview

The HS Global Style Rotation Index invests according to investment styles that dominate at each

stage of the economic cycle as determined by the Credit Suisse Cycle Clock, an indicator that is a

measure of the output gap. The HOLT®1 framework is used to identify stocks with appropriate

characteristics for the relevant economic cycle stage. Expert financial ratios and rules are used to

pinpoint these qualities systematically.

Cumulative Index Performance Performance Summary

40

60

80

100

120

140

160

180

200

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Live date: October 2009

Sept 2016 YTD

Last 12-Mo.

Since Live

Return 0.57% 6.18% 9.97% 10.97%

Volatility 12.96% 15.13%

Sharpe Ratio 0.74 0.71

Draw dow n 12.20% 22.79%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World 96.8%

-21.8%

50.1%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 1.6% 0.8% 3.6% 5.1% 4.2% -0.7% -1.5% 0.9% 5.9% 2.9% -3.2% -0.9%

2008 -7.9% 1.0% -2.2% 3.0% 4.0% -8.1% 0.3% 0.0% -11.8% -19.4% -5.4% 4.4%

2009 -5.8% -8.7% 6.1% 10.5% 12.4% -0.8% 6.5% 2.7% 3.9% -0.5% 4.2% 2.6%

2010 -4.2% 1.0% 6.7% 0.1% -8.7% -2.5% 8.1% -4.0% 10.5% 4.8% -2.1% 7.1%

2011 2.2% 3.7% 1.1% 5.1% -1.0% -0.5% -1.6% -8.2% -10.1% 11.3% -1.3% -0.7%

2012 5.2% 4.1% 1.2% -2.2% -8.9% 3.9% 2.5% 2.6% 3.2% -0.5% 0.9% 1.6%

2013 6.4% -0.1% 2.5% 2.4% 0.3% -2.3% 6.4% -1.1% 5.5% 3.9% 2.1% 2.5%

2014 -3.8% 5.1% 0.5% 0.7% 3.4% 2.2% -1.9% 3.2% -2.8% 0.5% 1.6% -1.1%

2015 -2.3% 6.0% -1.3% 1.4% 1.3% -2.0% 2.5% -5.8% -3.6% 5.2% -0.9% -0.7%

2016 -5.2% 0.5% 6.2% 0.5% 1.3% 0.1% 3.4% -0.9% 0.6%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The HS Global Style Rotation Index (HSGSRTR Index) gained 0.6% in September 2016, while the MSCI World (TR) Index gained 0.5%. Year to date, the HS Global Style Rotation Index has increased by 6.2%, compared to a gain of 5.6% for the MSCI World (TR) Index. Over the month, the highest contribution came from the Health Care, Financials and Real Estate sectors which had weightings of 18%, 9% and 1% respectively, as of 31 August 2016. Consumer Staples, Consumer Discretionary and Telecommunication Services had the largest negative impact on the performance of the index. Across countries, Japan, Britain and Switzerland generated the highest contributions in September. United States, Denmark and Germany had the largest negative impact on the performance of the index. Over the month, the best and worst performing stocks were Mitsubishi Tanabe Pharma (Health Care) and Cognizant Tech Solutions (Information Technology), respectively. The index was last rebalanced in August 2016 and is due to be rebalanced again in November 2016.

For more information regarding this index, please contact the Equities SIS Product Management team at [email protected].

1 HOLT® is Credit Suisse’s corporate performance and valuation financial advisory service.

13 October 2016

Systematic Alpha Monthly 14

HS Global Style Rotation Equity Hedged

Asset Class: Equities BBG Ticker: HSGSREH

Strategy Overview

The HS Global Style Rotation Equity Hedged Index goes short the MSCI World Index against a

long position in the HS Global Style Rotation Index to have a net exposure of zero. The index is

rebalanced quarterly.

Cumulative Index Performance Performance Summary

100

110

120

130

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Live date: April 2010

Sept 2016 YTD

Last 12-Mo.

Since Live

Return -0.03% -0.19% -1.99% 1.19%

Volatility 3.60% 3.26%

Sharpe Ratio -0.55 0.36

Draw dow n 2.87% 6.55%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World -53.5%

13.8%

-41.9%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 0.4% 1.3% 1.7% 0.7% 1.3% 0.0% 0.6% 0.8% 1.1% -0.2% 0.8% 0.3%

2008 -0.4% 1.3% -1.4% -2.4% 2.2% -0.3% 2.4% 1.2% 0.0% -0.5% 1.1% 1.2%

2009 2.7% 1.6% -1.3% -1.0% 2.9% -0.4% -1.9% -1.5% -0.2% 1.4% 0.1% 0.8%

2010 -0.1% -0.5% 0.5% 0.0% 0.8% 0.8% 0.0% -0.3% 1.0% 1.1% 0.1% -0.3%

2011 -0.1% 0.1% 2.0% 0.8% 0.9% 1.0% 0.1% -1.4% -1.5% 0.7% 1.1% -0.7%

2012 0.1% -0.9% -0.1% -1.2% -0.3% -1.2% 1.1% 0.0% 0.4% 0.1% -0.5% -0.4%

2013 1.2% -0.3% 0.1% -0.9% 0.2% 0.1% 1.0% 1.0% 0.5% 0.0% 0.2% 0.4%

2014 -0.2% 0.1% 0.3% -0.4% 1.3% 0.4% -0.4% 1.0% -0.2% -0.2% -0.4% 0.5%

2015 -0.6% 0.1% 0.2% -1.0% 0.9% 0.2% 0.6% 0.8% 0.0% -2.5% -0.5% 1.0%

2016 0.6% 1.2% -0.6% -1.2% 0.6% 1.1% -0.8% -1.1% 0.0%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The HS Global Style Rotation Equity Hedged Index (HSGSREH Index) lost 0.1% in September 2016. Over the same period, the MSCI World (Price) Index gained 0.4%. Year to date, the HS Global Style Rotation Equity Hedged Index declined by 0.2% while the MSCI World (Price) Index gained 3.8%. Over the month and on the long component of the index, the highest contribution came from the Health Care, Financials and Real Estate sectors which had weightings of 18%, 9% and 1% respectively, as of 31 August 2016. Consumer Staples, Consumer Discretionary and Telecommunication Services had the largest negative impact on the performance of the index. Across countries, Japan, Britain and Switzerland generated the highest contributions in September. United States, Denmark and Germany had the largest negative impact on the performance of the index. Over the month and on the long component of the index, the best and worst performing stocks were Mitsubishi Tanabe Pharma (Health Care) and Cognizant Tech Solutions (Information Technology), respectively. The long component of the index was last rebalanced in August 2016 and is due to be rebalanced again in November 2016.

For more information regarding this index, please contact the Equities SIS Product Management

team at [email protected].

13 October 2016

Systematic Alpha Monthly 15

HS Market Neutral Index Powered by HOLT®

Asset Class: Equities BBG Ticker: HSGMN

Strategy Overview

The HS Market Neutral Index Powered by HOLT® uses a strategy popular with hedge funds, with

the main aim of achieving stable returns: the emphasis is on reducing risk rather than maximizing

outperformance. Approximately 75 stocks are held on the expectation that their share prices will

go up (long position) and the same number of stocks are held on the expectation that their share

prices will go down (short position). Companies included typically exhibit strong/weak cash flows,

are undervalued/overvalued, and experience positive/negative investor sentiment. HOLT® uses

expert financial ratios and rules to pinpoint these characteristics systematically.

Cumulative Index Performance Performance Summary

85

90

95

100

105

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Live date: September 2007

Sept 2016 YTD

Last 12-Mo.

Since Live

Return 0.18% -5.14% -4.88% -1.39%

Volatility 4.56% 5.42%

Sharpe Ratio -1.07 -0.26

Draw dow n 7.58% 15.44%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World 19.3%

-42.7%

15.9%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 0.0% 0.2% -0.6% 2.9% 1.0% -1.4% 1.1% -0.9% -1.3% -1.0% -2.3% 0.6%

2008 0.2% -2.7% 1.4% -2.3% 0.9% -2.3% -0.5% -0.8% -1.5% 1.2% 1.2% -0.1%

2009 2.0% -1.1% -1.4% -2.0% 5.8% -2.5% -1.7% 3.1% -2.8% -0.2% 0.9% -2.0%

2010 0.2% -0.6% 2.9% 0.3% -1.5% -1.1% 1.8% 1.4% 2.2% 0.9% -0.4% 0.6%

2011 1.8% -0.7% 1.1% 0.7% -0.4% -0.5% -1.3% -0.9% -1.0% 2.1% -2.4% 1.2%

2012 0.0% -1.3% -2.7% 1.4% -0.3% -1.5% 1.3% -0.7% 1.4% 1.4% 0.1% 1.6%

2013 2.3% -0.6% -1.7% 2.1% 1.0% -2.4% 1.3% -0.7% -1.4% 0.1% 2.0% 0.1%

2014 0.0% 1.7% 1.2% -0.4% -1.7% -0.7% -0.8% -0.9% -1.1% -0.2% -0.4% -1.6%

2015 -1.4% 0.4% 0.8% -0.2% 2.2% 0.9% -1.8% -0.5% -1.3% -1.0% 1.2% -0.1%

2016 -2.0% -2.0% 0.3% 0.8% 0.8% -3.4% -0.9% 1.1% 0.2%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The HS Market Neutral Index (HSGMN) gained 0.2% in September 2016. Over the same time period, the HFRX Equity Market Neutral Index (HFRXEMN) gained 0.5%. Year to date, the HS Market Neutral Index declined by 5.1% while the HFRXEMN Index declined by 3.8%. The index was rebalanced in early September 2016 and will be rebalanced again in December 2016. Across regions, Germany, Italy and Japan were the best performing geographies in September. Spain, France and South Africa had the largest negative impact on the performance of the index. Consumer Discretionary, Financials and Information Technology were the best performing sectors, while Industrials, Health Care and Real Estate had the largest negative impact on the performance of the index. With regards to the legs of the index, the long side generated positive contribution and the short side of the index produced a negative return.

For more information regarding this index, please contact the Equities SIS Product Management

team at [email protected].

13 October 2016

Systematic Alpha Monthly 16

Global Enhanced Momentum Strategy

Asset Class: Interest Rates BBG Ticker: CSGMEREU

Strategy Overview

The Global Enhanced Momentum Strategy (GEMS) uses a systematic trend-following mechanism

to allocate daily long/short positions in interest rate swaps (one-, two-, and five-year) across four

different yield curves (USD, EUR, CHF, and GBP).

Cumulative Index Performance Performance Summary

90

100

110

120

130

140

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Live date: January 2012

Sept 2016 YTD

Last 12-Mo.

Since Live

Return -0.51% -0.32% -1.00% -0.28%

Volatility 1.78% 1.61%

Sharpe Ratio -0.56 -0.17

Draw dow n 1.67% 2.92%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World -11.5%

30.0%

-21.3%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 0.6% -0.4% -0.7% -0.1% 1.0% 0.7% -0.4% 0.9% 0.9% -0.1% 1.6% -0.3%

2008 3.0% 0.2% -1.0% -0.7% 2.1% 1.1% 0.4% 0.9% 0.3% 4.6% 5.4% 3.3%

2009 1.5% -0.2% 0.5% 0.0% 0.3% -1.6% 0.7% 1.0% 0.9% -0.1% 0.3% -0.9%

2010 0.1% 1.3% 0.1% -0.5% 0.7% 0.4% 0.3% 0.8% -0.4% 0.1% -0.9% 0.2%

2011 -0.2% 0.0% -0.3% 0.4% 0.8% 0.5% 1.3% 1.5% 0.0% -0.6% -0.5% 0.0%

2012 0.7% -0.3% -0.7% -0.5% 0.5% 0.0% 1.1% 0.0% 0.0% -0.1% 0.2% 0.0%

2013 -0.2% -0.5% 0.0% 0.5% -0.6% 0.7% -0.9% -0.7% 0.0% 0.6% 0.2% -0.4%

2014 -0.3% -0.1% -0.3% -0.4% 0.3% -0.2% 0.0% 0.3% 0.1% 0.2% 0.4% 0.3%

2015 1.0% -0.6% -0.2% -0.3% -0.1% -0.2% -0.4% 0.2% 0.3% 0.2% -0.2% -0.7%

2016 0.3% 0.7% -0.6% -0.3% -0.5% 1.0% -0.2% -0.2% -0.5% Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

CSGEMS was affected by the choppiness in the rates market for September and fell by 51 bps over the month. Rates markets across the globe exhibited volatility for most of the month and with no clear trend to latch on to some of the swaps switched positions during the month. Rates have started trending lower towards the end and the swaps have correctly positioned themselves into receivers, but this positioning was not sufficient to counter the negative influence on the strategy from the choppy rate markets leading up until then.

For more information regarding this index, please contact the European Rates Structuring team at

13 October 2016

Systematic Alpha Monthly 17

GAINS 01E

Asset Class: Commodities BBG Ticker: CSGADER

Strategy Overview

Credit Suisse GAINS uses market information from Glencore, one of the world’s largest

commodity traders, to reweight the allocation of individual commodities dynamically in a

commodity index. Using “votes” from the commodity trading units, the index determines the

adjusted weights based on the commodity traders’ outlook on the physical market for each

commodity. The CS GAINS methodology can be applied to any commodity benchmark, including

BCOMSM, S&P GSCITM, and to a static index weighted by the relative importance of Glencore’s

underlying physical businesses. GAINS 01E is the BCOM benchmarked excess return index.

Cumulative Index Performance Performance Summary

80

100

120

140

160

180

Oct-08 Oct-10 Oct-12 Oct-14

Live date: October 2008

Sept 2016 YTD

Last 12-Mo.

Since Live

Return 3.32% 8.30% -0.56% 0.33%

Volatility 14.22% 15.22%

Sharpe Ratio -0.04 0.02

Draw dow n 17.69% 53.68%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World 49.6%

8.5%

91.6%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2008 0.5% 4.0%

2009 -0.1% -1.9% 4.6% 2.3% 13.0% -2.4% 1.2% 1.0% -0.4% 2.8% 4.4% 1.5%

2010 -7.1% 4.0% 0.4% 2.7% -7.7% -0.4% 6.6% -1.3% 7.8% 6.1% -0.6% 11.4%

2011 0.9% 1.8% 2.4% 3.2% -5.6% -5.7% 3.4% 2.7% -15.3% 7.1% -2.0% -2.3%

2012 3.3% 2.1% -4.2% 0.1% -8.5% 6.1% 6.3% 4.3% 0.8% -3.9% -0.3% -3.1%

2013 2.7% -3.9% 1.4% -2.8% -2.0% -4.7% 1.4% 3.0% -2.6% -0.8% -1.1% 1.1%

2014 0.9% 6.1% 0.6% 2.7% -2.5% 0.6% -4.8% -0.7% -6.0% -1.3% -3.6% -7.5%

2015 -3.1% 2.0% -4.6% 4.4% -2.1% 1.7% -10.2% -1.2% -3.4% -0.6% -6.7% -2.1%

2016 -1.1% -1.8% 3.8% 7.4% -0.7% 4.1% -4.5% -1.9% 3.3%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The Credit Suisse GAINS 01E Index returned 3.32% during the month. The first September-week saw a strong rally of crude oil and products on the back of larger-than-expected inventory decreases, a function of the production and logistics disruptions caused by the tropical storm Hermine. Gains were reversed fully the week

after unfortunately. Low demand growth specifically out of Asia was reported by the IEA, paired with an expectation of a prolonged S&D surplus given insufficiently elastic production figures. Price action then flattened in expectation of the OPEC meeting in Algiers on Sep 28. The 14 members agreed to cap production at 32.5 –

33Mb/d in 2017, causing an extended crude rally. The Philippines authorities completed their audit and based on environmental concerns the market priced in further mine closures, supporting Nickel prices specifically. The sector could not entirely emancipate itself from the US Federal Reserve’s rate hike expectations either, yet

following the release of the Fed’s minutes (no rate increase and a de-emphasis of future hike expectations), fundamentals quickly took hold again. Base Metals ended the month ~5% higher. Gold and Silver trade in line with expected central bank action. Both metals proved sensitive to the re-rating of rate hike expectations in the

US and the lack of additional stimulus from the ECB. Overall, the sector finished 0.70% higher after being up 3.75% earlier in the month. With Brazil facing drought and potential frost, Corn and Sugar yield expectations have been reduced, supporting prices. The WASDE report published on September 12 showed higher-than-

expected production of Soybean, leading to temporary weakness in Soybean and Bean Oil.

For more information regarding this index, please contact Mi-Sonn Kim ([email protected]) in Commodities Sales.

13 October 2016

Systematic Alpha Monthly 18

Commodity Backwardation

Asset Class: Commodities BBG Ticker: CSCUBKER

Strategy Overview

The CS Commodity Backwardation Index dynamically allocates to selected components

displaying the highest degree of backwardation in their curve structure, aiming to capture the

commodities with the tightest supply/demand balance in the investment universe.

Cumulative Index Performance Performance Summary

80

140

200

260

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Live date: March 2012

Sept 2016 YTD

Last 12-Mo.

Since Live

Return 2.38% 4.56% 3.15% -7.73%

Volatility 12.28% 11.45%

Sharpe Ratio 0.26 -0.67

Draw dow n 11.64% 43.26%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World 47.5%

6.6%

64.7%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 -2.3% 5.5% 2.1% 6.1% 1.5% -2.0% 5.7% -4.8% 6.6% 3.4% -3.5% 1.7%

2008 3.6% 12.6% -5.0% 7.2% 6.8% 7.8% -8.1% -3.8% -7.9% -23.2% -4.9% 6.3%

2009 -0.6% -2.4% 7.1% 1.7% 13.7% -0.6% 7.2% 4.1% 2.4% 3.1% 3.9% 1.4%

2010 -4.9% 3.2% 1.7% 4.7% -6.0% -1.5% 3.6% 1.6% 9.5% 9.6% 0.0% 12.5%

2011 4.2% 6.7% 1.1% 1.9% -3.9% -2.0% 3.8% -1.6% -14.7% 7.5% -0.2% -2.4%

2012 7.4% 5.6% -0.8% -2.6% -9.7% 3.6% 6.5% 7.7% 0.1% -3.8% 1.0% -2.3%

2013 3.2% -2.6% 0.5% -3.0% 0.2% -2.7% 2.4% 2.5% -2.5% -0.5% -0.4% -0.6%

2014 -1.1% 4.2% 1.7% 1.6% -0.9% 0.5% -4.7% -0.8% -5.0% -4.3% -4.8% -7.1%

2015 -1.7% -0.4% -0.9% 5.4% -2.6% -0.5% -6.9% -2.9% -3.5% 3.0% -5.9% 1.1%

2016 -3.7% 4.1% 1.5% 6.3% -3.2% 3.0% -1.9% -3.4% 2.4%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The Credit Suisse Backwardation Index returned 2.38% during the month. The first September-week saw a strong rally of crude oil and products on the back of larger-than-expected inventory decreases, a function of the production and logistics disruptions caused by the tropical storm Hermine. Gains were reversed fully the week after unfortunately. Low demand growth specifically out of Asia was reported by the IEA, paired with an expectation of a prolonged S&D surplus given insufficiently elastic production figures. Price action then flattened in expectation of the OPEC meeting in Algiers on Sep 28. The 14 members agreed to cap production at 32.5 – 33Mb/d in 2017, causing an extended crude rally. The Philippines authorities completed their audit and based on environmental concerns the market priced in further mine closures, supporting Nickel prices specifically. The sector could not entirely emancipate itself from the US Federal Reserve’s rate hike expectations either, yet following the release of the Fed’s minutes (no rate increase and a de-emphasis of future hike expectations), fundamentals quickly took hold again. Base Metals ended the month ~5% higher. Gold and Silver traded in line with expected central bank action. Both metals proved sensitive to the re-rating of rate hike expectations in the US and the lack of additional stimulus from the ECB. Overall, the sector finished 0.70% higher after being up 3.75% earlier in the month. With Brazil facing drought and potential frost, Corn and Sugar yield expectations have been reduced supporting prices. The WASDE report published on September 12 showed higher-than-expected production of Soybean, leading to temporary weakness in Soybean and Bean Oil.

For more information regarding this index, please contact Mi-Sonn Kim (mi-sonn.kim@credit-

suisse.com) in Commodities Sales.

13 October 2016

Systematic Alpha Monthly 19

Alternative Risk Premia

Global Carry Selector

Asset Class: Equities BBG Ticker: GCSCS

Strategy Overview

The Credit Suisse Global Carry Selector Index is an equity volatility arbitrage strategy that

extracts the equity risk premium embedded in the option prices of four global indices (S&P 500,

DJ Euro Stoxx 50, DAX, and Nikkei 225), while attempting to deliver a low beta to the equity

market. The strategy systematically sells variance swaps and opportunistically buys forward

variances as a hedge.

Cumulative Index Performance Performance Summary

80

120

160

200

240

280

320

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Live date: January 2009

Sept 2016 YTD

Last 12-Mo.

Since Live

Return 3.42% -1.17% 7.45% 10.02%

Volatility 13.37% 19.98%

Sharpe Ratio 0.52 0.49

Draw dow n 10.40% 35.39%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World 8.0%

0.2%

9.5%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 2.2% -5.2% 0.7% 1.6% 5.5% -0.6% -0.7% 7.3% 0.0% 6.1% 5.4% -0.2%

2008 -10.2% 0.1% 6.2% -0.2% 2.4% 1.1% -3.6% 0.8% -7.6% 5.0% 6.9% -1.2%

2009 6.1% 2.7% -1.4% 0.5% 0.9% 0.3% 1.6% 0.6% 6.1% -5.4% 3.8% 2.9%

2010 -1.2% 2.4% 5.2% -1.5% -13.5% -4.2% 9.5% 3.8% 3.9% 5.5% -4.4% 7.5%

2011 1.0% 4.1% 5.7% 6.0% 1.1% 5.6% 3.8% 1.4% -0.2% 4.6% 1.8% 0.3%

2012 7.1% 7.5% 1.2% 1.5% -1.7% 3.8% 0.0% 1.0% 2.8% -1.2% 4.7% 0.4%

2013 3.7% -2.0% -1.6% 2.4% -1.0% -0.6% 1.9% -7.4% 1.2% 1.9% 0.3% -0.9%

2014 -8.3% 2.9% -2.0% 3.2% 2.3% 1.2% 0.8% -3.4% 3.3% -7.4% 0.2% -5.8%

2015 5.2% 6.3% -0.9% 2.7% 4.5% 0.4% -4.1% -15.7% -12.8% 2.5% 2.4% 3.0%

2016 -2.0% 1.6% -0.1% -6.4% 4.0% -5.3% 0.9% 3.2% 3.4%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The Credit Suisse Global Carry Selector Index (“the Index”) delivered a positive performance of

+3.4% for September. From the August roll date (19 August 2016), the Index was short a variance

swap in the Nikkei 225 Index with a volatility strike of 20.30%. The Index had no long volatility

position as of the August roll date. These positions delivered a positive return of +2.4% to the

Index in September to the roll date. On the most recent roll date (16 September 2016), the Index

was short a variance swap in the Eurostoxx 50 Index with a volatility strike of 19.74%. The Index

had no long volatility position as of the latest roll date. These positions delivered a positive return

of +1.0% to the Index in September from the roll date..

For more information regarding this index, please contact the Equities SIS Product Management

team at [email protected].

13 October 2016

Systematic Alpha Monthly 20

Global Carry Selector II

Asset Class: Equities BBG Ticker: GCSCS2

Strategy Overview

The Credit Suisse Global Carry Selector II is an equity volatility arbitrage strategy that extracts the

equity risk premium embedded in the option prices of four global indices (S&P 500, DJ Euro Stoxx

50, DAX, and Nikkei 225) while attempting to deliver a low beta to the equity market. The strategy

systematically sells variance swaps and opportunistically buys forward variances as a hedge. It

succeeds the Global Carry Selector Index, launched in January 2009.

Cumulative Index Performance Performance Summary

80

100

120

140

160

180

200

220

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Live date: June 2012

Sept 2016 YTD

Last 12-Mo.

Since Live

Return 1.21% -0.41% -0.94% -2.08%

Volatility 10.38% 8.94%

Sharpe Ratio -0.14 -0.26

Draw dow n 10.36% 21.83%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World 5.6%

7.6%

4.4%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 0.9% -1.2% -0.7% 0.7% 1.6% 0.0% -1.1% 1.8% -0.1% 2.2% 0.6% 1.9%

2008 -3.8% 0.4% -0.8% 1.0% 0.4% 0.5% 1.4% 1.5% -2.4% 9.1% 3.4% 0.9%

2009 -0.8% 2.2% 0.7% 0.7% 2.0% 1.5% 2.1% 0.6% 1.8% -1.3% 1.0% 3.1%

2010 -1.3% 0.5% 3.1% -3.2% 0.8% -3.1% 5.2% 1.6% 2.5% 2.7% -1.8% 3.5%

2011 1.6% 0.8% 0.0% 1.9% 0.7% -0.7% 1.3% 8.3% 1.1% -0.5% 3.0% 1.7%

2012 2.6% 2.0% 1.5% -0.2% 0.9% 4.4% -0.5% 0.5% 1.8% 0.5% 0.3% -0.3%

2013 1.0% -2.1% 0.5% -1.4% -3.7% -3.4% 2.3% -1.5% 2.0% 1.3% 0.3% 1.0%

2014 -2.1% 1.9% 0.2% 1.7% 1.6% 0.8% -1.3% 0.0% 0.6% -6.0% 0.1% 0.4%

2015 -3.6% 4.0% -0.3% 0.2% 0.8% 2.5% -1.8% -6.6% -1.8% 0.2% 0.7% -1.8%

2016 -8.0% 9.8% 0.2% -1.9% 2.6% -6.7% 2.0% 1.4% 1.2%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The Credit Suisse Global Carry Selector II Index (the "Index") delivered a positive return of +1.2% for

September. On the August roll date (19 August 2016), the Index was short a variance swap in the

Eurostoxx 50 Index with a volatility strike of 22.15%, in addition to the existing short variance swap

positions in the Eurostoxx 50 Index with a volatility strike of 31.17% and in the S&P 500 Index with a

volatility strike of 14.84% (with one and two months remaining, respectively). The Index had no long

volatility position as of the August roll date. These positions delivered a negative return of -0.4% in

September to the roll date. On the most recent roll date (16 September 2016), the Index was short a

new variance swap in the Nikkei 225 Index with a volatility strike of 24.73%, in addition to the

existing short variance swap positions in the S&P 500 Index with a volatility strike of 14.84% and in

the Eurostoxx 50 Index with a volatility strike of 22.15% (with one and two months remaining,

respectively). The Index had no long volatility position as of the latest roll date. These positions

delivered a positive return of +1.7% to the Index in September from the roll date.

For more information regarding this index, please contact the Equities SIS Product Management

team at [email protected].

13 October 2016

Systematic Alpha Monthly 21

Advanced Relative Value Volatility Index

Asset Class: Equities BBG Ticker: CSEAARVL

Strategy Overview

The Credit Suisse Advanced Relative Value Volatility Index aims to capture the term premium or

discount embedded in the carry (roll yield) of the S&P 500 VIX futures curve based on the

expected decay at the short- and medium-term of the VIX futures curve. The index maintains a

limited exposure to the absolute level of the VIX index by entering into a long or short position in

the S&P 500 VIX Short-Term Futures Index ER (Bloomberg: SPVXSP), while taking an opposite

position in the S&P 500 VIX Medium-Term Futures Index. It incorporates a loss-control

mechanism.

Cumulative Index Performance Performance Summary

80

100

120

140

160

180

200

Apr-08 Apr-10 Apr-12 Apr-14 Apr-16

Live date: September 2012

Sept 2016 YTD

Last 12-Mo.

Since Live

Return -0.73% 6.80% 2.01% -3.63%

Volatility 6.78% 6.22%

Sharpe Ratio 0.30 -0.58

Draw dow n 6.73% 22.65%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World 42.3%

-16.7%

12.7%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2008 2.9% -2.6% -1.1% 1.1% 2.1% 13.1% 0.0% 0.5%

2009 -0.2% 0.3% 0.1% 1.6% 0.0% 1.0% 1.5% 1.2% 2.8% 0.3% 1.5% 1.9%

2010 0.2% 0.7% 3.6% 1.4% -1.4% -0.8% 3.2% 2.2% 3.2% 2.4% 0.1% 1.7%

2011 0.4% -1.3% -1.5% 3.3% 0.4% -1.0% -1.7% 6.6% 2.2% -1.6% 0.3% 0.6%

2012 3.7% 1.3% 4.7% -1.1% -2.0% 3.7% -0.7% 1.9% 0.2% -1.5% 0.8% -0.8%

2013 -1.7% -0.7% 2.4% -2.4% 0.7% -1.4% 2.6% -1.2% 0.4% -1.2% 1.2% -2.2%

2014 -0.5% -2.0% -0.4% -0.1% 2.9% 0.8% -1.7% -1.0% -1.2% -3.1% 1.3% -4.0%

2015 -1.4% 2.1% 1.2% 1.8% 1.3% -2.3% 0.0% -5.0% -0.9% -1.0% -1.5% -2.1%

2016 -0.7% -1.8% 3.6% 1.8% 2.9% -4.2% 3.8% 2.2% -0.7%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

Advanced RVOL was down 0.73% in September (SPVXSP Index: -4.63%, SPVXMP Index: -

3.17%). The index had average position of -20% / 20% weights on the short-term and mid-term

VIX future Index as VIX future curve remained in contango during the month. Advanced RVOL

was down as volatility increased due to uncertainty ahead of BOJ/Fed meeting causing short-term

future Index to increase more than mid-term future Index.

For more information regarding this index, please contact US Equity Derivatives Structuring at

13 October 2016

Systematic Alpha Monthly 22

Mean Reversion Index on Euro Stoxx 50

Asset Class: Equities BBG Ticker: CSEAMREU

Strategy Overview

The Credit Suisse Mean Reversion Index aims to provide direct exposure to weekly mean

reversion on the Euro Stoxx 50 Index through a liquid and transparent strategy. The index isolates

exposure to mean reverting behavior by adjusting its exposure based on the prevailing volatility

regime.

Cumulative Index Performance Performance Summary

100

120

140

160

180

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Live date: March 2013

Sept 2016 YTD

Last 12-Mo.

Since Live

Return 0.56% 10.93% 11.38% 3.44%

Volatility 7.82% 7.72%

Sharpe Ratio 1.40 0.41

Draw dow n 3.83% 10.64%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World 13.0%

11.6%

17.0%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 2.7% -0.1% 2.2% -0.8% 0.2% 2.6% 0.4% 3.4% 1.0% 0.0% 0.3% 0.6%

2008 -3.8% 5.5% 0.6% -0.5% 0.9% -2.4% 0.8% 1.7% 5.9% -1.9% 1.5% 3.7%

2009 -1.1% -1.5% -1.9% 1.5% 0.4% 1.7% -3.3% 0.7% 0.7% -1.0% -0.5% 1.9%

2010 -2.0% 1.4% -0.9% 2.9% 2.0% -0.9% 1.9% -0.3% -0.5% -0.3% 0.1% 0.8%

2011 0.8% 2.0% -1.2% -1.9% 2.0% 2.2% 2.0% -5.8% 5.2% 3.7% 2.6% -0.4%

2012 -0.4% 0.8% 0.8% 0.3% 0.6% 2.7% 6.2% -0.2% -1.2% 4.3% 0.3% -0.6%

2013 0.4% 2.1% -0.4% 4.2% -1.7% 1.7% -1.2% 0.0% -2.2% -0.3% 0.4% -0.7%

2014 0.0% -1.4% 1.9% -0.1% 0.7% 0.6% 1.7% -2.9% 0.5% -4.5% 0.0% 1.3%

2015 0.0% -1.1% 1.1% 1.5% 0.7% 0.5% -1.3% -1.8% 2.8% -2.5% 0.9% 2.2%

2016 0.3% 2.1% 0.9% -1.4% -0.3% 7.5% -0.2% 1.1% 0.6%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The Credit Suisse Mean Reversion on EuroSTOXX50 Index delivered a positive return of 0.6% in

September while the underlying price return index on the EuroSTOXX50 finished the month with a

negative performance of -0.7%. The index started the month slightly negative as European equity

markets initially trended upwards. A sharp reversal temporarily brought the index into the black,

however the strategy fell back to negative territory as the Eurostoxx 50 continued to fall lower.

Finally, several big swings in the Eurostoxx 50 towards the end of month enabled the index to

recover and end the month positively.

For more information regarding this index, please contact the Equities SIS Product Management

team at [email protected].

13 October 2016

Systematic Alpha Monthly 23

Dividend Alpha Index on Euro Stoxx 50

Asset Class: Equities BBG Ticker: CSEADVAE

Strategy Overview

The Credit Suisse Dividend Alpha Index invests in Euro Stoxx 50 dividend futures to

systematically harvest the embedded dividend risk premium. The index looks to isolate the

dividend risk premium by going long the two front futures contracts and stripping out the portion of

the return attributable to equity price action with an offsetting position in the Euro Stoxx 50 price

index.

Cumulative Index Performance Performance Summary

60

80

100

120

140

160

180

Jul-08Jul-09Jul-10Jul-11Jul-12Jul-13Jul-14Jul-15Jul-16

Live date: October 2013

Sept 2016 YTD

Last 12-Mo.

Since Live

Return 1.28% 4.10% 3.69% 1.39%

Volatility 3.00% 3.96%

Sharpe Ratio 1.23 0.35

Draw dow n 2.16% 5.74%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World -11.0%

17.2%

-6.3%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2008 1.9% -1.0% -18.5% 12.1% -2.6%

2009 -1.2% 9.2% -0.4% 3.6% 3.6% 4.1% 7.0% -0.3% 4.3% 3.7% 4.0% 2.0%

2010 2.0% -1.3% 0.7% 0.7% -4.7% -2.0% 4.4% 2.6% 2.6% -0.9% -0.6% -0.4%

2011 3.1% 1.6% 0.6% -0.1% -0.3% -0.1% 0.1% -1.3% 5.5% -3.9% -0.7% -0.4%

2012 7.1% 4.4% -1.4% 1.2% -1.0% 1.0% -7.1% 5.2% 1.5% 3.2% -0.3% -1.2%

2013 1.0% 0.6% 0.0% 1.9% 1.0% -2.8% 0.1% 1.6% 0.3% -0.1% -0.3% 0.9%

2014 1.2% -0.3% 0.1% -0.3% -1.3% -0.8% 0.8% -0.3% 1.4% -2.0% 2.6% -1.4%

2015 -2.1% 3.7% 1.0% 1.1% 0.5% -0.6% 0.4% -2.3% -1.5% -0.4% 0.0% 0.0%

2016 0.6% 2.3% 1.1% 0.1% -0.1% -0.8% -0.2% -0.3% 1.3% Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The Credit Suisse Dividend Alpha Total Return Index delivered a positive return of +1.3% in September, while European equities performed negatively, with the EuroSTOXX50 Total Return Index losing -0.6%. At the beginning of the month, the dividend exposure was 29% in the 2016 dividend future with the remaining 71% in the 2017 dividend future. The index's performance was primarily driven by the performance of the 2017 dividend future, which gained +1.0% during the month, in contrast to the 2016 dividend future which gained +0.4% over the same period. The beta hedging component had a positive contribution to the Index in September (+0.5%).

For more information regarding this index, please contact the Equities SIS Product Management

team at [email protected].

13 October 2016

Systematic Alpha Monthly 24

Adaptive Volatility Index Global

Asset Class: Interest Rates BBG Ticker: CSVIXAEU

Strategy Overview

The Adaptive Volatility Index exploits the bias between implied and realized volatility in global

interest rate options markets (USD, EUR, JPY) by selling one-month into ten-year swaptions and

delta-hedging until expiry. The strategy aims to improve risk-adjusted returns by adjusting its

leverage based on the prevailing volatility environment. Four versions of CSAVI are available, one

for each market (USD, EUR and JPY) and CSAVI Global, which combines the three strategies

based on equal weighting.

Cumulative Index Performance Weekly Correlation with Benchmarks

Last 12 months

MSCI World 30.2%

-3.4%

-2.2%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016

Source: Credit Suisse; Data as of 09/30/2016

Performance Summary

CSAVI Global (CSVIXAEU) Sept 2016 YTD Last 12-Mo. Since Live (Sep 2012)

Return 0.58% 3.24% 4.93% 2.37%

4.07% 4.06%

1.21 0.58

3.07% 7.53%

Volatility

Sharpe Ratio

Drawdown

CSAVI USD (CSVIXUSD) Sept 2016 YTD Last 12-Mo. Since Live (Mar 2009)

Return 0.67% 6.15% 8.42% 12.89%

5.69% 9.28%

1.48 1.39

3.88% 17.28%

Volatility

Sharpe Ratio

Drawdown

CSAVI EUR (CSVIXEUR) Sept 2016 YTD Last 12-Mo. Since Live (Sep 2012)

Return -1.20% 6.44% 6.70% 4.42%

5.12% 6.12%

1.31 0.72

3.16% 10.07%

Volatility

Sharpe Ratio

Drawdown

CSAVI JPY (CSVIXJPY) Sept 2016 YTD Last 12-Mo. Since Live (Jan 2011)

Return 2.28% -2.81% -1.45% 1.99%

5.82% 6.44%

-0.25 0.31

5.92% 20.14%

Volatility

Sharpe Ratio

Drawdown

Source: Credit Suisse; Note: Data as of 09/30/2016

September 2016 Performance Commentary

The Adaptive Volatility Index Global gained 0.58% in September. The USD and JPY sub-

strategies gained 0.67% and 2.28%, respectively; the EUR sub-strategy lost 1.2%. The leverage

ratio is 0.5 for USD and EUR; and 0.5 for JPY most of the time in September, except 1.0 for the

20th

roll day.

For more information regarding this index, please contact the European Rates Structuring team at

50

100

150

200

250

300

350

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

13 October 2016

Systematic Alpha Monthly 25

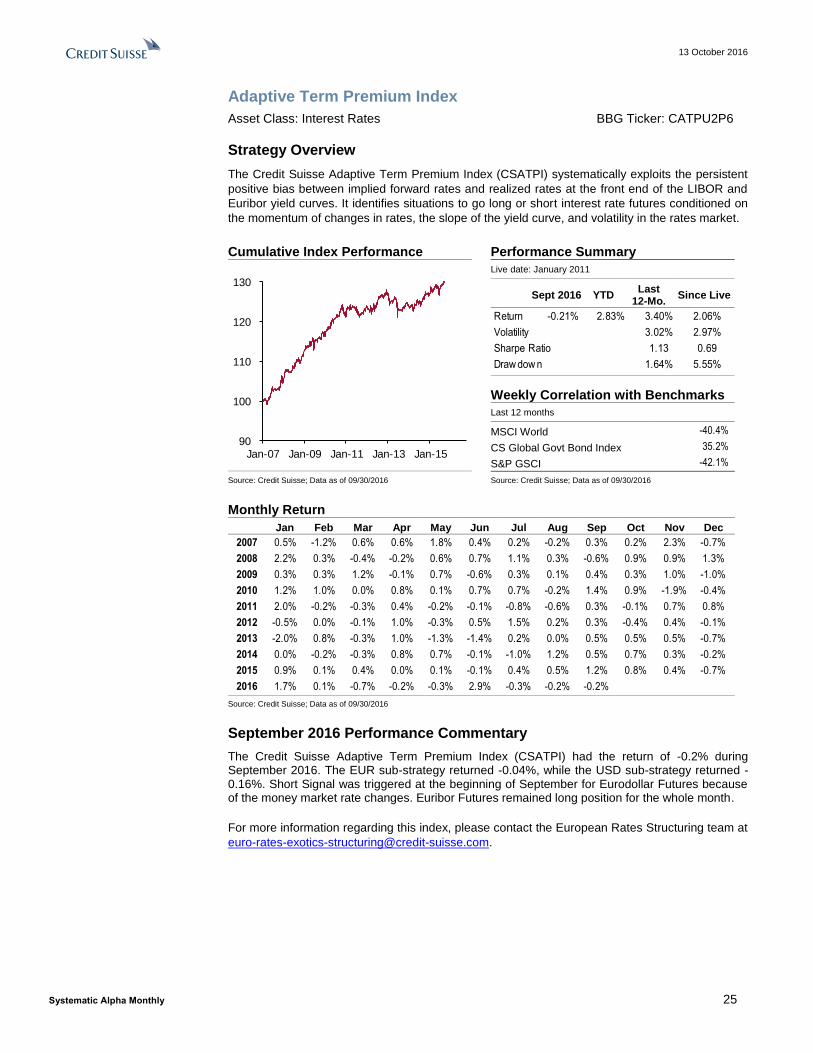

Adaptive Term Premium Index

Asset Class: Interest Rates BBG Ticker: CATPU2P6

Strategy Overview

The Credit Suisse Adaptive Term Premium Index (CSATPI) systematically exploits the persistent

positive bias between implied forward rates and realized rates at the front end of the LIBOR and

Euribor yield curves. It identifies situations to go long or short interest rate futures conditioned on

the momentum of changes in rates, the slope of the yield curve, and volatility in the rates market.

Cumulative Index Performance Performance Summary

90

100

110

120

130

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Live date: January 2011

Sept 2016 YTD

Last 12-Mo.

Since Live

Return -0.21% 2.83% 3.40% 2.06%

Volatility 3.02% 2.97%

Sharpe Ratio 1.13 0.69

Draw dow n 1.64% 5.55%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World -40.4%

35.2%

-42.1%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 0.5% -1.2% 0.6% 0.6% 1.8% 0.4% 0.2% -0.2% 0.3% 0.2% 2.3% -0.7%

2008 2.2% 0.3% -0.4% -0.2% 0.6% 0.7% 1.1% 0.3% -0.6% 0.9% 0.9% 1.3%

2009 0.3% 0.3% 1.2% -0.1% 0.7% -0.6% 0.3% 0.1% 0.4% 0.3% 1.0% -1.0%

2010 1.2% 1.0% 0.0% 0.8% 0.1% 0.7% 0.7% -0.2% 1.4% 0.9% -1.9% -0.4%

2011 2.0% -0.2% -0.3% 0.4% -0.2% -0.1% -0.8% -0.6% 0.3% -0.1% 0.7% 0.8%

2012 -0.5% 0.0% -0.1% 1.0% -0.3% 0.5% 1.5% 0.2% 0.3% -0.4% 0.4% -0.1%

2013 -2.0% 0.8% -0.3% 1.0% -1.3% -1.4% 0.2% 0.0% 0.5% 0.5% 0.5% -0.7%

2014 0.0% -0.2% -0.3% 0.8% 0.7% -0.1% -1.0% 1.2% 0.5% 0.7% 0.3% -0.2%

2015 0.9% 0.1% 0.4% 0.0% 0.1% -0.1% 0.4% 0.5% 1.2% 0.8% 0.4% -0.7%

2016 1.7% 0.1% -0.7% -0.2% -0.3% 2.9% -0.3% -0.2% -0.2%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The Credit Suisse Adaptive Term Premium Index (CSATPI) had the return of -0.2% during September 2016. The EUR sub-strategy returned -0.04%, while the USD sub-strategy returned -0.16%. Short Signal was triggered at the beginning of September for Eurodollar Futures because of the money market rate changes. Euribor Futures remained long position for the whole month.

For more information regarding this index, please contact the European Rates Structuring team at

13 October 2016

Systematic Alpha Monthly 26

Commodity Backwardation RV

Asset Class: Commodities BBG Ticker: CSCUBKAE

Strategy Overview

The Credit Suisse Commodity Backwardation RV Index maintains a long exposure to the CS

Commodity Backwardation Index, which dynamically allocates to selected components displaying

the highest degree of backwardation in their curve structure, aiming to capture the commodities

with the tightest supply/demand balance in the investment universe, and a short exposure to the

Bloomberg Commodity Index.

Cumulative Index Performance Performance Summary

80

140

200

260

320

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Live date: February 2009

Sept 2016 YTD

Last 12-Mo.

Since Live

Return -0.72% -4.25% 4.98% 2.88%

Volatility 10.51% 8.41%

Sharpe Ratio 0.47 0.34

Draw dow n 10.64% 10.64%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World -16.9%

0.3%

-55.9%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 -2.0% 2.5% 1.5% 5.4% 1.8% -0.3% 4.0% -0.8% -1.1% 0.4% -0.1% -2.7%

2008 -0.3% 0.5% 1.5% 3.7% 4.2% -1.1% 3.9% 3.6% 3.8% -1.9% 2.1% 10.8%

2009 4.7% 2.0% 3.6% 1.0% 0.7% 1.3% 4.0% 4.7% 0.8% -0.2% 0.3% -0.6%

2010 2.3% -0.5% 2.9% 2.8% 0.9% -1.8% -3.1% 4.2% 2.2% 4.6% 0.4% 1.8%

2011 3.2% 5.4% -0.9% -1.5% 1.2% 3.0% 0.8% -2.6% 0.1% 0.9% 2.0% 1.4%

2012 4.9% 2.9% 3.4% -2.1% -0.5% -1.8% 0.1% 6.4% -1.6% 0.1% 0.9% 0.3%

2013 0.8% 1.5% -0.2% -0.2% 2.4% 2.0% 1.1% -0.9% 0.0% 1.0% 0.4% -1.8%

2014 -1.4% -2.1% 1.3% -0.8% 2.0% -0.1% 0.3% 0.2% 1.3% -3.5% -0.7% 0.5%

2015 1.6% -2.9% 4.2% -0.3% 0.1% -2.2% 3.8% -2.0% -0.1% 3.5% 1.4% 4.2%

2016 -2.0% 5.7% -2.3% -2.2% -3.0% -1.1% 3.3% -1.6% -0.7%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The Credit Suisse Backwardation RV Strategy returned -0.72% during the month. Industrial

Metals had a strong month (up 2.56%, driven mainly by Lead) however the contribution was negative from all other sectors (especially energy which was down 1.12%).

For more information regarding this index, please contact Mi-Sonn Kim (mi-sonn.kim@credit-

suisse.com) in Commodities Sales.

13 October 2016

Systematic Alpha Monthly 27

Commodity Momentum Long/Short

Asset Class: Commodities BBG Ticker: CSCUMLSE

Strategy Overview

The Credit Suisse Momentum Long/Short Index aims to produce positive absolute returns

regardless of the commodity cycle. It takes long positions in the commodities exhibiting the

strongest upward price trends and short positions in the commodities exhibiting the strongest

downward price trends.

Cumulative Index Performance Performance Summary

80

120

160

200

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Live date: February 2009

Sept 2016 YTD

Last 12-Mo.

Since Live

Return -0.07% -7.14% 2.44% 2.05%

Volatility 14.21% 10.95%

Sharpe Ratio 0.17 0.19

Draw dow n 14.75% 14.75%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World -37.0%

15.3%

-82.9%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 -0.2% 1.4% -0.3% 5.1% 0.9% -3.7% -2.4% 4.1% 1.6% 2.5% 4.0% 2.7%

2008 -2.2% 3.0% 1.2% 1.8% 9.5% 4.6% -4.7% -2.4% -0.9% -2.0% -0.2% -0.5%

2009 1.0% 0.2% -2.2% -0.3% -3.1% -4.3% 3.1% 7.2% -1.3% -2.2% 0.1% 2.9%

2010 0.9% 0.9% 7.9% -1.9% -5.5% -5.6% -6.9% 5.6% -0.6% 2.4% -1.8% 2.6%

2011 0.5% 5.9% 0.3% 4.2% -0.4% -2.3% 0.0% 2.9% -4.0% 0.6% 3.0% -1.6%

2012 1.2% 3.3% 3.1% -1.0% -0.1% -2.7% 3.2% 3.2% -7.4% -0.5% -0.1% -1.9%

2013 0.3% -0.6% 0.6% 3.2% 1.0% 1.3% 2.0% 0.4% 0.4% 0.7% 2.0% 2.6%

2014 -1.0% -4.9% -0.7% 2.8% 1.2% -0.4% 3.7% 0.1% 4.0% -3.5% 3.0% 1.7%

2015 3.4% -8.6% 3.3% -3.7% -0.4% -1.7% 1.6% -0.6% 1.4% 1.9% 1.8% 5.4%

2016 0.6% 2.0% -2.8% -3.4% -2.6% -0.6% 4.0% -4.2% -0.1%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The Credit Suisse Momentum Long/Short returned -0.07% during the month. The gains in Industrial Metals, Agriculture, and Precious Metals (0.29%, 0.31%, and 0.33% respectively) were counterbalanced by the loss in Energy (-1.00%).

For more information regarding this index, please contact Mi-Sonn Kim (mi-sonn.kim@credit-

suisse.com) in Commodities Sales, or Victor Belyaev ([email protected]) in

Commodities Structuring.

13 October 2016

Systematic Alpha Monthly 28

Commodity Custom 24 Alpha

Asset Class: Commodities BBG Ticker: CSCUS24A

Strategy Overview

The Credit Suisse Custom 24 Alpha Index provides exposure to a congestion arbitrage strategy in

commodities. It maintains a leveraged long exposure to a version of the Bloomberg Commodity

Index which rolls the underlying futures positions earlier than normal, and a leveraged short

exposure to the Bloomberg Commodity Index itself.

Cumulative Index Performance Performance Summary

80

140

200

260

320

380

440

500

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Live date: February 2009

Sept 2016 YTD

Last 12-Mo.

Since Live

Return 1.10% 8.60% 15.15% 11.13%

Volatility 8.15% 10.31%

Sharpe Ratio 1.86 1.08

Draw dow n 6.23% 12.34%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World -15.5%

11.9%

-15.8%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 -0.4% 2.1% -0.6% 4.6% -0.4% 4.4% -0.6% 4.1% 2.2% 1.5% 4.7% 3.7%

2008 1.3% 2.4% 1.1% 0.2% -1.2% 0.1% -0.2% 1.6% 1.2% 4.0% 0.7% 6.9%

2009 5.8% 7.5% 2.7% 6.1% 2.2% 0.2% -0.6% 2.4% 1.6% 1.9% 2.7% 1.9%

2010 1.9% 0.5% 1.0% 3.2% 1.0% -1.3% -2.4% 4.8% -1.3% 3.2% 0.6% -0.2%

2011 1.4% 8.1% 0.0% 0.7% 1.0% 0.7% 1.1% 2.1% -0.3% -1.0% -0.9% 1.2%

2012 0.9% 0.9% 1.3% -3.5% 6.8% -8.9% 1.8% 3.9% -0.3% 0.2% 1.6% 1.5%

2013 0.8% 1.6% 0.8% 1.7% 6.3% -2.3% 2.8% 2.8% 0.8% 0.4% 0.1% -0.8%

2014 -2.2% 4.9% 1.6% 1.2% 0.1% 3.8% 2.4% 0.8% 0.1% 1.5% 1.2% 1.7%

2015 0.9% 0.5% 0.5% -1.9% -2.4% 1.1% -0.7% -0.1% 0.2% 3.4% 0.6% 3.1%

2016 -1.5% 4.4% 1.0% -1.7% 1.7% 2.2% 0.3% 0.8% 1.1%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The Credit Suisse Custom 24 Alpha returned 1.10% during the month. There was a positive performance in all sectors apart from Livestock (-0.30%). The main driver was the strong performance in Energy (1.17%).

For more information regarding this index, please contact Mi-Sonn Kim (mi-sonn.kim@credit-

suisse.com) in Commodities Sales, or Victor Belyaev ([email protected]) in

Commodities Structuring.

13 October 2016

Systematic Alpha Monthly 29

Commodity Custom 88 Enhanced

Asset Class: Commodities BBG Ticker: CSCUE88E

Strategy Overview

The Credit Suisse Custom 88 Enhanced Index provides dynamic exposure to carry returns in

commodities. It allocates short exposure to time spreads in selected commodities with the tenor

of the spreads varying according to the relative risk/reward.

Cumulative Index Performance Performance Summary

80

100

120

140

160

180

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Live date: February 2009

Sept 2016 YTD

Last 12-Mo.

Since Live

Return 0.94% 2.30% 3.85% 2.24%

Volatility 4.11% 3.14%

Sharpe Ratio 0.93 0.71

Draw dow n 2.20% 3.61%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World -36.0%

3.2%

-52.4%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 -0.5% 1.6% 0.9% 1.4% 0.4% 0.6% 0.7% 1.9% 1.2% 1.6% 0.9% 1.4%

2008 2.4% 1.2% 2.2% 0.4% 0.5% 1.6% -0.2% -0.7% 0.1% 1.6% -0.1% 2.6%

2009 1.0% 1.6% 0.4% 2.2% -1.5% 0.9% 1.5% 2.6% -1.3% -0.2% 1.2% -0.7%

2010 0.8% -0.5% 0.5% 0.5% 0.5% -0.6% -0.9% 1.1% -0.1% 1.1% 0.3% -0.2%

2011 0.0% 2.0% 1.2% 1.9% 1.2% 0.7% 0.0% 0.6% -0.3% 0.2% -0.1% 0.4%

2012 1.0% 0.6% 1.7% -0.1% -0.5% -0.7% -0.1% 0.6% -0.4% 0.1% -0.1% 0.5%

2013 -0.8% 0.7% -0.5% 0.3% 0.5% -0.9% -0.3% -0.2% 0.7% 1.1% 0.3% -0.1%

2014 -0.4% -0.4% -1.0% 1.1% 1.3% 0.0% 1.9% 0.6% -1.1% 1.4% -0.7% 1.1%

2015 1.2% 1.1% 0.6% -1.2% -0.2% 0.3% 0.2% -0.6% 0.0% -0.1% 1.2% 0.5%

2016 0.3% 2.2% -0.2% -0.1% 0.2% -1.4% 1.4% -1.0% 0.9%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The Credit Suisse Enhanced 88 Strategy returned 0.94% during the month. Lean Hogs had a very good month, returning 1.36% with moderately negative performance in the other components.

For more information regarding this index, please contact Mi-Sonn Kim (mi-sonn.kim@credit-

suisse.com) in Commodities Sales, or Victor Belyaev ([email protected]) in

Commodities Structuring.

13 October 2016

Systematic Alpha Monthly 30

FX Metrics Carry

Asset Class: Currencies BBG Ticker: FXMXCEUS

Strategy Overview

The Credit Suisse FX Metrics Carry: Foreign Currency Strategy systematically trades FX carry in

18 currencies with one-month Cash Settled Forwards. It invests in an equally weighted basket of

top high-yielding currencies and selling an equally weighted basket of low-yielding currencies.

Cumulative Index Performance Performance Summary

85

90

95

100

105

110

115

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Live date: March 2010

Sept 2016 YTD

Last 12-Mo.

Since Live

Return 0.61% 5.47% 8.25% -0.67%

Volatility 9.33% 7.32%

Sharpe Ratio 0.89 -0.09

Draw dow n 7.67% 20.39%

Weekly Correlation with Benchmarks

Last 12 months

MSCI World 66.8%

-45.9%

43.2%

CS Global Govt Bond Index

S&P GSCI

Source: Credit Suisse; Data as of 09/30/2016 Source: Credit Suisse; Data as of 09/30/2016

Monthly Return

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 1.5% -0.1% -45.9% 89.2% 3.2% 2.1% -0.6% -3.0% 2.2% 1.9% -48.2% 87.2%

2008 -2.9% -1.2% -6.2% 5.1% 1.8% -1.7% 2.4% 0.0% -6.4% -9.2% -0.6% -0.5%

2009 0.8% 2.3% 2.5% 3.2% 2.2% 2.0% -0.4% -1.1% 2.1% 1.0% -2.3% 4.1%

2010 -1.3% -0.5% 2.1% 3.0% -2.6% -0.6% -0.2% -1.5% 2.3% -0.2% 1.0% 1.4%

2011 -2.3% 0.3% 1.9% 0.9% -0.7% -0.5% -1.3% -1.1% -4.0% 3.9% -1.2% 1.1%

2012 2.1% 2.4% -2.6% -0.5% -1.2% 1.5% 1.0% -1.0% -0.2% -0.1% 0.1% 1.8%

2013 0.8% 0.5% 0.9% 0.7% -3.1% -2.3% -1.5% -2.6% 1.8% 0.5% -0.3% -2.0%

2014 -1.3% 1.8% 3.1% 0.1% 0.7% 0.5% 0.6% 1.9% -2.4% 1.4% -0.2% -0.5%

2015 -2.5% 0.0% -1.3% -0.1% -0.6% -1.3% -2.5% -4.3% -2.4% 3.5% 2.1% -2.7%

2016 -1.1% -0.5% 2.3% 0.5% -1.1% 3.8% 0.5% 0.3% 0.6%

Source: Credit Suisse; Data as of 09/30/2016

September 2016 Performance Commentary

The FX Metrics Carry index gained 0.61% for the month of September 2016. The strategy