Sylvie Cornot -Gandolphe CEDIGAZ - 13 June 2014 General...Sylvie Cornot -Gandolphe . CEDIGAZ . ......

31

Gas and coal competition in the EU power sector Sylvie Cornot-Gandolphe CEDIGAZ Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

Transcript of Sylvie Cornot -Gandolphe CEDIGAZ - 13 June 2014 General...Sylvie Cornot -Gandolphe . CEDIGAZ . ......

Gas and coal competition in the EU power sector

Sylvie Cornot-Gandolphe

CEDIGAZ

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

Objectives and Contents of the Report Main findings State of play of gas and coal competition in the EU power

sector The European paradox

Main causes of the European paradox European and international developments

Consequences None of the EU climate and energy objectives are met

Coal renaissance in the EU? Conclusion: Gas and Coal contest

Outline

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

Objectives and Contents

Two main objectives: To analyse competition

between gas and coal in the EU power sector (coal renaissance?)

To draw conclusions for future gas demand by the power sector

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

Objectives and Contents

Contents: Five Chapters EU electricity market Gas prices in Europe Coal prices The EU CO2 market Gas and coal competition in

the future

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

Main Findings

State of play –2013

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

EU Gas Demand: the lost decade

420

440

460

480

500

520

540

bcm

0

100

200

300

400

500

600

bcm

Power sector Industry

Non energy consumption Residential/Services

District heating Others

In 2013, EU gas demand decreased for the third consecutive year - 1% in 2013, after -3% in 2012 and –6% in 2011

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

EU Gas demand in the Power sector

0

20

40

60

80

100

120

140

160

180

bcm

Germany Netherlands United Kingdom

Spain Italy France

Belgium Others

Decrease in gas consumption by the power sector (2013 vs. 2010): 51 bcm

Germany

12%

Netherlands 8%

United Kingdom

30% Spain 14%

Italy 16%

France 7%

Belgium 5%

Others 8%

Gas demand by the power sector has decreased by 51 bcm since 2010 The equivalent of the total French gas market…

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

EU coal market

EU total coal consumption Change in coal use (2012 vs. 2009) Mt

The EU paradox: EU coal demand is rising… While gas demand is falling

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

The European paradox

EU electricity generation, Gas vs. Coal and RES US electricity generation, Gas vs. Coal and RES

Coal and RES are displacing natural gas in the EU power sector

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Coal Natural gas RES

Main causes of the European paradox

European and international developments

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

Decrease in total and residual electricity demand

1500

1700

1900

2100

2300

2500

2700

2900

3100

330019

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

13f

TWh

EU electricity demand

EU electricity demand is declining (economic crisis, efficiency gains). Fast development of RES decreases residual load addressed to other fuels and decreases wholesale electricity prices

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Fast development of RES

Residual demand

Other RES

Wind

Hydro (incl.Pumped hydro)Nuclear

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

Coal competitiveness Cheap coal import prices thanks to US shale

gas revolution Coal import prices

0

50

100

150

200

250

US$

/ton

ne

Asia Europe

Coal imports in the EU, by supplier (2012)

Coal prices have decreased by 38% since the middle of 2011

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

Coal competitiveness Reinforced by the increase in gas import prices and

the collapse of CO2 prices

European gas import prices increased by 42% from 2010 to 2013, in line with crude oil prices. CO2 prices collapsed

0

5

10

15

20

25

30

35

€/tC

O2

CO2 Settlement Price

0

5

10

15

20

25

30

US$

/MBt

u

Regional gas prices vs. crude oil prices

Crude oil, Brent LNG, Japan

Natural gas, Europe Natural gas, US

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

A perfect storm for CCGTs

-30

-20

-10

0

10

20

30

€/M

Wh

German clean spark and dark spreads

Average Clean Dark spot base

Average Clean Spark spot base

Running gas-fired power plants is a loss-making business

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

Consequences

None of the EU climate and energy objectives are met

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

The EU ETS is not leading to decarbonized electricity

CO2 emissions by the EUETS power sector

0

200

400

600

800

1000

1200

1400

2008 2009 2010 2011 2012

Mt

Coal Gas Others

Switch from gas-to-coal means that CO2 emissions in the EU ETS have not decreased since 2009.

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

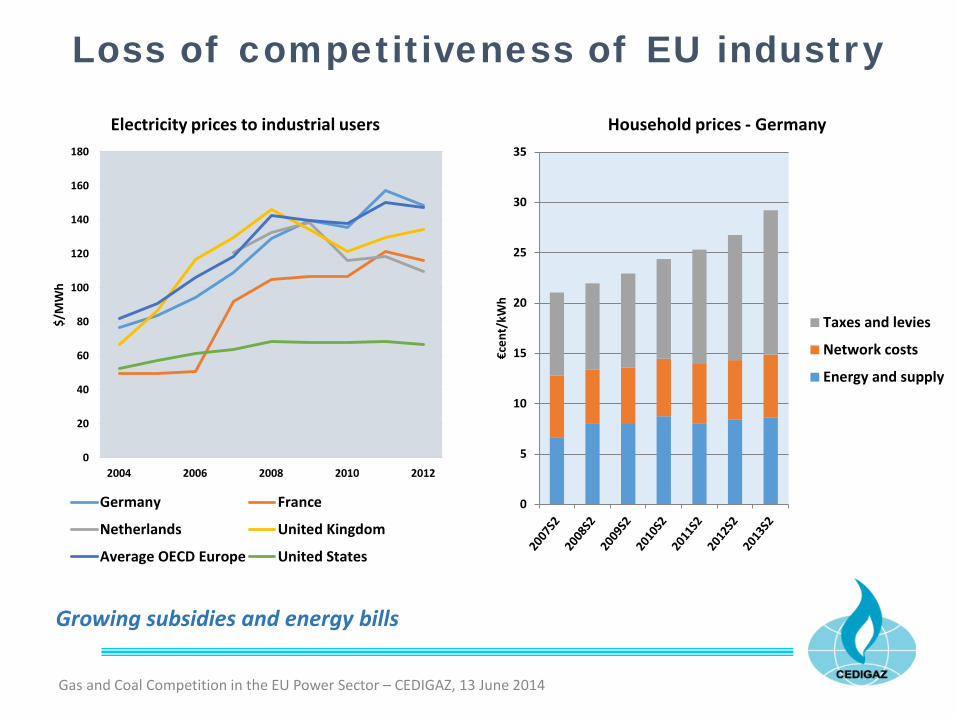

Loss of competitiveness of EU industry

0

20

40

60

80

100

120

140

160

180

2004 2006 2008 2010 2012

$/M

Wh

Electricity prices to industrial users

Germany France

Netherlands United Kingdom

Average OECD Europe United States

Growing subsidies and energy bills

0

5

10

15

20

25

30

35

€cen

t/kW

h

Household prices - Germany

Taxes and levies

Network costs

Energy and supply

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

Security of supply is no more guaranteed Mothballing/Closure of CCGTs

• Low utilization of CCGTs • Closure or mothballing of gas-

fired power plants – 25 GW in the past two years – including new-build efficient CCGTs

• Financial and operational consequences

• No investment in new conventional plants

0

2

4

6

8

10

12

14

16

18

2010 2011 2012 2013

€ bi

llion

Generation asset write-downs by major EU power utilities

If all gas plants under review by EU power utilities are closed, a total capacity of about 50 GW will close, or 28% of the current gas fleet capacity

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

A coal renaissance in the EU?

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

This period of grace should end by 2020. Before if CO2 prices increase Highly dependent on EU ETS reform and Government interventions

2013: a turning point?

Coal 8,9

Gas -10,4

Oil -0,6

Nuclear -2,5

Hydro -0,6

Biomass 2,9

Wind -0,9

Solar 1,9

-15

-10

-5

0

5

10

TWh

Germany - Electricity generation 2013/2012

Coal -11,5

Oil -0,2

Gas -4,3

Nuclear 0,2

Hydro -0,6

Wind and Solar 8,6

Others 2,4

-15,0

-10,0

-5,0

0,0

5,0

10,0

TWh

UK - Electricity generation 2013/2012

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

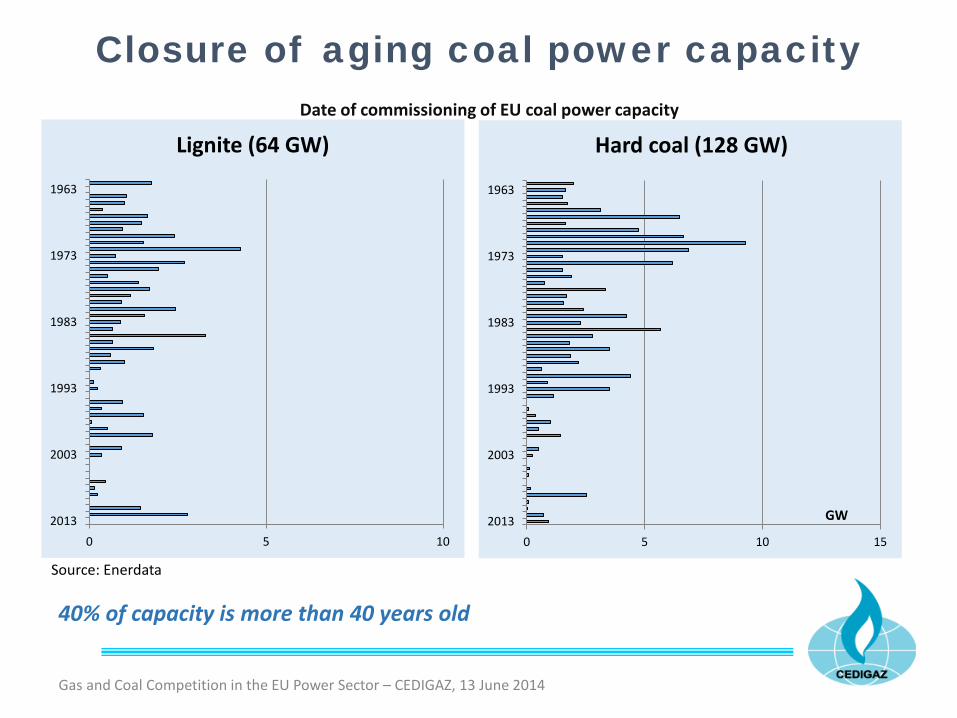

Closure of aging coal power capacity

0 5 102013

2003

1993

1983

1973

1963

Lignite (64 GW)

0 5 10 152013

2003

1993

1983

1973

1963

Hard coal (128 GW)

GW

40% of capacity is more than 40 years old

Date of commissioning of EU coal power capacity

Source: Enerdata

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

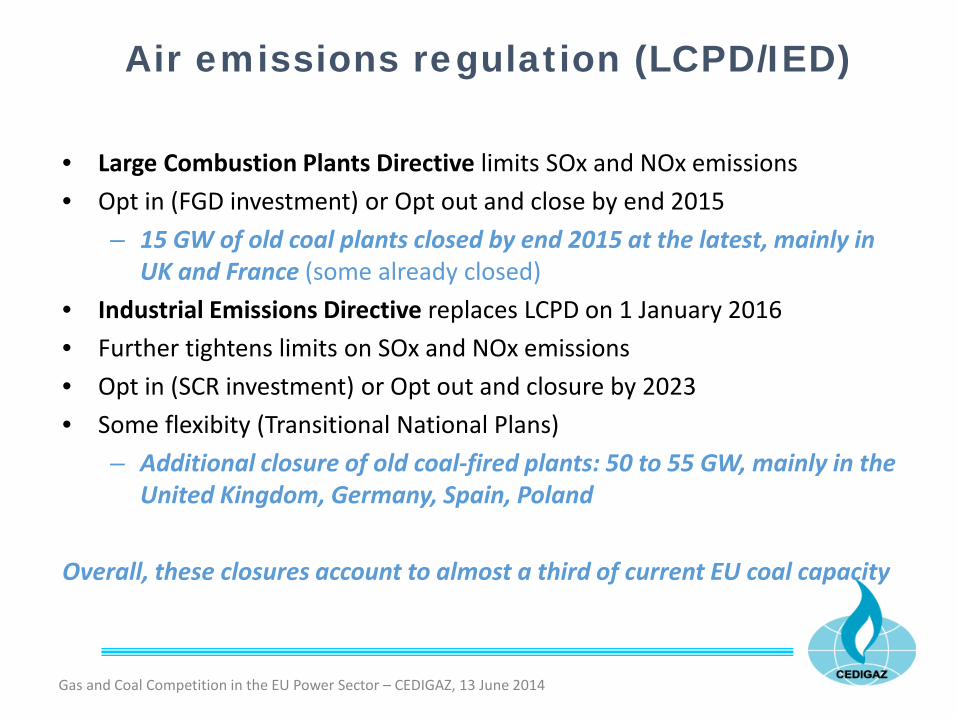

Air emissions regulation (LCPD/IED)

• Large Combustion Plants Directive limits SOx and NOx emissions • Opt in (FGD investment) or Opt out and close by end 2015

– 15 GW of old coal plants closed by end 2015 at the latest, mainly in UK and France (some already closed)

• Industrial Emissions Directive replaces LCPD on 1 January 2016 • Further tightens limits on SOx and NOx emissions • Opt in (SCR investment) or Opt out and closure by 2023 • Some flexibity (Transitional National Plans)

– Additional closure of old coal-fired plants: 50 to 55 GW, mainly in the United Kingdom, Germany, Spain, Poland

Overall, these closures account to almost a third of current EU coal capacity

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

CO2 taxes/energy policies against coal in some countries

UK introduced a Carbon Price Floor (CPF) on 1 April 2013 at £15.70/tCO2 Power companies must pay £4.94/t and this rises to £18.08 by 2015-16 (until 2020). That is on top

of the EU carbon price

UK requires at least 300MW net CCS on any new coal project

The Netherlands introduced a coal tax in 2013 at a level of €13.65/t of coal. Additionally 10% biomass co-firing is mandatory.

Dutch National Energieakkoord: deal with four electricity producers to close down five older coal fired power plants.

Spanish economy cannot sustain coal subsidies and has announced they will end in December 2014

ETS derogation decision impacting on investment decisions in Poland Scandinavian countries: Phase-out of coal. Conversion to biomass

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

EU ETS reform Can the phoenix rise from the ashes?

• Structural reform of the EU ETS • 2030 Climate and Energy Framework • Emissions reduction by 40% by 2030 • Fast-track EUAs backloading (Feb 2014) • Market stability reserve

Different possible futures

Source: Climate Economics Chaire, January 2014

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

Conclusion

Gas and Coal contest

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

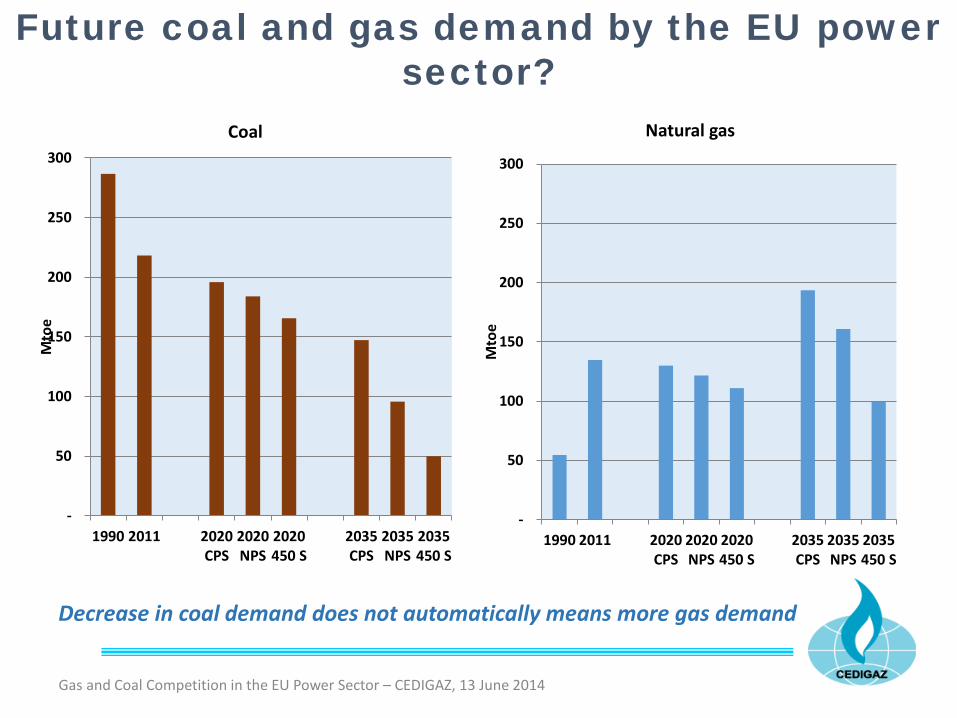

Future coal and gas demand by the EU power sector?

-

50

100

150

200

250

300

1990 2011 2020CPS

2020NPS

2020450 S

2035CPS

2035NPS

2035450 S

Mto

e

Coal

-

50

100

150

200

250

300

1990 2011 2020CPS

2020NPS

2020450 S

2035CPS

2035NPS

2035450 S

Mto

e

Natural gas

Decrease in coal demand does not automatically means more gas demand

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

A period of grace for coal, but short-lived

Short term Security of supply and competitiveness favour coal (even

with the recent decrease in gas prices) BUT Government intervention (UK carbon tax, end of subsidies to

coal mining in Spain, etc) Air quality regulation RES development: coal is starting to be pushed out of the

system CO2 price signal? Caveat: Russia-Ukraine crisis

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

Capacity crunch must be adressed

Almost of third of gas and coal capacity are closing/at risk of closure

No investment in new conventional plants Security of electricity supply must be adressed urgently

Capacity adequacy (GW) Flexible generation (TWh)

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

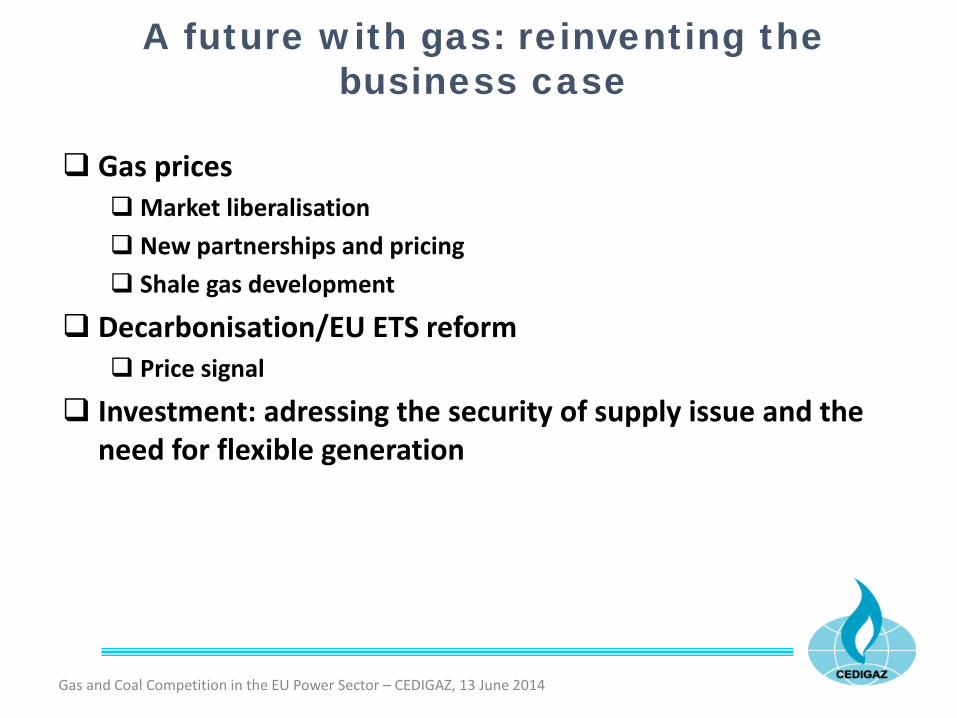

A future with gas: reinventing the business case

Gas prices Market liberalisation New partnerships and pricing Shale gas development

Decarbonisation/EU ETS reform Price signal

Investment: adressing the security of supply issue and the need for flexible generation

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

GAS AND COAL COMPETITION in the EU Power Sector (June 2014)

ORDER FORM Please send me a copy of GAS AND COAL COMPETITION in the EU Power Sector. Price list for the report, PDF format (for more than five users, please contact us): Name: ___________________________________________________________________ Position: __________________________________________________________________ Company: _________________________________________________________________ Address: __________________________________________________________________ __________________________________________________________________________ Country: __________________________________________________________________ Tel: _________________________________Fax:__________________________________ E-mail:____________________________________________________________________ VAT registration number (for EU customers):______________________________________ One user licence Five user licence Membership: Full / Corporate Member Associate/Corresponding Member Non Member I enclose a cheque Please invoice me (Credit Card payment available at http://www.cedigaz.org/ecommerce/studies-01.aspx) Date: Signature: Please return to (by e-mail or mail): CEDIGAZ 1-4 avenue de Bois-Préau, 92852 Rueil Malmaison, France. Tel: +33 1 47 52 67 20 [email protected] Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014

Base price Five users license CEDIGAZ Full & Corporate Members € 1 500 € 3 000 CEDIGAZ Associate & Corresponding Members € 2 000 € 4 000 Non members € 3 000 € 6 000

Thank you

CEDIGAZ 1-4 avenue de Bois-Préau 92852 Rueil-Malmaison – France +33 1 47 52 67 20 [email protected] www.cedigaz.org

Gas and Coal Competition in the EU Power Sector – CEDIGAZ, 13 June 2014