SYLLABUS - rccmindore.comrccmindore.com/wp-content/uploads/2015/06/Advance... · SYLLABUS Class –...

39

M.Com 1 st Sem. Subject- Advanced Accounting 45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 1 SYLLABUS Class – M.Com. I Sem. Subject – Advanced Account UNIT – I Advanced problems of Final Accounts UNIT – II Advanced Problems of Bank Reconciliation Statement, Rectification of Errors, Accounting for Non Profit Organisation. UNIT – III Accounting from Incomplete Records, Accounting for Insurance Claim. UNIT – IV Investment A/c, Voyage A/c, Insolvency A/c. UNIT – V Dissolution of partnership firm including sales of Firm and Amalgamation.

Transcript of SYLLABUS - rccmindore.comrccmindore.com/wp-content/uploads/2015/06/Advance... · SYLLABUS Class –...

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 1

SYLLABUS

Class – M.Com. I Sem.

Subject – Advanced Account

UNIT – I Advanced problems of Final Accounts

UNIT – II Advanced Problems of Bank Reconciliation Statement,

Rectification of Errors, Accounting for Non Profit Organisation.

UNIT – III Accounting from Incomplete Records, Accounting for

Insurance Claim.

UNIT – IV Investment A/c, Voyage A/c, Insolvency A/c.

UNIT – V Dissolution of partnership firm including sales of Firm and

Amalgamation.

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 2

UNIT-I FINAL ACCOUNTS

According to American Institution of Certified Public Accountant Committee:- “Accounting as the art of recording, classifying and summarizing in a significant manner and in terms of money transactions and events which are in part at least, of a financial character, and interpreting the results thereof”. From the above definition, it can be said that “Accounting is science of recording and classifying trading transaction of financial nature and is an art in which financial results are summarized and interpreted.” Characteristics of Accounting

1) Accounting is science as well as an art. 2) The transaction and events relating to financial nature are recorded in it. 3) All transaction and events are recorded in monetary terms. 4) It maintain complete, accurate, permanent and legible records of all transaction in a systematic

manner. 5) It analyses the results of all the transaction in detail.

Objectives of Accounting 1. To Maintain a Systematic Record Accounting is done to maintain a systematic record of the monetary transactions of the firm which is the initial step leading to the creation of the financial statements. Once the recording is complete, the records are classified and summarized to depict the financial performance of the enterprise. 2. To Ascertain the Performance of the Business The income statement also known as the profit and loss account is prepared to reflect the profits earned or losses incurred. All the expenses incurred in the course of conducting the business are aggregated and deducted from the total revenues to arrive at the profit earned or loss suffered during the relevant period. 3. To Protect the properties of the Business The information about the assets and liabilities with the help of accountancy, provides control over the resources of the firm, because accounting gives information about how much the business has to pay to others ? And how much the business has to recover from others? 4. To Facilitate Financial Reporting Accounting is the precursor to finance reporting. The vital liquidity/solvency position is comprehended through the Cash and Funds Flow Statement elucidating the capital transactions. 5. To Facilitate Decision making Accounting facilitates in decision making. The American Accounting Association has explained this while defining the term accounting, it says accounting is, the process of identifying measuring and communicating economic information to permit informed judgments and decisions by users of the information. Accounting As Science and Art Accounting is both a science and an art. Science as well we know is the systematical body of knowledge establishing relationship between causes and their effects. In other words, science has its own concepts, assumptions and principles which are universal and verifiable. Accounting as discipline has also its own assumptions, concepts and principles, which have got universal application. Accounts have systematically and scientifically developed accounting equation and rules of debit and credit. It makes accounting, Science. Art is the practical application of the knowledge. Accounting as discipline is used in the maintenance of books of accounts practically in the real life situations and day-to day affairs of the business, so it is an art also. It can now be safely concluded that Accounting is both science and an art.

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 3

BOOK-KEEPING Book-Keeping is the proper and systematic keeping or maintenance of the books of accounts. Book-Keeping starts from the identification of business transactions. These transactions must be supported by the documents and they must be financial in nature. For example, selling goods for cash in an accounting transaction, because cash is received and goods are going outside the business. The transaction will increase cash and reduce goods. Book-Keeping involves the following process:

1. Identifying accounting transactions 2. Initial record of accounting transactions 3. Preparation of ledger accounts 4. Balance Ledger accounts 5. Preparation of trial balance

DIFFERENCE BETWEEN BOOK-KEEPING AND ACCOUNTING

S.No Basis of Difference Book-Keeping Accounting 1 2 3 4 5 6 7

Transaction Posting Total and Balance Objects Adjustments and Rectification of errors Scope Final Accounts

Trading transactions are recorded in primary books. Entries are posted in ledger from journal and subsidiary books It includes totaling of journal and finding of balances of ledger. The object of Book-keeping is to write all trading transactions in a reasonable manner. In Book-keeping entries of adjustments and rectification of errors are not included. Scope of Book keeping is narrow. Final Account is not prepared in Book-Keeping.

Entries written in primary books are checked and verified. Posting are checked whether correctly posted or not. On the basis of balances of ledger final accounts are prepared The object of accounting is to analyse the transactions written in the books. Accounting includes entries of adjustments and rectification of errors. Scope of Accounting is wide. Final account preparation is must.

Final Accounts

The final object of every businessman is to earn profit. He is interested to know how much profit he has earned or how much loss he has incurred during the year. For the purpose income tax payment, financial position, distribution of dividend and for the future planning it becomes necessary to ascertain the profit or loss for the year. At the end of the year a trial balance is extracted from the ledger balances and then on the basis of the trial balance, closing entries are passed and final Accounts are prepared. The process of preparing Final Accounts from the original records is as under.

Recording of transaction in Journal or Subsidiary books

Postings into ledger from Journal or subsidiary books.

Preparation of Trial balance from ledger accounts

Preparation of Final Accounts on the basis of Trial balance and other information To know the trading results (Profit or loss) for the accounting period and the financial position as it the end of accounting period the final accounts are prepared. The final accounts consists of :

1. Manufacturing Account 2. Trading and Profit & Loss Account

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 4

3. Balance sheet The followings points must be considered while preparing final accounts from trial balance 1. Debit items of Trial Balance:- The items of expenses or assets appear on debit side of Trial balance.

The expenses (the benefit of which is derived within the accounting year in which they are incurred are called revenue expenses. These are debited either to trading account or profit & Loss Account.) Direct expenses such wages. Carriage inwards, freight etc. are debited to trading and indirect exp. such as salaries, rent repairs etc. are debited to profit & Loss account. The expenses the benefit of which is derived in many years are called capital expenditure. These expenditure are called assets and they appear in the assets side of Balance sheet e.g. Building, Machinery, Furniture, Vehicle etc.

2. Credit items of Trial Balance: The items of incomes, gains or liabilities appear in the credit side of trial balance. The receipts are divided into two parts capital receipts and revenue receipts. Capital receipts are liabilities items they are mentioned in the liabilities side or deducted from the assets side of Balance sheet. Revenue receipts are called incomes. It is again divided into direct and indirect incomes. Direct incomes means sale proceeds of the goods which is credited to Trading Account. Indirect incomes are other incomes not directly related to the main business activities such as rent commission, interest, dividend etc received. These are credited to profit and loss account.

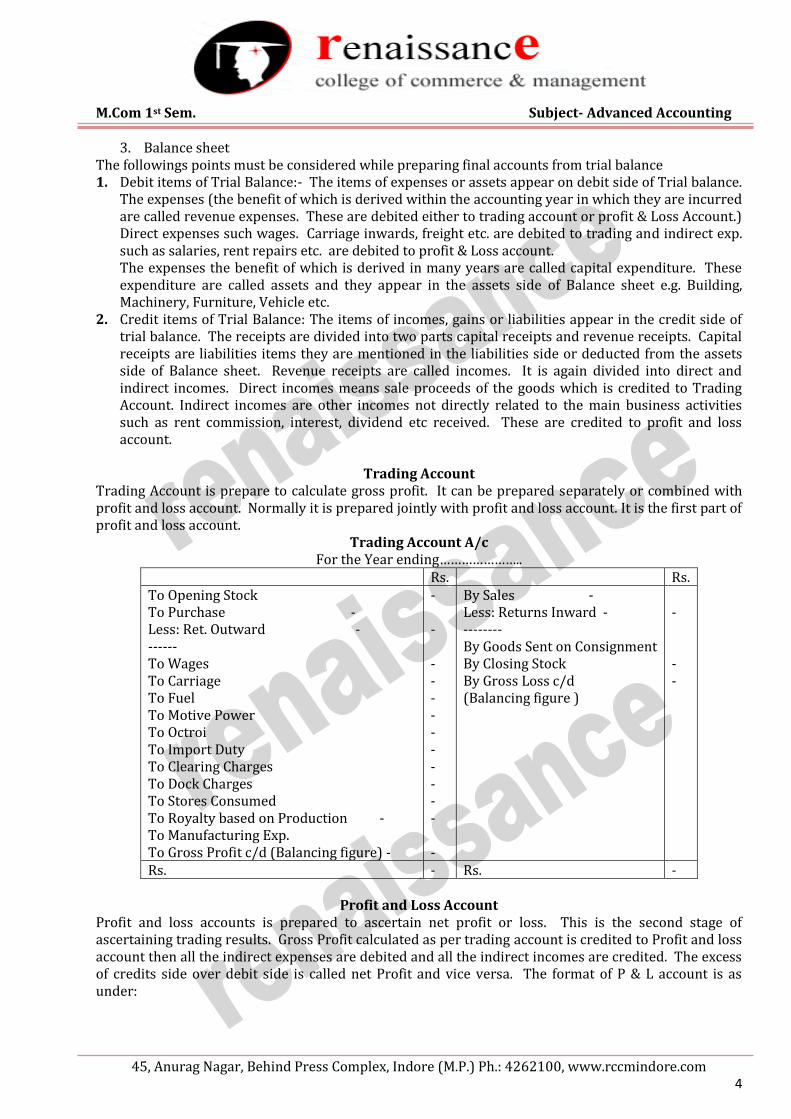

Trading Account

Trading Account is prepare to calculate gross profit. It can be prepared separately or combined with profit and loss account. Normally it is prepared jointly with profit and loss account. It is the first part of profit and loss account.

Trading Account A/c For the Year ending…………………..

Rs. Rs. To Opening Stock To Purchase - Less: Ret. Outward - ------ To Wages To Carriage To Fuel To Motive Power To Octroi To Import Duty To Clearing Charges To Dock Charges To Stores Consumed To Royalty based on Production - To Manufacturing Exp. To Gross Profit c/d (Balancing figure) -

- - - - - - - - - - - - -

By Sales - Less: Returns Inward - -------- By Goods Sent on Consignment By Closing Stock By Gross Loss c/d (Balancing figure )

- - -

Rs. - Rs. -

Profit and Loss Account Profit and loss accounts is prepared to ascertain net profit or loss. This is the second stage of ascertaining trading results. Gross Profit calculated as per trading account is credited to Profit and loss account then all the indirect expenses are debited and all the indirect incomes are credited. The excess of credits side over debit side is called net Profit and vice versa. The format of P & L account is as under:

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 5

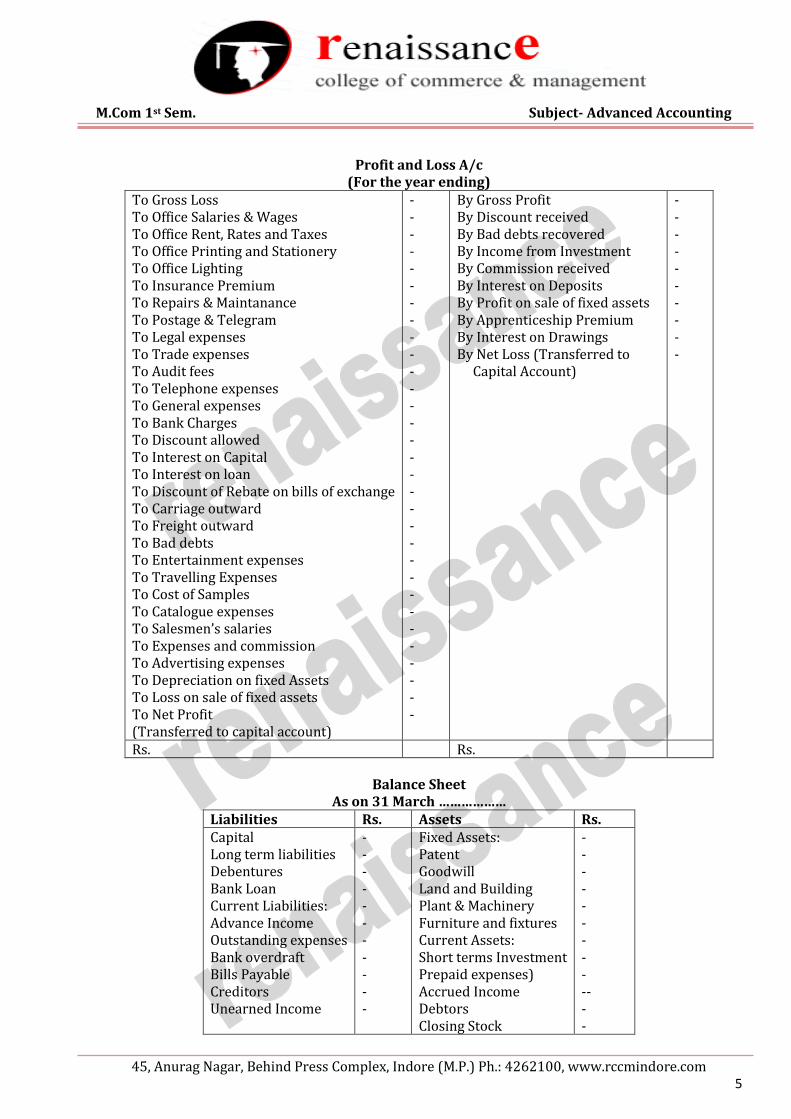

Profit and Loss A/c

(For the year ending) To Gross Loss To Office Salaries & Wages To Office Rent, Rates and Taxes To Office Printing and Stationery To Office Lighting To Insurance Premium To Repairs & Maintanance To Postage & Telegram To Legal expenses To Trade expenses To Audit fees To Telephone expenses To General expenses To Bank Charges To Discount allowed To Interest on Capital To Interest on loan To Discount of Rebate on bills of exchange To Carriage outward To Freight outward To Bad debts To Entertainment expenses To Travelling Expenses To Cost of Samples To Catalogue expenses To Salesmen’s salaries To Expenses and commission To Advertising expenses To Depreciation on fixed Assets To Loss on sale of fixed assets To Net Profit (Transferred to capital account)

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

By Gross Profit By Discount received By Bad debts recovered By Income from Investment By Commission received By Interest on Deposits By Profit on sale of fixed assets By Apprenticeship Premium By Interest on Drawings By Net Loss (Transferred to Capital Account)

- - - - - - - - - -

Rs. Rs.

Balance Sheet As on 31 March ………………

Liabilities Rs. Assets Rs. Capital Long term liabilities Debentures Bank Loan Current Liabilities: Advance Income Outstanding expenses Bank overdraft Bills Payable Creditors Unearned Income

- - - - - - - - - - -

Fixed Assets: Patent Goodwill Land and Building Plant & Machinery Furniture and fixtures Current Assets: Short terms Investment Prepaid expenses) Accrued Income Debtors Closing Stock

- - - - - - - - - -- - -

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 6

Bank Balance Cash Balance

- -

Closing Entries

At the end of the year after preparing trial balance a list of unrecorded items is prepared which is called list of adjustment for which adjustment entries are passed. Now closing entries will be passed. The purpose of closing entries is to closed all those accounts which comes in trading and profit & Loss and these accounts are mainly related to goods and expenses and incomes. Procedure for closing entries- The accounts which are shown on the debit side of trading and profit & Loss account are transferred to these account by writing “By Trading account/Profit and loss account” in all those accounts. Similar in the accounts (appearing on the credit side of trading and profit and loss account) To trading or profit & Loss account is written The major closing entries are as under:

(1) For opening stock, purchase, sales return and all direct expenses Trading A/c Dr. To Opening Stock A/c To Purchases A/c To Sales return A/c To Wages a/c To Carriage Inward A/c

(2) For sales and purchase return Sales A/c Dr. Purchase return Dr. To Trading A/c

(3) For gross profit or loss: (a) Profit Trading A/c Dr. To Profit and Loss A/c (b) loss Profit and loss A/c Dr. To Trading Account

(4) For indirect expenses Profit & Loss A/c Dr. To Salaries A/c To Commission a/c To Discount allowed a/c To Advertisement A/c

(5) For indirect in comes and gains Interest eared a/c Dr. Discount a/c Dr. Commission a/c Dr. Divident a/c Dr. To Profit & Loss A/c

(6) For Net profit or net loss (a) For Net Proift

P & L A/c Dr. To Capital A/c

(b) For Net loss A/c Capital A/c Dr. To P & L Account

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 7

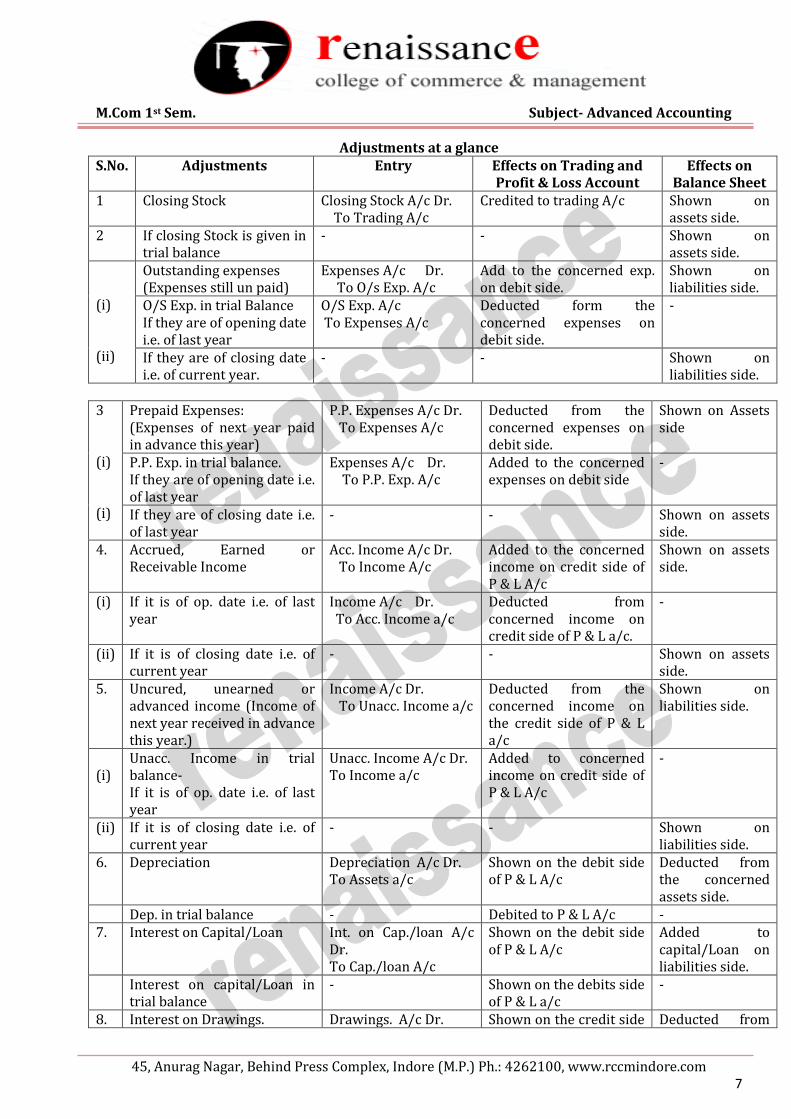

Adjustments at a glance S.No. Adjustments Entry Effects on Trading and

Profit & Loss Account Effects on

Balance Sheet 1 Closing Stock Closing Stock A/c Dr.

To Trading A/c Credited to trading A/c Shown on

assets side. 2 If closing Stock is given in

trial balance - - Shown on

assets side. (i) (ii)

Outstanding expenses (Expenses still un paid)

Expenses A/c Dr. To O/s Exp. A/c

Add to the concerned exp. on debit side.

Shown on liabilities side.

O/S Exp. in trial Balance If they are of opening date i.e. of last year

O/S Exp. A/c To Expenses A/c

Deducted form the concerned expenses on debit side.

-

If they are of closing date i.e. of current year.

- - Shown on liabilities side.

3 (i) (i)

Prepaid Expenses: (Expenses of next year paid in advance this year)

P.P. Expenses A/c Dr. To Expenses A/c

Deducted from the concerned expenses on debit side.

Shown on Assets side

P.P. Exp. in trial balance. If they are of opening date i.e. of last year

Expenses A/c Dr. To P.P. Exp. A/c

Added to the concerned expenses on debit side

-

If they are of closing date i.e. of last year

- - Shown on assets side.

4. Accrued, Earned or Receivable Income

Acc. Income A/c Dr. To Income A/c

Added to the concerned income on credit side of P & L A/c

Shown on assets side.

(i) If it is of op. date i.e. of last year

Income A/c Dr. To Acc. Income a/c

Deducted from concerned income on credit side of P & L a/c.

-

(ii) If it is of closing date i.e. of current year

- - Shown on assets side.

5. Uncured, unearned or advanced income (Income of next year received in advance this year.)

Income A/c Dr. To Unacc. Income a/c

Deducted from the concerned income on the credit side of P & L a/c

Shown on liabilities side.

(i)

Unacc. Income in trial balance- If it is of op. date i.e. of last year

Unacc. Income A/c Dr. To Income a/c

Added to concerned income on credit side of P & L A/c

-

(ii) If it is of closing date i.e. of current year

- - Shown on liabilities side.

6. Depreciation Depreciation A/c Dr. To Assets a/c

Shown on the debit side of P & L A/c

Deducted from the concerned assets side.

Dep. in trial balance - Debited to P & L A/c - 7. Interest on Capital/Loan Int. on Cap./loan A/c

Dr. To Cap./loan A/c

Shown on the debit side of P & L A/c

Added to capital/Loan on liabilities side.

Interest on capital/Loan in trial balance

- Shown on the debits side of P & L a/c

-

8. Interest on Drawings. Drawings. A/c Dr. Shown on the credit side Deducted from

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 8

To Int. on Drawings of P & L A/c capital on liabilities side.

9 Credit purchases not recorded

Purchase A/c Dr. To Creditor’s A/c

Added to purchases on the debit side of Trading A/c

Added to creditors on liabilities side.

10. Credit purchases return not recorded.

Creditor’s A/c Dr. To P/R a/c

Deducted from purchases on the debit side

Deducted from creditors on liabilities side.

11 Credit sales not recorded Debtor’s A/c Dr. To Sales A/c

Added to sales on the credit side of Trading A/c.

Added to debtors on assets side.

12. Credit sales returns not recorded.

S/R A/c Dr. To Debtor’s A/c

Deducted from sales on the credit side of Trading A/c.

Deducted form debtors on assets side.

13. Goods given as charity or free samples

Charity/Adv. A/c Dr. To Purchases Trading A/c

i. Deducted from purchases/credited to trading A/c

-

ii. Shown on the debit side of P & L A/c

14. Drawings of goods by owner Drawings A/c Dr. To Purchases/Trad. A/c

Deducted from purchases credited to trading A/c

Deducted from capital on liabilities side.

15. Goods stolen/damaged by fire: Example : Goods of Rs. 10,000 stolen, claim accepted 6,000

Ins. Co. A/c Dr. 6000 P & L A/c Dr. 4000 To Purchases/ Trad. A/c 10,000

i. Rs. 10,000 deducted from purchases/credited to Trading A/c ii. Rs. 4,000 debited to P & L A/c

Rs. 6,000 shown on assets side as Insurance Co.

16. Goods in transit: (Goods bought yet in transit)

i. If it is already included in purchases

Goods in transit A/c Dr. To Trading A/c

Credited to Trading A/c Shown on assets side.

ii. If it is not already included in Purchases. (Note: If nothing is cleared in the sum, a note must be given.

i. Purchases A/c Dr. To Creditor’s A/c ii. Goods in trans. A/c Dr. To Trading A/c

ii. Credited to Trad. A/c ii. Shown on asse. Side.

17. Goods sold on approval basis: Example- Goods costing Rs. 500 sold on approval for Rs. 600 which is recorded as actual sales.

i. Sales A/c Dr. 600 To Customer 600 Note- This entry is passed by sale price.

i. Rs. 600 deducted from sales on credit side of Trading A/c

i. Rs. 600 deducted from debtors on assets side.

ii. Stock on approval a/c Dr. 600 To Trading A/c 600 Note- This entry is passed by lower of the cost or market price of the goods sold.

ii. Rs. 500 (Being lower of cost or market price) are shown on credit side of Trading A/c

ii. Rs. 500 (Being lower of cost or market price) are shown on assets side.

18. Purchase of assets: - i. Shown on

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 9

a. Not rerecorded at all Assets A/c Dr. To vendor

assets side. ii. Shown on lib. Side

b. Wrongly included in purchases A/c

Asset A/c Dr. To Purchases A/c

Deducted from purchases on debit side of Trad. A/c

Shown on assets side.

c. Installation charges included in wages A/c

Asset A/c Dr. To Wages A/c

Deducted from wages on debit side of Trad. A/c

Added to the concerned asset on assets side.

d. Depreciation on the above asset.

Depreciation A/c Dr. To Asset A/c

Debited to P & L A/c Deducted from the asset on assets side.

19 a.

Over/under valuation of stock: Over valuation of Opening Stock.

Capital A/c Dr. To Op. Stock/Trad. A/c

The Difference is either deducted from op. stock or credited to Trading A/c

The Difference is deducted from capital on liabilities side.

b. Under valuation of opening stock.

Op. stock/Trad. A/c Dr. To Capital A/c

The Difference is either added to op. stock or debited to Trading A/c

The difference is added to capital on liabilities side

c. Over valuation of closing stock.

Trading A/c Dr. To Cost stock A/c

The Difference is either deducted from clo. Stock or debited to Trading A/c

The difference is added to closing stock.

20. Personal use of business assets: Example- 25% of the use of business car is for personal purposes. Car exp. Rs. 2000 and deprecation Rs. 800

Drawings A/c Dr. 700 To Car Exp. A/c 500 To Car Dep. A/c 200

P & L A/c – To Car Exp. (2000×75%) 1500 To Car Dep. (800×75%)600

i. Liab. Rs. 700 deducted from Cap. ii. Assets: Rs. 800 deducted from car.

21. Cheque/B/R/ received from debtors:

Bank/B/R/ A/c Dr. To Debtor’s A/c

Assets Side: i. Deducted from deb. ii. Added to Bank/B/R.

22. Dishonour of Cheque/ B/R received from debtors

Debtor’s A/c Dr. To Bank/B/R A/c

- Assets Side: Add to debtor deducted from Bank.

23. Dishonour of discounted/endorsed B/R

Debtor’s A/c Dr. To Bank/Creditors’

- i. Assets side : added to debtors ii. Deducted from bank on assets side/added to creditors on liabilities side.

24. Discounting of a B/R due next year.

- - Liabilities side : shown below total in inner column as contingent liabilities.

25. Deposit from debtor wrongly Debtor’s A/c Dr. - i. Assets side :

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 10

deducted from debtor’s A/c To Deposit from debtors A/c

Added to debtors. ii. Liabilities side : Added to creditors

26. Settlement with creditors: Example: A creditor for Rs. 400 is settled at Rs. 320.

- - -

a. If it is assumed that payment of Rs. 320 is recorded but discount is not recorded.

Creditors A/c Dr. 80 To Discount 80

P & L A/c: By Discount A/c 80

Liabilities side: Rs. 400 deducted from creditors.

b. If it assumed that whole the transaction is omitted.

Creditors A/c Dr. 400 To Bank A/c 320 To Discount 80

P & L A/c: By Discount A/c 80

Liabilities side: Rs. 400 deducted from creditors. Asset side : Rs. 320 deducted from bank

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 11

UNIT-II Bank Reconciliation Statement

Theoretically speaking there should not any disagreement between cash book (Bank Balance) and pass book Balance (Bank Statement), as all banking transactions are recorded in the both the books. But generally it is found that bank balance as per cash book does not tally with bank balance as per pass Book or Bank statement. Hence to reconcile (to match/to make compatible) the above balances and explaining the reasons for the difference between them ‘Bank reconciliation statement is prepared. Definitions According to Batliboi “A Reconciliation statement is, prepared at periodical intervals with a view to indicate the items which cause such agreement between the balance as per the Bank columns of the cash Book and the Bank pass book on any such date’. According to R.G. Williams ‘A statement is prepared to tally balance shown by bank for customer and balance of bank shown by cash book of the customer is called bank reconciliation statement.’ Characteristics/Features of Bank Reconciliation statement

1. It is prepared by the customer (trader), i.e., holder of the account. 2. It contains a complete and satisfactory explanation of the difference in balances as per the Cash

Book and Pass Book (Bank Statement) 3. Normally it is prepared on closing date of accounts, i.e., Dec. 31 or Jan. 30, or March 31. 4. Sometimes it is prepared at the end of the every month after preparing Cash Book or regularly

after certain interval to check the accuracy of Cash Book. 5. It is neither a journal nor a ledger. 6. It is prepared in a statement form with the vertical presentation of facts. 7. It starts with a given balance of any book and ends with balance of other book, e.g., if it starts

with Balance as per Cash Book, then ends with Balance as per Pass Book. 8. For arithmetical calculations all the reasons are grouped in ‘ADD’ and ‘LESS’ categories

respectively. It can be prepared by preparing plus Minus columns. 9. It shows causes of disagreement and amount thereof. 10. It is not legally compulsory to prepare Bank Reconciliation Statement. 11. It shows the bank balance as per Cash Book or Pass Book (Bank Statement) at the end of the

period. Objectives/Importance/Need/Advantages of preparing B.R.S.

(i) To know the accuracy of entries in the Cash Book and the Pass book (ii) To know the errors in Cash Book and Pass Book. (iii) Check on the embezzlement of cash (iv) Mechanism of Internal control (v) Trace the ignorance, mistakes done by employees of bank who prepare pass book and

cashier who prepares Cash Book (vi) Control time lag of transactions taking place.

Nature of Balance Positive Balance = Debit balance of cash book Credit balance of Pass Book Negative Balance (overdraft) = ● Credit balance of Cash Book Debit balance of Pass Book

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 12

Preparation of Bank Reconciliation Statement Taking Balance as per cash book: When we start with the balance as per cash Book we have to see the impact on Pass Book balance. The items which increase pass book balance are added and which reduce pass book balance are deducted. Taking Pass Book Balance- When we start with Pass Book Balance we have to see the impact on Cash Book. The items/transactions which increase cash book balance are added and transactions which reduce cash book balance are deducted. Causes of difference between the Balances of cash book and Pass Book I. Transactions which have been recorded in cash book but not in Pass Book.

(i) Cheques/drafts issued but not presented for payment (ii) Cheques/Bills/drafts etc sent to bank for collection but not collected. (iii)

II. Transactions which have been recorded in Pass Book but not recorded in Cash Book. (i) Interest allowed on credited by Bank (ii) Bank commission, Bank charges, interest on overdraft charged by Bank. (iii) Collection of dividend and interest and receipt of direct payment from Debtors. (iv) Direct payment by Bank (v) Dishonour of Discounted Bill (vi) Bills receivable directly collected by Bank (vii) Retiming a bill under rebate

III. Error in Cash Book

(i) Error of omission such as cheque/cash deposited into Bank but not recorded in the cash book, cheques issued but not entered in the Cash Book, Cash withdrawn from the bank but not entered in the cash book.

(ii) Error of recording such as cheque deposited into bank but entered in the cash column/Discount column, cheque deposited into bank but recorded in the Bank column on the payment side of cash book, amount of deposit differs from actual amount of cash or cheque in cash book.

(iii) Error of over/under casting of bank column of cash book. (iv) Error of carry forward of balance (v) Cheque received from debtor recorded in cash book but not deposited into bank for

collection. IV Error in Pass Book

(i) Error of omission such as cheques & bills collection by bank but not entered in pass book on wrong posting in another customer’s account.

(ii) Error of recording such as Deposit recorded on withdrawal side and vice versa, amount of deposit differs from actual amount in Pass Book.

(iii) Error of under/overcastting of Deposit column/withdrawal column. (iv) Error of carrying forward. (v) Cheque received from customer but not recorded in customer’s Account.

RECTIFICATION OF ERRORS Financial Accounts are prepared at the final stage to give the financial position of the business on the basis of information supplied by the trail balance. Thus, the accuracy of the trail balance determines to a great extent. Trial balance provides only proof of the arithmetical accuracy of the books of accounts. But it is not a conclusive proof.

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 13

It can be concluded, therefore, that if the trial balance does not agree, there are errors, and if trial balance does agree there may be errors in the account books. TYPES OF ERRORS The types of errors can be illustrated in the following chart:

ERRORS

Rectification of Errors – The errors must be rectified at the earliest from the point of view of rectification, the errors may be classified into the following two categories :

(a) Error which do not affect the Trail balance (b) Errors which affect the Trail balance

This distinction is relevant because the errors which do not affect the trial balance usually take place in two accounts in such a manner that is can be easily rectified through a journal entry whereas the errors which affect the trial balance usually affect one account and a journal entry is not possible for rectification unless a suspense account has been appended. Rectification of Errors which do not affect the trail Balance – These errors are committed in two or more accounts. Such errors are also known as two sided errors. They can be rectified by recording a journal entry giving the correct debit and credit to the concerned accounts. These errors are explained below: 1. Errors of Omission- An errors of omission is one where a transaction has not been recorded in the

books of account.

For example omission to record goods sold to Rajesh, the rectify entry is Rajesh A/c Dr. To Sales (Being goods sold was not passed through books) 2. Error of Recording – Errors of recording means a wrong amount is recorded in the subsidiary

books. For e.g. a purchase of Rs. 8,000 to Mahesh is recorded as Rs. 800. The rectifying entry will be –

Purchases A/c Dr. 7,200

To Mahesh 7200 3. Errors of Posting to wrong Account- Following are the errors of posting to

Errors of

Principle

Errors of

Omission

Errors of

Commission

Compensating

Errors

Complete

Omission

Partial

Omission

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 14

wrong account. (a) Correct Amount on the correct side to wrong account (b) Wrong Amount on the correct side to wrong account (c) Wrong Amount on the wrong side to wrong account (d) Correct Amount on the wrong side to wrong account

For e.g. Sales to Ravina Rs. 10,000 is posted to Ravi’s A/c Rectify entry is Ravina Dr. 10,000 To Ravi 10,000 4. Error of Principle- Sometimes errors of recording are made due to ignorance of principles, i.e., correct distinction is not made between capital receipt and revenue receipt, between capital expenditure and revenue expenditure, between capital losses and gains and revenue losses and gains etc. For e.g. Furniture purchased on credit wrongly recorded in purchases book Rectify entry is – Furniture A/c Dr. To Purchases A/c Rectification of Errors which affect the trial balance :-. There are some errors due to which the trail balance does not agree. These are the errors which are disclosed by the trial balance. These errors are also called one-sided errors. Such errors should first be located and then rectified by giving an explanatory note or by giving a journal entry with the help of a suspense account Following are some errors responsible for disagreement of trial balance

(1) Errors of Casting – Casting is the process of totaling the transactions at the end of a period. An error of casting may be due to over casting or under casting. This type of errors may arise in any subsidiary book. For e.g. If the sales book has been under cast by Rs. 100 The rectification of the error will be done by crediting sales account.

(2) Errors of Posting – Errors of posting means a posting of wrong amount or posting in the wrong side. For e.g. Raj’s account is debited with Rs. 750 instead of Rs. Rs. 705 the mistake lies only in this account. This will rectified by crediting Raj’s A/C with 45. If there is a suspense A/c, the entry will be

Suspense A/c Dr. 45

To Raj 45

(3) Errors of Carry forward - The errors occurs when total of one page is wrongly copied on the next page. In order to rectify such errors, an explanatory note is given and if the suspense A/c is opened, then the correction is through a journal entry with the help of a suspense Account.

SUSPENSE ACCOUNT

When the Trial Balance does not tally, efforts are made to make the trail balance tally, but if these efforts fail, then temporarily the difference of Trail Balance is transferred to an account which is called “Suspense Account”.

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 15

Suspense Account. Will be shown in the Balance Sheet on asset aside if debit balance or on the liabilities side if credit balance. During the course of preparation of final accounts errors are located, they are corrected through the suspense A/c Effect on Profit and Losses Account All such rectifying entries which are related to normal account, affect profit or loss, hence after making rectifications, all nominal account which are affected should be taken into consideration and their amounts be considered for assessing the exact amount of loss or profit. Effect on Balance Sheet All such rectifying entries which are related with personal and real accounts affect the Balance Sheet. Rectifying entries related with nominal account affect profit or loss and this profit or loss is taken to Balance Sheet. Hence, these entries also affect Balance Sheet.

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 16

UNIT-III ACCOUNTS RELATED WITH INCOMPLETE RECORDS

Accounts from incomplete records is an incomplete inaccurate, unscientific and unsystematic style of account keeping. Incomplete account records are those records which fall short of complete double entry system. These records contain either both the aspects of a transaction or only one aspect or no aspect at all of a transaction. Definitions According to kohlar “A system of book keeping in which as a rule only records of cash and of personal accounts are maintained, it is always incomplete double entry system, varying with circumstances.” According to J.R. Botaiboi “The term single entry system is applied to a style of book-keeping under which only the personal account of the debtors and creditors are kept. It is not any particular system of book-keeping, but the Double Entry system is an incomplete and disjoined form.” Characteristics of Accounts from incomplete Records

Maintenance of personal account Maintenance of cash book Dependence on original vouchers Preparation of financial statements. Accuracy of financial statements. Lack of uniformity Suitability for small traders, petty shop keepers and other professionals Less expensive Lack of Legal recognition Flexibility

Advantages of Single Entry System

Easy & simple system Economical Flexibility in nature Time saving Suitability

Disadvantages of Single Entry System

Tax evasion possible No record of impersonal accounts Difficulty in ascertaining net profit & financial position Encourages fraud Lack of business statistics Difficulty in comparison

DIFFERENCE BETWEEN DOUBLE ENTRY & SINGLE ENTRY SYSTEM ON THE BASIS OF

Recording of both aspects Types of Accounts Preparation of Trial Balance Preparation of Trading and Profit & Loss a/c Financial Position

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 17

Adjustments Utility Proof Assumptions and Principles Reliability Expensive Fraud

ACCOUNTING IN SINGLE ENTRY SYSTEM Ascertainment of profit/Loss under incomplete Rerecords There are two methods which can be used for ascertaining profit/losses 1. Net worth/statement of Affairs methods 2. Conversion method Net worth/Statement of Affairs Methods To find out profit or loess by this method firstly capital in the beginning and at the and of the year is calculated by preparing two statement of Affairs, one in the beginning of the year and second at the end of the year. Then after a statement of profit is prepared to find out profit or loss of the period. Statement of profit or loss

Capital at the end of the year (Closing capital) Add: Total drawing during the year Add: Capital withdrawn Add: Interest on drawings Less: Additional capital introduced during the year Less: Capital at the beginning of the year (initial capital) Less: Interest on capital, Less: Any remuneration payable to proprietor

x x x x x x x x x x x x x x x x x x x x x x x x

Profit (+) or Loss (-) for the year x x x Note: Other possible adjustments to be done in statement of profit so at to calculate Net profit are as follows Add:-

(i) Interest on investments (ii) Interest on drawings, Deposits (iii) Prepaid expenses (iv) Appreciation of fixed Assets (v) Undervaluation of Assets

Less:- (i) Outstanding expenses (ii) Depreciation on fixed assets (iii) Overvaluation of assets (iv) Bad debts (v) Provision for bad debts (vi) Interest on capital (vii) Interest on loan

Conversion Method Conversion method involves conversion of single entry into double entry. In this method proper profit and loss a/c and balance sheet is prepared. It can be done by two methods

1. Full conversion method 2. Abridged conversion method

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 18

In practice conversion of records maintained on single entry system into double entry records is a lengthy and time consuming task and hence the firms mostly adopt abridged conversion method. In order to convert single entry into double entry all the information are not there hence it is necessary to calculate missing items/figures. Various missing figures to be calculated are opening capital, cash and bank balance opening or closing Debtors, opening or closing creditors, Bills receivable, Bills payable, Cash purchases, Cash sales, Opening or closing stock, Credit purchase, Credit sales etc.

Practically conversion into dual aspect is done by the above procedure but from exam. Point of view this would be lengthy procedure. In the exam, information given in the questions are solved without preparing any Trial Balance, directly accounts are opened for ascertaining the balances. There would be certain missing information which are ascertained by preparing related accounts. Students should open the following accounts from which missing information will be ascertained: 1. Cash Book – Cash book is prepared according to the information of receipts and payments given in

the question. If transactions related to Bank are also given then two column, one for cash and other for bank are opened in the Cash Book. For finding missing figure from cash book following points should be taken into the consideration: a. Opening cash or bank balance and closing cash or bank balance are given in the question. If any

one of the opening or closing balance is not given, and if difference is this account is credit balance then it would be opening cash balance and if debit balance then it would be closing cash balance.

b. If both opening and closing balances are given and even them there may be difference in the cash book. If credit side is shorter than debit side then difference amount may be treated as payment to creditors and if debit side is shorter than credit side then difference amount may be treated as receipt from debtors.

c. If both opening and closing balance along with amount of payment to creditors and receipt from debtors are given in the question, even then there is a difference in debit side then difference amount will be treated as cash sales and if difference is in credit side, then difference amount will be treated as cash purchases.

d. Also the cash book may contain information regarding sundry income or expenses which are credited or debited into profit & loss a/c accordingly. There would be withdrawal by the proprietor which should be debited to the capital account of the proprietor as drawings.

e. Opening cash balance is written on the debit side and closing cash balance is written on the side of the cash book, but in cash of overdraft, opening balance should be written on the credit side while closing balance should be written on the debit side.

Cash Book

Receipts Cash Bank Payments Cash Bank To Balance b/d To Debtors To Sales (Cash sales) To Bills Receivables To Capital (Additional) To Sundry income To Balance c/d (Clos. Overdraft)

By Balance b/d (op. Overdraft) By Creditors By Purchases (Cash purchase) By Bills Payable By Drawings By Expenses By Assets Purchase By Balance c/d

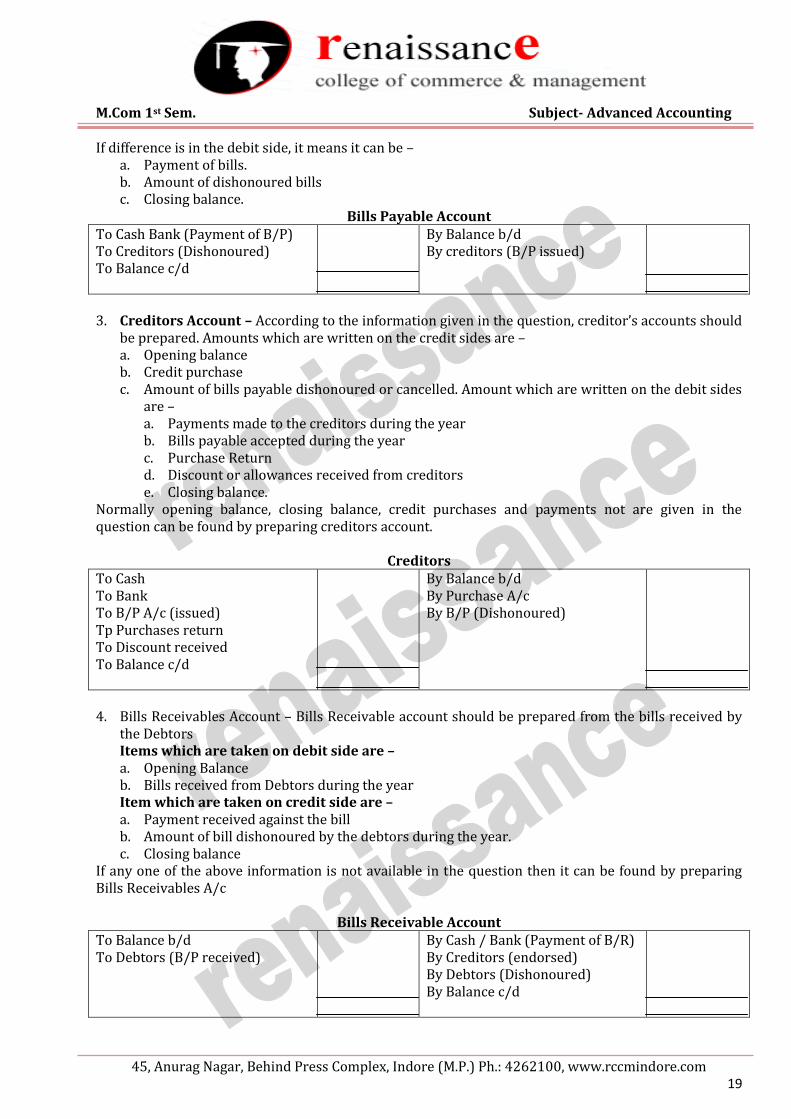

2. Bills Payable A/c – If any information is given regarding bills payable in the question, then bills

payable account should be opened to find out the missing figure. If difference is in the credit side, it means it can be – a. Opening balance b. Bills Payable issued to creditors during the year

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 19

If difference is in the debit side, it means it can be – a. Payment of bills. b. Amount of dishonoured bills c. Closing balance.

Bills Payable Account To Cash Bank (Payment of B/P) To Creditors (Dishonoured) To Balance c/d

By Balance b/d By creditors (B/P issued)

3. Creditors Account – According to the information given in the question, creditor’s accounts should

be prepared. Amounts which are written on the credit sides are – a. Opening balance b. Credit purchase c. Amount of bills payable dishonoured or cancelled. Amount which are written on the debit sides

are – a. Payments made to the creditors during the year b. Bills payable accepted during the year c. Purchase Return d. Discount or allowances received from creditors e. Closing balance.

Normally opening balance, closing balance, credit purchases and payments not are given in the question can be found by preparing creditors account.

Creditors To Cash To Bank To B/P A/c (issued) Tp Purchases return To Discount received To Balance c/d

By Balance b/d By Purchase A/c By B/P (Dishonoured)

4. Bills Receivables Account – Bills Receivable account should be prepared from the bills received by

the Debtors Items which are taken on debit side are – a. Opening Balance b. Bills received from Debtors during the year Item which are taken on credit side are – a. Payment received against the bill b. Amount of bill dishonoured by the debtors during the year. c. Closing balance

If any one of the above information is not available in the question then it can be found by preparing Bills Receivables A/c

Bills Receivable Account To Balance b/d To Debtors (B/P received)

By Cash / Bank (Payment of B/R) By Creditors (endorsed) By Debtors (Dishonoured) By Balance c/d

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 20

5. Debtors Account – Usually credit sales, opening debtors, closing debtors and amount received from debtors are given in the question. If any one of the above information is not given then it should be found by preparing debtors account. Debit side items are – a. Opening balance b. Credit purchase a. Amount of bills dishonoured Credit side items are – a. Amount received from debtors b. Bills drawn during the year c. Sales Return d. Discount or allowances given to debtors e. Closing balance.

Debtors To Balance b/d To Sales A/c To B/R (Dishonoured)

By Cash By Bank By B/R A/c By Sales return By Discount allowed By Allowance By Balance c/d

Insurance claims Introduction A contract of insurance is a contract under which one party known as insurer undertakes to indemnify the other party known as insured on the happening of an unforeseen event in consideration for a fixed amount known as premium. Though the liability of the insurer to indemnify arises on the happening of an event the liability is limited to the amount of actual less suffered by the insured. However in case of under insurance, the insurance liability is limited to the extent of the coverage. There are four main types of stock:

Raw materials and components - ready to use in production Work in progress - stocks of unfinished goods Finished goods ready for sale Consumables - for example, fuel and stationery

Claim for Loss of Stock When the subject matter of fire insurance is subjected to risk of loss the claim for such loss can be calculated as follows:

1. Where proper stock records are maintained and such records are not destroyed by fire. The following steps are involved: a. Ascertain the value of stock on the date of occurrence of fire by referring to stock record. b. Ascertain the amount of stock lost by fire. The following formula is used.

Amount of stock lost by fire o Value of stock on the date of fire -Value of stock saved or salvaged

c. Apply the average clause if applicable. The following formula is used.

Claim = Loss suffered x Sum Insured

Actual Insurable Value

2. Where proper records are not maintained or such records are destroyed by fire:

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 21

As records are not maintained it is somewhat difficult to know the value of stock lost and consequently the claim on such loss of stock. The following steps are involved:

a. Determine the estimated value of stock on the date of occurrence of fire by preparing a memorandum trading account for the period of commencement of accounting year to the date of occurrence of fire. This is shown under the following Performa.

Memorandum Trading A/c Particulars Amount Particulars Amount To opening stock To purchases To manufacturing expenses To gross profit (Calculated as percentage of sales)

xx xx xx

xxx

By sales By closing stock

xx xx

xxx

b. Ascertain the amount of stock lost by the occurrence of fire. The following formula is used: Amount of stock lost by fire = Value of stock as shown by Memorandum Trading a/c – Value of stock saved or salvaged.

c. Apply the average clause, if applicable. Claim Settling Process

1. Intimation to Insurance Company: The insured must give immediate intimation to the insurance company regarding the loss. The necessary details like the day, date, time and causes of fire and in case of marine insurance, ship and voyage taken should be mentioned.

2. Assessment of the loss: The insured makes an assessment of the actual loss. Such assessment is required to fill the claim forms correctly in respect of the loss of goods or property.

3. Submission of the claim form: the insured must fill all possible details in the claim form. He must lodge the claim form within 15 days of the fire to claim compensation. In case of marine insurance, the insured should lodge a claim with the following documents: Original Insurance Policy Copy of pill of Lading A copy of commercial Invoice A copy of packing list Survey report Claim Bill

Delay in submission of claim form may result in non-acceptance of the claim.

4. Evidence of Claim: Along with the claim form, the insured must send certain proof of fire and other records, if available and if necessary. The evidence should enable the insurance company to deter-mine the amount of loss.

5. Verification of Form: The claim form along with the sup-porting evidence is verified by the insurance company. The insurance company then appoints the surveyors to conduct an assessment of the actual loss.

6. Survey: After the receipt of the form, and necessary verification, the insurance company appoints the surveyors to assess the actual loss. The surveyors conduct the necessary investigations. They investigate into the cause of fire, the actual amount of property lost and other relevant details. The surveyors then make the report of their findings and assessment of the loss.

7. Landing Remarks: In case of marine insurance, the insured should obtain landing remarks, from the port authorities, if survey report is not obtained.

8. Appointment of the arbitrator: There may be v dispute regarding the amount of claim. In such a case, an arbitrator is appointed, acceptable to both the parties, to settle the amount of the loss.

9. Settlement of Claims: If there is no dispute between the two parties, as to the amount of loss, the insurance company then makes necessary payment to the insured. In case of marine insurance, the amount of money is paid to India Exporter in Indian rupees. If the claimant is not a resident of India, payment maybe made in foreign currency.

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 22

UNIT-IV Investment Accounts

Meaning of Investment Investments are the amounts which are invested as capital or in some securities of Public or Private sector for earning income. Meaning of Investment Accounts- An account to find position of investment and profit and loss on this investment Type of Securities: (i) Central Govt. Securities, (ii) State Govt. Securities, (iii) Securities of local authorities, (iv) Non-Govt. Securities or Securities of Private sector, Private Institutions or Persons. E.g. bonds, shares debentures, etc.

TYPES OF INVESTMENTS

1. Fixed Investments: These investments are made with the sole object of making fixed income in the shape of interest or dividend or both. Not to make profit by selling them.

2. Floating Investment: These investments are made with the sole object of making profit by selling them when prices are favourable. They are valued at cost price or market price, whichever is lower.

SALE AND PURCHASE PRICE OF INVESTMENTS

1. At Par Price: When investments are purchased or sold at face value. e.g. share of Rs. 100 at Rs. 100.

2. At Discount Price: When investments are purchased at less than face value, this is purchase at discount, as share of Rs. 100 is purchased at Rs. 98.

3. At premium Price: When investments are purchased or sold at above face value, it is known as purchase at Premium; as a share of Rs. 100 is purchased at Rs. 102.

INTEREST ON INVESTMENTS

Cum-interest and Ex-interest Purchase and Sale If after sometime of the date of declaration of interest investments are purchased and buyer gets the right of receiving interest on the next declaration date of interest for whole period, i.e., the period from the last declaration date before the date of purchase upto the next declaration date which falls after the date of purchase, such purchase is called cum-interest purchase. From sellers point of view, it is known as cum-interest sale. In case of ex-interest, the price quoted is exclusive of interest from the last date of interest payment to the date of transaction i.e. in this case buyer has to pay to the seller the accrued interest in addition to the price for the investment.

EXPENSES OF SALE AND PURCHASE OF INVESTMENT

Expenses of sale and purchase mostly are Brokerage, Commission and Stamp Fee, etc. These expenses are always added in the purchase price whether these purchase are cum-int. or ex-int. These expenses are always deducted from the sale price whether these sale are cum-int or ex-int.

Value of Investment at a Glance Cum-int. Purchase

Purchase Price + Purchase Expenses. – Interest for the period from last declaration date upto date of purchase.

Ex-int. Purchase

Purchase Price + Purchases Exps. – Interest is neither added nor deducted, but is paid separately for the period from the last declaration date upto the date of purchase.

Cum-int. Sale Sale Price – Sales Exps. – Interest for the period from last declaration take up to date of sale.

Ex-int. Sale Sale Price – Sales Exps. Interest is neither added nor deducted. Interest is taken separately from the last declaration date upto the date of sale.

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 23

Journal entries for Investment Accounting: a) For investment purchase: Investment A/c dr. Interest /dividendA/c dr. To Bank A/c. b) For investments sold: Bank A/c dr. To investment A/c To interest/dividend A/c

c) Interest received on due date: Bank A/c dr. To interest /dividend A/c d) Amount of interest or dividend transferred to P&L Ac at the end of the year:

Interest /dividend A/c dr. To P&L A/c

Rules to be considered while preparing investment account. 1 .Interest on debentures or bonds is to be calculated twice in a year while dividend on shares is to be calculated once in a year. 2. Interest/dividend is calculated on the face value of securities/shares. 3. Expenses and brokerage will also be calculated on face value of securities. 4. In case of purchases, expenses will be added and in case of sale, expenses will be deducted. 5. In case of cum-interest transaction, back-interest will be deducted, and in case of ex-interest ransaction, back-interest will not be deducted but it will be calculated and recorded separately. If nothing is mentioned, then it will always be considered as cum-interest transaction. 6. Due interest will be calculated on investments on due dates at given rates. 7. If the last date of interest and the date of year ending are not the same, then accrued interest will be calculated from the last date of interest up to the date of year ending. The following entry is passed: Accrued interest A/c Dr. Interest A/c Next year , the opening entry will be : Interest A/c Dr. To Accrued Interest A/c 8. Closing balances of the investments will be calculated on the following basis: a) If investments are of fixed type , then at cost. b) If investments are of floating nature , then they are valued at cost or market price , whichever is less. 9 .If the market price of debentures or bonds is given cum-interest and accrued interest is also calculated then the amount of accrued interest will first be deducted from the market price and remaining value will be compared with cost price.

METHODS OF KEEPING INVESTMENT ACCOUNT Investment Account can be kept in two ways namely (i) To prepare Investment Account and Interest Account separately, and (ii) To prepare Columnar Investment Account. Investment Account: When investments are floating, then its balance is transferred to Profit and Loss account. If all the investment are not sold, then closing balancing of investment is valued at cost price or market price whichever is lower. If Investments are fixed, then its balance is carried forward, at cost. Closing of Interest Account : Balance of Interest Account is transferred to Profit and Loss Account.

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 24

Closing of Accrued Interest Account: Accrued interest is the interest for the period from that date of declaration of interest (which is closer to closing date of the year) upto the closing date of the year. Balance of this account is carried forward. This interest has been earned but has not been received.

INVESTMENTS ON WHICH DIVIDENDS ARE EARNED

1. Cum-div. Purchase and Sale Dividend is the income which a shareholder receives on the shares of a company. This dividend is based on the profit of whole year of the company. If shareholder sells his shares cum-dividend after the date of declaration of dividend and before the date of receipt of dividend, then buyer gets the right of getting dividend on these shares. Therefore, seller takes the amount of dividend also in addition to the price of shares from the purchaser. Real price of shares can be found out by deducting the amount of dividend from the market price of shares.

2. Ex-div. Purchase and Sale Under this case whatever amount is received by the seller for investment, same is treated as price of investment. No amount of dividend is added to or deducted from it. 1

INSOLVENCY ACCOUNT

MEANING OF INSOLVENCY Any person, who fulfils the following two conditions, is called insolvent:

i. His liabilities should be more than his assets; and ii. He must be adjudged insolvent by a competent Court.

In India insolvency is governed by two acts, viz, i. The Presidency Towns Insolvency Act, 1909, which applies to the persons residing in the

Presidency towns of Mumbai, Kolkata, Chennai. Delhi. ii. The Provincial Insolvency Act, 1920, which applies to the persons residing in the rest of

India. The insolvency proceeding will be conducted by the official assignee in presidency towns and by the official receiver in other places. INSOLVENCY PROCEDURE

1. Petition for adjudication as insolvent may be presented either by the debtor or by the creditor in a Court having jurisdiction under this Act.

a. A creditor shall be entitled to present an insolvency petition against a debtor if the debts owing by the debtors to the creditors, amounts to five hundred rupees, the debt is a liquidated sum payable either immediately or at some certain future time; and the act of insolvency has occurred within three months before presentation of petition.

b. A debtor shall be entitled to present an insolvency petition if he is unable to pay his debts, and : (i) his debts amount to five hundred rupees;(b) he is under arrest to imprisonment in execution of the decree of any Court for the payment of money, or (c) an order of attachment is subsisting against his property.

2. When an insolvency petition has been accepted, the court shall make an order fixing a date for hearing the petition .

3. It may appoint an interim receiver of the property of the debtor and may direct him to take immediate possession thereof.

4. If the Court is satisfied that the petition the reasonable, it shall make an order of adjudication and shall specify in such order the period within which the debtor shall apply for his discharge.

5. Effect of an Order of Adjudication (i) on making the order of adjudication, the whole of the property of the insolvent shall become divisible among the creditors, (ii) the insolvent shall aid to the utmost of his power in the realization of his property and the distribution of his proceeds among his creditors.

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 25

Difference between both Acts Basis of difference Presidency Towns Insolvency Act

1909 Provisional Insolvency Act 1920

1. Government dues

All Govt. dues are considered preferential.

Here also all Govt. dues are treated as preferential.

2. Legal liability

The compensation payable under Factories Act, Workmen Compensation Act etc. are preferential

Here also these payments are preferential.

3. Salary due to clerks during the last four months

The maximum amount per head is Rs.300

The figure is Rs. 20 per head.

4. Wages due to workers during the last four months

The maximum amount per head is Rs.100

The figure is Rs. 20 per head

5. Rent One month’s rent is preferential Rent is treated unsecured. Rate if final dividend Net amount realizable from assets – Liquidation expenses Rate of dividend = Amount payable to unsecured creditors

STATEMENT OF AFFAIRS

Gross Liabilities

Liabilities (as stated and estimated by the Debtor)

Expected to Rank

Assets (as stated and estimated by the Debtor)

Estimated to Produce

Rs. Unsecured Creditors as per list A Fully Secured Creditors as per list B Estimated value of Securities ………………….. surplus Less: Amount thereof carried to list C…………. Balance thereof to contra Partly Secured Creditors as per list C Less: Estimated value of Securities Preferential Creditors as per list D (Creditors for Rates, Taxes, Salaries and Wages, etc. , payable, in full as per list D) Deducted as per contra

Rs.

Property as per list E viz: a. Cash at Bankers b. Cash in hand c. Cash deposited with Solicit or for cost of Petition d. Stock-in-Trade e. Machinery f. Trade Fixture Fittings, Utensils, etc. g. Furniture h. Life Ins.Policies i. Other Property Book debts as per list F viz: Good Doubtful Bad Bills of exchange or other similar Securities as per List G Surplus from Securities in the hands of creditors fully Secured (per contra) Deduct: Creditors for Preferential, Rates, Taxes, Salaries and Wages, etc. (per contra)

Rs.

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 26

Rs

Deficiency as per List H Rs.

SPECIMEN OF DEFICIENCY ACCOUNT Excess of assets over liabilities or capital interest on Capital Trading Profits Profit on speculation Liabilities waived off Loan from wife Profit on realization Deficiency as per statement of affairs Rs.

Rs.

-------

Excess of liabilities over assets or losses from business Drawings Bad Debts Other Losses: Stock Furniture Buildings Plant & Machinery, etc. Bills discounted & dishonored Trade Expenses Speculation Losses, etc. Rs.

Rs.

------

Difference between Profit and Loss Account and Deficiency Account basis of difference Profit and Loss Account Deficiency Account 6. Date of Preparation 7. Period of its Preparation 8. Capital 9. Difference 10. Sides

This is often prepared at the end of financial year. It is prepared in all the year during which business is carried on Capital is recorded in it. Excess of debit over credit of this account is a loss and excess of credit over debit of this account is profit. In this account left side is for expenses and losses and right hand side for gain and income.

It is prepared only once in life of the business and that too, only if insolvency occurs. Capital is recorded in it. Excess of the amount of right side over the amount of left side is called deficiency. Its left hand side is for gains and right hand side is for losses.

Difference between Balance Sheet and Statement of Affairs

Basis of difference Balance Sheet Statement of Affairs 1. Date of Preparation

It is often prepared at the end of the year.

It is prepared at the time of insolvency.

2. Use of Lists Lists are not used for writing of assets Lists are used for assets and

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 27

and liabilities

liabilities.

3. Records of Assets

All real and fictitious assets are recorded in it.

Only real assets are recorded in it.

4. Value of assets

Fixed assets are shown after deduction of depreciation.

Fixed assets are shown at realizable value.

5. Assets lodged as security

Assets as a security are shown in the assets side.

The assets lodged as security are not shown in the assets side but shown in the liability side along with the concerning loan.

6. Record of Liabilities

Columns of gross liabilities and expected to rank are not made in it.

These columns are made in it.

7. Total

Total of liabilities is equal to total of assets.

Total liabilities are more than total of assets and this excess is called deficiency.

8. Number

It is prepared for all the year during which business is carried on.

It is prepared only once i.e. at the time of insolvency.

9. Object

It is prepared for knowing the financial position of the concern.

It is prepared to shoe the inability of the debtor to pay this debts.

10. For whom prepared

It is prepared for the sake of proprietor and others.

It is prepared for the satisfaction of the Court.

11. Def. A/c

Deficiency Account is not prepared along with it.

Deficiency Account is prepared along with it.

12. Act

In case of Sole Trader and Firm, there is no act for its preparation but in the case of Companies it is prepared according to the Companies Act.

It is prepared under the Presidency Towns insolvency Act or Provincial Insolvency Act.

13. Pref. Crs.

Preferential Creditors are not deducted in the assets side.

Preferential Creditors are deducted in the assets side.

14. Capital Capital is shown in the liabilities side. Capital is not shown in the liabilities side.

Voyage Account Voyage accounts are maintained by shipping companies which undertakes transport of goods and programmers from one part to another. The consideration charged is freight or fare. The service rendered by shipping companies is commercial in nature and hence it is desirable to know the profit or loss involved in every voyage. Voyage accounting It resembles to a profit & loss account. It is prepared for each voyage (i.e. inward and outward voyage undertaken by a ship, unlike other organization which prepares Profit & Loss account at the end of accounting year. On the debit side of voyage account all expenses incurred are recorded and on the

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 28

credit side at income are recorded. The difference between these two sides indicates profit or loss on a particular voyage. This profit or loss is transferred to the profit & loss account of a shipping company or the charter of a ship. Expenses which appear on the Debit Side of Voyage Account

1. Address Commission – It is commission paid by a shipping company to agents who procure business to it. This amount is fixed as certain percentage on the total freight (inward and outward) earned.

2. Coal – Coal is used as a fuel by the ship. This can be recorded in any of the two ways. Firstly the opening of coal and the purchases of the same are debited to voyage account and the closing stock of coal credited to voyage account. Alternatively, the purchases of coal are added to opening stock and closing stock of coal is deducted to get the cost of coal consumed.

3. Consumable or Sundry Stores – These include items such as cotton waste, oil grease etc. used in a ship for as particulars voyages.

4. Insurance premium – This may relate to a ship or cargo carried. Proportionate amount of premium applicable for the voyage is to be considered in the voyage a/c.

5. Depreciation on the Ship – Depreciation on the ship relating to voyage period is to be considered in the voyage a/c.

6. Stevedoring Charges – It refers to loading and unloading charges incurred by a shipping company during the voyage of a ship.

7. Dispatch money – The refund of excess freight collected by a shipping company to the shipper of goods is known as dispatch money.

8. Salaries and wages payable to the crew of the ship are debited to voyage account. 9. Harbor and Port Charges – These are expenses incurred by a shipping company at various

ports. 10. Administration Expenses – This includes printing stationery, postage and such other

expenses. Income which appear on the Credit

1. Freight earned – The charges collected by the shipping company form the shippers of goods for carrying goods high seas are known as freight. It is earned on the outward and inward journey of a ship.

2. Primage – The additional freight collected by a shipping company from the shippers of goods is known as primage. In the earlier years primage was collected with a view to pay to the captain of the ship to encourage him to take special care of cargo. In recent time the primage is returned by the shipping company.

3. Passage money – It represents the fare collection by a shipping company from passengers carried in a ship during a particular voyage.

Incomplete Voyage When the journey is still progress at the end of the year it is regarded as incomplete voyage. The proportionate expenses relating to incomplete voyage is treated as voyage in progress and carried forward as Voyage in Progress. It appears on the credit side of voyage account as incomplete voyage appears in the voyage account on the debit side as “To freight received in advance” or “passage money received in advance”. Suppose one voyage has to complete by going to Landon from Mumbai and then return from London to Mumbai. At the end of year, if travelling from Landon to Mumbai is continuing, at that time, we have to calculate expenses and incomes on incomplete voyage and treat according to accounting rule.

a. Receiving of Advance Income – We will deduct advance income of incomplete voyage from total voyage income or show in the debit side of voyage account.

b. Paying of advance Expenses – We also will deduct advance expenses of incomplete voyage from total expenses of show in credit side of voyage account

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 29

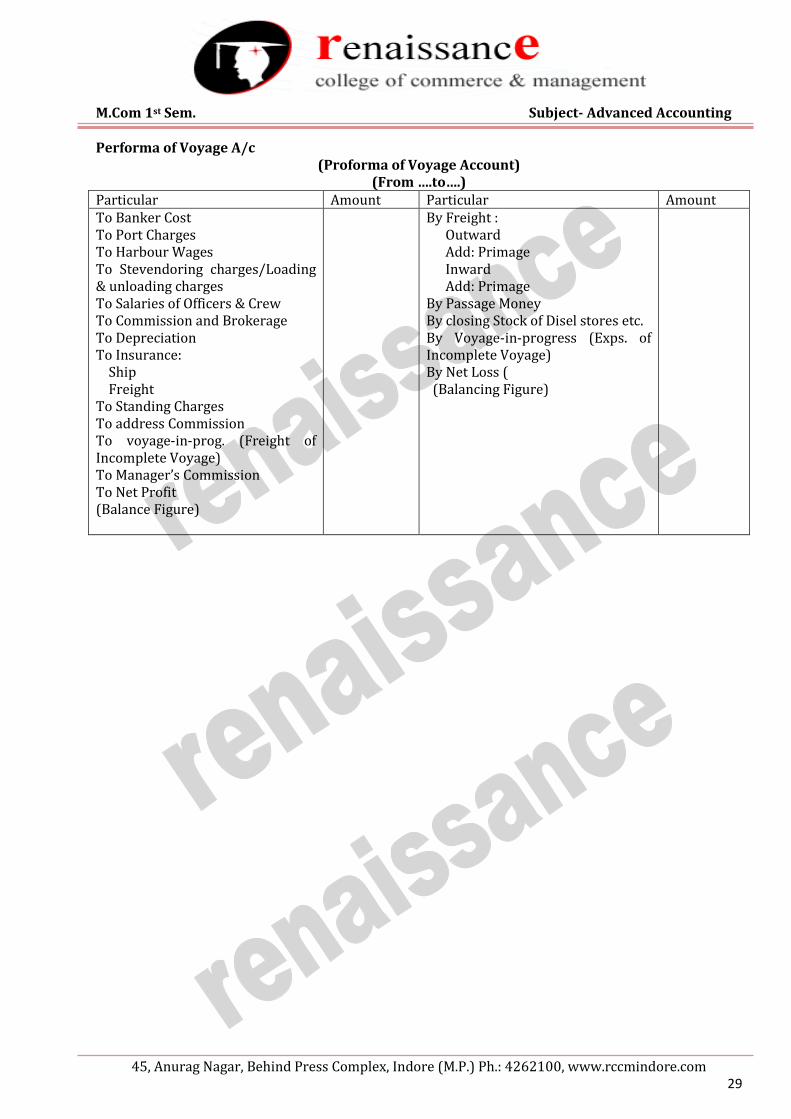

Performa of Voyage A/c (Proforma of Voyage Account)

(From ….to….) Particular Amount Particular Amount To Banker Cost To Port Charges To Harbour Wages To Stevendoring charges/Loading & unloading charges To Salaries of Officers & Crew To Commission and Brokerage To Depreciation To Insurance: Ship Freight To Standing Charges To address Commission To voyage-in-prog. (Freight of Incomplete Voyage) To Manager’s Commission To Net Profit (Balance Figure)

By Freight : Outward Add: Primage Inward Add: Primage By Passage Money By closing Stock of Disel stores etc. By Voyage-in-progress (Exps. of Incomplete Voyage) By Net Loss ( (Balancing Figure)

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 30

UNIT-V DISSOLUTION OF PARTNERSHIP FIRM WITH INSOLVENCY

Dissolution of firm – The dissolution of partnership between all the partners of a firm is called the dissolution of the firm. In the case of dissolution of a firm, the business of the firms is closed down and its affairs are wound up. The assets are realized and the liabilities are paid off. Model of dissolution of firm – 1) Dissolution without the intervention of the court

a) Dissolution by agreement b) Compulsory dissolution c) Dissolution on the happening of certain contingencies. d) Dissolution by notice

2) Dissolution by the court a) Insanity b) Permanent incapacity c) Misconduct d) Breach of agreement e) Transfer of interest f) Loss in business g) Just and equitable

Steps in the dissolution process – Step 1 Prepare a balance sheet of the firm as on the date of the dissolution of the firm. Step 2 Realize the non-cash assets which are not acceptable for distribution in their present form,

pay the debts of the firm to third parties. Realization account is prepared to calculate the loss or profit on realization of assets and settlement of liabilities. Loss or profit on realization of assets and settlement of liabilities is transferred to partners’ capital accounts.

Step 3 Pay the amount due to each partner ratably for advances (or Loan) Step 4 Pay the available cash to the partners. Accounting treatment on dissolution of firm – In case of dissolution of firm the following accounts are prepared to close the books of the firm –

1) Realisation Account 2) Partners’ loan account 3) Parnters’ capital account 4) Cash or bank account

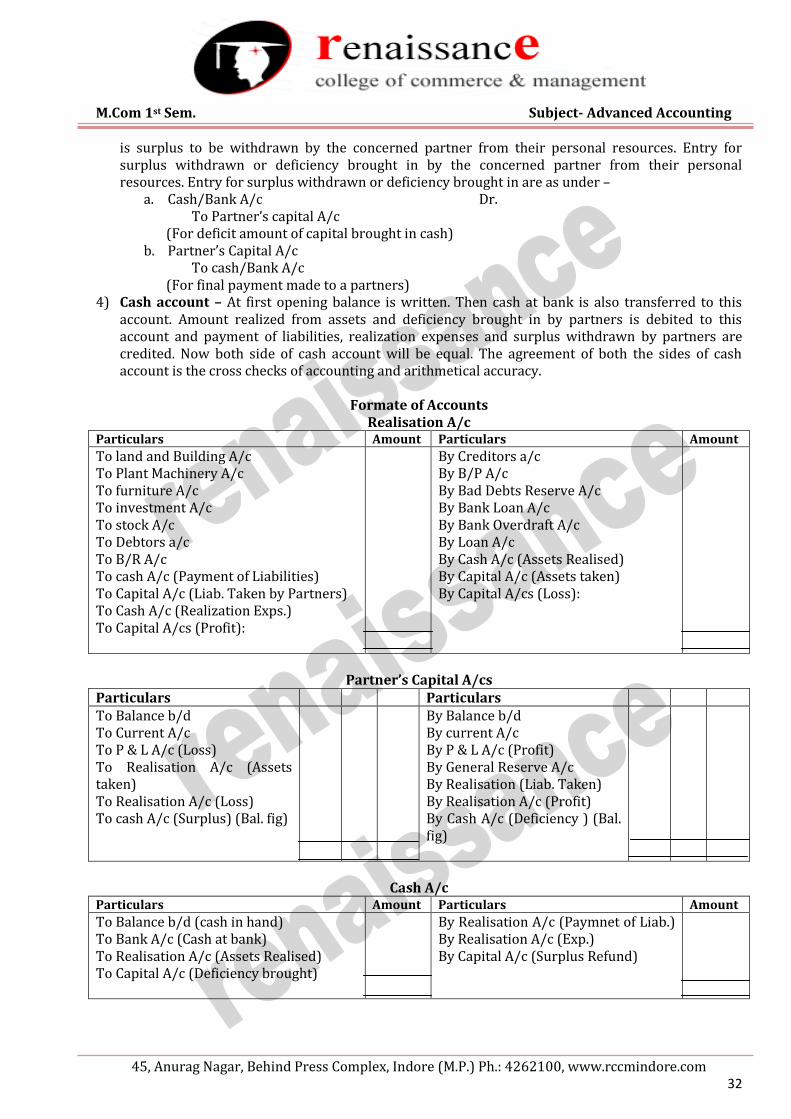

1) Realization account – This is a special type of account. It is a nominal account. The purpose of

preparing this account is to find out the result of realization of assets and discharge of liabilities. The following steps involved in preparing this account.

Step 1. For Transfer of all accounts given in the balance sheet a. For transfer of assets – All the assets except cash in hand, cash at bank, debit balance of

current accounts of partners and fictitious assets are transferred to debit of this account at book values as under –

Realisation A/c Dr. To Various assets (individually) (For transfer of various assets to realization a/c)

b. For transfer of outside liabilities – All the external liabilities including partners loan are transferred to the credit of realization account at book value as under –

Various Liabilities A/c Dr. To Realisation A/c

(For transfer of various liabilities to realisation a/c)

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 31

Note: Liabilities have got credit balance, so debiting to close them. Step 2. Disposal of assets

a. For sale of assets Cash / Bank A/c Dr.

To Realisation A/c (For assets realised in cash)

b. Asset taken over by partner Partner's Capital A/c Dr.

To Relisation A/c (For assets taken over by a partner)

Step 3. Entry for payment of dissolution expenses a. For cash payment

Realisation A/c Dr. To Cash / Bank A/c

(For payment of dissolution expenses) b. For payment made by a partner

Realisation A/c Dr. To Partner's Capital A/c

(For dissolution expenses paid by a partner) Note : if any partner is to bear all expenses of realisation, no journal entry is required in the books of the firm but in this case if the partner is paid the realisation expenses, the following entry will be made :

Partner's Capital A/c Dr. To Cash / Bank A/c

(For dissolution expenses paid on behalf of a partner.) Step 4. Entry for payment of outside liabilities :

a. For cash payment Realisation A/c Dr.

To Cash / Bank A/c (For payment to outside liabilities)

b. For liabilities taken over by a partner Realisation A/c Dr.

To Partner's Capital A/c (For liabilities taken over by a partner)

Step 5. Entry for closing realisation account a. In case of profit

Realisation A/c Dr. To Partners' Capital A/c

(For profit on realisation transferred to partner's capital a/cs in their profit sharing ratio) b. In case of loss

Partners' capital A/cs Dr. To Realisation A/c

(For loss on realisation transferred to partners' capital a/cs in their profit sharing ratio) Note : (1) Intangible assets such as goodwill, patents, copyrights, prepaid expense are normally value less in case of dissolution. So if a question is silent it should be presumed that nothing could be realised from such assets. (2) If question is silent about the realisation of tangible assets it is presumed that their book values have been realised. 2) Partner’s loan Account – This are transferred to the credit side of realization account and the

payments there of are shown on debit side of realization account. Alternatively the payment can be credited directly to cash account.

3) Partner’s capital accounts – All the reserved and undivided profit or loss, realization profit or loss, balance of current accounts. Now the difference is adjusted in cash if there is credit balance it

M.Com 1st Sem. Subject- Advanced Accounting

45, Anurag Nagar, Behind Press Complex, Indore (M.P.) Ph.: 4262100, www.rccmindore.com 32

is surplus to be withdrawn by the concerned partner from their personal resources. Entry for surplus withdrawn or deficiency brought in by the concerned partner from their personal resources. Entry for surplus withdrawn or deficiency brought in are as under –

a. Cash/Bank A/c Dr. To Partner’s capital A/c

(For deficit amount of capital brought in cash) b. Partner’s Capital A/c

To cash/Bank A/c (For final payment made to a partners) 4) Cash account – At first opening balance is written. Then cash at bank is also transferred to this

account. Amount realized from assets and deficiency brought in by partners is debited to this account and payment of liabilities, realization expenses and surplus withdrawn by partners are credited. Now both side of cash account will be equal. The agreement of both the sides of cash account is the cross checks of accounting and arithmetical accuracy.

Formate of Accounts

Realisation A/c Particulars Amount Particulars Amount

To land and Building A/c To Plant Machinery A/c To furniture A/c To investment A/c To stock A/c To Debtors a/c To B/R A/c To cash A/c (Payment of Liabilities) To Capital A/c (Liab. Taken by Partners) To Cash A/c (Realization Exps.) To Capital A/cs (Profit):

By Creditors a/c By B/P A/c By Bad Debts Reserve A/c By Bank Loan A/c By Bank Overdraft A/c By Loan A/c By Cash A/c (Assets Realised) By Capital A/c (Assets taken) By Capital A/cs (Loss):

Partner’s Capital A/cs

Particulars Particulars To Balance b/d To Current A/c To P & L A/c (Loss) To Realisation A/c (Assets taken) To Realisation A/c (Loss) To cash A/c (Surplus) (Bal. fig)

By Balance b/d By current A/c By P & L A/c (Profit) By General Reserve A/c By Realisation (Liab. Taken) By Realisation A/c (Profit) By Cash A/c (Deficiency ) (Bal. fig)

Cash A/c

Particulars Amount Particulars Amount