Proceedings of the 2000 RAeS Conference on Light Aircraft ...

Upload

swiftCategory

view

51download

2

SWIFT Welcome

Address

Alain Raes

Chief Executive, APAC & EMEA

Welcome

2015 Delegates

8,212

A Smart Financial Centre

Innovation

Regulation

Cyber

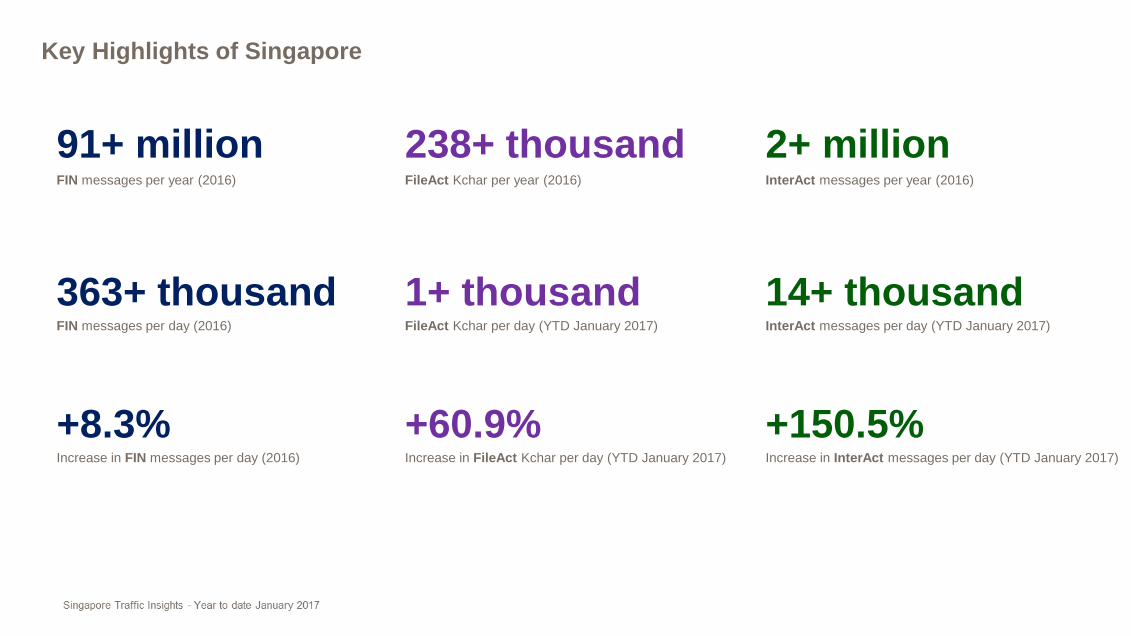

Key Highlights of Singapore

91+ million FIN messages per year (2016)

363+ thousand FIN messages per day (2016)

+8.3% Increase in FIN messages per day (2016)

238+ thousand FileAct Kchar per year (2016)

1+ thousand FileAct Kchar per day (YTD January 2017)

+60.9% Increase in FileAct Kchar per day (YTD January 2017)

2+ million InterAct messages per year (2016)

14+ thousand InterAct messages per day (YTD January 2017)

+150.5% Increase in InterAct messages per day (YTD January 2017)

ASEAN region Key Highlights

200+ million FIN messages per year (2016)

831+ thousand FIN messages per day (YTD January 2017)

+17.1% Increase in FIN messages per day (YTD January 2017)

ASEAN Traffic Insights - Year to date January 2017 6

49+ million FileAct Kchar per year (2016)

347+ thousand FileAct Kchar per day (YTD January 2017)

>999% Increase in FileAct Kchar per day (YTD January 2017)

3+ million InterAct messages per year (2016)

16+ thousand InterAct messages per day (YTD January 2017)

+159.7% Increase in InterAct messages per day (YTD January 2017)

Achieving

Financial

Integration in the

ASEAN Region

Internal Disparities External Dependencies

Corporates underserved Slow FMI Modernisation

Low Digital Competency Stakeholder Alignment

Core problems hindering ASEAN Financial Integration

- AEC Blueprint 2025

“ASEAN in 2025: A Highly Integrated and Cohesive Economy”

Intra-ASEAN Disparity Increasing

Growth in Value Reduction in Value

Arrow width : Value of commercial flow, 2016

Bubble size: Total value of Incoming & outgoing commercial flows, 2016

%ages: Weighted total incoming & outgoing commercial flows with SG, 2016

Source: SWIFT Business Watch

ASEAN-5 & LCMVB Commercial Flows

LCMVB Commercial Flows - Geographic Split

..nearly half of cross-border, intra-ASEAN

commercial flow payments (by value) were

settled outside of ASEAN in 2016

US Dollar is predominant currency

settling 85% of total intra-ASEAN

commercial flows by weight, with usage

increasing by 10% in 2016

External Dependency For Payments Intermediation

Source: SWIFT Business Watch

Still reach

non-initiative

banks

Accessible

by any bank

Reaching

any bank

Tracker

Directory Observer

SLA rulebook

Core transaction banks

Value-added product suite

Messaging technologies

The future of

cross-border

payments

For banks

11

12

One year on, here are the achievements

4,000+ Average live payments / day

21 Banks successfully piloted

12 Banks are exchanging live gpi payments for

their corporate customers

93 Banks across

60+ Corridors (e.g. US – China; UK – Denmark; UK – Italy;

UK – Netherlands)

224 Countries

75% Of payments traffic on SWIFT represented

80,000+ Total live payments

13

A whole new world for banks and corporates

Confirmation Information

Speed &

Transparency

Certainty

50%

Europe,

Middle East,

Africa

30%

Asia Pacific

20%

Americas

64. National Australia Bank

65. Natixis

66. Nedbank

67. Nordea Bank*

68. Oversea-Chinese Banking Corporation

69. PKO Bank Polski

70. Promsvyazbank

71. Rabobank

72. Raiffeisen Bank International

73. Resona Bank

74. Royal Bank of Canada*

75. Royal Bank of Scotland

76. Sberbank

77. Siam Commercial Bank

78. Silicon Valley Bank

79. Skandinaviska Enskilda Banken

80. Société Générale

81. SpareBank 1

82. Standard Bank of South Africa

83. Standard Chartered Bank*

84. Sumitomo Mitsui Banking Corporation*

85. Swedbank

86. Tadhamon International Islamic Bank

87. TMB Bank

88. Toronto-Dominion Bank

89. UBS

90. U.S. Bank

91. UniCredit*

92. United Overseas Bank

93. Wells Fargo*

48. ICICI Bank

49. IndusInd Bank

50. Industrial and Commercial

Bank of China*

51. ING Bank*

52. Intesa Sanpaolo*

53. Intl. FCStone

54. Investec

55. Itaù Unibanco

56. JPMorgan Chase Bank*

57. Kasikornbank

58. KBC Bank

59. KEB Hana Bank

60. Lloyds Bank

61. Mashreq Bank

62. Maybank

63. Mizuho Bank*

31. Commerzbank

32. Crédit Agricole

33. Crédit Mutuel-CIC Banques

34. Credit Suisse

35. CTBC Bank

36. Danske Bank*

37. DBS Bank*

38. Deutsche Bank

39. DNB Bank

40. Ecobank

41. E.Sun Commercial Bank

42. Erste Group Bank

43. Fifth Third Bank

44. FirstRand Bank

45. Handelsbanken

46. Helaba Landesbank Hessen-

Thüringen

47. HSBC Bank

(*) Pilot bank in 2016

1. ABN AMRO Bank

2. ABSA Bank

3. Alfa-Bank

4. Agricultural Bank of China

5. Australia and New Zealand

Banking Group*

6. Axis Bank

7. Banco Bilbao Vizcaya Argentaria

8. Bangkok Bank

9. Bank of America Merrill Lynch*

10. Bank of China*

11. Bank of New York Mellon*

12. Bank of Nova Scotia

13. Bank of the Philippine Islands

14. Bank of Tokyo-Mitsubishi UFJ*

15. Banco Bradesco

16. Banco Santander

17. Banco de Crédito del Peru

18. Banco do Brasil

19. Banorte

20. Banque Européenne d’Investissement

21. Barclays*

22. Bidvest Bank

23. BNP Paribas*

24. Budapest Bank

25. CaixaBank

26. Canadian Imperial Bank of Commerce

27. China Construction Bank

28. China Merchants Bank

29. Citibank*

30. Commonwealth Bank of Australia

93 gpi banks

Channelling payments

into 224 countries

Representing 75% of all

SWIFT cross-border

payments

Global traction

14

CSP | Framework

Customer Security Programme

While all SWIFT customers are

individually responsible for the security of

their own environments, a concerted,

industry-wide effort is required to

strengthen end-point security

On May 27th SWIFT announced its

Customer Security Programme that

supports customers in reinforcing the

security of their SWIFT-related

infrastructure

CSP focuses on mutually reinforcing

strategic initiatives, and related enablers

15

Transforming the ASEAN

landscape with Innovation

and Cybersecurity