Swedbanks first quarter results 2011 CEO presentation

24

Swedbank’s first quarter 2011 results Michael Wolf, CEO Erkki Raasuke, CFO Göran Bronner, CRO

-

Upload

swedbank -

Category

Economy & Finance

-

view

593 -

download

3

description

Swedbank's CEO Michael Wolf presents the first quarter results 28 April 2011.

Transcript of Swedbanks first quarter results 2011 CEO presentation

Swedbank’s first quarter 2011 resultsMichael Wolf, CEOErkki Raasuke, CFOGöran Bronner, CRO

Strong start to the year

• Net profit of SEK 3.9bn for Q1

• Core Tier 1 capital ratio of 14.9 per cent

• Return on equity of 16.1 per cent in Q1

2

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11

Net profit performance

Lehman contribution

Follow-up on priorities 2011

• Customer focus

• Growth in selected segments

• Quality and effectiveness

• Robust and low-risk balance sheet

3

NII supported by higher interest rates• One-offs and higher stability fee shadowing underlying NII growth• Improving deposit margins in Retail • Government guarantee cost kept within Treasury

4

Net interest income

4 023 3 799 3 980

4 527

Retail LC&I Baltic Banking

Russia, Ukraine

Treasury, Other

173

2 925

117

850

-171 997

29 188

-148

-433

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11

(SE

Km

)

4 527

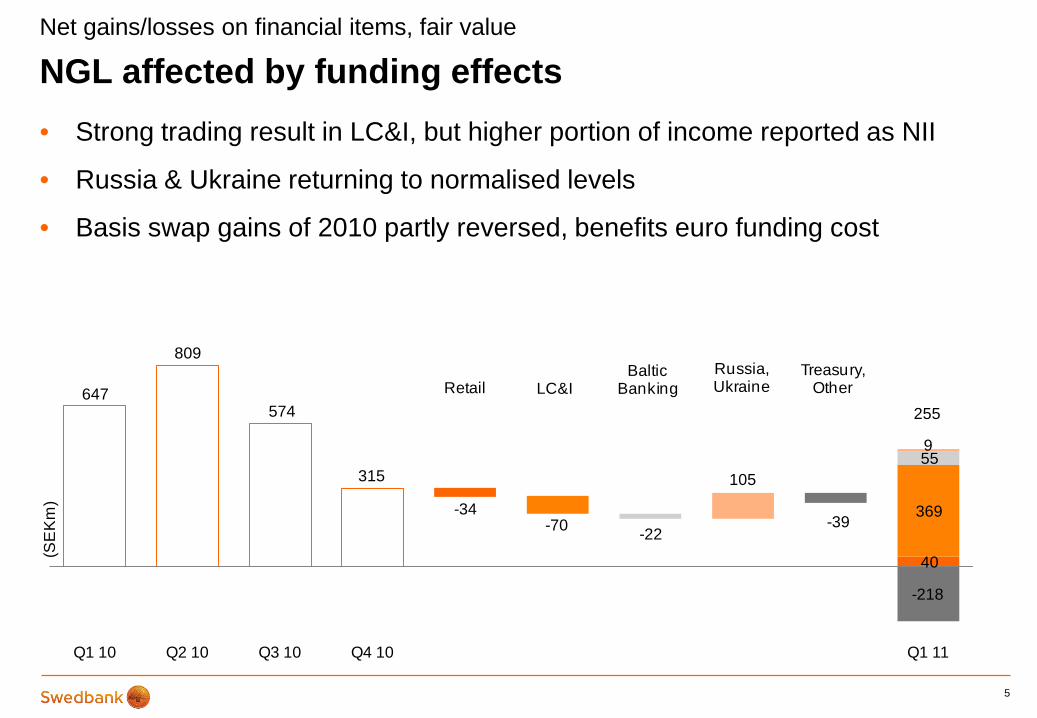

NGL affected by funding effects• Strong trading result in LC&I, but higher portion of income reported as NII

• Russia & Ukraine returning to normalised levels

• Basis swap gains of 2010 partly reversed, benefits euro funding cost

5

Net gains/losses on financial items, fair value

647

809

574

315

Retail LC&IBaltic

BankingRussia, Ukraine

Treasury, Other

-34

40

-70369

-22

55 105

9

-39

-218

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11

(SE

Km

)

255

Stable year-on-year expenses• Enhancing internal capabilities

– Key recruitments in Q1– Lower consultancy costs

• Improving cost/income ratio driven by one-off income

6

Expenses

4 391 4 423 4 238 4 590

Retail LC&I Baltic Banking

Russia, Ukraine

Treasury,Other

-30

2 193

-18

859

-39

658

-39172

-80 502

0.57 0.57 0.55 0.580.52

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11

(SE

Km

)

4 384

7

First quarter 2011 results

Income statementSEKm Q1 11 Q4 10 Δ Q1 10Net interest income 4 527 4 527 0 4 023

Net commission income 2 301 2 538 -237 2 282

Net gains/losses 255 315 -60 647

Other 1 369 578 791 715

Total income 8 452 7 958 494 7 667

Total expenses 4 384 4 590 -206 4 391

Profit before impairments 4 068 3 368 700 3 276

Total impairments - 970 - 77 -893 2 260

Operating profit 5 038 3 445 1 593 1 016

Tax expense 1 182 693 489 469

Profit attributable to shareholders 3 852 2 750 1 102 536

8

First quarter 2011 results

Key ratios

Volumes, SEKbn Q1 11 Q4 10 Δ Q1 10Lending to the public 1 141 1 146 -5 1 168

Deposits from the public 502 517 -15 496

Covered bonds 477 410 66 389

Key ratios Q1 11 Q4 10 Q1 10Return on equity, % 16.1 11.7 2.4

Cost-income ratio 0.52 0.58 0.57

Core funding ratio, %* 114 121 127

Core Tier 1 capital ratio, %** 14.9 13.9 12.3

* Lending/(deposits+covered bonds+retail bonds), ** Basel 2

SEK 91bn term funding issued in Q1 2011

9

Liquidity & Funding

Issuance Q1 & maturities full year 2011 • First US covered bond issue (144A), dual tranche of USD 1bn each

• Two EUR benchmark covered bonds

• Maturities of nominal SEK 121bn for the remainder of 2011

• Average maturity of wholesale funding, including short-term funding, 30 months (39 months for covered bonds)

(nominal SEKbn)

-80

-60

-40

-20

0

20

40

60

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Continued improvements

• Asset quality – Decreasing impaired loans– FR&R/Ektornet according to plan

• Substantial recoveries – all countries

• Lehman income

• RWA decreased by SEK 22.3bn in Q1– SEK 11.0bn lower credit risk– SEK 8.7bn lower market risk

• Strong funding position

10

Risk highlights

Net recoveries of SEK 972m in Q1

• Net recoveries in all CEE countries

• Sweden – also recoveries

• Collateral revaluations, repayments and rating migration

11

Asset quality

2 210

963

120

-483-972

-1 500

-1 000

-500

0

500

1 000

1 500

2 000

2 500

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11

SEKmCredit impairments

Retail LC&I Baltic Banking Russia & Ukraine Other

One-off income in US commercial real estate lending

• One-off pre-tax income of SEK 716m in Q1 after agreement with Lehman

• Remaining gross exposure was USD 1.1bn as of 31 March 2011, consisting of 35 assets

• No. of repossessed assets are expected to increase (2 as of today)

• Over-collateralisation still intact

12

Asset quality

Corporate risk weights – focus on capital efficiency

• Several different work streams

• Expected gradual effect in small steps

• History not enough to predict future– Stress tests key steering tool– Transparency

13

Capital management

Source: SEB Enskilda Equity Research

0

10

20

30

40

50

60

70

80

90

Handelsbanken Swedbank SEB Nordea

%Corporate risk weights,

development Q1 09 - Q4 10

Buy-back programme

• As of 31 March the excess capital amounts to SEK 9.9bn

• Gradually during four quarters

• Both A-shares and preference shares

14

Capital management

13.0%

Risk appetite(ICAAP buffer,SEK 15.6bn)

Regulatory requirement(SEK 36.3bn)

Excess capital (SEK 9.9bn)

10.0%

7.0%

Extra buffer due to prevailing circumstances(SEK 15.6bn)

14.9%

Appendix

15

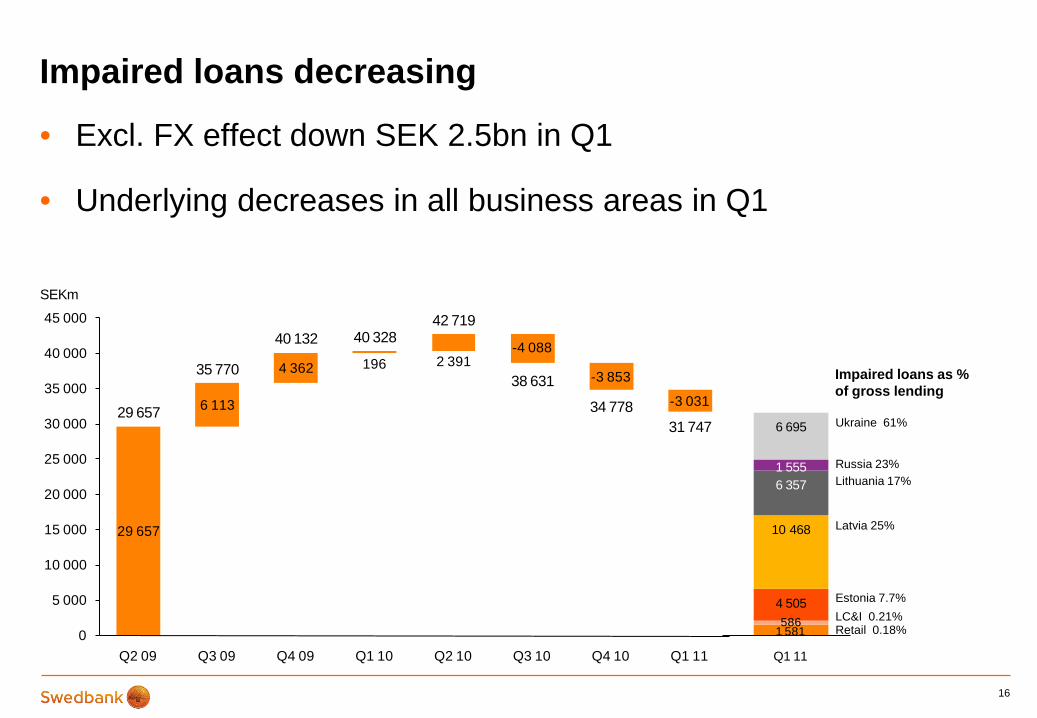

Impaired loans decreasing

• Excl. FX effect down SEK 2.5bn in Q1

• Underlying decreases in all business areas in Q1

16

Ukraine 61%

Russia 23%Lithuania 17%

Latvia 25%

Estonia 7.7%LC&I 0.21%Retail 0.18%

Impaired loans as % of gross lending

29 657

6 113

4 362 196 2 391-4 088

-3 853

-3 03129 657

35 770

40 132 40 32842 719

38 631

34 77831 747

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 000

Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11

SEKm

1 581586

4 505

10 468

6 3571 555

6 695

Q1 11

Loans past due 60 days – performance Q/Q

17

-150

-100

-50

0

50

100

150

200

250

Q1

10Q

2 10

Q3

10Q

4 10

Q1

11

Q1

10Q

2 10

Q3

10Q

4 10

Q1

11

Q1

10Q

2 10

Q3

10Q

4 10

Q1

11

Q1

10Q

2 10

Q3

10Q

4 10

Q1

11

Q1

10Q

2 10

Q3

10Q

4 10

Q1

11

EURm

Estonia Latvia Lithuania RussiaUkraine

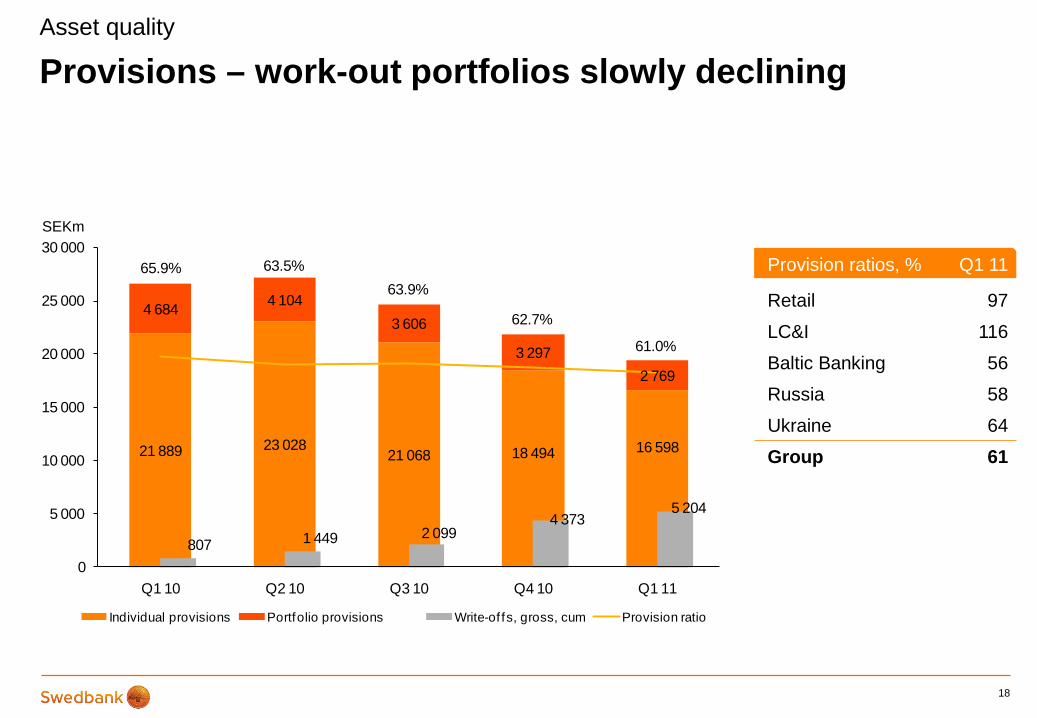

Provisions – work-out portfolios slowly declining

18

Provision ratios, % Q1 11

Retail 97

LC&I 116

Baltic Banking 56

Russia 58

Ukraine 64

Group 61

Asset quality

21 889 23 02821 068 18 494 16 598

4 684 4 1043 606

3 2972 769

807 1 449 2 0994 373

5 204

65.9% 63.5%63.9%

62.7%

61.0%

0

5 000

10 000

15 000

20 000

25 000

30 000

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11

SEKm

Individual provisions Portfolio provisions Write-of fs, gross, cum Provision ratio

Repossessed assetsAsset quality

19

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11

SEKm

Real Estate Residential Real Estate Commercial Passenger & Commercial Transport Shares Other

20

Real estate prices

Source: Swedbank, Estonian Land Board

Source: Swedbank, State Enterprise Centre of Registers

821

0200400600800

1 0001 2001 4001 6001 800

Jan-

05

May

-05

Sep

-05

Jan-

06

May

-06

Sep

-06

Jan-

07

May

-07

Sep

-07

Jan-

08

May

-08

Sep

-08

Jan-

09

May

-09

Sep

-09

Jan-

10

May

-10

Sep

-10

Jan-

11

Tallin

Nr.of deals EUR/m2Source: Swedbank

1 084

0200400600800

1 0001 2001 4001 6001 8002 000

Jan-

05

May

-05

Sep

-05

Jan-

06

May

-06

Sep

-06

Jan-

07

May

-07

Sep

-07

Jan-

08

May

-08

Sep

-08

Jan-

09

May

-09

Sep

-09

Jan-

10

May

-10

Sep

-10

Jan-

11

Vilnius

Nr.of deals EUR/m2

606

0200400600800

1 0001 2001 4001 6001 8002 000

Jan-

05M

ay-0

5S

ep-0

5Ja

n-06

May

-06

Sep

-06

Jan-

07M

ay-0

7S

ep-0

7Ja

n-08

May

-08

Sep

-08

Jan-

09M

ay-0

9S

ep-0

9Ja

n-10

May

-10

Sep

-10

Jan-

11

Riga

Nr.of deals EUR/m2

21

Long-term funding • Continued focus on covered bonds with Q1 issuance of SEK 85bn• SEK 4bn in senior unsecured issuance • 2 USD-denominated covered bond benchmark deals - of EUR 1bn each • 2 EUR-denominated covered bond benchmark deals of EUR 1bn and EUR 1.5bn • Total term funding maturities for the remainder of 2011 - of nominal SEK 121bn

21

Liquidity & funding

Long-term funding maturity profile, SEKbn

0

50

100

150

200

2011 2012 2013 2014 2015 2016

Senior unsecuredGuaranteed bonds

0

50

100

150

200

2011 2012 2013 2014 2015 2016

Covered bonds

22

Remaining government guaranteed debt • Exited the programme on 30 April 2010

• No issuance under the programme since summer 2009

• SEK 25bn of government guaranteed debt matured during Q1 2011

• Maturities of SEK 53bn for the remainder of 2011

22

Liquidity & funding

Maturity profile as per Q1 2011, SEKbn

0

20

40

60

2011 2012 2013 2014

USDSEKEURCHFHKDJPY

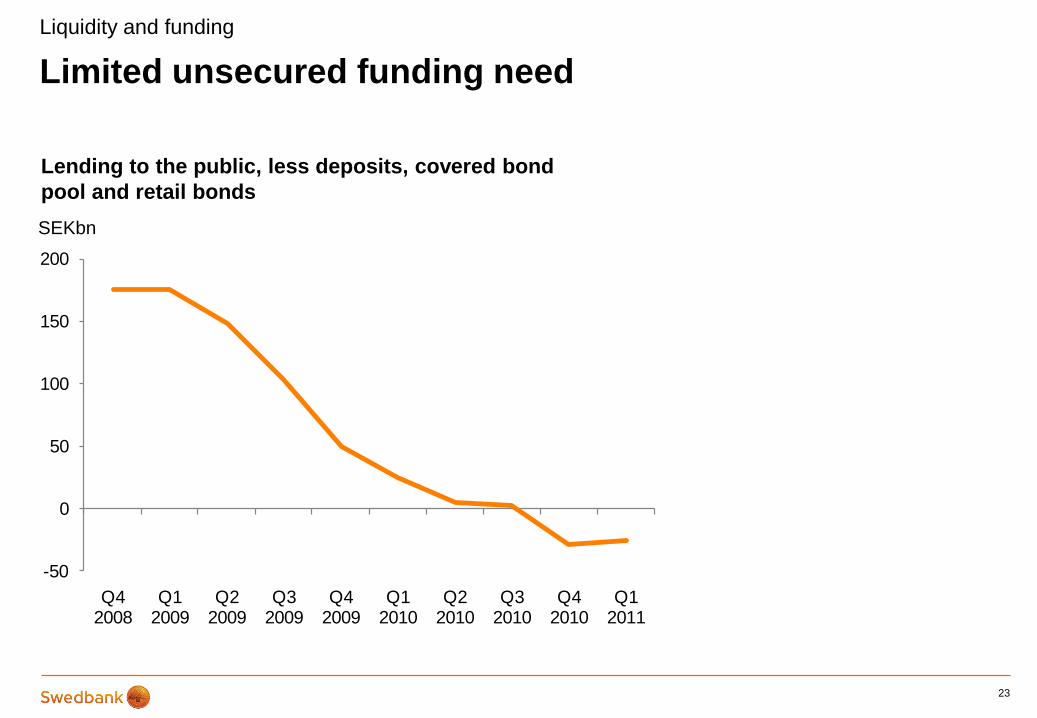

Limited unsecured funding need

23

Liquidity and funding

Lending to the public, less deposits, covered bond pool and retail bonds

-50

0

50

100

150

200

Q4 2008

Q1 2009

Q2 2009

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

SEKbn

Liquidity reserve*

24

Cash and holdings in central banks and deposits in other banks available o/n 63 437Securities issued or guaranteed by sovereigns, central banks or multilateral development banks 29 214Securities issued or guaranteed by municipalities or PSEs 0Covered bonds 53 366 - Issued by other institutions 53 272 - Own issued 93Securities issued by non-financial corporates 0Securities issued by financial corporates (excl. covered bonds) 1 869Other 0Total 147 886* As defined by the Swedish FSA

Liquid assets outside Treasury organisation 103 737

Total 251 623

SEKm