McGraw-Hill/Irwin ©2005 The McGraw-Hill Companies, All rights reserved McGraw-Hill/Irwin.

Upload

maud-gilbertCategory

view

217download

0

SwapsSwaps

Chapter 25

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.McGraw-Hill/Irwin

-225-2

Overview

The market for swaps has grown enormously and this has raised serious regulatory concerns regarding credit risk exposures. Such concerns motivated the BIS risk-based capital reforms. At the same time, the growth in exotic swaps such as inverse floater have also generated controversy (e.g., Orange County, CA). Generic swaps in order of quantitative importance: interest rate, currency, credit, commodity and equity swaps.

-325-3

Interest Rate Swaps

Interest rate swap as succession of forwards. Swap buyer agrees to pay fixed-rate Swap seller agrees to pay floating-rate.

Purpose of interest rate swap Allows FIs to economically convert variable-rate

instruments into fixed-rate (or vice versa) in order to better match the duration of assets and liabilities.

Off-balance-sheet transaction.

-425-4

Plain Vanilla Interest Rate Swap Example

Consider money center bank that has raised $100 million by issuing 4-year notes with 10% fixed coupons. On asset side: C&I loans linked to LIBOR. Duration gap is negative.

DA - kDL < 0 Second party is savings bank with $100

million in fixed-rate mortgages of long duration funded with CDs having duration of 1 year.

DA - kDL > 0

-525-5

Example (continued)

Savings bank can reduce duration gap by buying a swap (taking fixed-payment side).

Notional value of the swap is $100 million. Maturity is 4 years with 10% fixed-payments. Suppose that LIBOR currently equals 8% and

bank agrees to pay LIBOR + 2%.

-625-6

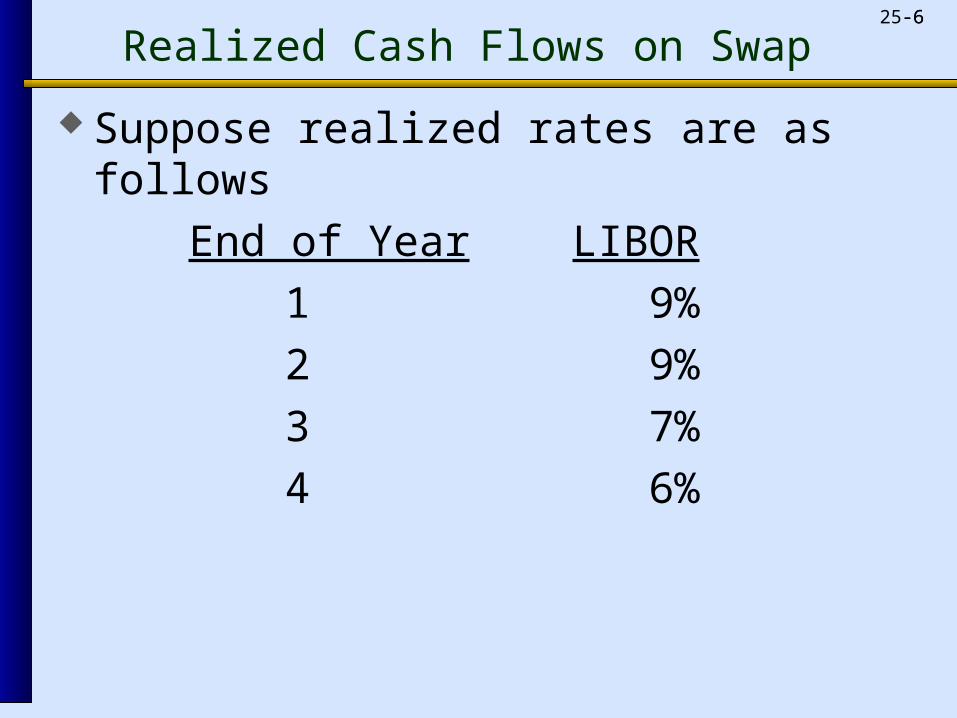

Realized Cash Flows on Swap

Suppose realized rates are as follows

End of Year LIBOR

1 9%

2 9%

3 7%

4 6%

-725-7

Swap Payments

End of LIBOR MCB Savings MCB

Year + 2% Payment Bank Net

1 11% $11 $10 +1

2 11 11 10 +1

3 9 9 10 - 1

4 8 8 10 - 2

Total 39 40 - 1

-825-8

Off-market Swaps

Swaps can be molded to suit needs Special interest terms Varying notional value

Increasing or decreasing over life of swap. Structured-note inverse floater

Example: Government agency issues note with coupon equal to 7 percent minus LIBOR and converts it into a LIBOR liability through a swap.

-925-9

Macrohedging with Swaps

Assume a thrift has positive gap such thatE = -(DA - kDL)A [R/(1+R)] >0 if rates rise.

Suppose choose to hedge with 10-year swaps. Fixed-rate payments are equivalent to payments on a 10-year T-bond. Floating-rate payments repriced to LIBOR every year. Changes in swap value DS, depend on duration difference (D10 - D1).

S = -(DFixed - DFloat) × NS × [R/(1+R)]

-1025-10

Macrohedging (continued)

Optimal notional value requiresS = E

-(DFixed - DFloat) × NS × [R/(1+R)]

= -(DA - kDL) × A × [R/(1+R)]

NS = [(DA - kDL) × A]/(DFixed - DFloat)

-1125-11

Currency Swaps

Fixed-Fixed Example: U.S. bank with fixed-rate assets

denominated in dollars, partly financed with £50 million in 4-year 10 percent (fixed) notes. By comparison, U.K. bank has assets partly funded by $100 million 4-year 10 percent notes.

Solution: Enter into currency swap.

-1225-12

Cash Flows from Swap

U.S. FI U.K. FI

Outflows (B/S) -10% × £50 -10% × $100

Inflows (Swap) 10% × £50 10% × $100

Outflows (Swap)

-10% × $100 -10% × £50

Net 10% × $100 -10% × £50

Rates on notes 10.5% 10.5%

-1325-13

Fixed-Floating + Currency

Fixed-Floating currency swaps. Allows hedging of interest rate and currency

exposures simultaneously Combined Interest Rate and Currency

(CIRCUS) Swap

-1425-14

Credit Swaps

Credit swaps designed to hedge credit risk. Involvement of other FIs in the credit risk shift

Total return swap Hedge possible change in credit risk exposure

Pure credit swap Interest-rate sensitive element stripped out

leaving only the credit risk.

-1525-15

Swaps and Credit Risk Concerns

Credit risk concerns partly mitigated by netting of swap payments.

Netting by novation When there are many contracts between

parties. Payment flows are interest and not principal. Standby letters of credit may be required. Greenspan stated that credit swap market

has helped strengthen the banking system’s ability to deal with recession

-1625-16

Pertinent Websites

BIS www.bis.org

Federal Reserve www.federalreserve.gov

FDIC www.fdic.gov

International Swaps and Derivatives Association www.isda.org

Moody’s Investor Services www.moodys.com

-1725-17

Pricing an Interest Rate Swap*

Example: Assume 4-year swap with fixed payments at

end of year. We derive expected one-year rates from the on-

the-run Treasury yield curve treating the individual payments as separate zero-coupon bonds and iterating forward.

-1825-18

Solving the Discount Yield Curve*

P1= 108/(1+R1) = 100 ==> R1 = 8% ==> d1

= 8%

P2 = 9/(1+R2) + 109/(1+R2)2 = 100 ==> R2 = 9%

9/(1+d1) + 109/(1+d2)2 = 100 ==> d2 = 9.045%

Similarly, d3 = 9.58% and d4 = 10.147%

-1925-19

Solving Implied Forward Rates*

d1 = 8% ==> E(r1) = 8%

1+ E(r2) = (1+d2)2/(1+d1) ==> E(r2) = 10.1%

1+ E(r3) = (1+d3)3/(1+d2)2 ==> E(r3) = 10.658%

1+ E(r4) = (1+d4)4/(1+d3)3 ==> E(r4) = 11.866%