Sustainability, externalities and the contribution of LCA 5/May7_13h30_Brigitte... ·...

17

Sustainability, externalities and the contribution of LCA Birgitte Holt Andersen, MSc., PhD, CWare, Belgium Martha Emneus, MSc. , AEHR, Copenhagen-Denmark

Transcript of Sustainability, externalities and the contribution of LCA 5/May7_13h30_Brigitte... ·...

Sustainability, externalities and the contribution of LCA

q Birgitte Holt Andersen, MSc., PhD, CWare, Belgium

q Martha Emneus, MSc. , AEHR, Copenhagen-Denmark

How the life-cycle-thinking approach can contribute to address the

issue of corporate

externalities

Pros and cons of different approaches

Is a combined framework the

most pragmatic approach and what are the

main challenges?

� Corporations produces nearly everything we consume � They generate the majority of global GNP and the main

drivers of job creation and social prosperity (Sukhdew, 2011)

� The unaccounted costs to society of doing business are huge – in the order of 3% of global GNP – representing trillions of dollars/EUROs ‘market failures’ (Trucost, 2010)

� Corporations could play a dominant role in getting things right

The unaccounted costs (and benefits) = externalities (good and

bads)

Sustainability = neutralising or internalising externalities A corporation is sustainable if the externalities > 0

Externality caused by the Corporation

External externality or societal issue

Pos

itiv

e

Popular workplace (Soc) Demand local sourced organic grown cereals (Env) High tax net-‐payer due to growing revenue (Eco)

Access to high-‐qualified workforce (Soc) Rich on natural raw materials (Env) Low risk investment climate (Eco)

Neg

ativ

e

Poor working condiEons (Soc) Emission of polluEons into the environment (Env) Tax avoidance (Eco)

High crime rate(Soc) Scarce clean water access (Env) Insufficient transport infrastructure (Eco)

� To show that they are responsible � Essential to manage business risks � To sustain and maintain license to

operate � Telling the positive story � To create new business opportunities

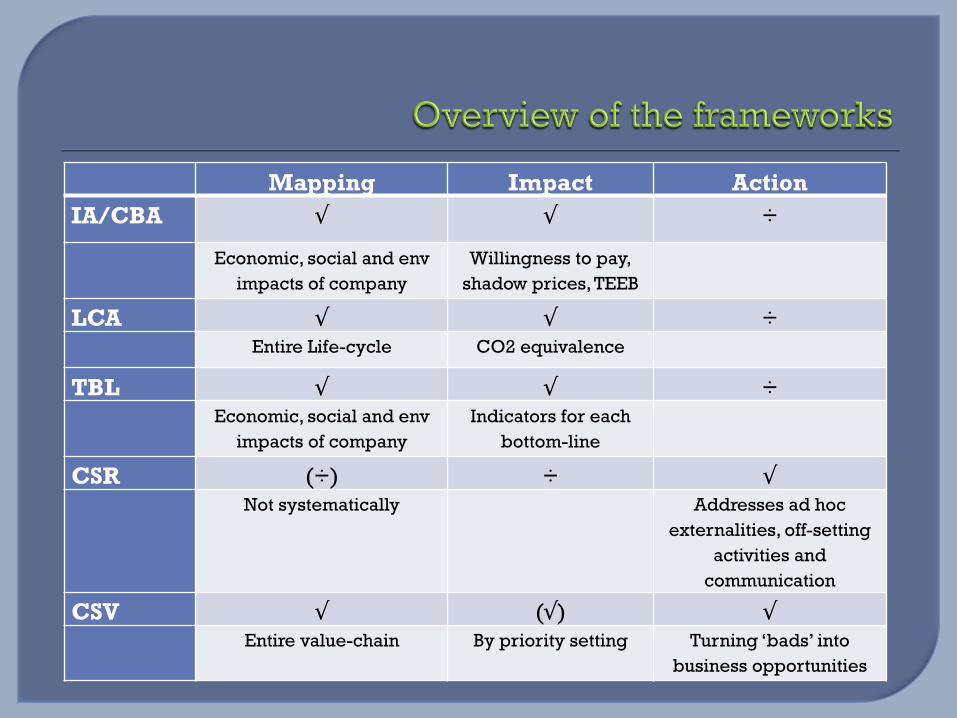

• Impact Assessment (IA) and Cost benefit analysis (CBA)

• Life cycle assessment (LCA) • The Triple-Bottom-Line (TBL) • Corporate Social Responsibility (CSR) • Creating Shared Value (CSV)

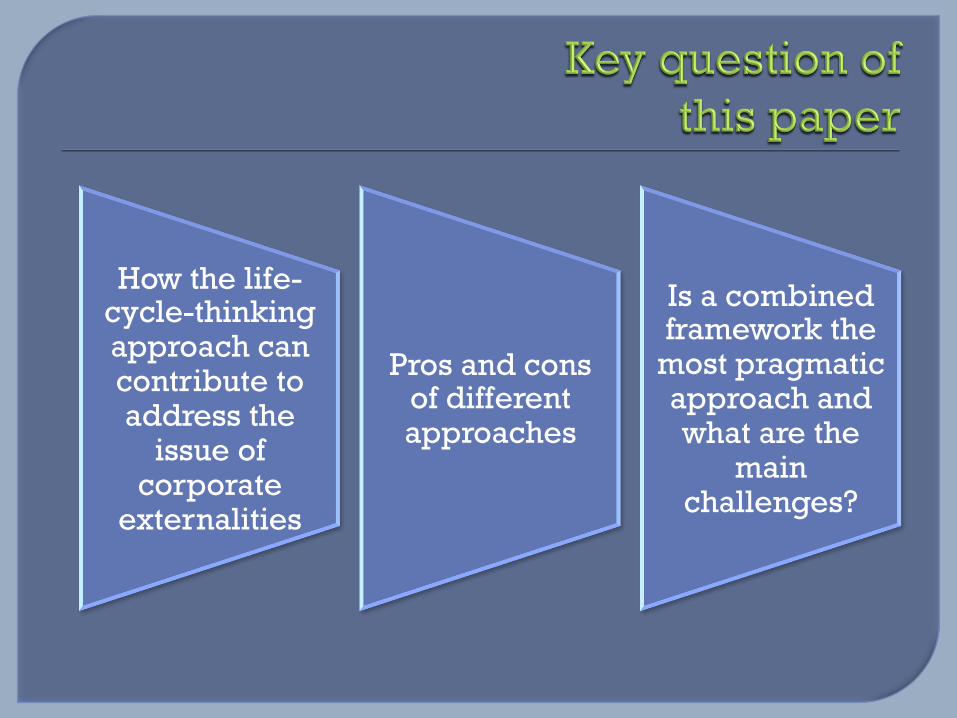

� IA and CBA are analysis of the consequences of an intervention (policy, project, new technology) compared to the situation without the intervention (Baseline)

Both IA and CBA often use a stakeholder-model to understand who the intervention will impact and how (first order beneficiaries, second order beneficiaries…)

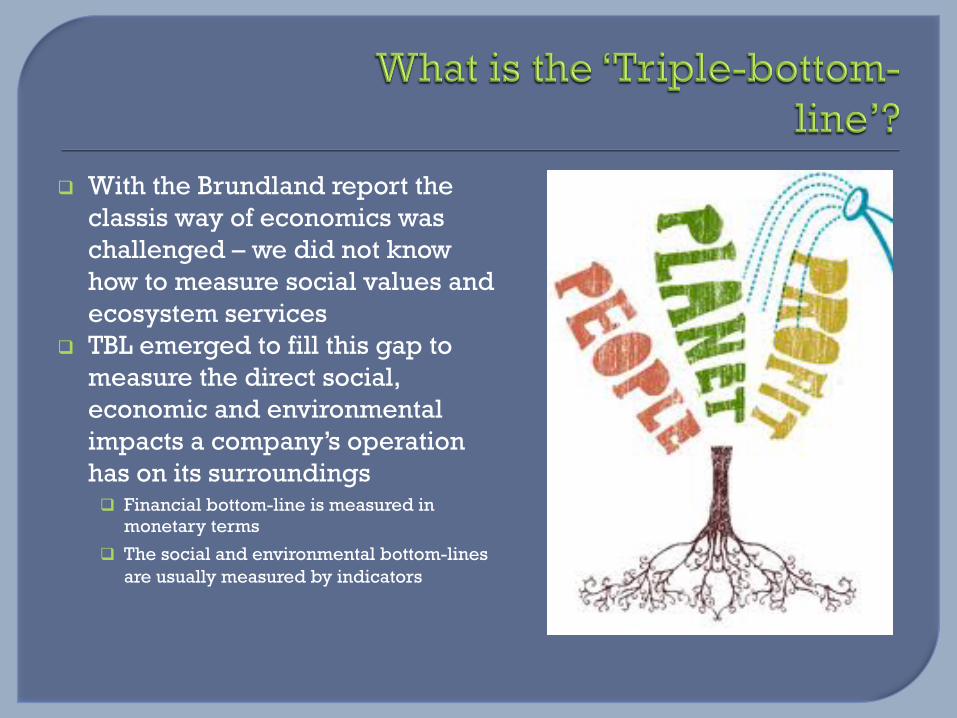

q With the Brundland report the classis way of economics was challenged – we did not know how to measure social values and ecosystem services

q TBL emerged to fill this gap to measure the direct social, economic and environmental impacts a company’s operation has on its surroundings q Financial bottom-line is measured in

monetary terms

q The social and environmental bottom-lines are usually measured by indicators

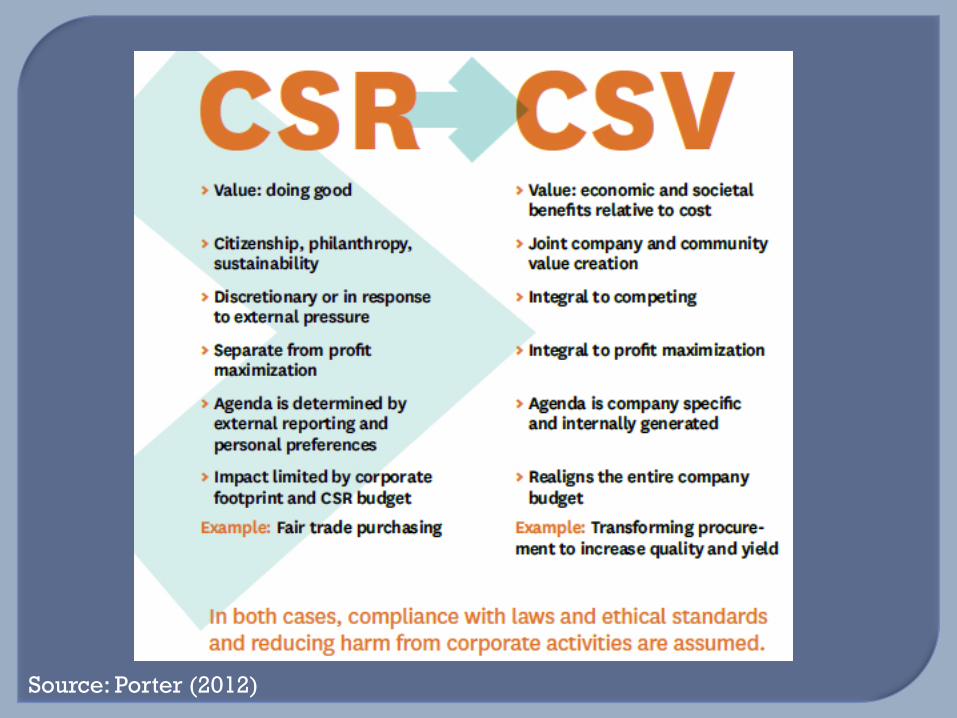

Source: Porter (2012)

Mapping Impact Action IA/CBA √ √ ÷ Economic, social and env

impacts of company Willingness to pay,

shadow prices, TEEB

LCA √ √ ÷ Entire Life-cycle CO2 equivalence TBL √ √ ÷ Economic, social and env

impacts of company Indicators for each

bottom-line

CSR (÷) ÷ √ Not systematically Addresses ad hoc

externalities, off-setting activities and

communication CSV √ (√) √ Entire value-chain By priority setting Turning ‘bads’ into

business opportunities

Company

Local communities

Girls’ lacking access to

education

Complementary business sectors

Increased risks of

flooding

High un-employment

Environment

Employees Share-holders

Customers

Suppliers

Other stakeholders

Too small to invest in sustainability

Increased Obesity

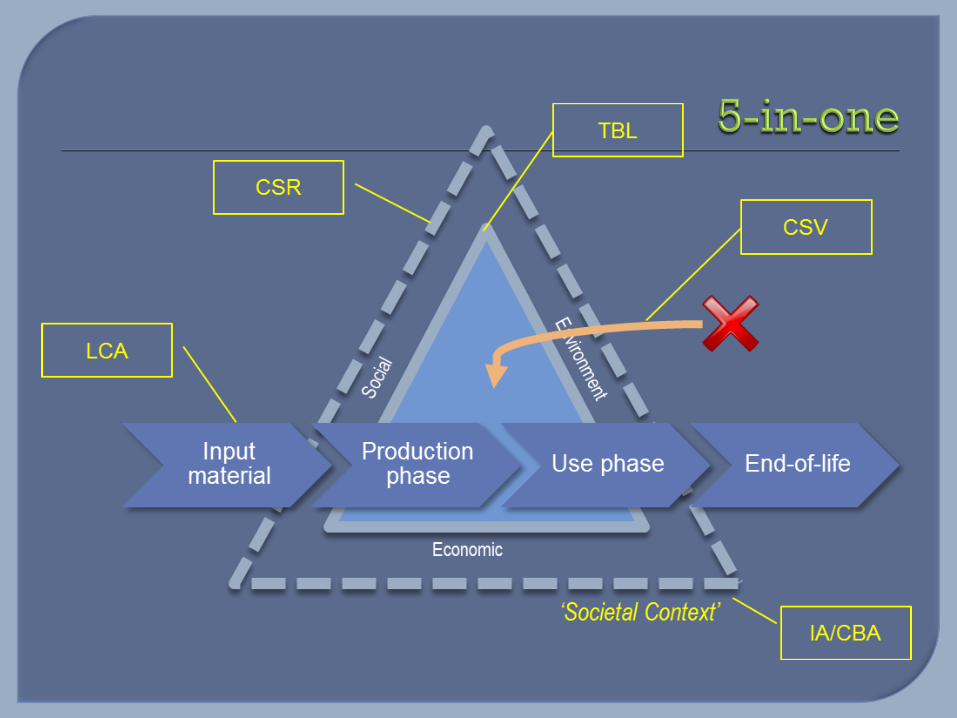

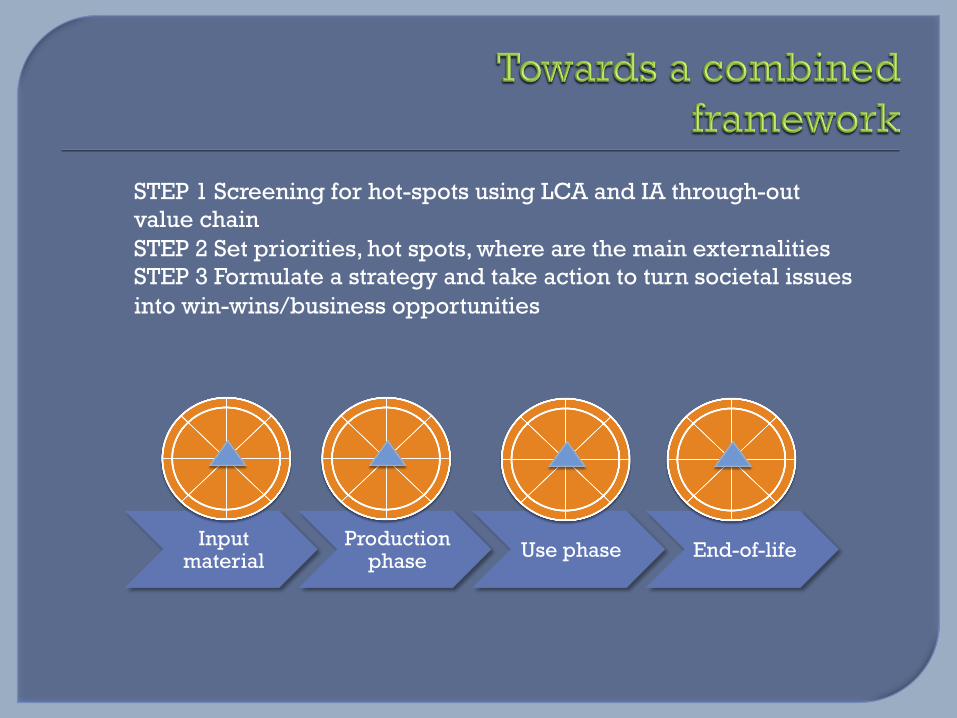

Input material

Production phase Use phase End-of-life

STEP 1 Screening for hot-spots using LCA and IA through-out value chain STEP 2 Set priorities, hot spots, where are the main externalities STEP 3 Formulate a strategy and take action to turn societal issues into win-wins/business opportunities

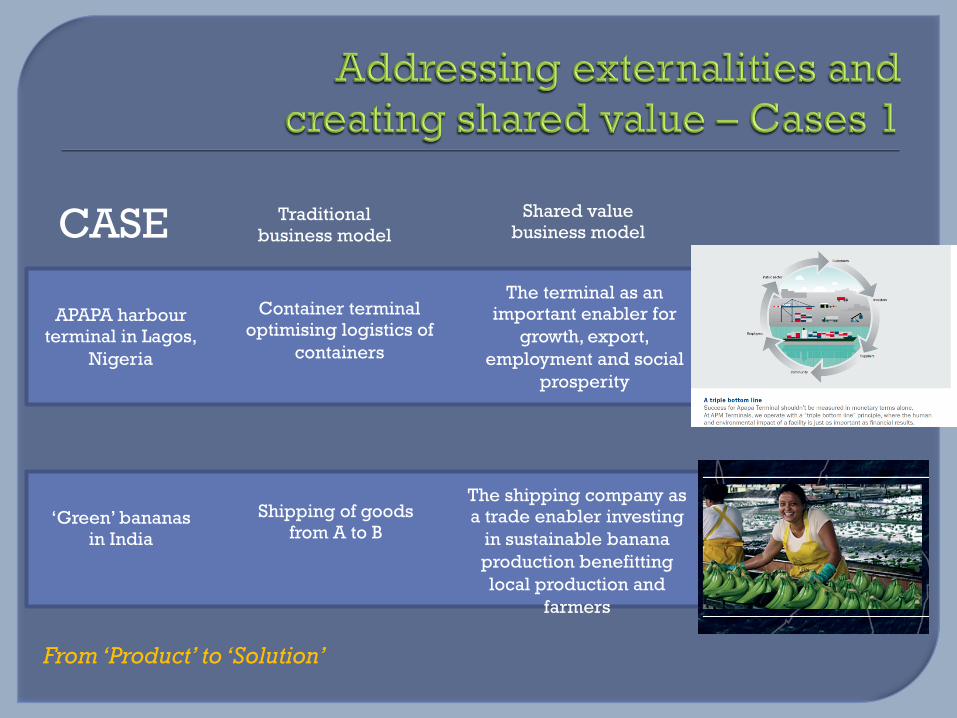

Traditional business model

Shared value business model CASE

APAPA harbour terminal in Lagos,

Nigeria

Container terminal optimising logistics of

containers

The terminal as an important enabler for

growth, export, employment and social

prosperity

‘Green’ bananas in India

Shipping of goods from A to B

The shipping company as a trade enabler investing

in sustainable banana production benefitting local production and

farmers

From ‘Product’ to ‘Solution’

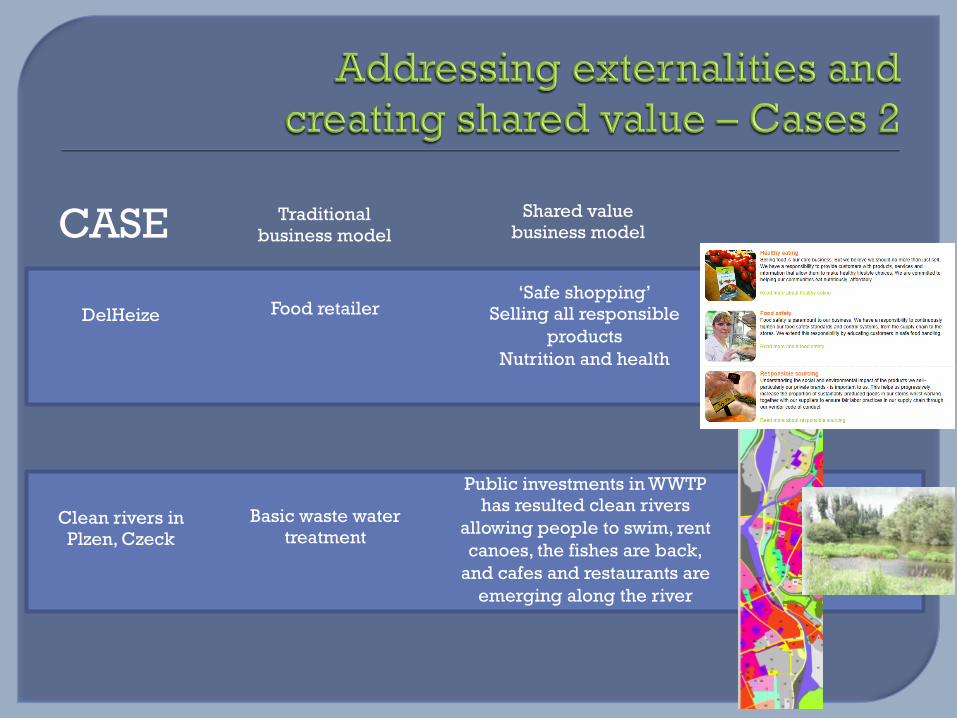

Traditional business model

Shared value business model CASE

DelHeize Food retailer ‘Safe shopping’

Selling all responsible products

Nutrition and health

Clean rivers in Plzen, Czeck

Basic waste water treatment

Public investments in WWTP has resulted clean rivers

allowing people to swim, rent canoes, the fishes are back,

and cafes and restaurants are emerging along the river

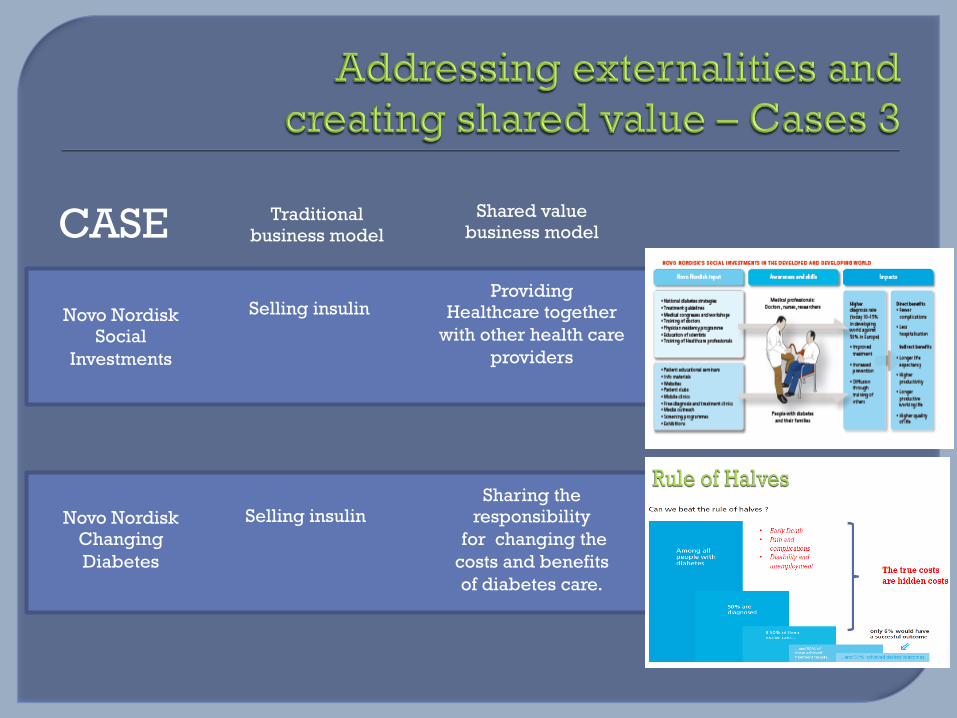

Traditional business model

Shared value business model CASE

Novo Nordisk Social

Investments

Selling insulin Providing

Healthcare together with other health care

providers

Novo Nordisk Changing Diabetes

Selling insulin Sharing the

responsibility for changing the costs and benefits of diabetes care.

� It is important to understand externalities to define a sustainable strategy

� Each of the frameworks discussed can contribute with different elements

� Combining the frameworks - chances are good to catch the whole picture