Susan Applegate, AECOM Peter Glynn, TCOM … Glynn, TCOM Moderator: David Eck government contracting...

12

1 government contracting Estimating Systems Update Susan Applegate, AECOM David Bodenheimer, Crowell & Moring Peter Glynn, TCOM Moderator: David Eck 2 government contracting Panelists Susan Applegate, Director of Pricing AECOM [email protected] (817) 984.2594 @DHG_GovCon #DHG_GC20 David Bodenheimer, Partner Crowell & Moring LLP [email protected] (202) 624.2713 Peter Glynn, Business and Programs Financial Manager TCOM, LP [email protected] (214) 334.3233

Transcript of Susan Applegate, AECOM Peter Glynn, TCOM … Glynn, TCOM Moderator: David Eck government contracting...

1government contracting

Estimating Systems UpdateSusan Applegate, AECOMDavid Bodenheimer, Crowell & MoringPeter Glynn, TCOMModerator: David Eck

2government contracting

Panelists

Susan Applegate, Director of [email protected](817) 984.2594

@DHG_GovCon#DHG_GC20

David Bodenheimer, PartnerCrowell & Moring [email protected](202) 624.2713

Peter Glynn, Business and Programs Financial ManagerTCOM, [email protected](214) 334.3233

3government contracting

Applicability of the Business System Rule: Estimating System

• The Business System Rule will apply to any DOD CAS Covered contracts

• Reference DFAR Sub‐part 242‐70:– Contractor Business System Deficiencies242.7000

• Contract Clauses– Contractor Business Systems 252.242.7005– Estimating System 252.215.7002 (17 criteria)

@DHG_GovCon#DHG_GC20

4government contracting

Current Priority Areas –Proposals and Estimating

• Subcontract Cost/Price Analyses• Consolidated Bill of Material• Forward Pricing Rates – Adequate Budgetary Data• Adequate Basis of Estimates (BOEs)• Proposal Cover Sheets• Proposal Index• Proposal Traceability • Use of Historical Data• Pricing of CLINs

@DHG_GovCon#DHG_GC20

5government contracting

Other Proposal/Estimating Areas

• Proposal Walk‐thrus– Very useful to understand proposal supporting data and estimating techniques

– This area needs to be stressed more

• Proposal data requests and response times– Usually not a problem when readily available data is requested

– Seen 24 hours requests for data not readily available

@DHG_GovCon#DHG_GC20

6government contracting

Other Proposal/Estimating Areas

• Sample Sizes– Usually the same sample – 57 or 58 items– Sample Size does not seem to be reduced based on internal/third party reviews or adequacy of business system

• DCMA/DCAA Analyses of Supplier Proposals– Need a better process to improve timeliness of assist audits

– Proposals under audit thresholds ($100 million cost type and $10 million FFP) usually not reviewed

– Companies still need to document assist audit requests– Companies need to improve analyses of supplier proposals

@DHG_GovCon#DHG_GC20

7government contracting

Estimating System Disapproval

• Gain good understanding of deficiencies– Examples

• Provide response and corrective action• Obtain DCAA buy‐in• Have specific plan for

– Weekly status meetings with DCAA/DCMA– Dates corrective action will be completed– Dates DCAA will complete fiscal year audit– Dates DCAA/DCMA will provide estimates system approvals

@DHG_GovCon#DHG_GC20

8government contracting

Defective Pricing’s Back!

• Tina’s Ups & Downs– Boom Years – 1960s to 1980s

• Vietnam & other conflicts

– Lean Years – 2000s• FASA, IPTS, & De‐emphasis

– TINA Redux – 2013 to Today• Old Awards (2006‐2009)• Lots of Audit Buzz• ASBCA Appeals • IG Subpoenas

TINA’s Back!

@DHG_GovCon#DHG_GC20

9government contracting

Proving Defective Pricing

Remember the 5 “Points”Government bears burden of proof for “five points” of defective pricing

1. Cost or Pricing Data

2. Data Reasonably Available

3. Not Disclosed or Known to Government

4. Government Reliance on Data

5. Causation of Increased Price

DCAA Audit Manual

@DHG_GovCon#DHG_GC20

10government contracting

Battling Forward Pricing

Forward Pricing RatesDCAA Allegations• Must tell PCOLegal Realities• FAR § 15-407-3 (a) vs.

(b)• DFARS § 215.407-3

(ACO)• Disclosure & Relianceo FMC, 87-1 BCA 19,544o Litton, 93-2 BCA 25,707o Texas Inst., 89-1 BCA

21,489

FAR § 15‐407‐3(a) When certified cost or pricing data are required, offerors are required to describe any forward pricing rate agreements (FPRAs) in each specific pricing proposal to which the rates apply and to identify the latest cost or pricing data already submitted in accordance with the FPRA. All data submitted in connection with the FPRA, updated as necessary, form a part of the total data that the offeror certifies to be accurate, complete, and current at the time of agreement on price for an initial contract or for a contract modification. (See the Certificate of Current Cost or Pricing Data at 15.406‐2.) (b) Contracting officers will use FPRA rates as bases for pricing all contracts, modifications, and other contractual actions to be performed during the period covered by the agreement. Conditions that may affect the agreement’s validity shall be reported promptly to the ACO. If the ACO determines that a changed condition invalidates the agreement, the ACO shall notify all interested parties of the extent of its effect and status of efforts to establish a revised FPRA.

@DHG_GovCon#DHG_GC20

11government contracting

Abusing Judgments

Facts vs. Judgments

DCAA/DOJ Allegations• Estimates & Escalation

Pricing Realities• FAR § 2.101 (judgments)• Contract Pricing Ref. Guide

• “educated guesses”

Judgments OkayASBCA Precedent“We find that the subject escalation factor was not cost or pricing data.” UTC,04-1 BCA 32,556Audit Guidance (DCAM 14-104.7)

@DHG_GovCon#DHG_GC20

12government contracting

Demanding Use

Use vs. Disclosure

DCAA/DOJ Allegations• Failed to use cost data

Audit Realities

Disclosure OnlyASBCA Precedent (TINA)“The plain language of the Act does not obligate a contractor to use any particular cost or pricing data to put together its proposal. Indeed, TINA does not instruct the manner or method of proposal preparation.”United Technologies Corp., 04-1 BCA 32,556

Federal Precedent (FCA)• Martin-Baker (D.C. Cir. 2004)• UTC (6th Cir. 2015) (no law or

regulation requiring use)

@DHG_GovCon#DHG_GC20

13government contracting

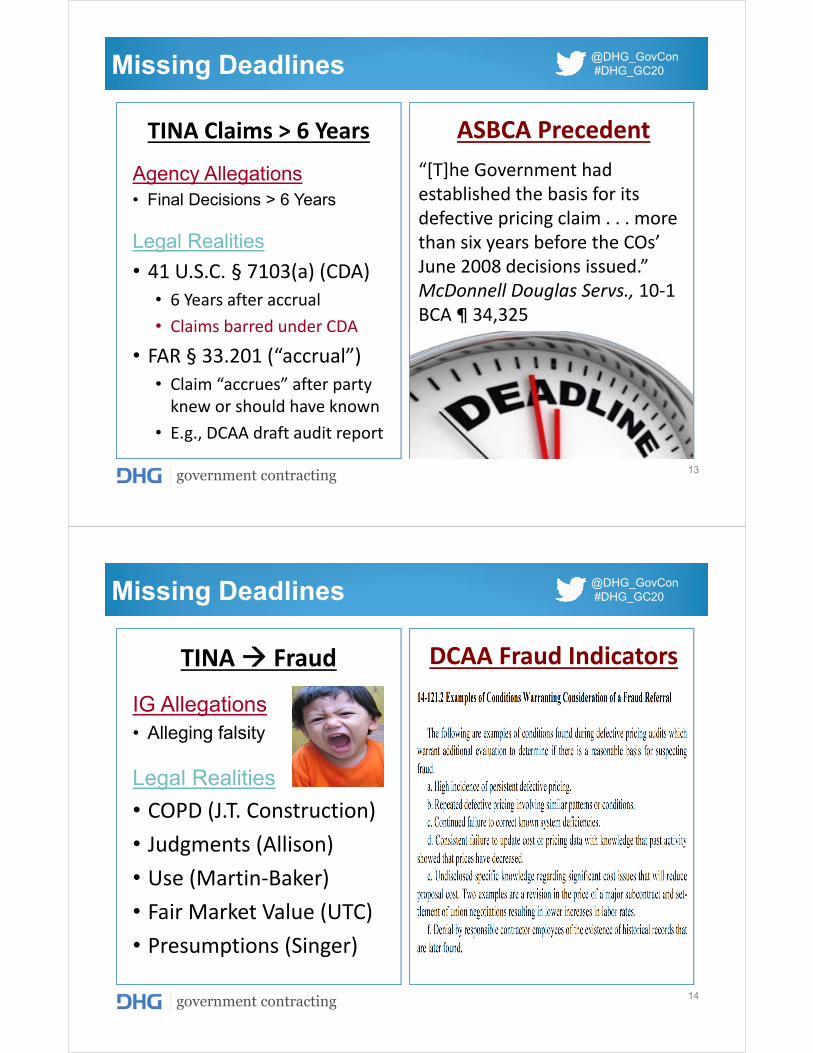

Missing Deadlines

TINA Claims > 6 Years

Agency Allegations• Final Decisions > 6 Years

Legal Realities• 41 U.S.C. § 7103(a) (CDA)

• 6 Years after accrual• Claims barred under CDA

• FAR § 33.201 (“accrual”)• Claim “accrues” after party knew or should have known

• E.g., DCAA draft audit report

ASBCA Precedent“[T]he Government had established the basis for its defective pricing claim . . . more than six years before the COs’ June 2008 decisions issued.” McDonnell Douglas Servs., 10‐1 BCA ¶ 34,325

@DHG_GovCon#DHG_GC20

14government contracting

Missing Deadlines

TINA Æ Fraud

IG Allegations• Alleging falsity

Legal Realities• COPD (J.T. Construction)• Judgments (Allison)• Use (Martin‐Baker)• Fair Market Value (UTC)• Presumptions (Singer)

DCAA Fraud Indicators

@DHG_GovCon#DHG_GC20

15government contracting

Resolving TINA Disputes

Litigation vs. ADRPCO Allegations• No Independence• Rubberstamping DCAA

Legal Realities• Contract Disputes Act (CDA)• Resolution vs. Litigation

• FAR § 15.407‐1(d)• Due Process Right to Respond

• Opportunity to Rebut• Sooner = Better

3rd Party OversightADR Policy (FAR § 33.204)

“Agencies are encouraged to use ADR procedures to the maximum extent practicable.”

ADR Procedure (FAR § 33.214)• Objective: inexpensive &

expeditious• Agreement (e.g., ASBCA

sample forms)

Other Ideas• Contracting Officer as Neutral• Government Counsel as

Gatekeeper

@DHG_GovCon#DHG_GC20

16government contracting

DDP 2/4/2015 Memo on Commercial Items

• Contracting Officer (C) should make a Commercial Item Determination within 10 business days

• Key consideration – Am I paying a fair and reasonable price?

• Preference – use market based pricing when determining fair and reasonable price

• If market based pricing is not available, CO may use cost based analysis – “Other than certified cost or pricing date

• DCMA will establish the cadre of acquisition professionals to provide expert advice on commercial items

@DHG_GovCon#DHG_GC20

17government contracting

DODIG Reports on Price Reasonableness

• Excess Inventory and Contract Pricing Problems Jeopardize the Army Contract with Boeing to Support the Corpus Christi Army Depot (DODIG‐2011‐061, 5‐3‐2011)

• Improved Guidance Needed to Obtain Fair and reasonable Prices for Sole‐Source Spare Parts Procured by the Defense Logistics Agency from the Boeing Company (DODIG‐2013‐090, 6/7/2013)

@DHG_GovCon#DHG_GC20

18government contracting

DODIG Reports on Price Reasonableness

• Defense Logistics Agency Aviation Potentially Overpaid Bell Helicopter for Sole‐Source Commercial Spare Parts (DODIG‐2014‐088, 7/3/2014)

• U.S. Air Force May be Paying Too Much for F117 Engine Sustainment (DODIG‐2015‐058, 12/22/2014)

@DHG_GovCon#DHG_GC20

S U S A N A P P L E G AT E | B I O G R A P H Y

��Susan Applegate is Director of Strategic Pricing at AECOM. Ms. Applegate is responsible for providing overall leadership in identifying market opportunities, directing business and competitive analyses, and developing pricing strategies and tactics to pursue identified opportunities for the Management Services Group. She leads cross-functional teams to understand market dynamics, business performance, and devise effective pricing strategies and tactics. She contributes to the development of the business case, competitive assessment, risk mitigation and negotiation strategy in support of customer business proposals. In addition, she leads teams to review and analyze client requirements or challenges and develops cost associated proposals that ensure profitability and high client satisfaction. Her experience encompasses all contract types, including: ID/IQ, CPAF, CPIF, CPFF, and FFP.

Susan’s core competencies include: compliance issue resolution, financial analysis, forecasting, strategic planning, budgeting, proposal pricing, risk management, technology integration, and yield/revenue management. She has extensive knowledge of FAR, DFAR, and CAS.

Susan Applegate Director Strategic Pricing

C A R E E R H I G H L I G H T S Developed price-to-win strategies and

led efforts to ensure compliance with Cost Accounting Standard (CAS), including development of disclosure statements

Developed Cost Estimating System

Manual resulting in DCMA Estimating System Approval

Received NASA Silver Dollar Quality

Award for outstanding performance in supporting budget activities

Prior to joining the AECOM management team in 2013, she gained over 20 years of progressive responsibility in project controls, estimating and pricing, and cost management, including:

Senior Director Cost Strategy, DynCorp Inc. Senior Manager, Project Controls, Agility Defense and Government Services

Senior Manager, Project Controls and Senior Proposal Manager, IAP World Services, Inc.

Cost & Pricing Manager, CH2M HILL

Cost Accounting Manager, DRS Technologies

Program Cost Control & Schedule Analyst VI, Northrop Grumman

Senior System Analyst, ExecuSys, Inc. and Walt Disney World

Manager, Budgets/Forecasting, McDonnell Douglas Space & Defense Systems Ms. Applegate has a Master’s in Business Administration, Accounting & Finance, Rochester Institute of Technology, Rochester, New York; and a Bachelor of Science, Biomedical Photographic Communication (with honors), Rochester Institute of Technology, Rochester, New York. She has served as Assistant Professor at Embry-Riddle Aeronautical University, Webster University, and Brevard Community College where she taught accounting, finance, operations research, and management information systems.

David Eck

Director, Government Contract AdvisoryTysons, VA

Contact 703.970.0480 [email protected]

Experience

David has more than 31 years of experience working in the government accounting field. He has extensive knowledge and experience in all aspects of government laws and regulations, including the Federal Acquisition Regulations, individual agency supplements to the FAR, the Truth in Negotiations Act, the Cost Accounting Standards, and the Office of Management and Budget (OMB) Circulars. Prior to working with Dixon Hughes Goodman, David worked over 30 years with the Defense Contract Audit Agency (DCAA) at field, regional and headquarters offices. Over the last several years, he was the Regional Director of DCAA’s Central and Mid-Atlantic Regional Offices and responsible for auditing over 100 major contractors and several thousand smaller contractors. David has extensive knowledge and experience with:

x Contractor business systems x Contract proposals and postaward (defective pricing) audits x Forward pricing rate proposals x Incurred cost submissions x CAS compliance, disclosure statements, and cost impact statements x Terminations/equitable adjustment proposals x Earned Value Management System (EVMS) guidelines x Audits of grants, cooperative agreements, and contracts at educational institutions and other nonprofit

organizations, including A-133 Single Audits

He has participated extensively in the development of changes to the FAR, DFARS, and the OMB Circulars, more recent noting his participation in the development of the new Contractor Business Systems DFARS rule. David was also responsible for development and implementation of DCAA’s contract audit policy, including the Contract Audit Manual and standard audit programs. He led the development of the Parametric Estimating Manual, which contributed to improving estimating techniques to price government contracts.

Professional & Civic Involvement� American Institute of Certified Public

Accountants, Member

Licenses & Certifications � CA Certified Public Accountant #39862

Education � California Polytechnic State University, San Luis

Obispo, Bachelor of Science in Accounting � Central Michigan University, Master of Science in

Administration

Pete Glynn

Pete Glynn is the business and programs financial manager at TCOM LP. His responsibilities include oversight of estimating, pricing, project controls and compliance. Before joining TCOM, Pete was the vice president of project controls for the KBR Infrastructure, Government and Power group with responsibility for estimating and pricing, project controls and project risk management. Previously, Mr. Glynn served as the director of accounting and finance for KBR Government Operations. This included financial management, accounting and internal controls for business operations and regional offices in the United States, UK, and Australia. Pete has worked in the defense industry for over 28 years. He began his career as an electrical design engineer with Westinghouse Electric Corporation in 1982. He continued with various engineering management and project management assignments. In 1990, he moved to TCOM LP as a project manager in the international systems division and became vice president of program management in 1998. Pete has a B.S. in electrical engineering from the State University of New York and a M.S. in management from Johns Hopkins University. Prior to attending college, he served in the U.S. Marine Corps.