SURVEY ON THE EVOLUTION OF WOOD FUEL PRICES … · SURVEY ON THE EVOLUTION OF WOOD FUEL PRICES IN...

25

SURVEY ON THE EVOLUTION OF WOOD FUEL PRICES IN 2016-2017 October 2017 Study conducted on behalf of ADEME by : CODA Stratégies Contract no. : 16MAR001765 Technical coordination: Mrs. Alice Fautrad Generation and Renewable Energies Forestry Supply Bioeconomics Service SYNTHESIS

Transcript of SURVEY ON THE EVOLUTION OF WOOD FUEL PRICES … · SURVEY ON THE EVOLUTION OF WOOD FUEL PRICES IN...

SURVEY ON THE EVOLUTION OF WOOD FUEL PRICES IN 2016-2017

October 2017

Study conducted on behalf of ADEME by : CODA Stratégies Contract no. : 16MAR001765

Technical coordination: Mrs. Alice Fautrad Generation and Renewable Energies

Forestry Supply Bioeconomics Service

SYNTHESIS

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 2 sur 25

ACKNOWLEDGEMENTS We would like to express our gratitude to Mrs. Alice Fautrad, of the ADEME Forestry Supply Bioéconomics service, whose valuable assistance was essential to the success of the present study.

INSTRUCTIONS FOR QUOTING THIS SYNTHESIS

Author : Jean-Claude Migette.

Silviya Yordanova

Date of publication : 2017

Titre : SURVEY ON THE PRICES OF WOOD FUELS 2015-2016

ADEME SYNTHESIS.

Number of pages : 25 pages

Any representation or reproduction of the contents herein, in whole or in part, without the consent of the author(s) or their assignees or successors, is illicit under the French Intellectual Property Code (article L 122-4) and constitutes an infringement of copyright subject to penal sanctions. Authorised copying (article 122-5) is restricted to copies or reproductions for private use by the copier alone, excluding collective or group use, and to short citations and analyses integrated into works of a critical, pedagogical or informational nature, subject to compliance with the stipulations of articles L 122-10 – L 122-12 incl. of the Intellectual Property Code as regards reproduction by reprographic means.

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 3 sur 25

1. The objectives, scope and methodology of the study

1.1. The objectives of the study

As part of its policy to promote the transition of the national energy mix, the French government has set ambitious goals for the wood and biomass sector, especially in terms of heating use.

Thus, for domestic wood heating systems, the objectives of the authorities focus on an increase in the number of units from 5.8 million in 2006 to 7.3 million in 2012 and to 9 million in 2020. However, the technological advancement of heating equipment efficiency and improvements in home insulation are likely to limit any upward impact on wood consumption, which is slated to stay constant, at roughly 7.4 Mtoe. The French energy transition law aims at boosting the penetration of renewable energies from 13.7% in 2012 to 32% in 2032. Wood currently represents 50% of renewable energy in France, with hydro being a distant second (25%).

In a study conducted in June 2013, ADEME estimates that about 7.4 million households, or 47% of the total individual household park, use wood heating. Associated wood consumption is estimated at 7.3 Mtoe, of which 6.9 Mtoe being wood logs. The corresponding volume amounts to 31.9 Mm3 for wood logs alone, and 33.8 Mm3 in total. While auxiliary heating accounted for 70% of wood heating use in 1999, figures are currently equally divided between auxiliary and main heating. 1

The commercial and industrial sectors, as well as the collective housing sector, also see ambitious growth objectives. ADEME estimated that, in order to increase the share of renewable energies to 23% by 2020, as stipulated under the European Climate & Energy package, the renewable heat generation capacity will have to increase by 600 000 toe on an annual basis, compared to 250-300.000 toe during the previous period 2. To achieve this target, the Renewable Heat Fund has been expanded over the 2015-2017 period and is expected to reach € 420 million in 2017.

In this context, ADEME is focusing on a number of issues. One of these issues is ensuring the competitiveness of different wood and biomass fuel prices, in the context of strong variability of electricity and fossil fuels. Monitoring the evolution of these prices is a necessity, which ADEME has taken on over the past 10 years by publishing regular surveys on the evolutions of the prices of various wood and biomass fuels.

The quality of the fuels used by companies and by individuals plays a crucial role in meeting the environmental constraints associated with their use. Identifying and understanding the distribution channels, the extent to which certified products are used, and on a general note, the quality of the wood are factors of major importance. It is thus necessary to get a better understanding of the distribution of the higher quality fuels and of the noticeable differences in their prices.

The market for wood and biomass fuels remains characterized by wide discrepancies in terms of prices, packaging, means of delivery and relative importance of various distribution channels.

In this context, ADEME required a study which, on one hand, continues the publication of surveys and indexes since 2003 and, on the other hand, extends the work by analyzing in greater detail various factors that influence wood fuel prices (delivery and packaging, composition in terms of wood species, moisture content, regional diversity ...).

Regarding fuels used on commercial, industrial and collective housing premises, ADEME uses, since 2013, data from official surveys conducted by the CEEB, under an INSEE mandate. However, as these surveys do not integrate delivery costs, data cannot be directly compared with the prices of

1 ADEME, STUDY ON DOMESTIC WOOD HEATING/ MARKETS AND SUPPLY, June 2013 2 ADEME AND YOU, NO 79, OCTOBER 2014

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 4 sur 25

other energy sources (natural gas, oil ...); taking these limits into account, a methodology for the evaluation of the delivery costs was developed in 2015, in order to provide a comparison on a homogenous basis.

The study conducted by CODA Strategies thus contains, in the first report, the results of a survey conducted among distributors of wood fuels mainly for domestic heating purposes. In order to situate the French market in the international context, the report also includes international data on wood pellets prices. The second report is dedicated to identifying and presenting wood prices for commercial, industrial and collective housing markets. This second report is supported by CEEB data, and sees the use of the above-mentioned method of estimating delivery costs.

1.2. The methodology Two major markets are analyzed throughout the study: The domestic wood heating market and the collective and industrial market. The methods of collecting and processing data are specific to each

of these markets.

An in-depth survey of domestic sector prices

A survey of more than 366 wood fuels suppliers, statistically representative of the different provider profiles on the market, was conducted. This survey was used to determine the current prices for the those fuels most used within households (wood logs, pellets, reconstituted logs and sticks...) Moreover, the factors influencing the variation in wood prices on the domestic market were measured: the impact according to the region where the fuels were sold, the period of the transaction, the delivery options, the impact of labeling and of the quality and the types of the wood sold.

The information obtained through the survey was enriched via an internet price collection campaign. This was obviously done in order to enlarge the dataset and thus to ensure a better representativeness of the sample at a regional level.

Regarding the domestic market, a recently published ADEME study on the wood heating sector, highlighted the strong variety of distribution channels focusing on the household market3 and the relatively minor role of professional purchasing channels. The annual survey of the sector conducted by AGRESTE4, estimated that household wood consumption stands at 32.3 million m3, of which only 4.6 million m3 comes from a professional distribution channel. The prices listed in this report apply only to those wood purchases which are official formal business transactions, and as such, that are invoiced. These prices are representative of less than 20% of overall domestic wood consumption..

In this study, the Lower Heating Value of wood logs is considered to be 2000 kWh LHV / wood log. This value corresponds to wood (moisture content below 20%, satisfactory diameter, hardwood) meeting the France® Bois Bûche standard, which represents the bulk of the wood sold by professional distribution channels, although it doesn’t reflect the average LHC of wood on the market in France, which tends to be closer to 1500 kWh/ log.

3 ADEME « Study on the domestic heating wood market», June 2013 4 AGRESTE - Timber harvest and sawnwood production in 2012– AGRESTE PRIMEUR – The firewood harvest is estimated at 4.8 Mm3 according to AGRESTE compared to 4.3 Mm3 in 2012

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 5 sur 25

Use of data provided by professional organizations for the collective and industrial sectors, estimation of delivery costs

The price of wood chips and hedgerows as well as the prices of the rest of the different fuel types used in the collective and industrial markets were analyzed based on data obtained from price surveys conducted by trade associations and professional organizations, most notably by the CEEB, under an INSEE mandate (for the provision of the survey). Additional data processing was carried out to include VAT rates and especially transportation costs within the overall prices.

Besides presenting prices and indexes published by these organizations, the report describes and analyzes the methodology involved in the data collection and analysis process.

Delivery costs of wood fuels were also estimated in order to establish a relevant comparable base of the different energies used in the collective and industrial sector. This estimation is based on a methodology developed throughout a survey of more than 80 heating plants and is fueled by 15 interviews conducted with experts on the market. Its use allows integrating delivery costs within the overall prices. In 2017, this survey was reconducted, thus ensuring that the updated estimate of average delivery costs remains still representative of the reality of the market.

2. Wood prices on the domestic market

2.1. The price competitiveness of wood energy The use of wood as a primary energy source among households has been increasing in the past few years. The aforementioned study conducted under an ADEME mandate, has highlighted the fact that 50% of households currently owning a wood heating system, use it as a primary source of heating. In 1999, this same ratio stood at only 30%. This evolution further warrants the interest in obtaining a better understanding of the competitiveness of wood as an energy source, according to the different usage scenarios.

2.1.1. Auxiliary heating use

Throughout this report, wood heating systems are considered as an auxiliary heating solution when their overall contribution to the thermal requirements of the household is minor. As such, the tariffs taken into account when comparing the price of wood fuels and other energies are chosen as to ensure coherence according to this type of usage:

• Propane : 13 kg tank • Electricity : 1 700 kWh/year, 6 kVA subscription • Gas : B0 Tariff, 2 326 kWh HHV/year

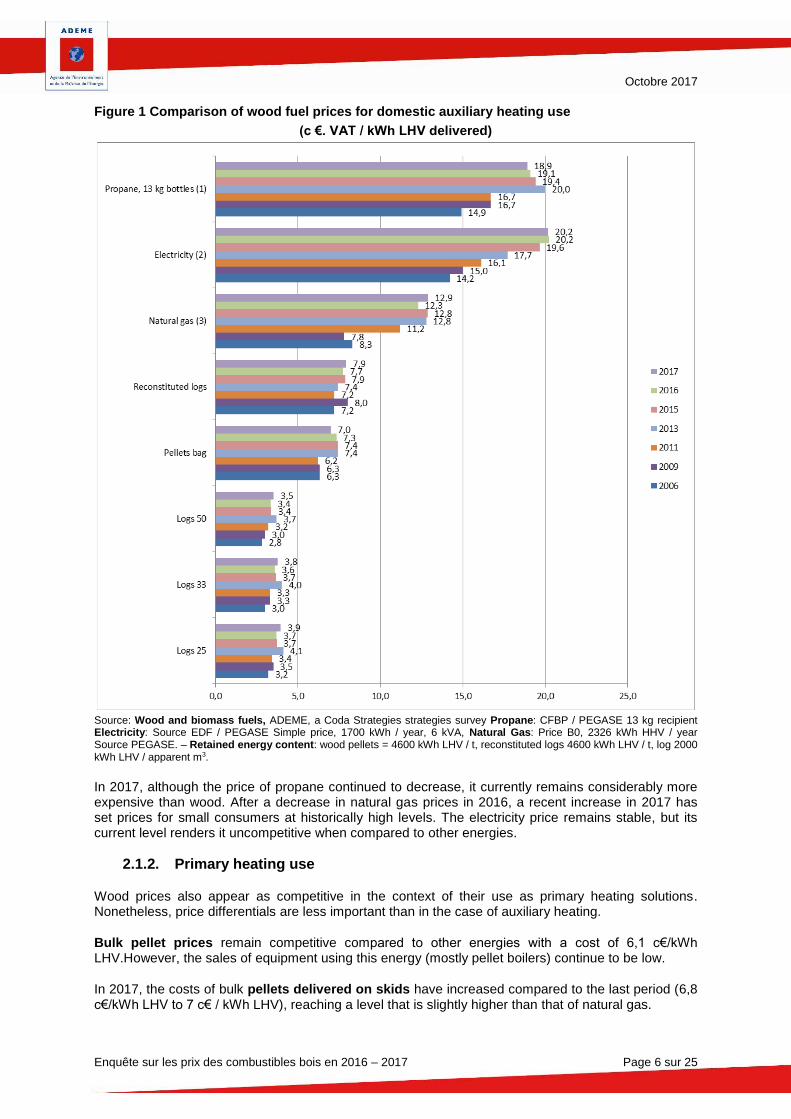

For wood and biomass fuels, in the case of pellets, 15 kg bags are considered mainly because their packaging appears to be the most appropriate for this type of use Reconstituted logs are predominantly used in auxiliary heating, due to their high price. However, they can also be used, as a complement to the traditional wood log for a primary heating solution (for example to ensure a steady flame or during the ignition process). The following chart provides a price comparison for various fuel types used in auxiliary heating applications. It reflects the evolution of prices over the 2006-2017 period. The chart clearly shotw that for auxiliary heating, wood appears to be the most competitive of energies. This conclusion stands for all of the available types of wood fuels covered in this study (logs, pellets).

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 6 sur 25

Figure 1 Comparison of wood fuel prices for domestic auxiliary heating use

(c €. VAT / kWh LHV delivered)

Source: Wood and biomass fuels, ADEME, a Coda Strategies strategies survey Propane: CFBP / PEGASE 13 kg recipient Electricity: Source EDF / PEGASE Simple price, 1700 kWh / year, 6 kVA, Natural Gas: Price B0, 2326 kWh HHV / year Source PEGASE. – Retained energy content: wood pellets = 4600 kWh LHV / t, reconstituted logs 4600 kWh LHV / t, log 2000 kWh LHV / apparent m3.

In 2017, although the price of propane continued to decrease, it currently remains considerably more expensive than wood. After a decrease in natural gas prices in 2016, a recent increase in 2017 has set prices for small consumers at historically high levels. The electricity price remains stable, but its current level renders it uncompetitive when compared to other energies.

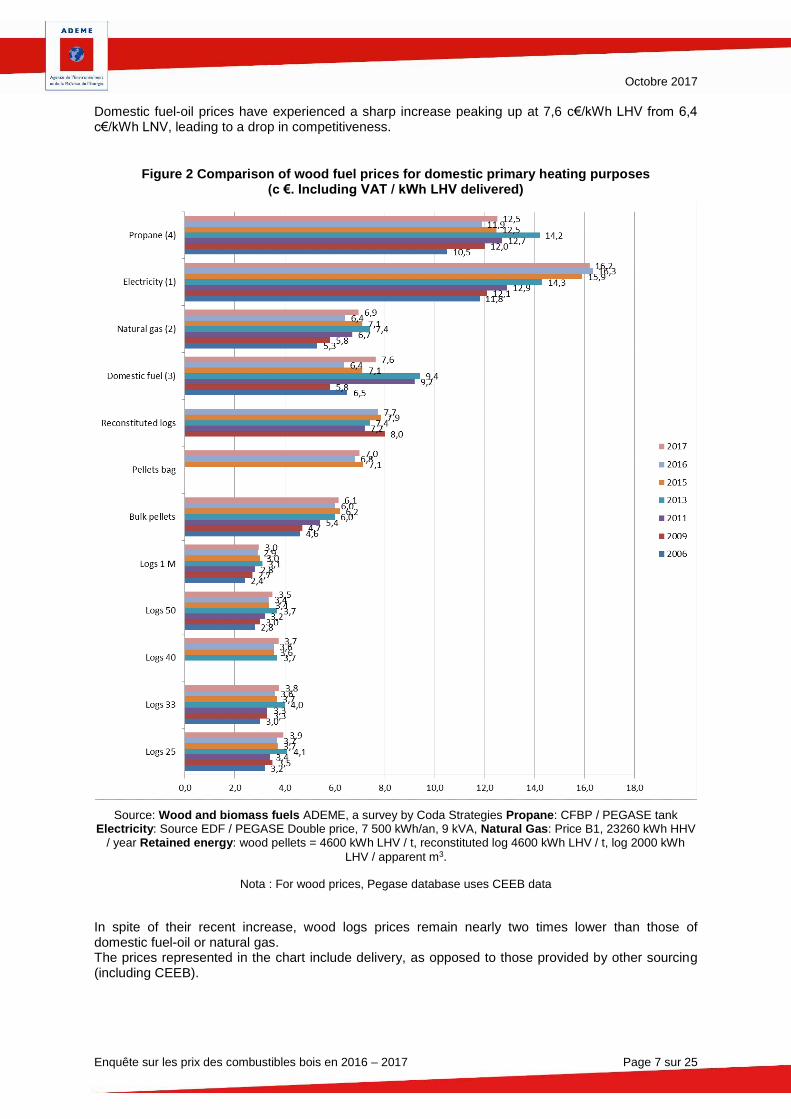

2.1.2. Primary heating use

Wood prices also appear as competitive in the context of their use as primary heating solutions. Nonetheless, price differentials are less important than in the case of auxiliary heating.

Bulk pellet prices remain competitive compared to other energies with a cost of 6,1 c€/kWh LHV.However, the sales of equipment using this energy (mostly pellet boilers) continue to be low.

In 2017, the costs of bulk pellets delivered on skids have increased compared to the last period (6,8 c€/kWh LHV to 7 c€ / kWh LHV), reaching a level that is slightly higher than that of natural gas.

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 7 sur 25

Domestic fuel-oil prices have experienced a sharp increase peaking up at 7,6 c€/kWh LHV from 6,4 c€/kWh LNV, leading to a drop in competitiveness.

Figure 2 Comparison of wood fuel prices for domestic primary heating purposes (c €. Including VAT / kWh LHV delivered)

Source: Wood and biomass fuels ADEME, a survey by Coda Strategies Propane: CFBP / PEGASE tank Electricity: Source EDF / PEGASE Double price, 7 500 kWh/an, 9 kVA, Natural Gas: Price B1, 23260 kWh HHV

/ year Retained energy: wood pellets = 4600 kWh LHV / t, reconstituted log 4600 kWh LHV / t, log 2000 kWh

LHV / apparent m3.

Nota : For wood prices, Pegase database uses CEEB data

In spite of their recent increase, wood logs prices remain nearly two times lower than those of domestic fuel-oil or natural gas. The prices represented in the chart include delivery, as opposed to those provided by other sourcing (including CEEB).

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 8 sur 25

2.2. Evolution of wood prices throughout the recent period

The most relevant way of measuring the evolution of wood prices is the analysis of the cost per kWh LHV, including VAT and delivery. This indicator takes into account the differences in the energy outputs of the multiple fuel types on a comparable basis. Integrating delivery costs allows to highlight the most common domestic supply scenario, for those consumers going through official supply channels.

While the overall increase in wood prices has remained moderate throughout the past few years,, the dynamics associated to each market should be distinguished. A deeper analysis shows that while the prices of wood logs have progressed slowly over the past few years, those of pellets have witnessed a significant rise over 2011-2014 period, with 2015 somewhat breaking this trend.

For pellets in bags, the conditioning explains a significant chunk of the evolution of the prices:

Prices of pellets delivered bulk on pallets have slightly increased over the period (+3%)

Retail prices of pellets in bags (sold individually decreased by 4% since 2016 reaching the level of pellet delivered bulk on pallets

This convergence is tied to the increasing volume of sales of pellets in bags in DIY stores which tend to be following an aggressive pricing policy.

Figure 3 Evolution of retail wood fuel prices (domestic)

(Including delivery, in c€ including VAT / kWh LHV)

Source ADEME - Survey conducted by CODA Strategies

(*) The weighted average price of logs is calculated by assigning to the different log sizes a coefficient equal to their weight in household purchases, as estimated by the survey conducted by ADEME in 2013: 25 cm: 4%, 33 ( and 40) cm: 14%, 50 cm 52% 1M: 9%. (ADEME study, in May 2013, the domestic wood heating: markets and supplies)

In the interest of consistency,, the prices of the different sources of energy as shown in the chart above include delivery.

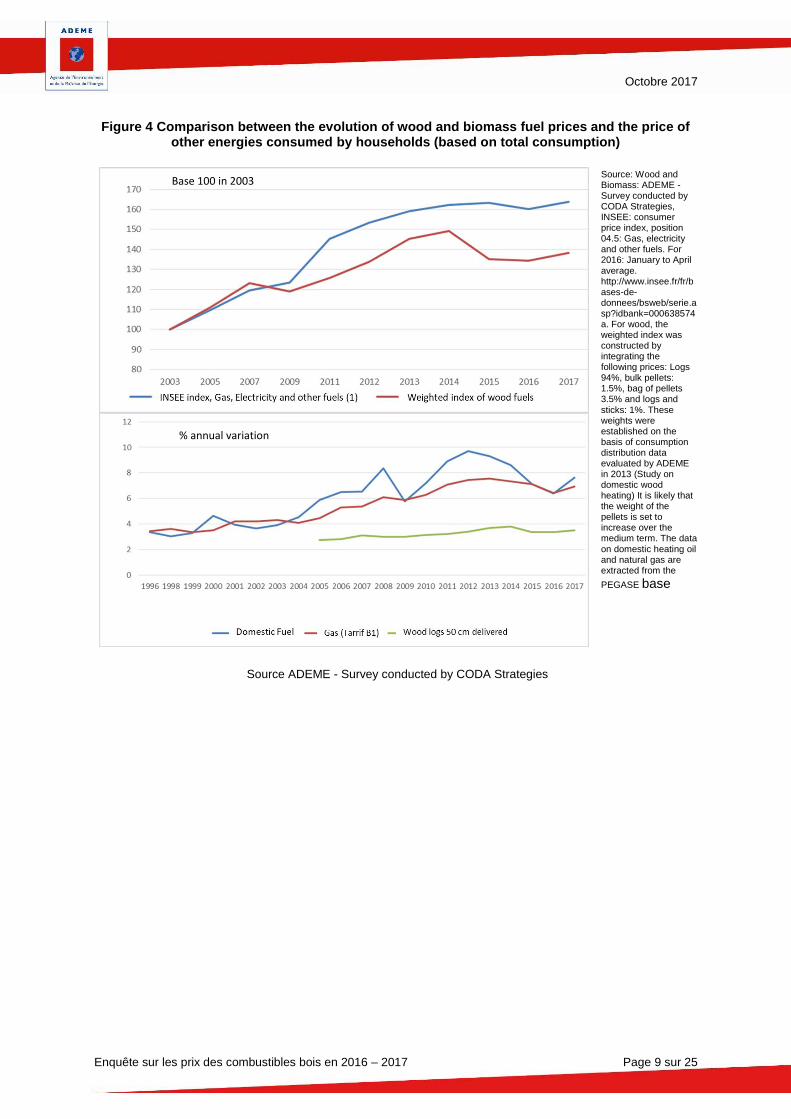

The comparison between the evolution of energy prices in general and the price of wood and biomass fuels in particular demonstrates a more or less parallel evolution between 2006 and 2009. Starting in 2009, the tendency changes as a result of the sharp growth in global energy prices, with wood and biomass fuel prices remaining stable.

On average, energy prices increased by 3.3% annually between 2006 and 2017, whereas wood fuel prices increased by only 1.8% p.a. The decrease in prices recorded in 2015 and 2016 weighs heavily on the overall evolution of the prices of wood fuels over the period.

It should nonetheless be noted that a high-level analysis of overall household energy budgets / costs does not entirely reflect what is otherwise an important decrease in fuel and natural gas prices throughout 2015 and 2016.

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 9 sur 25

Figure 4 Comparison between the evolution of wood and biomass fuel prices and the price of

other energies consumed by households (based on total consumption)

Source: Wood and Biomass: ADEME - Survey conducted by CODA Strategies, INSEE: consumer price index, position 04.5: Gas, electricity and other fuels. For 2016: January to April average. http://www.insee.fr/fr/bases-de-donnees/bsweb/serie.asp?idbank=000638574 a. For wood, the weighted index was constructed by integrating the following prices: Logs 94%, bulk pellets: 1.5%, bag of pellets 3.5% and logs and sticks: 1%. These weights were established on the basis of consumption distribution data evaluated by ADEME in 2013 (Study on domestic wood heating) It is likely that the weight of the pellets is set to increase over the medium term. The data on domestic heating oil and natural gas are extracted from the

PEGASE base

Source ADEME - Survey conducted by CODA Strategies

Base 100 en 2003

% annuel de variation

Base 100 in 2003

% annual variation

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 10 sur 25

2.3. Factors influencing the prices of wood for heating

The wood market is experiencing significant price variations as can be seen in the example below.

Figure 5 Price dispersion per stere of logs (50 cm, delivered)

Source ADEME - Survey conducted by CODA Strategies. X-axis: No of observation, Y-axis: Price, including VAT, per stere

The analysis shows that a significant number of factors influence wood prices: the location, the quality of the products, the delivery methods, the degree of moisture, the essence of the wood, etc ... The present study provides a number of insights on the impact of these different factors.

2.3.1. Factors related to location

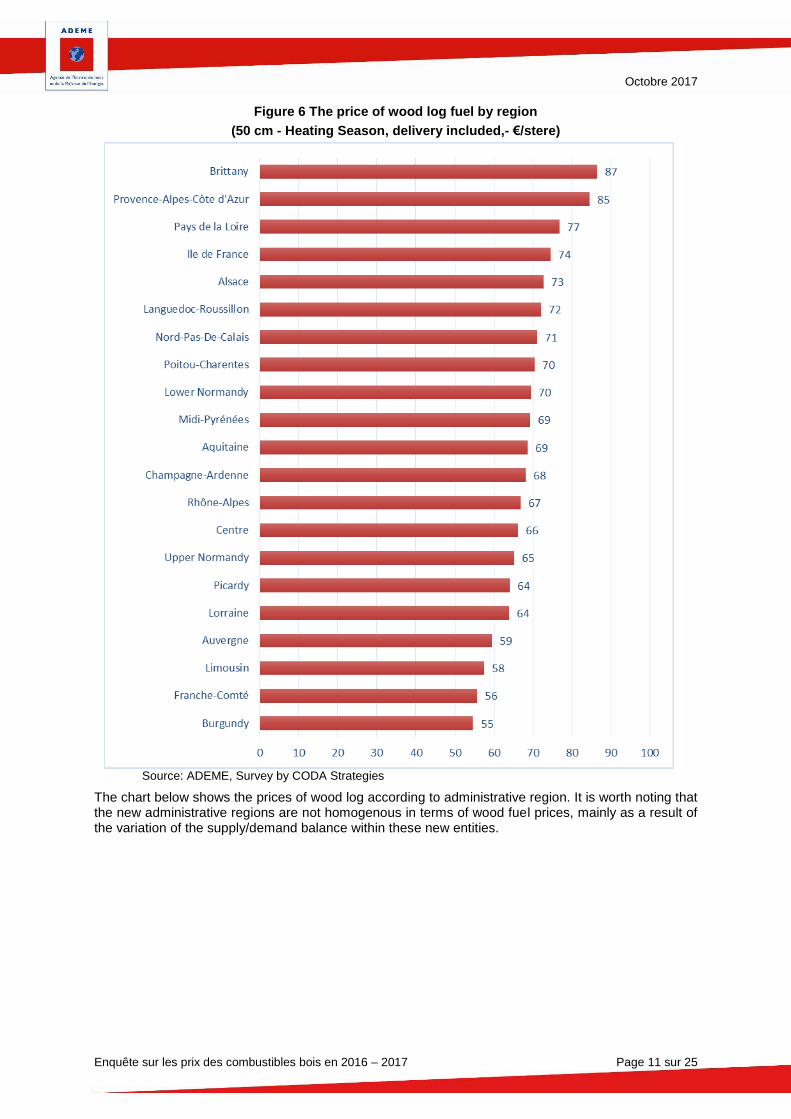

Geographical location highly influences the price of wood for domestic use, with significant differences among French administrative regions.

The highest wood log prices are observed in Birttany, Provence Alpes Côte-d’Azur, Pays de la Loire and Ile de France. On the opposite, Burgundy, Franche-Comté and Limousin display the lowest prices. The disparity between the 3 most expensive and the 3 less expensive regions is in excess of 33%. The main factor explaining the difference is the availability of wood in the regions.

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 11 sur 25

Figure 6 The price of wood log fuel by region

(50 cm - Heating Season, delivery included,- €/stere)

Source: ADEME, Survey by CODA Strategies

The chart below shows the prices of wood log according to administrative region. It is worth noting that the new administrative regions are not homogenous in terms of wood fuel prices, mainly as a result of the variation of the supply/demand balance within these new entities.

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 12 sur 25

Figure 7 Wood log prices, per administrative region

(50 cm – Heating Season - including delivery - €/stere)

Source ADEME – Enquête réalisée par CODA Stratégies.

2.3.2. Labels and certifications

With regards to wood logs, roughly 23% of the companies interiewed in the survey offered labelled products, a share which represents a strong increase from 2015 levels. The most widespread label is France Bois Bûche with 10% of the companies in the survey offering wood logs presenting this label. The number of companies supplying products with multiple labels remains insignificant.

The use of labeling schemes varies extensively according to the profile of the supplier. Currently 27% of entities distributing multiple fuels offer wood logs covered by a label, whereas only 17% of forest owner-producer-distributor companies did so..

The average price of 50 cm labelled logs, including delivery, is 8% higher than logs without any labeling (74€ vs. 68€).

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 13 sur 25

Figure 8 The impact of labeling schemes on the price of wood

(Labeling rates per delivered stere of 50 cm logs)

Source: ADEME, Survey by CODA Strategies.

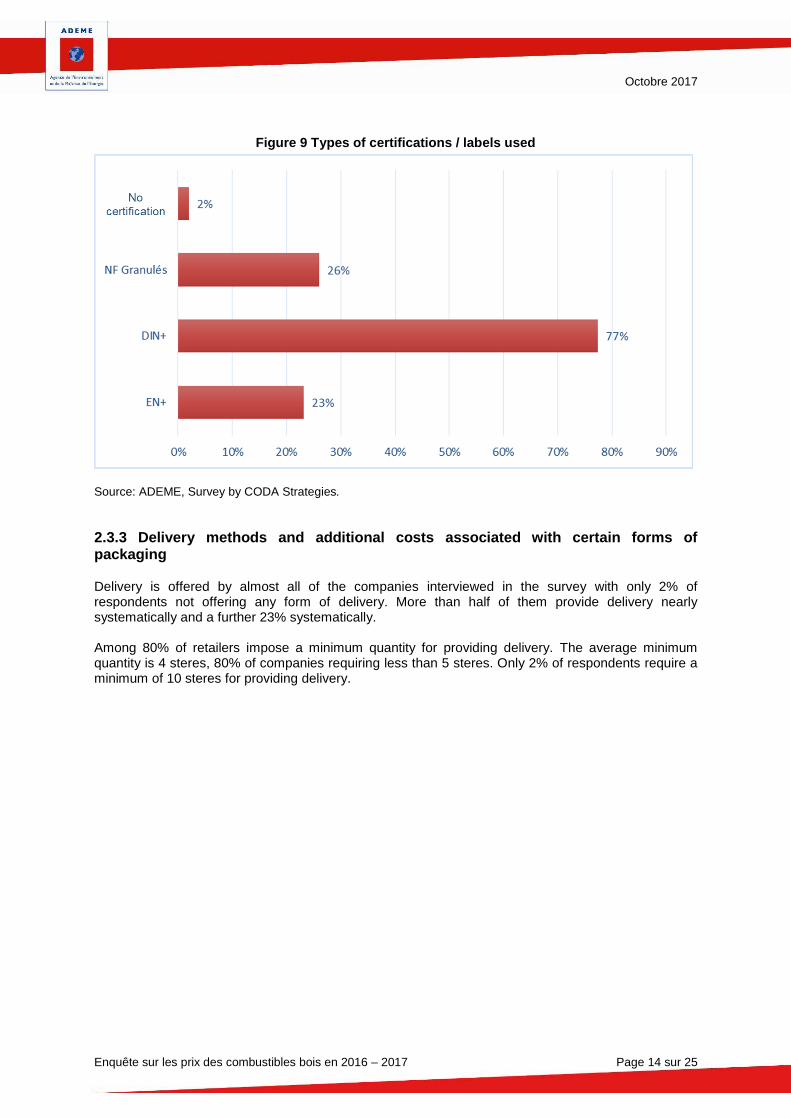

On the market for pellets, distributors offer mostly labeled or certified products.

77% of the interviewees sell products covered by DIN PLUS5, which makes this certification scheme, by far, the most popular on the market. 26% of respondents to the survey offer NF Granulés certified pellets, and a further 23% focus on EN+ certification. No significant price differences were observed between certified and non-certified products.

5 The pellets are subject to a norm generally accepted throughout Europe: the European Committee for Standardization (CEN) established in 2010 a European norm, the EN14961-2 norm, which now regulates European standards on solid biofuels. The standard is public and certifications may be awarded by independent accredited laboratories Other standards and certifications, that existed before EN 14961-2 was established, continue to be used:

• The DIN PLUS certification is the best known. DIN PLUS is a trademark owned by the German body Din Certco. • The NF Pellets Biofuels certification. The brand is owned by AFNOR, which mandates the FCBA, the Technological Institute Forest

Cellulose Wood-built furniture, for the management of this certification. • The ENplus certification, the most recent one, is managed by the European Pellet Council, mandated by the DEPI, the German

organization for heating with pellets, who owns the trademark. • Registered by Inter Region Wood, the collective mark "France Bois Buche: French companies who get involved®" unites and validates

the quality procedures implemented by the French inter-regional authority for forestry and wood. • The program for the recognition of forestry certification schemes or PEFC (the Pan European Forest Certification now known as the

Program for the Endorsement of Forest Certification schemes) is an environmental label aimed to promote and certify sustainable forest management.

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 14 sur 25

Figure 9 Types of certifications / labels used

Source: ADEME, Survey by CODA Strategies.

2.3.3 Delivery methods and additional costs associated with certain forms of packaging

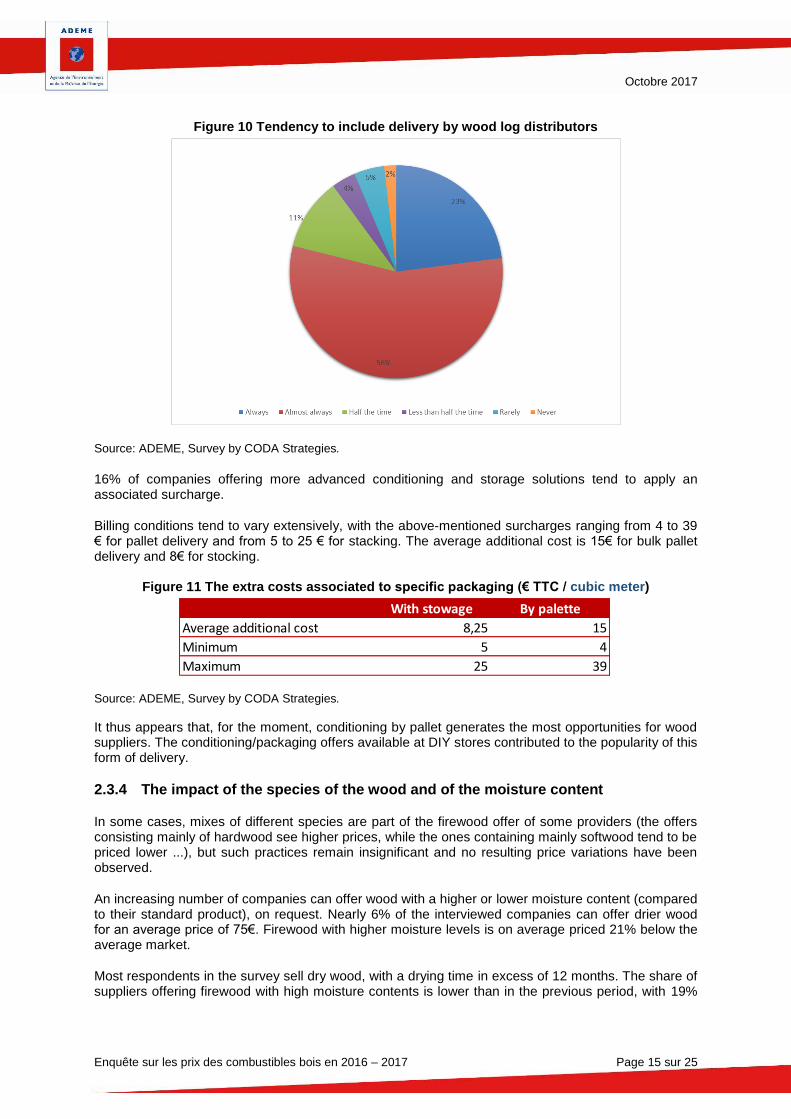

Delivery is offered by almost all of the companies interviewed in the survey with only 2% of respondents not offering any form of delivery. More than half of them provide delivery nearly systematically and a further 23% systematically. Among 80% of retailers impose a minimum quantity for providing delivery. The average minimum quantity is 4 steres, 80% of companies requiring less than 5 steres. Only 2% of respondents require a minimum of 10 steres for providing delivery.

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 15 sur 25

Figure 10 Tendency to include delivery by wood log distributors

Source: ADEME, Survey by CODA Strategies.

16% of companies offering more advanced conditioning and storage solutions tend to apply an associated surcharge.

Billing conditions tend to vary extensively, with the above-mentioned surcharges ranging from 4 to 39 € for pallet delivery and from 5 to 25 € for stacking. The average additional cost is 15€ for bulk pallet delivery and 8€ for stocking.

Figure 11 The extra costs associated to specific packaging (€ TTC / cubic meter)

With stowage By palette

Average additional cost 8,25 15

Minimum 5 4

Maximum 25 39

Source: ADEME, Survey by CODA Strategies.

It thus appears that, for the moment, conditioning by pallet generates the most opportunities for wood suppliers. The conditioning/packaging offers available at DIY stores contributed to the popularity of this form of delivery.

2.3.4 The impact of the species of the wood and of the moisture content

In some cases, mixes of different species are part of the firewood offer of some providers (the offers consisting mainly of hardwood see higher prices, while the ones containing mainly softwood tend to be priced lower ...), but such practices remain insignificant and no resulting price variations have been observed.

An increasing number of companies can offer wood with a higher or lower moisture content (compared to their standard product), on request. Nearly 6% of the interviewed companies can offer drier wood for an average price of 75€. Firewood with higher moisture levels is on average priced 21% below the average market.

Most respondents in the survey sell dry wood, with a drying time in excess of 12 months. The share of suppliers offering firewood with high moisture contents is lower than in the previous period, with 19%

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 16 sur 25

of respondents offering moderately dry wood and only 10% selling wood with high moisture levels (green wood).

Retailers of dry wood usually declare a moisture content below 15%, whereas those offering green wood declare a moisture content superior to 35%.

Figure 12 Offers containing various moisture contents and their impacts on market prices

(50 cm logs- €including VAT and delivery )

Source: ADEME, Survey by CODA Strategies

2.3.5 Commercialization outside the heating season

Currently, the number of companies selling firewood at dedicated off-season prices is very limited despite a slight increase compare to the last period: 8% of respondents use this two-tier pricing. Whenever such pricing schemes are used, the differences between prices during the heating season and outside of it are of roughly 7%. Also, for companies engaging in such differentiated pricing schemes, prices for 50 cm logs during the heating season tend to be higher than those of their competitors (74.4 € during the heating season versus 70€ for the whole of the market).

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 17 sur 25

Figure 13 Rate of discount for sales outside of the heating season

(Wood log – 50 cm- including delivery)

Source: ADEME, Survey by CODA Strategies

The interviews with the different market stakeholders tend to show that the development of off-season offers is perceived as contributing to the improvement of the market. In the case of wood logs, such schemes allow distributors to make a tariff differentiation for those households having the possibility of storing the firewood throughout spring and winter, thus benefitting from lower tariffs. This would allow retailers to better position their offers with regards to informal channels: wood sold off-season would be more competitive price-wise while a low moisture content wood would ensure a differentiation in terms of quality.

The stakes are even more significant for pellets, mainly because the development of off-season deals would allow for a more adequate balance between production, which takes place throughout the year, and consumption, which is excessively concentrated during the heating period

2.4. The French pellets market in the European context

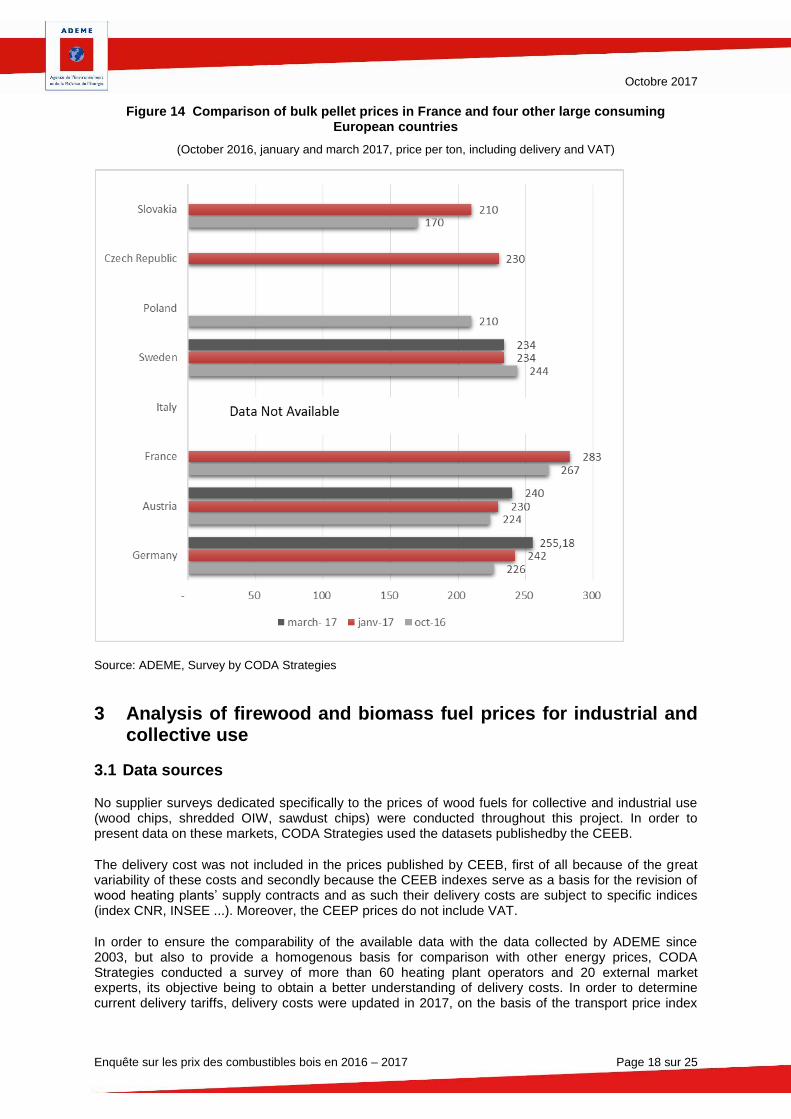

A comparison of prices at international, and particularly at European level, is difficult to conduct due to the lack of common indicators between the different countries. The most homogeneous basis for comparison is the price of bulk pellets. The pertinence of such an exercise is nonetheless limited by the relatively low use of this form of commercialization is very limited on the domestic sector in France. Within these limitations, the comparison between French and European prices shows that national prices, which were for a long time among the lowest in Europe, are currently higher than those observed on the national markets of other pellet-consuming countries. Thus, in the first quarter of 2017, the average price of bulk pellets, including delivery, increased to € 283 per ton according to the survey (€ 272.4 according to data released by the CEEB), while, during the same period, the price for EN Plus A1 or ISO 17225-2 A1-certified pellets was € 242 in Germany and € 230 in Austria. These findings can be explained, at least in part, by the French market’s strong demand for pellets conditioned in bags, which tends to impact bulk supply and thus competition, but also by the absence of regulatory mechanisms on the market, and in particular the poor development of off-season offer practices that would allow for a better balance between production and consumption.

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 18 sur 25

Figure 14 Comparison of bulk pellet prices in France and four other large consuming European countries

(October 2016, january and march 2017, price per ton, including delivery and VAT)

Source: ADEME, Survey by CODA Strategies

3 Analysis of firewood and biomass fuel prices for industrial and collective use

3.1 Data sources

No supplier surveys dedicated specifically to the prices of wood fuels for collective and industrial use (wood chips, shredded OIW, sawdust chips) were conducted throughout this project. In order to present data on these markets, CODA Strategies used the datasets publishedby the CEEB.

The delivery cost was not included in the prices published by CEEB, first of all because of the great variability of these costs and secondly because the CEEB indexes serve as a basis for the revision of wood heating plants’ supply contracts and as such their delivery costs are subject to specific indices (index CNR, INSEE ...). Moreover, the CEEP prices do not include VAT.

In order to ensure the comparability of the available data with the data collected by ADEME since 2003, but also to provide a homogenous basis for comparison with other energy prices, CODA Strategies conducted a survey of more than 60 heating plant operators and 20 external market experts, its objective being to obtain a better understanding of delivery costs. In order to determine current delivery tariffs, delivery costs were updated in 2017, on the basis of the transport price index

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 19 sur 25

published by the CNR (Comité National Routier)6, Moreover, VAT at different rates was included, with the comparisons being presented bot with and without VAT.

A survey of 60 commercial and municipal heating plants using pellets was conducted in order to establish the real pellet price paid by those stakeholders. Indeed, the survey of bulk pellet providersdoesn’t take into account the discounts obtained on large quantity purchases which could be considerably important in the case of these professional or municipal users with high consumption rates.

3.2 The competitiveness of wood and biomass fuels for collective and industrial use

The comparison of the prices of different sources of energy on a homogenous basis can be conducted by integrating the estimated delivery costs and incorporating VAT.

6 The index used is the one that applies to cereal and grain delivery trucks, which resemble most those vehicles used for wood chip deliveries ( sliding-floor semi-trailers).

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 20 sur 25

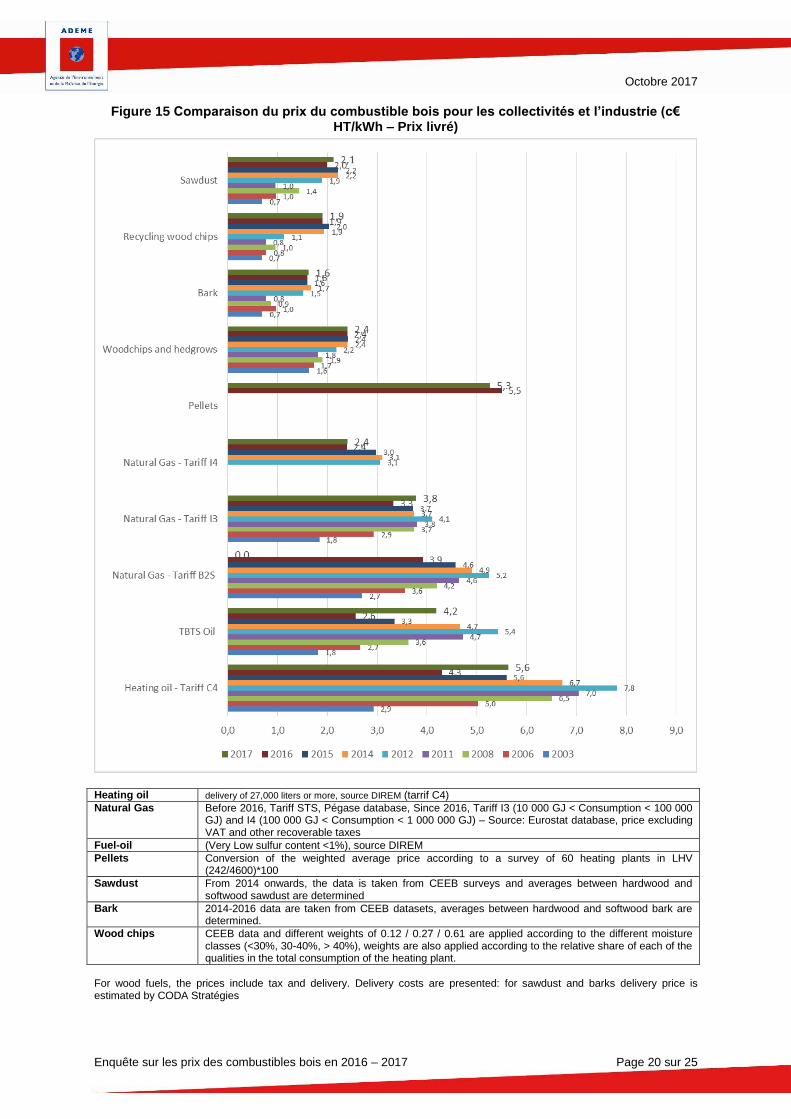

Figure 15 Comparaison du prix du combustible bois pour les collectivités et l’industrie (c€ HT/kWh – Prix livré)

Heating oil delivery of 27,000 liters or more, source DIREM (tarrif C4) Natural Gas Before 2016, Tariff STS, Pégase database, Since 2016, Tariff I3 (10 000 GJ < Consumption < 100 000

GJ) and I4 (100 000 GJ < Consumption < 1 000 000 GJ) – Source: Eurostat database, price excluding VAT and other recoverable taxes

Fuel-oil (Very Low sulfur content <1%), source DIREM Pellets Conversion of the weighted average price according to a survey of 60 heating plants in LHV

(242/4600)*100 Sawdust From 2014 onwards, the data is taken from CEEB surveys and averages between hardwood and

softwood sawdust are determined Bark 2014-2016 data are taken from CEEB datasets, averages between hardwood and softwood bark are

determined. Wood chips CEEB data and different weights of 0.12 / 0.27 / 0.61 are applied according to the different moisture

classes (<30%, 30-40%, > 40%), weights are also applied according to the relative share of each of the qualities in the total consumption of the heating plant.

For wood fuels, the prices include tax and delivery. Delivery costs are presented: for sawdust and barks delivery price is estimated by CODA Stratégies

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 21 sur 25

For local authorities / municipalities and industries, the prices of wood chips, shredded OIW, bark and sawdust chips appear to be competitive, especially when compared to natural gas and fuel-oil, which are both directly competing energies. Nonetheless, one should note that for big consumers (Tariff I4 for Natural Gas), wood chip and natural gas prices are on a par.

The past few years have witnessed a significant increase in the prices of saw-mill by-products and industrial waste (i.e. from pulp and paper). For these fuels, short-term price differences can be significant – this highlights the strong volatility of the market and of the supply-demand balance. Over the medium term, prices in MWh LHV for the different fuels tend to converge.

This could be explained by the fact that large heating plants tend to use other fuels as complement to to wood chips (recycled woodchips, sawdust, bark…) in order to benefit from a competitive price mix. Therefore, as demand for these products increases, the price has a tendency to go up. In the specific case of recycled wood chips, the end of their regulated “waste” status that occurred in 2014 has lead to a series of constraints and cost increases.

In order to obtain the prices of wood pellets destined to the supply of professional heating plants, CODA Strategies conducted a specific survey with the operators of a number of these plants. The most obvious element observed is the strong disparity in pellet prices according to plant size. The evolution of these prices cannot be presented due to a lack of continuity in the data. The average price weighted by consumed quantities is estimated at 242 €, per ton, including delivery and VAT, this price being 14.5% lower than the one declared by the suppliers (for the retail market). The difference results from the discount obtained by the plant operators. The price disparity has become more important over the last year (11% in 2016). Multiple price negotiations have occurred and it is safe to estimate that in order to obtain better conditions, buyers have based their positions on the evolution of gas prices. On top of that, as the collective heating market for bulk deliveries has developed strongly, it has become more attractive for suppliers, especially as the domestic “bulk” market has tended to stagnate. Under these conditions, it is becoming apparent that suppliers of pellets are becoming more willing to work on their tariffs in an effort to develop and improve their positions on the market.

Figure 16 Pellet prices for collective heating and commercial heating plants

(Price per ton including delivery and VAT)

Source ADEME – Study conducted by CODA Strategies

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 22 sur 25

3.3 The evolution of prices for collective and industrial use throughout the recent period

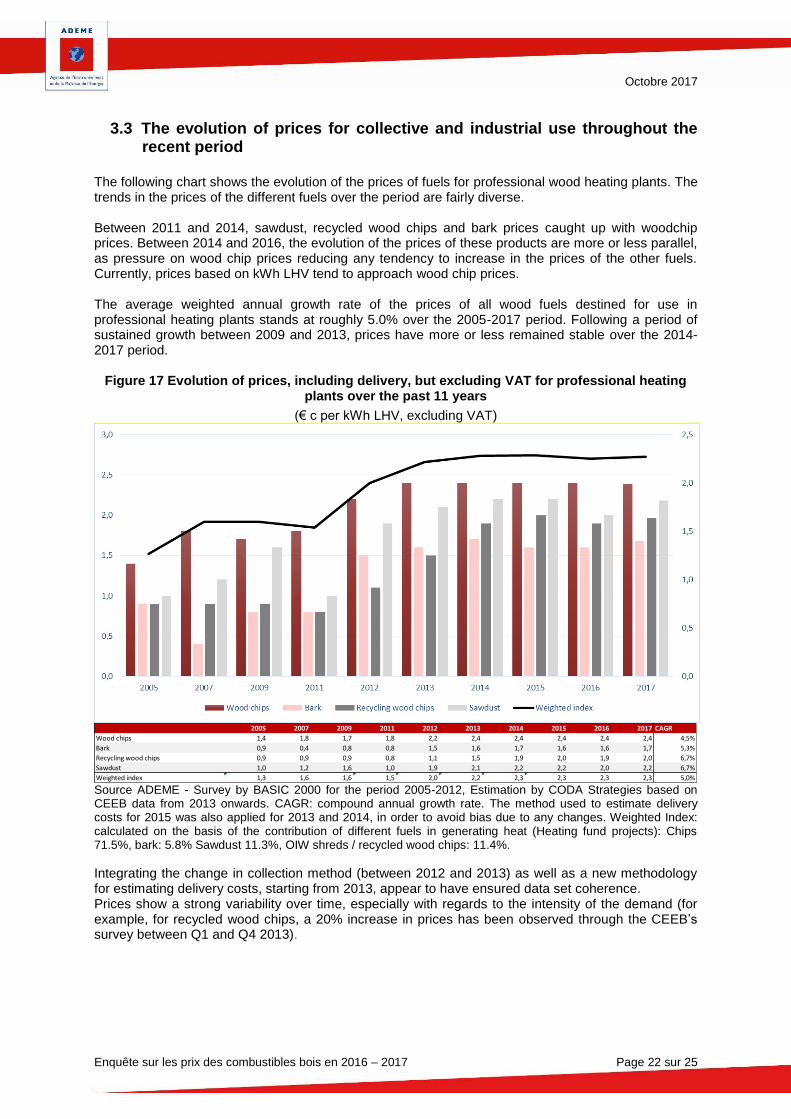

The following chart shows the evolution of the prices of fuels for professional wood heating plants. The trends in the prices of the different fuels over the period are fairly diverse. Between 2011 and 2014, sawdust, recycled wood chips and bark prices caught up with woodchip prices. Between 2014 and 2016, the evolution of the prices of these products are more or less parallel, as pressure on wood chip prices reducing any tendency to increase in the prices of the other fuels. Currently, prices based on kWh LHV tend to approach wood chip prices. The average weighted annual growth rate of the prices of all wood fuels destined for use in professional heating plants stands at roughly 5.0% over the 2005-2017 period. Following a period of sustained growth between 2009 and 2013, prices have more or less remained stable over the 2014-2017 period.

Figure 17 Evolution of prices, including delivery, but excluding VAT for professional heating plants over the past 11 years

(€ c per kWh LHV, excluding VAT)

2005 2007 2009 2011 2012 2013 2014 2015 2016 2017 CAGR

Wood chips 1,4 1,8 1,7 1,8 2,2 2,4 2,4 2,4 2,4 2,4 4,5%

Bark 0,9 0,4 0,8 0,8 1,5 1,6 1,7 1,6 1,6 1,7 5,3%

Recycling wood chips 0,9 0,9 0,9 0,8 1,1 1,5 1,9 2,0 1,9 2,0 6,7%

Sawdust 1,0 1,2 1,6 1,0 1,9 2,1 2,2 2,2 2,0 2,2 6,7%

Weighted index 1,3 1,6 1,6 1,5 2,0 2,2 2,3 2,3 2,3 2,3 5,0% Source ADEME - Survey by BASIC 2000 for the period 2005-2012, Estimation by CODA Strategies based on CEEB data from 2013 onwards. CAGR: compound annual growth rate. The method used to estimate delivery costs for 2015 was also applied for 2013 and 2014, in order to avoid bias due to any changes. Weighted Index: calculated on the basis of the contribution of different fuels in generating heat (Heating fund projects): Chips 71.5%, bark: 5.8% Sawdust 11.3%, OIW shreds / recycled wood chips: 11.4%.

Integrating the change in collection method (between 2012 and 2013) as well as a new methodology for estimating delivery costs, starting from 2013, appear to have ensured data set coherence. Prices show a strong variability over time, especially with regards to the intensity of the demand (for example, for recycled wood chips, a 20% increase in prices has been observed through the CEEB’s survey between Q1 and Q4 2013).

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 23 sur 25

Conclusion

The dynamics observed in 2017 on the domestic and collective markets differed extensively.

On the domestic market, after a decrease in 2015 and 2016, prices recovered via a 3% to 6% increase, according to fuel type.

Following mild weather conditions in 2014-2015 and 2015-2016, which led to an to accumulation of stocks and aggressive tariff policies aimed at limiting them, prices returned to their regular levels in 2016-2017, with previous’ years attempts at decreasing stocks reducing downward price pressure. However, the relative warmth of the 2016-2017 winter, has kept prices from rebounding. An analysis of the data over the recent period highlights the importance of the climate factor, which continues to play an important role in explaining the annual changes in prices.

The pellets market was not impacted by this price recovery tendency, pellet prices decreasing during the 2016-2017 season. On the one hand, this situation is the natural consequence of the improved positions of a series of new suppliers, and in particular of DIY stores which tend to adopt aggressive tariff policies.. On the other hand, the previously important price competitiveness of these fuels has virtually eroded, as the other energies – fossil fuels in particular (natural gas, fuel oil), have seen strong price decreases during the last two years.

Beyond the short-term phenomena, one of the factors penalizing the national market, especially when compared to those of neighboring countries is the slow pace of its professionalization and of its structuring. This is clearly visible, for example, in the fact that seasonal price differentiation practices are still relatively uncommon in France, compared to other European countries where they are well entrenched. “Off-season” offers are few and far between – their impact on individuals’ purchasing strategies (e.g. purchasing wood in spring, for storage throughout the summer) is marginal. Moreover, the market sees practically no differentiation through quality of supply.

The wood and biomass fuels market remains strongly marked by regional differences. These differences are caused on one side by the ease of access to the resource, and on the other by different competitive situations: in regions with a scarcity of resources, offers than run parallel to the conventional supply chain are obviously less visible, and as such, have a considerably lower impact on prices.

On the wood log market, a price that would balance producers’ books, as declared by market professionals, would be around € 80-85 per stere, which is about 10 € higher than current prices. The recovery of the prices observed in 2017 is thus insufficient to ensure long-term stability of the sector.

On the market for fuels destined for use in professional heating plants, prices of the multiple sources continue to converge. In 2012 recycled wood chips were 2 times cheaper than conventional wood chips; today the price gap is still fairly significant, but it only stands at around 20%. The 2014 withdrawal of the waste status for this type of fuel has lead to more rigorous quality management and implicitly to an increase in the production cost.

Over the last year, prices for professional customers have increased, under the influence of a number of factors: the mildness of the past few winter, the general decrease in fossil fuel prices and the slowdown of investment efforts in the sector destabilizing the supply-demand balance (a great deal of investments in fuel production have been made in the hopes of an important increase in the demand, which, however, has remained unconvincingly stable).

In the medium-term, an upward price correction could occur should the aforementioned factors be reversed: a new increase of the different incentives and especially a significant rebound in gas prices impacting consumer behavior. . The long awaited expansion of the carbon taxation scheme is also likely to contribute to improving the competitiveness of wood and biomass fuels.

Prices paid by professional end-users vary wildly according to the quantities consumed, the quality of the wood and the relative ease of delivery. Studying the delivery costs has shown that not only are these highly variable, but that they also account for an average of roughly 20% of overall final fuel

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 24 sur 25

costs (obviously, including delivery) This variability is connected to the geographical situation of the heating plant (distance from the forest, urban density and ease of circulation…), to the acquired volumes which may result in different forms of organization and on the potentialities of optimizing deliveries from one region to another (e.g. possibility of delivering other products to avoid an empty return run).

Throughout the recent period, delivery costs have remained more or less stable, as the factors driving these costs upward (general expenses and overheads, payroll growth and equipment costs) have been compensated by the drops in Diesel prices, the increases in productivity levels as well as the reduction in average delivery distances. This reduction in distance is itself the consequence of supply seriously overtaking demand, thus facilitating local procurement.

Octobre 2017

Enquête sur les prix des combustibles bois en 2016 – 2017 Page 25 sur 25

ABOUT ADEME

The French Environment and Energy

Management Agency (ADEME) is a public

agency under the joint authority of the

Ministry of Ecology, Sustainable

Development and Energy, and the Ministry

for Higher Education and Research. The

agency is active in the implementation of

public policy in the areas of the environment,

energy and sustainable development.

ADEME provides expertise and advisory

services to businesses, local authorities and

communities, government bodies and the

public at large, to enable them to establish

and consolidate their environmental action.

As part of this work the agency helps finance

projects, from research to implementation, in

the areas of waste management, soil

conservation, energy efficiency and

renewable energy, air quality and noise

abatement.

www.ademe.fr.